INTERNSHIP REPORT

ON

“A STUDY ON EPSF AT ASCENT HR PVT LTD.”

BY

RAMASHESHA TJ

1NZ17MBA60

Submitted to

DEPARTMENT OF MANAGEMENT STUDIES

NEW HORIZON COLLEGE OF ENGINEERING,

OUTER RING ROAD, MARATHALLI,

BANGALORE

In partial fulfillment of the requirements for the award of the degree of

MASTER OF BUSINESS ADMINISTRATION

Under the guidance of

SANTHOSH

Assistant professor

2017-19

CERTIFICATE

This is to certify that RAMASHESHA T.J. bearing USN 1NZ17MBA60, is a bonafide student of

Master of Business Administration course of the Institute 2017-19, autonomous program,

affiliated to Visvesvaraya Technological University, Belgaum. Internship report on “EPSF AT

ASCENT HR (P) LTD” is prepared by him/her under the guidance of Prof. SANTHOSH. In

partial fulfillment of requirements for the award of the degree of Master of Business

Administration of Visvesvaraya Technological University, Belgaum Karnataka.

Signature of internal Guide Signature of HOD Signature of Principal

DECLARATION

I, RAMASHESHA TJ, hereby declare that the Internship report entitled “EPSF AT ASCENT

HR (P) LTD” with reference to “New Horizon College of Engineering” Bellandur, prepared by

me under the guidance of prof. SANTHOSH. faculty of M.B.A Department, New Horizon

College of Engineering.

I also declare that this Internship is towards the partial fulfillment of the university regulations

for the award of the degree of Master of Business Administration by Visvesvaraya Technological

University, Belgaum.

I have undergone an industry Internship for a period of Eight weeks. I further declare that this

report is based on the original study undertaken by me and has not been submitted for the award

of a degree/diploma from any other University / Institution.

Signature of Student

Place:

Date:

TABLE OF CONTENTS

CHAPTERS PARTICULARS PAGE NUMBERS

Chapter-1 INTRODUCTION

1.1 Introduction

1.2 Services offered

1.3 Training sessions at Ascent HR

1.4 the organizational structure

1.5 General introduction

1.6 Basics concepts of Income Tax

1.7 Tax rates

1.8 Industry profile

1.9 Company profile

1.10 SWOT analysis of the company

1.11 Financial statements

1-38

Chapter-2 LITERATURE REVIEW

2.0 Review of Literature

39-41

Chapter-3 RESEARCH METHODOLOGY

3.0 Need for the study

3.1 Objectives of the study

3.2 Topic chosen for the study

3.3 Theoretical background of the study

3.4 Sampling design

3.5 Duration of the research

3.6 Source of data

3.7 Limitations of the study

42-56

Chapter-4 DATA ANALYSIS AND INTERPRETATION

4.1 Data analysis and interpretation

4.2 Tables and graphs

4.3 Dependants eligible for each investment

4.4 Learning experience

56-69

Chapter-5 Findings and Suggestions

5.1 Summary of findings

70-72

5.2 Suggestions

5.3 Conclusions

Bibliography 73

Annexure 74

EXECUTIVE SUMMARY

Tax planning is an essential part of our financial planning. Efficient tax planning enables us to

reduce our tax liability to the minimum. This is done by legitimately taking advantage of all tax

exemptions, deductions rebates and allowances while ensuring that your investments are in line

with their long-term goals.

The purpose of the study is to find out the impact of life insurance premium over income tax

reduction of salaried employees at Ascent HR Pvt. Ltd. And to improve income tax proof

verification process.

The present project is on ‘A Study on EPSF at Ascent HR Pvt. Ltd’ which has been done in

Ascent HR Pvt. Ltd. Bangalore for a duration of 8 weeks which includes industry and company

details.

The company Ascent HR Pvt. Ltd. is situated in Bangalore which is engaged in the business of

multi-dimensional financial services as well as HR solutions.

Ascent HR Pvt. Ltd. is a Consultant company, a trusted name in the financial services arena,

provides you with the entire gamut of financial services under one ceiling. Our team is highly

skilled with experienced employees. Our efforts are to provide more services to our customers.

Our company provides these services:

HR solutions

Taxation

Payroll

The main purpose of doing this project is to analyze the financial statements of the company, to

know the tax benefits available for the individual and suggest to a customers of Ascent HR Pvt.

Ltd regarding tax plans, payroll services and help desk services.

Ultimately this project helps Ascent HR Pvt. Ltd. to give suggestions to its customers about the

tax planning and savings and making them to utilize to utilize this services accurately.

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 1

A STUDY ON EPSF AT ASCENT HR (P) LTD

CHAPTER -1

1.1 INTRODUCTION:

Ascent Human Solution (P) Limited is a professional HR Consulting & Talent Search

Organization deals into the greatest resource called Human. Ascent is Team of passionate

experts in Executive Search industry and committed to build leadership teams for our

clients. The world today in a service economy where the key differentiator is the quality

of people, we at Ascent Human Solution Pvt. Ltd. always acts as a “Human Solution

Architect“ and have made it easier for our clients’ to acquire the Best Talent who make

the Difference and turn opportunity into a big Business Deal . To complement its

Executive Search activities, Ascent Human Solutions offers a complete suite of

innovative, flexible and effective HR Consulting services. Our approach emphasizes a

dynamic interaction of close personal proximity, which aims for value-added assessments

as the result of our cooperation.

1.2 SERVICES OFFERED

1. Executive Search Solution

2. Permanent Recruitment Solutions

3. Temporary Staffing / Outsourcing Solutions

4. Payroll & Compliance Management Solutions

Interview procedure at Ascent HR:

In Ascent HR company, when I reach company for interview, I gone through three stage of

interview procedure for selection i.e.., written test, HR interview and technical interview

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 2

with manager and finally after three days I received an offer to work with the company

as a Consultant (intern).

So, the company has divided its work mainly based on Human Resources Solutions and

Payroll. In the sense we can say the service offered by the company is taxation, payroll,

human resources, and staffing and software solutions.

So I reached office as per the scheduled date and I met an HR. Nivedha, she took me to

the training room and there many interns has come along with them I become the one and

I started completing formalities of a company and opened a new bank account for salary

or stipend.

1.3 Training sessions at Ascent HR:

After completion of all formalities they started training for us based on taxation and

before starting the sessions they asked some kind of simple questions on taxation to

check the basics.

From next day of my joining they started training for the interns. The person who took a

training session is Ambika Prasad. So he is the Assistant Manager at Ascent HR

Company for Bangalore Region. He started training from the scratch of taxation so that

we can understand better.

In the whole training sessions I learnt about the basics of tax as well as full details of

deductions under sections 80C to 80U and many more at the end of the training, they had

been conducted an Assessment test for the interns and I can say great fully I got highest

score in the test and they sent me to the Payroll department.

In the payroll department, the work of mine is Employee Proof Submission Form as well

as tax validation and approval. It is headed by the Team Leader Ranjith. The practical

work was taught by the seniors and since I am a quick learner I started working on it

soon.

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 3

The clients for my work were;

Thomson Reuters

AXA business

AstraZeneca

1.5 GENERAL INTRODUCTION

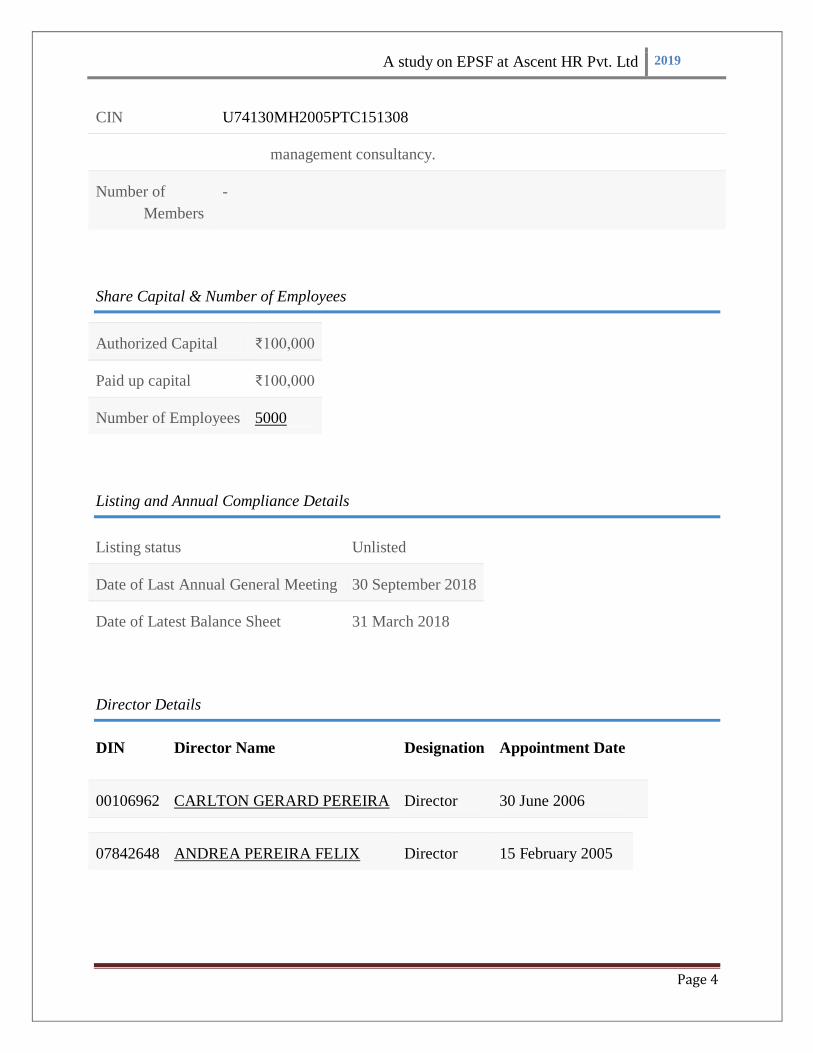

CIN U74130MH2005PTC151308

Company Name ASCENT HR SOLUTIONS PRIVATE LIMITED

Company Status Active

RoC RoC-Mumbai

Registration

Number

151308

Company

Category

Company limited by Shares

Company Sub

Category

Non-govt company

Class of

Company

Private

Date of

Incorpora

tion

15 February 2005

Age of Company 14 years, 1 month, 16 days

Activity Legal, accounting, book-keeping and auditing activities; tax consultancy;

market research and public opinion polling; business and

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 4

CIN U74130MH2005PTC151308

management consultancy.

Number of

Members

-

Share Capital & Number of Employees

Authorized Capital ₹100,000

Paid up capital ₹100,000

Number of Employees 5000

Listing and Annual Compliance Details

Listing status Unlisted

Date of Last Annual General Meeting 30 September 2018

Date of Latest Balance Sheet 31 March 2018

Director Details

DIN Director Name Designation Appointment Date

00106962 CARLTON GERARD PEREIRA Director 30 June 2006

07842648 ANDREA PEREIRA FELIX Director 15 February 2005

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 5

OUR VISION

To be recognized as a Result Oriented, Innovative and Dedicated partner to clients, constantly

delivering effective HR Solutions that meet client expectations.

OUR MISSION

To partner our clients to create a competitive edge by providing the best talent and HR Solutions

thereby enabling them to focus on their core business.

Tax planning is an essential part of our financial planning. Efficient tax planning enables

us to reduce our tax liability to the minimum. This is done by legitimately taking

advantage of all tax exemptions, deductions rebates and allowances while ensuring that

your investments are in line with their long-term goals.

The purpose of the study is to find out the impact of life insurance premium over income

tax reduction of salaried employees at Ascent HR Pvt. Ltd. And to improve income tax

proof verification process.

The taxes are the basic source of revenue for the Government. Revenue raised from the

taxes are utilized for meeting the expense of Government like, provision of education,

infrastructure facilities such as roads, dams etc. Taxes are broadly divided into two parts

i.e. direct taxes and indirect taxes. The tax that is levied directly on the income or wealth

of a person is called direct tax. Income tax is one of form of direct taxes.

The levy of income tax in India is governed by the Income Tax Act, 1961 and Income

Tax Rules, 1962. It is charged on the Total Income and to derive the total income one

must know certain concepts of the Income Tax Act, these are related to person,

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 6

residential status, assessment year, previous year, assessee etc. Here, in this lesson we

will discuss the various basic concepts of Income Tax Act. At the end of this lesson, you

will understand the types of taxes, meaning of taxes, components of income tax law,

various concepts like assessment year, previous year, income, person, assessee, capital

and revenue receipts etc. you will also get to know about the basic steps in the calculation

of tax liability.

Tax is the financial charge imposed by the Government on income, commodity or

activity. Government imposes two types of taxes namely Direct taxes and Indirect taxes.

Direct tax is one where burden of tax is directly on the payer example income tax,

Indirect tax is paid by the person other than the one who utilizes the product or service

example Excise duty, Custom duty, Service tax, Sales Tax, Value Added Tax. – The

taxes are collected for serving the primary purpose of providing sufficient revenues to the

State.

These have become an instrument through which the social and economic objectives of a

welfare State could be achieved. They are utilized now for providing incentives for larger

earnings and more savings, fostering industrial development by selective concessions,

restraining ostentatious expenditure, checking inflationary pressures and achieving social

objectives. – Article 265 of the Constitution provides that no tax shall be levied or

collected except by authority of law.

Thus, the tax proposed to be levied or collected must be within the legislative

competence of the legislature imposing the tax. Further, the law imposing the tax, like

other laws, must not violate any fundamental right. – Income tax is an entry appearing in

the union list, thus the responsibility for collection of income-tax vests with the Central

Government.

Entry 82 of List I to the Seventh Schedule of the Constitution of India confers power on

Parliament to levy taxes on income other than agricultural income. – The taxes and duties

referred to in the Union list except those referred to in Articles 268 and 269, surcharge on

taxes and duties and any cess levied by the Parliament for specific purposes are to be

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 7

collected by the Government of India and are to be distributed between the Union and the

States in the manner prescribed by the President by order. – Income tax being direct tax

happens to be the major source of revenue for the Central Government.

The responsibility for collection of income-tax vests with the Central Government. This

tax is leviable and collected under Income-tax Act, 1961 (hereinafter referred to as the

Act). The entire amount of income tax collected by the Central Government is classified

under the head:

1. Corporation Tax (Tax on the income of the companies); and

2. Income tax (Tax on income of the non-corporate assessees)

– The Income-tax Act, in its present form came into force on and from 1st April, 1962. Before

this, the Indian Income-tax Act, 1922 was in force. The procedural matters with regard to

income-tax are governed by the Income-tax Rules, 1962, its earlier counterpart being the

Income-tax Rules, 1922. – The Income tax Act contains the provisions for determination

of taxable income, determination of tax liability, procedure for assessment, appeal,

penalties and prosecutions. It also lays down the powers and duties of various income tax

authorities.

– Finance Act: Every year a Budget is presented before the parliament by the Finance Minister.

One of the important components of the Budget is the Finance Bill. The Bill contains

various amendments in the Income-Tax Act and prescribes the rates of taxes. When the

Finance Bill is approved by both the houses of parliament and receives the assent of

President, it becomes the Finance Act. – Notifications: The CBDT issues notifications

from time to time; these are for the proper administration of the Income Tax Act.

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 8

1.6 BASIC CONCEPTS OF INCOME TAX ACT:

“Income Tax is levied on the total income of the previous year of every person.” To levy

income tax, one must have an understanding of the various concepts related to the charge

of tax like previous year, assessment year, Income, total income, person etc.

PERSON [SECTION 2(31)]

Income-tax is charged in respect of the total income of the previous year of every person.

Hence, it is important to know the definition of the word person. As per section 2(31),

Person includes: – an individual: – a Hindu undivided family: – a company – a firm – an

association of persons or a body of individuals whether incorporated or not: – a local

authority: – every artificial, juridical person, not falling within any of the above

categories

An individual:

A natural human being i.e.., male, female, minor or a person of sound or unsound mind.

ASSESSEE [Section 2(7)] in common parlance every tax payer is assesses. However, the

word ‘assesses’ has been defined in Section 2(7) of the Act according to which ‘assessee’

means a person by whom any tax or any other sum of money (i.e. interest, penalty etc.) is

payable under the Act and includes:

(a) Every person in respect of whom any proceeding under this Act has been taken for the

assessment of his income or assessment of fringe benefits or of the income of any other

person in respect of which he is assessable or to determine the loss sustained by him or

by such other person or to determine the amount of refund due to him or to such other

person.

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 9

(b) Every person who is deemed to be an assessee under any provision of this Act.

(c) Every person who is deemed to be an assessee in default under any provision of this Act.

Accordingly, assessee is a person by whom tax or any other sum is payable under the

Act. The expression “other sum of money” includes – fine, interest, penalty and tax or –

person to whom any refund of tax etc. is due under the Act or – if any proceeding under

the Act has been taken against any person, he is also an assessee. Remember, the

proceedings must be initiated under the provisions of the Act.

In other words, a single enquiry letter issued by the Income-tax Department without

reference to any specific provision of the Act does not constitute proceeding under the

Act and, as such, till proceedings are initiated under the Act, the person may not become

an assessee within the ambit of Section 2(7) of the Act.

ASSESSMENT YEAR [SECTION 2(9)]

“Assessment year” means the period of twelve months commencing on 1st April every

year.

Thus it is normally period beginning on 1st April of one year and ending on 31st March

of the next year. Income of previous year of an assessee is taxed during the following

assessment year at the rates prescribed by the relevant Finance Act.

PREVIOUS YEAR (SECTION 3)

Previous year means the financial year immediately preceding the assessment year.

Income earned in a year is taxable in the next year.

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 10

The year in which income is earned is known as previous year. From the assessment year

1989-90 onwards, all assessees are required to follow financial year (i.e. April 1st of one

year to March 31st of next year) as previous year.

The uniform previous year has to be followed for all sources of income. In case of newly

set up business or profession or a source of income newly coming into existence, the first

previous year will be the period commencing from the date of setting up of

business/profession or as the case may be, the date on which the source of income newly

comes into existence and ending on the immediately following March, 31.

INCOME

The definition of Income as given in Section 2(24) of the Act starts with the word

includes therefore the list is inclusive not exhaustive. The definition enumerates certain

items, including those which cannot ordinarily be considered as income but are treated

statutorily as such. Income includes not only those things which the interpretation clause

declares rather it also includes all things which the word signifies according to its natural

import. As per section 2(24), the term income includes:

1. Profits and gains;

2. Dividend;

3. Voluntary contributions: Voluntary contributions received by : – a trust created wholly

or partly for charitable or religious purposes, or – an institution established wholly or

partly for such purposes or by an association or institution referred to in clause (21) or

clause (23) or – a fund or trust or institution established for charitable purposes and

notified under section 10(23C)(iv) or (v) or – any university or other educational

institution or by any hospital referred to in sub-clause (iiiad) or sub-clause (vi) of section

10 (23C) or – any hospital or other institution referred to in sub-clause (iiiae) or sub-

clause (via) of clause (23C) of section 10 – An electoral trust.

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 11

4. The value of any perquisite or profit in lieu of salary taxable.

5. Any special allowance or benefit specifically granted to the assessee to meet expenses

wholly, necessarily and exclusively for the performance of the duties of an office or

employment of profit.

6. City Compensatory Allowance/ Dearness allowance: Any allowance granted to the

assessee either to meet his personal expenses at the place where the duties of his office or

employment of profit are ordinarily performed by him or at a place where he ordinarily

resides or to compensate him for the increased cost of living.

7. Benefit or Perquisite to a Director: The value of any benefit or perquisite, whether

convertible into money or not, obtained from a company by: (a) a director, or (b) a person

having substantial interest in the company, or (c) a relative of the director or of the person

having substantial interest, and any sum paid by any such company in respect of any

obligation which, but for such payment, would have been payable by the director or other

person aforesaid;

8. Any Benefit or perquisite to a Representative Assessee: the value of any benefit or

perquisite (whether convertible into money or not) obtained by any representative

assessee under Section 160(1)(iii)/(iv) or beneficiary, or any amount paid by the

representative assessee in respect of any obligation which, but for such payment, would

have been payable by the beneficiary;

9. Any sum chargeable under section 28, 41 and 59 : – Any sum chargeable to tax as

business income under Section 28(ii), any amount taxable in the hands of a trade,

professional or similar association (for specific services performed for its members) as its

income from business under Section 28(iii), and deemed profits which are taxable under

Sections 41 and 59 of the Act; – Any sum chargeable to income-tax under clause (iiia) of

Section 28, i.e. profits on sale of a licence granted under the Imports (Control) Order,

1955, made under the Imports and Exports (Control) Act, 1947 [inserted by the Finance

Act, 1990, with retrospective effect from 1.4.1962]; – any sum chargeable to income-tax

under clause (iiib) of Section 28 i.e., cash assistance (by whatever name called), received

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 12

or receivable by any person against exports under any scheme of the Government of

India.

Any sum chargeable to income-tax under clause (iiic) of Section 28 i.e., any duty of

customs or excise re-paid or re-payable as drawback to any person against exports under

the Customs and Central Excise Duties Drawback Rules, 1971. – the value of any benefit

or perquisite whether convertible into money or not; taxable as income under Section

28(iv) in the case of person carrying on business or exercising a profession; – any sum

chargeable to income-tax under clause (v) of Section 28;

10. Capital Gain: Any capital gains chargeable to tax under Section 45; since the definition

of income in Section 2(24) is inclusive and not exhaustive capital gains chargeable under

Section 46(2) are also assessable as income.

11. Insurance Profit: The profits and gains of any business of insurance carried on by a

mutual insurance company or by a co-operative society computed in accordance with the

provisions of Section 44 or any surplus taken to be such profits and gains by virtue of the

profits contained in the First Schedule to the Income-tax Act;

12. Banking income of a Co-operative Society: The profits and gains of any business of

banking (including) providing credit facilities carried on by a cooperative society with its

members.

13. Winnings from Lottery: Any winnings from lotteries, crossword puzzles, races,

including horse-races, card-games and games of any sort or from gambling or betting of

any form.

9 (i) "lottery" includes winnings, from prizes awarded to any person by draw of lots or by

chance or in any other manner whatsoever, under any scheme or arrangement by

whatever name called; (ii) "card game and other game of any sort" includes any game

show, an entertainment programme on television or electronic mode, in which people

compete to win prizes or any other similar game;

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 13

14. Employees Contribution Towards Provident Fund: Any sum received by the assessee

from his employees as contributions to any provident fund or superannuation fund or any

fund set-up under the provisions of the Employees State Insurance Act, 1948 (34 of

1948) or any other fund for the welfare of such employees.

15. Amount Received under Keyman Insurance Policy: Any sum received under a Keyman

Insurance Policy including the sum allocated by way of bonus on such policy. Keyman

Insurance Policy means a life insurance policy taken by a person on the life of another

person who is or was the employee of the first mentioned person or is or was connected

with the business of the first mentioned person in any manner whatsoever.

16. Amount received for not carrying out any activity: Any sum referred to in Section

28(va), i.e. any sum, whether received or receivable in cash or kind, under an agreement

for – (i) not carrying out any activity in relation to any business or profession;

[Amendment vide Finance Act, 2016] (ii) not sharing any know-how, patent, copyright,

trade-mark, license, franchise or any other business or commercial right of similar nature

or information or technique likely to assist in the manufacture or processing of goods or

provision for services:

17. Any sum referred to in clause (v) or (vi) of sub-section (2) of section 56;

18. Gift received for an amount exceeding ` 50,000: Any sum of money or value of property

referred to in clause (vii) or clause (viia) of sub-section (2) of Section 56.

19. Consideration received for issue of shares: Any consideration received for issue of shares as

exceeds the fair market value of the shares referred in section 56(2)(viib).

20. Amount received as an advance or otherwise in the course of negotiation for transfer of a

capital asset referred to in clause (ix) of section 56(2).

21. Assistance in the form of a subsidy or grant or cash incentive or duty drawback or waiver or

concession or reimbursement (by whatever name called) by the Central Government or a

State Government or any authority or body or agency in cash or kind to the assessee other

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 14

than the subsidy or grant or reimbursement which is taken into account for determination

of the actual cost of the asset in accordance with the provisions of Explanation 10 to

clause (1) of section 43. [Sub-clause (xviii) of clause (24) of section 2 inserted vide

Finance Act, 2015, W.E.F. 1-4-2016]

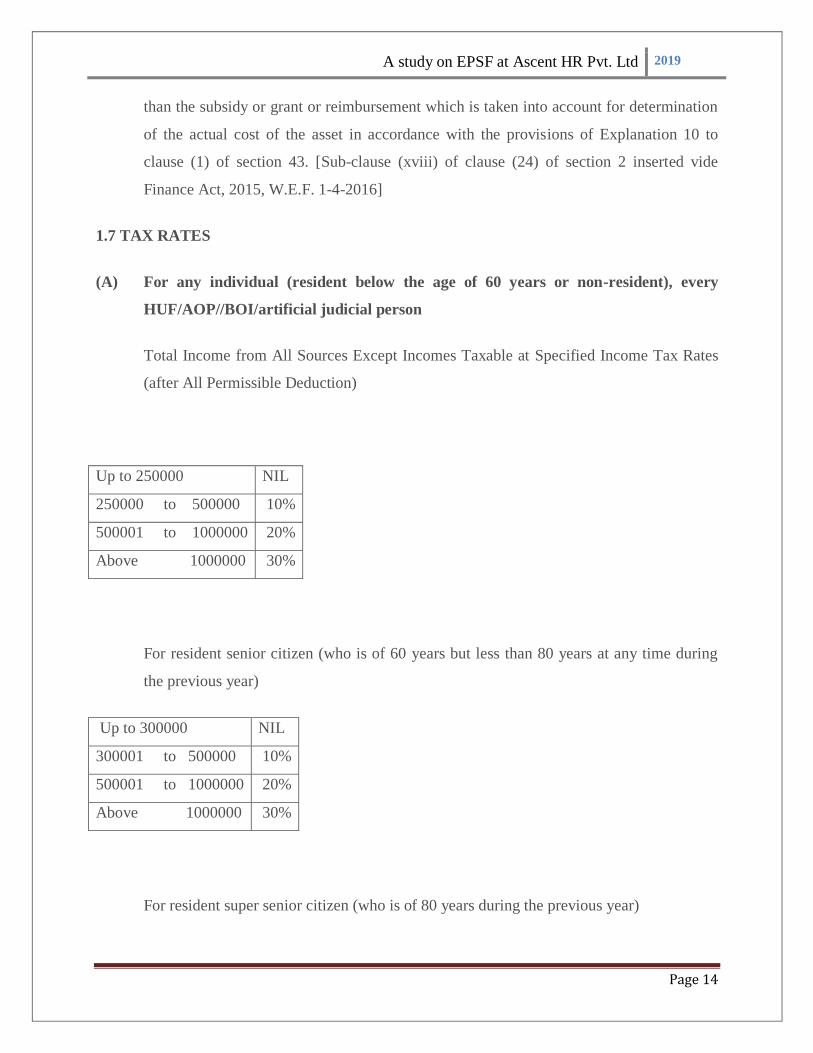

1.7 TAX RATES

(A) For any individual (resident below the age of 60 years or non-resident), every

HUF/AOP//BOI/artificial judicial person

Total Income from All Sources Except Incomes Taxable at Specified Income Tax Rates

(after All Permissible Deduction)

Up to 250000 NIL

250000 to 500000 10%

500001 to 1000000 20%

Above 1000000 30%

For resident senior citizen (who is of 60 years but less than 80 years at any time during

the previous year)

Up to 300000 NIL

300001 to 500000 10%

500001 to 1000000 20%

Above 1000000 30%

For resident super senior citizen (who is of 80 years during the previous year)

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 15

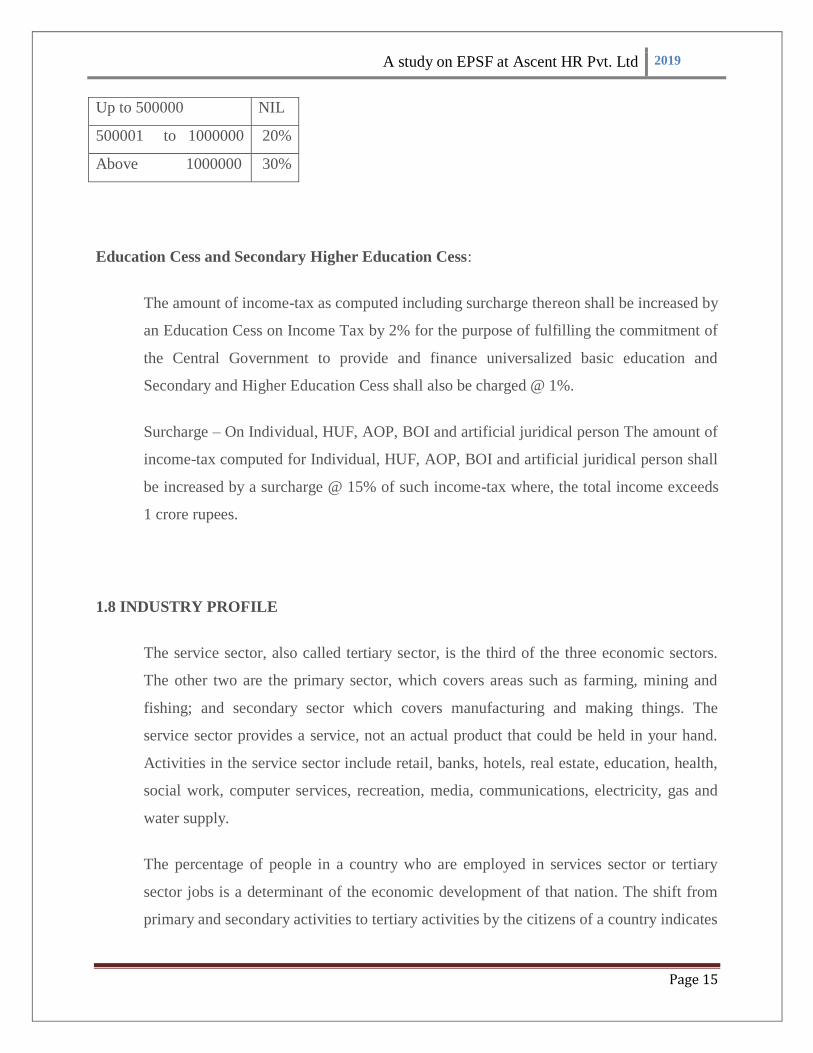

Up to 500000 NIL

500001 to 1000000 20%

Above 1000000 30%

Education Cess and Secondary Higher Education Cess:

The amount of income-tax as computed including surcharge thereon shall be increased by

an Education Cess on Income Tax by 2% for the purpose of fulfilling the commitment of

the Central Government to provide and finance universalized basic education and

Secondary and Higher Education Cess shall also be charged @ 1%.

Surcharge – On Individual, HUF, AOP, BOI and artificial juridical person The amount of

income-tax computed for Individual, HUF, AOP, BOI and artificial juridical person shall

be increased by a surcharge @ 15% of such income-tax where, the total income exceeds

1 crore rupees.

1.8 INDUSTRY PROFILE

The service sector, also called tertiary sector, is the third of the three economic sectors.

The other two are the primary sector, which covers areas such as farming, mining and

fishing; and secondary sector which covers manufacturing and making things. The

service sector provides a service, not an actual product that could be held in your hand.

Activities in the service sector include retail, banks, hotels, real estate, education, health,

social work, computer services, recreation, media, communications, electricity, gas and

water supply.

The percentage of people in a country who are employed in services sector or tertiary

sector jobs is a determinant of the economic development of that nation. The shift from

primary and secondary activities to tertiary activities by the citizens of a country indicates

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 16

that it is on the path of progress. India's services sector accounts for around 60 per cent of

its gross domestic product (GDP) and has matured considerably during the last few years.

The growth in the services sector can be attributed mostly to the emergence of the Indian

Information Technology (IT) and IT enabled Services (ITES) sectors as well as e-

commerce. The services sector in India comprises a wide range of activities such as

transportation, logistics, financial, business process outsourcing services, healthcare,

trading, and consultancies, among many others.

Furthermore, with the Government of India's liberal foreign direct investment (FDI)

policies, the services sector has attracted the highest amount of foreign equity among all

other sectors in the Indian economy. Increasingly service sector businesses need to focus

on what is now being called the ―knowledge economy‖. They need to keep ahead of

other businesses by understanding what it is their customers want and be in a position to

give it to them quickly and at low cost.

BPO Industry in India

In India, Business Process Outsourcing (BPO) is the fastest growing segment of the ITES

(Information Technology Enabled Services) industry. Factors such as economy of scale,

business risk mitigation, cost advantage; utilization improvement and superior

competency have all lead to the growth of the Indian BPO industry. Business process

outsourcing in India, which started around the mid-90s, has now grown by leaps and

bounds.

Business process outsourcing:

The term Business Process Outsourcing or BPO as it is popularly known, refers to

outsourcing in all fields. A BPO service provider usually administers and manages a

particular business process for another company.

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 17

Interesting facts about the Indian BPO industry:

The BPO sector in India is estimated to have reached a 54 per cent growth in revenue

The demand for Indian BPO services has been growing at an annual growth rate of 50%

The BPO industry in India has provided jobs for over 74,400 Indians. This number is

continuing to grow on a yearly basis. The Indian BPO sector is soon to employ over 1.1

million Indians

70% of India's BPO industry's revenue is from contact centers, 20% from data entry work

and the remaining 10% from information technology related work

Indian BPOs handle 56% of the world's business process outsourcing.

Services offered by Indian BPO companies:

Customer support services: 24/7 inbound / outbound calls center services that address

customer queries and concerns through phone, email and live chat.

Technical support services: Installation, product support, running support,

troubleshooting, usage support and problem resolution for computer software, hardware,

peripherals and internet infrastructure.

Telemarketing services: Interacting with potential customers and creating interest for the

customer's services/ products. Up-selling, promoting and cross selling to existing

customers and completing online sales processes.

IT helpdesk services: Level 1 and 2 multi-channel support, system problem resolutions,

technical problem resolution, and office productivity tools support, answering product

usage queries and performing remote diagnostics.

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 18

Insurance processing: New business acquisition and promotion, claims processing, policy

maintenance and policy management.

Data entry and data processing: Data entry from paper, books, images, e-books, yellow

pages, web sites, business cards, printed documents, software applications, receipts, bills,

catalogs and mailing lists.

Data conversion services: Data conversion for databases, word processors, spreadsheets

and software applications. Data conversion of raw data into PDF, HTML, Word or

Acrobat formats.

Book-keeping and accounting services: Maintenance of the customer's general ledger,

accounts receivables, accounts payables, financial statements, bank reconciliations and

assets / equipment ledgers.

Form processing services: Online form processing, payroll processing, medical billing,

insurance claim forms processing and medical forms processing.

1.9 COMPANY PROFILE

ASCENT HR

People Management is a key business function that has a direct impact on

competitiveness, efficiency of operations, and long-term profitability of an organization.

Which is why, organizations have been investing enormous time and resources in the HR

function, which diverts focus from the organization‘s core business.

Ascent Consulting precisely addresses this anomaly through its 360 degree HR

Management Solutions that transform the HR service delivery. While these solutions

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 19

accomplish cost reduction, greater efficiencies and improved quality, our larger effort is

aimed at improving organizational efficiency and not just creating incremental change.

Ascent has achieved this by building the right mix of skills and knowledge required for

an effective Outsourced HR Management function. Our solutions employ a matrix of

technology, domain expertise, streamlined business workflow, and highly skilled people

to create tangible, measurable, performance improvements throughout the client‘s

organization.

Ascent is recognized as one of the most trusted partners in this business by clients around

the world. We work as an extension of our client‘s business. Our management and

delivery teams are passionate about building efficiencies in our clients business.

Our bespoke technology solutions for H R Needs are unique in the industry and are

backed by the best of industry practices in Data management, Information Security, Data

Privacy, anywhere access and very user friendly processes.

Founders

Subramanyam S

Subramanyam, is the Founder, President and CEO of Ascent HR. He is a Corporate

Lawyer and a Fellow member of the Institute of Company Secretaries of India. Subbu,

had close to two decades of experience in Finance, Legal, Tax and Business

Management, having worked in these areas in various corporates as a passionate

professional before venturing to be an entrepreneur by setting up Ascent HR in the year

2002.

Geeta L

Geeta, is the Co-Founder and the Senior Vice President of Operations at Ascent HR.

Geeta is a Fellow member of the Institute of Chartered Accountants of India and a

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 20

Member of the Institute of Costs and Works Accountants of India. Prior to founding

Ascent HR, Geeta had close to a decade of experience in Audits, Taxation and Finance.

GLOBAL SMALL BUSINESS SUITE

HRMS

COMPLIANCE

BENEFITS

PAYROLL

Management Team

Keshav Chander

Keshav is the Vice President Sales & Marketing at Ascent HR. He has been part of the

management team since 2005 and has contributed immensely in its growth phase.

Rajendra Prasad Sappa (Rajan)

Rajendra Prasad Sappa (Rajan), is the General Manager of Payroll Operations handling

both Global and India at Ascent HR. He is a qualified Chartered Accountant. Prior to

Ascent HR, he was with Honeywell where he worked for 2 years in Payroll, Taxation and

Finance. He has been part of the Ascent HR team since 2005 and his contributions have

helped the company to grow in leaps and bounds.

Surendra A

Surendra A is Senior Manager Finance at Ascent HR. He is a Chartered Accountant.

Prior to Ascent HR, he had close to 3 years of experience in Audits, Taxation and

Finance. Having started his career at an Audit Firm, he later established himself as a

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 21

chartered accountant at Bangalore. Surendra has been part of the Ascent HR team since

2007 and plays a major role in our organization.

Narayan Bhat P

Narayan Bhat P, is a Senior Manager Software Development of the Power Pay Team at

Ascent. He has completed his Masters in Computer Applications. He joined Ascent in the

year 2006. All the internal software applications are developed under his gudance. He

had close to 4 years of experience in IT Infrastructure and Software applications before

joining Ascent . He started his career at Ascent as a Consultant.

Premraj K

Premraj K is a Senior Manager Software Development, leading the Power HR team. He

has completed his Masters in Computer Application. He has close to 12 years of

experience in software technologies like PHP, .net, SQL and Oracle before joining

Ascent HR. He was deputed at Symm Solutions Limited by Ascent HR and later joined

Ascent HR in 2012.

He played a major role in developing the HRMS & mobile applications and ensuring that

the applications were user friendly.

Muarlidhar S

Muarlidhar S, has been the Chief Information Security Officer ( CISO) at Ascent since

2009. He has completed his Bachelor of Science. As an Information Security Specialist

he ensures the certification standards are maintained. He has experience in Audits and IT

Infrastructure. He started his career at Ascent HR as a freelancer and later established

himself as a CISO at Bangalore.

John S Theophilus

John Sunil Theophilus, heads Global Sales as a General Manager at Ascent HR. He has

completed his Bachelors of Science. He started his career in Sales and his work has taken

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 22

him overseas and now Bangalore. He joined Ascent HR in 2010 and since then he has

been independently leading this team.

Sachin A Biraj

Sachin A Biraj, Vice President, heads the Legal division at Ascent HR. In the early years

of Ascent HR he joined Ascent HR to assist in the legal issues. He rejoined Ascent HR in

2016. He has close 15 years of experience in labour aspects. His team takes care of all

legal issues pertaining to the company and they handle all audits, HR, legal and advisory

issues for all the clients of the company. They are the legal professionals and assist the

organization on all legal matters including training the internal teams including the

clients. They ensure legal support, decisive settlement and quick resolution of critical

issues.

Indushekar G Vellal

As an Associate Vice President Sales & Marketing, Indushekar G Vellal handles all

Small & Medium Companies. He has completed his Post Graduation in Marketing. He

had close to 10 Years of experience in Strategic & Technical Planning, Business

Development and Marketing before joining Ascent HR in 2011. He had earlier worked

with Computer Garage Pvt. Ltd Bangalore.

Pradeep Srivastava

Pradeep Srivastava, Vice President, heads Ascent Staffing Solutions which is a division

of Ascent HR. He has more than 28 years of experience in HR, Talent management,

Client Acquisition, Training and Development and Industrial Relations. His team caters

to Staffing Solutions across the country. He has been part of Ascent HR team since 2015.

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 23

Services provided by Ascent Hr

HR Outsourcing

As an emerging global leader in the HR Outsourcing space, Ascent provides intuitive and

customized solutions to any enterprise irrespective of its size / scale. Our solutions

address the needs from integrated HR outsourcing solutions or complicated multi country

Payroll services to handling benefits and Compliance services across the world.

Types of HR Outsourcing service

Payroll & Compliance

Benefits Administration & Consulting

Labour Compliances

HR Consulting

Training Support

Payroll & Compliance

PAYROLL Processing is a mundane, repetitive and data-intense activity which can be a

drain on the productivity, resource utilization and costs, in the HR function of any

organization. At the same time, any errors in the data can trigger conflicts in the

workplace as well as with statutory bodies. Outsourcing Payroll Processing is the best

solution as it frees up critical human resources who can now focus on the strategic

aspects of HR.

Ascent manages intricate and time-consuming tasks of payroll processing and related

compliance requirements and powers you to focus on your business. All of the vital

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 24

payroll information, reports, and advises are made available within the agreed timeframe

through a secure web delivery system. Our services can work either as a standalone

support or seamlessly integrate with any other legacy system at your organization.

PAYROLL COMPLIANCES

Devising & developing suitable compliance processes

Devising Manuals & Systems for statutory compliances

Monitoring regulatory compliances & filing of necessary returns / records with

appropriate authorities

Handling Inspections & representations

Auditing finance / accounts processes for internal control / SOX

Devising and implementation of suitable MIS Budgets for effective control Tax Planning

& Compliance.

Regulatory Management

Provident Fund

Employee State Insurance

Profession Tax

Labour Welfare Fund

Welfare Trust Administration

Gratuity

Superannuation

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 25

Key Benefits:

One stop solution to manage nation-wide Payroll legislations

Expertise in Labour Laws of which Payroll is a sub sect

Non-core activity outsourced to a Corporate accountable Partner

Overheads by way of manpower and travel reduced

Exceptional rapport with government officials

Voluminous activity taken care of by Ascent

Complete assurance on compliance

Benefits Administration & Consulting:

Contemporary Employee Benefits solutions require a profound knowledge of

employment markets, current practices, employee needs, and compliance requirements.

Ascent‘s decade-long experience and in-depth knowledge of the HR domain, from both

the talent optimization as well as the regulatory perspectives, creates a unique advantage

based on local market knowledge, cost-efficient processes, innovation expertise, and

compliance experience. This has helped us develop and deliver tax-efficient Flexible

Benefit structures that meet both the employee‘s needs as well as organizational needs

such as employee retention and satisfaction.

Ascent partners with experts in compensation structuring, and effective insurance plans,

to achieve a vast number of seemingly contradictory objectives:

Controlling overall implication of CTC

Using insurance benefits to attract and retain the right employees

Creating time and cost-savings

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 26

Managing financial and regulatory risks

Keeping employees healthy and productive

Securing the best solutions, pricing, and service from health and benefit vendor

Labour Compliances:

Managing Human resource related compliance in an organization is a complex process in

any country of the world. In addition to innumerable documents and procedures, the

correct interpretation of the laws is also a challenge. A competent partner who can take

complete ownership of the process and validate each of the steps being undertaken saves

the hassle, reduces costs, streamlines HR processes and ensures smooth operations.

Ascent is one such enabler and offers Compliance Management related to labour laws

which help the corporate focus on their core business while being law-abiding entities.

Ascent takes care of various aspects of regulatory compliances including: obtaining

registrations or licenses, observing routine compliance covering remittances/ taxes, filing

necessary returns, maintaining required registers & records, handling inspections by

government officials, representations before Govt. authorities etc.

We also help our clients obtain the necessary exemptions for uninterrupted and hassle-

free operations. We will apprise the client of any changes in the legislations for

appropriate and timely action, to ensure total compliance.

Key Services:

Labour Law Compliance

Registrations

Designing Compliance Framework

Audits & Health Check

Representations

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 27

Advisory

Key Benefits:

A single solution to handle variations in central and state laws

Improved focus on the core business

Hassle-free liaison with peripheral stakeholders

Minimized external irritants

Staying compliant at all times

Cost savings on manpower and administrative overheads

Enhanced reputation of the organization‘s in a community

HR Consulting

Ascent has the knowledge and ability to provide HR consulting solutions across the value

chain, right from acquisition planning to cost optimization to separation management

design.

Recruiting and sourcing strategy:

o Mapping HR strategy to business strategy

o Recruitment planning and roadmap

o Identification of perception of the company brand

o Cost optimization for sourcing

Compensation and benefits:

Benchmarking study

Compensation structuring and restructuring

Design of benefits or variable pay plans

Compensation and benefits scenario modeling to predict the cost impacts of pay variation

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 28

Training, education, and development:

Skill mapping and gap analysis

Benchmarking studies

Learning management system design

Career development programme design

Workforce management:

Strategic workforce planning

Global grading system to level jobs across functions, business units, and countries

Succession planning

Retention planning and employee engagement study

Employee satisfaction study

Performance management:

Cascading alignment and design

Performance measurement system

KRA design

Separation management

Separation management system design

Exit diagnostics for root cause analysis

Others:

Employee efficiency modeling and resource optimization to understand ROI

Organization structuring and restructuring

HR Outsourcing analysis and planning

HR policy management in M&A or Restructuring

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 29

Training Support:

Ascent has always believed in sharing its deep knowledge of the HR practice to educate –

and bring about awareness in – our clients.

Towards this end, we have developed extensive training plans for clients to ensure better

management of HR services, compensation planning, benefits planning, and compliance.

These training programs are delivered either as training sessions addressing a number of

corporate, or as interactive workshops, customized to the needs of a specific business and

its practices.

HR AUTOMATION:

Ascent‘s HR Automation suite comprises five different applications, built over a

knowledge base of vast experience and real life scenarios.

Types of HR Automation services

a. Power HR

b. STOHRM

c. HR Berry

d. Power Pay

e. Power CMS

Power HR

Comprehensive Human Resource Integrated Solution covering all aspects from Hire to

Retire Ascent‘s acclaimed Power-HR Solution underpins our development strategy and is

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 30

the cornerstone of HR and Payroll departments worldwide. Fully integrated, easy to use,

flexible, intuitive and functionally rich, it meets the criteria for all types of organizations,

regardless of headcount. Key modules of Power-HR are illustrated here.

STOHRM

Modern businesses operate in highly competitive, complex, dynamic, and global

environments. A company must easily, thoroughly, and accurately understand its global

workforce (mobile, diverse, and skilled) in order to leverage it in creative and innovative

ways, make quick and meaningful business decisions, and ultimately rise above the

competition.

STOHRM Human Resource Management modules provide the foundation on which our

customers build their HR and Payroll strategies. These modules deliver a complete,

affordable, on demand solution that empowers business leaders through self-service. It

offers a dedicated, multi-functional and highly-flexible Human Resource solution that has

a simple and intuitive interface that drives employees to use the applications—this means

greater adoption of, and engagement with, the software by your workforce.

HR Berry:

Employee/Manager self services for Small or Medium Enterprises

HR Berry is an easy and efficient HR tool with a comprehensive Employee and Manager

Self-service solution supported by workflow-processes that allow employees to enter

details, and enable managers to approve various transactions along with viewing the staff

records. Extensive Help facilities and innovative product functionality ensure that the

client can extend self-service benefits throughout the company thereby empowering

employees and saving management time. HR Berry will provide the employee and

manager the following functionalities

Power Pay

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 31

Global Payroll Processing application, Power Pay is the main Payroll Processing engine

that drives our multi-country, Payroll Processing capabilities. It seamlessly integrates

with the HR Berry, Power HR & Smart Reports applications making this a unique

proposition.

Power-CMS

Comprehensive Compliance Management Solution for India Ascent‘s innovative

approach is best seen in this product which is a result of our extensive research and years

of experience in handling real life situations. At Ascent we understand a client‘s needs

not just from the process perspective but also from that of legal / compliance obligations.

We believe in assuring our clients a zero-tolerance experience in managing their

compliance needs. That is why, the product is designed to suit or be customized for any

new legislative change, and also for process enhancement in voluntary governance

standards. While Power CMS is not just a processing application, it has a complementing

interface in demonstrating the assurance through real-time dashboards and access to

compliance information at the click of a mouse

Certificates & Accreditations

ISMS (ISO 27001:2013) certified for Information Security Management

QMS (ISO 9001:2008) certified for Quality Management Processes

SSAE 16 Type II certified (formerly SAS 70 Type II)

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 32

1.10 SWOT ANALYSIS OF OUR COMPANY

The ‘SWOT’ stands for Strengths, Weakness, Opportunities and Threads.

By observing the company I came to know some of Strengths, Weakness, Opportunities

and Threads. Which are as follows:

1) STRENGTHS:

More number of clients

Reputation of the company

Wider growth

Good service provider

It is a MNC Accountability, Adoptability and Adequacy

2) WEAKNESS:

Small Company

Difficulty in balance with the last month of F.Y.

Low investment

More competition

3). OPPORTUNITIES:

Expansion of firm

Access of more investment

Getting more clients for business

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 33

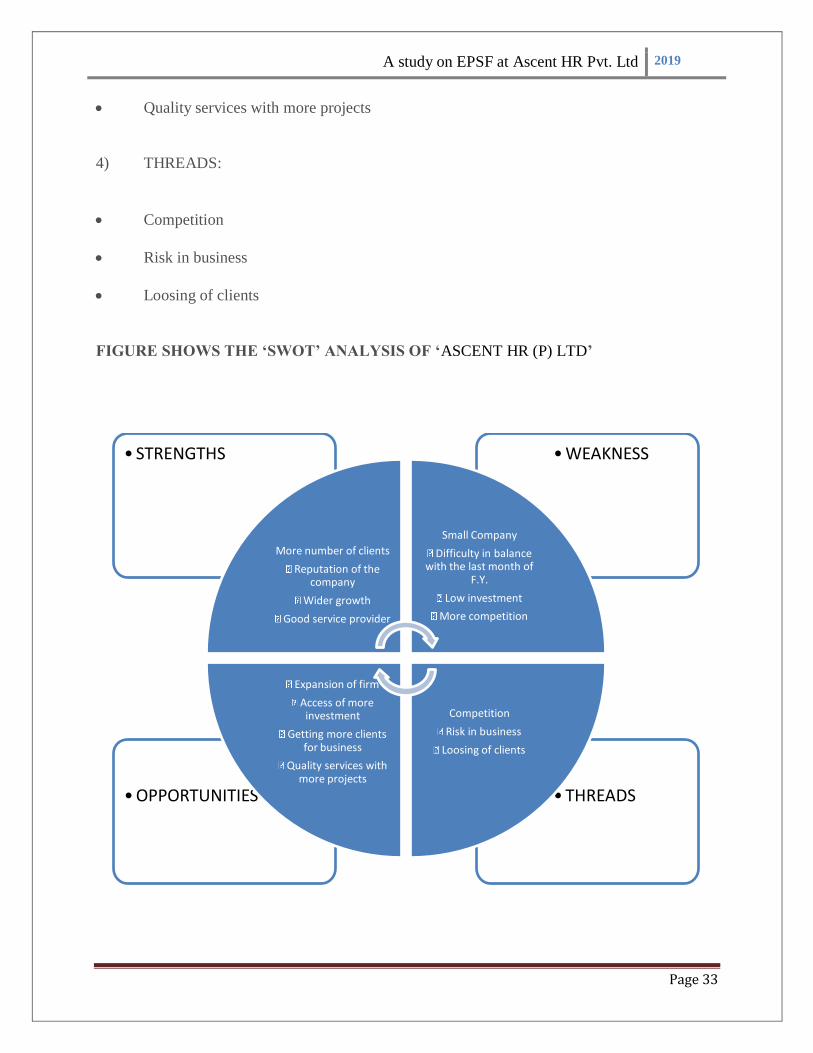

Quality services with more projects

4) THREADS:

Competition

Risk in business

Loosing of clients

FIGURE SHOWS THE ‘SWOT’ ANALYSIS OF ‘ASCENT HR (P) LTD’

•THREADS •OPPORTUNITIES

•WEAKNESS • STRENGTHS

More number of clients

Reputation of the company

Wider growth

Good service provider

Small Company

Difficulty in balance with the last month of

F.Y.

Low investment

More competition

Competition

Risk in business

Loosing of clients

Expansion of firm

Access of more investment

Getting more clients for business

Quality services with more projects

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 34

These are the Strengths, weakness, Opportunities and Threads of the ASCENT HR (P)

LTD. So by keeping in view of this ‘SWOT’ analysis, I can able to find problems and I

can also suggest some remedies to come out from that problem.

The company can go through this analysis to get more clients for their business and it is

also helpful to expand their business.

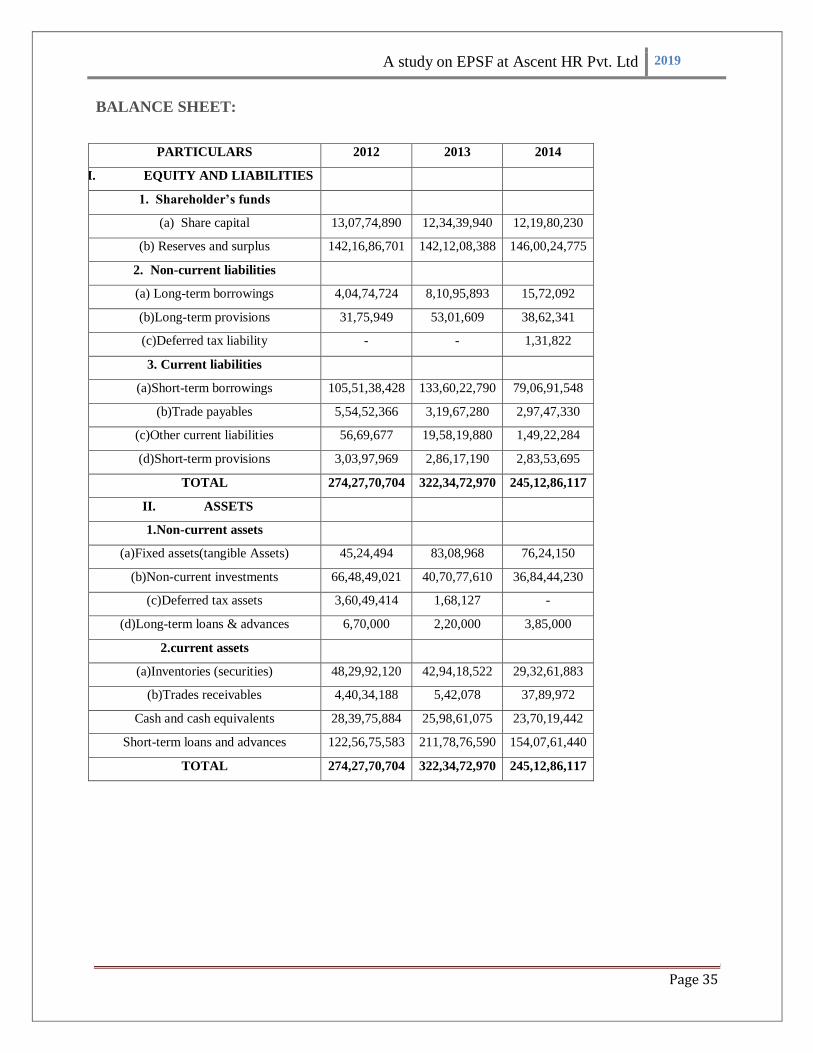

1.11 The analysis is done with the help of the following balance sheet.

PROFIT AND LOSS STATEMENT

PARTICULARS 2012 2013 2014

1.Revenue from operations 21,01,28,282 34,55,39,116 35,24,85,449

2.Other income 1,19,40,331 7,72,145 32,31,142

3.TOTAL Revenue 22,20,68,613 34,63,11,261 35,57,16,591

4.Expenses

Employee benefits expense 4,15,43,868 3,52,53,883 5,06,78,423

Finance costs 7,68,80,452 16,75,79,216 19,44,90,307

Depreciation 4,46,304 9,82,526 15,74,568

Other expenses 2,55,10,346 3,72,63,364 3,82,09,040

Provision for standard assets 31,75,949 21,25,660

5.Total Expenses 14,75,56,919 24,32,04,650 28,49,52,338

6.Profit before tax 7,45,11,694 10,31,06,612 7,07,64,252

7.Tax expense for the year 2,58,68,461 3,56,18,834 (40,05,191)

8.Profit after tax 6,74,87,778 7,47,69,443

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 35

BALANCE SHEET:

PARTICULARS 2012 2013 2014

I. EQUITY AND LIABILITIES

1. Shareholder’s funds

(a) Share capital 13,07,74,890 12,34,39,940 12,19,80,230

(b) Reserves and surplus 142,16,86,701 142,12,08,388 146,00,24,775

2. Non-current liabilities

(a) Long-term borrowings 4,04,74,724 8,10,95,893 15,72,092

(b)Long-term provisions 31,75,949 53,01,609 38,62,341

(c)Deferred tax liability - - 1,31,822

3. Current liabilities

(a)Short-term borrowings 105,51,38,428 133,60,22,790 79,06,91,548

(b)Trade payables 5,54,52,366 3,19,67,280 2,97,47,330

(c)Other current liabilities 56,69,677 19,58,19,880 1,49,22,284

(d)Short-term provisions 3,03,97,969 2,86,17,190 2,83,53,695

TOTAL 274,27,70,704 322,34,72,970 245,12,86,117

II. ASSETS

1.Non-current assets

(a)Fixed assets(tangible Assets) 45,24,494 83,08,968 76,24,150

(b)Non-current investments 66,48,49,021 40,70,77,610 36,84,44,230

(c)Deferred tax assets 3,60,49,414 1,68,127 -

(d)Long-term loans & advances 6,70,000 2,20,000 3,85,000

2.current assets

(a)Inventories (securities) 48,29,92,120 42,94,18,522 29,32,61,883

(b)Trades receivables 4,40,34,188 5,42,078 37,89,972

Cash and cash equivalents 28,39,75,884 25,98,61,075 23,70,19,442

Short-term loans and advances 122,56,75,583 211,78,76,590 154,07,61,440

TOTAL 274,27,70,704 322,34,72,970 245,12,86,117

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 36

LIQUIDITY RATIOS:

SL NO. RATIO FORMULA 2012 2013 2014

1 Current ratio Current assets

Current liabil0ities

2036677775

1146658440

=1.78

2807698265

1592427140

=1.76

2074832737

863714857

=2.06

2 Quick ratio Liquid assets

Current liabilities

1553685655

1146658440

=1.35

237827943

1592427140

=1.49

1781570854

863714857

=2.06

3 Cash ratio Cash

Current liabilities

283975884

1146658440

=0.25

259861075

1592427140

=0.16

237019442

863714857

=0.27

LEVERAGE RATIOS:

SL NO RATIO FORMULA 2012 2013 2014

1 Debt-equity ratio Debt

Equity

11903099113

1552461591

=0.77

1678824642

1544648328

=1.09

869281112

1582005005

=0.55

2 Debt to assets ratio Debt

Total assets

1190309113

3742770704

=0.43

1678824642

3223472970

=0.52

869281112

2451286117

=0.35

3 Net worth ratio Networth

Total assets

1552461591

2742770704

=0.57

1544648328

3223472970

=0.48

1582005005

2451286117

=0.65

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 37

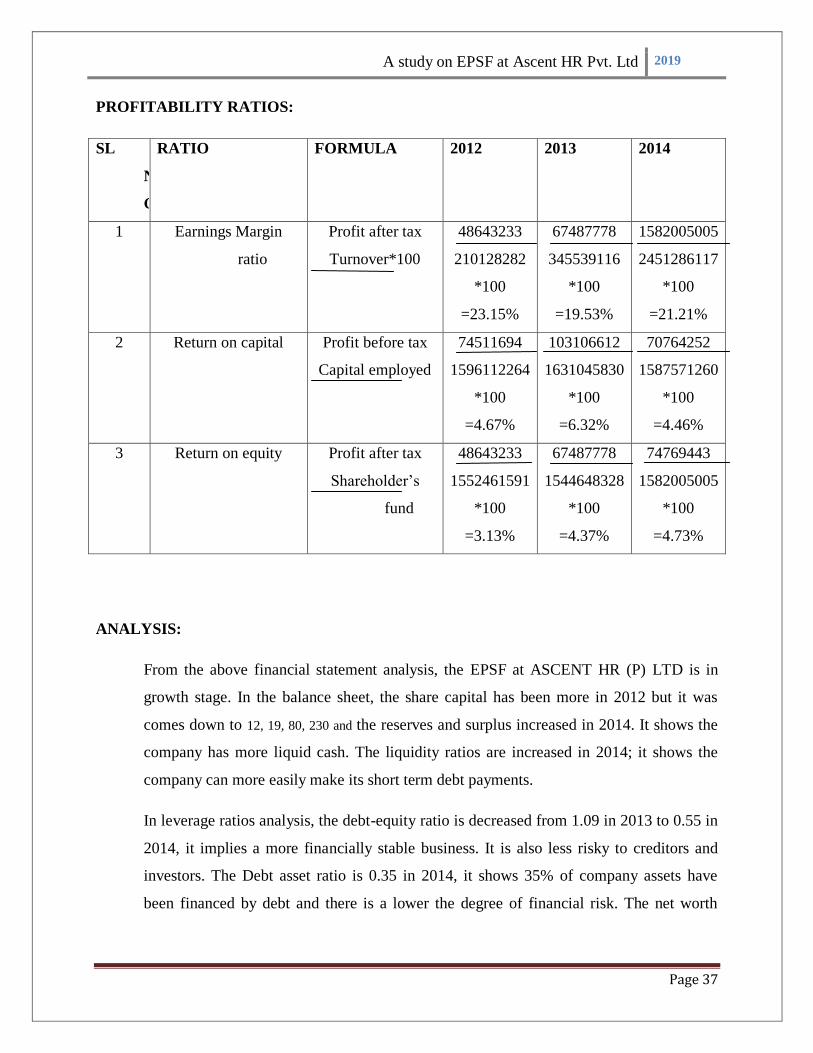

PROFITABILITY RATIOS:

SL

N

O

RATIO FORMULA 2012 2013 2014

1 Earnings Margin

ratio

Profit after tax

Turnover*100

48643233

210128282

*100

=23.15%

67487778

345539116

*100

=19.53%

1582005005

2451286117

*100

=21.21%

2 Return on capital Profit before tax

Capital employed

74511694

1596112264

*100

=4.67%

103106612

1631045830

*100

=6.32%

70764252

1587571260

*100

=4.46%

3 Return on equity Profit after tax

Shareholder’s

fund

48643233

1552461591

*100

=3.13%

67487778

1544648328

*100

=4.37%

74769443

1582005005

*100

=4.73%

ANALYSIS:

From the above financial statement analysis, the EPSF at ASCENT HR (P) LTD is in

growth stage. In the balance sheet, the share capital has been more in 2012 but it was

comes down to 12, 19, 80, 230 and the reserves and surplus increased in 2014. It shows the

company has more liquid cash. The liquidity ratios are increased in 2014; it shows the

company can more easily make its short term debt payments.

In leverage ratios analysis, the debt-equity ratio is decreased from 1.09 in 2013 to 0.55 in

2014, it implies a more financially stable business. It is also less risky to creditors and

investors. The Debt asset ratio is 0.35 in 2014, it shows 35% of company assets have

been financed by debt and there is a lower the degree of financial risk. The net worth

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 38

ratio is increased from 0.57 in 2012 to 0.65 in 2014; this increase in net worth indicates

good financial health or sound financial health of a company.

In the Profitability ratio analysis, the earnings margin ratio is decreased from 23.15% in

2012 to 19.53% in 2013 which in turn increased to 21.21% in 2014; it measures how

effectively a company can convert turn over into net income. An extremely low profit

margin would indicate the expenses are too high and the management need to budget and

cut expenses. The return on capital employed ratio is decreased from 6.32% in 2013 to

4.46% in 2014; it indicates that less favorable because less profit is generated by each

rupee of capital employed. And return on equity is gradually increased from 3.13% in

2012 to 4.37% and 4.73% in 2013 and 2014 respectively. It shows a company can use the

money from share holder’s to generate profits and grow the company.

Therefore, the overall financial reports analysis shows that EPSF at ASCENT HR (P)

LTD is in good financial position and well performed growing company.

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 39

CHAPTER-2

LITERATURE REVIEW

2.0 REVIEW OF LITERATURE:

Savita and Rohtak Lokesh Gautam(2013) ―Income Tax Planning: A Study of Tax

Saving Instruments‖ The purpose of the study is to find out the most suitable and popular

tax saving instrument used to save tax and also to examine the amount saved by using

that instrument. Over all findings reveals that the most adopted tax saving instrument is

Life Insurance policy, which got the first rank in this study and the second most adopted

tax saving instrument is Provident Fund.

Dr. Ahuja, Girish and Dr. Gupta, Ravi. (2007) ―Systematic approach to Income Tax and

Central Sales Tax‖ Book, Bharat Law House Pvt. Ltd. Publication, New Delhi.

Lal, B.B and Vashisht, N. (2008) ― Direct Taxes, Income Tax, Wealth Tax and Tax

planning‖ Book, Pearson Education, New Delhi.

Singh and Sharma (2007) made an attempt to study the perception of tax professionals

with regard to Indian Income Tax System by collecting primary data from 100 tax

consultants operating in Punjab and Haryana. Factor Analysis of data showed that seven

factors – reduction in tax evasion, extension of relief to taxpayers, incentives for

dependents and honest taxpayers, broadening the tax base, e-filing of returns, adequacy

of deductions and impact of exempt-exempt tax system played an important role in

determining the effectiveness of Indian tax system.

It was observed that most of the tax consultants were satisfied with tax rates. However,

majority showed dissatisfaction with regard to price level adjustment. It was also

observed that most of the taxpayers consulted tax experts because they found it cheap.

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 40

A study conducted by Nagajothi, R.S. and Hasanbanu, S. (2007)86 article ―A Study of

the Insurance Perspective in Uthamapalayam Taluk‖ Indian journal of marketing revealed

that in India, the insurance has not been on the main agenda of either individuals or

corporate.

Hence, reforms encompass not merely regulatory intervention but also promotional effort

to develop the market. The steady growth of the industry, as also the consolidation of

private players progressively bears a silent testimony to the proactive regulatory regime

in place in India.

A study conducted by Bodla, B.S. and Sushma Rani Verma (2007)87 article ―Life

Insurance Policies in Rural Area and Understanding Buyer Behavior, ICFAI University

revealed that insurance sector plays a very important role in the development of any

economy and it provides long-term funds for infrastructure development and at the same

time strengthens the risk taking ability.

A study conducted by Tanmay Acharya, Harshita Mishra and Venkataseshaiah, S.

(2007)88 article ―Customer Preferences in Insurance Industry in India‖. The ICFAI

journal of marketing services revealed that the purchasing decision of the consumer

depends on quality, accessibility, company type, recommendations and promptness of

service. India is poised to experience major changes in its insurance markets as insurers

operate in an increasingly deregulated and liberalized environment. For consumers,

opening up of the insurance sector will mean new products, better packaging and

improved customer service.

Patil, P.B. and Thakkar, P.N. (2007)89 article ―Impact of Disinvestment on Banking and

Insurance Sector‖ revealed that a strong competition among the insurance companies has

led to better services being provided by customer satisfaction can be known from the

customer retention ratio. Now most of the companies are customer centric approach,

rather than product centric approach which is leading to customer-retention ratio.

A study conducted by Sunayna Khurana (2008)91 article ―Customer Preferences in Life

Insurance Industry in India‖, revealed that the insurance sector plays a very important role

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 41

in the development of any economy. It is necessary for the economic and overall

development of any country. In today‘s competitive economy, the business, finance and

insurance sector plays a very important role. More and more job opportunities are

available in these sectors.

A study conducted by Raju, S. and Gurupandi, M. (2009)92 in their article ―Analysis of

the Socio Economic Background and Attitude of the Policyholders towards Life

Insurance Corporation of India‖, Smart Journal of Business Management Studies revealed

that the study was of great help to the policyholders, as it was aimed at finding the

attitude towards the services of Life Insurance Company. Hence the prospective

customers, who propose to buy the insurance products and avail of the services of an

insurance company for the first time, can get benefited by the best service provider.

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 42

CHAPTER-3

RESEARCH METHODOLOGY

3.0 NEED FOR THE STUDY

A study on the impact of Life Insurance premium Income Tax deduction to salaried

employees at Ascent HR Pvt. Ltd.

3.1 OBJECTIVES OF THE STUDY

1. To understand concept of Life Insurance Premium as a tax benefit component

2. To study the concept of proof verification

3. To analyze reasons for rejections in Life Insurance Premium

4. To provided suitable suggestions based on findings

5. To analyze the concept of tax validation

6. To evaluate the Quality Check (QC)

7. To analyze the proofs that forms a part of deduction under 80C to 80U

8. To understand the benefits available for an employee to get tax deduction

3.2 TOPIC CHOOSEN FOR THE STUDY

A study on EPSF at Ascent HR Pvt. Ltd

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 43

3.3 THEORETICAL BACKGROUND OF THE STUDY:

Insurance

Meaning

Insurance is a promise of compensation for any potential future losses. It facilitates

financial protection by reimbursing losses during crisis. There are many insurance

companies offering a wide range of insurance options to choose from. Some of the

popular insurance policies are life insurance, health insurance, automobile insurance and

home insurance.

Several insurances provide comprehensive coverage with affordable premiums.

Premiums are the amount of money that is charged by the insurance companies from the

insurer for a particular insurance policy. These are periodical payment and insurers have

diverse premium options. The periodical insurance premiums are calculated according to

the total insurance amount.

Definition of Insurance

David King ―A funds generally range from lifetime security for you and your

beneficiaries to immediate needs such as the education expenses of your children. A life

insurance plan gives benefits to your family or another beneficiary in case of untimely

death.‖

Types of Insurance

Major types of insurances are as mentioned below

Life insurance:

Life insurance is a financial security for the family after the insurer passes away. It helps

the family overcome the loss of income resulting from the death of the insurer. The

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 44

person who has been named as the beneficiary receives the amount after the insurer

passes away.

Automobile insurance:

Automobile insurance is aimed at the owner of a vehicle and covers damages and legal

expenditures resulting in financial losses such as accidents.

Health insurance:

Health insurance takes care of the cost of medical treatment and other expenditures.

Premium is the amount of money paid by the policy-holder or their sponsor (who is

basically an employer to the health plan to buy health coverage. The dental insurance

covers the dental costs of the insurer.

Credit insurance:

Credit insurance is a kind of a life insurance and is helpful in times of financial crisis.

Borrowers often fail to repay debts, loans and mortgages due to certain unavoidable

circumstances. These can be paid off with credit insurance.

Property insurance:

Property protection insurance provides protection from risks associated to theft, fire,

floods, and so on. Property insurance will also provide financial protection to the

homeowner in case somebody who has been injured on the property decides to sue. This

type of insurance can be further classified into specialized forms as follows:

Fire insurance

Earthquake insurance

Flood insurance

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 45

Home insurance

Boiler insurance

Life Insurance premium

Meaning:

A life insurance policy provides cash payment when a person dies. This payment is

known as the death benefit. Many people buy life insurance to protect the people who are

dependent on them.

Others buy life insurance as a way to leave a cash gift to their spouse, children,

grandchildren, and charities at their death. If you have made the decision to buy a policy,

you may wonder which type of policy to choose since there are several different types of

policies.

The policy is written on the life of a person, known as the insured. The owner makes

payments, known as premiums, to the insurance company for the policy. In return, the

insurance company agrees to pay the death benefit to the beneficiary if the insured dies

within the stated term.

Types of life insurance premium:

Term Insurance: Term Insurance, as the name implies, is for a specific period, and has the

lowest possible premium among all insurance plans. You can select the length of the term

for which you would like coverage, up to 35 years. Payments are fixed and do not

increase during your term period. In case of an untimely death, your dependents will

receive the benefit amount specified in the term life insurance agreement. You can

customize Term life insurance with the addition of riders, such as Child, Waiver of

Premium, or Accidental Death. Endowment Insurance:

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 46

There is a savings quotient linked to such policies. They come with a specified maturity

period, as decided by the insurer. On the occurrence of any unforeseen event of the death

or permanent disability, during the tenure of the policy; the sum assured will be received

by the said beneficiaries to the policy. If the insured survives the term of the policy, the

agreed maturity benefits become payable.

Whole Life Insurance:

Whole Life Policies have no fixed end date for the policy; only the death benefit exists

and is paid to the named beneficiary. The policy holder is not entitled to any money

during his or her own lifetime, i.e., there is no survival benefit. This plan is ideal in the

case of leaving behind an estate.

Primary advantages of Whole Life Insurance are guaranteed death benefits, guaranteed

cash values, and fixed and known annual premiums.

Money-Back Plan:

In a Money-Back plan, you regularly receive a percentage of the sum assured during the

life time of the policy. Money-Back plans are ideal for those who are looking for a

product that provides both - insurance cover and savings.

It creates a long-term savings opportunity with a reasonable rate of return, especially

since the payout is considered exempt from tax except under specified situations.

ULIP:

Unit-linked Insurance Plans (ULIPs), introduced by the private players, are hugely

popular, because they combine the benefits of life insurance policies with mutual funds.

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 47

A certain part of the premium is invested in listed equities/debt funds/bonds, and the

balance is used to provide for life insurance and fund management expenses.

Pension Plan:

Insurance companies offer two kinds of pension plans - endowment and unit linked.

Endowment plans invest in fixed income products, so the rates of return are very low.

Unit-linked plans are more flexible. You can stop contributing after 10 years and the fund

will keep compounding your corpus till the vesting date. You can opt for higher exposure

in the stock market for your plan if your risk appetite allows it. Lower risk options like

balanced funds are also offered.

Riders: Comprehensive coverage:

In addition to the insurance plan of your choice, you might want to consider additional

risk covers, in which case you can you can opt for riders: additional benefits that can be

purchased with an insurance policy.

Examples of riders include the Term rider, the Accidental Death Benefit rider, and the

Critical Illness rider. Choosing the right set of riders ensures a comprehensive insurance

cover.

Only the premiums paid up to the date of death will be refunded; after deducting the

expenses incurred by the insurer for issuing the cover.

Benefits of life insurance

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 48

Almost all the above mentioned life insurance policies serve as a boon to face the

uncertainties in life boldly. Some of the general benefits of these plans are as follows.

Death Benefits: Most of the Life Insurance Policies provides protection to the family or

the guarantor in case of unfortunate death of the nominee.

Maturity Benefits: During the time of maturity you will get the guaranteed money back

plus other added benefits mentioned in the plan. In some of the plans there is also an

option to withdraw certain money during regular interval.

Tax Benefit: As per section 80C of Income Tax Act the amount you pay as a premium is

benefited from your tax amount, however this is limited upto Rs. 150000 per annum.

Loan Facility: Some of the Insurance Policies allow you to take loan against your policy.

In this case loan amount depends on the life insurance policy, premiums paid and the

overall term.

Riders: Riders are some added benefits along with the life insurance coverage. Some of

the insurance policies allow you to invest part of your premium amount on market shares

thereby helping to gain extra bonus.

Life Insurance Companies in India

AEGON Life Insurance

Aviva Life Insurance

Bajaj Allianz Life Insurance

Bharti AXA Life Insurance

Birla Sun Life Insurance

A study on EPSF at Ascent HR Pvt. Ltd 2019

Page 49

Canara HSBC OBC Life Insurance

DHFL Pramerica Life Insurance

Edelweiss Tokio Life Insurance

Exide Life Insurance

Future General India Life Insurance

HDFC Standard Life Insurance

ICICI Prudential Life Insurance

IDBI Federal Life Insurance

India First Life Insurance Company Ltd - India First

Kotak Life Insurance

Life Insurance Corporation of India

Max Newyork Life Insurance

PNB MetLife Insurance

Reliance Life Insurance

Sahara Life Insurance

SBI Life Insurance