UN IVERSI TÀ DEGL I STUD I DI SI ENA F A C O L T À D I E C O N O M I A

QUADERNI SENESI DI ECONOMIA AZIENDALE E DI RAGIONERIA COLLANA DIRETTA DA GIUSEPPE CATTURI

ROBERTO DI PIETRA ANGELO RICCABONI

OPENING A “WINDOW” ON

ITALIAN ACCOUNTING HARMONIZATION:

A FIVE YEAR EMPIRICAL ANALYSIS

Serie interventi, n° 52 Siena, aprile 1999

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 2

OPENING A “WINDOW” ON

ITALIAN ACCOUNTING HARMONIZATION:

A FIVE YEAR EMPIRICAL ANALYSIS

ROBERTO DI PIETRA* - ANGELO RICCABONI**

ABSTRACT: In this study we analyse the degree of harmonization in annual accounts published by a significant sample of Italian quoted companies from 1992 to 1996. It is particularly useful to observe the evolution of accounting practices in Italy during this period following the enactment of the European Directives on annual and consolidated accounts. This analysis attempts to verify if a relationship exists between accounting practices and the characteristics of the Italian accounting regulation model. We have used the VAN DER TAS rating method based on the determination of analytical measures. Our research results show that the “material harmonization” of Italian accounting practices is directly linked to the key role of the legislature (the role of the fiscal authorities appears to be particularly incisive); it is not governed by the procedures of a private or governmental rule-making body, nor is it based on accounting standards. As to informational distortions created by fiscal regulations, these may be better appreciated when

*) Associate professor of Economia Aziendale, Dipartimento di Sistemi e Istituzioni per l’Economia, Università di L’Aquila. **) Associate professor of Economia Aziendale, Dipartimento di Studi Aziendali e Sociali, Università di Siena. Address for correspondence: Dipartimento di Studi Aziendali e Sociali, Facoltà di Economia - Università degli Studi di Siena - Piazza San Francesco, n° 17 - 53100 - Siena - Tel.: +39-577-298658 - Fax: +39-577-298641 - E-mail: [email protected] / [email protected].

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 3

accounting regulation is assessed within its distinctive political system. The concentration indexes recorded for the period under study and with respect to certain formal accounting aspects (layout and content) and substantial aspects (valuation criteria) in the first case illustrate a trend toward limited levels of accounting harmonisation, while in the second case the evolution observed confirms high levels of accounting harmonisation. In short the results of our research confirm that Italian accounting regulation would seem to have arisen directly from the Italian political system as a whole within the context of a vast process of regulation involving numerous subjects interacting according to largely unpredictable mechanisms.

SUMMARY: 1. Introduction and research methods; 2. Characteristics of the selected quoted companies; 3. Analysis of layout and content; 4. Analysis of valuation criteria; 5. Conclusions; Bibliography.

1. INTRODUCTION AND RESEARCH METHODS

In this study we have analysed the accounting practices of a significant sample of Italian quoted companies in order to appreciate the capacity of the accounting regulation model to achieve greater accounting harmonisation in balance sheets prepared following the imposition of the European directives. The C index of comparison proposed by L. VAN DER TAS (1988) was used to reveal that “material harmonization” in accounting practices may be observed in contexts with a strong pole of normative influence (fiscal authority or CONSOB), and to show that heterogeneity emerges when this element does not exist.

The aim of the surveys conducted was to verify if a coherent relationship exists between the accounting practices adopted in compiling annual accounts and the nature of the accounting regulation model in use within the Italian scenario.

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 4

Thus we intend to discover if a greater or lesser extent of accounting harmonisation as measured with L. VAN DER TAS’s index might derive from the characteristics and application of the Italian model for issuing accounting regulation.

The practices followed in the preparation of annual accounts and the utilization of information by various stake-holders in fact represent the feed-back of conformation to European regulation.

The preparers of annual reports above all need accounting practices which affirm a series of generally accepted or uniform processes and interpretations. The spreading of uniform accounting practices in applying the current norms calls for the presence of a generally accepted standard setting body which should have independent and normative powers.

We have considered two approaches to the evaluation and measurement of the harmonization process. The first method was proposed by J. S. W. TAY and R. H. PARKER (1990), and the second, an application of the index of comparability, was introduced by L. VAN DER TAS (1988, 1992a)(1).

According to TAY and PARKER, a dichotomy between harmonization and standardization in accounting does not exist, as the first states in a dynamic sense what the second illustrates in a static sense. Being able to measure the uniformity or heterogeneity of the accounting practices in a given country allows us to note the evolutionary process of accounting procedures and to carry out international comparisons(2).

(1) On the measurement of the degree of harmonization we also refer to the following contributions: G. S. H. ARCHER, P. DELVAILLE and S. J. MCLEAY (1994,1995) R. MAJALA (1994), R. D. NAIR and W. G. FRANK (1981), L. VAN DER TAS (1992b, 1992c, 1992d), J. S. W. TAY and R. H. PARKER (1992). (2) See the terminological distinctions proposed by J. S. W. TAY and R. H. PARKER (1990).

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 5

An analysis of uniformity and heterogeneity in the accounting procedures of a given country is conceptually closely related to the idea of harmony – lack of harmony proposed and measured by L. VAN DER TAS (1988). The author, taking into consideration the HIRSCHMAN-HERFINDAHL index, defines the index of comparison (C index) by stating that two annual accounts may be compared in their use of an accounting processes with respect to a particular problem, or that they may adopt the same solution or the same valuation criteria(3). The index proposed by VAN DER TAS compares the annual accounts of two or more firms and measures the potential and maximum number or possible effective comparisons.

For the “i” adopted method and the “n” considered firms, the number of effective comparisons will be given by the sum of all the pairs of comparable firms, or rather:

( a 1

2 − a

1 ) + ( a

2

2 − a

2 ) + . . . + ( a

i

2 − a

i )

2

with “a” representing the firms which adopt the same treatment or accounting method “i”. For the effective comparisons of “n(n - 1)/2” potentials, the determination of comparability index “C” is added:

CIndex =

a t 2

t = 1

i

∑

− n

n 2

− n

(3) The concentration index may be formalized as follows:

H = p i 2

i = 1

m ∑

where “H” is the HIRSCHMAN-HERFINDAHL index, “m” are the accounting methods of which alternatives and “pi” are the frequencies relative to each method. Even if the exponent H is easily determined, it does not grant the significance of the changes in the degree of harmony to follow, nor does it consider the possibility of “multiple methods”. Regarding the limits connected to the application of the concentration index, see the considerations proposed by J. S. W. TAY and R. H. PARKER (1990).

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 6

The index thus constructed implicitly hypothesizes that every firm adopts a single accounting process in response to a given specific problem. If one considers the possibility of multiple methods (the principal method expressed in the balance sheet or in the income statement plus the others reported in the notes to the accounts), the formal expression of the index is complicated, since the comparisons (a jk

2 − a jk ) must also be added for the firm which

uses the methods ranging from “j” to “k”. In each case, the index of comparison expresses values from 0 to 1, or rather from null to the maximum(4).

In this study we have adopted the formula for a single method, as we have not compared the recourse to alternative methods reported in the notes to the accounts. We will, however, refer to two guiding principles:

a) accounting procedures are affected by the structure of the Italian accounting regulation model(5);

b) the observed practices depend upon the existence of one or more poles of normative influence which should be characterized by the key-role of the legislature in a context in which accounting regulation policy arises from a system which must be considered as a whole.

In the following paragraph we will describe the nature of a characteristic sample of principal Italian quoted companies. In the third and fourth paragraphs we will expound our analysis, separately considering the aspects of layout, content and valuation criteria in connection with the preparation of annual accounts by the companies included in the sample. These observations will

(4) In 1992 the same author proposed a perfected version of the “C index” which was used as a reference in the study by G. S. H. ARCHER, P. DELVAILLE and S. J. MCLEAY (1994). (5) See A. RICCABONI (1998), R. DI PIETRA (1997) and R. DI PIETRA and A. RICCABONI (1998).

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 7

illustrate the variety of accounting practices revealed by the study and suggest a pattern of causes for uniformity or heterogeneity.

2. CHARACTERISTICS OF THE SELECTED QUOTED COMPANIES

Our sample of reference was created by considering some of the most important Italian quoted companies. The 25 firms included in the survey satisfied the following criteria: a) they weresubject to the norms foreseen by the Civil Code on the subject of annual accounts(6); b) they had been quoted for the entire period under consideration, that is, starting from 1992.

The sample group thus defined consists of 25 firms classified within the first 70 positions of the ranking for capitalisation compiled as of 31 December 1996 by the Milanese Stock Market Council(7). This leads us to presume that the observations in this study overestimate the Italian situation, given that the sample represents the best and most advanced accounting procedures and those procedures which are able to induce widespread emulation.

The sample is heterogeneous, as it includes categories of companies which perform profoundly different business activities. The sample includes 12 industrial firms, 1 commercial firm, 3 service firms and 9 financial holdings of industrial investments. In proportional terms, the sample may be represented with the following graph:

(6) Quoted companies which are subject to special budgetary norms (banks, insurance companies, credit and financial agencies, etc.) were excluded. (7) Table 1 indicates in parentheses the positions held by each company in their classification by capitalisation published on 31 1996 by the Stock Market Committee. It should also be noted that 14 out of 25 (over55%) of the companies included in our sample group are listed among the top 40 in this classification.

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 8

Figure 1 - Sample composition

SAMPLE COMPOSITION

48%4%

12%

36%

Industrial Companies

Commercial Companies

Service Companies

Financial Holdings

The sample provides ample illustration of the variety of accounting practices as it includes companies characterized by evident management specificity, and because it presents the most advanced degree of accounting practices in Italy. The results will also enable us to detect imitative practices on the part of companies and small and medium sized businesses.

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 9

Table 1 - The quoted companies included in the sample

INDUSTRIAL COMPANIES COMMERCIAL COMPANIES SERVICE COMPANIES FINANCIAL HOLDINGS

1. Benetton (23) 2. Saipem (26) 3. Sirti (31) 4. Olivetti (36) 5. Italcementi (37) 6. Mondadori Editore (43) 7. Snia BPD (47) 8. Cartiere Burgo (52) 9. Sorin Biomedica (58) 10. Magneti Marelli (60) 11. Falch (65) 12. Marzotto (66)

1. La Rinascente (42) 1. Telecom Italia (4) 2. Italgas (17) 3. Autostrade (39)

1. Stet (2) 2. Fiat (6) 3. Montedison (16) 4. Pirelli SPA (18) 5. Parmalat (22) 6. Ifil (25) 7. Ifi PRV (49) 8. Avir Finanziaria (56) 9. Cir (69)

The economic nature of the sample companies reveals a considerable prevalence of private capital firms, even if this prevalence is not necessarily repeated in the types of management.

As to ownership status, the sample consists of: a) 76% private capital companies; b) 12% entirely government - owned companies; c) 12% partly government - owned companies.Some of the sample companies, although they conduct different types of business activity, belong to the same economic group(8). This presents an extremely interesting point, being that parent companies tend to spread uniform accounting conduct within the same group. To more easily manage the complex procedure of consolidating the annual accounts of subsidiary companies, parent companies publish accounting manuals for the preparation of annual accounts. Specific and sometimes minute procedures subsequently become the norms of accounting conduct in layout , content and valuation criteria.The fact that the sample is entirely composed of quoted companies influences accounting practices, (8) For instance IFI and La Rinascente belong to the “Agnelli” group or Stet, Telecom and Alitalia are part of the “IRI” group.

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 10

since these companies are obliged to submit annual accounts to audit. The quoted firms, because of their numerous categories of stake-holders, are also subject to examination and to the strong normative powers of CONSOB in the compilation of annual accounts.

Table 2 - Ownership of the companies included in the sample Companies Economic nature of the ownership

Private Partly government owned Government owned

I) Industrial companies 1. Benetton 2. Saipem 3. Sirti 4. Olivetti 5. Italcementi 6. Mondadori Editore 7. Snia BPD 8. Cartiere Burgo 9. Sorin Biomedica 10. Magneti Marelli 11. Falch 12. Marzotto

X X X X X X X X X X

X X

Sub Total 10 - 2

II) Commercial companies 1. La Rinascente

X

Sub Total 1 - -

III) Service companies 1. Telecom Italia 2. Italgas 3. Autostrade

X X

X

Sub Total - 1

IV) Financial holdings 1. Stet 2. Fiat 3. Montedison 4. Pirelli SPA 5. Parmalat 6. Ifil 7. Ifi PRV 8. Avir Finanziaria 9. Cir

X X X X X X X X

X

Sub Total 8 1 -

TOTAL 19 3 3

After a long and troubled process, Legislative Decree n° 127 of 1991 enacted the Fourth Directive in Italy(9). We analysed the (9) According to law, the new rules were to be followed starting with the annual accounts of June 30, 1993, even though most Italian companies close their

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 11

annual accounts published during the period 1993-1997, beginning our observation of the accounting conduct of the quoted companies included in the survey a year prior to the moment in which the application of the European Directives enacted with Legislative Decree n° 127 of 1991 was to become obbligatory. This allowed us to note how certain firms had already adapted their accounting practices to the new norms during the transitional period.

This analysis aimed to establish if over the years companies had developed the tendency to compile their operating budgets with harmonized accounting practices in line with the objectives set by the European Directive.

In fact, the directives on accounting matters issued at the Community level were issued to pursue the objective of accounting harmonization and launch a convergence process of the accounting submittal and practices of the various EC countries and therefore of the accounting practices in the firms operating within Europe.

The European directives, issued in 1978 and in 1983 (n° 78/660/EEC and n° 83/349/EEC), present a minimal normative content. Of note is the inclusion of options which each country has enacted by selecting a specific series of possibilities conceded by the Community legislation. Legislative Decree n° 127 of 1991 represents the political result of an accounting regulation process strongly influenced by the structural and dynamic characteristics of the Italian accounting regulation model. It is, in other words, the result of a vast process of regulation involving numerous subjects interacting according to considerably unpredictable mechanisms: Italian accounting regulation seem to have arisen directly from the Italian political system as a whole(10).

accounts on December 31. Regarding the enactment process of the Community directives in matters of annual accounts we refer to the following contributions: F. DEZZANI, P. PISONI and L. PUDDU (1991), A. PROVASOLI (1988). (10) See R. DI PIETRA and A. RICCABONI (1998).

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 12

3. ANALYSIS OF LAYOUT AND CONTENT

We define layout and content as all of the questions which have an immediate effect on the form of presentation of the items in the annual accounts. The regulations of the Fourth Directive which have been enacted in Italy have cited (in various points and at various levels) the accounting principle of clarity(11).

Respect for the principle of clarity and the specific regulations contained in Decree Law n° 127 created considerable practical problems during the initial compilations of annual accounts prepared in accordance with the norms of the European Directive. The issues that we will consider in this paragraph are only some of those faced by the preparers of annual accounts, and the resulting procedures are extremely significant for the analysis of uniformity or heterogeneity in the resulting accounting practices.

We have examined the following points in the analysis of layout and content: a) alpha-numerical codification of the items; b) indication of the items with an amount equal to zero; c) disclosure of debtors and creditors over short and medium-long terms; d) subdivision of the items; e) regrouping and addition of the items f) adaptation of the items.

a) The alpha-numerical codification of the items

The adopted Balance sheet and Income statement reports are characterized by the presence of alphabetical codes (capital and small letters) and numerical codes (Roman and Arabic numerals). The indication of such codes is not clearly obligatory under law, leaving ample discretion to the preparers of the annual accounts and allowing extremely heterogeneous accounting practices.

An examination of the annual accounts of the sample companies has revealed and confirmed two tendencies; some firms, mostly

(11) See G. CATTURI (1992).

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 13

industrial and commercial companies, have adopted alpha-numerical codes (in some cases inconsistently) while other firms have adopted a series of practices which include all of the possible alternatives. If the compared accounting procedure tends to be uniform in the use of capital letters and Roman numerals, this much cannot be said for the detail of items with Arabic numerals and small letters.

We do not intend to enter into the merits of the question, but it must be pointed out that the use of the codes, without a specific legal obligation, creates an opportunity for problems. Alpha-numerical codes must be used if they offer a significant advantage in terms of a greater clarity in the annual accounts. The “Commissione per la Statuizione dei Principi Contabili - CSPC” (the Commission for the Enactment of Accounting Principles) has argued that the indication of alpha-numerical codes does not furnish any supplementary information and that the use of these codes may disrupt the harmony of the layout of the annual accounts (CSPC Document n° 12 of 1994)(12).

The practices assumed by the 25 sample firms in seven different approaches to the problem of indicating or not indicating alpha-numerical codes is summarised below:

(12) The Commission stated that the use of these codes is not obligatory as the letters and numbers do not constitute parts of the denomination of each item, but are justified for the possibility of being easily recalled in the legislative text. Recourse to alpha-numerical codes is not however expressly prohibited given that it could contribute to, or could lend greater extrinsic clarity to the annual accounts. One of these opportunities, concerning the use of codes, could always be used to indicate the sub-items and the items identified with capital letters and Roman numerals. This method was explained by E. COLUCCI and F. RICCOMAGNO (1997).

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 14

Table 3 - The use of alpha-numerical codes for the items of the annual accounts

ACCOUNTING PRACTICE NUMBER OF FIRMS 1992 1993 1994 1995 1996

a) Strict indication of all codes 3 12 12 12 13

b) Inconsistent indication of all codes - 1 1 1 -

c) Indication of all items preceded by capital letters, Roman numerals and small letters

- 1 1 1 1

d) Strict indication of all items preceded by capital letters and Roman numerals

- 2 2 2 2

e) Indication of items preceded by capital and small letters

- 1 - - -

f) Indicazione of items preceded only by small letters - 1 - - -

g) No codes 22 7 9 9 9

TOTAL 25 25 25 25 25 “C INDEX” 0.78 0.29 0.34 0.35 0.38

It is of interest to note that in the operating budgets for 1992, three companies had already chosen to adopt the norms stipulated in Legislative Decree n° 127 of 1991.

The value of the VAN DER TAS index confirms the limited uniformity in the accounting practices assumed by the sample firms, even if a gradual trend toward the adoption of alpha-numerical codes has begun to emerge with time.

b) The indication of items with amounts equal to zero

Another question in the preparation of the annual accounts is the problem of the real necessity to include all of the items listed in articles 2424 and 2425 of the Civil Code even when they do not represent any amount. Decree Law n° 127 lacks an explicit instruction relative to this problem. Consequently, researching the solution proposed by the Fourth Directive, we find that only the items with a value other than zero in the concluded financial year or in the previous year must be indicated in order to guarantee the clarity and comparability of the presented information. This

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 15

solution is also in line with the proposal of the CSPC in Document n° 12 of 1994(13).

The examined annual accounts clearly demonstrate how companies have established a heterogeneous series of practices which include not only absolute solutions, but also possible intermediate solutions. We may summarise these observations as follows:

Table 4 - The indication of items with values equal to zero ACCOUNTING PRACTICES NUMBER OF FIRMS

1992 1993 1994 1995 1996

a) Indication of all items - 4 4 3 3

b) Indication of all items preceded by capital letters, Roman and Arabic numerals and indication of other items only if assigned a value

- 3 - 1 1

c) Indication of all items preceded by capital letters and Roman numerals and indication of other items only if assigned a value

2 5 9 8 8

d) Indication of all items preceded by capital letters and indication of other items only if assigned a value

- 4 7 8 5

e) Indication only of those items not equal to zero 23 9 5 5 8

TOTAL 25 25 25 25 25 “C INDEX” 0.85 0.20 0.24 0.23 0.23

In considering layout and content we are therefore faced with a series of extremely heterogeneous accounting practices, a problem resulting from the obvious absence of a standard -setting body truly capable of providing uniformity in emerging accounting procedures.

(13) This solution, besides being included in Document n°12 of the CSPC, corresponds to the criteria stated by the Judicial Court of the European Community, which clarifies the contents of Article 4 -5° of the Fourth Directive. The Court orders that “Profit or loss is not indicated as an item of the income statement or balance sheet when it does not constitute any amount, except when

an item exists which corresponds to the preceding year’s operational

expenses...”. According to the Judicial court, the order of the Directive, besides being clear and precise, is also unconditional and not subject to an assimilated option.

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 16

The practices observed during the course of the five operating years examined would appear to reveal a relative lack of harmonious conduct.

c) The disclosure of short and medium-long term credits and

liabilities

Article 2424 of the Civil Code orders that for each liability item included in the fixed assets, the amounts payable within the following year should be indicated; for each liability item included in the current assets, the amounts payable beyond the following financial year should be indicated. The provisions of the Civil Code allow for considerable problems at the practical level, as nothing is stated regarding the method for separate disclosure of short-term liabilities and credits in comparison with those over medium-long terms. The annual accounts of the companies examined illustrates a variety of solutions.

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 17

Table 5 - The disclosure of credits and liabilities over short and medium-long terms

ACCOUNTING PRACTICES NUMBER OF FIRMS 1992 1993 1994 1995 1996

a) Subdivision of each credit and liability item into two ulterior items, indicating respectively the sums payable within the following financial year and those payable beyond the following financial year

12 11 10 10

b) Indication of the total sums for each credit and liability item and a separate column for the items payable within the following financial year or beyond the following financial year

8 7 6 6

c) Indication of the value of the credits and liabilities payable within the following financial year or payable beyond the following financial year by means of a note in lime on the statement of assets and liabilities

2 2 5 5

d) Separate indication of the credits and liabilities payable within the following financial year followed by a repetition of the same items for values payable beyond the following financial year

2 3 1 1

e) No practices observed: accounting statements in which frozen credit includes only sums payable beyond the following financial year and floating assets and liabilities include only sums payable within the following financial year

1 2 3 3

TOTAL 25 25 25 25 “C INDEX” 0.32 0.32 0.24 0.24

The most widespread practice, even if not predominant, provides for the duplication of each credit and liability item, indicating the payable amounts within the following financial year and those payable beyond the following financial year. This procedure creates a multiplication of the number of items which inevitably weighs down the structure of the annual reports.

An appropriate balance needs to be found between the informative necessity to separate the short term and medium-long term liabilities, and the need to compile a clear, non-redundant annual report. Even if the procedure which indicates the overall amount for each credit and liability and shows the overall amounts regarding the financial assets or working capital and liabilities within or beyond the following financial year in a separate column is valid, this solution was chosen by only a restricted number

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 18

companies in the sample. The VAN DER TAS index calculated for the five financial years observed displays a curious tendency toward a heterogeneity of accounting practices.

d) The subdivision of items(14)

Within the discretional space granted by the EC legislation and assimilated with Decree Law n° 127 we will point out the various procedural options and a more analytical presentation of the items provided by the law(15).

In our analysis we focused on some items which are frequent objects of subdivision, such as Revaluation reserves (“Riserve di rivalutazione”), Accrued income or expenses and Deferred income or charges (“Ratei e Risconti attivi” and “Ratei e Risconti passivi”). The emerging practice is growing recourse to the subdivision of items. This practice is often distinguished by extreme variety and heterogeneity of the items concerned. Of the 25 quoted companies in the sample, a surprising number have used this practice: more than 50% up until 1994 e more than 75% in 1995 and 1996. Recourse to the subdivision of items makes annual reports easily distinguished by the specificity of management

(14) The possibilities of subdividing, regrouping, adding and adapting the items of the annual accounts constitute the principal derogations of the obligatory outlines provided by the Community Legislature. These derogations introduce elements of flexibility to the rigid provisions of article 2423 of the Civil Code. The opportunity of conceded de jure power translates the specific reality of the firm, in its dimensional nature and specific management, to the level of accounting procedure in the possibility to assume practices, methods and treatments which are extremely heterogeneous. (15) The ulterior subdivision of items is allowed if these items respect three qualifications: a) the items must be preceded by Arabic numerals; b) the comprehensive amount must not be eliminated; c) the relative amount must not be eliminated. In every case the recourse to subdivision of items must remain consistent with the principle of clarity, and the reports of annual accounts must remain documents of synthesis.

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 19

according to a philosophy which varies greatly within the considered group.

Relative observed practices are summarised in the following table:

Table 6 - The subdivision of items ACCOUNTING PRACTICES NUMBER OF FIRMS

1992 1993 1994 1995 1996

a) Subdivision only of revaluation reserves 2 - 1 4 1

b) Subdivision of revaluation reserves and and of accruals and payables

6 - 2 2 2

c) Subdivision of revaluation reserves and other items - 2 5 5 6

d) Subdivision of accruals and payables 6 5 4 4 3

e) Subdivision of accruals and payables and other items - 6 1 - 2

f) Subdivision of other items - 1 1 5 7

g) No subdivisions 11 11 11 5 4

TOTAL 25 25 25 25 25 “C INDEX” 0.29 0.27 0.24 0.14 0.16

Growing recourse to the subdivision of balance sheet items in addition to those considered here demonstrates the significance of the modifications to the format for the statement of assets and liabilities and the income statement by quoted companies faced with particular needs in representing their economic status.

e) The regrouping and addition of items

Article 2423-ter of the Civil Code provides for the possibility of regrouping items, within limits, if they are coded with Arabic numerals(16).

In examining the annual accounts of the sample companies, it seems that apparently none of them have made recourse to the grouping of items. This is not necessarily to say that none of them have done so. The Civil Code does not require the indication of (16) The grouping of items must respect the following conditions: a) the amount of items considered in the grouping must be insignificant; b) the grouping must favor the clarity of annual accounts, returning in the Note to the accounts the separate indication of the involved items.

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 20

items which are the object of grouping, and it is possible that some companies may have resorted to grouping without explicity stating so. The same article of Civil Code stipulates the addition of these ulterior items when certain information cannot be included in the provided items. The insertion of a new item into the outline of the annual accounts becomes necessary if the relative information is already evident. Even though the obligation must be interpreted in a restrictive sense, the majority of the sample companies have found that the items provided by law do not satisfy their needs. We witness a wide variety of practices in the choice of items to be added, depending upon the choice of benefits from the concessions of the Civil Code.

The addition of an item allows a firm to furnish necessary additional information which may be distinctive to its management. The item Financial credits (“Crediti finanziari”) is the most frequently added and has proven particularly important for financial holdings(17). The following table summarises the practices of the sample group regarding the addition of items:

(17) CONSOB, in a communication of 23 February 1994, approved the addition of the item Financial credits among the financial assets which are not fixed assets.

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 21

Table 7 - The addition of ulterior items to the civil law outline of annual accounts

ACCOUNTING PRACTICES NUMBER OF FIRMS 1992 1993 1994 1995 1996

a) Addition of non-frozen financial credit 3 5 4 4 6

b) Addition of payments into joint accounts 3 2 1 1 4

c) Aggiunta di altre voci - 3 3 4 1

d) Addition of non-frozen financial credit and financial reports with associate companies

- 1 1 1 1

e) Addition of payments into joint accounts and other items - - 1 1 1

f) Addition of non-frozen financial credit and other items - - 2 2 -

g) Addition of non-frozen financial credit and payments into joint accounts

1 - 1 1 -

h) No additions 18 13 12 10 12

TOTAL 25 25 25 25 25 “C INDEX” 0.53 0.31 0.25 0.19 0.29

The trend observed regarding the option to include items in addition to those prescribed by the format in the Civil Code appears to be in line with the observations made in the preceding case, given that the number of firms resorting to this practice increased between 1992 and 1996. However, since this phenomenom involved various balance sheet items, it contributed to an irregular progression of the L. VAN DER TAS INDEX.

f) The adaptation of items

Article 2423-ter of the Civil Code states that items indicated with Arabic numerals must be adapted when their use is required for business of a certain nature. A limited and diminishing number of quoted companies has adapted certain items in preparing their annual accounts as the following synthesis illustrates:

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 22

Table 8 - The adaptation of items in annual accounts ACCOUNTING PRACTICES NUMBER OF FIRMS

1992 1993 1994 1995 1996

a) Bank and postal deposits 2 2 1 -

b) Multiple items 3 1 1 2

c) Other items 1 1 1 -

d) No adaptations 19 21 22 23

TOTAL 25 25 25 25 “C INDEX” 0.58 0.70 0.77 0.85

The final opportunity for intervention foreseen by article 2423-ter of the Civil Code was only scarsely made use of by quoted Italian companies since in growing numbers they had opted to not resort to adaptation of the items in the statement of assets and liabilities and the income statement.

*****

The following table and figure reports the “C” index calculated on our analysis of layout and content .

Table 9 - Analysis of Layout and Content “C” INDEX 1992 1993 1994 1995 1996

a) alpha-numerical coding of balance sheet items

0.78 0.29 0.34 0.35 0.38

b) indication of balance sheet items with a value of zero

0.85 0.20 0.24 0.23 0.23

c) balance sheet disclosure of short and medium-long term credits and liabilities

- 0.32 0.32 024 0.24

d) subdivision of balance sheet items 0.29 0.27 0.24 014 0.16 e) regrouping and addition of balance sheet items

0.53 0.31 0.25 0.19 0.29

f) adaptation of balance sheet items - 0.58 0.70 0.77 0.85

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 23

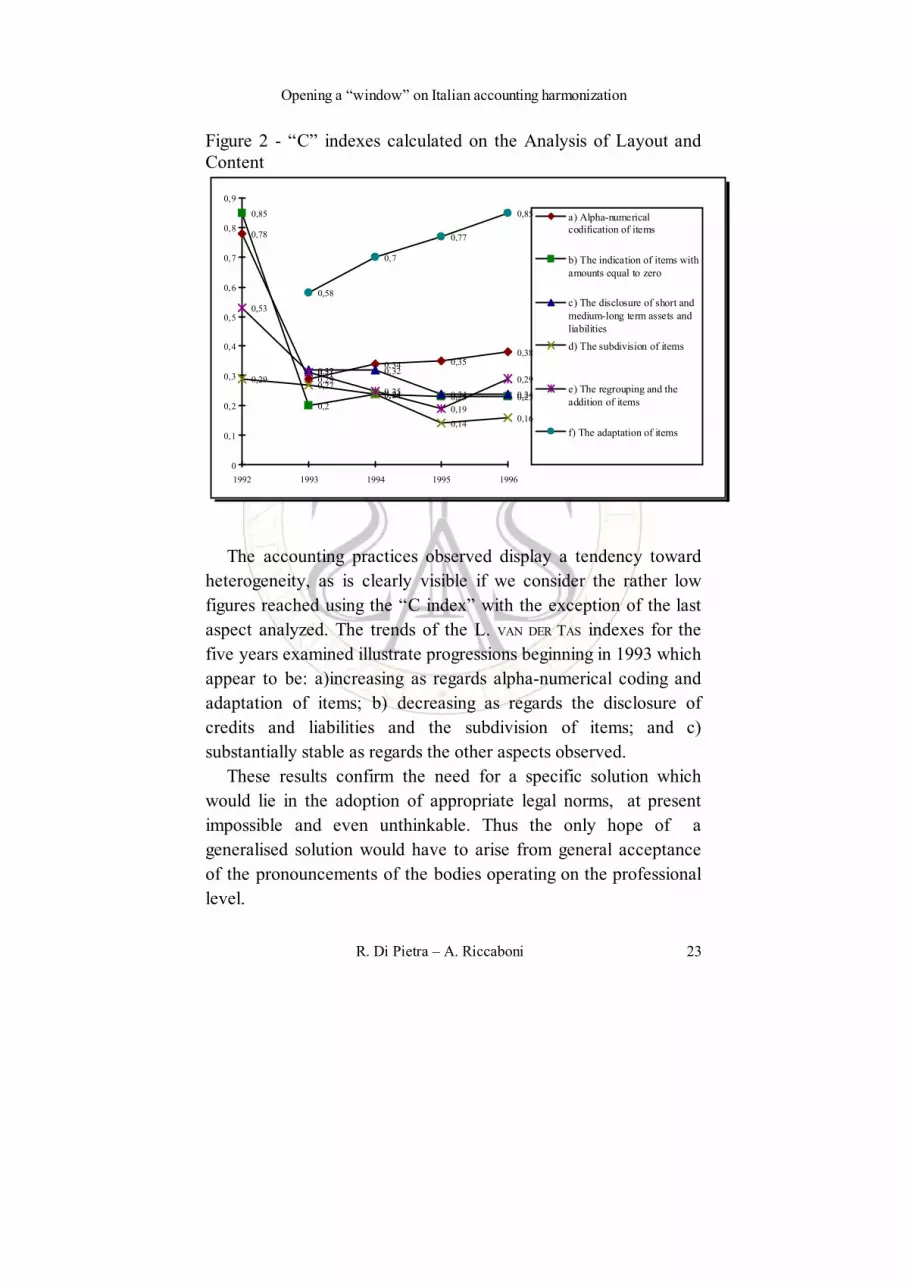

Figure 2 - “C” indexes calculated on the Analysis of Layout and Content

0,78

0,29

0,34 0,350,38

0,85

0,20,24 0,23 0,23

0,32 0,32

0,24 0,24

0,290,27

0,24

0,140,16

0,53

0,31

0,25

0,19

0,29

0,58

0,77

0,85

0,7

0

0,1

0,2

0,3

0,4

0,5

0,6

0,7

0,8

0,9

1992 1993 1994 1995 1996

a) Alpha-numericalcodification of items

b) The indication of items withamounts equal to zero

c) The disclosure of short andmedium-long term assets andliabilities

d) The subdivision of items

e) The regrouping and theaddition of items

f) The adaptation of items

The accounting practices observed display a tendency toward heterogeneity, as is clearly visible if we consider the rather low figures reached using the “C index” with the exception of the last aspect analyzed. The trends of the L. VAN DER TAS indexes for the five years examined illustrate progressions beginning in 1993 which appear to be: a)increasing as regards alpha-numerical coding and adaptation of items; b) decreasing as regards the disclosure of credits and liabilities and the subdivision of items; and c) substantially stable as regards the other aspects observed.

These results confirm the need for a specific solution which would lie in the adoption of appropriate legal norms, at present impossible and even unthinkable. Thus the only hope of a generalised solution would have to arise from general acceptance of the pronouncements of the bodies operating on the professional level.

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 24

The fact that all the considered aspects of layout and content face us with a series of heterogeneous solutions justifies the presence of the ample discretionary space conceded by the legislature while it also highlights the lack of application of the pronouncements issued by the “Commission for the Enactment of Accounting Principles” and where lacking, faithful interpretation of the legal norms.

4. ANALYSIS OF THE VALUATION CRITERIA

We define valuation criteria as all of the aspects regarding the calculation of specific items. The valuation criteria, as seen for layout and content, must be rooted in the principle of clarity.

In examining the adopted practices regarding valuation criteria, we have considered the following aspects: a) recording of financial leasing; b) determination of the quotas of depreciation; c) computation of anticipated depreciation; d) utilization of the “Fiscal appendix”; e) investment valuation.

a) The recording of financial leasing

The Civil Code does not prescribe any accounting process relative to financial leasing. According to the general accounting principle of the pre-eminence of substance over form, a solution which provides for the entering of goods held on lease with the tangible assets emphasizes liabilities toward the leasing company(18). The approach advised by the CSPC stipulates that at the beginning of

(18) The prevalence of substance over form is also affirmed in Document n° 11 of the CSPC. The lack of regulation on leasing in the Fourth Directive has led the national standard setting bodies and numerous international accounting bodies to confront this question. The practices followed in the European Countries can be seen in the comparative study by the FEE in 1991.

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 25

the contract the goods held on lease should be entered as fixed assets, thus demonstrating the debt to the leaser in the liabilities(19).

Examination of the accounting practices of the sample companies reveals practices which are entirely different from those described above. All of the firms recorded their leasing fees in the income statement and reported them in memorandum accounts referring to commitments, “conti d’ordine rappresentanti gli impegni” (total accounts of the residual fees payable)(20). This practice is in contrast with the principle of the prevalence of substance over form, and with Document n° 11 of the CSPC. The absolute uniformity of the practice throughout the sample group may be explained by referring to fiscal law(21). The deductibility of leasing fees conceded by the Italian fiscal authority to the firm utilizing the goods encourages these firms to opt for the observed accounting practice even though it has never been expressly prescribed.

In this case the VAN DER TAS index does indicate the maximum value for all the observed accounting periods (see Table 10).

(19) The initial amount of intangible assets and liabilities must correspond to the current value of the payments scheduled in the leasing contract, which in the course of use of the goods should be systematically subjected to a depreciation process as prescribed in article 2426 of the Civil Code. (20) The adoption of this procedure for entering goods held in leasing can reduce the capacity of the annual accounts to supply a true picture of the considered firm. (21) Article 67 of DPR n° 917 of 22 December 1986 orders that the leasor can depreciate the leased goods in constant quotas of depreciation for the duration of the contract, while the lessee can deduct the entire leasing fee only if these costs are indicated in the income statement.

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 26

Table 10 - The recording of financial leasing ACCOUNTING PRACTICES NUMBER OF FIRMS

1992 1993 1994 1995 1996

a) Inclusion of paid leasing instalments in the income statement, reporting the total residual fees payable in memorandum accounts of commitments

25 25 25 25 25

b) Goods held on lease entered as fixed assets with indication in the liabilities of the debt toward the leaser

- - - - -

TOTAL 25 25 25 25 25 “C INDEX” 1 1 1 1 1

Observation of the five fiscal years studied reveals a conscious, lasting preference for one of the two methods for processing financial leasing already starting in 1992. None of the quoted companies surveyed chose to enter the financial leasing contract among the items in the statement of assets and liabilities. Therefore the value of the C index remained stable at its maximum possible level, indicating maximum uniformity in practices.

b) The determination of depreciation allowances

Article 2426 of the Civil Code prescribes that fixed assets (tangible and intangible) whose utilisation is limited in time must be “systematically depreciated” in every financial year in relation to their “residual possibility of utilisation”(22).

The idea of depreciation introduced with the enactment of the European accounting directives is also in line with the position expressed by the CSPC (Document n° 4 of 1979). The interpretation of the norms in the Civil Code and the position expressed in Italian accounting principles do not exclude the use of diverse depreciation criteria. In other words, the systematic nature of depreciation does not necessarily permit the adoption of criteria at constant quotas. The depreciation allowances must be determined in relation to the levels of development of the

(22) The Civil Code outlines a “perspective” of depreciation in which the quotas must be determined on the basis of possible future use of the fixed assets.

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 27

considered firm and therefore must reflect its specificity and its particular vision for the future.

On the basis of the preceding consideration one appreciates how it would be extremely difficult to reconcile the perspective in the civil norms with that in the fiscal norms, given that the latter hypothesizes standardized deductions. The fiscal provisions in fact prevail, as they bind firms to include all their operating expenses for the financial year which are acknowledged as fiscal deductions in the income statement(23).

An attempt to reconcile the two normative laws was made at least at a formal level through the predisposition of a special Fiscal appendix within the table of the income statement. The use of this appendix would have allowed all firms to record the depreciation transpired by applying the civil norms separately from the requirements of the fiscal norms; or rather would have allowed the presentation of a income statement in which the fiscal alterations are clearly noted(24).

If we refer to the accounting practices assumed by the sample companies, a rather widespread practice emerges in which most of the firms made use of depreciation criteria at a constant quota.

In the annual accounts published in 1994 ten companies expressly declared adoption of quotas of fiscal depreciation,

(23) Article 75-4° of The Collected Laws on the Consolidation of Direct Taxes (“Testo Unico delle Imposte Dirette - TUIR”) stated in a directive that “the expenses and the other negative components are admitted in deduction and in

the criteria of charges in the Income statements relative to the expenses of the

financial year” (DPR 917 of 22 December 1986). The deduction of the quotas of depreciation from the taxable income is admissable only if they are not superior to those resulting from the application of coefficients set by the Ministry of Finance. Article 68 of TUIR also orders that the coefficients for categories of homogeneous goods are fixed on the basis of a “normal period of deterioration and use” in the various production sectors. (24) The Fiscal appendix was incomprenhensibly eliminated by Decree Law n° 416 of 29 June 1994.

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 28

holding them adequate to express the hypothetical economic process of civil law criteria and of accounting principles. Another five companies adopted fiscal criteria, although they failed to declare as much in the Note to the accounts. In conclusion, a growing number of the sample companies adopted criteria of a fiscal nature in the valuation of tangible assets (in 1996 more than 80%). Only in 1993 did one company make use of an accounting procedure for depreciation which demonstrated the incompatibility of economic-technical quotas and fiscal quotas. In 1996 only four companies used depreciation criteria for tangible assets based on the economic-technical valuation. We may summarize the observed practices in the following table:

Table 11 - The determination of depreciation allowances ACCOUNTING PRACTICES NUMBER OF FIRMS

1992 1993 1994 1995 1996

a) Fiscal quotas deemed adequate 9 11 11 9 9

Quotas in correspondence with fiscal quotas 7 6 8 11 12

Economic-technical quotas and indication of excess depreciation in the fiscal appendix

- 16

1 18

- 19

- 20

- 21

b) Economic-technical quotas (not in correspondence with fiscal quotas)

9 7 6 5 4

TOTAL 25 25 25 25 25 “C INDEX” 0.52 0.58 0.62 0.67 0.72

The VAN DER TAS index indicates a tendency toward uniform procedures, confirming the considerable influence of fiscal norms over the accounting practices of Italian quoted companies.

c) The computation of anticipated depreciation

Comprehension of the fiscal norm regarding depreciation is even more vital when considering anticipated depreciation. This is an instrument which allows the firms to apply a tax deferment in relation to the level of structural investments carried out within the

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 29

financial year(25). Article 67-3° of the Collected Laws (TUIR) prescribes that the maximum deductibility criteria for depreciation allowances permitted using fiscal coefficients may be raised up to twice during the financial year in which the goods entered in use for the first time, and in the next two financial years on the condition that the excess is provided for in a special non-distributable reserve.

The calculation of anticipated depreciation therefore foresees the setting aside of earnings in net income among the “other reserves” and the use of the Fiscal appendix for the “reserves formed exclusively in the application of fiscal norms”, while the deferred taxes on anticipated depreciation to be calculated on the basis of the liabilities in the "tax fund"(26).

Of the 25 analyzed companies, only eleven during 1992-1993 and twelve during 1994-1996 made recourse to anticipated depreciation. Half of these were industrial firms. In 1993 the most widespread procedure was that adopted by seven of the eleven firms, which calculated anticipated depreciation using the

(25) The recourse to anticipated depreciation is a State controlled instrument of fiscal politics which can provide investment incentives and can reinforce the self-financing of firms. In other words, the Italian tax system is not neutral, as it influences investment choices through fiscal regulations. Fiscally anticipated depreciation, substituting the value of the true economic depreciation, influences investment decisions. (26) The following bodies have intervened on the accounting processing of anticipated depreciation: ASSIREVI (research document n° 35 of 1993) “accounting treatment of anticipated depreciations in annual accounts”, ASSONIME (circular n° 42 of 1994) “modifications in the regulations of annual income”, “Consiglio Nazionale dei Dottori Commercialisti e dei Ragionieri - CNDC” (National Council of Certified Public Accountants and Accountants), (draft of document n° 14 on the Fiscal appendix of the Income statement) and CONSOB (communication of 12 April 1994).

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 30

accounting process described above - which is, moreover, one of the two procedures acknowledged by CONSOB(27).

We may summarise the observed practices in the following table:

Table 12 - The calculation of anticipated depreciation ACCOUNTING PRACTICES NUMBER OF FIRMS

1992 1993 1994 1995 1996

a) Depreciation set aside in special depreciation reserves disclosed in the debt balance*

8

b) Depreciation set aside in a generic depreciation reserve in the debt balance *

3

c) Method a) CONSOB** 4

d) Method b) CONSOB** 7

f) Depreciation disclosed as adjustment of fixed assets***

12 12 12

TOTAL 11 11 12 12 12 “C INDEX” 0.58 0.52 1 1 1

Fiscal year 1992; ** Fiscal year 1993; *** Fiscal years 1994, 1995 e 1996

The processing of anticipated depreciation clearly reveals how its lack of mention in the norms of the Civil Code, especially after 1994, led companies which had taken advantage of the opportunity offered by the fiscal norms to resort to a special form of processing each year. Once the fiscal appendix was abolished in 1994, the methods advised by CONSOB were entirely replaced with “fiscal” practices imposing the adjustment of fixed assets for the total sum of anticipated depreciation declared during the year.

This lack of continuity is therefore the result of large-scale normative changes which have failed to reduce widespread adhesion to the valuation criteria imposed by the fiscal norms influenced by CONSOB’s recommendations in 1993.

(27) CONSOB predisposed two methods: a) “allocation to item 25 of the income statement”; b) “allocation to item 24 of the income statement”. In the first method the deferred taxes must be determined, while in the second method the amounts of the allocated future fiscal obligations are indicated in the Notes to the accounts.

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 31

d) Utilisation of the fiscal appendix

The case of the fiscal appendix is one of extreme interest which reveals the nature of the Italian system of accounting regulation. Its introduction in 1991 in Legislative Decree n°127 and its almost immediate elimination facilitate explanation of the politics of accounting regulation within the framework of a scenario in which a key role is played by the legislature(28).

The Fourth Directive establishes that possible changes in the fiscal value of some aspects of assets must be shown and justified in the Note to the accounts. In enacting the Directive, the Italian legislature has tried to emphasize this fact by ordering the explicit disclosure of negative income components (correction of value and depreciations) in the income statement. These function exclusively as opportunities to gain otherwise unattainable fiscal advantages. The use of the fiscal appendix in the income statement, or rather the use of items 23, 24 and 25, gave rise to much criticism. The main criticism concerned the loss of neutrality in the annual accounts.

Accounting practice has generally resolved the problem of interpretative uncertainty by avoiding items 24 and 25 of the income statement. The problems underlying the fiscal appendix were expressed in the decision to eliminate it from the income statement, in this way accepting the fiscal obfuscation of annual accounts as a given fact. The elimination of the fiscal appendix by Decree Law n° 416 of 29 June 1994 made the 1993 annual accounts “unique” for those companies which used it. It will be difficult for any company to compare their annual accounts prior to 1993 with for 1993 and logically with those which follow. A study by the FEE in 1991 compared the accounting processing of

(28) See R. DI PIETRA and A. RICCABONI (1998).

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 32

deferred taxation used by companies in other countries of the EEC with very interesting results.

Of the 25 observed companies, only ten used the fiscal appendix in 1993. This does not necessarily mean that these firms adopted economic-technical valuation criteria, but rather that the advantages of the fiscal norms were “masked” and “confused” with the values derived from the application of civil principles. Examination has revealed an only partially correct application of the fiscal appendix, which was primarily used by industrial firms to calculate the previously considered anticipated depreciation.

The value of the VAN DER TAS index calculated for the 1993 annual accounts confirms uniformity of practice among the firms considered as to the utilization of the Fiscal appendix in the sense of its absolute non-utilization. This practice was implicitly confirmed by the abolition of the Fiscal appendix in 1994, making it impossible to calculate the C index for the years following 1993 on this subject.

e) The valuation of investments

Article 2426 establishes that investments entered among financial assets may be appraised according to the cost method or according to the equity method. The first criteria refers to an adjusted value, or rather to the purchase value which does not take the economic consequences for the controlled companies into consideration(29). The second criteria attributes a value to the single investments corresponding to the net equity capital of the investor in proportion to the quota of capital possessed after the appropriate technical

(29) The use of historical cost criterion is inadequate in the case of the valuation of investments in controlled or associated companies, as it does not include the valuation of the variations of net equity of the participated company.

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 33

adjustments have been carried out(30). In order to determine of the purchase price, reference must be made to the criteria indicated in article 2426, which provides that the price may be calculated with one of the following methods: a) weighted average cost, b) First-in, First-Out (FIFO) and c) Last-In, First-Out (LIFO)(31).

The financial assets must, above all, refer to the lower of the values obtained using the cost method or the equity method.

Our analysis shows an almost absolutely uniform procedure in the calculation of investments. One of the most significant innovations introduced with the enactment of the European directives was completely ignored. All of the firms studied adopted the cost method, even if the current fiscal norm is “ambiguous” since the possibility of adopting the criteria for net equity capital presents the risk that the exemption on the possible capital gain might be eliminated by the lacking conversion of Decree n° 554 of 1993 into law(32). Italian firms, faced with the risk of having to bear the fiscal imposition on the capital gains generated by the application of the “equity method”, preferred the cost criteria. It should also be noted that in great part (more than 50%) the financial holding firms appraised investments by means of the typically fiscal Step by step LIFO method(33).

(30) Valuation according to the cost method is obligatory for many shares of investments and for investments in firms which are not controlled or connected, while this method is optional for investments qualified according to the criteria indicated in article 2359. (31) The cost criteria, however calculated, supplies a value which must be adjusted to the hard losses of value of the investments in controlled firms. (32) The fiscal law provisions in force during the period of the enactment of the Fourth Directive induced the legislature to introduce the net equity capital criteria as a right rather than an obligation. (33) In LIFO at annual increments, a stratification of costs proceeds year after year, or rather the balance constitutes “distinct items for operational expenses of formation”.

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 34

Table 13 - The valuation of financial investments ACCOUNTING PRACTICE NUMBER OF FIRMS

1992 1993 1994 1995 1996

a) Investments appraised according to adjusted value criteria

25 25 25 25 24

b) Investments appraised according to the net equity method

- - - - 1

TOTAL 25 25 25 25 25 “C INDEX” 1 1 1 1 0.92

The survey performed on the five fiscal years examined showed that only one quoted company appraised its investments according to the equity method in 1996. This slightly reduced the value of the C index for that year.

* * * * *

Examination of accounting practices regarding valuation criteria in the preparation of annual accounts reveals the following VAN DER TAS C INDEX:

Table 14 - Analysis of valuation criteria “C” INDEX 1992 1993 1994 1995 1996

a) recording of financial leasing 1 1 1 1 1 b) determination of depreciation allowances

0,52 0,58 0,62 0,67 0,72

c) computation of anticipated depreciation

0,58 0,53 1 1 1

d) use of the fiscal appendix - 0,5 - - - e) valuation of investments 1 1 1 1 0,92

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 35

Figure 3 - C indexes calculated on the Valuation criteria

1 1 1 1 1

0,52

0,580,62

0,670,72

0,58

0,52

1 1 11 1 1 1

0,92

0,71

0,77

0,57

0

0,2

0,4

0,6

0,8

1

1,2

1992 1993 1994 1995 1996

a) The recording of financialleasing

b) The determination of thedepreciation allowances

c) The computation ofanticipated depreciation

d) The investments valuationcriterion

Linee 5

f) The adaptation of items

The accounting practices observed are marked by an evident tendency toward uniformity clearly demonstrated in the elevated levels of the VAN DER TAS index (consistently above 50% for all the years surveyed).The limited use of the fiscal appendix reflects another considerably uniform practice, given that the majority of the firms preferred to take the far more convenient path of fiscal obfuscation of the annual accounts. Decree Law n° 416 of 1994, which eliminated the fiscal appendix, simply sanctioned an unofficial but widespread procedure.

It should be pointed out that all the considered valuation criteria present a series of uniformly adopted solutions which in some cases are in open contrast with the prevalent approaches of the CSPC or the interpretations of civil law. In as much as the Commission represents the authoritative opinion of the professional guilds, it has not been generally recognised by an Italian standard setting body, a

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 36

necessary condition for opposing the impact of fiscal norms on accounting practices.

In considering all five of the valuation criteria studied we witness the prevailing influence of the fiscal authority. The solutions adopted in accounting practice prove to be more or less explicitly in accordance with the fiscal norms. The annual accounts for 1993 illustrated illustrated the normative authority of CONSOB prior to the abolition of the fiscal appendix.

5. CONCLUSIONS

This survey has sought to examine the accounting practices observed by the foremost Italian quoted companies in order to identify the trends determining the extent of accounting harmonisation.

Through analysis of the balance sheets relative to the five fiscal

years 1992-1996 we have attempted to appreciate the effects of the

imposition of the European Directives on accounting practices and

balance sheet format. The results obtained clearly demonstrate that

both the imposition of the EU norms and their impact on the

compilation of annual accounts reveal the essence of the Italian

accounting regulation system, in its policies and working

mechanisms. As it is now necessary to recognize the influence of the EU normative law on Italian accounting practices, we have also tried to present a focused and timely analysis illustrating not only the variety of solutions adopted, but also the motivations underlying such solutions. The attainment of European accounting harmonization necessarily depends on the affirmation of an identical procedure for processing annual accounts in all countries. In the case of Italy, verification of the practice of given procedures was made possible by referring to the annual accounts

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 37

prepared during the period 1992-1996, following the initial applications of the norms born of the EU Directive. Our observations, based on a sample of 25 Italian quoted companies representative of the formost companies operating in the industrial, commercial and service sectors or in industrial investments, were focused on the layout, content and valuation criteria of the annual accounts. In order to analyse the selected accounting practices we elected to adopt the instrument for measuring accounting harmonisation proposed by L. VAN DER TAS in the aim of discerning with the utmost simplicity whether the applied accounting practices facilitated or rather impeded the comparability of balance sheet items for particular questions (e.g., “item by item”). The trends displayed by the C indexes thus calculated revealed only scarce standardisation of accounting practices associated with layout and content, probably as a result of the discretional freedom granted by the norms of the Civil Code on these matters, confirming the preeminent authority of the legislature in Italy. Very little has been accomplished by the interpretative interventions of the CSPC, which lacks the necessary general recognistion to make it a true standard-setting body. The absence of such a body hinders the spread of correct and standardised accounting practices whose only hope, for the moment, lies in the progressive development of typical imitative procedures. The affirmation of accounting practices, at least as concerns layout and content, remains uninfluenced by the type of business carried out. In the analysis of valuation criteria, the survey conducted revealed VAN DER TAS indexes indicative of thoroughly standardised accounting practices. The accounting practices displayed a relative tendency toward uniformity, confirmed by high levels of the van der Tas index. The limited use of the fiscal appendix in 1993 and its immediate

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 38

abolition in June 1994 clearly demonstrate how the firms unanimously rejected the adoption of items 24 and 25, resorting to the more convenient option of fiscal obfuscation of the annual accounts. In a context such as Italy’s, which is based on the traditional authority of government, the absence of a generally accepted standard setting body has endowed the legislature with key powers and provided for a particularly strong influence exercized by the tax authorities. The discretional freedom inherent to the norms and their vagueness on many issues (as in the case of financial leasing) have contributed to the adoption of accounting practices in accordance with tax laws. The influence of fiscal norms was limited by the intervention of CONSOB only with regard to the question of recording anticipated depreciation in 1993; in all other cases the interpretative intervention of the CSPC and that of ASSONIME and ASSIREVI have fundamentally had little impact. It should also be noted that some accounting practices which particularly reflect Civil norms are the result of choices made within a group and subsequently adopted by participating member firms. It should also be noted that some quoted companies attempted to adopt suitable accounting practices prior to the imposition of Legislative Decree n° 127 of 1991. In conclusion, the analysis of the accounting practices adopted by the quoted companies during the fiscal period 1992-1996 has made it possible to discern the peculiar characteristics of the Italian accounting regulation scenario. The overall heterogeneity of the accounting practices observed during the analysis of layout and content and the evident uniformity confirmed in the analysis of valuation criteria equally demonstrate how the system of accounting regulation in Italy is affected by the interaction of numerous figures, although the role played by the legislature is clearly preeminent.

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 39

A final analysis reveals the absence of a generally accepted standard-setting body and lends authority to the prevailing role of the tax authorities. In fact, the impact of the Fourth Directive on observed accounting practces was bound to be affected, at least initially, by a series of structural and dynamic factors, particularly of the fiscal variety, as is the case of the Italian system as a whole. Of course, legal and Civil Code norms in particular must be adhered to when annual accounts are prepared in Italy. However, the criteria for evaluation are greatly affected by tax laws. Additional useful guidance for the preparation of annual accounts may be found in CSPC documents and International Accounting Standards. For quoted companies CONSOB plays an important role with reference to account auditing, and this has affected the activity of professional accounting bodies and stimulated intervention on the part of the judicial system. The Italian model of accounting regulation is consequently distinguished by its adherence to a traditional model of regulation involving the participation of a large number of subjects who assume importance in relation to the legislative body(34). This model bears no resemblance to those typically considered in international comparative research, in which the term “political” tends to assume a connotation limited to the regulatory activity performed by a particular rule-making body. The results obtained in this analysis, the structure of the Italian accounting regulation system and the need to cope with increasingly complex operative problems cry out for the creation of an Italian standard setting body with the prestige and authority necessary to guarantee acknowledgement of its regulatory functions and provide unwavering guidance in our economic-business setting. The “Commission for the Establishment of

(34) See G. MAJONE (1991; 1996).

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 40

Accounting Principles” would be the most suitable institution to undertake such vital progress which today is more necessary than ever. Overcoming the present situation appears to be, in fact, the indispensable factor for eliminating the informative distorsions induced by the adoption of fiscal norms and the opportunities granted by the enactment of the European Directive. The government’s decision to reduce the extent of direct state intervention in the economy has led to significant privatisation, deregulation and delegification campaigns. This decision has also begun to display some interesting effects on accounting regulation, even if the outcome of this process is still unpredictable. On one hand, certain acts of deregulation would seem to confirm a trend toward self-regulation with the aim of guaranteeing some form of government recognition for the regulation issued by professional bodies. On the other, the trend toward the establishment of sectorial authorities motivated by clear aims of delegislation might instead mistakenly presume a similar evolution in the field of accounting regulation. In spite of the progression of these trends, our survey of the accounting practices of quoted companies confirms the persistence of the existing model of accounting regulation which will undoubtedly continue to influence future developments and practice. In fact, the politics underlying accounting regulation appear as yet to be rooted in a system which will long influence the regulatory future of this sector, whichever solution is to be gradually adopted, be it the instituiton of a government standard-setting body or, as is more probable, governement recognition of a private standard-setting body.

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 41

BIBLIOGRAPHY

ARCHER G.S.H. , DELVAILLE P., MCLEAY S.J., (1994), Harmonization and the comparability of financial statement items in the annual accounts of

European multilisted companies, Research Papers in Banking and Finance, School of Accounting, Banking and Economics, Bangor.

ARCHER G. S. H. , DELVAILLE P., MCLEAY S.J., (1995), The measurement of harmonization and the comparability of financial statement items: within

country and between-country effects, Journal of Accounting and Business Research, Spring.

CATTURI G., (1989), Teorie contabili e scenari economico-aziendali, CEDAM, Padova.

CATTURI G., (1992), La redazione del bilancio di esercizio, (seconda edizione), CEDAM, Padova.

CLARKE F. L., DEAN G. W., OLIVER K. G., (1997), Corporate collapse, Cambridge University Press, Cambridge.

COLUCCI E., RICCOMAGNO F., (1997), Il bilancio d’esercizio e il bilancio consolidato, Analisi e soluzioni tecniche, CEDAM, Padova.

COMMISSIONE PER STATUIZIONE DEI PRINICIPI CONTABILI, (aa.vv.), Commissione congiunta del Consiglio Nazionale dei Dottori Commercialisti e del Consiglio Nazionale dei Ragionieri, Principi contabili, CEDAM, Padova.

DEZZANI F., PISONI P., PUDDU L., (1991), Il bilancio e la IV Direttiva CEE, Giuffré, Milano

DI PIETRA R., (1997), Accounting regulation models in Italy, France and Spain, in Comparative studies in accounting regulation in Europe , Edited by FLOWER J. and LEFEBVRE C., ACCO, Leuven.

DI PIETRA R. and RICCABONI A., (1998), Regulating accounting within the political system: the key-role of the legislature in Italy, paper presented at the Workshop on Accounting Regulation (University of Siena, 5-7 March).

FEE, (1991), European survey of published accounts, Routledge, London.

FEE, (1994), Investigation of emerging accounting areas, Routledge, London.

FLOWER J. (a cura di), (1994), The regulation of financial reporting in the Nordic countries, Fritzes.

HOPWOOD A., (1994), Some reflections on ‘The harmonization of accounting within the EU’, European Accounting Review, n° 2.

MAJALA R., (1994), Problems of measuring the harmony of financial reports, 17th Annual Congress of the EAA, Venice.

Opening a “window” on Italian accounting harmonization

R. Di Pietra – A. Riccaboni 42

MAJONE G., (1991), Lo Stato regolatore, in Rivista trimestrale di Scienza dell’Amministrazione, n° 3.

MAJONE G., (1996), Regulating Europe, Routledge, London.

MCLEAY S.J., (1994), Comparative methods in accounting: Toward an

encompassing research strategy, School of accounting, banking and economics , Research papers series, June.

NAIR R.D., FRANK W.G., (1973-1979), The harmonization of international accounting standards, The International Journal of Accounting (Education and Research), Fall. 1981.

NOBES C., (1992), International classification of financial reporting, (second edition), Routledge, London and New York.

PROVASOLI A., (1988), La IV e la VII Direttiva CEE nel progetto di attuazione, Rivista dei Dottori Commercialisti, n° 3.

RICCABONI, (1998, forthcoming), Accounting regulation process in Italy, in The politics of accounting regulation in Europe, edited by MCLEAY S., Macmillan.

RICCABONI A., GHIRRI R., (1994), European Financial Reporting - Italy, Routledge, London.

TAY J.S.W., PARKER R.H., (1990), Measuring international harmonization and

standardization, Abacus, n° 1.

TAY J.S.W., PARKER R.H., (1992), Measuring international harmonization and

standardization: a reply, Abacus, n° 1.

VAN DER TAS L., (1988), Measuring harmonization of financial reporting

practice, Accounting and Business Research,.

VAN DER TAS L., (1992a), Evidence of EC financial reporting practice

harmonization, The case of deferred taxation, European Accounting Review, n° 1.

VAN DER TAS L., (1992b), Measuring international harmonization and

standardization: a comment, Abacus, September.

VAN DER TAS L., (1992c), Harmonization of financial reporting: With a special

focus on the European Community, Datawyse, Maastricht.

VAN DER TAS L. (1992d), Measuring international harmonization and

standardization: a comment, Abacus, Vol. 28, n° 2.

Recommended