“A STUDY ON COMPARISON OF CUSTOMER

SATISFACTION AMONG THE USERS OF DIFFERENT

MOBILE PAYMENT SYSTEMS”

Project Report submitted to

UNIVERSITY OF CALICUT

In partial fulfillment of the requirement for the award of the degree of

BACHELOR OF COMMERCE

Submitted by

EBY MARTIN

(CCASBCM151)

Under the supervision of

Mrs. KALPA SIVADAS

DEPARTMENT OF COMMERCE

CHRIST COLLEGE (AUTONOMOUS), IRINJALAKUDA

MARCH 2021

CHRIST COLLEGE (AUTONOMOUS), IRINJALAKUDA

CALICUT UNIVERSITY

DEPARTMENT OF COMMERCE

CERTIFICATE

This is to certify that the project report entitled “A STUDY ON

COMPARISON OF CUSTOMER SATISFACTION AMONG THE

USERS OF DIFFERENT MOBILE PAYMENT SYSTEMS” is a bonafide

record of project done by EBY MARTIN, Reg. No. CCASBCM151, under my

guidance and supervision in partial fulfillment of the requirement for the award

of the degree of BACHELOR OF COMMERCE and it has not previously

formed the basis for any Degree, Diploma and Associateship or Fellowship.

Prof. K.J.JOSEPH Mrs.KALPA SIVADASCo-ordinator Project Guide

DECLARATION

I, EBY MARTIN, hereby declare that the project work entitled “A

STUDY ON COMPARISON OF CUSTOMER SATISFACTION AMONG

THE USERS OF DIFFERENT MOBILE PAYMENT SYSTEMS” is a record

of independent and bonafide project work carried out by me under the

supervision and guidance of Ms.Kalpa Sivadas , Assistant Professor,

Department of Commerce, Christ College, Irinjalakuda.

The information and data given in the report is authentic to the best of my

knowledge. The report has not been previously submitted for the award of any

Degree, Diploma, Associateship or other similar title of any other university or

institute.

Place: Irinjalakuda EBY MARTIN

Date: CCASBCM151

ACKNOWLEDGEMENT

I would like to take the opportunity to express my sincere gratitude to allpeople who have helped me with sound advice and able guidance.

Above all, I express my eternal gratitude to the Lord Almighty under whosedivine guidance; I have been able to complete this work successfully.

I would like to express my sincere obligation to Rev.Dr. Jolly Andrews,Principal-in-Charge, Christ college Irinjalakuda for providing various facilities.

I am thankful to Prof. K.J.Joseph, Co-ordinator of B.Com (Finance), forproviding proper help and encouragement in the preparation of this report.

I am thankful to Mrs.Smitha Antony, Class teacher for her cordial support,valuable information and guidance, which helped me in completing this taskthrough various stages.

I express my sincere gratitude to Mrs. Kalpa Sivadas, Assistant Professor,whose guidance and support throughout the training period helped me tocomplete this work successfully.

I would like to express my gratitude to all the faculties of the Department fortheir interest and cooperation in this regard.

I extend my hearty gratitude to the librarian and other library staffs of mycollege for their wholehearted cooperation.

I express my sincere thanks to my friends and family for their support incompleting this report successfully.

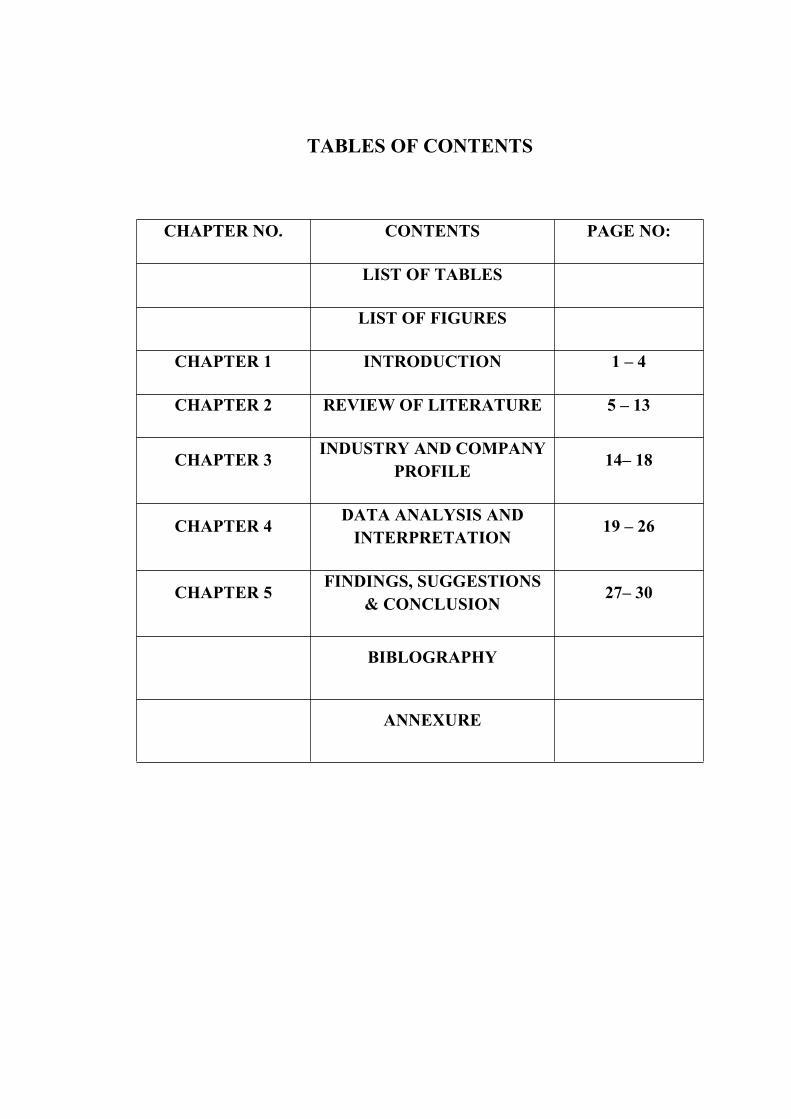

TABLES OF CONTENTS

CHAPTER NO. CONTENTS PAGE NO:

LIST OF TABLES

LIST OF FIGURES

CHAPTER 1 INTRODUCTION 1 – 4

CHAPTER 2 REVIEW OF LITERATURE 5 – 13

CHAPTER 3INDUSTRY AND COMPANY

PROFILE 14– 18

CHAPTER 4 DATA ANALYSIS ANDINTERPRETATION

19 – 26

CHAPTER 5 FINDINGS, SUGGESTIONS& CONCLUSION

27– 30

BIBLOGRAPHY

ANNEXURE

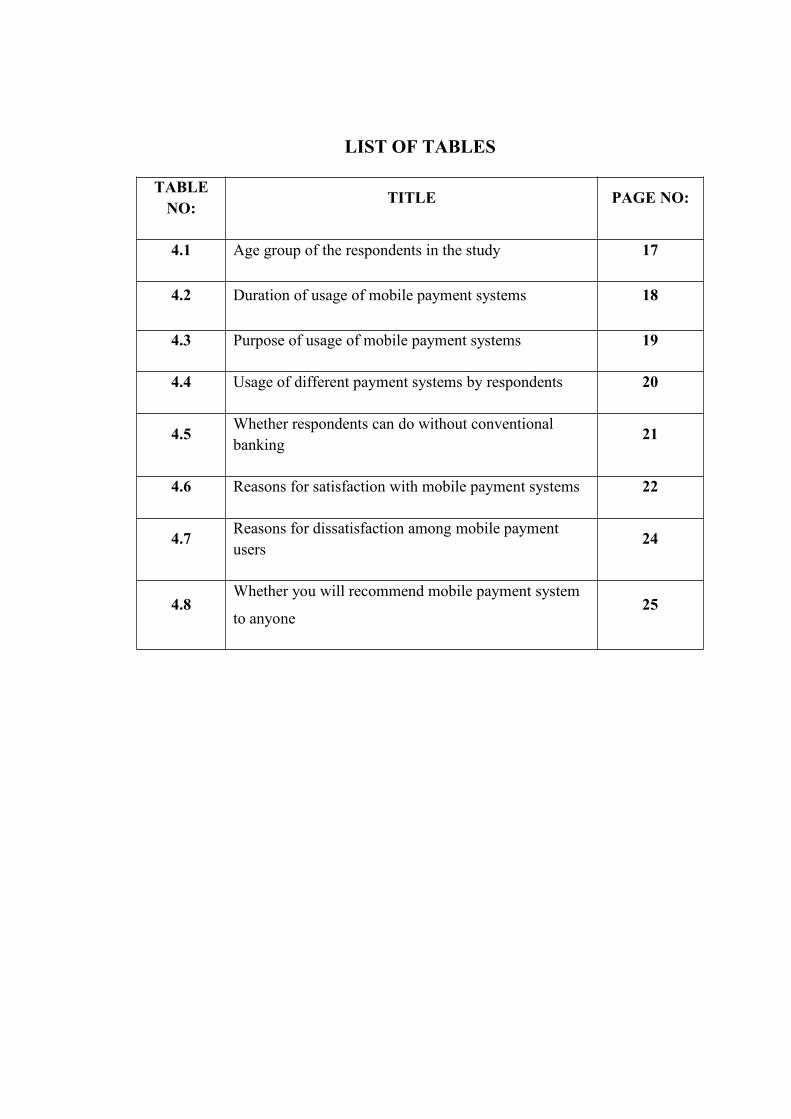

LIST OF TABLES

TABLENO: TITLE PAGE NO:

4.1 Age group of the respondents in the study 17

4.2 Duration of usage of mobile payment systems 18

4.3 Purpose of usage of mobile payment systems 19

4.4 Usage of different payment systems by respondents 20

4.5 Whether respondents can do without conventionalbanking

21

4.6 Reasons for satisfaction with mobile payment systems 22

4.7 Reasons for dissatisfaction among mobile paymentusers

24

4.8Whether you will recommend mobile payment system

to anyone25

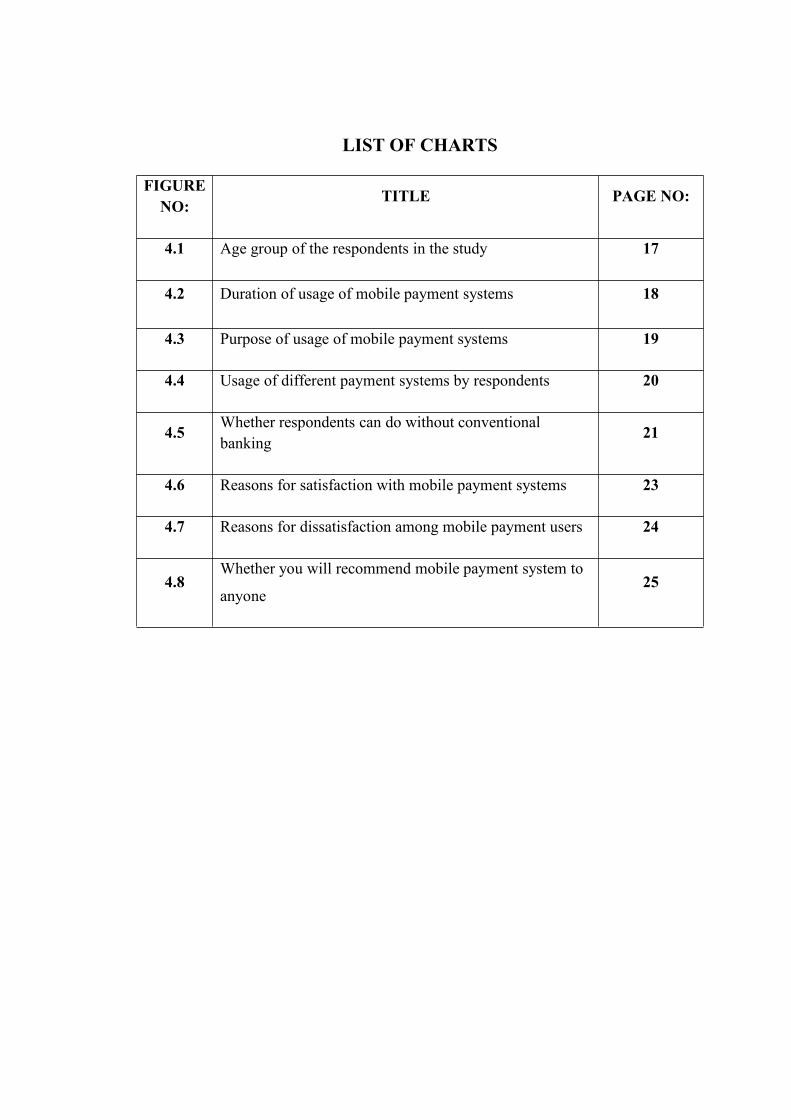

LIST OF CHARTS

FIGURENO: TITLE PAGE NO:

4.1 Age group of the respondents in the study 17

4.2 Duration of usage of mobile payment systems 18

4.3 Purpose of usage of mobile payment systems 19

4.4 Usage of different payment systems by respondents 20

4.5 Whether respondents can do without conventionalbanking 21

4.6 Reasons for satisfaction with mobile payment systems 23

4.7 Reasons for dissatisfaction among mobile payment users 24

4.8Whether you will recommend mobile payment system to

anyone25

CHAPTER I

INTRODUCTION

1

1.1 Introduction

Invention of computer in 1960’s and later,introduction of world wide web(www) in

1989 led to revolutionary changes in electronic payment system.As electronic

payment systems evolved,payment process was minimized to just a few simple

steps,which can be done at remote locations away from the bank.

Cash is the de-facto mode of payment across the globe.More than 95% of the

transactions in India are still cash-based.Other modes of payment,specially digital

payments,have grown steadily for the past many years.While Credit and Debit cards

are the most popular cashless modes of payment introduced more than 3 decades ago

in India,the adoption is still slow and steady.There are challenges in adoption due to

lack of infrastructure,connectivity and PoS machines.The penetration is low amongst

small ticket merchants as well as tier-2,tier-3 cities since banks lack the will to

promote PoS adoption for small businesses.

With each passing year,a lot of new solutions are added to the e-payment

process,which is stimulating e-commerce growth.Since the first decade of 21st

century,global giants like amazon pay and Payu are in the field.In 2010,Indian

entrepreneurs developed Paytm,which has evolved into various fields of cashless

transaction.Though Google Pay came into the field later,their operations are

increasing at breath taking speed. Google had the advantage of being the largest net

browser company and they are a household name all over the world.

Demonetization disrupted the cash economy for a while with a rise in digital payments.

Digital payments growth has been accelerated by four years due to demonetization .

Since then , the cash is back , but mobile payments are being used twice as much .

Currently, less than 5 percentage of the transactions are cashless and there has been a

strong push by the government for digital payment by promoting mobile-based

payment methods like USSD as well as Adhar based payments like AEPS and mobile

ATMs. There are plenty of cashless payment options that have grown in last 3 years –

like UPI, Net banking , Open banking apps, USSD , AEPS etc.The driving force in

2

the evolution of the payment system has been the need to give users the ease of doing

it as it directly affects the purchase pattern of a customer.

It is because of this reason that Mobile wallets like MobiKwik,PayTM,Amazon

Pay,Google Pay,Oxigen have become the forerunners of the digital payment

industry.While these wallets are penetrating into very small businesses and non-tier-1

cities initially with their cash-backs,they have innovated and provided easy user

experience that needs minimum learning by a user.For example,payment via scanning

a QRCode or simply entering merchant’s mobile number is easy.Sending money to a

friend to clear debts is just a click-or-two away.To add on to this,apart from

simplifying payments,the value added services like bill payments,ticket booking

provided by these wallets have made them the preferred payment option of the savvy

Indian consumer.

Demonetization gave big momentum to the growth of e-payment systems in India.But

even now only small percentage of consumers have cashless transactions.E-payment

systems are generally simple to operate,efficient and at the same time secure also.

1.2 Statement of the problem

Traditionally,purchase of goods involved transfer of physical cash from the buyer to

the retailer.With the introduction of debit/credit cards,cashless transactions could be

done electronically,at least in many of the supermarkets and shops.But for smaller

vendors like vegetable sellers and for those who do door to door sale of fish,there

were logistical issues.With the evolution of e-payment portals like Google

Pay,amazon pay,Paytm,cash transactions could be done with smart phones,by the

click of a button and thus the transactions are simple,cashless and are available for

local vendors at the point of sale (POS).

1.3 Scope of the Study

Study is planned to know what percentage of sample population is using the e-

payment services.Over last two decades,e-payment has tremendously changed the

3

way we do business.By doing this comparative study,we get the level of satisfaction

achieved by customers,using different e-payment portals.

1.4 Objectives of the study

1.4.1 To study usage of e-payment systems for business transactions in the sample

population.

1.4.2 To identify the satisfaction level of customers,using e-payment systems.

1.4.3 To identify the reasons for preference of e-payment system over traditional

payment method.

1.5 Research Design

1.5.1 Nature of Study:Study is descriptive in nature.

1.5.2 Nature of Data:Both primary and secondary data were used.

1.5.3 Sources of data

Primary data:Questions were designed in a systematic manner,covering adequate

and relevant aspects of the study.Survey was done with the help of online

questionnaire.

Secondary data:Secondary data was collected from books,journals and websites.

1.6 Sample Design

1.6.1 Nature of Population:Mostly middle class population.

1.6.2 Sample Unit:Sample unit is of 50 people.

1.6.3Method of sampling:Convenience sampling is used in this study.(Non-

probability method)

1.6.4 Size of Sample: Sample of 50 respondents ,mostly comprising of college

students and also members of middle class families from Thrissur district.

4

1.7 Tools for Analysis

Following tools are used in the study

-Percentage

-Charts:Bar diagram,pie chart

1.8 Limitations of the study

1. Due to Covid 19 pandemic,there was restricted mobility.Hence there was

difficulty in collecting the data.

2. For a facility like e-payment services,which is used by large percentage of

population,sample size should have been larger to get a more accurate result.

1.9 Chapterisation

Chapter 1:In this chapter,it includes introduction,statement of the problem,scope of

the study,objectives of the study,research design,sample design,tools for analysis and

limitations of the study.

Chapter 2:In this chapter,it specifies conceptual review and empirical literature.

Chapter 3:This chapter consists of company profile.

Chapter 4:In this chapter,the data analysed in a detailed manner.The data are

represented in bar chart and pie chart

Chapter 5:Findings and conclusion from the data analysed are represented in this

chapter.

CHAPTER II

REVIEW OF LITERATURE

5

2.1 Review of Literature

Since 1990’s,payment systems has undergone drastic changes.Important

developments responsible for these changes are rapid increase in usage of debit and

credit cards;computerisation in banking operations and the introduction of world

wide web(www).These changes lead to tremendous changes in digital cash

transactions.As digital transactions are easy,inexpensive,fast and secure,more and

more people around the world are using cashless payment system.For Central banks

and governments,less currency is in circulation and it is less burden for their

economy. Use of smart mobile phones,which can be carried as a personal device

gave a big push in the development of digital economy.

Over the last decade,online shopping has come up in a big way and many of the

online business firms has come up with their ‘apps’ for cashless transactions.

In India,economy is booming since the introduction of liberalisation in 1991 and the

concept of digital transaction was a welcome change .Reserve Bank of India took the

role of facilitator in making these changes available in banking operations with the

introduction of RTGS,NEFT,Aadhar enabled BHIM app etc.Value of internet

economy in India in 2020 is around US $ 250 billion .

Digital payment systems like Paytm and Phonepe are of Indian origin is popular in

India over the last decade.Amazon Pay was launched in India in 2017.Although

Google Pay made a entry during late part of last decade,it became very popular soon.

Studies on usage of cashless payment systems in India are very few.Digital payments

is in evolving stage and many new systems and new versions of the existing payment

systems are introduced every year.Literature search didn’t show any serious study on

penetration of cashless payment systems in Kerala nor comparative studies on usage

of the system and customer satisfaction.

6

2.2 Conceptual review

History of e-payment systems in India

History of evolution of e-payment systems in India is fascinating. In 1991 India

introduced liberalization policies that allowed the entry of private banks into the

country.HSBC was the first bank to set up an Automated Teller Machine(ATM) in

India.Soon,ATM’s began spreading through the country and ‘plastic money’,in the form

of debit cards and credit cards,slowly began gaining popularity as well.According to RBI

statistics,there are currently over two lakh ATM’s operated by 46 banks in

India.Computerisation first entered the Indian banking industry in 1988,and internet

banking in the 1990’s. After the path breaking step of ‘Liberalisation of Indian Economy’

in 1991 by Dr Manmohan Singh , licences were issued for establishing new generation

private banks .Notable among them were HDFC Bank , ICICI Bank , Axis Bank and

Kotak Mahindra Bank. These ‘Newgen ‘ banks are at the forefront of digital

transformation of banking industry in India at present.

In the 2000s online payment systems-like Real Time Gross Settlement(RTGS), National

Electronic Funds Transfer(NEFT),started being used.While NEFT and other forms of

online payment required a computer and often featured lengthy transaction times,the new

wave of e-payments brought about by digital wallets has made transferring money a lot

easier and quicker.Since internet availability and smartphone usage have become

virtually ubiquitous,e-wallets like PayU,Paytm,Google Pay and MobiKwik are being

used by millions for financial transactions,both personal and commercial.The

government,too is pushing its‘cashless economy’ policy with the Unified Payments

Interface(UPI)system backed up by the BHIM App-an Aadhaar-based mobile wallet

which can used to make digital payments directly from bank accounts.. Success of UPI

scheme in fast transfer of cash by digital means is unprecedented.

Demonetisation move of 2014 saw a sharp uptake in cashless transactions. In November

and December 2016-mobile wallet transactions recorded a 114 percent rise,Point of

Sale(PoS) transactions showed a 88 percent rise and mobile banking transactions rose by

30 percent .From November 2016 to May 2017,the total digital transactions in India went

7

up by 23 % .Demonetisation move of 2014 saw a sharp uptake in cashless transactions in

November and December 2016-mobile wallet transactions recorded a 114 percent

rise,Point of Sale(PoS) transactions an 88 percent rise,and mobile banking transactions a

30 percent November 2016 to May 2017 ,the total digital transactions in India went up by

23 percent,from 22.4 million to 27.5 million.A Google-BCG study also predicts that the

Indian digital payments industry will grow to $500 billion by 2020,accounting for 15

percent of the GDP.But in a country whose economy was 90 percent cash-reliant pre-

demonetisation,cash remains the most commonly used medium for financial

transactions.RBI data shows that as of April 2017, Rs 2171 billion was withdrawn via

ATM’s,while UPI transactions at that point were at Rs 22.41 billion,meaning that UPI

replaced cash by merely one percent.Unlike digital payments ,which rely on a steady

internet connection and acceptance from both buyer and seller,cash is quick,easy,and

instantly available for further offline transactions.That makes it the mode of payment of

choice for Indians right now.This is unlikely to change until the digital infrastructure in

the country is improved to the extent that every Indian,no matter how remote their

location,can make digital transactions as easily as they can pay with cash.

The future of digital payments lies in providing further simplified and secured user

experience,while increasing its adoption by leading socio-economic changes at the grass

root level.Mobile wallets are good,but still need taking out the smartphone followed by

some action by the user,which is no better than taking out the credit card for

payment.Next simplification lies in secure identification and payments(by face

detection,voice,sound)which can further disrupt and exponentially grow the digital

payments wave.

We are still a long way from reaching a stagnation point for innovation in digital

payments,considering the fact that every tech giant in the world is competing to amaze

their customers(or capture new ones)with an improved payment process.We are all set to

take the big leap in making payment an action driven to an intention driven process.

For the old generation,the moment someone utters the word ‘bank’,we generally visualize

cheque books,files,tellers,and papers along with a number of crunching bankers in

8

cubicles.But try explaining this to a millennial banking customer,he may miss the

picture.Today,banks have undergone a complete makeover,becoming more

viable,accessible and hi-tech.Internet banking,mobile banking,SMS banking,e-wallets,etc.

have made banking an evolving independent universe.

The Problem

Increasingly ,people are getting accustomed to new age banking technologies while

enjoying banking from the comfort of their homes.

But,it hasn’t removed the glitches in the system.Sharing of personal and sensitive

data,prolonged transaction time & method, and reliance on data connection are some of

the drawbacks existing in the system.

UPI or Unified Payments Interface is a payment system,launched by National Payments

Corporation of India (NPCI) and regulated by the Reserve Bank of India that facilitates

the instant fund transfer between two bank accounts on the mobile platform.UPI is the

back bone of the many of mobile based payment systems introduced in India.It’s a

transformational change that has triggered a paradigm shift in the payment sector while

facilitating a more cashless economy and sculpting a newly modeled Digital

India.UPI,being implemented in 30+ banks have enabled consumers to resolve banking

issues.

The un-banked population can be classified into broad categories: those who do not open

accounts due to lack of banking infrastructure, those who for various reasons (such as

poverty and lack of valid identity papers) do not pass the required account opening

criteria, and those who currently see no requirement to open an account. This process can

be broken into three aspects: opening a bank account, managing the account, and having

access to a set of financial services and products. To open an account, one has to satisfy

the bank’s KYC (Know Your Customer) norms. For the un-banked, providing a valid

identity is a challenge. To that end, the Unique Identification Authority of India (UIDAI)

has embarked on a mission to offer a single source of identity verification which can also

be used to open bank accounts. Managing the account is something that mobile money

solutions will make much easier, faster and cheaper, both for the customers and the banks.

9

The key challenge is to determine if it is possible to devise demand driven financial

products and services which make for a compelling reason to open an account. For

example, a common need is a low value, low cost loan, for which the un-banked can

typically offer no collateral. If this need can be addressed, via an appropriate business

model, then managing that loan in terms of repayments is much easier over a mobile

device. In this context, mobile payment solutions can certainly help by providing an

effective channel for money transfer for both categories of the un-banked.

The issue of depositing money into a bank account where banks do not have a presence is

addressed by the concept of banking correspondents.

Though mobile payments allow payments to be made electronically, they do not enable

depositing money into a bank. The Reserve Bank of India (RBI) tended to this issue by

creating the post of a banking correspondent (BC). The role of a BC is to act as an

interface between the bank and its customers in places where traditional banking is not

feasible. Banks can appoint a trusted third party as a BC in a village. All the villagers

who wish to transact with the bank can get in touch with the BC. Deposit and withdrawal

of money is handled by the BC. When a person deposits money at the BC, their account

immediately gets credited. The person can then use their mobile phone for additional

transactions.

The major difference between mobile banking and mobile payments is the total

absenteeism of the bank account number. In mobile banking or Internet banking, money

can be transferred only when the account number of the payee is known before-hand. The

account of the payee has to be registered with the payer and only then can a fund transfer

happen.

In mobile payments, the account number is masked from being public. One need not

know the account number of a person to transfer money. This opens up a range of

possibilities from buying tickets to paying auto fare, both of which would not have been

feasible had the account number been mandatory for a simple transaction.

In the case of India, the RBI has played a pivotal role in facilitating e-payments by

making it compulsory for banks to route high-value transactions through real-time gross

10

settlement (RTGS) and also by introducing NEFT (National Electronic Funds Transfer)

and NECS (National Electronic Clearing Services) which has encouraged individuals and

businesses to switch. India is one of the fastest-growing countries for payment cards in

the Asia-Pacific region. Behavioral patterns of Indian customers are also likely to be

influenced by their internet accessibility and usage, which currently is about 32 million

PC users, 68% of whom have access to the net. However these statistical indications are

far from the reality where customers still prefer to pay "in line" rather than online, with

63% payments still being made in cash. E-payments have to be continuously promoted

showing consumers the various routes through which they can make these payments

like ATM's, the internet, mobile phones and drop boxes.

Due to the efforts of the RBI and the (BPSS) now over 75% of all transaction volume are

in the electronic mode, including both large-value and retail payments. Out of this 75%,

98% come from the RTGS (large-value payments) whereas a meager 2% come from

retail payments. This means consumers have not yet accepted this as a regular means of

paying their bills and still prefer conventional methods. Retail payments if made via

electronic modes are done by ECS (debit and credit), EFT and card payments.[2]

10 Best Indian Payment Gateways in 2020:

1.Google Pay

2.PhonePe

3.Dhani

4.BHIM Axis Pay

5.PayTM

6.MobiKwik

7.Yono by SBI

8.ICICI Pockets

9.HDFC PayZapp

10.Amazon Pay

11

2.3 Empirical Literature

Dr Pallavi.P & Meenal.A(2018)studied the frequently used electronic payment system by

the e-commerce users of Indore Division.It was found from the study that Debit card is

the most frequently used e-payment system amongst the e-commerce users.Net banking

is second most frequently used type of electronic payment system.E-cash/E-wallet like

Paytm etc is third type of e-payment system which is used amongst the e-commerce

users of e-payment system.Lastly,Credit card is the least used type of e-payment system

amongst the e-commerce users. The study addresses the primary concerns of the e-

commerce users of different types of electronic payment system and targeting the

broader segment of potential customers to use the different types of electronic payment

system.

Dr.S.Manikndan & J.Mary (2017)in their study in Chennai city showed mobile wallet

usage awareness was spreading among the people in India due to government policy of

demonetization.The security issues are tight and reduced risk factors will automatically

increase the adoption of mobile wallet.Apart from these issues the convenience and ease

of use has gained popularity for mobile wallet and it can be concluded that there will be a

tremendous growth in adoption of mobile wallet in the forthcoming years.

Dr.Sangeetha & K.Myilswamy(2020) on their study on electronic banking in people

around Coimbatore showed that the technology is useful to customers as well as banks

and other organizations.To increase efficiency ,service quality of banks ,safety and

integrity, E-Banking can be used in a rightful way.Based on the results,there is no

significant difference between personal factors like age, profession,annual income and

category of the bank chosen and the satisfaction level of the customers.Also there is no

significant difference between personal factors like age,profession,annual income and

category of the bank chosen and the problems of E-Banking services.The result of the

study shows that customers are using only few facilities of various E-Banking services

available.

Sumathy &K.P.,(2017) found that it is necessary to move away from the cash-based

system to cashless (electronic)payment system. The results showed that it will provide

12

several advantages like it reduces the currency management cost,track every transactions,

check tax avoidance or fraud etc., enhances financial inclusion and progressively

integrate the parallel economy with the main stream.Furthermore,the usage of mobile

wallets crosses the boundaries of big cities and gains popularity in villages also.

Khan et al(2017)examined that a better integration of online payment systems with the

present financial and telecommunication infrastructure was needed for a prosperous

future of this payment mode.They also found that future work may be directed towards

the legislation of various factors responsible for contributing in the effective adoption of

online payment systems all over the world.

Javed Anwar(2017)direct comparison between Google Tez and Pay tm is not easy

because both of them work differently. Google Tez connects to your bank accout using

Indian government Unified Payment Interface(UPI),which is an interface that allows

money to be moved from almost any bank account in India to any other account

immediately and in real-time.When the user installs Paytm,he or she also has to create a

Paytm account.This account then becomes an e-wallet where certain amount of

money(the monthly limit for regular users is Rs 20,000)can be kept.This e-wallet,once

the money is gone,has to be recharged using a debit card,credit or through Paytm

authorised recharge points.

Sanchita Dash(2020)Google Pay has taken a comfortable lead in India’s payments market

over rivals like PhonePe, Amazon Pay,and a one-time market leader,Paytm.However, for

Google,the up and coming Whatsapp Pay may prove to be the real challenge.Google Pay

had 75 million transacting users in May 2020,while PhonePe had 60 million users and

Paytm had 30 million.

Rakuten(2020)According to a survey conducted by Rakuten Insight in India,a large share

of respondents between 16 to 54 years of age stated to have frequently used some form of

e-payment method as of February 2020.Around 30 percent of respondents between 16 to

34 years of age stated that they used electronic payment methods everyday,wheras only

six percent of respondents who were 55 years or older used e-payment methods daily in

India.

13

Shakir Ali & Wasim Aktar (2017)concluded that India was fast emerging as one of the

largest and strong economies.For sustained development and growth with robust

economic development,certain integral factors like improved transparency,corporate

governance and restricting the parallel cash based economy was essential.Such

developments could be feasible only with rural India also embracing the digital payments

and digital transactions.Considering the quantum of opportunities that are unfolding for

market dynamics of digital payments,improved solutions in terms of UPI’s,mobile

wallets,and digital transactions with more secured features,ease of transactions and

reduced cost of managing the digital payments could lead to more potential developments

and supporting in improved conditions of digital payments processing in rural sectors.

Ashwin Gadge &Dr.Priti(2019)found that,from the various available techniques of

payment,digital or non-digital,maximum 32% of the customers still use cash as the

preferred mode of transaction,Debit/credit cards(28%),NTFS(2%),Mobile wallets(31%)

and RTGS(null)and net banking(7%).It was found from the research that the use of

mobile wallets is becoming very popular among the residents of village Bramhapuri.

Respondents agree that digital payment is very important and plays a significant role as it

saves the very crucial time of the people,but,there is moderate agreement by the

customers towards improvisation in the quality of services with the introduction of digital

banking and payment sources.It was found that the people felt traditional banking was

better and convenient way and this was the main reason for not choosing digital payment

techniques.Backup power problem and load shedding are also to be done on regular basis

in rural area,which also hamper while implementing digital payment system as it requires

constant supply of electricity.

CHAPTER III

COMPANY PROFILE

14

3.1 Introduction

Speed of evolution of mobile digital payments is unmatched in the history of payment

system.Important catalysts in this unparalleled changes are the computerisation of

banking system,introduction of internet in late 1980’s and the universal use of mobile

phones.Ease of use,speed of operation and secure nature of transactions made the system

to thrive.As years go by,people want their transactions to be faster and safer and the

systems are evolving all the time.

Over the last decade,many online business companies,banks,start ups and even net

browser company like Google have come up with apps for digital transactions.Most of

these transactions are free of cost.

For online business giant like Amazon,payment system made the process of purchase and

transfer of cash made very easy.For internet search engine company Google,it is a means

of maintaining their brand name.Since the brand Google is a popular household

name,customer base is increasing in geometric progression.

Last decade has also seen the introduction and increasing popularity of mobile payment

systems like Paytm,Phonepe in India.Now almost any transactions like cash payment on

purchase,bill payment,transfer of cash or paying for your train or cinema tickets can be

made through digital system.

Competition in this field is fierce and cut throat and the Indian start up companies will

find it difficult to survive and to make profit.Hopefully,this study will throw some light

on the usage of e-payment systems in Kerala and also will find out the customer

satisfaction with the usage of cashless payment systems.

3.2 Top 10 Digital Payment Systems in India in 2021

As shopping patterns continue to evolve,thanks to Covid 19,even mobile and digital

wallets in India have evolved with it.With UPI making payments seamless,mobile wallets

and digital payment apps have been surpassing credit card usage and are slowly

beginning to replace the traditional payment methods.

15

A mobile wallet or digital wallet,in simple terms,is a virtual mobile-based wallet where

one can store cash for making mobile,online or offline payments.There are various types

of mobile wallets in India,such as open,semi-open,semi-closed and closed-depending on

the type of usage and payments that can be made.Wallets are growing rapidly as they

help in increasing the speed of transaction,especially for e-commerce companies and all

e-commerce marketplaces have integrated with such mobile wallets too.With the launch

of UPI,it has become even easier,as the transfer happens directly from the bank account

rather than from a wallet.

Here are some of the top 10 digital wallet and the top online payments apps in India and

what they offer to their customers.Top pick is Google Pay,which is also the No.1 digital

wallet and UPI payment app right now.

1. Google Pay(formerly known as Tez)

As its part of the Google ecosystem,they have scaled up their use base quickly,despite

being a late entrant.It is currently the No.1 digital wallet and one of the top online

payments apps in India.With Google Pay we can send money to friends,pay bills and buy

online,recharge your phone-all via UPI and directly from bank account.Since Google Pay

works with existing bank account ,which means money is safe with the bank.There’s no

need to worry about reloading wallets and we don’t need to do additional KYC-which is

required for all the other apps.We can also earn scratch cards and other rewards,with the

cashback directly being transferred into the bank account.Now we can also recharge

mobile or monthly utility bills.Since the introduction of UPI,wallets have become very

popular with users preferring account to account transfer via UPI.

2. PhonePe(earlier part of Flipkart)

Next in the list of top online payment apps in India is PhonePe.PhonePe started in 2015

and in just 4 years it has been able to cross the 100 million download mark.From UPI

payments to recharges,money transfers to online bill payments,we can do it all on

PhonePe.Its got a very good user interface and is one of the safest and fastest online

payment experience in India.

16

3. Dhani

Dhani App is part of the Indiabulls group and has multiple features.It is not only a regular

e-wallet app but it can also be combined with Dhani SuperSaver Card.Dhani also has a

reward & loyalty program for Dhani customers wherein customers can play games and

win cash to pay for mobile recharge,EMI payments,Insurance,and also for new Dhani

products.This can be combined with Dhani Super Saver Rupay(physical and virtual

card)which has assured 5% cashback on all purchases done via the card and its

completely free for the first month.

4. BHIM Axis Pay

BHIM Axis Pay is a UPI banking app that lets transfer of money instantly to anyone

using just a smartphone.It can also make online recharges to a prepaid mobile and DTH

set-top boxes directly from the app.

5.PayTM

PayTM is one of the largest mobile commerce platforms and one of the top online

payments apps in India,offering its customers a digital wallet to store money and make

quick payments.Launched in 2010,this e-wallet app works on a semi-closed model and

has a mobile market,where a customer can load money and make payments to merchants

who have operational tie-ups with the company.It was originally the No.1 digital wallet

in India before UPI being introduced.Apart from making e-commerce transactions,this e-

wallet app can also be used to make bill payments,transfer money and avail services from

merchants from travel,entertainment and retail industry.They also have UPI enabled

payments.

6.Mobikwik

MobiKwik is an independent mobile payment network that connects 25 million users

with 50,000 retailers and more.This e-wallet app lets its users add money using

debit,credit card,net banking and even doorstep cash collection service,which can,in

turn,be used to recharge,pay utility bills and shop at marketplaces.Owing to the growing

17

need for convenience,MobiKwik has also recently tied up with large and small-time

grocery,restaurants and other offline merchants.

Another unique feature they have is their expense tracker which allows setting budget for

expenses across all payment instruments and it uses SMS data to analyse and control

spends.No wonder it made to the list of top online payment apps in India.

7.Yono by SBI

The mobile wallet application was launched by State Bank of India to let users transfer

money to other users and bank accounts,pay bills,recharge,book for

movies,hotels,shopping as well as travel.It’s semi-closed prepaid wallet offers its services

in 13 lamguages and is available for non-SBI customers as well.This app also allows its

customers to set reminders for dues,money transfers and view the mini-statement for the

transactions carried out.

8.ICICI Pockets

Pockets by ICICI is a digital bank that offers a mobile wallet for its customers.It provides

the convenience of using any bank account in India to fund the mobile wallet and pay for

transactions.

With Pockets,one can transfer money,recharge,book tickets,send gifts and split expenses

with friends.This wallet uses a virtual VISA card that enables its users to transact on any

website or mobile application in India and provides exclusive deals or packages from

associated brands.

9.HDFC PayZapp

PayZapp is a complete payment solution giving the power to pay in just One

Click.PayZapp lets us to recharge mobile,DTH and data card,pay utility bills,compare

and book flight tickets,bus and hotels,shop,buy movie tickets,music and groceries,avail

great offers at SmartBuy,and send money to anyone in our phone book.

18

10.Amazon Pay

Amazon Pay is an online payments processing service that is owned by Amazon.It is also

a top online payment app in India and the global market.Launched in 2007 globally and

in India in 2017,Amazon Pay uses the consumer base of Amazon and focuses on giving

users the option to pay with their Amazon accounts on external merchant

websites,including apps like BigBazaar etc.We also get to shop on Amazon using

Amazoon Pay.Amazon Pay has also tied up with fintech companies such as ZestMoney

to enable no-cost EMI payment options on its platform.This makes it easy for consumers

to purchase products on Amazon and pay for it through affordable monthly instalments.

CHAPTER IV

DATA ANALYSIS AND

INTERPRETATION

19

DATA ANALYSIS AND INTERPRETATION

Total of 50 respondents completed the online survey and all of them were using mobile

payment systems. Genders were equally represented in the survey.Overall,sample

comprised mostly of middle class population aged 18 years and above and all were

familiar with mobile payment solutions.

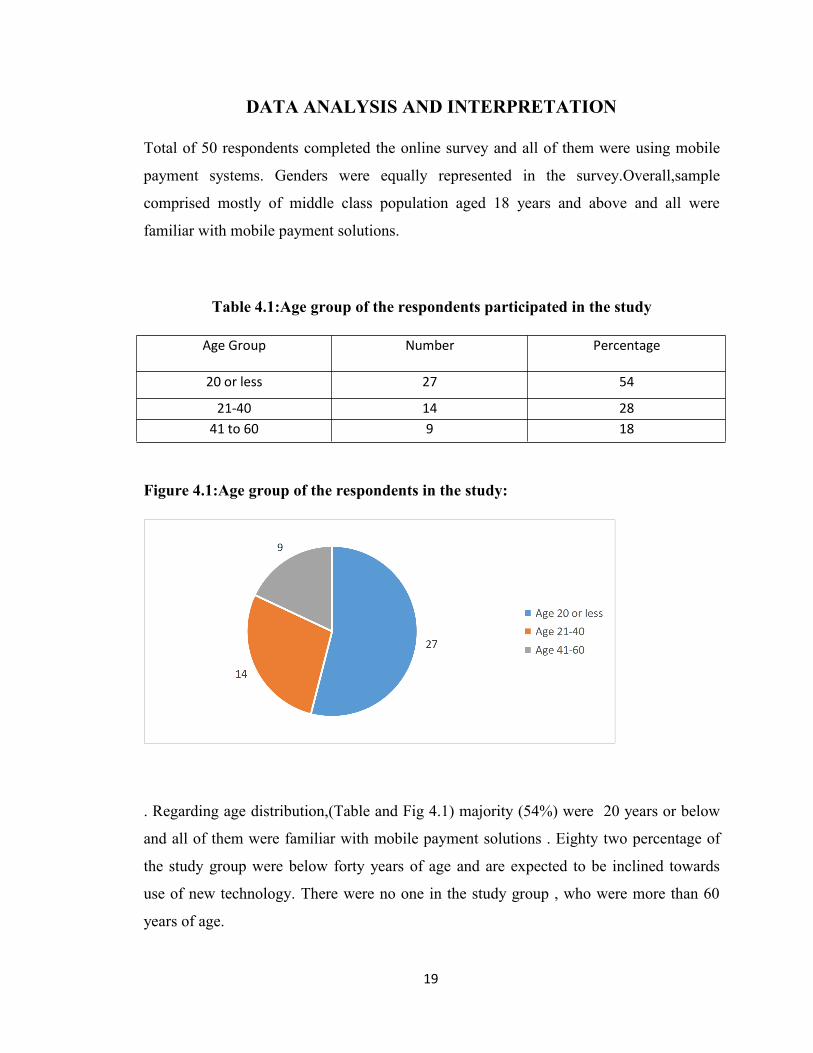

Table 4.1:Age group of the respondents participated in the study

Age Group Number Percentage

20 or less 27 54

21-40 14 2841 to 60 9 18

Figure 4.1:Age group of the respondents in the study:

. Regarding age distribution,(Table and Fig 4.1) majority (54%) were 20 years or below

and all of them were familiar with mobile payment solutions . Eighty two percentage of

the study group were below forty years of age and are expected to be inclined towards

use of new technology. There were no one in the study group , who were more than 60

years of age.

20

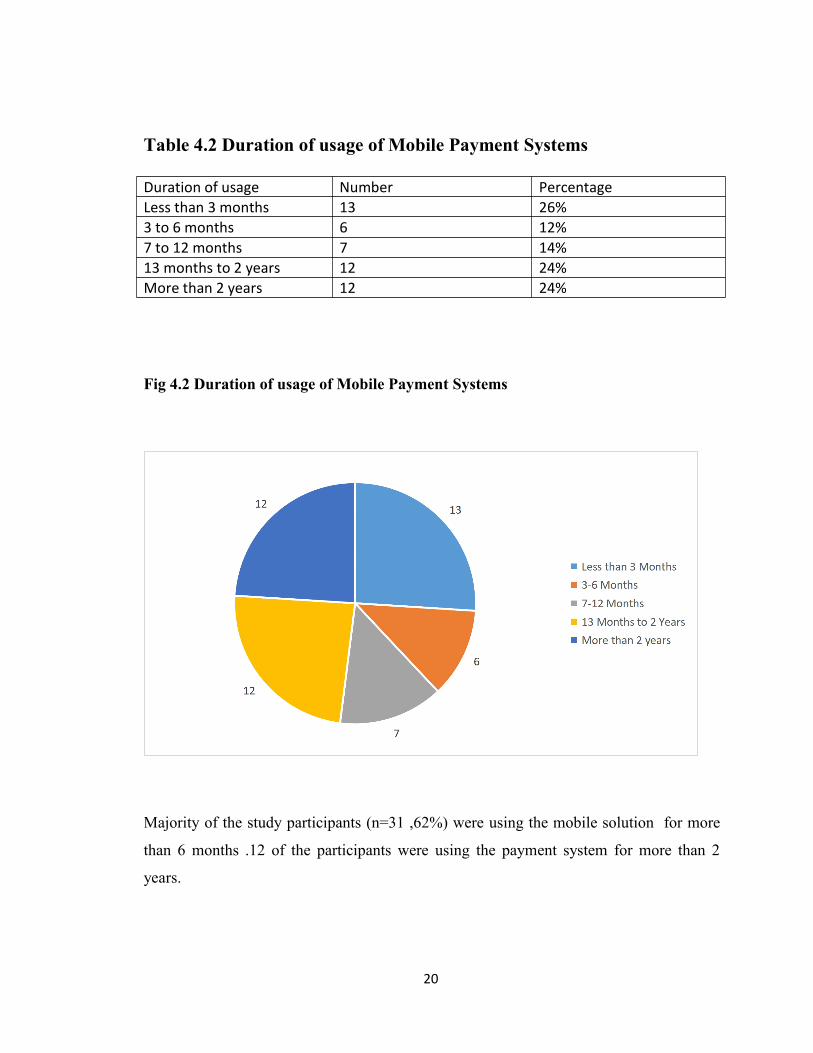

Table 4.2 Duration of usage of Mobile Payment Systems

Duration of usage Number PercentageLess than 3 months 13 26%3 to 6 months 6 12%7 to 12 months 7 14%13 months to 2 years 12 24%More than 2 years 12 24%

Fig 4.2 Duration of usage of Mobile Payment Systems

Majority of the study participants (n=31 ,62%) were using the mobile solution for more

than 6 months .12 of the participants were using the payment system for more than 2

years.

21

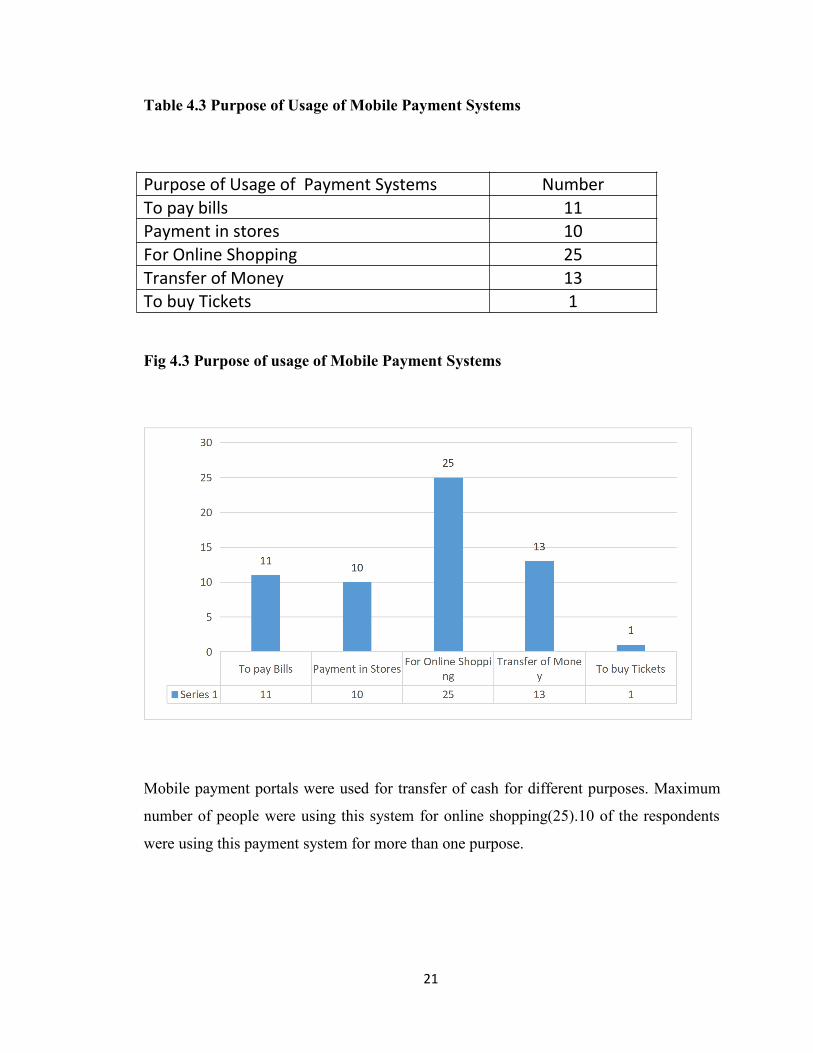

Table 4.3 Purpose of Usage of Mobile Payment Systems

Purpose of Usage of Payment Systems NumberTo pay bills 11Payment in stores 10For Online Shopping 25Transfer of Money 13To buy Tickets 1

Fig 4.3 Purpose of usage of Mobile Payment Systems

Mobile payment portals were used for transfer of cash for different purposes. Maximum

number of people were using this system for online shopping(25).10 of the respondents

were using this payment system for more than one purpose.

22

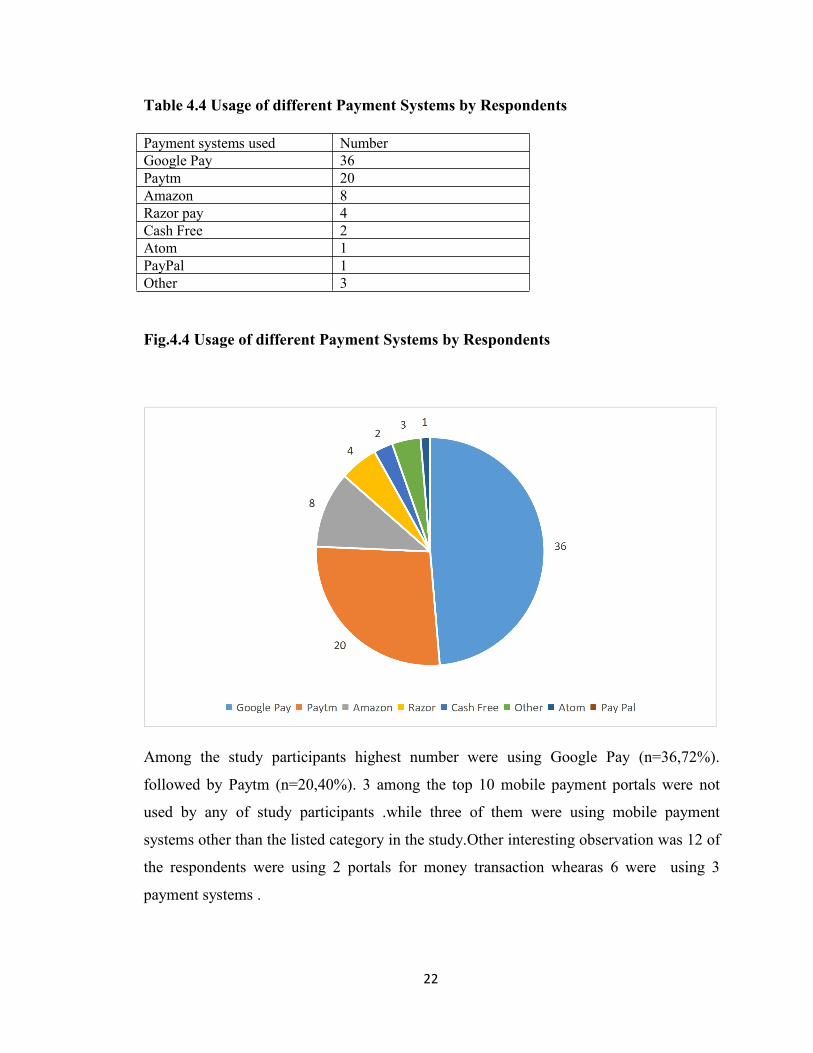

Table 4.4 Usage of different Payment Systems by Respondents

Payment systems used NumberGoogle Pay 36Paytm 20Amazon 8Razor pay 4Cash Free 2Atom 1PayPal 1Other 3

Fig.4.4 Usage of different Payment Systems by Respondents

Among the study participants highest number were using Google Pay (n=36,72%).

followed by Paytm (n=20,40%). 3 among the top 10 mobile payment portals were not

used by any of study participants .while three of them were using mobile payment

systems other than the listed category in the study.Other interesting observation was 12 of

the respondents were using 2 portals for money transaction whearas 6 were using 3

payment systems .

23

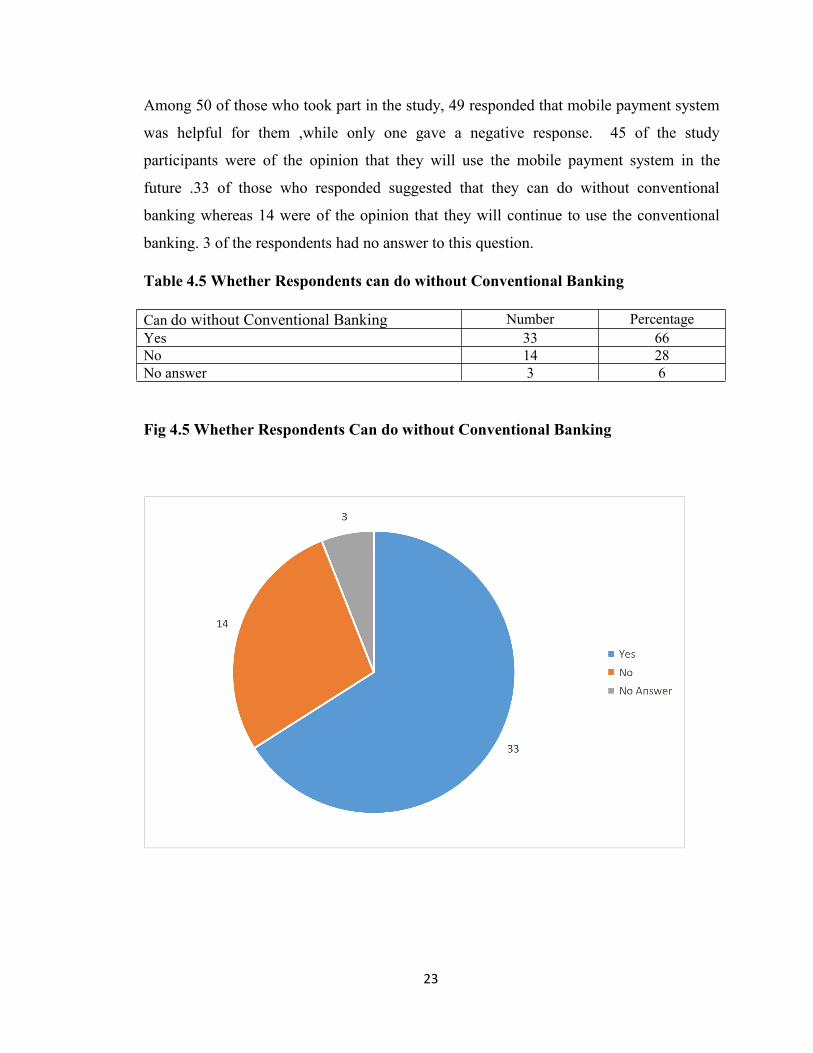

Among 50 of those who took part in the study, 49 responded that mobile payment system

was helpful for them ,while only one gave a negative response. 45 of the study

participants were of the opinion that they will use the mobile payment system in the

future .33 of those who responded suggested that they can do without conventional

banking whereas 14 were of the opinion that they will continue to use the conventional

banking. 3 of the respondents had no answer to this question.

Table 4.5 Whether Respondents can do without Conventional Banking

Can do without Conventional Banking Number PercentageYes 33 66No 14 28No answer 3 6

Fig 4.5 Whether Respondents Can do without Conventional Banking

24

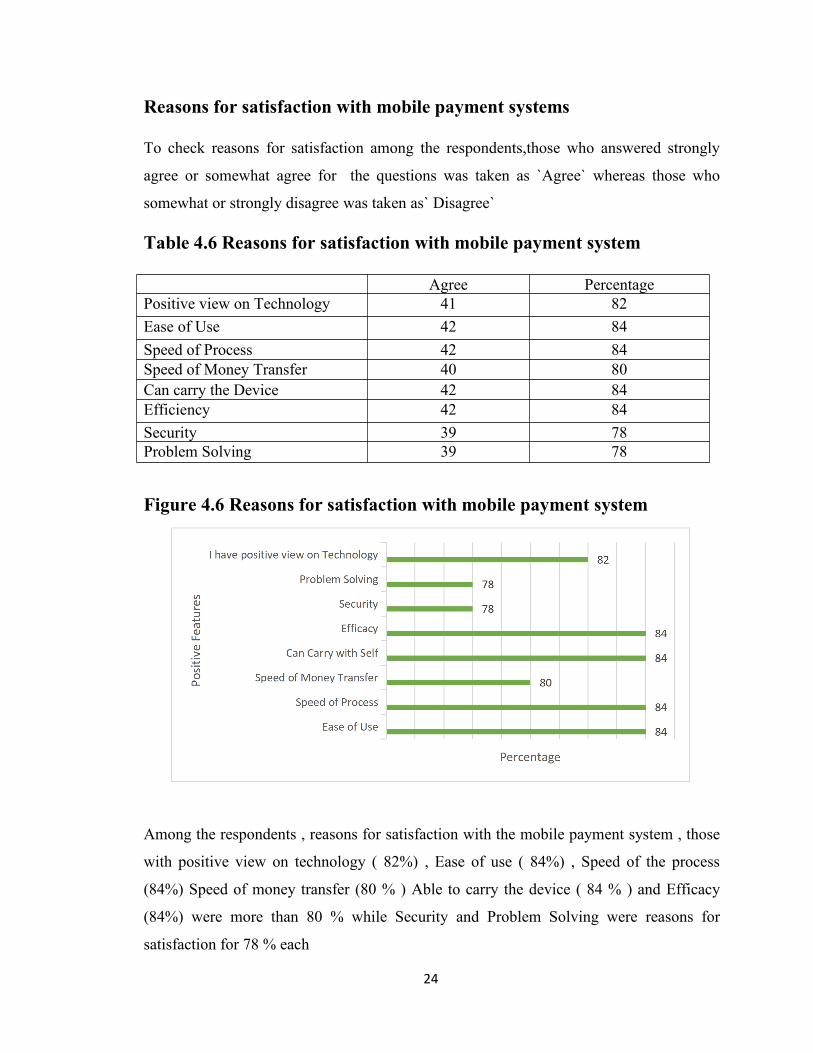

Reasons for satisfaction with mobile payment systems

To check reasons for satisfaction among the respondents,those who answered strongly

agree or somewhat agree for the questions was taken as `Agree` whereas those who

somewhat or strongly disagree was taken as` Disagree`

Table 4.6 Reasons for satisfaction with mobile payment system

Agree PercentagePositive view on Technology 41 82Ease of Use 42 84Speed of Process 42 84Speed of Money Transfer 40 80Can carry the Device 42 84Efficiency 42 84Security 39 78Problem Solving 39 78

Figure 4.6 Reasons for satisfaction with mobile payment system

Among the respondents , reasons for satisfaction with the mobile payment system , those

with positive view on technology ( 82%) , Ease of use ( 84%) , Speed of the process

(84%) Speed of money transfer (80 % ) Able to carry the device ( 84 % ) and Efficacy

(84%) were more than 80 % while Security and Problem Solving were reasons for

satisfaction for 78 % each

25

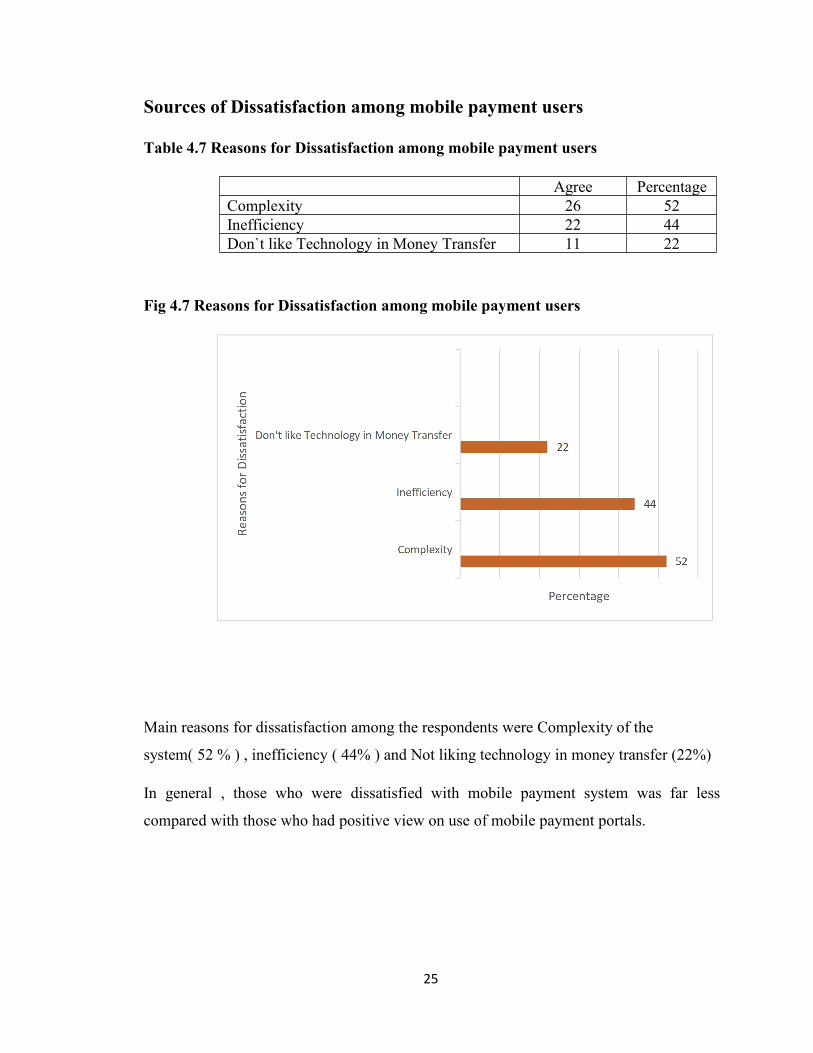

Sources of Dissatisfaction among mobile payment users

Table 4.7 Reasons for Dissatisfaction among mobile payment users

Agree PercentageComplexity 26 52Inefficiency 22 44Don`t like Technology in Money Transfer 11 22

Fig 4.7 Reasons for Dissatisfaction among mobile payment users

Main reasons for dissatisfaction among the respondents were Complexity of the

system( 52 % ) , inefficiency ( 44% ) and Not liking technology in money transfer (22%)

In general , those who were dissatisfied with mobile payment system was far less

compared with those who had positive view on use of mobile payment portals.

26

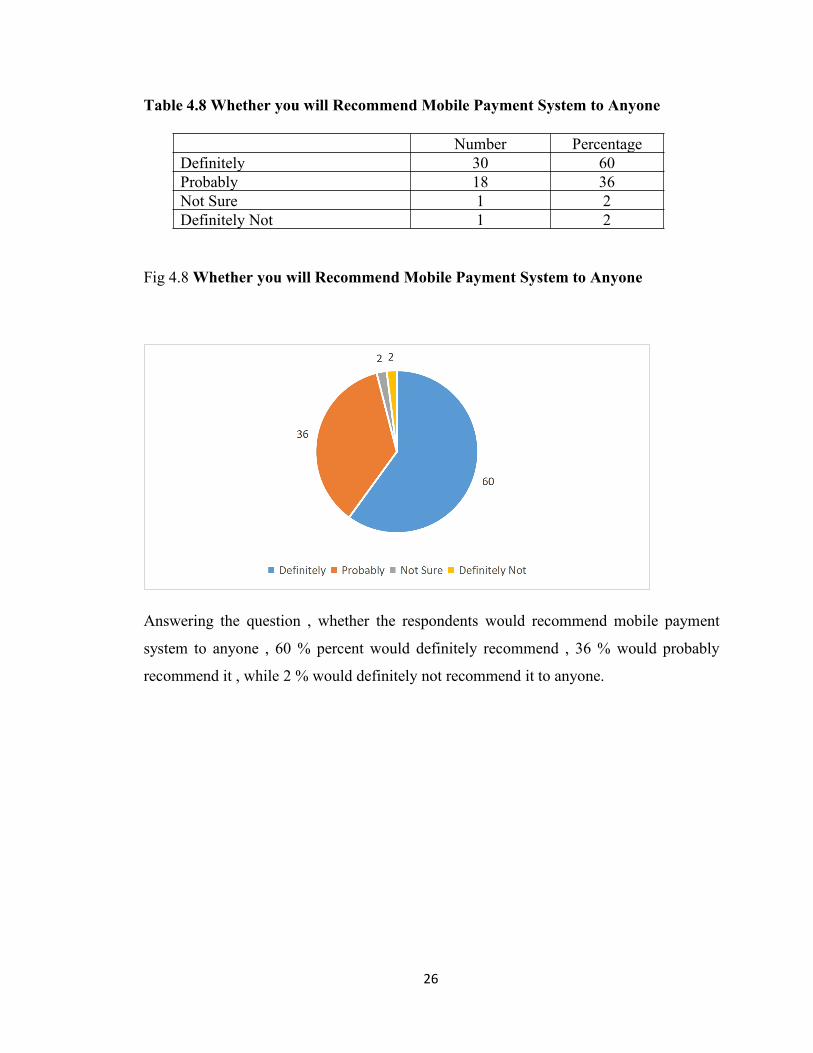

Table 4.8 Whether you will Recommend Mobile Payment System to Anyone

Number PercentageDefinitely 30 60Probably 18 36Not Sure 1 2Definitely Not 1 2

Fig 4.8Whether you will Recommend Mobile Payment System to Anyone

Answering the question , whether the respondents would recommend mobile payment

system to anyone , 60 % percent would definitely recommend , 36 % would probably

recommend it , while 2 % would definitely not recommend it to anyone.

CHAPTER V

FINDINGS , SUGGESTIONS AND

CONCLUSIONS

27

FINDINGS:

54% of the study participants were 20 years or less and are expected to be more

technology oriented,.82% of the respondents are 40 years or less and none in the study

are above 60 years .Hence with a higher percentage of younger population a positive

response towards the usage of technology is expected in study like this on use of

technology in money transfer.

Highest number of respondents(n=25) was using mobile payment portals for online

shopping . Next in order was for transfer of money,to pay bills and for paying in

stores.Only 1 among 50 of the study group was using the payment system for buying

tickets.10 among the study group were using the portals for more than 1 purpose

Majority of the study group (62%) have been using the payment system for more than 6

months and 24% were using it for more than 2 years

Regarding the usage of different payment systems, 36 in the study group were using

Google Pay while 20 of them were using Paytm.Amazon Pay was used by 8 respondents

while Razor ,Atom ,CashFree and PayPal weee used by smaller number of participants 3

of the top 10 mobile payment portals were not used by anyone in the study population 3

of them were using payment systems other than those listed in the study. 12 in the study

were using 2 payment portals while 6 were using 3 payment systems

49 of the respondents (98%) opined that payment systems was useful for them while 1 of

the respondents gave a negative response to the question. 72% of the respondents will

definitely use mobile payment system in future while 18% will probably use it. 4% will

not definitely use the system in the future

66% were of the opinion that with the use of mobile payment systems they can do

without conventional banking while 28% would still continue to use conventional

banking

28

Among the reasons for satisfaction with payment systems::

82% were of the opinion that they had a positive view on technology

84% each were satisfied with mobile payment systems because of

Ease of use

Speed of process

Can carry the device with them

Efficiency

80% were statisfed with the speed of money transfer

78% each were satisfied with the security and the problem solving capability of th mobile

payment system .

Sources of dissatisfaction among the respondents were

Complexity of the payment system: 52%

Inefficiency 44%

`Don’t like technology in money transfer` 22%

29

Suggestions

Understanding how users perceive current mobile payments and what drives their

satisfaction and dissatisfaction is important for mobile payment providers ,merchants

and consumers

Knowing what drives users to satisfaction can help mobile payment providers to

develop more successful future applications and improve existing solutions

Study should be done on larger population representing different age groups and also

people from different socioeconomic categories .

As the technologies are evolving at a rapid rate,studies should be done at regular

intervals to check the changes in customer satisfaction with changing times.

Moble payment systems consists of different categories like money transfer, online

payments , paying in stores and also paying bills

It is advisable to conduct studies in each category of payment to have more realistic

view on satisfaction/dissatisfaction among the users of these payment portals

Research also need to be done on merchants perspective to have different angle of

view on the payment portals.

Money transactions are essential part of every person`s day to day life . Government

should encourage more local payment portals to start as start ups with new

technology and give financial assistance to deserving candidates to thrive and

flourish.

30

Conclusion

Thus study on customer satisfaction of mobile payment users showed some interesting

findings.As the respondents were mostly in the late teens , 20’s or 30’s they are mostly

technology driven . Around 80% of the study population had a positive view on various

parameters of customer satisfaction .Sources of dissatisfaction are mostly because feeling

of complexity in the system and also because of a feeling that the system is inefficient

As time goes by new technologies will be added and the mobile payment system is bound

to improve As far as the government and central banks are concerned,with the new

technology, there is less requirement for printing of currency and also less currency in the

circulation . As the transactions are easy,secure and speed of money transfer is rapid

whether it is paying a bill,transferring money from one account to another or online

shopping,more and more people will use the technology for money transfers.

At present people in different walks of life whether rich or poor , young or old are using

smart phones, online payment system has come to stay and is bound to improve the

quality of life of future generations

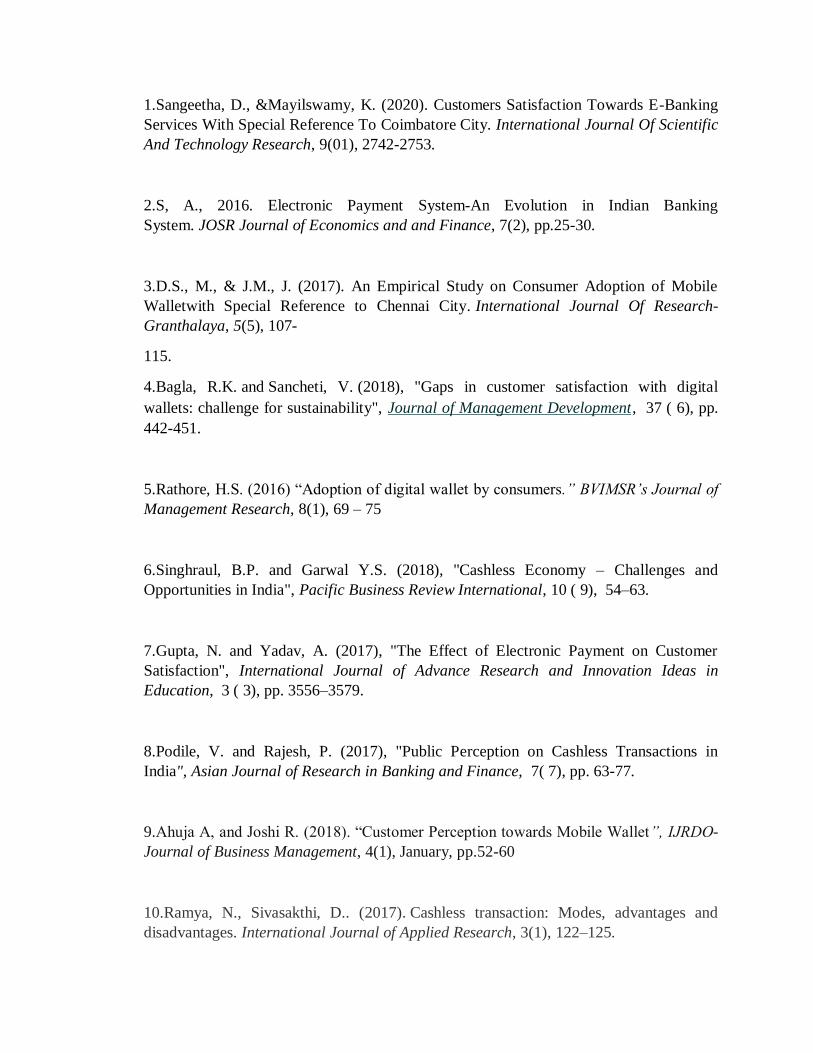

BIBLIOGRAPHY

1.Sangeetha, D., &Mayilswamy, K. (2020). Customers Satisfaction Towards E-Banking

Services With Special Reference To Coimbatore City. International Journal Of Scientific

And Technology Research, 9(01), 2742-2753.

2.S, A., 2016. Electronic Payment System-An Evolution in Indian Banking

System. JOSR Journal of Economics and and Finance, 7(2), pp.25-30.

3.D.S., M., & J.M., J. (2017). An Empirical Study on Consumer Adoption of Mobile

Walletwith Special Reference to Chennai City. International Journal Of Research-

Granthalaya, 5(5), 107-

115.

4.Bagla, R.K. and Sancheti, V. (2018), "Gaps in customer satisfaction with digital

wallets: challenge for sustainability", Journal of Management Development, 37 ( 6), pp.

442-451.

5.Rathore, H.S. (2016) “Adoption of digital wallet by consumers.” BVIMSR’s Journal of

Management Research, 8(1), 69 – 75

6.Singhraul, B.P. and Garwal Y.S. (2018), "Cashless Economy – Challenges and

Opportunities in India", Pacific Business Review International, 10 ( 9), 54–63.

7.Gupta, N. and Yadav, A. (2017), "The Effect of Electronic Payment on Customer

Satisfaction", International Journal of Advance Research and Innovation Ideas in

Education, 3 ( 3), pp. 3556–3579.

8.Podile, V. and Rajesh, P. (2017), "Public Perception on Cashless Transactions in

India", Asian Journal of Research in Banking and Finance, 7( 7), pp. 63-77.

9.Ahuja A, and Joshi R. (2018). “Customer Perception towards Mobile Wallet”, IJRDO-

Journal of Business Management, 4(1), January, pp.52-60

10.Ramya, N., Sivasakthi, D.. (2017). Cashless transaction: Modes, advantages and

disadvantages. International Journal of Applied Research, 3(1), 122–125.

APPENDIX

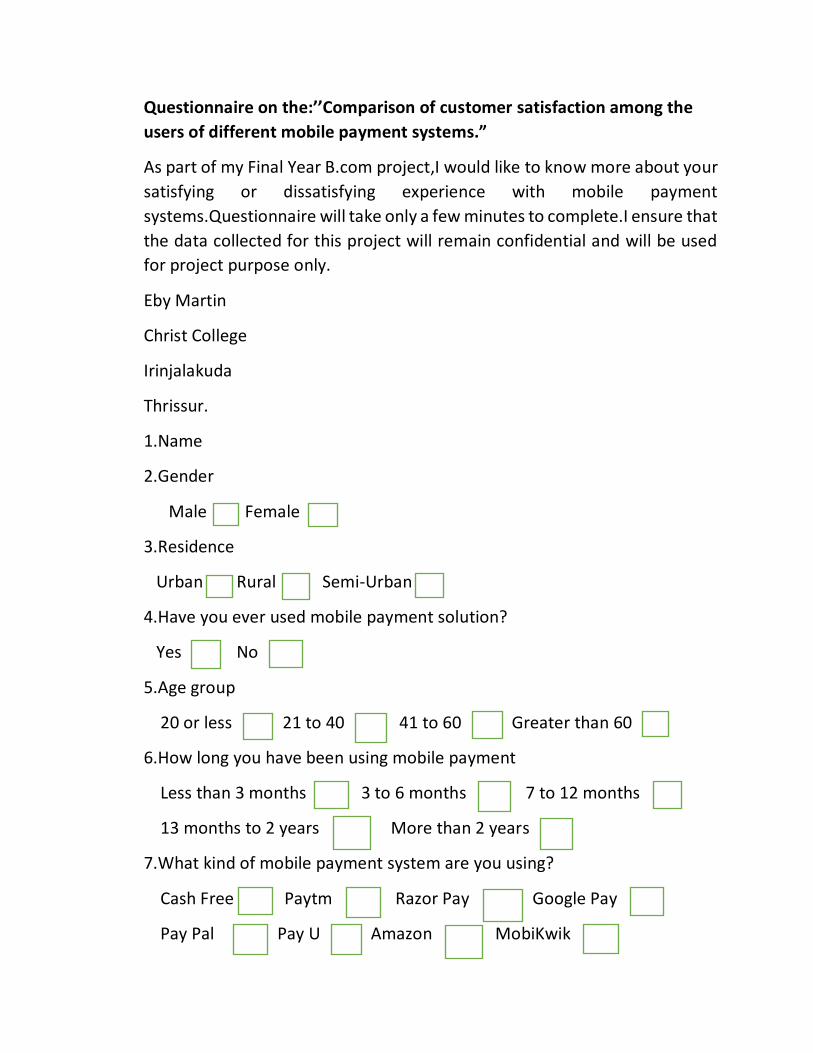

Questionnaire on the:’’Comparison of customer satisfaction among the

users of different mobile payment systems.”

As part of my Final Year B.com project,I would like to know more about your

satisfying or dissatisfying experience with mobile payment

systems.Questionnaire will take only a few minutes to complete.I ensure that

the data collected for this project will remain confidential and will be used

for project purpose only.

Eby Martin

Christ College

Irinjalakuda

Thrissur.

1.Name

2.Gender

Male Female

3.Residence

Urban Rural Semi-Urban

4.Have you ever used mobile payment solution?

Yes No

5.Age group

20 or less 21 to 40 41 to 60 Greater than 60

6.How long you have been using mobile payment

Less than 3 months 3 to 6 months 7 to 12 months

13 months to 2 years More than 2 years

7.What kind of mobile payment system are you using?

Cash Free Paytm Razor Pay Google Pay

Pay Pal Pay U Amazon MobiKwik

Atom Paykun Any other

8.Is the mobile payment system helpful for you during the COVID-19

situation?

Yes No

9.For what purposes are you using mobile payment?

Paying in store after purchase For online shopping

To pay bills To buy tickets Transferring money

to another person

10.Would you use the mobile payment in the future?

Definitely Probably Not sure

Probably not Definitely not

11.Can do without conventional banking

Yes No

12.Would you recommend the mobile payment to the colleagues or contacts

within your industry

Definitely Probably Not sure

Probably not Definitely not

Do you agree or disagree with the following statements

Strongy Somewhat Somewhat Strongly

disagree disagree agree agree

13.I have positive view on technology

14.Ease of use of

payment system

15.Speed of the process

16.Speed of the money transfer

17.Can carry the device with me

18.Efficiency of the system

19.Security

20.Problem solving

Sources of Dissatisfaction

Strongly disagree

Somewhat disagree

Somewhat agree

Strongly agree

21.Complexity of the system

22.Inefficiency of the system

23.I don’t like new technology in money transfer

Recommended