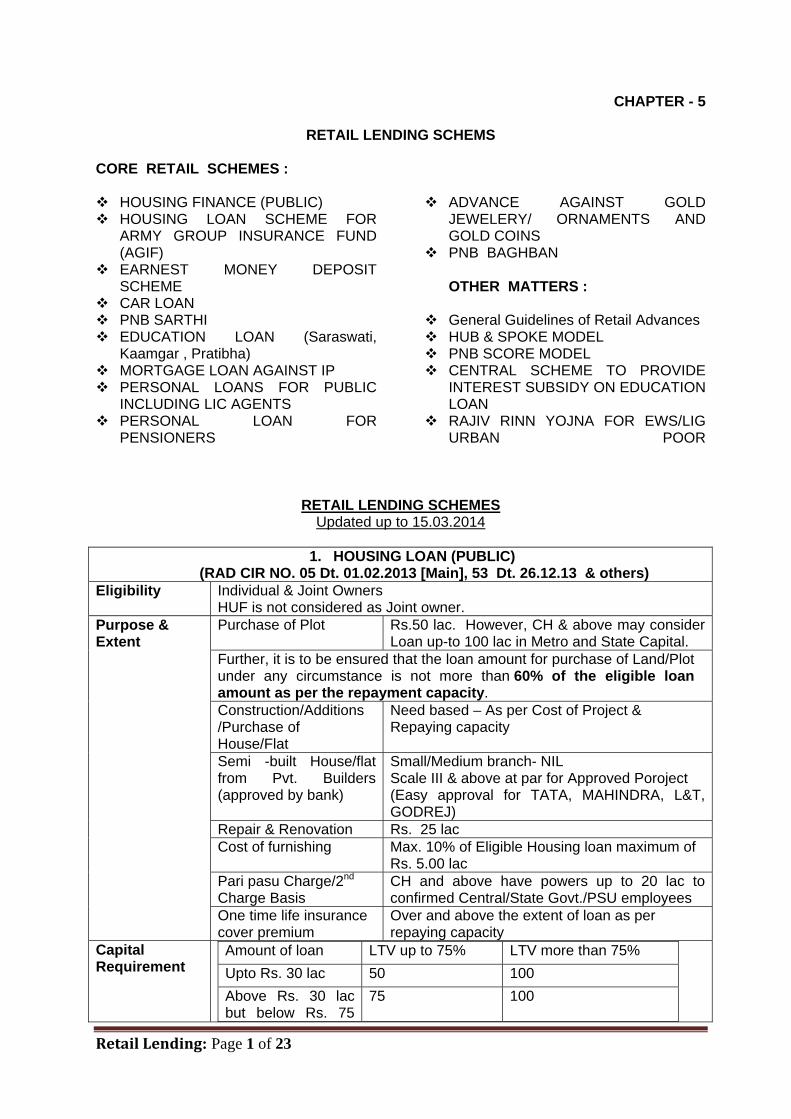

Retail Lending: Page 1 of 23

CHAPTER - 5

RETAIL LENDING SCHEMS

CORE RETAIL SCHEMES :

HOUSING FINANCE (PUBLIC) HOUSING LOAN SCHEME FOR

ARMY GROUP INSURANCE FUND (AGIF)

EARNEST MONEY DEPOSIT SCHEME

CAR LOAN PNB SARTHI EDUCATION LOAN (Saraswati,

Kaamgar , Pratibha) MORTGAGE LOAN AGAINST IP PERSONAL LOANS FOR PUBLIC

INCLUDING LIC AGENTS PERSONAL LOAN FOR

PENSIONERS

ADVANCE AGAINST GOLD JEWELERY/ ORNAMENTS AND GOLD COINS

PNB BAGHBAN OTHER MATTERS :

General Guidelines of Retail Advances HUB & SPOKE MODEL PNB SCORE MODEL CENTRAL SCHEME TO PROVIDE

INTEREST SUBSIDY ON EDUCATION LOAN

RAJIV RINN YOJNA FOR EWS/LIG URBAN POOR

RETAIL LENDING SCHEMES

Updated up to 15.03.2014

1. HOUSING LOAN (PUBLIC) (RAD CIR NO. 05 Dt. 01.02.2013 [Main], 53 Dt. 26.12.13 & others)

Eligibility Individual & Joint Owners HUF is not considered as Joint owner. Purchase of Plot Rs.50 lac. However, CH & above may consider

Loan up-to 100 lac in Metro and State Capital. Further, it is to be ensured that the loan amount for purchase of Land/Plot under any circumstance is not more than 60% of the eligible loan amount as per the repayment capacity. Construction/Additions /Purchase of House/Flat

Need based – As per Cost of Project & Repaying capacity

Semi -built House/flat from Pvt. Builders (approved by bank)

Small/Medium branch- NIL Scale III & above at par for Approved Poroject (Easy approval for TATA, MAHINDRA, L&T, GODREJ)

Repair & Renovation Rs. 25 lac Cost of furnishing Max. 10% of Eligible Housing loan maximum of

Rs. 5.00 lac Pari pasu Charge/2nd Charge Basis

CH and above have powers up to 20 lac to confirmed Central/State Govt./PSU employees

Purpose & Extent

One time life insurance cover premium

Over and above the extent of loan as per repaying capacity

Capital Requirement

Amount of loan LTV up to 75% LTV more than 75% Upto Rs. 30 lac 50 100 Above Rs. 30 lac but below Rs. 75

75 100

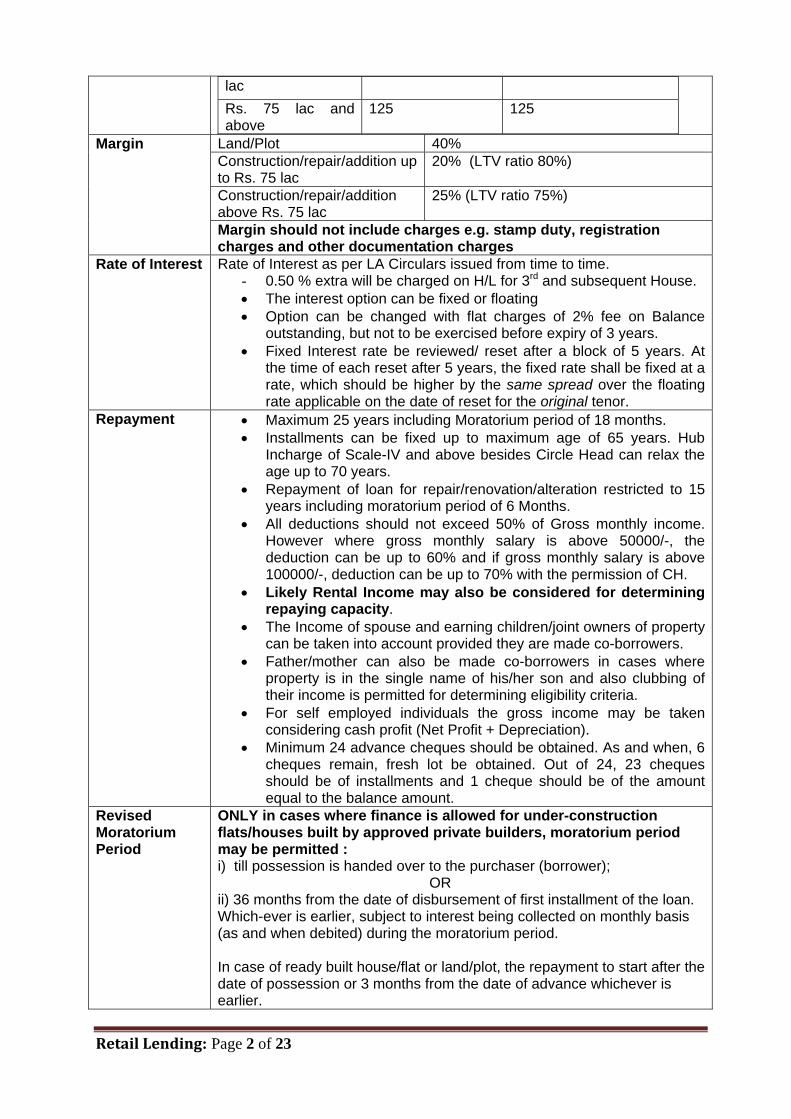

Retail Lending: Page 2 of 23

lac Rs. 75 lac and above

125 125

Land/Plot 40% Construction/repair/addition up to Rs. 75 lac

20% (LTV ratio 80%)

Construction/repair/addition above Rs. 75 lac

25% (LTV ratio 75%)

Margin

Margin should not include charges e.g. stamp duty, registration charges and other documentation charges

Rate of Interest Rate of Interest as per LA Circulars issued from time to time. - 0.50 % extra will be charged on H/L for 3rd and subsequent House. • The interest option can be fixed or floating • Option can be changed with flat charges of 2% fee on Balance

outstanding, but not to be exercised before expiry of 3 years. • Fixed Interest rate be reviewed/ reset after a block of 5 years. At

the time of each reset after 5 years, the fixed rate shall be fixed at a rate, which should be higher by the same spread over the floating rate applicable on the date of reset for the original tenor.

Repayment • Maximum 25 years including Moratorium period of 18 months. • Installments can be fixed up to maximum age of 65 years. Hub

Incharge of Scale-IV and above besides Circle Head can relax the age up to 70 years.

• Repayment of loan for repair/renovation/alteration restricted to 15 years including moratorium period of 6 Months.

• All deductions should not exceed 50% of Gross monthly income. However where gross monthly salary is above 50000/-, the deduction can be up to 60% and if gross monthly salary is above 100000/-, deduction can be up to 70% with the permission of CH.

• Likely Rental Income may also be considered for determining repaying capacity.

• The Income of spouse and earning children/joint owners of property can be taken into account provided they are made co-borrowers.

• Father/mother can also be made co-borrowers in cases where property is in the single name of his/her son and also clubbing of their income is permitted for determining eligibility criteria.

• For self employed individuals the gross income may be taken considering cash profit (Net Profit + Depreciation).

• Minimum 24 advance cheques should be obtained. As and when, 6 cheques remain, fresh lot be obtained. Out of 24, 23 cheques should be of installments and 1 cheque should be of the amount equal to the balance amount.

Revised Moratorium Period

ONLY in cases where finance is allowed for under-construction flats/houses built by approved private builders, moratorium period may be permitted : i) till possession is handed over to the purchaser (borrower); OR ii) 36 months from the date of disbursement of first installment of the loan. Which-ever is earlier, subject to interest being collected on monthly basis (as and when debited) during the moratorium period. In case of ready built house/flat or land/plot, the repayment to start after the date of possession or 3 months from the date of advance whichever is earlier.

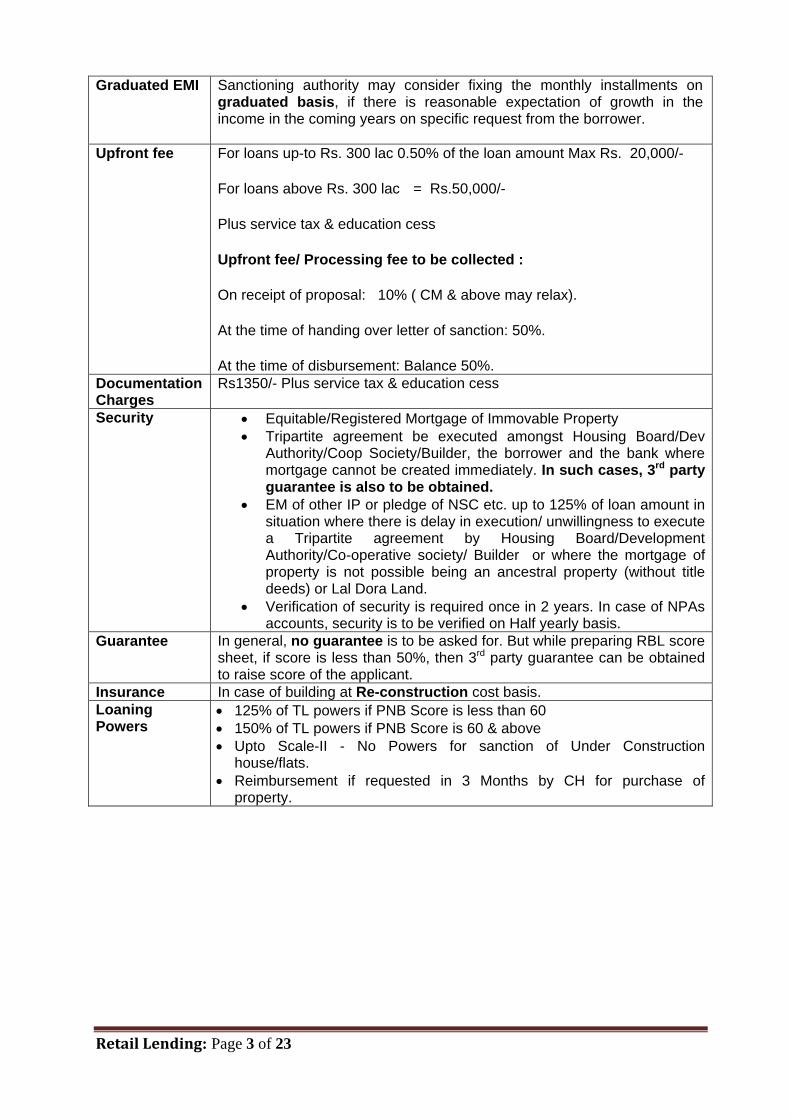

Retail Lending: Page 3 of 23

Graduated EMI Sanctioning authority may consider fixing the monthly installments on graduated basis, if there is reasonable expectation of growth in the income in the coming years on specific request from the borrower.

Upfront fee For loans up-to Rs. 300 lac 0.50% of the loan amount Max Rs. 20,000/-

For loans above Rs. 300 lac = Rs.50,000/-

Plus service tax & education cess

Upfront fee/ Processing fee to be collected :

On receipt of proposal: 10% ( CM & above may relax).

At the time of handing over letter of sanction: 50%.

At the time of disbursement: Balance 50%. Documentation Charges

Rs1350/- Plus service tax & education cess

Security • Equitable/Registered Mortgage of Immovable Property • Tripartite agreement be executed amongst Housing Board/Dev

Authority/Coop Society/Builder, the borrower and the bank where mortgage cannot be created immediately. In such cases, 3rd party guarantee is also to be obtained.

• EM of other IP or pledge of NSC etc. up to 125% of loan amount in situation where there is delay in execution/ unwillingness to execute a Tripartite agreement by Housing Board/Development Authority/Co-operative society/ Builder or where the mortgage of property is not possible being an ancestral property (without title deeds) or Lal Dora Land.

• Verification of security is required once in 2 years. In case of NPAs accounts, security is to be verified on Half yearly basis.

Guarantee In general, no guarantee is to be asked for. But while preparing RBL score sheet, if score is less than 50%, then 3rd party guarantee can be obtained to raise score of the applicant.

Insurance In case of building at Re-construction cost basis. Loaning Powers

• 125% of TL powers if PNB Score is less than 60 • 150% of TL powers if PNB Score is 60 & above • Upto Scale-II - No Powers for sanction of Under Construction

house/flats. • Reimbursement if requested in 3 Months by CH for purchase of

property.

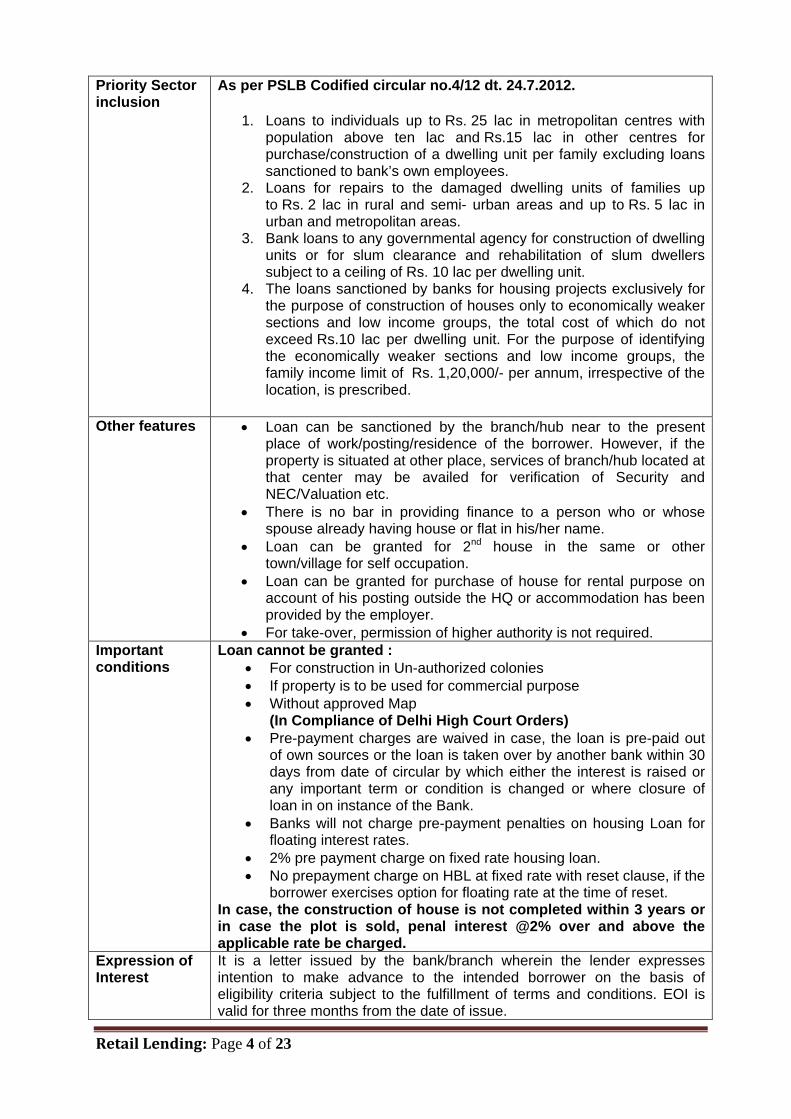

Retail Lending: Page 4 of 23

Priority Sector inclusion

As per PSLB Codified circular no.4/12 dt. 24.7.2012.

1. Loans to individuals up to Rs. 25 lac in metropolitan centres with population above ten lac and Rs.15 lac in other centres for purchase/construction of a dwelling unit per family excluding loans sanctioned to bank’s own employees.

2. Loans for repairs to the damaged dwelling units of families up to Rs. 2 lac in rural and semi- urban areas and up to Rs. 5 lac in urban and metropolitan areas.

3. Bank loans to any governmental agency for construction of dwelling units or for slum clearance and rehabilitation of slum dwellers subject to a ceiling of Rs. 10 lac per dwelling unit.

4. The loans sanctioned by banks for housing projects exclusively for the purpose of construction of houses only to economically weaker sections and low income groups, the total cost of which do not exceed Rs.10 lac per dwelling unit. For the purpose of identifying the economically weaker sections and low income groups, the family income limit of Rs. 1,20,000/- per annum, irrespective of the location, is prescribed.

Other features • Loan can be sanctioned by the branch/hub near to the present place of work/posting/residence of the borrower. However, if the property is situated at other place, services of branch/hub located at that center may be availed for verification of Security and NEC/Valuation etc.

• There is no bar in providing finance to a person who or whose spouse already having house or flat in his/her name.

• Loan can be granted for 2nd house in the same or other town/village for self occupation.

• Loan can be granted for purchase of house for rental purpose on account of his posting outside the HQ or accommodation has been provided by the employer.

• For take-over, permission of higher authority is not required. Important conditions

Loan cannot be granted : • For construction in Un-authorized colonies • If property is to be used for commercial purpose • Without approved Map

(In Compliance of Delhi High Court Orders) • Pre-payment charges are waived in case, the loan is pre-paid out

of own sources or the loan is taken over by another bank within 30 days from date of circular by which either the interest is raised or any important term or condition is changed or where closure of loan in on instance of the Bank.

• Banks will not charge pre-payment penalties on housing Loan for floating interest rates.

• 2% pre payment charge on fixed rate housing loan. • No prepayment charge on HBL at fixed rate with reset clause, if the

borrower exercises option for floating rate at the time of reset. In case, the construction of house is not completed within 3 years or in case the plot is sold, penal interest @2% over and above the applicable rate be charged.

Expression of Interest

It is a letter issued by the bank/branch wherein the lender expresses intention to make advance to the intended borrower on the basis of eligibility criteria subject to the fulfillment of terms and conditions. EOI is valid for three months from the date of issue.

Retail Lending: Page 5 of 23

Issuance of Provisional Interest Certificates

To assist the branches in printing system generated provisional interest certificates, functionality has been developed in MIS Server at ‘PNBRPT 3/56a’ enabling printing of same, which is based on following logic: i) The interest charged in the account from the month of April onward to

the month of last application of interest on actual basis. ii) The interest for the remaining period of the financial year ending next

March on notional basis. iii) The calculation of notional interest is based on monthly product. iv) The notional interest is calculated on the outstanding balance on the

first day of the month after adding interest notionally calculated for the previous month and deducting the installment amount (flow amount as given in the ‘E’ details)

v) The sum of interest for 12 months (actual+notional) is printed in the certificate generated through this functionality.

vi) There is no credit other than the installment (flow amount) and debit other than the interest amount.

Takeover Investigation of title

In cases of take-over of housing loans, where the original title deed remains in the possession of previous financer and is released only after disbursement of loan by our branch, Law Division has suggested the following steps :-

Certified copy of the title deeds be obtained from the concerned

office of Sub-Registrar/Registrar of Assurance by the counsel of the Bank and he should give the search report as per the above-said Circular of Law Division. The other documents like previous electricity bill, water bill, house tax receipt etc. be also examined to satisfy about ownership of proposed borrower.

The counsel and Branch Manager should visit the site personally and identify the property in question including sanction of the map.

The Branch Office should draw credit information report from CIBIL data base to have information about availment from other banks and repayment of loan status.

The party should request his/her banker to allow examination of original title deed. The other bank is obligated to allow examination of original on the request of borrower. Under Section 60B of Transfer of Property Act, 1882, Mortgagor is entitled at all reasonable times, at his/her request and his/her own cost and on payment of the mortgagee’s costs and expenses in this behalf, to inspect and make copies or abstracts of, or extracts from, documents of title relating to the mortgaged property which are in custody or power of the mortgagee. In case of reluctance on the part of existing financer, the above provision of law can be quoted.

Group Total Suraksha – TATA-AIG Scheme for Housing Loan

The scheme provides life cover for Housing Loan borrowers on voluntary basis after payment of One time premium which is borne by the borrower and can be financed by bank with 20% margin. The other features of the scheme are as under:

• The age must be between 18-65 years. The maximum coverage is 70 years.

• Term of coverage is 1-25 years. • Sum assured will be Rs.. 1000 minimum and maximum is

equivalent to loan amount as per bank norms. • Full payment of Housing loan before expiry of original duration shall

not terminate the insurance coverage. • The amount of premium with service tax be credited directly in

account no. 0554002100026089 of TATA-AIG Life Insurance Co.

Retail Lending: Page 6 of 23

Ltd. with narration of HL account no. and name. • Maximum two borrowers are eligible for joint policy. They should be

immediate next kin or spouse. • Non-finance cases can also be covered. • Administration charges @5% on premium plus service tax be

credited to bank’s revenue. Example A loan of Rs. 100000 is sanctioned to a borrower aged 40 years. The loan is repayable in 15 years. The premium will be Rs. 1339 + ST Rs. 137.92 + Administration charges Rs. 66.95 + ST Rs. 6.90 = Rs. 1550.77. The complete procedure and guidelines are contained in RAD Cir. No. 2/11 dt. 01.01.2011. It has been decided to extend the validity of tie up arrangement with TATA AIG under GROUP TOTAL SURAKSHA for further six months with revised Non Medical Limits (NML) under the offering and revised NML are as under:

Age (Yrs) Revised Limit 18-40 80 lac 41-45 60 lac 46-50 40 lac 51-60 25 lac 61-70 10 lac

(RAD Cir. No. 18/11 dt. 27.04.11 & 37/11 dt. 29.09.2011)

OD facility to existing HL borrowers

There is competitive scheme in our bank to provide Overdraft to HL borrowers. The features of the scheme are as under:

• OD limit from Rs. 50000/- to Rs.25 lacs or up to 75% of realizable value of property. (Over Rs. 5 lac maximum 25% of HL sanctioned)

• OD limit is meant for personal use. • The limit is secured by way of EM of IP. • Interest is serviced on regular basis. • OD limit is reviewed on annual basis. • The sanction is outside the purview of RAB model. • There should not be any serious IR irregularity. • The processing fee is NIL. The documentation charges are

Rs.450/-.

Scheme Code: ODPRH Interest Code: For < 75lacs = ODPUB & > 75 lacs = ODPAB OD for personal use should not be sanctioned to those who have availed loan for purchase of plot, construction on which is yet to be completed. (RAD Cir. No. 06/14 dt. 04.02.2014)

PNB Flexible Housing Loan Scheme

This is an attractive variant of Housing Loan Scheme offered by the PNB for its customers. Under this scheme, OD facility is made available to the HL borrower. He can deposit his savings and withdraw the same as per his requirement. The features of the scheme are as under:

Retail Lending: Page 7 of 23

Eligibility • Age of the applicant must be less than 50. • Existing HL borrowers can also apply provided their

loan account is regular and no IR irregularity persists.

Purpose • All purposes as per original scheme except Purchase of Land / Plot.

Extent Term Loan 80% Overdraft 20% • After lapse of 3 years, enhancement in OD will be

allowed equal to reduction in Term Loan and thereafter on yearly basis.

• After lapse of 5 years, 20% increase in original limit is allowed in the shape of TL/OD for personal needs.

• Market Value of Property should be sufficient to cover the margin of 25%

• After attaining age of 55 years, OD facility will be reduced on monthly basis so that whole limit and T/L are adjusted by the end of 65 years.

• Maximum OD limit should not exceed 50% of Total limit.

• HL can be sanctioned by the branch/hub situated near the workplace/posting/residence.

• Security verification can be done by nearby branch. • Rate of Interest as given above in the table in Housing

Loan scheme (general) For Overdraft portion, R/I is same as for HL. (RBD Cir 33/18.10.04, 10/13.02.07 & LA 75/22.06.13)

2. HOUSING LOAN SCHEME FOR PUBLIC

For extending additional loans to the members of Army Group Insurance Fund (AGIF) on pari passu basis – Tripartite Agreement (RAD Cir. 08/2012 dated 30/03/2012

Purpose & Extent

To advance additional housing loans to AGIF members on pari passu basis, CH & above are empowered to consider loan on pari passu or second charge basis for loan amount of maximum upto Rs. 20 lac in respect of confirmed employees of Central/State Govt./PSUs, who have raised funds for construction/acquisition of accommodation from other sources and need supplementary finance.

Eligibility AGIF members (individual/ jointly), who have/are availed/availing HBA from AGIF & desire additional loan to cover the cost of dwelling unit.

Income of spouse, earning children/ father/mother/ likely rental income, etc. can be taken into consideration while assessing the repaying capacity.

Retail Asset Branch (RAB) In charge in the rank of Scale-IV & above/Circle Head may relax the repayment period upto the age of 70 years or 25 years of tenure, whichever is earlier.

Rate of Interest As decided by the Bank from time to time.

(Presently, 0.50% concession in Rate of Interest, 100% waiver of upfront fee & documentation charges and 5% concession in margin subject to minimum of 20% or as decided by the Bank from time to time are being offered to Defence Personnel)

Retail Lending: Page 8 of 23

Repayment Loan to be repaid by way of EMI payable every month at the end of each calendar month with moratorium period of 18 months. Pending the commencement of EMI, the borrower shall pay interest every month on the disbursed loan at the applicable rate.

Pay regular EMIs every month as indicated by the Bank throughout the tenure of loan.

Borrower may chose to pay higher EMI during the service period and a lesser EMI post-retirement to the Bank or the borrower may chose to step up the EMI at periodic interval.

Security Bank to hold a pari passu charge with AGIF on the property. During service, AGIF insurance and benefits (after deducting dues to

AGIF) will stand security to loan advanced by the Bank. However, the additional security offered by way of insurance coverage shall be in addition to the primary security.

Others Application of the AGIF Member may be submitted at any branch/RAB nearest to the place of service/ place of domicile.

All other terms & conditions of Bank’s Housing Loan Scheme for Public shall apply mutatis mutandi in respect of customized Scheme for AGIF members.

Further, the Tripartite Agreement as per Annexure-I be got executed for financing additional housing loans to AGIF members on pari passu basis.

All concerned are advised to note the above guidelines for compliance.

3. RAJIV RINN YOJNA FOR EWS/LIG URBAN POOR (EX : ISHUP) (RAD Cir No. 03 Dt. 24.01.2014) in place of w.e.f. 01.10.2013.

Purpose The scheme provides home loans with GOI interest subsidy to EWS/ LIG persons of Urban areas to buy or construct houses, who does not own a house in his/her, spouse, dependent children. Addition in < 40 Sq Mtr area is also allowed. (1 room/kitchen/toilet/BR) Renovation purpose is not covered. Scheme is operative from 01.10.2013 to 31.03.2017 (upto 12th plan)

Eligibility

Individual as well as Group Housing borrowers of Economically Weaker Section (EWS) and Low Income Groups (LIG) as under: Category Average household Annual Income EWS Upto Rs.1,00,000/-

LIG Rs.1,00,001/- to Rs.2,00,000/- State Govt. / Local Urban Bodies will nominate the officials/agency/ authority to certify EWS/LIG category alongwith self declaration of prospective borrower.

Quantum of loan

EWS Individual : Upto Rs. 5 lac* for house of at least 21 square meters. LIG Individual : Upto Rs. 8 lac* for house of at least 28 square meter. *Loans above 5 lacs if needed, would be at unsubsidized rates. (Both)

Margin 10% = LTV not exceed 90%. Stamp/Registration charges will not be part of margin. Plot cost may be part of margin.

Upfront fee/ Doc. charges

Nil

Rate of Interest As per Housing loan. Presently : Floating = Base Rate i.e. 10.25% Fixed = 0.50% above floating rates

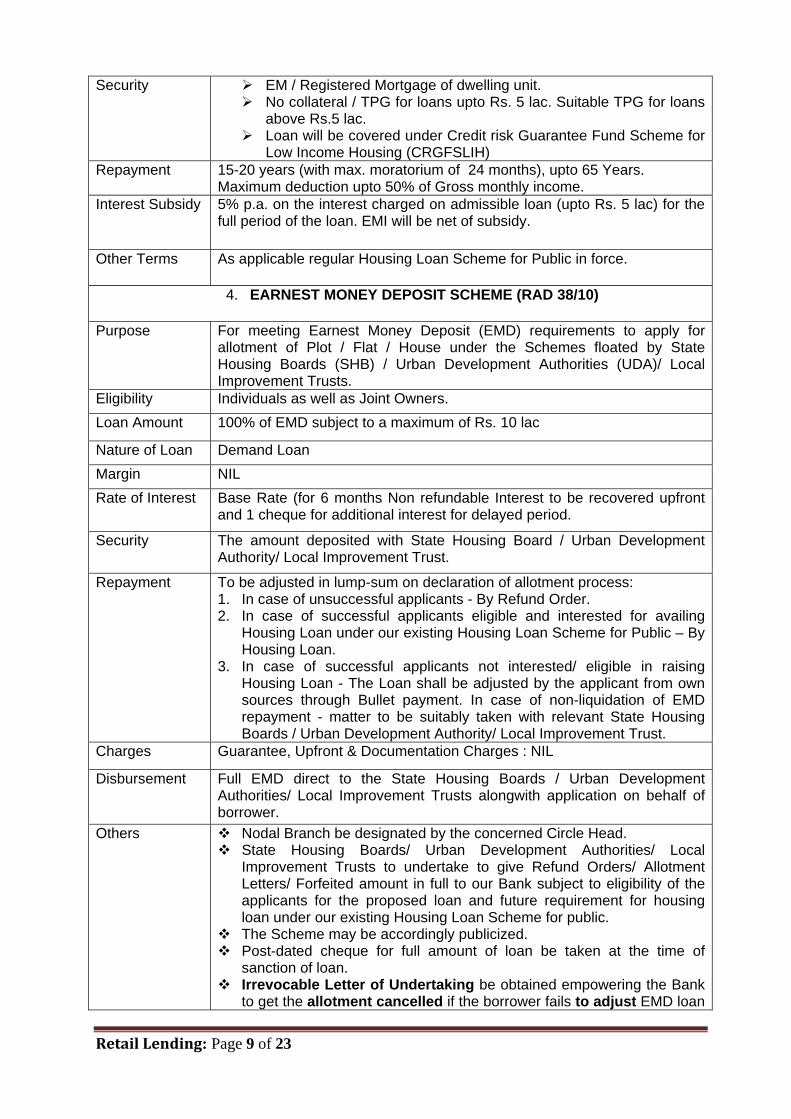

Retail Lending: Page 9 of 23

Security EM / Registered Mortgage of dwelling unit. No collateral / TPG for loans upto Rs. 5 lac. Suitable TPG for loans

above Rs.5 lac. Loan will be covered under Credit risk Guarantee Fund Scheme for

Low Income Housing (CRGFSLIH) Repayment 15-20 years (with max. moratorium of 24 months), upto 65 Years.

Maximum deduction upto 50% of Gross monthly income. Interest Subsidy 5% p.a. on the interest charged on admissible loan (upto Rs. 5 lac) for the

full period of the loan. EMI will be net of subsidy.

Other Terms As applicable regular Housing Loan Scheme for Public in force.

4. EARNEST MONEY DEPOSIT SCHEME (RAD 38/10)

Purpose For meeting Earnest Money Deposit (EMD) requirements to apply for allotment of Plot / Flat / House under the Schemes floated by State Housing Boards (SHB) / Urban Development Authorities (UDA)/ Local Improvement Trusts.

Eligibility Individuals as well as Joint Owners. Loan Amount 100% of EMD subject to a maximum of Rs. 10 lac

Nature of Loan Demand Loan Margin NIL Rate of Interest Base Rate (for 6 months Non refundable Interest to be recovered upfront

and 1 cheque for additional interest for delayed period.

Security The amount deposited with State Housing Board / Urban Development Authority/ Local Improvement Trust.

Repayment To be adjusted in lump-sum on declaration of allotment process: 1. In case of unsuccessful applicants - By Refund Order. 2. In case of successful applicants eligible and interested for availing

Housing Loan under our existing Housing Loan Scheme for Public – By Housing Loan.

3. In case of successful applicants not interested/ eligible in raising Housing Loan - The Loan shall be adjusted by the applicant from own sources through Bullet payment. In case of non-liquidation of EMD repayment - matter to be suitably taken with relevant State Housing Boards / Urban Development Authority/ Local Improvement Trust.

Charges Guarantee, Upfront & Documentation Charges : NIL

Disbursement Full EMD direct to the State Housing Boards / Urban Development Authorities/ Local Improvement Trusts alongwith application on behalf of borrower.

Others Nodal Branch be designated by the concerned Circle Head. State Housing Boards/ Urban Development Authorities/ Local

Improvement Trusts to undertake to give Refund Orders/ Allotment Letters/ Forfeited amount in full to our Bank subject to eligibility of the applicants for the proposed loan and future requirement for housing loan under our existing Housing Loan Scheme for public.

The Scheme may be accordingly publicized. Post-dated cheque for full amount of loan be taken at the time of

sanction of loan. Irrevocable Letter of Undertaking be obtained empowering the Bank

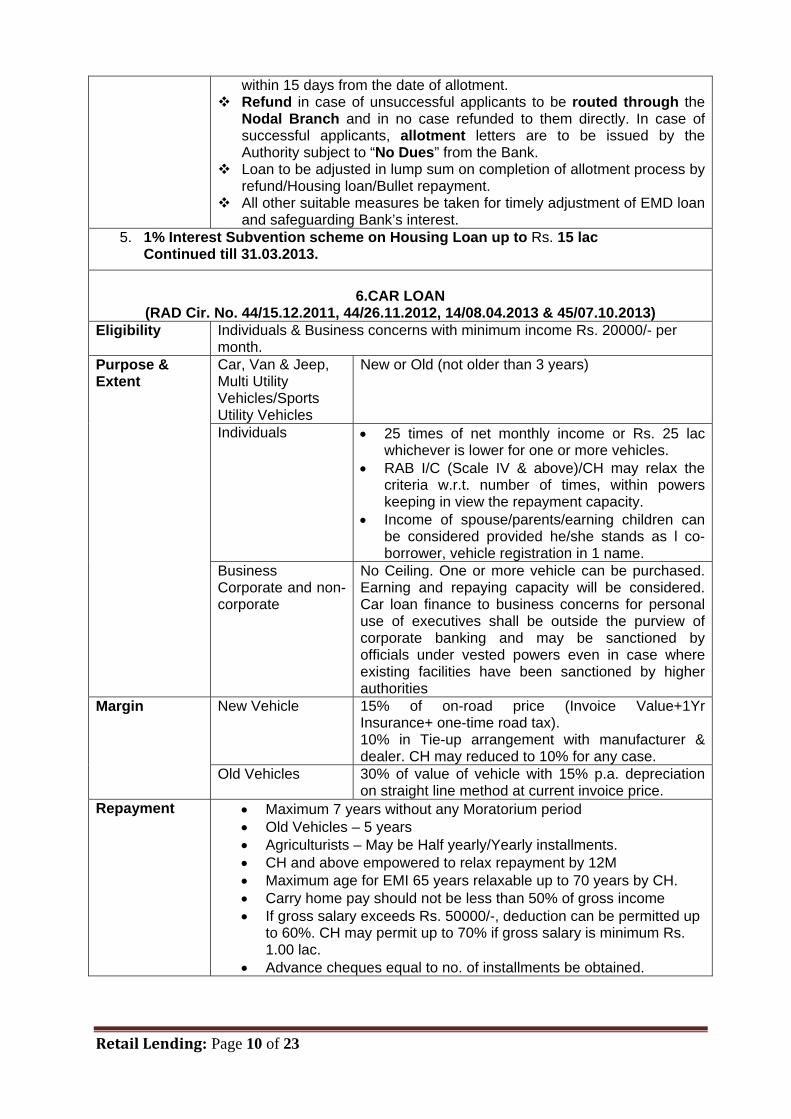

to get the allotment cancelled if the borrower fails to adjust EMD loan

Retail Lending: Page 10 of 23

within 15 days from the date of allotment. Refund in case of unsuccessful applicants to be routed through the

Nodal Branch and in no case refunded to them directly. In case of successful applicants, allotment letters are to be issued by the Authority subject to “No Dues” from the Bank.

Loan to be adjusted in lump sum on completion of allotment process by refund/Housing loan/Bullet repayment.

All other suitable measures be taken for timely adjustment of EMD loan and safeguarding Bank’s interest.

5. 1% Interest Subvention scheme on Housing Loan up to Rs. 15 lac Continued till 31.03.2013.

6.CAR LOAN

(RAD Cir. No. 44/15.12.2011, 44/26.11.2012, 14/08.04.2013 & 45/07.10.2013) Eligibility Individuals & Business concerns with minimum income Rs. 20000/- per

month. Car, Van & Jeep, Multi Utility Vehicles/Sports Utility Vehicles

New or Old (not older than 3 years)

Individuals • 25 times of net monthly income or Rs. 25 lac whichever is lower for one or more vehicles.

• RAB I/C (Scale IV & above)/CH may relax the criteria w.r.t. number of times, within powers keeping in view the repayment capacity.

• Income of spouse/parents/earning children can be considered provided he/she stands as l co-borrower, vehicle registration in 1 name.

Purpose & Extent

Business Corporate and non-corporate

No Ceiling. One or more vehicle can be purchased. Earning and repaying capacity will be considered. Car loan finance to business concerns for personal use of executives shall be outside the purview of corporate banking and may be sanctioned by officials under vested powers even in case where existing facilities have been sanctioned by higher authorities

New Vehicle 15% of on-road price (Invoice Value+1Yr Insurance+ one-time road tax). 10% in Tie-up arrangement with manufacturer & dealer. CH may reduced to 10% for any case.

Margin

Old Vehicles 30% of value of vehicle with 15% p.a. depreciation on straight line method at current invoice price.

Repayment • Maximum 7 years without any Moratorium period • Old Vehicles – 5 years • Agriculturists – May be Half yearly/Yearly installments. • CH and above empowered to relax repayment by 12M • Maximum age for EMI 65 years relaxable up to 70 years by CH. • Carry home pay should not be less than 50% of gross income • If gross salary exceeds Rs. 50000/-, deduction can be permitted up

to 60%. CH may permit up to 70% if gross salary is minimum Rs. 1.00 lac.

• Advance cheques equal to no. of installments be obtained.

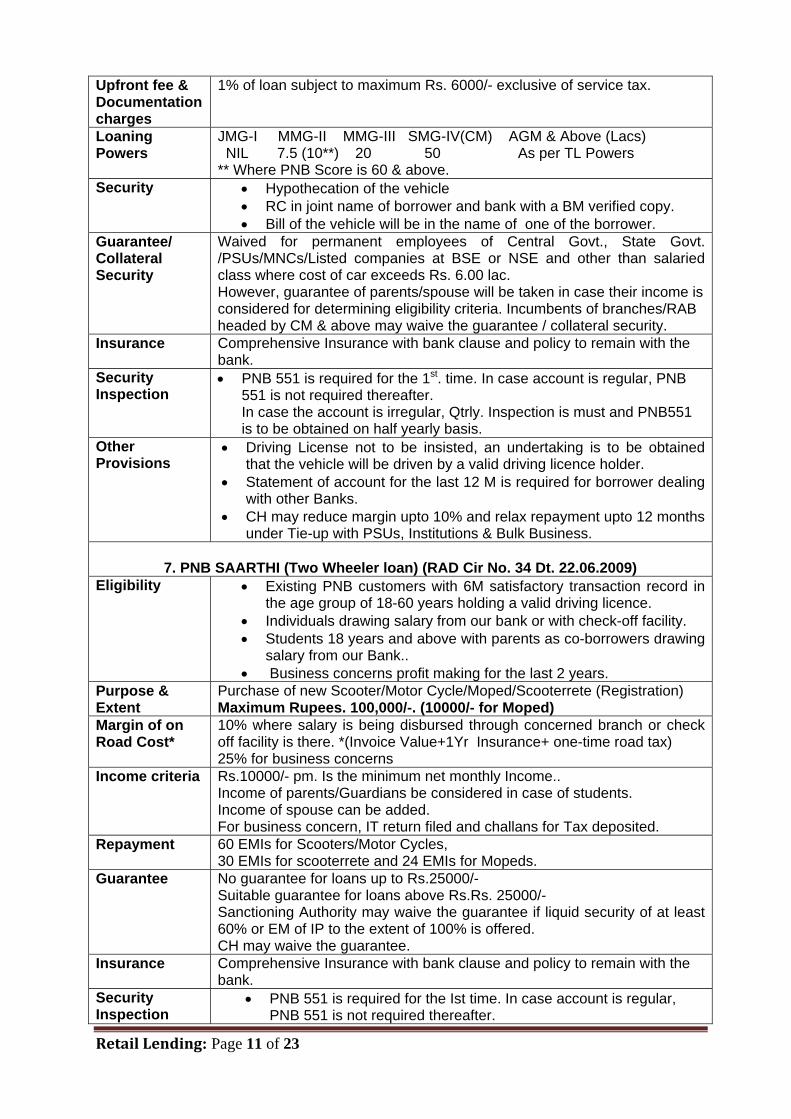

Retail Lending: Page 11 of 23

Upfront fee & Documentation charges

1% of loan subject to maximum Rs. 6000/- exclusive of service tax.

Loaning Powers

JMG-I MMG-II MMG-III SMG-IV(CM) AGM & Above (Lacs) NIL 7.5 (10**) 20 50 As per TL Powers ** Where PNB Score is 60 & above.

Security • Hypothecation of the vehicle • RC in joint name of borrower and bank with a BM verified copy. • Bill of the vehicle will be in the name of one of the borrower.

Guarantee/ Collateral Security

Waived for permanent employees of Central Govt., State Govt. /PSUs/MNCs/Listed companies at BSE or NSE and other than salaried class where cost of car exceeds Rs. 6.00 lac. However, guarantee of parents/spouse will be taken in case their income is considered for determining eligibility criteria. Incumbents of branches/RAB headed by CM & above may waive the guarantee / collateral security.

Insurance Comprehensive Insurance with bank clause and policy to remain with the bank.

Security Inspection

• PNB 551 is required for the 1st. time. In case account is regular, PNB 551 is not required thereafter. In case the account is irregular, Qtrly. Inspection is must and PNB551 is to be obtained on half yearly basis.

Other Provisions

• Driving License not to be insisted, an undertaking is to be obtained that the vehicle will be driven by a valid driving licence holder.

• Statement of account for the last 12 M is required for borrower dealing with other Banks.

• CH may reduce margin upto 10% and relax repayment upto 12 months under Tie-up with PSUs, Institutions & Bulk Business.

7. PNB SAARTHI (Two Wheeler loan) (RAD Cir No. 34 Dt. 22.06.2009)

Eligibility • Existing PNB customers with 6M satisfactory transaction record in the age group of 18-60 years holding a valid driving licence.

• Individuals drawing salary from our bank or with check-off facility. • Students 18 years and above with parents as co-borrowers drawing

salary from our Bank.. • Business concerns profit making for the last 2 years.

Purpose & Extent

Purchase of new Scooter/Motor Cycle/Moped/Scooterrete (Registration) Maximum Rupees. 100,000/-. (10000/- for Moped)

Margin of on Road Cost*

10% where salary is being disbursed through concerned branch or check off facility is there. *(Invoice Value+1Yr Insurance+ one-time road tax) 25% for business concerns

Income criteria Rs.10000/- pm. Is the minimum net monthly Income.. Income of parents/Guardians be considered in case of students. Income of spouse can be added. For business concern, IT return filed and challans for Tax deposited.

Repayment 60 EMIs for Scooters/Motor Cycles, 30 EMIs for scooterrete and 24 EMIs for Mopeds.

Guarantee No guarantee for loans up to Rs.25000/- Suitable guarantee for loans above Rs.Rs. 25000/- Sanctioning Authority may waive the guarantee if liquid security of at least 60% or EM of IP to the extent of 100% is offered. CH may waive the guarantee.

Insurance Comprehensive Insurance with bank clause and policy to remain with the bank.

Security Inspection

• PNB 551 is required for the Ist time. In case account is regular, PNB 551 is not required thereafter.

Retail Lending: Page 12 of 23

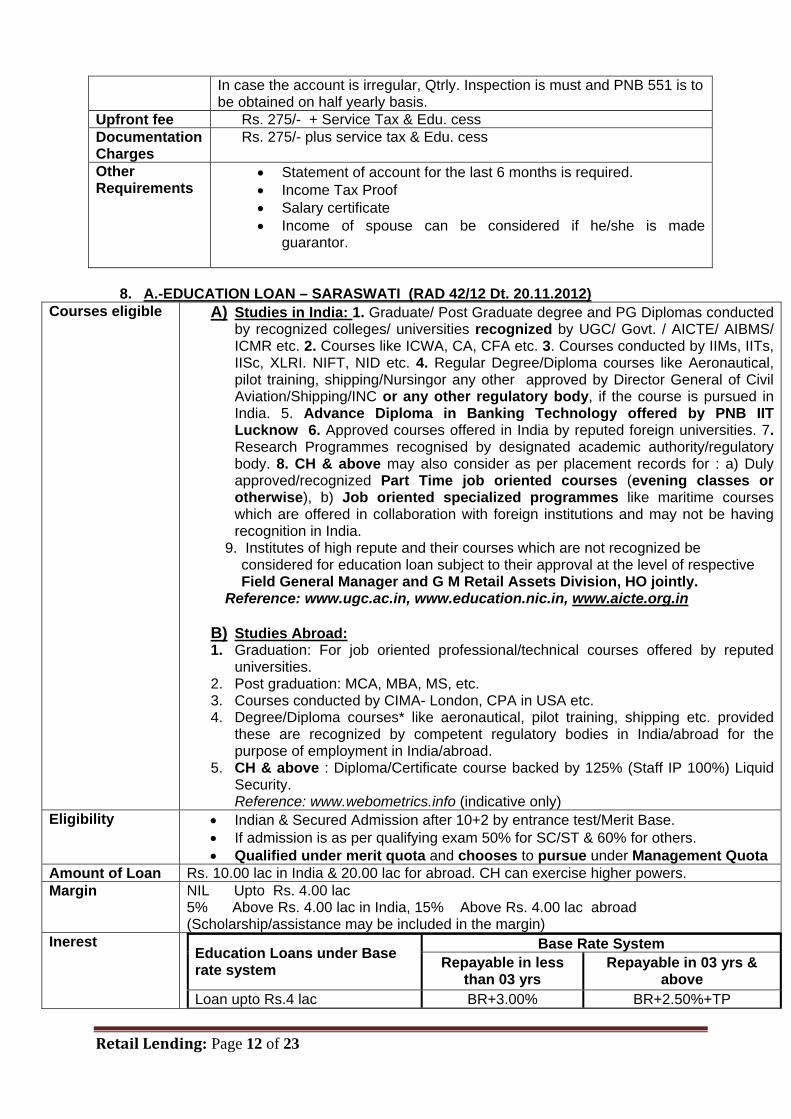

In case the account is irregular, Qtrly. Inspection is must and PNB 551 is to be obtained on half yearly basis.

Upfront fee Rs. 275/- + Service Tax & Edu. cess Documentation Charges

Rs. 275/- plus service tax & Edu. cess

Other Requirements

• Statement of account for the last 6 months is required. • Income Tax Proof • Salary certificate • Income of spouse can be considered if he/she is made

guarantor.

8. A.-EDUCATION LOAN – SARASWATI (RAD 42/12 Dt. 20.11.2012)

Courses eligible A) Studies in India: 1. Graduate/ Post Graduate degree and PG Diplomas conducted by recognized colleges/ universities recognized by UGC/ Govt. / AICTE/ AIBMS/ ICMR etc. 2. Courses like ICWA, CA, CFA etc. 3. Courses conducted by IIMs, IITs, IISc, XLRI. NIFT, NID etc. 4. Regular Degree/Diploma courses like Aeronautical, pilot training, shipping/Nursingor any other approved by Director General of Civil Aviation/Shipping/INC or any other regulatory body, if the course is pursued in India. 5. Advance Diploma in Banking Technology offered by PNB IIT Lucknow 6. Approved courses offered in India by reputed foreign universities. 7. Research Programmes recognised by designated academic authority/regulatory body. 8. CH & above may also consider as per placement records for : a) Duly approved/recognized Part Time job oriented courses (evening classes or otherwise), b) Job oriented specialized programmes like maritime courses which are offered in collaboration with foreign institutions and may not be having recognition in India.

9. Institutes of high repute and their courses which are not recognized be considered for education loan subject to their approval at the level of respective Field General Manager and G M Retail Assets Division, HO jointly. Reference: www.ugc.ac.in, www.education.nic.in, www.aicte.org.in

B) Studies Abroad: 1. Graduation: For job oriented professional/technical courses offered by reputed

universities. 2. Post graduation: MCA, MBA, MS, etc. 3. Courses conducted by CIMA- London, CPA in USA etc. 4. Degree/Diploma courses* like aeronautical, pilot training, shipping etc. provided

these are recognized by competent regulatory bodies in India/abroad for the purpose of employment in India/abroad.

5. CH & above : Diploma/Certificate course backed by 125% (Staff IP 100%) Liquid Security. Reference: www.webometrics.info (indicative only)

Eligibility • Indian & Secured Admission after 10+2 by entrance test/Merit Base. • If admission is as per qualifying exam 50% for SC/ST & 60% for others. • Qualified under merit quota and chooses to pursue under Management Quota

Amount of Loan Rs. 10.00 lac in India & 20.00 lac for abroad. CH can exercise higher powers. Margin NIL Upto Rs. 4.00 lac

5% Above Rs. 4.00 lac in India, 15% Above Rs. 4.00 lac abroad (Scholarship/assistance may be included in the margin)

Inerest Base Rate System Education Loans under Base rate system Repayable in less

than 03 yrs Repayable in 03 yrs &

above Loan upto Rs.4 lac BR+3.00% BR+2.50%+TP

Retail Lending: Page 13 of 23

Loan over Rs.4 lac to upto Rs.7.50 lac BR+4.00% BR+3.50%+TP

Loan over Rs.7.50 lac BR+3.50% BR+3.00%+TP Security Up to Rs. 4 L: NIL

> Rs 4 L upto Rs. 7.5 L: 3rd party guarantee. > Rs 7.50 Lacs EM of IP/Other Coll. Security. • Hyp of assets if created out of loan amount. • Co-obligation of students’ parents as well as assignment of future income of

student in loan > Rs. 7.5 L. For married persons, co-obligator can be spouse or parents or parents-in-law. Grand parents can also become co-obligants.

More than one loan in a family

In case of receipt of application for > than 1 loan for student borrower from a family, loan be considered individual wise & not family wise subject to max repaying capacity of parents. Rs. 4 L loan without security are meant for individuals & not for family.

Top-up Loans Top up loans may be sanctioned to students for pursuing further studies within overall eligibility limits with appropriate reschedulement of existing loans and required permission by the CH.

Age of student No restriction Income Criteria No Income criteria are prescribed for the parents. Priority Sector Rs.10.00 lacs in India and Rs.20.00 las for abroad. Repayment Loans upto Rs. 7.50 lacs – upto 10 years

Loans above Rs. 7.50 lacs – upto 15 years Moratorium/ Holiday period Course period + 1 year or 6 M after getting job whichever is earlier, extended MAX. upto 2 yrs with informing CH

Calculation of Interest

Simple interest during moratorium period & kept in a separate a/c.

Interest concession

1% interest concession is allowed if it is serviced during holiday period. 0.50% for women borrowers w.e.f 08.03.09 and 0.50% for PNB Score of 80 & above (Fresh)

Constitutes of Loan

Tuition fees, Hostel charges, Exam fees, Library/Lab charges, Books, Equipment, Instruments, Uniform, Building fund, Refundable deposit, Study Tours, Project work, Travel expenses & Computers. (Advances for Computers are allowed in Computer/Management courses only) with cap of 10+20%.

Fee Reimb Within 6 M. CH can allow > 6 M also on merits. Post-sanction Follow up

Follow up with college/university for getting progress report at regular intervals. Life Insurance as per option of borrower. PAN within 1 year of disbursement.

8. B - EDUCATION LOAN – PNB PRATIBHA (RAD 27/11 Dt. 12.07.2011)

Courses Eligible Premier Institutes, which include (i) Business Schools, (ii) Engineering Colleges, (iii) Medical Colleges and other reputed Institutes, shall be eligible to avail loan under the Scheme. These premier Institutes, numbering 103, have been segregated in three lists, which are available as per Annexures ‘A’, ‘B’ & ‘C’.

Student Eligibility • Indian National and Secured Admission • Secured admission in 103 premier institutions.

Amount of Loan Need based Finance subject to repaying capacity of the parents/students with margin and following ceilings: India : i. Max. Rs.15.00 lac as per list at Annexure ‘A’ – 08 Institutes. ii. Max. Rs.10.00 lac as per list at Annexure ‘B’ – 57 Institutes. iii. Max. Rs. 07.50 lac as per list at Annexure ‘C’ – 38 Institutes.

Margin NIL Upto Rs. 4.00 lac 5% Above Rs. 4.00 lac in India, (Scholarship/assistance may be included in the margin)

Security i. Co-obligation of parents/guardian as joint co-borrowers. ii. No collateral security to be obtained, iii. The student borrower to be offered Optional Life Insurance Cover

under the name ‘Vidya Rin Kavatch’ from Kotak Mahindra Old Mutual

Retail Lending: Page 14 of 23

Life Insurance Co. Ltd. (KLI). Interest Rate i. For Loans (repayable in 3 yrs. & above)

upto Rs.15 lac – Base Rate + 1.50% + TP .

ii. For Loans(repayable in less than 3 yrs)

Upto Rs.15 lac - Base Rate + 1.50% Other Guidelines 1. All other terms & conditions of the remaining parameters as prescribed under

Bank’s existing Education Loan Scheme, PNB Saraswati, shall apply mutatis mutandis for PNB PRATIBHA. 2.Field functionaries’ upto the level of Field General Manager/ General Manager (RAD, HO) shall not exercise their vested powers for permitting any relaxation/ concession under the brand PNB PRATIBHA. 3. All other Institutes shall continue to be covered under the extant provisions of Bank’s existing Education Loan Scheme – PNB Saraswati.

Interest concession 1% interest concession (Beginning to Last payment) is allowed if it is serviced during holiday period. Rebate of 0.5% is also allowed to female students.

8. C - EDUCATION LOAN – PNB KAAMGAR (RAD 32/12 Dt. 08.09.2012)

Courses Eligible 1. Vocational / Skill development courses of duration from 2 months to 3 years leading to certificate/ diploma offered by a recognised State/ Central Govt. institution or Statutory/ technical body or training department of Govt. etc. like courses offered by Industrial Training Institutes (ITIs), Industrial Training Centres (ITCs) and Polytechnic Institutes. 2. Institutes of high repute and their courses which are not recognized be considered for Education Loan subject to their approval at the level of respective Field General Manager and General Manager Retail Assets Division, HO jointly.

Student Eligibility • Should be an Indian National. • Student should have secured admission in a course run or supported by a

Ministry / Dept./ Organization of the Govt. or a company / society / organization supported by National Skill Development Corporation or State Skill Missions / State Skill Corporations, preferably leading to a certificate / diploma / degree, etc. issued by a Govt. organization or an organization recognized / authorized by the Govt. to do so.

Amount of Loan i) For Course upto 3 months Rs.20,000/- ii) above 3 to 6 months Rs 50,000/ iii) above 6 months to 1 year Rs 75,000/- iv) above 1 year Rs 1,50,000/- For Course above 1 year CH has full power Max Rs. 2,00,000/-

Margin NIL Security - Co-obligation of parents/guardian as joint co-borrowers.

- No collateral security/Third Party Guarantee to be obtained, Repayment For Course upto 1 year – In 2 to 5 years (Moratorium 6 months )

For Course above 1 year – In 3 to 7 years (Moratorium 12 months* ) *MAX. upto 2 yrs with informing CH + Extension of course period upto 2 yrs

Interest Rate Repayable in less than 3 yrs. - Base Rate + 3.00 Repayable in 3 yrs. & above - Base Rate + 2.50 + TP

Expenses Considered

- Tuition/ course fee. - Examination/ Library/ Laboratory fee. - Caution deposit. - Purchase of books, equipments and instruments. - Any reasonable expenditure found necessary for completion of the course.

Retail Lending: Page 15 of 23

Interest concession 1% interest concession is allowed if it is serviced during holiday period. Rebate of 0.5% is also allowed to female students.

9.PERSONAL LOAN TO PUBLIC (RBDA 23/01.05.09 & 27/26.05.09)

Eligibility Only PNB A/C holders are eligible. Min 6 M salary should be routed in the a/c or 6 m satisfactory transaction record for non salary saving a/cs.

Permanent Defence, CRPF, BSF & ITBP Personnel (Not to be granted to those who are due to retirement within next 24 Months.

Confirmed permanent employees of Central/state Govt./PSUs/Reputed COs./Schools/Institute/Hospitals etc who fulfill any of the following conditions:

1. Route of salary through branch or 2. Check-off facility Professionally qualified practicing doctors viz. MBBS, BDS & above having relationship with us min 6 Months having annual income of Rs. 4 Lac & above. Doctors should be tax payers for 3 years and ITRs be kept on record.

Check off Facility Employer undertakes to deduct monthly installment & remit towards for loan till itsliquidation & also confirms attachment of terminal dues.

Purpose & Extent Personal needs. Min Rs. 50000 & Maxi Rs. 4 Lac or 20 times net salary whichever is lower & Rs. 5 Lac for those salaried persons who have completed 3 years in present organization & drawing net monthly salary not less than Rs. 30000/-.

Nature TL or OD. Sanction Disbursement

All branches can generate leads for processing at RABs. However disbursement only by branches having recovery % not less than 90% under scheme at end of previous year.

Min net monthlyincome :

Metro Rs.15000/- p.m. Urban Rs.12500/- p.m. SU & Rural Rs.10000/- p.m. Defence Personnel & Teachers : Rs.7500/- p.m. CH may relax upto 12500/-, 10000/- & 7500/- for M/U/SU-R areas.

Margin Nil. Repayment TL – 60 EMIs OD- Reducing DP spread over 60 M.

Defence Personnel – 36 M. Amount of EMI should not be more than 50% of net monthly income. 60 PDCs (max) signed by borrower along with letter of deposit be obtained. PDCs not applicable where check off facility.

Guarantee Suitable 3rd party guarantee. CH/CM may waive. RBL Sheet PNB Score system will be applicable & score at least 50% marks. Other requirements - In case of Army personnel, a copy of authority letter be sent to Controller of Defence

Account (CDAO) Pune so that salary is remitted till liquidation of loan - Statement of account for at least 6 m. be obtained. - Affidavit that no other loan from other bank is availed be obtained. - Copy of IT return for previous 3 years be obtained. Form 16 be taken if loan is granted to employee. - A Registered letter be sent to the employer informing about details of loan raised by the employee. - It is clarified that branches eligible for disbursement/ maintaining the a/cs shall obtain blanket permission from CH for disbursement in next 25 a/cs.

Personal Loans for public – inclusion of LIC agents (RAD Cir 04/11 Dt. 07.01.2011)

LIC agents who earn regular commission from LIC and having account with our branch can avail personal loans from our bank provided: • Age is below 60 years & they are having agency for the last 5 years, • Minimum Income required is Rs. 10000 p.m. • Maxi loan amount is Rs. 2 L or 15 times average monthly commission. • 3rd party guarantee or Collateral up to 100% of loan amount. • Repayment in 60M up to 65 years. • The interest rate will be Bank Rate + 5%

10. LOAN FOR PENSIONERS (RAD 08/14 Dt. 07.02.2014)

Eligibility Pensioners drawing pension from the branch, Family Pensioners, DPDO Pensioners, Ex-employees.

Retail Lending: Page 16 of 23

Personal Loans for Pensioners

The amended guidelines are as under: Maximum Loan amount: Age up to 70 yrs 3.00 lac or 18 M pension (20 M in for defense

pensioners) Age >70 up to 75 yrs 1.50 lac or 18M pension (20 M in for defense

pensioners) Age > 75 yrs 0.70 lac or 12M pension

Deduction Take home Pension should not be less than 50% of monthly pension. Nature DL or TL or OD on monthly reducing DP. Margin Nil ROI OD= BR+3.50, DL/TL = <3Yrs: BR+3.25 & >3Yrs : BR+2.75+TP Guarantee Personal guarantee of spouse eligible for family pension or any other

family member or 3rd party guarantee. Repayment 60 EMIs . 24 EMIs in case age is more than 75 years which can be extended

up to 48 months by the sanctioning authority. Misc. • PPO be kept with the loan documents – Not required.

• Affidavit from the pensioner that present disbursing branch will not be changed without bank’s consent.

• Loan can be availed more than once only after adjustment of earlier loan. Upfront fee Nil. Doc. Charges Upto 2 lacs Rs 270/- + ST & above Rs.450/- + ST.

11.SCHEME FOR LOAN AGAINST MORTGAGE OF IP

Eligibility Business Enterprises, Professional & Self Employed – Cash Profits for the last 3 years and net Profits during immediate previous year. Min net profit Rs. 120000/- p.a. after adding back dep & interest. For Trusts, Societies and Educational institutions – 3 years criteria is not applicable.

Purpose & Extent

Business purpose : Net Income should be 1.5 times the EMI. (Min Rs. 10.00 lac & Maxi Rs. 1.00 crore.)

Status of the Scheme

- The scheme will be available for advance of Rs. 10 L & above but up to Rs. 100 L for business needs only in respect of prospective borrowers. - Nature of facility will be TL. OD facility can also be sanctioned in exceptional circumstances on monthly reducing DP repaid in maxi 84 M.

Nature Term Loan & OD. Assessment of Limit :

Maxi limit 80% of realizable value of IP or 3 times the annual gross income/gross profits (4 times in case of OD)Whichever is lower. However Net Income should be double the EMI (1.5 times in case of business units)

Repayment Max. 84 months. EMI up to 65 years of age in case of salaried class. OD – Monthly reducing DP limit is liquidated in 84 installments.

Security - 125% of Loan amount

EMI of House/flat/commercial property/self occupied or vacant house in the name of borrowers/spouse/Sole Prop/Partner/firm/parents. The loan can be granted to prop on mortgage of property in the name of firm. Finance can be made against leasehold property if the lease deed permits and loan is repaid before expiry of lease period.

Insurance At reconstruction cost excluding value of land. Other requirements

- The property against which loan is being sanctioned should not generally form part of Primary/collateral security in some other loan. - Income of spouse/parents/children can be added provided he/she is made co-borrower. - In case of business units, partner/director can be made guarantor if his income is added for determining EMI. - Security be inspected once a year in regular accounts, half yearly in irregular accounts and quarterly in NPAs. -Loans in Rural areas be disbursed only after the area is approved by Circle Head.

CIRCULARS RBDA 07/27.03.06, 22/05.07.06, 46/29.12.06, 05/10.01.07, 16/26.02.07, 47/07, 12/08, 53/08 & 60/09 Dt. 30.11.2009

12. PNB BAGHBAN SCHEME (CIR RAD 05/2014 Dt. 04.02.2014)

Eligibility Senior citizens owning Self-occupied property. If property in single name, there must be

Retail Lending: Page 17 of 23

will in favour of spouse & it should be registered. In case of joint property, one of the spouses must be of 60 years & above. The other spouse should be at least 58 years old. If there is no spouse, loan will be made in favour of single.

Purpose & Extent

To address the financial needs of senior citizens owning self occupied property (house) for leading a decent life, not for speculative/Trading purpose(Undertaking). Maximum amount Rs. 100 lacs.

Margin 20% of realizable value of property to arrive at the qualifying amount. Income Criteria

Not required.

Rate of Intt. BR+2.50 (Fixed) subject to reset after 5 years (Complete on 31st March). Disburseme-nt of Loan

In fixed monthly installments (to be calculated on reverse annuity basis) during loan tenor or till death of last surviving spouse, whichever is earlier. Life Certificate in November every year be obtained (Annex-VII)

Tenor of Loan

Age group of 60-70 years 15-20 years Age group above 70years 10-15 years.

Insurance Against fire, Earthquake and other calamities at the cost of borrower Security EM of IP in favour of bank. Valuation of property to be got done from approved valuer &

at a span of 5 years. Upfront fee Amount equal to half month’s loan subject to maximum of Rs. 15000/- + ST Doc. Chgs. Nil. Repayment The loan becomes due for payment after 6 months from death of both the spouses. In

case the loan is not repaid by legal heirs within 6 months from the death, the bank is within its right to sell the property for adjustment of the loan in case the consent of the legal heirs is not received within 6 months from the death of last survivor.

Others • Residual life of property should be at least 20 years. • Purpose of loan should not be speculation or trading. • It should be ensured that the will executed by borrower is the last will. • Life certificate is to be obtained once in a year in November.

Ancestral property as security

In case of residential property, which is ancestral and self-occupied, powers are vested with Circle Head(s) subject to safeguards as provided under the parameter - ‘Security’.

TL under PNB Baghban Scheme

A lump sum TL can be sanctioned up to Rs. 15.00 lac. The cases can be considered by HO only for medical purpose to senior citizens for treatment of self, spouse and dependents.

13. ADVANCE AGAINST GOLD/SILVER JEWELLERY/ORNAMENTS

Eligibility Against Gold Jewellery/Ornaments & Gold Coins (Coins weight maximum upto 50 grams) of Schedule Banks.

Purpose & Extent

Priority & Non- priority sector (Productive or Non-productive purpose) Productive purpose : Need base without any ceiling Non-productive : Maximum Rs. 10.00 lac.

Nature DL for 12 months/18 months or OD on annual renewal basis Margin Gold : 5%-Rs.2100/- per gm upto 31.12.13 (RAD 43 dt 04.10.2013) Repayment Principal : DL – Within 12/18 months by 12 EMIs or 4 Quarterly Installments or one time. OD

– Annual renewal with interest servicing. Intt - Agrl : Yearly/HLY & others as & when levied.

Insurance Finance Division HO has already taken Bankers’ indemnity policy covering loss of cash/ with the bank to the extent of Rs. 1.00 crore. The Division will obtain additional cover accordingly.

Security Verification :

Metal should be got tested by government-approved shroff. Where Govt. approved shroff is not available, CH may approve the same. The shroff will verify the genuineness of the metal and its market value. Valuation charges to shroff will be paid Rs.3.00 per thousand maximum Rs.300/- (RAD 24/30.07.2012)

Safe custody of Security

Metal will be kept in a separate sealed box in Joint custody. There should be entry in the relevant register (PNB 313).

Sale of The metal can be sold if loan is not repaid after giving Regd. Notice, valuation be obtained

Retail Lending: Page 18 of 23

Security from shroff. The minutes of sale will be recorded and excess amount realized will be paid to borrower.

Important Changes

In repayment capacity is to be ascertained and ensured at the time of sanction i.e. net monthly income of borrower is sufficient to meet the monthly interest obligation. • Disbursement by credit of SB account of the borrower.

CIRCULARS RBDA 44/25.08.09, RAD 14/12.04.2012, 02/01.01.14

GENERAL GUIDELINES OF RETAIL ADVANCES

Condition of 6 M relationship for considering retail loans

Various Retail loan schemes envisage that the borrower must have satisfactory transaction record with our bank. The condition may now be relaxed in the following cases:

1. Hub Incharge in Scale-IV and above be permitted to waive the condition if the borrower is permanent Grade –I/ Gazetted officer of Govt. Department/PSU (PF No. of the employee be obtained) or permanent employee of reputed Corporate under check off facility. (Reputed Corporate means ET500 companies or Limited concerns showing profits for the last 3 years or companies enjoying credit limit of minimum 5 crore with bank having PNB “A” or above rating.

2. CH can permit deviation on merits. (RBD-A Cir No. 39 dt. 20.7.2009)

Retail Advances – Core And Non-Core

Advances made under the following schemes are being reported under Retail Loan segment:- CORE RETAIIL SCHEME

a) Housing Loan; b) Car/Vehicle Loan; c) Education Loan; d) Personal Loan/Consumer Loan; e) Pensioner Loan; f) Gold Loan; g) Mortgage Loan (having sanctioned limit upto Rs. 1 crore); h) Reverse Mortgage Loan;

NON-CORE RETAIL SCHEME

i) Advances against Bank Deposits; j) Advances against Govt./Liquid Securities.

(RBD Adv. Cir. No. 30/10 dt. 30.7.2010) Loans to staff members under Public Scheme

All Staff members can avail loans under Public scheme. The important guidelines are as under:

• Loan for two wheelers can be availed even before stipulated period of 4/5 years of availing previous loan under concessional scheme.

• Personal loan to staff can be given even if they have not completed stipulated 5 years’ service.

• Housing loan for construction/repair can be availed despite availment of loan under concessional scheme.

• Take Home pay should not be less than 40%. • No documentation charges, Pre-payment charges & Up-front fee. • Housing loan for 2nd house can also be availed. • Balance of Principal should not exceed 80% of Terminal dues. • Housing loan can be given to staff even if there is lesser period of remaining service. • Income of Spouse can be added for determining repaying capacity. L&A Cir. No. 80

dt. 30.6.2011. • Loans will be sanctioned on same terms & conditions as applicable to public. L&A

Retail Lending: Page 19 of 23

Cir. No. 46 dt. 18.04.2013. Time norms – Retail Lending

The revised time norms are as under:

Nature of loan Time norms Non- Mortgage loans like Vehicle loan, Gold loan, Personal and Pensioners’ loans

3 days

Mortgage loans like HL, Adv against IP & Reverse Mortgage loan

RAB 7 days / others 10 days

Education Loan under Branch powers 1 week Education loan under CH powers 2 weeks

(RAD Cir. No. 34/11 dt. 1.9.2011)

CIR from CIBIL / EQUIFAX / EXPERIAN/ HIGHMARK

The revised guidelines are as under: (LA Cir. No. 32/14 dt. 14.03.2014) Loan amount less than Rs. 5,00,000/- For Retail & MSME or other facility where CIBIL Score is a parameter in PNB scoring model – One CIR from CIBIL or Experian or Equifax In other cases – One CIR from any CIC (without score) Loan amount Rs. 5,00,000/- and above

i. One CIR from CIBIL is mandatory + ii. One compulsory CIR from either Experian or Equifax

RECOVERY THROUGH ECS IN RETAIL LOANS

Existing guidelines are as under :

"Recovery/ Repayment of EMIs in housing loan accounts may also be considered through ECS/ Standing Instruction Mandate of the customers for debiting their accounts. Wherever ECS/ Standing Instructions are obtained, 2-3 PDCs are to be procured/ maintained by the branches/ Retail Asset Branches to keep remedy alive under Section-138 of Negotiable Instruments Act."

Bank has decided that henceforth the option of Electronic Fund Transfer (ECS Debit mandate/ Standing Instructions) be also considered for recovery of monthly installments in respect of the all Retail Loan Schemes and the instructions/ guidelines as above shall form part of Repayment Parameter of all these Retail Loan Schemes. Repayment through ECS be made popular amongst Retail borrowers. ( RAD Cir. No. 3/12 dt. 12.1.2012)

Capturing Mobile No. of Retail Borrowers in CUMM

Bank has desired that Mobile No. of all Retail Loan customers is duly entered in the system under CUMM. Reminders for payment of loan installments will be sent through SMS. There is no need to get separate mandate to register him for SMS Alert. (TBD Cir. No. 2/12 dt. 12.1.2012)

Changes effected in Monitoring of loan accounts

Fixing of first EMI – EMI be fixed in such a manner that the due date of 1st installment falls due (in the month in which the repayment commences) on the same date on which 1st disbursement has been made. SMS alert be sent to the borrowers 3 days before the EMI is due. 1st day = System generated SMS 7th day = System generated SMS 1st day = System generated SMS 8th – 9th day = 1st Telephonic contact

Retail Lending: Page 20 of 23

10th day = Personal Meeting of Branch official with borrower 15the day = 2nd telephonic contact 21st – 25th day = 1st Reminder. 30th day = Meeting of borrower with Branch official and official of the Circle Office. 37th-40th day - Registered Reminder with copy to guarantor - 2nd Reminder with copy to guarantor 45th day = Meeting of borrower with Branch official and 2nd man of the Circle Office. 75th day = Meeting of the borrower be held with Branch Incumbent and Circle Head. Before 90th day = Personal Contact by Incumbent himself again with borrower/guarantor / family members at his/their residence. Thereafter as per NPA norms. (RAD Cir. No. 20/12 dt. 31.5.2012)

Housing Loan – Statement of Account

In terms of one of the recommendations of Damodaran Committee, Banks should automatically provide annual account statement to Housing Loan customers without awaiting any specific request. Accordingly, it has been decided that Housing Loan statement of Account for previous financial year be provided to customers automatically in the first week of April every year.

HUB & SPOKE MODEL [RBD ADV 13/2010]

The Modified Model comes into effect from 01.04.2010 Retail credit dispensation, was being done through following delivery channels:

i) Hub & Spokes Model ii) CCPC Model iii) Independent branches such as LCBs/MCBs/LCBs

Amendments have now been made in Hub & Spokes Model. Hubs have now become Retail Asset Branches. Minimum one Retail Assets Branch at every city centre having 6 or more Branches. Branches attached with hubs (Retail Asset Branches) will only source the applications and these applications will be processed, sanctioned, disbursed and monitored at the Hub itself. Sanction of loans under Housing, Mortgage, Education, Auto and Bulk Personal loan schemes centralized at Retail Asset Branches. Other types of loans may be considered by all Branches. CH have the discretion to keep a maximum of 25% of total branches at the hub centre outside the purview of Hub and Spokes Model subject to certain conditions, which include:

a) The Branch is not under the “HIGH RISK” category. b) Branch has a recovery rate of more than 90% in retail loan category and NPAs are not more

than 1% under Retail Advances as at the end of previous half year. c) Adequate staff/infrastructure is available with the branch, especially to deal with mortgage related

cases. d) PNB score model has been installed at the branch and the staff is conversant with its use.

These branches shall be independent to carry out all activities pertaining to pre-sanction appraisal, disbursement, documentation and post-sanction monitoring. Circle Central Processing Cell (CCPCs), established for sanction of retail loans at other centres stand disbanded. All Moffusil Branches (outside the Hub centre) shall consider retail loans within their vested loaning powers subject to fulfillment of stipulations regarding branches outside the purview of Hub & Spoke Model (items (a) to (d) above). Branches not conforming to these, shall seek administrative clearance from their respective Circle Heads, on case to case basis, before considering the same at their level.

Retail Lending: Page 21 of 23

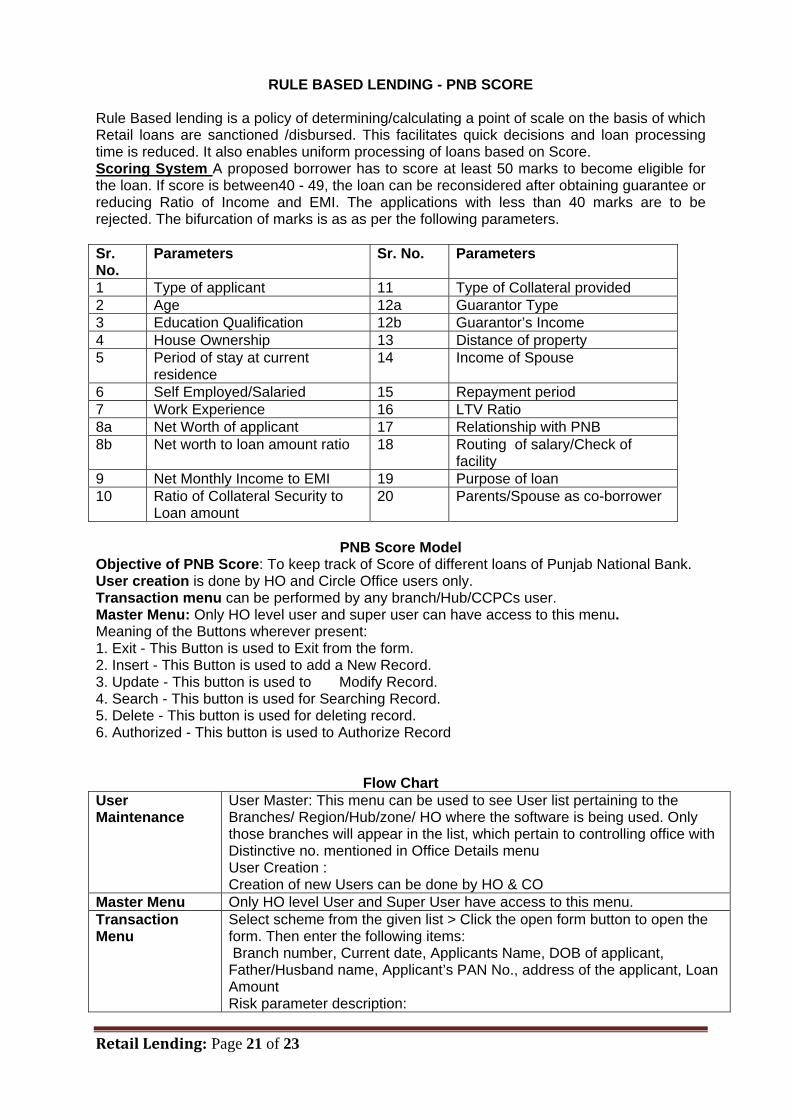

RULE BASED LENDING - PNB SCORE

Rule Based lending is a policy of determining/calculating a point of scale on the basis of which Retail loans are sanctioned /disbursed. This facilitates quick decisions and loan processing time is reduced. It also enables uniform processing of loans based on Score. Scoring System A proposed borrower has to score at least 50 marks to become eligible for the loan. If score is between40 - 49, the loan can be reconsidered after obtaining guarantee or reducing Ratio of Income and EMI. The applications with less than 40 marks are to be rejected. The bifurcation of marks is as as per the following parameters. Sr. No.

Parameters Sr. No. Parameters

1 Type of applicant 11 Type of Collateral provided 2 Age 12a Guarantor Type 3 Education Qualification 12b Guarantor’s Income 4 House Ownership 13 Distance of property 5 Period of stay at current

residence 14 Income of Spouse

6 Self Employed/Salaried 15 Repayment period 7 Work Experience 16 LTV Ratio 8a Net Worth of applicant 17 Relationship with PNB 8b Net worth to loan amount ratio 18 Routing of salary/Check of

facility 9 Net Monthly Income to EMI 19 Purpose of loan 10 Ratio of Collateral Security to

Loan amount 20 Parents/Spouse as co-borrower

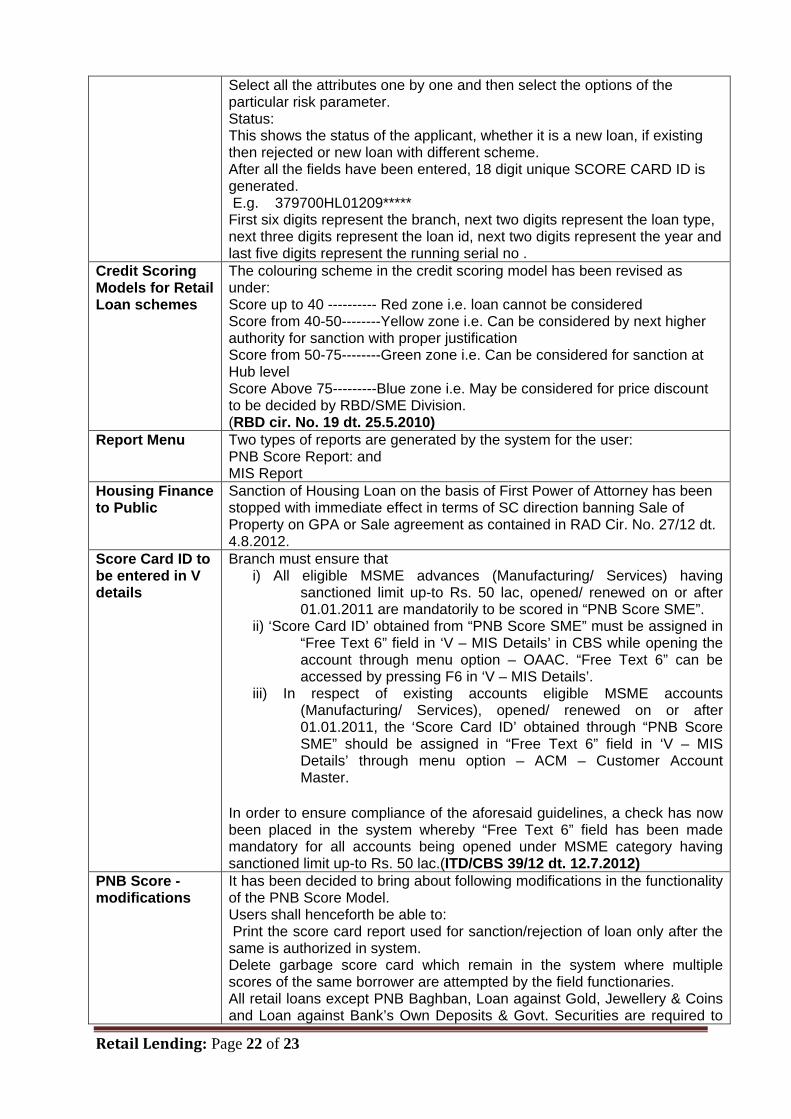

PNB Score Model

Objective of PNB Score: To keep track of Score of different loans of Punjab National Bank. User creation is done by HO and Circle Office users only. Transaction menu can be performed by any branch/Hub/CCPCs user. Master Menu: Only HO level user and super user can have access to this menu. Meaning of the Buttons wherever present: 1. Exit - This Button is used to Exit from the form. 2. Insert - This Button is used to add a New Record. 3. Update - This button is used to Modify Record. 4. Search - This button is used for Searching Record. 5. Delete - This button is used for deleting record. 6. Authorized - This button is used to Authorize Record

Flow Chart User Maintenance

User Master: This menu can be used to see User list pertaining to the Branches/ Region/Hub/zone/ HO where the software is being used. Only those branches will appear in the list, which pertain to controlling office with Distinctive no. mentioned in Office Details menu User Creation : Creation of new Users can be done by HO & CO

Master Menu Only HO level User and Super User have access to this menu. Transaction Menu

Select scheme from the given list > Click the open form button to open the form. Then enter the following items: Branch number, Current date, Applicants Name, DOB of applicant, Father/Husband name, Applicant’s PAN No., address of the applicant, Loan Amount Risk parameter description:

Retail Lending: Page 22 of 23

Select all the attributes one by one and then select the options of the particular risk parameter. Status: This shows the status of the applicant, whether it is a new loan, if existing then rejected or new loan with different scheme. After all the fields have been entered, 18 digit unique SCORE CARD ID is generated. E.g. 379700HL01209***** First six digits represent the branch, next two digits represent the loan type, next three digits represent the loan id, next two digits represent the year and last five digits represent the running serial no .

Credit Scoring Models for Retail Loan schemes

The colouring scheme in the credit scoring model has been revised as under: Score up to 40 ---------- Red zone i.e. loan cannot be considered Score from 40-50--------Yellow zone i.e. Can be considered by next higher authority for sanction with proper justification Score from 50-75--------Green zone i.e. Can be considered for sanction at Hub level Score Above 75---------Blue zone i.e. May be considered for price discount to be decided by RBD/SME Division. (RBD cir. No. 19 dt. 25.5.2010)

Report Menu Two types of reports are generated by the system for the user: PNB Score Report: and MIS Report

Housing Finance to Public

Sanction of Housing Loan on the basis of First Power of Attorney has been stopped with immediate effect in terms of SC direction banning Sale of Property on GPA or Sale agreement as contained in RAD Cir. No. 27/12 dt. 4.8.2012.

Score Card ID to be entered in V details

Branch must ensure that i) All eligible MSME advances (Manufacturing/ Services) having

sanctioned limit up-to Rs. 50 lac, opened/ renewed on or after 01.01.2011 are mandatorily to be scored in “PNB Score SME”.

ii) ‘Score Card ID’ obtained from “PNB Score SME” must be assigned in “Free Text 6” field in ‘V – MIS Details’ in CBS while opening the account through menu option – OAAC. “Free Text 6” can be accessed by pressing F6 in ‘V – MIS Details’.

iii) In respect of existing accounts eligible MSME accounts (Manufacturing/ Services), opened/ renewed on or after 01.01.2011, the ‘Score Card ID’ obtained through “PNB Score SME” should be assigned in “Free Text 6” field in ‘V – MIS Details’ through menu option – ACM – Customer Account Master.

In order to ensure compliance of the aforesaid guidelines, a check has now been placed in the system whereby “Free Text 6” field has been made mandatory for all accounts being opened under MSME category having sanctioned limit up-to Rs. 50 lac.(ITD/CBS 39/12 dt. 12.7.2012)

PNB Score - modifications

It has been decided to bring about following modifications in the functionality of the PNB Score Model. Users shall henceforth be able to: Print the score card report used for sanction/rejection of loan only after the same is authorized in system. Delete garbage score card which remain in the system where multiple scores of the same borrower are attempted by the field functionaries. All retail loans except PNB Baghban, Loan against Gold, Jewellery & Coins and Loan against Bank’s Own Deposits & Govt. Securities are required to

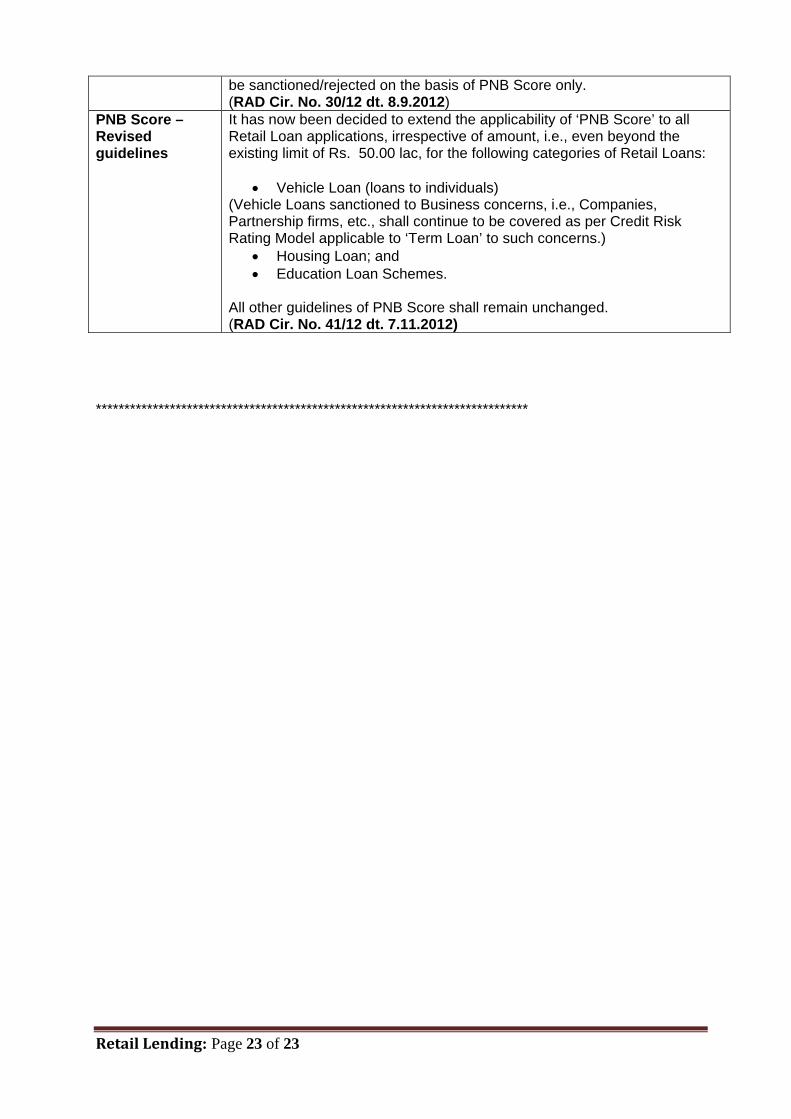

Retail Lending: Page 23 of 23

be sanctioned/rejected on the basis of PNB Score only. (RAD Cir. No. 30/12 dt. 8.9.2012)

PNB Score – Revised guidelines

It has now been decided to extend the applicability of ‘PNB Score’ to all Retail Loan applications, irrespective of amount, i.e., even beyond the existing limit of Rs. 50.00 lac, for the following categories of Retail Loans:

• Vehicle Loan (loans to individuals) (Vehicle Loans sanctioned to Business concerns, i.e., Companies, Partnership firms, etc., shall continue to be covered as per Credit Risk Rating Model applicable to ‘Term Loan’ to such concerns.)

• Housing Loan; and • Education Loan Schemes.

All other guidelines of PNB Score shall remain unchanged. (RAD Cir. No. 41/12 dt. 7.11.2012)

****************************************************************************

Recommended