1

Scoping note on subnational competitiveness in Georgia

July 24, 2020

World Bank Group1

1 The note was prepared by Austin Kilroy (Senior Economist) and Ceylan Oymak (Consultant), under the guidance of Marialisa

Motta and Ilias Skamnelos (Practice Managers), Sebastian Molineus (Country Director), and Evgenij Najdov (Program Leader).

The team is grateful for inputs and advice from Mariam Dolidze (Senior Economist), Tengiz Gogotishvili (Senior Urban Specialist),

Gabriel Goddard (Lead Economist), Dmitry Sivaev (Urban Specialist), Ifeyinwa Onugha (Private Sector Specialist), Nadeem

Karmali (Senior Economist), Conor Kearney (Regional Economic Development Consultant), the Tbilisi-based team of the United

Nations Development Programme, and most of all to the National Statistics Office of Georgia – Geostat for graciously sharing data

for the analysis. None of the detailed analysis in this document could have been done without the excellent firm-level data collected

by Geostat each year.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

2

Executive Summary

The objective of this scoping note is to inform decisions between the World Bank Group and the

Government of Georgia on engagements related to subnational growth and economic development.

The note is intended to be an initial review of the policy landscape and economic situation, using readily

available information and data. It provides information to determine if the topic of subnational

competitiveness could be pursued further within the partnership between the World Bank Group and the

Government of Georgia.

The note consists of three sections:

1. Review of the policy environment related to subnational competitiveness;

2. Benchmarking and recommendations for subnational competitiveness;

3. Estimating the impact of Covid-19 at subnational level.

1. Policy environment

• Georgia’s subnational competitiveness agenda is established by the Regional Development

Programme (RDP) 2018-2021. The RDP 2018-2021 aims to address competitiveness of Georgia’s

regions, leading to increased equality of economic outcomes in regions. It outlines five key

priorities for action: infrastructure; economy; human resources; endogenous development (local

initiatives and specializations); and institutional development. The RDP 2018-2021 is a relatively

comprehensive document and includes proposals for economic specialization of each of Georgia’s

regions.

• In preparation for the next RDP, a few key questions can illuminate issues to explore further.

Are the proposed economic specializations realistic? Will they be sufficient to guide investment

choices? Will the investments be effective in achieving their goals? A second set of questions

relates to the emphasis of the RDP on the regional scale (mkhare) for analysis and action. Georgia’s

subnational economy, like those in other countries, is driven by urban hubs. Does the RDP leverage

these growth drivers in its approach? The analysis in the subsequent section of the document aims

to provide information and ideas that can inform preparation of RDP 2022-2025, and/or substantiate

a discussion between the World Bank Group and Government of Georgia on subnational

competitiveness issues more broadly.

2. Benchmarking and recommendations for subnational competitiveness

• The Government’s emphasis on addressing inequalities between Tbilisi and other regions in

Georgia seems well-founded. Regional inequality of GDP per capita is substantially higher in

Georgia than in comparator countries such as Armenia, Turkey, Poland, or Hungary. Tbilisi

accounts for 32 percent of Georgia’s population, but 67 percent its gross value added, and 81 percent

of its foreign investment. The structure of economic activity is dramatically polarized: in Tbilisi,

70 percent of the population are formally employed, but outside Tbilisi only around 30 percent of

the population have formal jobs. The severity of the disparity means that regions outside Tbilisi

even lack enterprises that can generate economic growth. Large firms have been the strongest

drivers of economic growth in Georgia, and these large firms are concentrated in Tbilisi and a few

other cities.

• The regional economic specializations proposed by the RDP could be more selective, more

specific, and should be appraised before investment decisions are made. The RDP proposes

that some sectors (tourism, agro-processing, and renewable energy) have an economic potential in

most or all Georgia’s regions, yet economic data shows that agro-processing is mostly concentrated

in four regions. Wine-making, higher education and innovation, and mining and renewable energy

3

are concentrated in fewer regions than indicated in the RDP. Meanwhile light manufacturing is not

mentioned at all despite being successful in several regions. Overall, a more selective set of

specializations may be more realistic. The competitiveness requirements for each of these sectors

will need to be defined in more detail, and then appraised, before investment decisions can be taken.

Numerous industry studies and value chain studies have been carried out in Georgia, so the results

of those studies could be consolidated and leveraged.

• Georgia does have secondary nodes of economic activity outside Tbilisi—particularly at the

municipal level. These secondary cities can be leveraged in regional development efforts.

Examining the spatial distribution of sectors within regions can help focus public investments in

nodes of competitiveness. According to data from Georgia’s firm-level survey, agro-processing is

concentrated in Georgia’s cities, while 38 out of 64 municipalities have negligible or zero activity

in agro-processing. Agriculture is concentrated in some municipalities, with substantial variation

even between rural municipalities. High-value subsectors are concentrated in Tbilisi and a few other

municipalities: meat and dairy processing is focused in Tbilisi; high value manufacturing is found

mainly in Tbilisi, Rustavi, and Zestafoni. This analysis of high-value subsectors is useful to indicate

locations where each industry is most advanced and competitive. Such geographic concentrations

have increased over time. Existing nodes of activity in each sector have grown further, while other

municipalities have shrunk. New investment has focused on municipalities that are existing nodes

of economic activity (see Figure 1).

Figure 1: Sales (above) and investments (below) in high-value subsectors are concentrated in a few municipalities

Source: World Bank analysis of Geostat survey data

• The next RDP could be sharpened by focusing on nodes of growth within and across regions.

Georgia’s constraints on competitiveness and growth are likely to vary by sector, region, and

municipality. The current RDP focuses on economic specializations for each region, which may

4

have a strong basis in the political economy in Georgia, and resonates with the way Georgians

consider the geography of their country. However, this regional lens misses crucial elements of

economic development, particularly the concentration of economic activities in municipalities

within each region. The next RDP could focus on Georgia’s urban centres with populations above

40,0002, and the functional economic areas around them. Existing nodes of economic activity would

be the natural locations for specific investments to release those constraints, balancing the objectives

of economic growth and spatial equity. This approach would reach 80-90 percent of Georgia’s

population.

3. Estimating the impact of Covid-19 at subnational level

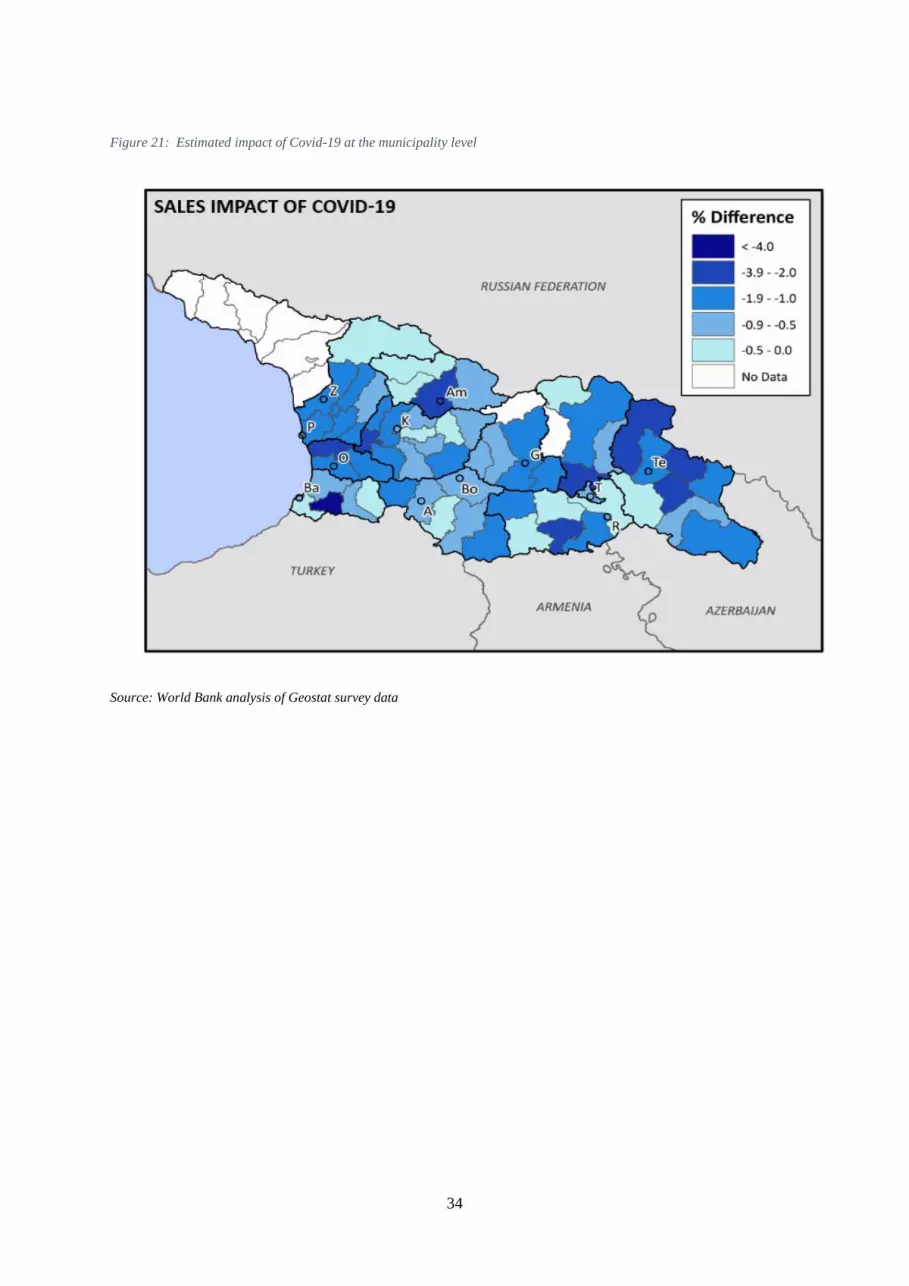

• The impact of a Covid-19 downturn will differ across Georgia, and therefore may require a

subnational lens on economic support measures. We estimated the likely effect on each

municipality, based on the mix of sectors in each municipality’s economy, and an estimate of the

impact of the pandemic per sector. Overall the economic shock induced by the pandemic will likely

impact most severely the smaller municipalities, because they have a higher share of sectors more

heavily affected by the downturn—especially tourism and transportation. Municipalities in Adjara,

Kakheti, plus Samtredia and Guria, are estimated to be affected most. The analysis is summarized

in Figure 2.

Figure 2: Estimated impact of Covid-19 at the municipality level

Source: World Bank analysis of Geostat survey data

Next steps

On the basis of these observations, some recommendations can be made for next steps on subnational

competitiveness work. These recommendations are:

I. Combine sectoral and regional studies to assist in prioritizing subnational investments and

interventions. Consolidate and leverage the industry and value chain studies for ‘economic

2 Tbilisi, Batumi, Kutaisi, Rustavi, Gori, Zugdidi, and Poti.

5

potential’ sectors to identify a more specific, targeted and appraised set of proposed regional

investments. For example, a lack of cold storage and packing facilities in fruit producing regions;

a need for training in emergency response in tourism regions; managerial capabilities in firms in

municipalities with concentrations of light manufacturing firms. Some constraints may affect many

regions—such as access to banks and finance, which may be a constraint in most municipalities

outside Tbilisi and some other cities. The approach should nuance the understanding of subnational

competitiveness by focusing on nodes of economic activity in municipalities within each region.

II. Assign specific responsibilities amongst government bodies to release constraints on

subnational competitiveness. In the next RDP, the constraints identified in the first step of analysis

could be mapped, and responsibilities for key investments and actions would be allocated to the

various levels of government (national, regional, and municipal). A roadmap would be created with

clearly defined targets and timelines for those investments and actions. The various ministries and

agencies would need to be accountable for achieving the milestones in the roadmap, and so the set

of actions must be specific and realistic.

III. Financing for subnational competitiveness. Develop a subnational competitiveness fund to

finance interventions to support competitiveness at the municipal and regional level. The fund

would balance the objectives of dispersing regional development outside Tbilisi while concentrating

it in nodes with the best chance of success. The fund could be institutionalized as a window within

the Municipal Development Fund (which until now has focused mainly local infrastructure), or

alternatively could be established separately by the Ministry of Economy. Funds could be applied

for by regions or municipalities through competition. Access to the funds would be conditional on

minimum access criteria (e.g. municipal and regional objectives that are approved by the national

government as being in line with the RDP; acceptable financial management processes; etc), and

perhaps can incorporate performance management through financial bonuses for achieving agreed

targets. The implementation structure for the fund could build on lessons from the Pilot Integrated

Regional Development Programmes (PIRDPs) in Georgia, by retaining the managing authority and

the structure of calls for proposals, and adding a performance framework at regional and municipal

levels.

6

Contents

Executive Summary ...................................................................................................................................... 2

1. Review of Georgia’s subnational competitiveness policy environment ............................................ 7

1.1. Government aims for subnational economic development ............................................................ 7

1.2. Actions, reforms and investments in support of the spatial priorities ............................................ 7

1.3. Notable features of the RDP approach ........................................................................................... 9

a. Are the proposed economic specializations realistic, sufficient, and effective? ............................ 9

b. Are regions the best scale for analysis and action? ...................................................................... 11

2. Benchmarking and recommendations for subnational competitiveness ........................................ 14

2.1. Does Georgia have an unusually severe problem in regional development? ............................... 14

2.2. Where are the best opportunities for subnational growth? ........................................................... 18

a. Where are Georgia’s tradable sectors currently concentrated in the regions?.............................. 18

b. How is regional concentration changing over time? .................................................................... 22

c. What interventions will be important for these subsectors? ......................................................... 31

3. Estimating the impact of Covid-19 at the subnational level ............................................................ 33

Next steps: Industry-level Diagnostics and Policy Levers ....................................................................... 35

4. Technical Appendix ............................................................................................................................ 37

4.1. Firm-level analysis of economic activity at the municipal level .................................................. 37

a. Firm-level survey data .................................................................................................................. 37

b. Limitations ................................................................................................................................... 37

c. Sector-based analysis ................................................................................................................... 39

d. Measuring economic activity ....................................................................................................... 40

e. High-value subsectors .................................................................................................................. 42

4.2. Coefficient of variation of regional inequality ............................................................................. 44

4.3. Disruption of economy activity during Covid-19 ........................................................................ 44

7

1. Review of Georgia’s subnational competitiveness policy environment

The purpose of this section is to summarize the main strategic priorities and actions undertaken at national

and subnational level. Key questions are:

• What are the Government’s declared aims for subnational economic development?

• What actions, reforms and investments are being undertaken?

• What opportunities may exist to improve these regional development initiatives?

1.1. Government aims for subnational economic development

The key strategic document for regional development in Georgia is the Regional Development

Programme (RDP) 2018-2021. The RDP 2018-2021 follows the RDP 2015-2017 and the State Strategy

for Regional Development 2010-2017. The RDP takes inspiration from “European Union recent approaches

to social-economic cohesion policy, including territorial integrated interventions and focus on the

exploitation of territorially differentiated potentials.”

The RDP outlines three key needs to be addressed:

1. Increased competitiveness of Georgian economy, through addressing socio-economic

characteristics of individual regions;

2. Increased equality of outcomes in regions (employment, poverty, focus on agriculture outside

Tbilisi [this is presented as a bad thing], depopulation, aging, access to basic services, healthcare).

3. A legal basis for regional development policy, including enhanced financial powers and institutional

capacity for local authorities.

These needs respond to a diagnosis of regional development problems in Georgia, especially:

• High emigration rate. Georgia lost more than 30 percent of its population in the last 25 years, with

outlying regions such as Racha-Lechkumi and Kvemo-Svaneti especially affected.

• High inequalities. For example: wages outside Tbilisi are 40-60% lower than wages in Tbilisi.

• Access to basic public services. For example: in some regions only 34% of households have a piped

water supply.

• Lack of equality of opportunity. For example: vocational education and training institutions are very

scarce in Kvemo Kartli and Samtskhe-Javakheti regions.

A total budget of GEL 18 billion is assigned to the RDP 2018-2021. The budget is drawn from the state

budget, donor funding, and cofinancing by beneficiaries of RDP support.

1.2. Actions, reforms and investments in support of the spatial priorities

The RDP 2018-2021 outlines five key priorities for action:

1. Infrastructure: transport, environmental, energy;

2. Economy: support to entrepreneurs; increased access to finance for innovative firms; improved

connections in the innovation system; increased exports of higher value-added products through

applying a smart specialization approach; support to development of tourism and agri-food;

increased investments including FDI.

3. Human resources: education reforms; social infrastructure; VET; higher education; R&D

institutions; labor market reforms to reduce skills mismatch; active labor market programs.

4. ‘Endogenous development’: involvement of citizens in improving living conditions at level of

municipalities; small scale infrastructure; diversification of local economies; increased availability

of public services in high mountainous areas; development of Black Sea ports for logistics

development; connection of Tbilisi with neighboring municipalities.

8

5. Institutional development: capacities of national and local authorities to support implementation of

RDP; strengthened analytic capacity of ministries including GEOSTAT’s capabilities for trends

analyses and regional data; a partnership principle in the policy cycle; and preparation of pilot

integrated regional development programmes co-financed by the EU.

There is a strong continuity between RDP 2018-2021 and RDP 2015-2017. The strategic diagnostic and

analysis in RDP 2018-2021 is substantially stronger, more detailed and sophisticated than the RDP 2015-

2017. Yet the proposed priorities are very similar: the first three priorities are almost the same as advocated

in RDP 2015-2017; the priorities of rural development and tourism in the RDP 2015-2017 have been

subsumed in the first three priorities in RDP 2018-2021; and the fourth and fifth priorities in RDP 2018-

2021 are new.

The RDP proposes economic ‘potentials’ for all regions in Georgia. These are summarized in Table 1:

the green cells indicate regions and sectors proposed by the RDP as economic potentials. The rationale for

these proposed specializations is not always clear: were they chosen according to actual historical

performance, or according to potential opportunities, or a combination of both? Some combination seems

likely: existing nodes of economic activity, plus expectations for tourism or agriculture in the weaker regions.

Table 1: Summary of regional ‘potentials’ proposed in RDP 2018-2021

Source: World Bank team summary of material in RDP 2018-2021, pages 60-63.

Each of the five priorities are defined with detailed Measures, and single main responsibilities are

assigned to line Ministries. The RDP is intended to be implemented by a network of relevant Ministries,

agencies, and other stakeholders. These include the following:

• Government Commission on Regional Development (GCRD), which coordinates activities between

ministries, discusses and endorses all strategic documents for RDP programming and

implementation, and facilitates thematic coordination with development partners.

• Ministry of Regional Development and Infrastructure (MRDI), which coordinates implementation,

liaises with line ministries on implementing program measures, reports on progress to the GCRD,

RDP Monitoring Committee, rest of the Government, and general public.

• Technical Coordination Unit, which acts as an inter-ministerial and interagency working group;

• Coordination Unit for donor programs

• Intermediate Bodies

• Local self-government bodies

• State Audit Office

• Other stakeholders, such as the National Council of Mountain Development, the Interagency

Coordination Council on Rural Development of Georgia, and the Georgian Regional Development

and Local Self-government Reform Commission.

Tbilisi Adjara Guria Imereti KakhetiMtskheta-

MtianetiRacha

Samegrel

o

Samtskh

e-

Javakheti

Kvemo

Kartli

Shida

Kartli

Agro-processing

Wine-making

Tourism

Mining

& renewable energy

Logistics

Higher education

& innovation

9

Main responsibilities are assigned to line Ministries. For example: support to enterprises is assigned to the

Ministry of Economy and Sustainable Development; integration of vulnerable groups is assigned to the

Ministry of Internally Displaced Persons; functional integration of Georgian urban territories is assigned to

the Ministry of Economy and Sustainable Development3.

Four pilot regions have been chosen for pilot integrated regional development programmes (PIRDPs).

The pilot regions are: Samtske-Javakheti, Imereti, Samegrelo-Zemo Svaneti, and Kakheti. Action in these

regions will be boosted by a total budget of EUR 67.2 million, including budget support from the EU of

EUR 40.5m4. The rationale for the PIRDPs is:

“the best way to build capacity of the administration and achieving tangible development results is the

preparation and realisation of pilot integrated regional development programmes. Such pilot programme (-s)

co-financed and managed at first stage directly by the European Commission, should be developed in line with

regional development strategy (-ies) and involve a broad range of national, regional and local stakeholders

allowing for mutual exchange and cooperation with use of Multi- Level Governance approach.”5

The PIRDP initiatives will prioritize:

(i) Urban renewal;

(ii) Unique tourism potential;

(iii) Improved competitiveness and support to innovations of SMEs;

(iv) Integrated local development;

(v) Technical support and capacity building of central and local administrations.

The implementation mechanisms for the PIRDPs are similar to those of operational programmes of

European Structural and Investment Funds in European Union member states. Calls for proposals are

issued; then project proposals are made by private sector, municipalities, civil society organizations, and

other stakeholders; proposals are evaluated; grants are contracted to recipients; and final compliance checks

are done by a technical coordination unit of the MRDI acting as a ‘Managing Authority’.

1.3. Notable features of the RDP approach

The RDP 2018-2021 is a comprehensive document and reflects many elements of good practice. It is

based on diagnostic analysis of the current situation and potential opportunities. Its framework for economic

development is based on specialization in selected economic sectors and niches, supported by interventions

to catalyze those opportunities. The scope of interventions covers a full range of constraints to growth.

These are good practices in designing regional development interventions. Box 1 outlines some of the World

Bank Group’s experience with subnational economic development which can help inform policies and

interventions in this area.

This section of the document will focus on two key features of the RDP which underpin its proposals

for subnational competitiveness: (a) prioritization of economic sectors; and (b) the emphasis on

regions. Each of these features is examined in turn. These issues are examined to provide ideas for a revised

approach to Georgia’s RDP, which could be implemented as part of a subsequent RDP (e.g. for years 2022-

2025).

a. Are the proposed economic specializations realistic, sufficient, and effective?

The RDP 2018-2021 proposes economic specializations for each region of the country. As summarized

by Table 1, above:

3 Regional Development Programme (RDP) of Georgia 2018-2021, Ministry of Regional Development and Infrastructure of

Georgia, p. 130. 4 ‘Regional Development Policy in Georgia’, presentation made by Deputy Minister of the Ministry of Regional Development and

Infrastructure, at European Week of Regions and Cities, Brussels, 7-10 October 2019. 5 RDP 2018-2021, p. 59.

10

• All regions are indicated as having

potential in tourism and in mining or

renewable energy;

• Almost all regions are indicated as having

potential in agro-processing and in

logistics;

• Very few regions are prioritized for higher

education or wine-making;

• None of the regions are listed with

potential for manufacturing.

For a policymaker, there are three critical

questions: Are these proposed specializations

realistic; Are they sufficient to guide investment

choices; and Will they be effective in achieving

their intended goals?

(i) Are the specializations realistic? The

proposed regional specializations will

need to be more selective. Georgia is

unlikely to have sufficient resources to

invest in tourism development, renewable

energy, and agro-processing equally in all

regions; nor is it realistic that all regions

would have equivalent potential in these

sectors. There might also be some doubt

that no region has potential in

manufacturing, despite the presence, for

example, of light manufacturing of

apparel in Batumi, Tbilisi and Kutaisi11.

Arguably the only truly strategic

proposals are to focus resources for higher

education and wine-making on three

regions which have special potential. A

similar regional selectivity should be

made in the other proposed sectors.

(ii) Are the specializations sufficient to

guide investment choices? A further

analysis of constraints on each

economic sector will be required. The

RDP 2018-2021 advocates a wide range

of interventions, such as infrastructure,

workforce skills, and access to finance—

but Ministries and agencies will need to

determine investment plans for specific

interventions, including what kind of

infrastructure/skills/finance will be

invested in. For instance: should agro-

processing infrastructure focus on

irrigation infrastructure, post-harvest

infrastructure of warehouses and cold

storage, transport and logistics

infrastructure, or all of the above, or

Box 1: Views on regional economic development

The World Bank Group has accumulated institutional

knowledge on subnational economic development through

analytic work and operations.

Main insights on ‘good practice’ include:

- World Development Report 2009: ‘Reshaping

Economic Geography’6. This flagship report reviewed

the evidence that urbanization is a crucial part of

building the economic efficiencies that are part of

economic growth and development. It proposed a

policy framework of 3 I’s: countries should primarily

focus on universal provision of basic ‘Institutions’

(education, healthcare, water, sanitation, and similar

essentials). Once those are established, leading regions

will have emerged, and ‘Infrastructure’ can be planned

to link lagging to leading areas. ‘Interventions’ such as

special regional development initiatives should be

considered only as a last resort, since they tend to be

risky to get right, and are inefficient. This paradigm has

informed the preparation of Urbanization Reviews7 in

many countries including Georgia, to benchmark each

country’s urban evolution against those three I’s, and to

recommend priority actions. The Georgia Urbanization

Review 8 recommended improvements in land

management systems, increased local government

capacity, and a ‘systems of cities’ approach to leverage

the economic specializations of Georgia’s major cities.

- Competitive Cities for Jobs and Growth9 provides a

knowledge base on competitiveness interventions at the

city and subnational levels. The report reviews the

experience of secondary cities around the world which

have outperformed their national economies. It

proposes four pillars for interventions to facilitate

increased productivity and competitiveness in city

economies: Institutions & Regulation; Infrastructure &

Land; Skills & Innovation; and Enterprise Support &

Finance. The report also highlights the crucial role of

public-private dialogue and creating a local growth

coalition; and in establishing an efficient

implementation structure to get action on the ground.

- A report on lagging regions across the European

Union10. Across Europe, inequalities between countries

are declining, but inequalities within countries are

growing. The report recommends focusing on equality

of opportunity and maximizing potential of each region.

Five policy priorities are: (i) addressing macro

weaknesses that hinder regional potential; (ii)

improving the regional business environment; (iii)

leveraging the productive potential of cities; (iv)

investing in workforce skills; and (b) strengthening local

governments and institutions.

- Analytic and operational work on lagging regions in

Europe, working closely with the European

Commission DG REGIO (the Directorate General for

Regional and Urban Policy). Projects have included: the

‘Catch-Up Regions’ projects in Poland and Slovakia;

the Danube Delta Integrated Territorial Investment (ITI)

in Romania; innovation programs at the subnational

level in Romania; and ‘Growth and Jobs in Eastern

Croatia’.

11

something else? Those choices should be informed by an analysis of each proposed economic sector

proposed to have a regional ‘potential’ (see Table 1, above), so that the interventions are configured

to release binding constraints on growth and development. For example, some regions may have

potential in citrus and tea, while others have potential in herbs, honey, or nuts. Different crops may

have different investment needs. These choices will be needed quickly, since the timespan of the

RDP is only three years, and there is insufficient time to invest in the full list of interventions

envisaged in the document12. Much of this analysis may be derived from the industry studies and

value chain studies already carried out by the Government and various other organizations in

Georgia. The results of those studies could be consolidated and leveraged by the implementers of

the RDP 2018-2021 to guide investment choices.

(iii) Will the investments be effective in achieving their goals? An appraisal of main proposed

investments will be necessary to ensure they are cost-effective and mitigate risks to meet their

goals. The RDP includes a diagnostic of the main dimensions of economic development—including

infrastructure, businesses, innovation, skills, and social services—but does not include an appraisal

of the feasibility for growth in each of the identified industries. For example, the RDP includes a

proposal for economic growth based on the logistics sector, but does not explain how logistics drives

growth. Presumably demand for logistics is derived from demand for consumer and industry goods,

so the logistics industry will grow only if other industries are growing. Additionally: would value

be derived from logistics services, or would goods simply transit Georgia on their way to larger

markets? And would logistics companies shipping freight find it more efficient to route through

Georgia or the South Caucasus compared to other routes? Appraisals would also examine if the

proposed interventions are the most optimal amongst alternatives. For example: to increase

productivity and competitiveness of firms in multiple sectors, a key constraint is often a lack of

managerial skills in private firms. Based on surveys in multiple countries, it seems that management

practices explain around 30 percent of the cross-country gap in total factor productivity—and as

much as 40 percent or more in countries such as Poland, Sweden, or Italy13. But managerial skills

are not mentioned in the RDP. Overall, these analyses—a clear theory of change, and an appraisal

of the proposed interventions—will be crucial to ensure that interventions achieve their intended

goals.

b. Are regions the best scale for analysis and action?

The RDP focuses on regions as the main unit of analysis and action. The choice of a regional scale

(rather than municipal or other spatial scale) is not explained clearly in the RDP, but may be connected with

the political economy of national-local government relations. Georgia’s 12 regions each have a regional

administration headed by a State commissioner, appointed by the Government of Georgia. By contrast, its

64 municipalities are controlled by Sakrebulo councils that are elected by local communities, and the five

largest cities have directly-elected Meri (mayors). This structure implies a political economy in which the

central Government will usually have a stronger link to regional administrations, which it appoints. The

6 World Bank (2008), World Development Report 2009: Reshaping Economic Geography, Washington DC: World Bank. 7 World Bank (2013), Planning, Connecting, and Financing Cities—Now: What city leaders need to know, Washington DC: World

Bank. 8 World Bank (2014), Georgia Urbanization Review: towards an urban sector strategy, report 86240 rev. 9 World Bank (2015), Competitive Cities for Jobs and Growth: What, Who, and How, Washington DC: World Bank. 10 Farole, Goga & Ionescu-Heroiu (2018), Rethinking Lagging Regions: using cohesion policy to deliver on the potential of

Europe’s regions, Washington DC: World Bank. http://pubdocs.worldbank.org/en/739811525697535701/RLR-FULL-online-2018-

05-01.pdf 11 The RDP mentions in its diagnostic section that industry and manufacturing are the most important economic activity sectors for

Kvemo-Kartli, Shida Kartli and Mtskheta-Mitaneti regions (constituting 25-31 percent of the gross value added), but does not list

manufacturing as having economic potential in any of the regions. 12 Some of these analyses may already be available in the strategies of line Ministries and other key documents. For example, the

agricultural specializations of each region in Georgia are summarized by crop and agricultural product in the Ministry of Regional

Development and Infrastructure’s regional development strategies for 2014-2021 produced in 2013—excerpted in World Bank

(2016), pp. 77-78. 13 Bloom, Sadun & Van Reenen (2017), ‘Management as a Technology?’, National Bureau of Economic Research Working Paper

22327, https://www.nber.org/papers/w22327

12

focus on regional boundaries will also naturally resonate with Georgians, who consider their regions almost

akin to small states with different traditions, culture, food, and mentality.

However, regions are not usually the most coherent scale for economic development. On one hand, the

European Union has channeled a substantial proportion of its regional development funds through the lens

of NUTS-2 regions14, especially for economic development through smart specialization. Yet cities are the

main nodes of economic growth: they are the natural scale for economic interactions. Agglomeration

economies play a substantial role in economic development—through ‘sharing, learning, and matching’ of

infrastructure, knowledge, and labor pools—to the extent that no country in the world has attained middle-

income status without moving to an urbanization level of around 45 percent or higher15. In other words:

cities, more than regions, are how economies function in practice. Accordingly the European Union is

presently transitioning towards strategies and interventions at the NUTS-3 level (the geographic scale below

regions). The 2021-2027 budget for European Union regional development funds emphasizes integrated

territorial interventions (ITIs) which can be focused on NUTS-3 administrative units. In Georgia, the choice

of regions as the scale for interventions will depend on how closely aligned they are with Georgia’s urban

and economic geography.

Georgia’s regions do include urban hubs, but overall the regional geographic boundaries do not align

with the urban network. Georgia is divided into 12 administrative and statistical regions, of substantially

differing sizes. The largest region (not counting Tbilisi) has 17 times as many inhabitants as smallest region.

All regions except Tbilisi and Adjara are predominantly rural, but there are nodal cities within each region.

The RDP recognizes there does exist a mismatch of administrative boundaries with economic activity: it

states that “in geographic terms, some socio-economic problems and potentials tend to cluster not necessarily

following the logic of administrative (or planning regions)…Black Sea Coastal Area, Tbilisi Functional Area

(Tbilisi, Mtskheta-Mtianeti, Kvemo Kartli), and high mountainous region” (page 11). However, the RDP

focuses on administrative regions, without a spatial lens within each region and across regions. If economic

activity is concentrated in nodes within each region, and often agglomerates across regional boundaries, how

could the RDP 2018-2021 framework be further nuanced to reflect this de facto economic geography?

In a revised approach during RDP 2022-2025, regions could take some actions, but with a spatial focus

on cities within each region plus a view across regional boundaries. In a city-focused framework, cities

would be prioritized as nodes for economic development, together with their economic hinterlands. Regions

would accept that economic activities are concentrated in cities, and therefore would plan strategic

interventions to leverage the potential of cities. The concentration of economic activities within each region

would need to be understood, to ensure that investments are not fragmented and disbursed thinly across the

whole area, but instead concentrated in the places where economic potential is highest.

The economic payoffs to the region will be driven by functional economic areas. Georgia has seven

urban centers with populations above 40,000: Tbilisi, Gori, Kutaisi, Batumi, Poti, Zugdidi-Anaklia, and

Rustavi. Telavi, Akhaltsikhe, Ozurgeti, Mtskheta, and perhaps Ambrolauri16 could be added, if each region

must have at least one designated urban center17. Each of these urban centers has a ‘functional economic

area’ around it: workers commute to jobs; farmers sell to urban markets; companies supply locally-traded

goods and services. A radius of 45-minute drive time could define the reach of each functional area, as a

typical upper bound for commuting and trading distance. When added together, this structure of urban

centers and functional economic areas covers 80-90 percent of Georgia’s population18. As shown in Figure

14 NUTS-2 is a statistical unit in the European Union, as an abbreviation of ‘Nomenclature of Territorial Units for Statistics’, level

2. Level 2 NUTS regions are typically provinces or other large regions within a country. The typical size for a NUTS-2 region is

two million inhabitants. 15 World Bank (2008), World Development Report 2009: Reshaping Economic Geography, Washington DC: World Bank, Figure 1. 16 The populations of these smaller municipalities are as follows: Telavi approximately 20,000; Akhalsikhe approximately 18,000;

Ozurgeti approximately 15,000; Mtskheta approximately 8,000; Ambrolauri approximately 2,500. 17 These 12 urban centers were earlier granted the status of ‘self-governing cities’ in Georgia’s Local Self-Government code,

approved by the Georgian parliament on February 5, 2014. Subsequently on June 30, 2017, the status of seven of these self-

governing cities was revoked, leaving only Tbilisi, Kutaisi, Rustavi, Poti, and Batumi. Summarized in Council of Europe (2018),

‘Local and regional democracy in Georgia’, Report on 35th Session, November 7, 2018. p.9.

https://rm.coe.int/CoERMPublicCommonSearchServices/DisplayDCTMContent?documentId=09000016808e551a 18 A very similar proposal has been made in NALAG (2013), ‘Decentralization, Region Development, Spatial Planning Aspects and

Policy Milestones for Georgia’, Tbilisi: National Association of Local Authorities of Georgia (NALAG), pp. 83-89.

13

3, all of these urban centers are within 20-40 kilometers of Georgia’s main east-west highway19, meaning

that they are all linked to each other.

Figure 3: Population density of self-governing units (left side) and distance from Georgia’s major highway (right side)

Source: Tbilisi State University and Jumpstart Georgia 2012, compiled for World Bank (2014) Georgia Urbanization

Review

This approach finds a balance between a focus on Georgia’s largest cities and a focus on all regions.

At certain times it has been proposed in Georgia to focus on the ‘Big Four’ cities: Tbilisi, Batumi, Kutaisi,

and Rustavi. That approach might be most efficient, but it is likely to sacrifice a degree of spatial equity,

since it covers only 41 percent of the country’s population. But a regional approach aiming to cover all

regions neglects the real-world structure of population and economic activity. The approach of functional

economic areas presented in this analysis proposes an intermediate framework, which brings some of the

benefits of both approaches. In other words, the emphasis on regions may be maintained because of

Georgia’s governance structure, but each region will need to focus on functional areas within their territory,

and to plan interventions with neighboring regions to leverage functional areas that span across

administrative boundaries.

The RDP does include a measure to support functional integration of urban areas of Georgia, but it is

tiny in relation to the other measures. The total budget for this measure is GEL 0.2 million, which may

imply it is not taken seriously. The measure provides for a pre-feasibility study of effective cooperation

systems in the functional areas of Georgia’s biggest cities, especially in the areas of spatial planning, basic

services and education, and business cooperation. Arguably the study should have been conducted before

the RDP was finalized, not during implementation, so that it could help configure all other measures of the

RDP. These initiatives could be greatly scaled-up in the RDP 2022-2025. Concerted attention will also

need to be given to implementation mechanisms, since local government capacity for economic development

is likely to be relatively low. In principle, implementation mechanisms might still be focused on regional

governments, but with a stronger set of criteria and filters for investments to take place at municipal level.

19 Indeed 68 percent of Georgia’s population lives within 20km of the national highway, and 81 percent lives within 40km of the

national highway.

14

2. Benchmarking and recommendations for subnational competitiveness

The purpose of this section is to clarify subnational competitiveness objectives in Georgia. It is based

on a benchmarking of subnational competitiveness outcomes, which can provide guidance for policymakers.

Strategies for regional economic development are notoriously contentious, and it will be impossible to

satisfy all experts on this topic. For some practitioners, the RDP approach is overly focused on achieving

spatial equity, in trying to find economic solutions for all regions, rather than focusing on healthcare,

education and governance and letting the market then take its course20. For other practitioners, spatial

interventions are acceptable, but the RDP approach could be criticized for overemphasizing the ability of

policymakers to accurately ‘pick’ economic sectors for regional specialization21.

Two key questions help resolve this uncertainty. The deep disagreements on regional development

paradigms will not be resolved anytime soon globally. However, we can shed light on their relevance in

Georgia by asking two key questions:

1. Does Georgia have an unusually severe problem in regional development? If not, then perhaps

the preoccupation with spatial equity is misplaced; but if yes, then policymakers are correct to try

to address this problem.

2. Are the proposed specializations realistic, compared to current economic activities? The risk of

‘picking’ the wrong sectors is decreased if they are based on an understanding of current economic

activities. How do the proposed specializations match up with current economic activities, by sector

and location?

The analysis in this section is shaped by the insights of the previous section: that municipalities rather than

regions are likely to be a better unit for analysis; and that strategic prioritization will need to be more detailed.

2.1. Does Georgia have an unusually severe problem in regional development?

Compared to other countries of similar size and income level, Georgia’s regional disparities are

unusually severe. The RDP repeatedly emphasizes the disparity between the growth and prosperity of

Tbilisi and the stagnation and poverty of the rest of Georgia. The divergence in the value added by region

is considered one of the biggest barriers to the growth and prosperity of the country, exacerbated by poor

connectivity and weak infrastructure in the majority of the country22. But are Georgia’s regional disparities

unusually severe, or are they a ‘normal’ part of any country’s development trajectory? We calculated the

variance in GDP per capita by region, as shown in Table 2. This regional data indicates that Georgia has a

substantially higher variation in regional economic outcomes than comparator countries. The coefficient of

variation in GDP per capita across regions23 is 0.4 in Georgia, 0.31 in Armenia, 0.29 in Turkey, 0.15 in

Poland, and 0.10 in Hungary. Bulgaria has a slightly higher coefficient of variation, at 0.44. The main driver

of this high regional inequality in Georgia is Tbilisi: Tbilisi produces 45-67 percent of Georgia’s gross value

added24, and receives 81 percent of its foreign investment25. The coefficient of variation in GDP per capita

falls to 0.28 if Tbilisi is excluded. The same table also shows the ratio of GDP per capita in the largest city

to average GDP per capita in each country. On this measure, Georgia’s situation is less severe than in Poland

or Hungary, and is comparable to Bulgaria.

20 See, for example, the approach advocated by World Bank (2008), World Development Report 2009: Reshaping Economic

Geography, Washington DC: World Bank. 21 See pp. 72-77 in Farole, Goga & Ionescu-Heroiu (2018), Rethinking Lagging Regions: using cohesion policy to deliver on the

potential of Europe’s regions, Washington DC: World Bank. http://pubdocs.worldbank.org/en/739811525697535701/RLR-FULL-

online-2018-05-01.pdf 22 The Regional Development Programme of Georgia 2018-2021 23 The coefficient of variation is a measure of the magnitude by which GDP per capita varies across regions. It is calculated as the

standard deviation of the values, divided by the mean. 24 Figures vary depending on the source of data. 45 percent is taken from Geostat survey results. 67 percent appeared in a

presentation of the Georgian Ministry of Regional Development and Infrastructure. 25 Giorgobiani, Mzia (2019), ‘Regional Development Policy in Georgia’, presentation at European Week of Regions & Cities,

Brussels, 7-10 October 2019.

15

Table 2: Coefficient of variation in Georgia and for comparator countries26

Number

of

regions

Population

(millions,

2019)

Population

in the

largest city

(%)

National

GDP per

capita

(2018)

GDP per

capita in

the largest

city

Coefficient of

variation of

GDP per

capita across

regions

Proportion

of national

GDP in the

largest city

(%)

Georgia* 11 3.73 32 $4,717 $7,816 0.40 45

Armenia* 11 2.97 61 $4,212 -- 0.31 --

Bulgaria 29 7 18 $9,272 $15,657 0.44 40

Hungary 8 9.77 18 $16,161 $34,038 0.10 36

Poland 17 37.97 5 $15, 420 $34,770 0.15 17

Turkey 25 82 18 $9,370 $11,747 0.29 31 Note: * indicates nominal monthly wages at the regional level were used to compare regional inequality. -- denotes data not available.

GDP per capita at the urban level is from 2016 data for Bulgaria, 2017 data for Turkey and uses 2018 data for Georgia and Hungary. Regional

monthly wage distribution is based on 2018 data for Armenia and 2017 data for Georgia.

Sources: Geostat, World Bank, Organization for Economic Cooperation and Development (OECD), National Statistical Institute of Bulgaria, Turkish Statistical Institute, European Commission

The structure of economic activity is dramatically different between the capital city and Georgia’s

regions. As shown in Figure 4, in Tbilisi, nearly 70 percent of the population are formally employed, 13

percent are self-employed, and 17 percent are unemployed. Outside of Tbilisi, only around 30 percent of

the population are formally employed, while fully 60 percent are categorized as self-employed.27 Either this

implies a strong spirit of entrepreneurship outside the capital city, or—more likely—it implies a reliance on

survival entrepreneurship, i.e. any activities that will provide a minimal income. In other words, there is a

profound lack of formal jobs in most areas outside Tbilisi. A strategy of regional economic development

should take this finding into account: the companies that can generate economic growth mostly do not exist

outside Tbilisi.

Figure 4: Labor force distribution at the regional level, 2019.

Source: World Bank analysis of Geostat survey data.

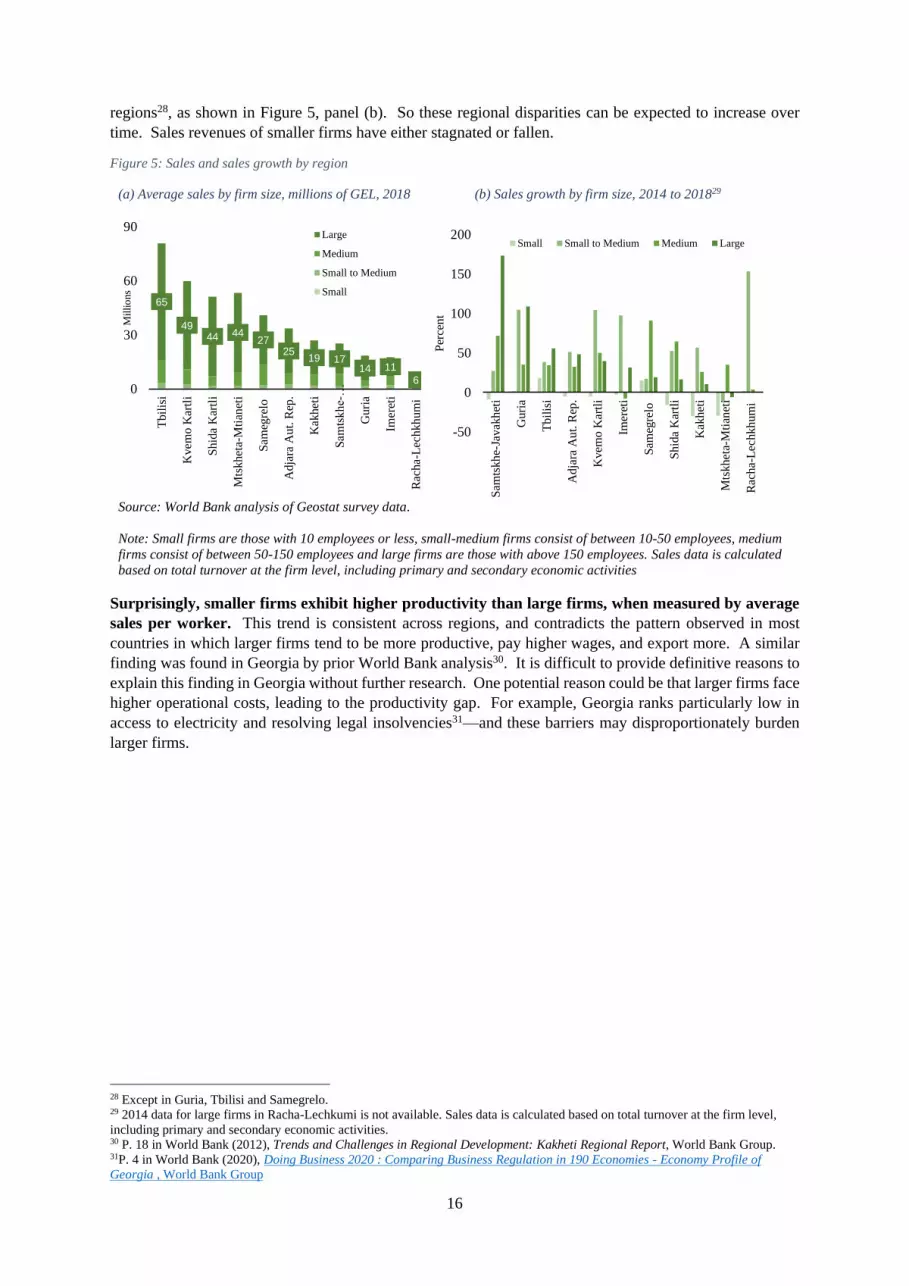

Georgia’s regional disparities have been shaped by the concentration of large firms in a few places.

Large firms are the primary driver of higher economic activity, and they are concentrated in Tbilisi and a

few other places, as shown in Figure 5, panel (a). In this sense, the locations of large firms underpin

Georgia’s regional economic disparities. Larger firms have also grown faster than other firms in almost all

26 The comparators were chosen for being neighboring countries, and/or for having similar levels of income or populations. The

analysis could be extended to other countries with similar income levels to Georgia, but regional economic data was not readily

available outside the OECD and EU countries. 27 Geostat Survey - Regional Statistics on Economic Activity 2019

69

39 3448

33 36 31 3241 36

0

20

40

60

80

100

Tb

ilisi

Sh

ida

Kart

li

Kvem

o K

art

li

Ad

jara

A/R

Sa

megre

lo

Imere

ti

Sa

mts

khe-J

ava

kheti

Guria

Mts

kheta

-Mtia

neti

Racha-L

ech

khum

i

Pe

rce

nt o

f to

tal la

bo

r fo

rce

Unemployed

Self-employed

Hired

16

regions28, as shown in Figure 5, panel (b). So these regional disparities can be expected to increase over

time. Sales revenues of smaller firms have either stagnated or fallen.

Figure 5: Sales and sales growth by region

(a) Average sales by firm size, millions of GEL, 2018 (b) Sales growth by firm size, 2014 to 201829

Source: World Bank analysis of Geostat survey data.

Note: Small firms are those with 10 employees or less, small-medium firms consist of between 10-50 employees, medium

firms consist of between 50-150 employees and large firms are those with above 150 employees. Sales data is calculated

based on total turnover at the firm level, including primary and secondary economic activities

Surprisingly, smaller firms exhibit higher productivity than large firms, when measured by average

sales per worker. This trend is consistent across regions, and contradicts the pattern observed in most

countries in which larger firms tend to be more productive, pay higher wages, and export more. A similar

finding was found in Georgia by prior World Bank analysis30. It is difficult to provide definitive reasons to

explain this finding in Georgia without further research. One potential reason could be that larger firms face

higher operational costs, leading to the productivity gap. For example, Georgia ranks particularly low in

access to electricity and resolving legal insolvencies31—and these barriers may disproportionately burden

larger firms.

28 Except in Guria, Tbilisi and Samegrelo. 29 2014 data for large firms in Racha-Lechkumi is not available. Sales data is calculated based on total turnover at the firm level,

including primary and secondary economic activities. 30 P. 18 in World Bank (2012), Trends and Challenges in Regional Development: Kakheti Regional Report, World Bank Group. 31P. 4 in World Bank (2020), Doing Business 2020 : Comparing Business Regulation in 190 Economies - Economy Profile of

Georgia , World Bank Group

65

4944 44

2725

19 1714 11

60

30

60

90

Tbil

isi

Kvem

o K

artl

i

Shid

a K

artl

i

Mts

khet

a-M

tian

eti

Sam

egre

lo

Adja

ra A

ut.

Rep

.

Kak

het

i

Sam

tskh

e-…

Guri

a

Imer

eti

Rac

ha-

Lec

hkh

um

i

Mil

lio

ns

Large

Medium

Small to Medium

Small

-50

0

50

100

150

200

Sam

tskh

e-Ja

vak

het

i

Guri

a

Tbil

isi

Adja

ra A

ut.

Rep

.

Kvem

o K

artl

i

Imer

eti

Sam

egre

lo

Shid

a K

artl

i

Kak

het

i

Mts

khet

a-M

tian

eti

Rac

ha-

Lec

hkh

um

i

Per

cen

t

Small Small to Medium Medium Large

17

Figure 6: Average productivity by firm size, thousand GELs per worker, 2018

Source: World Bank analysis of Geostat survey data. Sales data is calculated based on total turnover at the firm level,

including primary and secondary economic activities

This unusual trend in productivity levels changes when the analysis is restricted to only manufacturing

sectors. There are regional variations in productivity levels by firm size, where in 4 of the 11 regions, large

firms exhibit higher levels of productivity and in the remaining regions except Imereti, small-to-medium or

medium size firms are higher in productivity compared to small firms. Further research and between-sector

comparisons can provide insight into the experiences of types of firms across sectors.

Figure 7: Average productivity by firm size in manufacturing, thousand GELs per worker, 2018

Source: World Bank analysis of Geostat survey data. Sales data is calculated based on total turnover at the firm level/

0

100

200

300

400

500

600

700

Adja

ra A

ut.

Rep

.

Guri

a

Imer

eti

Kak

het

i

Kvem

o K

artl

i

Mts

khet

a-M

tian

eti

Rac

ha-

Lec

hkh

um

i

Sam

egre

lo a

nd Z

emo

Sam

tskh

e-Ja

vak

het

i

Shid

a K

artl

i

Tbil

isi

Small Small to Medium Medium Large

Sales per worker, thousands GEL

0

50

100

150

200

250

300

Adja

ra A

ut.

Rep

.

Guri

a

Imer

eti

Kak

het

i

Kvem

o K

artl

i

Mts

khet

a-M

tian

eti

Rac

ha

Sam

egre

lo a

nd Z

emo

Sam

tskh

e-Ja

vak

het

i

Shid

a K

artl

i

Tbil

isi

Small Small to Medium Medium Large

18

2.2. Where are the best opportunities for subnational growth?

In this section, two channels of analysis help determine how the regional economic specializations

proposed by the RDP might be optimized.

• First, we examine the location of the economic sectors proposed by the RDP.

• Second, we examine how this spatial landscape is changing over time, and where the future of

these sectors is likely to be.

These two analyses can be compared with the specializations proposed in the RDP.

Most analysis in this section is derived from the Geostat firm-level survey. The survey covers 5,000-6,000

firms and individual entrepreneurs for the years of 2014, 2015, 2016, 2017, and 2018. More information

on the survey is given in Appendix 1.

a. Where are Georgia’s tradable sectors currently concentrated in the regions?

Examining regional and firm-level data, the following observations can be noted:

(i) Tbilisi dominates all economic sectors except agriculture, forestry and fishing. Table 4 shows

industry output by region of Georgia, and clearly demonstrates the dominance of Tbilisi in all sectors

of the economy except agriculture. Some secondary nodes are visible: for example, Manufacturing

shows secondary nodes in Kvemo Kartli and Imereti; and Transport and Storage shows a secondary

node in Samegrelo32.

Table 4: GDP of all regions, 2018 (million GEL)

Source: World Bank analysis of Geostat 2018 regional statistics

(ii) However, in relative terms, each region has one or more economic specializations. Table 5

shows the relative specializations of each region of Georgia, by calculating location quotients33. For

32 In Agriculture, forestry and fishing, Kakheti dominates the sector. Indeed, 38 percent of all Georgia’s agricultural land is located

in Kakheti—according to Government of Georgia, Ministry of Regional Development and Infrastructure. (2013) ‘Kakheti Regional

Development Plan 2014-2021’. Secondary nodes for agriculture are in Kvemo Kartli, Imereti. Shida Kartli, and some other regions. 33 The methodology for these calculations is to divide the share of each industry in the regional economy by the share of each

industry in the national economy. The logic for this calculation is the same as for Revealed Comparative Advantage calculations

using export data. If the quotient is above 1 then the region specializes in that industry (relative to the region’s share in the national

economy), and if the number is below 1 then the industry is underrepresented in that region.

NACE rev.

2Economic Activities Tbilisi Adjara Guria Imereti Kakheti

Mtskheta-

MtianetiRacha

Samegrel

o

Samtskhe-

Javakheti

Kvemo

Kartli

Shida

KartliTOTAL

A Agriculture, forestry and fishing 44 145 83 414 741 80 40 299 269 522 379 3 016

B Mining and quarrying 189 19 6 56 24 21 3 20 24 82 14 457

C Manufacturing 1 625 167 50 481 205 185 23 171 206 707 120 3 940

D Electricity, gas, steam and air conditioning supply 404 42 12 120 51 46 6 42 51 176 30 980

E Water supply; sewerage, waste management, remediation 121 12 4 36 15 14 2 13 15 53 9 293

F Construction 2 185 581 24 91 39 15 9 74 71 85 39 3 213

G Wholesale and retail trade; repair of motor vehicles 4 160 372 35 246 81 29 4 136 50 195 99 5 406

H Transportation and storage 1 676 254 9 76 8 15 1 353 7 51 11 2 462

I Accommodation and food service activities 1 113 319 38 65 52 80 10 38 63 19 3 1 800

J Information and communication 763 73 5 63 26 19 4 32 14 48 31 1 077

K Financial and insurance activities 1 328 128 50 268 132 27 16 109 37 137 119 2 350

L Real estate activities 2 411 540 127 402 163 147 23 180 138 187 112 4 431

M Professional, scientific and technical activities 669 53 12 104 21 15 6 29 10 48 36 1 005

N Administrative and support service activities 289 50 5 49 23 20 3 9 9 32 23 510

O Public administration, defence, social security 1 082 236 63 384 129 94 23 241 93 323 232 2 900

P Education 583 168 54 274 139 42 16 137 76 146 104 1 740

Q Human health and social work activities 701 164 19 260 92 48 16 107 25 101 100 1 633

R Arts, entertainment and recreation 551 132 52 145 53 27 9 52 26 101 33 1 182

S Other service activities 160 30 3 48 21 7 3 21 14 23 16 347

T Activities of households as employers 11 5 2 6 1 0 0 5 0 3 2 37

(=) GDP at basic prices 20 064 3 492 651 3 587 2 018 932 214 2 068 1 200 3 040 1 514 38 779

(+) Taxes on products 3 120 543 101 558 314 145 33 322 187 473 235 6 031

(-) Subsidies on products 109 19 4 19 11 5 1 11 7 16 8 210

(=) GDP at market prices 23 075 4 016 749 4 126 2 320 1 072 246 2 378 1 380 3 496 1 741 44 599

19

example, Racha has a relative specialization in Agriculture, Forestry and Fishing; Education; Health

and Social Work; Household Activities; and some other sectors (where ‘location quotients’ are

above 1.0). Adjara has clear specializations in Construction, and Accommodation and Food Service

(as a proxy for Tourism). These specializations are not obvious from the absolute values of industry

output shown in Table 4: they appear only once relative sizes of the regional economies are

considered.

Table 5: Location quotients of all regions, 2018

Source: World Bank analysis of Geostat regional statistics

(iii) However, these regional economic specializations are not fully consistent with the potentials

proposed by the RDP. Table 6: Location quotients of all regions using firm-level data for

subsectors, 2018 shows location quotient calculations for the economic sectors proposed in the

RDP34. The table highlights the cells with location quotients above 1.0, indicating the regions with

disproportionately large shares of each industry. These can be compared with the economic

specializations proposed by the RDP, in green text.

Table 6: Location quotients of all regions using firm-level data for subsectors, 2018

Source: World Bank analysis of Geostat firm-level survey

Some observations can be made about the consistency of the RDP economic potentials with current

economic activities:

34 Close approximations are utilized; for example: ‘Tourism’ is accommodation and food services; ‘Logistics’ is Transportation and

storage; ‘Mining’ includes renewable energy sectors; ‘Higher education’ includes research and development and ‘Professional

Services’ include construction.

Economic Activities Tbilisi Adjara Guria Imereti KakhetiMtskheta-

MtianetiRacha Samegrelo

Samtskhe-

Javakheti

Kvemo

KartliShida Kartli

Agriculture, forestry and fishing 0.0 0.5 1.6 1.5 4.7 1.1 2.4 1.9 2.9 2.2 3.2

Mining and quarrying 0.8 0.5 0.8 1.3 1.0 2.0 1.0 0.8 1.7 2.3 0.8

Manufacturing 0.8 0.5 0.8 1.3 1.0 2.0 1.0 0.8 1.7 2.3 0.8

Electricity, gas, steam and air conditioning supply 0.8 0.5 0.8 1.3 1.0 2.0 1.0 0.8 1.7 2.3 0.8

Water supply; sewerage, waste management, remediation 0.8 0.5 0.8 1.3 1.0 2.0 1.0 0.8 1.7 2.3 0.8

Construction 1.3 2.0 0.5 0.3 0.2 0.2 0.5 0.4 0.7 0.3 0.3

Wholesale and retail trade; repair of motor vehicles 1.5 0.8 0.4 0.5 0.3 0.2 0.1 0.5 0.3 0.5 0.5

Transportation and storage 1.3 1.1 0.2 0.3 0.1 0.3 0.1 2.7 0.1 0.3 0.1

Accommodation and food service activities 1.2 2.0 1.2 0.4 0.6 1.8 1.0 0.4 1.1 0.1 0.0

Information and communication 1.4 0.8 0.3 0.6 0.5 0.7 0.6 0.5 0.4 0.6 0.7

Financial and insurance activities 1.1 0.6 1.3 1.2 1.1 0.5 1.2 0.9 0.5 0.7 1.3

Real estate activities 1.1 1.4 1.7 1.0 0.7 1.4 0.9 0.8 1.0 0.5 0.6

Professional, scientific and technical activities 1.3 0.6 0.7 1.1 0.4 0.6 1.1 0.5 0.3 0.6 0.9

Administrative and support service activities 1.1 1.1 0.5 1.0 0.9 1.6 1.0 0.3 0.6 0.8 1.1

Public administration, defence, social security 0.7 0.9 1.3 1.4 0.9 1.4 1.4 1.6 1.0 1.4 2.0

Education 0.6 1.1 1.8 1.7 1.5 1.0 1.7 1.5 1.4 1.1 1.5

Human health and social work activities 0.8 1.1 0.7 1.7 1.1 1.2 1.7 1.2 0.5 0.8 1.6

Arts, entertainment and recreation 0.9 1.2 2.6 1.3 0.9 1.0 1.3 0.8 0.7 1.1 0.7

Other service activities 0.9 1.0 0.5 1.5 1.2 0.8 1.5 1.1 1.3 0.9 1.2

Activities of households as employers 0.6 1.6 3.3 1.6 0.6 0.5 1.6 2.5 0.3 1.1 1.7

Tbilisi Adjara Guria Imereti KakhetiMtskheta-

MtianetiRacha Samegrelo

Samtskhe-

Javakheti

Kvemo

KartliShida Kartli

Agriculture 0.3 0.1 1.4 1.0 2.4 0.7 5.7 1.2 0.4 4.4 1.9

Agro-processing 1.1 0.0 0.1 0.1 3.1 2.9 1.4 0.5 3.1 0.0 0.7

Wine making 0.6 0.0 0.0 0.0 8.5 0.6 3.6 0.0 0.0 0.0 1.2

Tourism 1.4 1.4 2.3 0.5 0.2 1.1 0.8 0.1 1.6 0.1 0.2

Mining 0.1 0.6 8.4 7.0 1.3 1.7 7.9 0.7 2.3 1.7 1.6

Logistics 1.1 1.3 0.7 0.6 0.0 0.2 0.2 2.6 0.2 0.3 0.2

Higher education 1.5 1.2 0.1 0.5 0.0 0.0 0.0 0.0 0.1 0.4 0.3

Information Technology 1.5 0.1 0.0 0.5 0.1 0.1 0.0 0.0 0.1 0.1 3.6

Manufacturing 0.7 1.2 0.6 2.0 0.1 1.0 0.6 0.4 0.7 2.6 2.2

20

• Agro-processing is envisaged in the RDP to be an economic potential for 7 of 11 regions (all

except Adjara, Guria, Imereti, and Tbilisi). But economic data indicate that agro-processing is

concentrated in only three regions: Kakheti, Mtskheta Mtianeti, and Samtskhe-Javakheti;

• Tourism is envisaged in the RDP to be an economic potential for all regions; yet tourism

activities are weak in in Imereti, Kakheti, Racha, Samegrelo, Kvemo Kartli, and Shida Kartli.

(N.B. The low figures for tourism activities in some regions may be because activities like

wine-tasting and accommodation are conducted by enterprises for which wine-making is the

primary economic activity. So revenue is counted here under wine-making rather than

tourism).

• Wine-making is envisaged to be an economic potential in Kakheti, Shida Kartli, and Imereti

regions; yet wine-making is indicated not to be widespread in Imereti, and meanwhile is

indicated to be a relative specialization in Racha;

• Higher education and innovation is envisaged by the RDP to be an economic potential in

Tbilisi, Adjara, Kakheti, Samtskhe-Javakheti, and Imereti; yet the data indicates an existing

specialization only in Tbilisi and Adjara.

• Mining and renewable energy is envisaged in the RDP to be an economic potential for all 11

regions. However, activity is currently focused in Kvemo Kartli, Imereti, with very little in

other regions.

(iv) These surprising conclusions can be explained by looking within each region. ‘Regional’

economic potentials are concentrated in specific municipalities within each region. Maps are

shown in Figure 8 and Figure 9. For example:

• In Agro-processing, clear nodes exist around Georgia’s major cities, especially Tbilisi, Poti,

Zugdidi, Gori, Borjomi, and Telavi. But in 38 out of 64 municipalities, activity in agro-

processing is negligible (less than GEL 1 million in sales).

• Even in Agriculture, there are clear disparities between municipalities in rural areas, with

intense activity in some municipalities, but very low activity in others. For example,

municipalities of Chiatura, Ninotsminda, and Dusheti exhibit low activity, and municipalities

such as Sagarejo, Gardabani, Tetritskaro exhibit intense activity.

• In Tourism, there is a concentration in urban areas, plus some additional areas with mountains

or cultural heritage. Municipalities around Kazbegi, Svaneti, Gori, Borjomi, Telavi, and the

Black Sea coast have high tourism sales revenues, while neighboring municipalities even

within the same region have very low or zero revenues from tourism (such as Dedoplis Tskaro,

Aspindza, or Gardabani).

• In Wine-making, activity is concentrated in 1 out of 4 municipalities in Shida Kartli, and 3 out

of 12 in Imereti.

• Mining and renewable energy is highly concentrated in a few municipalities in each region.

• Higher education and innovation is concentrated in the larger cities in each region—i.e.

Tbilisi, Batumi, Kutaisi, Akhalsikhe, Rustavi, Telavi, Zugdidi, Gori, and a couple of others.

The confidence interval for these results is relatively wide, since the survey was not designed to be

representative by industry at the municipality level, so should be considered indicative rather than

conclusive.

21

Figure 8: Sales revenue by primary economic activity, 2018 (sectors mentioned in RDP)

Source: World Bank analysis of Geostat survey data

22

Figure 9: Sales revenue by primary economic activity, 2018 (additional sectors)

Source: World Bank analysis of Geostat survey data

b. How is regional concentration changing over time?

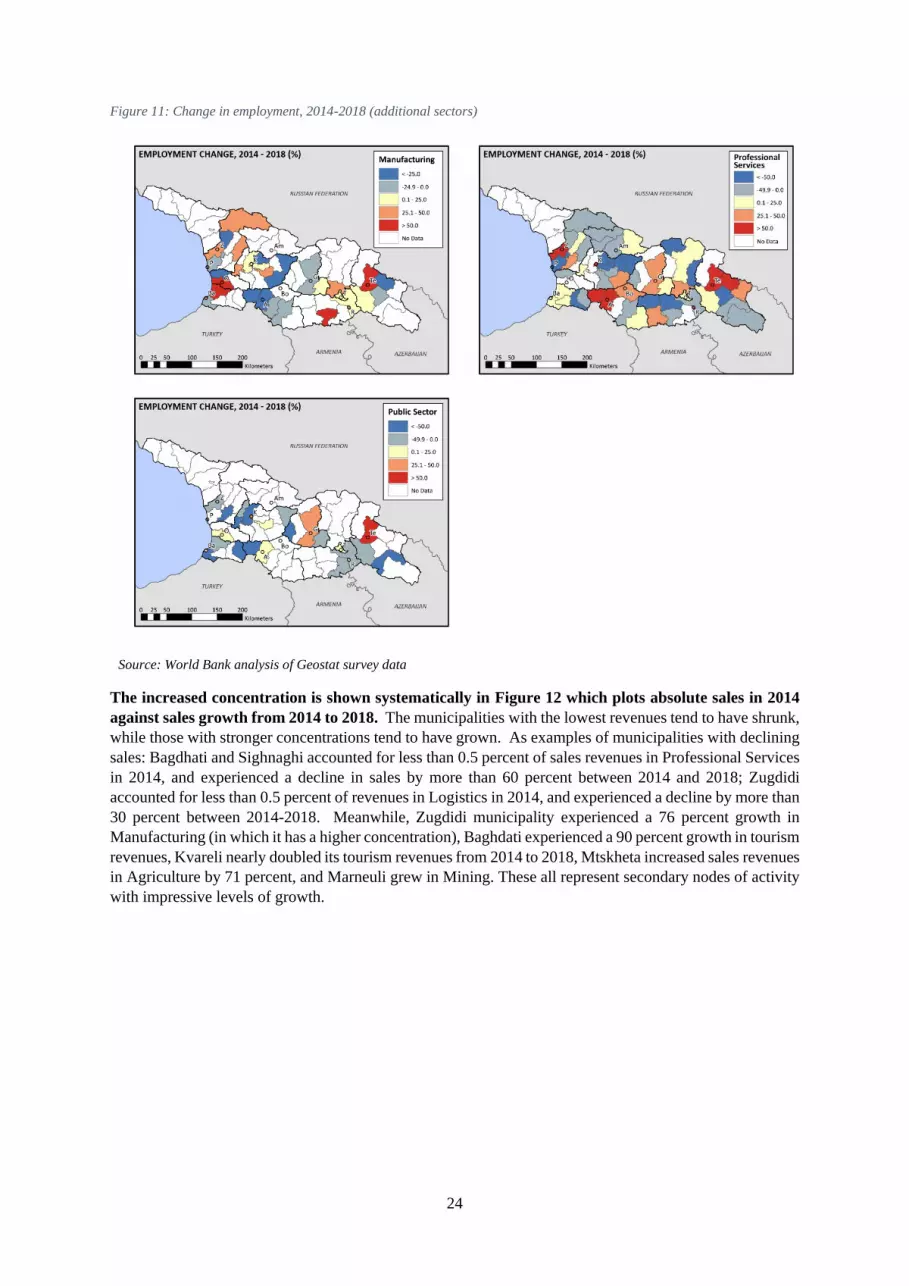

Examining data on employment and sales revenues, we find that sectoral concentrations are increasing

over time. Data on employment is shown in the maps in Figure 10 and Figure 11. Two main observations

can be made:

• None of the economic sectors are growing uniformly across the country. In all sectors, some

municipalities have shrunk in size while others have grown. For example in wine-making,

Ambrolauri and Gori have grown, while Akhmeta and Zestafoni municipalities have shrunk.

• Sectoral concentration has increased over time. For example, employment in tourism has grown

in the existing tourism nodes (Tbilisi, Kazbegi, Borjomi, Svaneti, Adjara, and some areas of

Kakheti) and has shrunk in rural non-mountainous areas, mostly along the east-west highway. As

another example, employment in agro-processing has grown in the existing nodes (some

municipalities of Kakheti, Shida Kartli and Svaneti) and has shrunk in other municipalities of those

same regions (mostly where it was not already strong).

23

Figure 10: Change in employment, 2014-2018 (sectors mentioned in RDP)

Source: World Bank analysis of Geostat survey data

24

Figure 11: Change in employment, 2014-2018 (additional sectors)

Source: World Bank analysis of Geostat survey data

The increased concentration is shown systematically in Figure 12 which plots absolute sales in 2014

against sales growth from 2014 to 2018. The municipalities with the lowest revenues tend to have shrunk,

while those with stronger concentrations tend to have grown. As examples of municipalities with declining

sales: Bagdhati and Sighnaghi accounted for less than 0.5 percent of sales revenues in Professional Services

in 2014, and experienced a decline in sales by more than 60 percent between 2014 and 2018; Zugdidi

accounted for less than 0.5 percent of revenues in Logistics in 2014, and experienced a decline by more than

30 percent between 2014-2018. Meanwhile, Zugdidi municipality experienced a 76 percent growth in

Manufacturing (in which it has a higher concentration), Baghdati experienced a 90 percent growth in tourism

revenues, Kvareli nearly doubled its tourism revenues from 2014 to 2018, Mtskheta increased sales revenues

in Agriculture by 71 percent, and Marneuli grew in Mining. These all represent secondary nodes of activity

with impressive levels of growth.

25

Figure 12: Sales revenues, 2018 and Growth in sales revenues, 2014-2018 (by municipality)

Source: World Bank analysis of Geostat survey data

N.B.: Observations with 2014 sales below 1,000,000 GEL were dropped to avoid misleading results from small sample

sizes. Observations with sales growth higher than 100 percent were also dropped, since they represent very small

municipalities where small additions or subtractions to sales revenues lead to huge changes in ‘growth’.

This trend of increasing concentration is supported by new investments, which have concentrated in

areas where economic activity in each sector is already strong. For example, Agro-processing

investments of more than 5 million GEL are almost always in municipalities where Agro-processing sales

are already above 5 million GEL. As another example, Tourism investments have concentrated in Batumi,

Borjomi, Kobuleti and Tbilisi—all places where sales and employment in the tourism sector have grown and

are among the leading municipalities in Tourism sales revenues. Investment in higher education has included

Telavi, Kutaisi, and Batumi, where the sector is growing; meanwhile other municipalities such as

Akhaltsikhe where employment and sales are shrinking have received lower investments.

-100

-80

-60

-40

-20

0

20

40

60

80

100G

row

th in

sal

es r

even

ues

20

14

-20

18

(%

)

Sales revenues, 2014(GEL)

Agriculture

Mining

Agro processing

Wine making

Manufacturing

Tourism

Logistics

InformationTechnologyHigher education

26

Figure 13: Total investment, 2014-2018 (sectors mentioned in RDP)

Source: World Bank analysis of Geostat survey data

27

Figure 14: Total investment, 2014-2018 (other sectors)

Source: World Bank analysis of Geostat survey data

Figure 15 shows this pattern systematically by plotting sales revenues against investments. Each

observation in the graph corresponds to a sector in a municipality, at the two-digit sector level. The

correlation between these two variables indicates municipalities with larger sales in a given sector received

more investment. We show investment over the full five year period (2014-2018) to avoid distorting the

values with investments that are lumpy from year to year.

Figure 15: Sales revenue in 2014 vs. Investment received 2014-2018, (by sector-municipality)

Source: World Bank analysis of Geostat data

Note: Sales revenue under 1 mil. Lari in 2014 are excluded from the data.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

Inve

stm

ent

(th

ou

san

ds

GEL

), 2

01

4-

20

18

Sales revenues (GEL), 2014

Mining

Wine making

Tourism

InformationTechnologyProfessional services

Agriculture

Agro-processing

Manufacturing, other

Logistics

28

Incidentally, this pattern does not hold when normalizing for absolute size of the municipality. Figure

16 plots sales per employee against investment per employee. Each observation in the graph corresponds to

a sector in a municipality, at the two-digit sector level. Sales per employee and investment per employee do

not appear to be correlated35; i.e. more ‘productive’ municipalities [by sales revenue per employee] do not

appear to receive a higher rate of investment per employee.

Figure 16. Sales per employee (2018) vs. Aggregated investment per employee (2014-2018)

Source: World Bank analysis of Geostat survey data