Country-specific institutional effects on ownership:concentration and performance of continentalEuropean firms

Victoria Krivogorsky Æ Gary Grudnitski

Published online: 6 June 2009

� Springer Science+Business Media, LLC. 2009

Abstract This paper examines the effect of country-specific institutional con-

structs on the relationship between ownership concentration and performance for

firms in the eight Continental European countries of Austria, Belgium, Germany,

Spain, France, Italy, the Netherlands and Portugal. Using data from publicly-traded

firms owned by other companies (i.e., blocks), measures of the quality of investor

and creditor protection and the effectiveness of legal institutions are applied.

Employing a hierarchical moderated multiple regression analysis, differential

validity is established for the relationship between ownership concentration and

performance as measured by return on shareholders’ funds. This differential effect

comes from creditor protection regimes and is consistent with a relational corporate

governance model based on debt finance and concentrated ownership.

Keywords Ownership concentration � Country-specific institutional effects �Differential effects � Creditors’ and investors’ protection regimes �Legality � Corporate governance � Relational-based systems

1 Introduction

As greater emphasis is placed on global investing, the comparability of business

environments has taken on an increased level of importance. This emphasis has

created a heightened interest in research that provides evidence about the effect of

diverse controlling business environments on the financial position of companies.

Accordingly, this study is framed by recent developments in the corporate

governance literature related to the role of institutional environments in corporate

V. Krivogorsky (&) � G. Grudnitski

Charles W. Lamden School of Accountancy, College of Business Administration, San Diego State

University, San Diego, CA 92182, USA

e-mail: [email protected]

123

J Manag Gov (2010) 14:167–193

DOI 10.1007/s10997-009-9097-6

performance, ownership structure and benefits extraction. Within a framework of

relational investor systems, country-specific, institutional regimes related to creditor

and investor protection and legal enforcement are examined to determine whether

they affect the relationship between firm performance and ownership concentration.

The objective of this paper is to provide information that will help alleviate the

uncertainties of those parties wishing to broaden their investment portfolio to

include firms from outside of market-centered systems.

As an example, for US investors who want to diversify their holdings to include

Continental European firms, our paper is intended to address concerns about

corporate governance regimes (i.e., concentrated ownership) dissimilar to those

found in the US by providing an empirical analysis of the extent to which

institutional factors, functioning as intermediaries in limiting opportunistic behav-

ior, reduce or mitigate effects between levels of concentrated ownership and firm

performance.

Our finding that creditor protection in Continental European countries has a much

stronger differential influence than investor protection in restricting the degree to

which a firm’s profitability is impacted by large shareholders is consistent with

superiority of pre-insolvency credit rules, which traditionally follow the corporate

law (including law of incorporation) in Continental Europe. This influence means

that creditor protection has an impact on regulatory competition in corporate law,

(Enriques and Gelter 2006). Traditionally, these rules were given the highest

priority in European Directives as well as in the laws of individual Member States.

Therefore, regulation conflicts on pre-insolvency rules have generally been settled

over the years, meaning that they have been an organic part of corporate law for an

extended period of time. Moreover, EU Directives related to the corporate law

generally leave most decision-making power to Member States, where regulators

view corporate laws within a context of their national legal culture.

Using data from 891 publicly-traded firms in the Continental European (CE

hereafter) countries of Austria, Belgium, Germany, Spain, France, Italy, the

Netherlands, and Spain that are owned by other companies (i.e., blocks), we first

tested for a relationship between ownership concentration of the block and

performance. When controlling for firm-specific characteristics of industry, size,

rate of growth, and main stock exchange, a positive and significant relationship was

found between the degree of block ownership and firm performance as measured by

return on shareholders’ funds. Applying measures of the quality of investor and

creditor protection and the effectiveness of legal institutions and employing a

hierarchical moderated multiple regression analysis, differential validity was

detected for the relationship between ownership concentration and performance.

The differential and mitigating effect appears to come from creditor protection

regimes dealing with the extent to which the rules of a credit information system

facilitate lending and the legal rights of borrowers and creditors in collateral and

bankruptcy laws. We believe this finding is consistent with a corporate governance

model based on debt finance and control by banks in the dual role of shareholders

and major creditors, and should help assuage the fears of investors who are

unfamiliar with relational- or concentrated owner-based systems.

168 V. Krivogorsky, G. Grudnitski

123

The remainder of this paper is organized as follows. Section 2 analyzes prior

research, Sect. 3 develops the hypotheses, Sect. 4 defines the variables and country-

specific indexes we employ, Sect. 5 defines the empirical model used, Sect. 6

describes the data used, Sect. 7 reports the results and Sect. 8 concludes the paper.

2 Prior research

This section is presented in two parts. The first part deals with alternative forms of

markets which distinguish major corporate governance models. Part two of this

section discusses the regulatory role of Continental European governmental

institutions and agencies in security markets, and the interaction between a firm

governance model and the institutional characteristics of the country in which a firm

is incorporated.

2.1 Market characteristics and governance structures

Economics literature (Roe 1993; Pistor 2004) identifies two major types of markets

which distinguish major corporate governance models: equity finance and control

by capital markets (‘‘market-centered’’), and debt finance and control by banks

(‘‘relational investor’’ or ‘‘controlling shareholder’’). Market-centered systems are

found mainly in common law countries such as the US and UK. They rely heavily

on market-related monitoring arrangements, and have built-in incentives and

disciplinary techniques designed to achieve superior managerial performance.

Further, market-centered systems are characterized by widely-spread shareholding

and thick financial markets.

In contrast to market-centered systems, relational investor systems exist in most

countries outside of the US and UK. Relational investor systems are characterized

by controlling inside coalitions, and thin trading of non-controlling stakes.1 An

important characteristic of relational investor systems is the existence of significant

banks, families, institutions and inter-corporate holdings (Faccio and Lang 2002),

firms with high debt-to-equity ratios and close ties to banks and in some cases, firms

owned by government or state entities.2 It is believed that the controlling

shareholder or dominant owner can help alleviate agency problems and serve as a

substitute or compliment to the market for corporate control (Jensen 1986;

Mikkelson and Partch 1997; Shleifer and Vishny 1986).

By introducing the dominant owner concept, we attempt to embrace the literature

on the congruence of voting and cash flow rights, and European laws impacting this

1 For example, according to the Netherlands Bureau for Economic Policy Analysis, in Germany 57% of

all large shareholders held more than 50% of an individual company’s stock, and 22% of all large

shareholders held more than 75% of an individual company’s stock. Additionally, in France, 59% of the

large firms had a majority owner.2 The World Bank/IFC survey (found at www.doingbusiness.org) reports that in 2007 the average

ownership concentration of firms in Italy and Austria was 58%, Germany 48%, Belgium 54%, and the

Netherlands 39%. These ownership concentrations for CE countries are in contrast to an average con-

centration rate of 19% for the UK.

Country-specific institutional effects on ownership 169

123

congruence. Because the European Union’s directive on large shareholdings (88/

627/EEC) is not supported by an efficient enforcement mechanism, meaningful

cross-country analysis is limited. As identified in European Association of Security

Exchange Dealer’s ‘‘Corporate Governance Principles and Recommendations,’’

cash flow rights in CE firms are widely dispersed and initial shareholders use one of

a variety of legal mechanisms (e.g., non-voting stock, trust company certificates,

voting rights restrictions) to retain or lock-in control of these firms.

Generally the controlling owner of a firm is defined as the one who controls an

absolute majority (i.e., over 50%) of the voting rights, or holds enough voting rights

to have de facto control. The de facto control threshold varies across CE countries.

For example, in France it is 40% whereas the mandatory bid threshold is 33.3%. As

a consequence of the difference in these two levels, an acquirer of a firm has to

make a mandatory takeover offer for all outstanding shares. In Germany the de facto

control threshold is 25% and the mandatory bid threshold established by the German

Takeover Code of 2002 is 30%.

Recent analyses of attempts to control shareholder activism show that monitoring

by financial intermediaries can be efficient in resolving collective action problems

among multiple investors (Calomiris and Kahn 1991; Black 1992; Rajan and

Diamond 2000). Financial intermediaries can be active in corporate governance and

corporate performance issues through the proxy process or through informal

discussions and decisions with the board and senior management of a firm. In CE

countries, thin equity markets and relatively small returns provide additional

incentives for financial intermediaries to be active.

Another rationale for relational investors to be more active in the controlling

shareholder system stems from market liquidity. Black (1990); Coffee (1991, 2002)

and Roe (1994) argue that it is precisely the highly liquid nature of the US

secondary markets3 that makes it difficult to provide incentives to large shareholders

to monitor a company’s financial position closely. Therefore, concentrated

ownership sacrifices liquidity, but enhances supervision, whereas dispersed

ownership enhances liquidity, but sacrifices supervision. Although closer proximity

lessens information asymmetry, there is an accompanying loss of critical

objectivity.

It is also worth noting that controlling shareholder ownership is not just

concentrated but stable over time. For example, in some CE countries (e.g., France),

companies reward shareholder loyalty by increasing their voting power. As a result,

freedom to make long-term investments often means pursuit of growth or private

benefits extraction at the cost of a suboptimal rate of return on equity investment.4

Hubbard and Love (2000) suggest that the level of private benefit extractions differs

among different types of controlling shareholders—extraction is lower when a

controlling shareholder’s stock is widely-held, as opposed to family-owned, and

when the divergence between control and equity is smaller. Obviously, regulatory

3 Enhanced liquidity in secondary markets is considered a benefit of dispersed ownership.4 It implies that equity investors in a relational system settle for a lower rate of return than investors in a

market system. In the case of institutions, the offsetting advantage lies in long-term business relationships

with the issuer.

170 V. Krivogorsky, G. Grudnitski

123

impediments matter less when controlling shareholders are involved, (Barca and

Becht 2001), unless the regulatory environments are robust enough to hinder the

controlling party.

The degree of discretion exercised by market institutions in a relational investor

system is less than in a market-based system. For example, in a relational investor

system governments actively intervene through rule enforcement to determine

which issuers have access to public financing. Governments in relational investor

systems, however, have shown little interest in specifying rules relating to market

microstructure issues or trading technicalities (Jackson and Roe 2008).

In areas where market infrastructure institutions enjoy regulatory responsibilities,

their powers are not exclusive because in most cases, regulators also bear some

authority in these same areas. Often, the law subjects the market institution’s

discretion in the exercise of its powers to oversight by a government agency. For

example, analysis of the regulatory framework in France suggests that rulemaking,

monitoring and enforcement of activities related to disclosure, corporate governance

and market abuse are under the Authorite des Marches Financieres (AMF—

administrative agency) supervision.5 In addition, all AMF rules require the approval

of the Ministry of Finance before going into force, and the Ministry can influence

the AMF deliberation process through its directly appointed representative on the

AMF board.

2.2 The role of government agencies and institutions in regulation

While the importance of investor and creditor protection has been addressed before

by LaPorta et al. (1998, 1999, 2000), Bushman and Smith (2001), Gugler et al.

(2003), and Gilson (2005), this study adopts a different perspective on the role of

institutional environments. First, we recognize that CE countries have a distinct

pattern of allocation of regulatory powers to government agencies and market

institutions. Coffee (2007) and Jackson and Roe (2008) characterize this pattern as a

‘‘government-led’’ model. In a government-led model, a central government shapes

the regulatory frameworks (regardless of a specialized administrative agency) to

maintain a tight grip over securities markets. Regulatory powers of market

institutions6 are conversely specific, carefully defined, and relate to areas where the

involvement of market institutions is strictly necessary (e.g., the trading process).

Even in these limited areas, the exercise of regulatory powers by market institutions

is often subject to approval by an administrative agency.

Allocation of powers in countries following the government-led model is

consistent with the view that stock exchanges are effective in regulating certain

aspects of securities markets where their involvement is either strictly necessary or

hugely beneficial. Even in these aspects, however, the regulatory role of stock

exchanges is kept to a bare minimum.

5 In Germany these activities are under the supervision of Bundesanstalt fur Finanzdienstleistungsauf-

sicht (an amalgamation of the administrative agencies previously responsible for the German insurance,

banking and securities industries) and Deutsche Borse (the Ministry of Finance).6 Market regulatory institutions can be considered as stock exchanges that provide a regulatory

framework for the operation of an organized market.

Country-specific institutional effects on ownership 171

123

In contrast to a government-led environment of limited rulemaking and authority

granted to markets, issuer disclosure in the US and UK for example, constitutes the

primary channel through which the market familiarizes itself with a firm. Especially

as ongoing disclosure takes place through bulletins and other methods of

dissemination of information that stock exchanges operate, the case for stock

exchanges retaining some regulatory powers over issuer disclosure is particularly

strong.

The second perspective we adopt is one in which institutional environments act

as intermediaries in limiting opportunistic behavior [Report of Center for European

Policy Studies (CEPS) 1995]. Specifically, indices of investor protection7 based on

the role of professional judges and attorneys, the level of legal justification required

in the process of dispute resolution, and the level of statutory control of or

intervention in a company’s administration are used. Further, CE states have

traditionally provided creditors with safeguards by emphasizing creditors’ protec-

tion in both corporate law and bankruptcy law (Enriques and Gelter 2006).8 In

particular, to measure the strength of creditors’ rights, we find indices of creditor

protection based on an analysis of practices utilized in each CE country to enforce

information correctness,9 creditors’ legal rights, and the level of information

disclosure available in the registries of these countries.

While the role of investor and creditor protection law on the books of a country is

instrumental in limiting opportunistic behavior, the picture is incomplete without a

measure of the effectiveness of a country’s institutions to enforce that law.

Accordingly, to measure the extent to which rules are consistently and successfully

enforced (i.e., their ‘‘legality’’), an index constructed by Berkowitz et al. (2003)

measuring the effectiveness of legal institutions is employed.

3 Hypotheses development

For purposes of this paper, two particular claims are central. First, a controlling

shareholder structure found in Continental Europe is associated with so called ‘‘bad

law.’’ This ‘‘bad law’’ is typically characterized by low equity market activism,10

distinct property relations and capital structure, which correlate with the qualities of

the institutional environment’s financial system architecture and legal environment

characteristics (Roe 1994; Bebchuk and Roe 1999). There is no consensus in the

literature, however, on why different countries developed different economic

strategies, which led to different ownership structures, and, eventually, to different

7 International Monetary Fund (2005).8 The Second Directive, Article 32 of the European Union Company Law requires a safeguard for

creditors in the event of reduction of capital. The Third and Six Directives require safeguards for creditors

in case of mergers and divisions (Articles 13 and 12, respectively).9 Practices to enforce information quality are measured as legal penalties for reporting inaccurate data,

the time to correct reported errors (usually less than two weeks), and the possibility of inspecting data.10 Typically controlling shareholders activism has an important impact on the performance and liquidity

of the equity market (Black 1992; Coffee 1991, 2002; Roe 1994). In CE countries, where equity markets

are thin and do not generate large returns, there is more reason for activism by concentrated owners.

172 V. Krivogorsky, G. Grudnitski

123

regulatory and financial systems. Bebchuk and Roe (1999) advocate an endogenous

explanation (i.e., a theory of path dependence) wherein powerful internal parties

such as managers and controlling shareholders are able to pressure lawmakers into

developing rules that allow internal parties to extract private benefits (this is the rent

seeking argument). LaPorta et al. (1998) and Leuz et al. (2003) dispute that

ownership concentration depends on the quality of regulatory systems. Instead they

advocate an exogenous explanation (laws and politics), and the way to improve the

efficiency of any system, whether its ownership is dispersed or concentrated, rests

with enhancing the quality of the regulatory environment and its enforcement.

The second claim central to this paper is that the function of the institutional

environment can be partially described by its role in solving agency conflict, which in

Continental Europe, is complicated in two ways. First, in most situations, agency

conflict is thought to arise from the separation of ownership and control. In the US

where shareholdings are widely-held, agency conflict is evidenced by the role of

independent directors serving on boards and instances of market devices such as

hostile takeovers. In Continental Europe, however, a controlling shareholder is viewed

as a key restraint on public corporation managers. This is the point that motivates the

efficiency defense of controlling shareholder systems. Because controlling share-

holders own large equity stakes for extended periods of time, they are more likely to

have an incentive either to monitor managers effectively or to manage the company

itself, and, because of proximity and lower information costs, nip agency problems in

the bud (Jensen 1986; Mikkelson and Partch 1997; Shleifer and Vishny 1986).

The other way the agency problem is complicated in Continental Europe relates

to the potential for controlling shareholders to extract private benefits using a degree

of control not afforded to minority shareholders (it drives the ‘‘bad law’’/controlling

shareholder regime nexus). Conditional on maintaining control, the less equity

controlling shareholders have, the greater their incentive to use control to extract

private benefits. This is due to the fact that increased productivity accrues to

shareholders in proportion to their equity, while the private benefits of control are

allocated based on governance power (Hubbard and Love 2000).

The efficiency of controlling shareholders can be further limited if a firm has its

own agency problems. Hubbard and Love (2000) suggest that the level of private

benefit extraction is lower when the stock of controlling shareholders is widely held.

To make a controlling shareholder system efficient, institutions must be instrumen-

tal in solving agency conflict by specifying substantive rules, requiring sufficient

disclosure and providing an effective enforcement mechanism to substitute for the

system’s lack of efficiency (Berndt 2000). For instance, LaPorta et al. (1999, 2000)

have identified various characteristics of the legal environment, such as the level of

investor and creditor protection, as being beneficial in solving the agency problem.

Additionally, Berkowitz et al. (2000, 2003) argue that enforcement and effective

legal institutions (hereafter denoted as legality) are critical for financial markets,

which in turn, are critical for economic development.

Balance achieved by the controlling shareholder structure depends on a tradeoff

between better monitoring and higher private benefit extraction. A difference in

attributes of institutional environments may result in a particular controlling

shareholder system having very different costs and benefits. Thus, the central

Country-specific institutional effects on ownership 173

123

implication of the controlling shareholder tradeoff structure is that national systems

can be consistent with alternative, and two very different equilibria (Durnev and

Kim 2005). Under the first equilibrium, the ownership pattern may reflect a structure

of an inefficient controlling shareholder system, where because of ‘‘bad institutions’’

the cost of private benefit extraction exceeds the benefit from monitoring

management, (i.e., minority shareholders are not worse off from controlling

shareholders’ monitoring efforts). Under the second equilibrium, the same

ownership pattern may reflect a structure of an efficient system because of the

‘‘good law.’’ Here, the benefit of monitoring exceeds the cost of private benefit

extraction. This more complex taxonomy provides a context to understand the role

of legal and quasi-legal institutions in supporting a particular ownership pattern.

Because the scales weighing better monitoring against higher private benefit

extraction may not always be tipped in the same direction or to the same degree, our

overarching hypothesis about the influence of blockholders11 on a firm’s perfor-

mance is without direction and is as follows:

H1 A firm’s performance is related to its ownership concentration by a block.

3.1 Differential factors

Differential factors on the relationship between ownership of a block and firm

performance are divided into two broad classes.12 These classes represent the

strength of a creditor’s and investor’s protection regimes in a country. Additionally,

the role that law plays in a country is further defined by incorporating the

differential factor of an index of legality.

3.1.1 The credit environment in continental Europe and the special role of banks

Two distinctive attributes characterize the credit environment in Continental

Europe. The first distinct attribute relates to the financial system architecture and

represents an institutional environment associated with the unique role of banks in

relational shareholder systems.

In Continental Europe the relationship of banks and clients is broadly defined as

‘‘the connection between a bank and a customer that goes beyond the execution of

simple, anonymous financial transactions’’ (Ongena and Smith 1998). Overall, the

role of banks in Continental Europe is consistent with the theory of trade off, which

suggests that generally in less liquid markets, banks have a higher involvement in

industries, but not necessarily through equity holdings (Bolton and von Tadden

11 A prevalent ownership concentration form in Continental Europe is another industrial company (i.e.,

block).12 We decided to exclude the importance of the equity market (IEM) as a differential variable mainly

because according to ORBIS, 86% of the firms in our sample list Euronext as their primary stock

exchange. Moreover, because of the research of Leuz et al. (2003) in which they found the importance of

equity markets in CE countries to be much less than those in Anglo-Saxon countries, we felt further

testing for a differential effect related to the importance of the equity market of a firm was unlikely to

yield worthwhile results.

174 V. Krivogorsky, G. Grudnitski

123

1998). The significance of primary banks comes from their role as the main source

of debt financing. As the Report of CEPS 2001 suggests, the overall level of debt

financing in Continental Europe is much higher than in the US.

Banks obtain their power through a nexus of circumstances. First, the power of a

bank in Continental Europe is increased directly as a result of its position as a holder

of both debt and equity of a firm, and as a custodian of the shares left to it by clients,

who have given written authorization to a bank to vote on their behalf. With this

power, expected default costs are reduced because a bank is interested in the overall

cash flow to either debt or equity claimants.13

A second factor adding to the power of banks stems from their ability to collect

information about customers and their role in negotiating loans. Through this ability

and by this role, banks are afforded a special position to affect the internal corporate

governance mechanisms of a CE firm. Bank representatives often sit on supervisory

councils and the management board, serve on interlocking Directorates, provide

capital, and work to cultivate overall strong relationships with senior management

(Pfannschmidt 1993; Schneider-Lenne 1994; Baum 1994; Becht and Boehmer 2003).

The second distinctive feature of the CE credit environment relates to the fact

that the European corporate law shields creditors. This shield is affected by granting

creditors an adequate system of protection under the First, Second (Article 32),

Third (Article 13) and Sixth (Article 12) Directives of the European Union

Company Law pertaining to the rules on disclosure, mergers, divisions and

reduction of capital. In effect, these Directives mimic market forces and provide

safeguards for creditors in the case of increased risk of default.

Accordingly, legal capital rules in Continental Europe are designed to reflect the

distinctive position of creditors. Contrary to US legal capital rules, CE firms are

subject to inflexible legal capital rules designed to mimic what is achieved in the US

through contractual bargaining and the use of bond covenants (Day et al. 2004).

With non-bond debt financing providing most of the capital, legal capital rules are

seen as helpful in providing a ready-made, off-the-shelf solution to reduce

transaction costs (Kubler 2004).

Some advocates for the legal model in Continental Europe view it as a means of

addressing the collective interests of creditors and to shield them from opportunistic

behavior that cannot easily be replicated contractually (Armour 2000; Schon 2004).

Lately, because of globalization, legal capital rules in Continental Europe have

undergone a transformation. Firms are beginning to use bonds as a source of capital.

Contracts are trending toward being based on profit and loss accounts and cash flow

statements data instead of balance sheet based measurements. These transformations

have caused the relationship of net assets to undistributed capital, which occupied a

central place in the traditional legal capital rules of CE counties, to gradually lose its

significance and be replaced by creditors originating their assessment of the

contractual terms from financial ratios (Citron 1992a, b; Day and Taylor 1996, 1997).

Firms consistently rate access to credit as among the greatest barriers to their

operation and growth. Historically, credit information correctness checkpoints and

13 This claim is applicable, however, only when a bank holds proportionate claims of all securities of a

firm.

Country-specific institutional effects on ownership 175

123

routine disclosure as well as creditor’s legal rights have been incorporated into the

universally applicable capital model employed in Continental Europe, and with

rigid capital rules losing their importance these two characteristics gain significance

as a part of a creditor protection mechanism to resolve collective action problems.

Following this line of reasoning, we hypothesize that credit information index14 and

the level of creditor legal rights index have strong differential validity on the

relationship between ownership concentration and performance.

H2 The relationship between ownership concentration by a block and perfor-

mance of a firm is affected if a firm is located in a country having strong creditor

protection regimes.

3.1.2 Investor protection

Along with the financial system architecture, this study examines the effect of three

specific characteristics of the investor legal environment that seems, a priori, likely

to be related to agency issues. In particular, the quality of the investor protection

regime assists in addressing the conflict between a controlling and non-controlling

shareholder. This conflict centers on the potential for a controlling shareholder to

extract private benefits of control, (which are not provided to a minority

shareholder) and drives the ‘‘bad’’ law/controlling shareholder regime nexus15

(LaPorta et al. 2002).

The LaPorta et al. (2002) study has already shown that the most basic

determinants of the corporate finance and governance in a country are the extent to

which a country’s law protects the rights of investors and the extent to which those

laws are enforced. A country’s investor protection scores used in the LaPorta et al.

(2002) study are largely based on shareholders’ voting rights from a corporate law

perspective. This approach follows the logic that an investor’s ability to exercise

rights assists in addressing agency problems, making the system more efficient.

Recognizing the extreme importance of the above claim, additional character-

istics of investor protection institutions are important in Continental Europe due to

the design of its corporate laws. Unlike in the US, where judicially-developed

principles of fiduciary duty are used, CE countries employ detailed legislation and

have comprehensive laws governing corporate groups (Black 2000). For instance,

individual shareholders in France are able by law16 to sue directors on behalf of the

corporation (action sociale ut sunguli), while, at least until recently, this was

difficult in Germany and even more difficult in Italy. The ability to sue directors in

France does not mean that French law is designed to favor the rights of minority

14 Practices utilized to enforce information correctness include legal penalties for reporting inaccurate

data and time to correct reported errors. Investor protection also includes several factors. Incorporated

into an index of creditor protection is the role of professional judges and attorneys, the level of legal

justification required in the process of dispute resolution, the level of statutory control or intervention of

the administration, admissibility and evidence evaluation and recording.15 This is consistent with empirical findings that firm value increase with the level of inside ownership, at

least over the lower ranges (McConnell and Servaes 1990).16 Although this ability to sue has long existed, it has only rarely been exercised.

176 V. Krivogorsky, G. Grudnitski

123

shareholders. In France (as well as in most CE countries), if the dominant owner

behavior has harmed the company, a court can deny minority shareholders the right

to sue if the law does not explicitly provide this right, and gives creditors of the

company priority in bringing suit. If an intention to harm (intention de nuire) cannot

be proven, shareholders are seldom given their ‘‘day in court.’’ In circumstances

such as these it is simpler to hold directors responsible for their actions as

individuals (‘‘qua individuals’’ or ‘‘qua investors’’ as opposed to ‘‘qua sharehold-ers’’), especially in cases of securities fraud, involving the failure to disclose

relevant information and providing false information on self-dealing transactions.

In this connection, investor protection characteristics related to the level of legal

involvement (such as shareholders’ ability to sue the directors for misconduct

(shareholders’ suability index or SSI)), matters related to public and shareholder

periodic disclosure (disclosure index or DI) and directors’ liability index (DLI) are

instrumental in supporting an effective legal process and limiting agency costs.

Accordingly, using these factors as the basis for determining an index of the

quality of investor protection, we hypothesize that in the CE countries where

corporate law consists of detailed legislation and rules instead of a broad principles-

based approach, the quality of investor protection has strong differential validity on

the relationship between ownership concentration and performance.

H3 The relationship between ownership concentration by a block and

performance of a firm is affected if a firm is located in a country having strong

investor protection regimes.

3.1.3 Legality

Motivated by the work of LaPorta et al. (1997, 1998) who make a case for the legal

code being the basis for efficient capital markets and development in post-socialistic

economies, Berkowitz et al. (2000, 2003) attempt to determine the importance of

enforcement and effective legal institutions (i.e., legality). They argue two key

notions. First, for the law to be effective, it must be meaningful in the context which

it is applied. Citizens of a country must have an incentive to use the law and demand

a country’s institutions enforce and develop the law. Second, legal intermediaries,

such as judges and lawyers, must have the capability and incentives to improve the

quality of the law in a manner which is responsive to the demand for legality by a

country’s citizens.

Berkowitz et al. (2000) believe that a country’s legality is really multidimen-

sional. These dimensions consist of measures of the effectiveness of the judiciary,

the rule of law, the absence of corruption, the risk of contract repudiation, and the

risk of government expropriation.

We believe that in the absence of effective enforcement and legal institutions, the

most comprehensive investor and creditor protection laws directed at limiting

opportunistic behavior by concentrated owners may be little more than ‘‘paper

tigers.’’ Accordingly, we hypothesize that in CE countries having strong legal

enforcement regimes, legality has strong differential validity on the relationship

between ownership concentration and performance.

Country-specific institutional effects on ownership 177

123

H4 The relationship between ownership concentration by a block and

performance of a firm is affected if a firm is located in a country having high

legality.

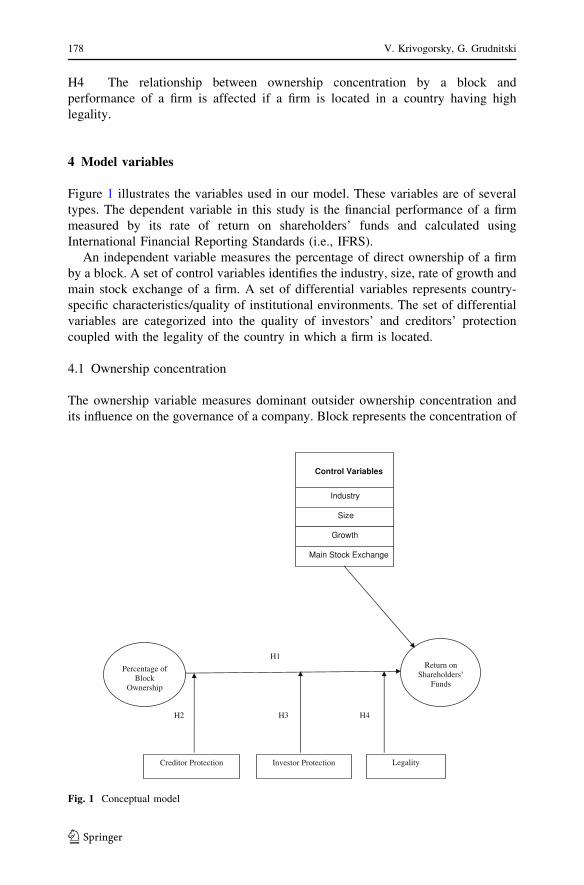

4 Model variables

Figure 1 illustrates the variables used in our model. These variables are of several

types. The dependent variable in this study is the financial performance of a firm

measured by its rate of return on shareholders’ funds and calculated using

International Financial Reporting Standards (i.e., IFRS).

An independent variable measures the percentage of direct ownership of a firm

by a block. A set of control variables identifies the industry, size, rate of growth and

main stock exchange of a firm. A set of differential variables represents country-

specific characteristics/quality of institutional environments. The set of differential

variables are categorized into the quality of investors’ and creditors’ protection

coupled with the legality of the country in which a firm is located.

4.1 Ownership concentration

The ownership variable measures dominant outsider ownership concentration and

its influence on the governance of a company. Block represents the concentration of

Return on Shareholders’

Funds

Control Variables

Industry

Size

Growth

Main Stock Exchange

Percentage of Block

Ownership

H1

Creditor Protection Investor Protection

H2 H3

Legality

H4

Fig. 1 Conceptual model

178 V. Krivogorsky, G. Grudnitski

123

blockholders’ ownership, and is stated in terms of the direct ownership of the largest

blockholder (another industrial company).

4.2 Country-specific characteristics

Over the last ten years most CE companies have joined the European Union (EU)

and transitioned to operating under its umbrella. This has resulted in these firms

having similar social and political climates, labor states of affairs, and employing

comparable levels of sophistication of business and financial management. EU firms

have operated in the same capital markets, with the same currency (the Euro). IFRS

was mandated in 2005 for those firms that were not early voluntary adopters.

EU firms belonged to the same section in terms of GDP per capita (www.rru.

worldbank.org). What remained different for CE firms were variations in the

country-specific17 characteristics pertaining to the quality of protection for investors

and creditors and the effectiveness of law enforcement.

We employ a set of measurements/environmental characteristics developed by

the World Bank and International Monetary Fund. These country-specific charac-

teristics are intended to assess the conditions of country-specific characteristics/

quality of institutional environments. Specifically, we examine the effect of five

specific types of legal business regimes within the categories of the quality of the

investor and creditor protection. Gauges of the quality of protection afforded

investors and creditors are indices formed by measuring the following character-

istics (see the Appendix for details about the construction and composition of each

index)18:

• Transparency of transactions (extend of disclosure index)—DI

• Liability for self-dealing (extend of directors’ liability index)—DLI

• Ability of shareholders to sue directors for misconduct—SSI

• Credit information index—CII

• Creditor legal rights—CLR

To the quality of creditor and investor law on the books, we include the numeric

values calculated by Berkowitz et al. (2000, 2003) for their legality index.

Berkowitz et al.’s (2000, 2003) legality index is constructed by aggregating the

individual legality proxies of the effectiveness of the judiciary, rule of law, the

absence of corruption, the risk of contract repudiation, and the risk of government

expropriation.19

Table 1 lists the value of each index for the eight countries from which our

sample of firms is drawn. From Table 1 we note that creditor protection based on

17 The country specific to a firm is the country in which the firm is incorporated.18 International Monetary Fund, World Economic Outlook Database, September 2005.19 Each proxy is on a 0 to 10 scale, where a value of 10 is highly effective and a value of 0 is highly

ineffective (or absent). For example, on the rule of law proxy the U.S. is scored 10 and South Korea is

scored 0. The single legality number for a country is derived from a principal components analysis of a

covariance matrix of the five proxies as follows: Legality = .381* (efficiency of the judiciary) ? .5778*

(rule of law) ? .5031* (degree of corruption) ? .3468* (risk of expropriation) ? .3842* (risk of contract

repudiation).

Country-specific institutional effects on ownership 179

123

creditor information and legal rights indices is strongest in France and Belgium and

weakest in Germany. From Table 1, investor protection based on disclosure

information, directors’ liability, and the facility to bring shareholder suits appears

strongest in Portugal and weakest in France. Finally, our eight countries fall into two

groups on the legality scale: Austria, Germany, the Netherlands, Belgium and

France at the high end; and Spain, Portugal and Italy on the low end.

4.3 Firm-specific control variables

Previous research (Pedersen and Thomsen 1998) finds industry, perhaps through

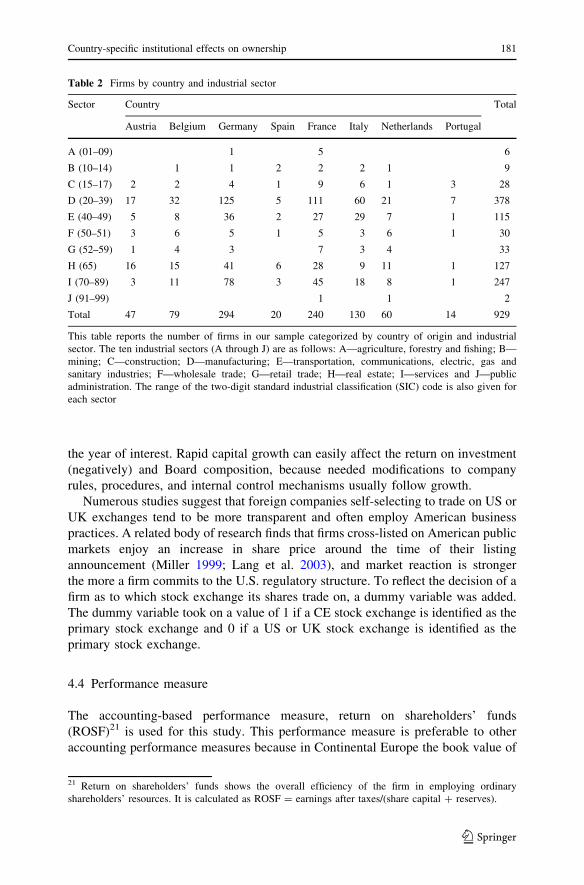

product market competition, influences a firm’s performance. Accordingly, Table 2

shows firms categorized on the basis of their two-digit SIC (Standard Industrial

Classification) code into one of ten (A through J) sectors.20 Table 2 shows almost

40% of our sample coming from the manufacturing sector (sector D). The finance,

insurance and real estate (sector H) and service (sector I) sectors together comprise

38% of our sample firms.

The importance of controlling for size stems from the results of research of Fama

and French (1995) who document that small firms have, on average, lower earnings

scaled by book value of equity, than large firms. In this study, size is a variable

computed as the logarithm of a firm’s total assets in Euros for fiscal year 2005.

Growth, as identified in Loebbecke et al. (1989), is measured as the difference in

average percentage change in total assets for two years prior (i.e., 2003 and 2004) to

Table 1 Country-specific/institutional characteristics

Country CII CLR DI DLI SSI LI

Austria 5 5 6 5 4 20.76

Belgium 6 7 4 6 7 20.82

France 6 8 5 1 5 19.67

Germany 3 3 6 5 5 20.44

Italy 5 9 5 2 6 17.23

Netherlands 6 3 5 4 6 21.67

Portugal 6 5 7 5 7 17.20

Spain 5 5 5 6 4 17.13

This table reports the values for the country-specific/institutional characteristics of firms from the eight

countries in Continental Europe. CII is the credit information index and ranges from 0 (weak credit

information index) to 10 (strong credit information index). CLR is the creditor legal rights index. It ranges

from 0 (weak legal rights) to 10 (strong legal rights). DI is the disclosure index. It ranges from 0 (no

disclosure requirements) to 10 (substantial disclosure requirements). DLI is the directors’ liability index,

and it ranges from 0 (no director liability) to 10 (substantial director liability). SSI is the shareholder suits

index. It ranges from 0 (shareholder has no access to information in pursuit of a law suit against a firm) to

10 (substantial access to information in pursuit of a law suit against a firm). LI is the legality index. It was

empirically derived by Berkowitz et al. (2000) to reflect the of efficiency of the judiciary system, rule of

law, level of corruption, risk of contract repudiation and risk of governmental appropriation

20 Because only a few firms populated sectors A and J (6 and 2 firms, respectively), these sectors and the

firms in these sectors were dropped from this analysis.

180 V. Krivogorsky, G. Grudnitski

123

the year of interest. Rapid capital growth can easily affect the return on investment

(negatively) and Board composition, because needed modifications to company

rules, procedures, and internal control mechanisms usually follow growth.

Numerous studies suggest that foreign companies self-selecting to trade on US or

UK exchanges tend to be more transparent and often employ American business

practices. A related body of research finds that firms cross-listed on American public

markets enjoy an increase in share price around the time of their listing

announcement (Miller 1999; Lang et al. 2003), and market reaction is stronger

the more a firm commits to the U.S. regulatory structure. To reflect the decision of a

firm as to which stock exchange its shares trade on, a dummy variable was added.

The dummy variable took on a value of 1 if a CE stock exchange is identified as the

primary stock exchange and 0 if a US or UK stock exchange is identified as the

primary stock exchange.

4.4 Performance measure

The accounting-based performance measure, return on shareholders’ funds

(ROSF)21 is used for this study. This performance measure is preferable to other

accounting performance measures because in Continental Europe the book value of

Table 2 Firms by country and industrial sector

Sector Country Total

Austria Belgium Germany Spain France Italy Netherlands Portugal

A (01–09) 1 5 6

B (10–14) 1 1 2 2 2 1 9

C (15–17) 2 2 4 1 9 6 1 3 28

D (20–39) 17 32 125 5 111 60 21 7 378

E (40–49) 5 8 36 2 27 29 7 1 115

F (50–51) 3 6 5 1 5 3 6 1 30

G (52–59) 1 4 3 7 3 4 33

H (65) 16 15 41 6 28 9 11 1 127

I (70–89) 3 11 78 3 45 18 8 1 247

J (91–99) 1 1 2

Total 47 79 294 20 240 130 60 14 929

This table reports the number of firms in our sample categorized by country of origin and industrial

sector. The ten industrial sectors (A through J) are as follows: A—agriculture, forestry and fishing; B—

mining; C—construction; D—manufacturing; E—transportation, communications, electric, gas and

sanitary industries; F—wholesale trade; G—retail trade; H—real estate; I—services and J—public

administration. The range of the two-digit standard industrial classification (SIC) code is also given for

each sector

21 Return on shareholders’ funds shows the overall efficiency of the firm in employing ordinary

shareholders’ resources. It is calculated as ROSF = earnings after taxes/(share capital ? reserves).

Country-specific institutional effects on ownership 181

123

balance sheet items is more value-relevant than earnings, and the efficiency of funds

employment is particularly important due to a well-developed credit market (Black

and White 2003).

Perhaps more importantly for this study, ROSF represents a performance

measure equally affected by investor and creditor protection environments. In the

EU, legal rules limiting managers’ discretion over the declaration of dividends or

any other way of conveying corporate assets to shareholders are intertwined with the

regulation of legal capital. Under the Second Directive Article 15(1) of the

European Union Company Law, no distributions to shareholders are to be made

when net assets are lower or would become lower than subscribed capital plus

certain reserves.22 Even if this does not protect creditors against normal business

risk, a public corporation is unable to convey funds to shareholders if net assets fall

below the subscribed capital unless shareholders vote for a capital reduction

procedure which includes certain safeguards for creditors (Articles 30–39).

Moreover, a reduction below the minimum capital is entirely ruled out (Article

34).23 An important point is that the actual computation of net assets within the

meaning of the Directive is basically a balance sheet test on the basis of the prior

financial year’s annual accounts. Thus, the extent of capital maintenance depends on

the applicable accounting rules. In this regard, the Fourth Directive harmonizes

accounting law for the EU in great detail, and bases individual accounts of the

accounting system on International Accounting Standards/International Financial

Reporting Standards (IAS/IFRS).

The use of an accounting-based financial ratio has certain advantages and

limitations over market measures such as Tobin’s Q. One advantage is that an

accounting-based performance measure is not affected by ‘‘market moods.’’

Another advantage is that it doesn’t suffer from an anticipation problem because

an accounting performance measure for one year reflects only the performance for

that year, although, obviously, one year’s performance creates short- and long-term

expectations about future performance.

5 The model

Empirical testing of the hypotheses employs hierarchical moderated multiple

regressions (MMR),24 including the determination of effect size and statistical

power of MMR (Aguinis et al. 2001; Aguinis and Stone-Romero 1997). MMR is

typically used to examine the relationships between a set of independent variables

22 These are reserves which may not be distributed except in the case of a reduction of subscribed capital

(a safeguard of creditors).23 As a remedy, Article 16 of the Directive of the European Union Company Law requires that

distributions received must be returned if the corporation proves that these shareholders knew of the

irregularity, ‘‘or could not in view of the circumstances have been unaware of it.’’24 MMR is employed because according to Saunders (1956) and Carte and Russell (2003), using

traditional moderated regression analysis (MRA) can lead to spurious conclusions (i.e., b3, the estimated

beta for the interaction term isn’t an indicator of moderator effect size, and thus, no conclusions on

differential validity can be drawn based on the significance of estimated beta).

182 V. Krivogorsky, G. Grudnitski

123

and a dependent variable after controlling for effects of some other independent

variables on the dependent variable. In our case MMR estimates the effects of

institutional regimes (i.e., moderators—X2 (DI, DLI, SSI, CII, CLR, LI) on the

strength of the relationship between ownership concentration (i.e., predictor

variable—X1 (blockholder ownership percentage) and the performance ratio (i.e.,

criterion variable—Y (ROSF)). The X2 variables are labeled as moderators because

they are exogenous and uncontrollable (Cohen and Cohen 1983); they are also

categorical (eight countries) and manipulated (Aguinis 2004).

To find evidence supporting the suggestion that the strength of the X1–Yrelationship varies as a function of X2, the sample estimate used as an indicator of

moderator effect size is the difference between R2 for the following two equations25

(Cohen and Cohen 1983; Carte and Russell 2003):

Y ¼ b0 þ b1X1 þ b2X2; R2; sub add ð1Þ

Y ¼ b0 þ b1X1 þ b2X2 þ b3Z;R2 sub mult; where Z ¼ X1 � X2: ð2ÞTo identify a presence of a differential effect, we test the null hypothesis: H0:

DR2 = R2 sub mult - R2 sub add = 0 using General Linear Method (GLM)

procedures. An F-statistic derived from Eq. 3 (below) that is significantly greater

than 1.0 leads to rejection of H0: DR2 = 0, and establishes strong differential

validity.

F½df ðsub mult� df add;N � df mult� 1Þ�¼ DR2=ðdf mult� df addÞ=ð1� R2; sub multÞ=ðN � df mult� 1Þ ð3Þ

Two additional steps were taken in the preparation of the data to avoid using the

statistic inappropriately or interpreting the results incorrectly. First, ratio scales are

employed for X1 and X2. Employing ratio scales enabled potential problems because

of the variability from linear transformation and confounding of main and differential

effects26 to be addressed. Second, all multiple-way interactions between ownership

concentration mechanisms and country-specific characteristics were decomposed into

two-way interactions. This decomposition was necessary because over-specification

of a model may lead to an increased standard error of the regression coefficients,

making the coefficients hardly interpretable (Cohen and Cohen 1983).

Also, to address the endogeniety problem leveled by Demsetz (1983), who

argued that ownership of a firm is an endogenous variable, we followed the lead of

the prior research (Thomsen and Pedersen 2000; Holmen and Hogfeldt 2000;

Ehrhardt and Nowak 2003; Goergen and Renneboog 2003; Kirchmaier and Grant

2006) providing empirical evidence on the stability of ownership in CE, which runs

counter to the endogeniety argument of Demsetz (1983). These studies find that

while shares may trade frequently, it is rare that the concentrated owner changes. It

is also worth noting that most Continental European countries have mandatory bid

regulations encouraging the stability and accumulation of control by the concen-

trated owner and even reward the loyalty of shareholders by increasing their voting

25 Implicit in all equations of our model is the inclusion of a set of firm-specific independent control

variables including the industry, size and primary trading market of a firm.26 Main effects can only be explained when differential effects are insignificant.

Country-specific institutional effects on ownership 183

123

power (see, for example, France). Further, Ehrhardt and Nowak (2003) indicate that

the dominant owner of a firm chooses the ownership structure so as to maximize a

firm’s value from their perspective. The exogeneity of the relationship between the

ownership and performance in Continental European countries has also been

supported in studies by Gugler et al. (2003) and Gilson (2005), Krivogorsky and

Grudnitski (2008). Based on the stability of the concentrated ownership in our

sample we are led to believe that concentrated owners have an opportunity to decide

the nature and amounts of investment, rather than the efficiency of investments

determining the identity of dominant owners.

6 The data

The data for this research was collected from ORBIS (Bureau van Dijk Electronic

Publishing (BvDEP) data provider). The initial sample included active, publicly-

traded companies (5,381 companies) located in the CE countries of Austria,

Belgium, France, Germany, Italy, the Netherlands, Portugal and Spain; and

members of the EU. Out of this sample, 929 companies had another industrial

company (i.e., a block) as their dominant owner. After excluding companies with

missing data, from sectors A and J, and all financial and insurance companies from

the one-digit SIC code of 6 (leaving only real estate companies from this one-digit

code), the final sample consisted of 891 companies.

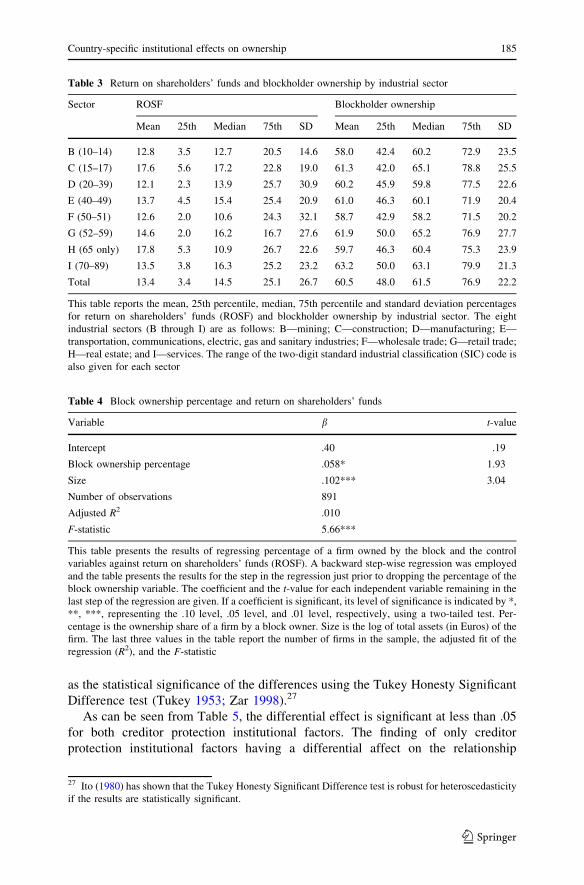

Table 3 gives the mean, standard deviation, and values for the 25th percentile,

median and 75th percentile for returns on shareholders’ funds and block ownership

concentration for each of the remaining industrial sectors for the 2005 fiscal year.

By comparing the mean and percentile values, the distributions for all sectors but H

appear to be symmetric. For sector H (finance, insurance and real estate) the mean

and percentile values for return on shareholders’ funds indicate the distribution is

skewed to the left. The mean and median for the block ownership percentage levels

are highly concentrated (all above 58%) and consistent throughout all industries.

7 Results

Table 4 provides the results of a test of the first hypothesis. It shows that block

ownership is positively and significantly (p B .10) related to return on shareholders’

funds. The table also reports only the control variable of the size (as measured by

the logarithm of total assets) of a firm is significant ((p B .001). Finally, for the

overall equation the F-statistic is significant at the p B .001 level.

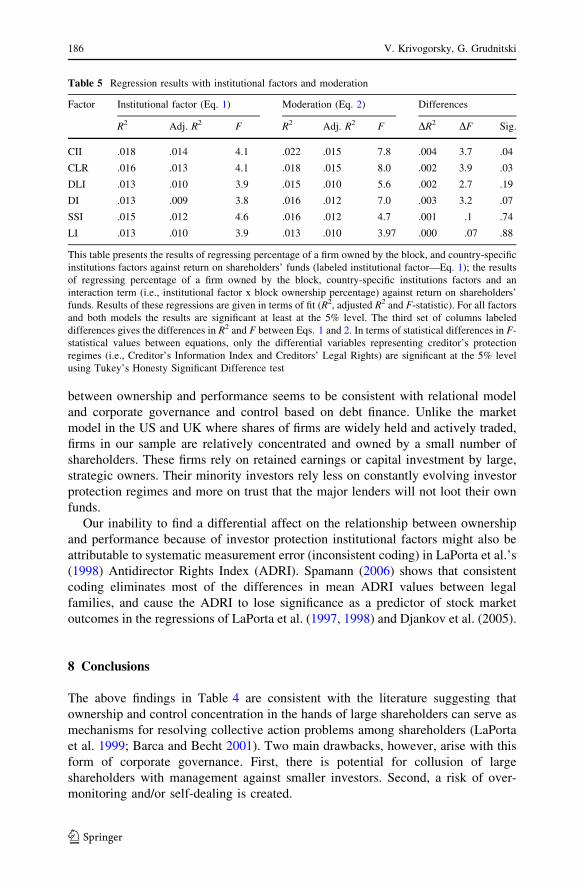

Table 5 displays the results of tests of the remainder of our hypotheses dealing

with the differential effects of the country-specific variables. The first set of

columns gives the fit statistics when the institutional variables are added (Eq. 1).

The second set of columns gives the fit statistics when interaction terms between

block ownership and institutional variables are added (Eq. 2). Finally, the third set

of columns provides the differences in fit between the two equations (Eq. 3) as well

184 V. Krivogorsky, G. Grudnitski

123

as the statistical significance of the differences using the Tukey Honesty Significant

Difference test (Tukey 1953; Zar 1998).27

As can be seen from Table 5, the differential effect is significant at less than .05

for both creditor protection institutional factors. The finding of only creditor

protection institutional factors having a differential affect on the relationship

Table 3 Return on shareholders’ funds and blockholder ownership by industrial sector

Sector ROSF Blockholder ownership

Mean 25th Median 75th SD Mean 25th Median 75th SD

B (10–14) 12.8 3.5 12.7 20.5 14.6 58.0 42.4 60.2 72.9 23.5

C (15–17) 17.6 5.6 17.2 22.8 19.0 61.3 42.0 65.1 78.8 25.5

D (20–39) 12.1 2.3 13.9 25.7 30.9 60.2 45.9 59.8 77.5 22.6

E (40–49) 13.7 4.5 15.4 25.4 20.9 61.0 46.3 60.1 71.9 20.4

F (50–51) 12.6 2.0 10.6 24.3 32.1 58.7 42.9 58.2 71.5 20.2

G (52–59) 14.6 2.0 16.2 16.7 27.6 61.9 50.0 65.2 76.9 27.7

H (65 only) 17.8 5.3 10.9 26.7 22.6 59.7 46.3 60.4 75.3 23.9

I (70–89) 13.5 3.8 16.3 25.2 23.2 63.2 50.0 63.1 79.9 21.3

Total 13.4 3.4 14.5 25.1 26.7 60.5 48.0 61.5 76.9 22.2

This table reports the mean, 25th percentile, median, 75th percentile and standard deviation percentages

for return on shareholders’ funds (ROSF) and blockholder ownership by industrial sector. The eight

industrial sectors (B through I) are as follows: B—mining; C—construction; D—manufacturing; E—

transportation, communications, electric, gas and sanitary industries; F—wholesale trade; G—retail trade;

H—real estate; and I—services. The range of the two-digit standard industrial classification (SIC) code is

also given for each sector

Table 4 Block ownership percentage and return on shareholders’ funds

Variable b t-value

Intercept .40 .19

Block ownership percentage .058* 1.93

Size .102*** 3.04

Number of observations 891

Adjusted R2 .010

F-statistic 5.66***

This table presents the results of regressing percentage of a firm owned by the block and the control

variables against return on shareholders’ funds (ROSF). A backward step-wise regression was employed

and the table presents the results for the step in the regression just prior to dropping the percentage of the

block ownership variable. The coefficient and the t-value for each independent variable remaining in the

last step of the regression are given. If a coefficient is significant, its level of significance is indicated by *,

**, ***, representing the .10 level, .05 level, and .01 level, respectively, using a two-tailed test. Per-

centage is the ownership share of a firm by a block owner. Size is the log of total assets (in Euros) of the

firm. The last three values in the table report the number of firms in the sample, the adjusted fit of the

regression (R2), and the F-statistic

27 Ito (1980) has shown that the Tukey Honesty Significant Difference test is robust for heteroscedasticity

if the results are statistically significant.

Country-specific institutional effects on ownership 185

123

between ownership and performance seems to be consistent with relational model

and corporate governance and control based on debt finance. Unlike the market

model in the US and UK where shares of firms are widely held and actively traded,

firms in our sample are relatively concentrated and owned by a small number of

shareholders. These firms rely on retained earnings or capital investment by large,

strategic owners. Their minority investors rely less on constantly evolving investor

protection regimes and more on trust that the major lenders will not loot their own

funds.

Our inability to find a differential affect on the relationship between ownership

and performance because of investor protection institutional factors might also be

attributable to systematic measurement error (inconsistent coding) in LaPorta et al.’s

(1998) Antidirector Rights Index (ADRI). Spamann (2006) shows that consistent

coding eliminates most of the differences in mean ADRI values between legal

families, and cause the ADRI to lose significance as a predictor of stock market

outcomes in the regressions of LaPorta et al. (1997, 1998) and Djankov et al. (2005).

8 Conclusions

The above findings in Table 4 are consistent with the literature suggesting that

ownership and control concentration in the hands of large shareholders can serve as

mechanisms for resolving collective action problems among shareholders (LaPorta

et al. 1999; Barca and Becht 2001). Two main drawbacks, however, arise with this

form of corporate governance. First, there is potential for collusion of large

shareholders with management against smaller investors. Second, a risk of over-

monitoring and/or self-dealing is created.

Table 5 Regression results with institutional factors and moderation

Factor Institutional factor (Eq. 1) Moderation (Eq. 2) Differences

R2 Adj. R2 F R2 Adj. R2 F DR2 DF Sig.

CII .018 .014 4.1 .022 .015 7.8 .004 3.7 .04

CLR .016 .013 4.1 .018 .015 8.0 .002 3.9 .03

DLI .013 .010 3.9 .015 .010 5.6 .002 2.7 .19

DI .013 .009 3.8 .016 .012 7.0 .003 3.2 .07

SSI .015 .012 4.6 .016 .012 4.7 .001 .1 .74

LI .013 .010 3.9 .013 .010 3.97 .000 .07 .88

This table presents the results of regressing percentage of a firm owned by the block, and country-specific

institutions factors against return on shareholders’ funds (labeled institutional factor—Eq. 1); the results

of regressing percentage of a firm owned by the block, country-specific institutions factors and an

interaction term (i.e., institutional factor x block ownership percentage) against return on shareholders’

funds. Results of these regressions are given in terms of fit (R2, adjusted R2 and F-statistic). For all factors

and both models the results are significant at least at the 5% level. The third set of columns labeled

differences gives the differences in R2 and F between Eqs. 1 and 2. In terms of statistical differences in F-

statistical values between equations, only the differential variables representing creditor’s protection

regimes (i.e., Creditor’s Information Index and Creditors’ Legal Rights) are significant at the 5% level

using Tukey’s Honesty Significant Difference test

186 V. Krivogorsky, G. Grudnitski

123

In an attempt to limit the potential abuse of minority shareholders and limit the

possibility of self-dealing, corporate laws of CE countries curb the power of large

shareholders (Gilson 2005; Jackson and Roe 2008). CE countries rely on the law

and regulations as the main mechanism for coordinating actions of relational

shareholders. Today, in Continental Europe the fundamental issues concerning

governance by these shareholders seem to be how to regulate large shareholders,

with an eye on protecting creditors as the main providers of capital, and obtaining

the right balance between the discretion of relational owners (and managers) and the

protection of small shareholders.

In this connection, corporate law in Continental Europe uses a variety of

strategies to police relational investors. First, potentially dangerous transactions

may require ex ante approval or ex post ratification (by disinterested parties).

Second, transactions may be reviewed by any interested party (including the Court)

ex post in light of a certain standard of conduct. In this case decision makers

(relational investors or managers) are held responsible for their actions both legally

or otherwise. And third, potentially problematic transactions may be subjected to a

specific disclosure requirement so as to facilitate the ex post evaluation of a firm’s

position by its minority investors.

The test of the differential validity of a country’s institutional regimes (results are

given in Table 5) suggests that creditor protection in CE countries has a much

stronger differential influence than investor protection in restricting the degree to

which a firm’s profitability is impacted by large shareholders. This result is

consistent with superiority of pre-insolvency credit rules, which traditionally follow

the corporate law (including law of incorporation) in Continental Europe. It means

that these rules have an influence on the regulatory competition in corporate law

(Enriques and Gelter 2006), and historically, these rules were given the highest

priority in European Union Directives, as well as in the laws of individual member

states. Therefore, conflict of regulations on pre-insolvency rules has generally been

settled over the years, meaning that they have been an organic part of corporate law

for an extended period of time. Moreover, EU Directives related to the corporate

law generally leave most of decision-making power to the member states, where

regulators view the corporate laws within a context of their national legal culture.

Thus, all regulations related to the creditor protection under-enforced on the EU

level are mandatory on the country level, and considered as a part of national

corporate law.

EU member states often engage in creditor protection measures that are far

beyond the requirements of EU law (Enriques and Gelter 2006; Esty and Megginson

2002). Thus, on the EU level, creditor protection institutions are intended to be

adequate safeguards by granting creditors (as main capital providers) an entitlement

to obtain some form of security in the event of high risk of debtor default.28 The

detailed conditions for exercising this right and an adequate system of protecting

creditors are laid down on a country level. According to some (Armour 2000;

Enriques and Macey 2001; Lutter 1998) creditor protection regulations historically

have a double role in CE countries. Their functions do not entirely lie in protecting

28 Second Directive, Section 6 offers a requirement on the minimum net assets.

Country-specific institutional effects on ownership 187

123

creditors from the risk of substantial losses resulting from an unfavorable business

development, but also in signaling to the market, thus erecting a barrier against the

creation of dubious corporations with an unreasonable amount of backing by

shareholders. For global investors who might be unfamiliar with the business

environment of CE countries, this is an important fact to consider in weighing the

risks associated with their investment decision.

Acknowledgments We are grateful to Per Olsson, Chew Chow, David DeBosky, Juergen Ernstberger,

Axel Haller, participants of 2006 American Accounting Association Annual meeting, 2007 Academy of

International Business Annual meeting, and anonymous referees for their helpful insights. We would like

to thank Juan Du and Anton Leonov for invaluable research assistance in preparing the data. We also

gratefully acknowledge financial support from CIBER SDSU and SDSU University Grants Program. Any

errors are our own.

Appendix: Creditor and investor protection moderator variables

Disclosure index (DI)

The corporate body that provides legally sufficient approval for the transaction

(0 = CEO/Chairman or managing Director alone; 1 = shareholders or Board of

Directors vote and CEO/Chairman can vote; 2 = Board of Directors vote and CEO/

Chairman cannot vote; 3 = shareholders vote and CEO/Chairman cannot vote).

Immediate disclosure to the public and/or shareholders (0 = none; 1 = disclo-

sure on the transaction only; 2 = disclosure on the transaction and CEO/Chairman

conflict of interest).

Disclosures in published periodic filings (0 = none; 1 = disclosure on the

transaction only; 2 = disclosure on the transaction and CEO/Chairman conflict of

interest).

Disclosures by CEO/Chairman to Board of Directors (0 = none; 1 = existence

of a conflict without any specifics; 2 = full disclosure of all material facts).

Requirement that an external body reviews the transaction before it takes place

(0 = no; 1 = yes).

Directors’ liability index (DLI)

Shareholder plaintiff’s ability to hold CEO/Chairman liable for damage to the

buyer-seller transaction caused to the company (0 = CEO/Chairman is not liable or

liable only if he acted fraudulently or in bad faith; 1 = CEO/Chairman is liable if he

influenced the approval or was negligent; 2 = CEO/Chairman is liable if the

transaction was unfair, oppressive or prejudicial to minority shareholders).

Shareholder plaintiff’s ability to hold the approving body (the CEO/Chairman or

Board of Directors) liable for damage to the company (0 = members of the

approving body are either not liable or liable only if they acted fraudulently or in

bad faith; 1 = liable for negligence in the approval of the transaction; 2 = liable if

the transaction is unfair, oppressive, or prejudicial to minority shareholders).

188 V. Krivogorsky, G. Grudnitski

123

Whether a court can void the transaction upon a successful claim by a

shareholder plaintiff (0 = rescission is unavailable or available only in case of

seller’s fraud or bad faith; 1 = available when the transaction is oppressive or

prejudicial to minority shareholders; 2 = available when the transaction is unfair or

entails a conflict of interest).

Whether CEO/Chairman pays damages for the harm caused to the company upon

a successful claim by the shareholder plaintiff (0 = no; 1 = yes).

Whether CEO/Chairman repays profits made from the transaction upon a

successful claim by the shareholder plaintiff (0 = no; 1 = yes).

Whether fines and imprisonment can be applied against CEO/Chairman (0 = no;

1 = yes).

Shareholder plaintiffs’ ability to sue directly or derivatively for damage the

transaction causes to the company (0 = not available; 1 = direct or derivative suit

available for shareholders holding at least 10% of the shares).

Shareholder suits index (SSI)

Documents available to the plaintiff from the defendant and witnesses during trial

(score 1 each for (1) information that the defendant has indicated he intends to rely

on for his defense; (2) information that directly proves specific facts in the plaintiff’s

claim; (3) any information that is relevant to the subject matter of the claim; and (4)

any information that may lead to the discovery of relevant information).

Ability of plaintiffs to directly question the defendant and witnesses during trial

(0 = no; 1 = yes, with prior approval by the court of the questions posed; 2 = yes,

without prior approval).

Plaintiff can request categories of documents from the defendant without

identifying specific ones (0 = no; 1 = yes).

Shareholders owning 10% or less of buyer’s shares can request that an inspector

investigate the transaction (0 = no; 1 = yes).

Level of proof required for civil suits is lower than that for criminal cases

(0 = no; 1 = yes).

Shareholders owning 10% or less of buyer’s shares can inspect transaction

documents before filing suit (0 = no; 1 = yes).

Credit information index (CII)

Doing Business surveys public registries and the largest private credit bureau in a

county to construct an indicator of how well the credit market functions. Credit

registries are institutions that collect and distribute credit information on borrowers.

Credit registries not only greatly expand access to credit, but by sharing credit

information, they help lenders assess risk and allocate credit more efficiently. Credit

registries also free entrepreneurs from having to rely on personal connections alone

when trying to obtain credit.

The indicator Doing Business constructs to represent the depth of the credit

market is designated CII (credit information index). CII measures the extent to

which the rules of a credit information system facilitate lending based on the scope

Country-specific institutional effects on ownership 189

123

of information distributed, the ease of access to information and the quality of

information.

The CII ranges from 0 (weak credit information index) to 10 (strong credit

information index). Higher index values indicate more extensive rules on the quality

and disclosure of information in the registry, and, hence, a higher quality of

protection of a creditor’s rights.

Creditor legal rights (CLR)

Doing Business examines collateral and bankruptcy laws and legal summaries.

Doing Business verifies what is collected by surveying financial lawyers to assess

the legal rights of borrowers and lenders in a country.

The strength of a country’s creditor legal rights index (CLR) is measured using

ten aspects of the rights of borrowers and creditors in collateral and bankruptcy

laws. These aspects include whether general rather than a specific description of

assets and debt is permitted in collateral agreements (expanding the scope of assets

and debt covered), any legal or natural person may grant or take security in assets, a

unified registry operates that includes charges over movable property, secured

creditors have priority both within bankruptcy and outside it, parties may agree on

out-of-court enforcement of collateral by contract, creditors may both seize and sell

collateral out of court, no automatic stay or ‘‘asset freeze’’ applies upon bankruptcy,

and the bankrupt debtor retains control of a firm.

The index ranges from 0 (weak legal rights) to 10 (strong legal rights).Where

legal rights are strong more credit is extended and benefits flow beyond those

gaining access to credit.

References

Aguinis, H. (2004). Regression analysis for categorical moderators. New York, NY: Guilford.

Aguinis, H., Petersen, S. A., & Pierce, C. A. (2001). Appraisal of homogeneity of error variance

assumption and alternatives to multiple regression for estimating moderating effects of categorical

variables. Organizational Research Methods, 2, 315–339.

Aguinis, H., & Stone-Romero, E. F. (1997). Methodological artifacts in moderated multiple regression