Embed Size (px)

Citation preview

1

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE CONSUMER PLAYBOOK

SALLY%LYONS%WYATT%Execu&ve(&(Prac&ce(Leader(

Consumer eating trends driving industry and

bakery growth

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%GAME%PLAN%

The(Equipment((Methodology)(

Top(Scores((Headlines)(

Past(and(Present(Teams((Ea&ng(Trends)(

Plays(of(the(Day((Millennials,(Hispanics,(H&W,(&(Retail)(

How(to(Win(Going(Forward((The(Strategy)(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%EQUIPMENT%

1 2 3Sales

Performance Shopping Behavior

Customer(AKtudes(

IRI Market Advantage™ 52 Weeks ending 1/24/16 – unless

noted otherwise

MULO+C = Food, Drug, MassX, Club, Dollar, Walmart, Military, and

Convenience

BAKERY = Bagels/Bialys, Bakery Snacks, English Muffins, Fresh Bread & Rolls, Pastry Doughnuts, Pies & Cakes

Technomic

IRI Consumer Network™ IRI 2015 Consumer Snacking Study

IRI 2013 Consumer Eating Study

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

TOP%SCORES%$1.3(Trillion(spent(in(ea&ng(and(drinking(in(a(diverse(landscape(

The(quest(for(simple(ingredients(and(fresh(products(is(

providing(opportuni&es(for(the(baking(community(to(

communicate(with(and(serve(American(shoppers(

Products(associated(with(nutri&on(fueling(growth(

Consumers(across(genera&ons(have(a(variety(of(ea&ng(

trends(that(will(impact(growth(over(the(next(5(years(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

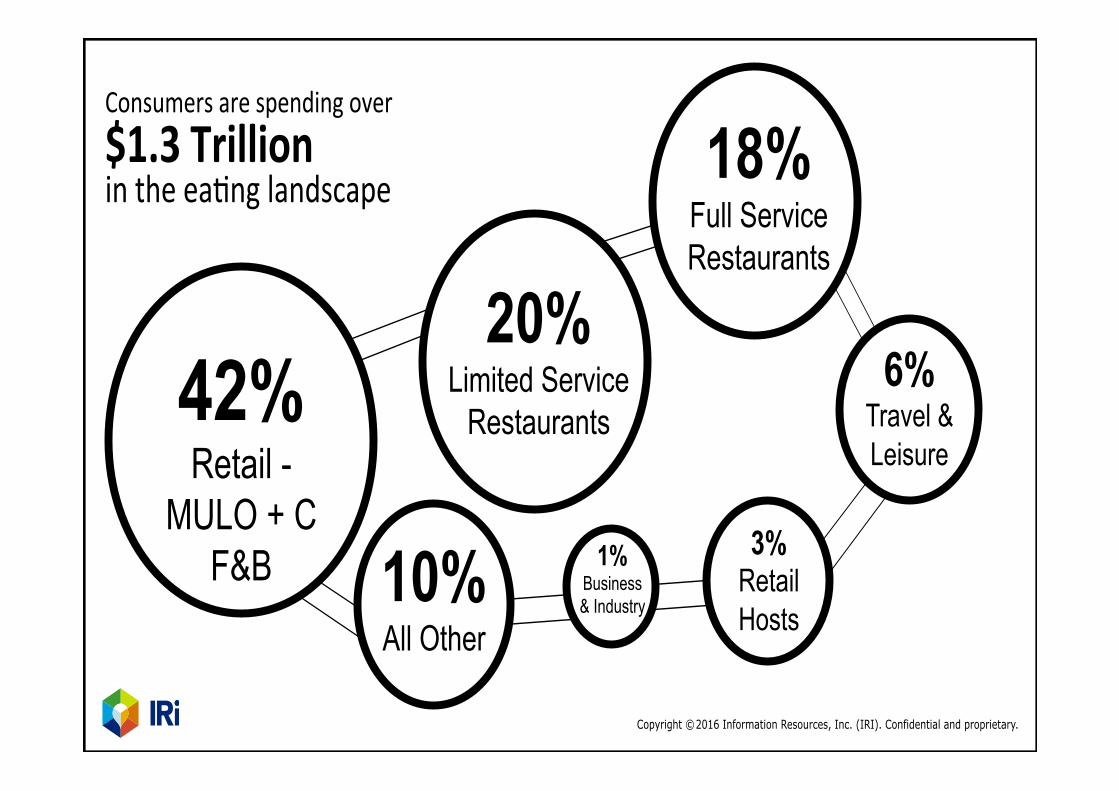

Consumers(are(spending(over(($1.3%Trillion%(in(the(ea&ng(landscape(

42% Retail -

MULO + C F&B

20% Limited Service

Restaurants 6%

Travel & Leisure

3% Retail Hosts

1% Business & Industry

18% Full Service Restaurants

10% All Other

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%EATING%LANDSCAPE%IS%DIVERSE%

Websites%

1

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE CONSUMER PLAYBOOK

SALLY%LYONS%WYATT%Execu&ve(&(Prac&ce(Leader(

Consumer eating trends driving industry and

bakery growth

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%GAME%PLAN%

The(Equipment((Methodology)(

Top(Scores((Headlines)(

Past(and(Present(Teams((Ea&ng(Trends)(

Plays(of(the(Day((Millennials,(Hispanics,(H&W,(&(Retail)(

How(to(Win(Going(Forward((The(Strategy)(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%EQUIPMENT%

1 2 3Sales

Performance Shopping Behavior

Customer(AKtudes(

IRI Market Advantage™ 52 Weeks ending 1/24/16 – unless

noted otherwise

MULO+C = Food, Drug, MassX, Club, Dollar, Walmart, Military, and

Convenience

BAKERY = Bagels/Bialys, Bakery Snacks, English Muffins, Fresh Bread & Rolls, Pastry Doughnuts, Pies & Cakes

Technomic

IRI Consumer Network™ IRI 2015 Consumer Snacking Study

IRI 2013 Consumer Eating Study

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

TOP%SCORES%$1.3(Trillion(spent(in(ea&ng(and(drinking(in(a(diverse(landscape(

The(quest(for(simple(ingredients(and(fresh(products(is(

providing(opportuni&es(for(the(baking(community(to(

communicate(with(and(serve(American(shoppers(

Products(associated(with(nutri&on(fueling(growth(

Consumers(across(genera&ons(have(a(variety(of(ea&ng(

trends(that(will(impact(growth(over(the(next(5(years(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Consumers(are(spending(over(($1.3%Trillion%(in(the(ea&ng(landscape(

42% Retail -

MULO + C F&B

20% Limited Service

Restaurants 6%

Travel & Leisure

3% Retail Hosts

1% Business & Industry

18% Full Service Restaurants

10% All Other

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%EATING%LANDSCAPE%IS%DIVERSE%

Websites%

1

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE CONSUMER PLAYBOOK

SALLY%LYONS%WYATT%Execu&ve(&(Prac&ce(Leader(

Consumer eating trends driving industry and

bakery growth

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%GAME%PLAN%

The(Equipment((Methodology)(

Top(Scores((Headlines)(

Past(and(Present(Teams((Ea&ng(Trends)(

Plays(of(the(Day((Millennials,(Hispanics,(H&W,(&(Retail)(

How(to(Win(Going(Forward((The(Strategy)(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%EQUIPMENT%

1 2 3Sales

Performance Shopping Behavior

Customer(AKtudes(

IRI Market Advantage™ 52 Weeks ending 1/24/16 – unless

noted otherwise

MULO+C = Food, Drug, MassX, Club, Dollar, Walmart, Military, and

Convenience

BAKERY = Bagels/Bialys, Bakery Snacks, English Muffins, Fresh Bread & Rolls, Pastry Doughnuts, Pies & Cakes

Technomic

IRI Consumer Network™ IRI 2015 Consumer Snacking Study

IRI 2013 Consumer Eating Study

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

TOP%SCORES%$1.3(Trillion(spent(in(ea&ng(and(drinking(in(a(diverse(landscape(

The(quest(for(simple(ingredients(and(fresh(products(is(

providing(opportuni&es(for(the(baking(community(to(

communicate(with(and(serve(American(shoppers(

Products(associated(with(nutri&on(fueling(growth(

Consumers(across(genera&ons(have(a(variety(of(ea&ng(

trends(that(will(impact(growth(over(the(next(5(years(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Consumers(are(spending(over(($1.3%Trillion%(in(the(ea&ng(landscape(

42% Retail -

MULO + C F&B

20% Limited Service

Restaurants 6%

Travel & Leisure

3% Retail Hosts

1% Business & Industry

18% Full Service Restaurants

10% All Other

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%EATING%LANDSCAPE%IS%DIVERSE%

Websites%

1

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE CONSUMER PLAYBOOK

SALLY%LYONS%WYATT%Execu&ve(&(Prac&ce(Leader(

Consumer eating trends driving industry and

bakery growth

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%GAME%PLAN%

The(Equipment((Methodology)(

Top(Scores((Headlines)(

Past(and(Present(Teams((Ea&ng(Trends)(

Plays(of(the(Day((Millennials,(Hispanics,(H&W,(&(Retail)(

How(to(Win(Going(Forward((The(Strategy)(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%EQUIPMENT%

1 2 3Sales

Performance Shopping Behavior

Customer(AKtudes(

IRI Market Advantage™ 52 Weeks ending 1/24/16 – unless

noted otherwise

MULO+C = Food, Drug, MassX, Club, Dollar, Walmart, Military, and

Convenience

BAKERY = Bagels/Bialys, Bakery Snacks, English Muffins, Fresh Bread & Rolls, Pastry Doughnuts, Pies & Cakes

Technomic

IRI Consumer Network™ IRI 2015 Consumer Snacking Study

IRI 2013 Consumer Eating Study

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

TOP%SCORES%$1.3(Trillion(spent(in(ea&ng(and(drinking(in(a(diverse(landscape(

The(quest(for(simple(ingredients(and(fresh(products(is(

providing(opportuni&es(for(the(baking(community(to(

communicate(with(and(serve(American(shoppers(

Products(associated(with(nutri&on(fueling(growth(

Consumers(across(genera&ons(have(a(variety(of(ea&ng(

trends(that(will(impact(growth(over(the(next(5(years(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Consumers(are(spending(over(($1.3%Trillion%(in(the(ea&ng(landscape(

42% Retail -

MULO + C F&B

20% Limited Service

Restaurants 6%

Travel & Leisure

3% Retail Hosts

1% Business & Industry

18% Full Service Restaurants

10% All Other

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%EATING%LANDSCAPE%IS%DIVERSE%

Websites%

1

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE CONSUMER PLAYBOOK

SALLY%LYONS%WYATT%Execu&ve(&(Prac&ce(Leader(

Consumer eating trends driving industry and

bakery growth

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%GAME%PLAN%

The(Equipment((Methodology)(

Top(Scores((Headlines)(

Past(and(Present(Teams((Ea&ng(Trends)(

Plays(of(the(Day((Millennials,(Hispanics,(H&W,(&(Retail)(

How(to(Win(Going(Forward((The(Strategy)(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%EQUIPMENT%

1 2 3Sales

Performance Shopping Behavior

Customer(AKtudes(

IRI Market Advantage™ 52 Weeks ending 1/24/16 – unless

noted otherwise

MULO+C = Food, Drug, MassX, Club, Dollar, Walmart, Military, and

Convenience

BAKERY = Bagels/Bialys, Bakery Snacks, English Muffins, Fresh Bread & Rolls, Pastry Doughnuts, Pies & Cakes

Technomic

IRI Consumer Network™ IRI 2015 Consumer Snacking Study

IRI 2013 Consumer Eating Study

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

TOP%SCORES%$1.3(Trillion(spent(in(ea&ng(and(drinking(in(a(diverse(landscape(

The(quest(for(simple(ingredients(and(fresh(products(is(

providing(opportuni&es(for(the(baking(community(to(

communicate(with(and(serve(American(shoppers(

Products(associated(with(nutri&on(fueling(growth(

Consumers(across(genera&ons(have(a(variety(of(ea&ng(

trends(that(will(impact(growth(over(the(next(5(years(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Consumers(are(spending(over(($1.3%Trillion%(in(the(ea&ng(landscape(

42% Retail -

MULO + C F&B

20% Limited Service

Restaurants 6%

Travel & Leisure

3% Retail Hosts

1% Business & Industry

18% Full Service Restaurants

10% All Other

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%EATING%LANDSCAPE%IS%DIVERSE%

Websites%

1

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE CONSUMER PLAYBOOK

SALLY%LYONS%WYATT%Execu&ve(&(Prac&ce(Leader(

Consumer eating trends driving industry and

bakery growth

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%GAME%PLAN%

The(Equipment((Methodology)(

Top(Scores((Headlines)(

Past(and(Present(Teams((Ea&ng(Trends)(

Plays(of(the(Day((Millennials,(Hispanics,(H&W,(&(Retail)(

How(to(Win(Going(Forward((The(Strategy)(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%EQUIPMENT%

1 2 3Sales

Performance Shopping Behavior

Customer(AKtudes(

IRI Market Advantage™ 52 Weeks ending 1/24/16 – unless

noted otherwise

MULO+C = Food, Drug, MassX, Club, Dollar, Walmart, Military, and

Convenience

BAKERY = Bagels/Bialys, Bakery Snacks, English Muffins, Fresh Bread & Rolls, Pastry Doughnuts, Pies & Cakes

Technomic

IRI Consumer Network™ IRI 2015 Consumer Snacking Study

IRI 2013 Consumer Eating Study

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

TOP%SCORES%$1.3(Trillion(spent(in(ea&ng(and(drinking(in(a(diverse(landscape(

The(quest(for(simple(ingredients(and(fresh(products(is(

providing(opportuni&es(for(the(baking(community(to(

communicate(with(and(serve(American(shoppers(

Products(associated(with(nutri&on(fueling(growth(

Consumers(across(genera&ons(have(a(variety(of(ea&ng(

trends(that(will(impact(growth(over(the(next(5(years(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Consumers(are(spending(over(($1.3%Trillion%(in(the(ea&ng(landscape(

42% Retail -

MULO + C F&B

20% Limited Service

Restaurants 6%

Travel & Leisure

3% Retail Hosts

1% Business & Industry

18% Full Service Restaurants

10% All Other

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%EATING%LANDSCAPE%IS%DIVERSE%

Websites%

2

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Food%Trucks%

THE%EATING%LANDSCAPE%IS%DIVERSE%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Restaurants%

THE%EATING%LANDSCAPE%IS%DIVERSE%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

VENDING%MACHINES%HAVE%EVOLVED%TO%ADDRESS%CONSUMER%NEEDS%AND%DEMAND%MOMENTS%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

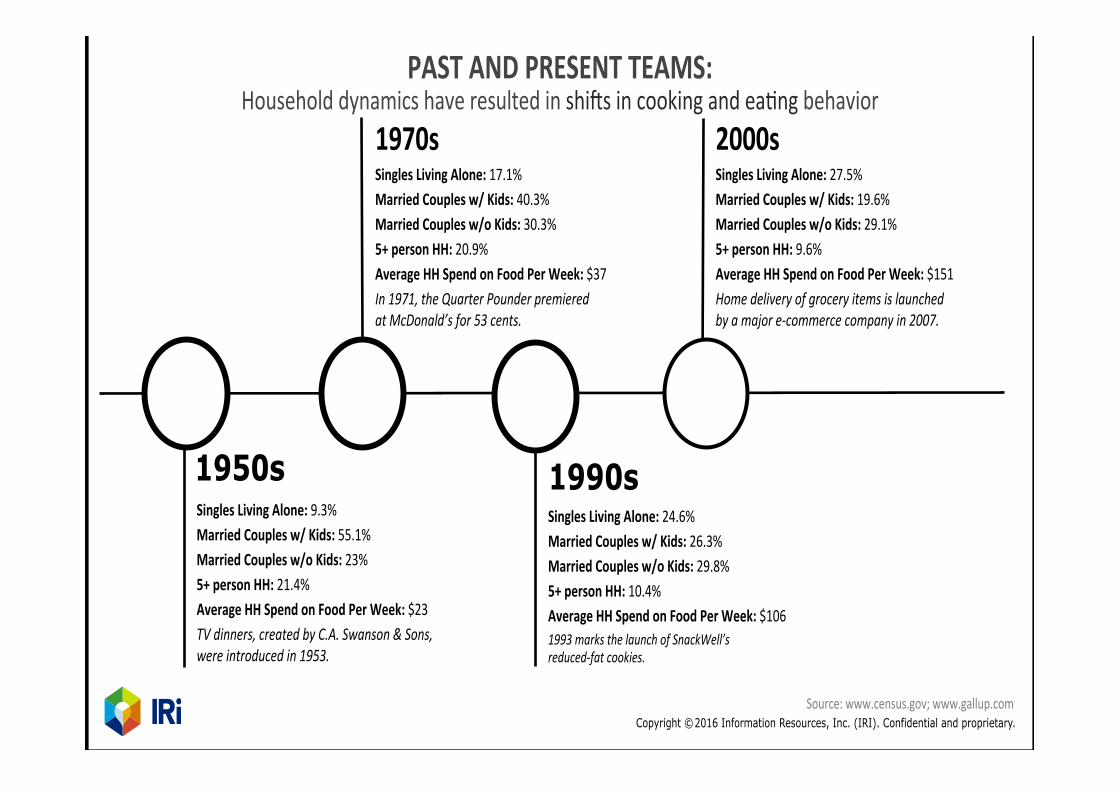

PAST%AND%PRESENT%TEAMS:%Household(dynamics(have(resulted(in(shiSs(in(cooking(and(ea&ng(behavior(

1950s Singles%Living%Alone:%9.3%(Married%Couples%w/%Kids:(55.1%(Married%Couples%w/o%Kids:(23%(5+%person%HH:(21.4%(Average%HH%Spend%on%Food%Per%Week:%$23(TV#dinners,#created#by#C.A.#Swanson#&#Sons,#were#introduced#in#1953.#

1970s%(Singles%Living%Alone:%17.1%(Married%Couples%w/%Kids:(40.3%(Married%Couples%w/o%Kids:(30.3%(5+%person%HH:(20.9%(Average%HH%Spend%on%Food%Per%Week:%$37(In#1971,#the#Quarter#Pounder#premiered#at#McDonald’s#for#53#cents.#

1990s Singles%Living%Alone:%24.6%(Married%Couples%w/%Kids:(26.3%(Married%Couples%w/o%Kids:(29.8%(5+%person%HH:(10.4%(Average%HH%Spend%on%Food%Per%Week:%$106(1993#marks#the#launch#of#SnackWell’s#reducedJfat#cookies.#

2000s%(Singles%Living%Alone:%27.5%(Married%Couples%w/%Kids:(19.6%(Married%Couples%w/o%Kids:(29.1%(5+%person%HH:(9.6%(Average%HH%Spend%on%Food%Per%Week:%$151(Home#delivery#of#grocery#items#is#launched#by#a#major#eJcommerce#company#in#2007.#

Source:(www.census.gov;(www.gallup.com(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

EVOLUTION%OF%%COOKING%AND%EATING%The%“Then”%Team%Tried and true family recipes

Three meals a day

Cooking as a chore

Source: WBTB Shopping Study, November 2014 Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

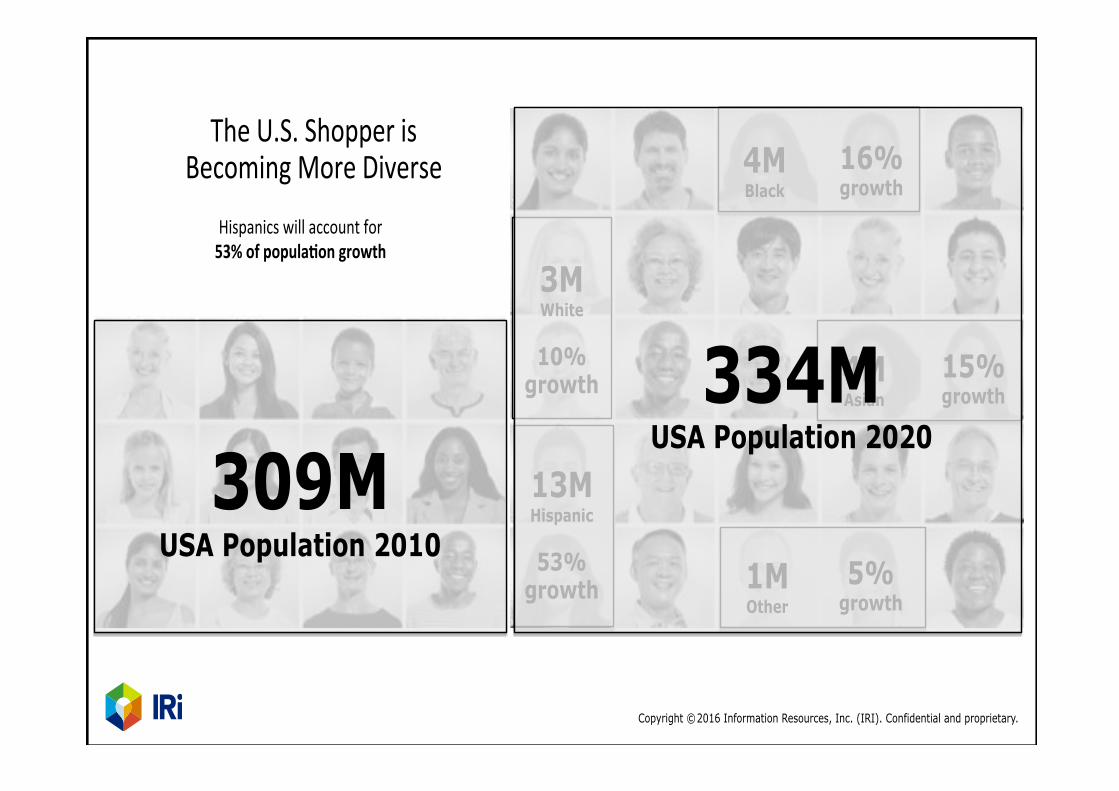

The(U.S.(Shopper(is((Becoming(More(Diverse(

309M USA Population 2010

3M White

10%

growth

13M Hispanic

53%

growth

4M Black

16% growth

4M Asian

15% growth

1M Other

5% growth

Hispanics(will(account(for((53%%of%popula\on%growth%

334M USA Population 2020

2

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Food%Trucks%

THE%EATING%LANDSCAPE%IS%DIVERSE%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Restaurants%

THE%EATING%LANDSCAPE%IS%DIVERSE%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

VENDING%MACHINES%HAVE%EVOLVED%TO%ADDRESS%CONSUMER%NEEDS%AND%DEMAND%MOMENTS%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PAST%AND%PRESENT%TEAMS:%Household(dynamics(have(resulted(in(shiSs(in(cooking(and(ea&ng(behavior(

1950s Singles%Living%Alone:%9.3%(Married%Couples%w/%Kids:(55.1%(Married%Couples%w/o%Kids:(23%(5+%person%HH:(21.4%(Average%HH%Spend%on%Food%Per%Week:%$23(TV#dinners,#created#by#C.A.#Swanson#&#Sons,#were#introduced#in#1953.#

1970s%(Singles%Living%Alone:%17.1%(Married%Couples%w/%Kids:(40.3%(Married%Couples%w/o%Kids:(30.3%(5+%person%HH:(20.9%(Average%HH%Spend%on%Food%Per%Week:%$37(In#1971,#the#Quarter#Pounder#premiered#at#McDonald’s#for#53#cents.#

1990s Singles%Living%Alone:%24.6%(Married%Couples%w/%Kids:(26.3%(Married%Couples%w/o%Kids:(29.8%(5+%person%HH:(10.4%(Average%HH%Spend%on%Food%Per%Week:%$106(1993#marks#the#launch#of#SnackWell’s#reducedJfat#cookies.#

2000s%(Singles%Living%Alone:%27.5%(Married%Couples%w/%Kids:(19.6%(Married%Couples%w/o%Kids:(29.1%(5+%person%HH:(9.6%(Average%HH%Spend%on%Food%Per%Week:%$151(Home#delivery#of#grocery#items#is#launched#by#a#major#eJcommerce#company#in#2007.#

Source:(www.census.gov;(www.gallup.com(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

EVOLUTION%OF%%COOKING%AND%EATING%The%“Then”%Team%Tried and true family recipes

Three meals a day

Cooking as a chore

Source: WBTB Shopping Study, November 2014 Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

The(U.S.(Shopper(is((Becoming(More(Diverse(

309M USA Population 2010

3M White

10%

growth

13M Hispanic

53%

growth

4M Black

16% growth

4M Asian

15% growth

1M Other

5% growth

Hispanics(will(account(for((53%%of%popula\on%growth%

334M USA Population 2020

2

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Food%Trucks%

THE%EATING%LANDSCAPE%IS%DIVERSE%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Restaurants%

THE%EATING%LANDSCAPE%IS%DIVERSE%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

VENDING%MACHINES%HAVE%EVOLVED%TO%ADDRESS%CONSUMER%NEEDS%AND%DEMAND%MOMENTS%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PAST%AND%PRESENT%TEAMS:%Household(dynamics(have(resulted(in(shiSs(in(cooking(and(ea&ng(behavior(

1950s Singles%Living%Alone:%9.3%(Married%Couples%w/%Kids:(55.1%(Married%Couples%w/o%Kids:(23%(5+%person%HH:(21.4%(Average%HH%Spend%on%Food%Per%Week:%$23(TV#dinners,#created#by#C.A.#Swanson#&#Sons,#were#introduced#in#1953.#

1970s%(Singles%Living%Alone:%17.1%(Married%Couples%w/%Kids:(40.3%(Married%Couples%w/o%Kids:(30.3%(5+%person%HH:(20.9%(Average%HH%Spend%on%Food%Per%Week:%$37(In#1971,#the#Quarter#Pounder#premiered#at#McDonald’s#for#53#cents.#

1990s Singles%Living%Alone:%24.6%(Married%Couples%w/%Kids:(26.3%(Married%Couples%w/o%Kids:(29.8%(5+%person%HH:(10.4%(Average%HH%Spend%on%Food%Per%Week:%$106(1993#marks#the#launch#of#SnackWell’s#reducedJfat#cookies.#

2000s%(Singles%Living%Alone:%27.5%(Married%Couples%w/%Kids:(19.6%(Married%Couples%w/o%Kids:(29.1%(5+%person%HH:(9.6%(Average%HH%Spend%on%Food%Per%Week:%$151(Home#delivery#of#grocery#items#is#launched#by#a#major#eJcommerce#company#in#2007.#

Source:(www.census.gov;(www.gallup.com(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

EVOLUTION%OF%%COOKING%AND%EATING%The%“Then”%Team%Tried and true family recipes

Three meals a day

Cooking as a chore

Source: WBTB Shopping Study, November 2014 Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

The(U.S.(Shopper(is((Becoming(More(Diverse(

309M USA Population 2010

3M White

10%

growth

13M Hispanic

53%

growth

4M Black

16% growth

4M Asian

15% growth

1M Other

5% growth

Hispanics(will(account(for((53%%of%popula\on%growth%

334M USA Population 2020

2

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Food%Trucks%

THE%EATING%LANDSCAPE%IS%DIVERSE%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Restaurants%

THE%EATING%LANDSCAPE%IS%DIVERSE%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

VENDING%MACHINES%HAVE%EVOLVED%TO%ADDRESS%CONSUMER%NEEDS%AND%DEMAND%MOMENTS%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PAST%AND%PRESENT%TEAMS:%Household(dynamics(have(resulted(in(shiSs(in(cooking(and(ea&ng(behavior(

1950s Singles%Living%Alone:%9.3%(Married%Couples%w/%Kids:(55.1%(Married%Couples%w/o%Kids:(23%(5+%person%HH:(21.4%(Average%HH%Spend%on%Food%Per%Week:%$23(TV#dinners,#created#by#C.A.#Swanson#&#Sons,#were#introduced#in#1953.#

1970s%(Singles%Living%Alone:%17.1%(Married%Couples%w/%Kids:(40.3%(Married%Couples%w/o%Kids:(30.3%(5+%person%HH:(20.9%(Average%HH%Spend%on%Food%Per%Week:%$37(In#1971,#the#Quarter#Pounder#premiered#at#McDonald’s#for#53#cents.#

1990s Singles%Living%Alone:%24.6%(Married%Couples%w/%Kids:(26.3%(Married%Couples%w/o%Kids:(29.8%(5+%person%HH:(10.4%(Average%HH%Spend%on%Food%Per%Week:%$106(1993#marks#the#launch#of#SnackWell’s#reducedJfat#cookies.#

2000s%(Singles%Living%Alone:%27.5%(Married%Couples%w/%Kids:(19.6%(Married%Couples%w/o%Kids:(29.1%(5+%person%HH:(9.6%(Average%HH%Spend%on%Food%Per%Week:%$151(Home#delivery#of#grocery#items#is#launched#by#a#major#eJcommerce#company#in#2007.#

Source:(www.census.gov;(www.gallup.com(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

EVOLUTION%OF%%COOKING%AND%EATING%The%“Then”%Team%Tried and true family recipes

Three meals a day

Cooking as a chore

Source: WBTB Shopping Study, November 2014 Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

The(U.S.(Shopper(is((Becoming(More(Diverse(

309M USA Population 2010

3M White

10%

growth

13M Hispanic

53%

growth

4M Black

16% growth

4M Asian

15% growth

1M Other

5% growth

Hispanics(will(account(for((53%%of%popula\on%growth%

334M USA Population 2020

2

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Food%Trucks%

THE%EATING%LANDSCAPE%IS%DIVERSE%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Restaurants%

THE%EATING%LANDSCAPE%IS%DIVERSE%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

VENDING%MACHINES%HAVE%EVOLVED%TO%ADDRESS%CONSUMER%NEEDS%AND%DEMAND%MOMENTS%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PAST%AND%PRESENT%TEAMS:%Household(dynamics(have(resulted(in(shiSs(in(cooking(and(ea&ng(behavior(

1950s Singles%Living%Alone:%9.3%(Married%Couples%w/%Kids:(55.1%(Married%Couples%w/o%Kids:(23%(5+%person%HH:(21.4%(Average%HH%Spend%on%Food%Per%Week:%$23(TV#dinners,#created#by#C.A.#Swanson#&#Sons,#were#introduced#in#1953.#

1970s%(Singles%Living%Alone:%17.1%(Married%Couples%w/%Kids:(40.3%(Married%Couples%w/o%Kids:(30.3%(5+%person%HH:(20.9%(Average%HH%Spend%on%Food%Per%Week:%$37(In#1971,#the#Quarter#Pounder#premiered#at#McDonald’s#for#53#cents.#

1990s Singles%Living%Alone:%24.6%(Married%Couples%w/%Kids:(26.3%(Married%Couples%w/o%Kids:(29.8%(5+%person%HH:(10.4%(Average%HH%Spend%on%Food%Per%Week:%$106(1993#marks#the#launch#of#SnackWell’s#reducedJfat#cookies.#

2000s%(Singles%Living%Alone:%27.5%(Married%Couples%w/%Kids:(19.6%(Married%Couples%w/o%Kids:(29.1%(5+%person%HH:(9.6%(Average%HH%Spend%on%Food%Per%Week:%$151(Home#delivery#of#grocery#items#is#launched#by#a#major#eJcommerce#company#in#2007.#

Source:(www.census.gov;(www.gallup.com(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

EVOLUTION%OF%%COOKING%AND%EATING%The%“Then”%Team%Tried and true family recipes

Three meals a day

Cooking as a chore

Source: WBTB Shopping Study, November 2014 Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

The(U.S.(Shopper(is((Becoming(More(Diverse(

309M USA Population 2010

3M White

10%

growth

13M Hispanic

53%

growth

4M Black

16% growth

4M Asian

15% growth

1M Other

5% growth

Hispanics(will(account(for((53%%of%popula\on%growth%

334M USA Population 2020

2

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Food%Trucks%

THE%EATING%LANDSCAPE%IS%DIVERSE%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Restaurants%

THE%EATING%LANDSCAPE%IS%DIVERSE%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

VENDING%MACHINES%HAVE%EVOLVED%TO%ADDRESS%CONSUMER%NEEDS%AND%DEMAND%MOMENTS%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PAST%AND%PRESENT%TEAMS:%Household(dynamics(have(resulted(in(shiSs(in(cooking(and(ea&ng(behavior(

1950s Singles%Living%Alone:%9.3%(Married%Couples%w/%Kids:(55.1%(Married%Couples%w/o%Kids:(23%(5+%person%HH:(21.4%(Average%HH%Spend%on%Food%Per%Week:%$23(TV#dinners,#created#by#C.A.#Swanson#&#Sons,#were#introduced#in#1953.#

1970s%(Singles%Living%Alone:%17.1%(Married%Couples%w/%Kids:(40.3%(Married%Couples%w/o%Kids:(30.3%(5+%person%HH:(20.9%(Average%HH%Spend%on%Food%Per%Week:%$37(In#1971,#the#Quarter#Pounder#premiered#at#McDonald’s#for#53#cents.#

1990s Singles%Living%Alone:%24.6%(Married%Couples%w/%Kids:(26.3%(Married%Couples%w/o%Kids:(29.8%(5+%person%HH:(10.4%(Average%HH%Spend%on%Food%Per%Week:%$106(1993#marks#the#launch#of#SnackWell’s#reducedJfat#cookies.#

2000s%(Singles%Living%Alone:%27.5%(Married%Couples%w/%Kids:(19.6%(Married%Couples%w/o%Kids:(29.1%(5+%person%HH:(9.6%(Average%HH%Spend%on%Food%Per%Week:%$151(Home#delivery#of#grocery#items#is#launched#by#a#major#eJcommerce#company#in#2007.#

Source:(www.census.gov;(www.gallup.com(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

EVOLUTION%OF%%COOKING%AND%EATING%The%“Then”%Team%Tried and true family recipes

Three meals a day

Cooking as a chore

Source: WBTB Shopping Study, November 2014 Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

The(U.S.(Shopper(is((Becoming(More(Diverse(

309M USA Population 2010

3M White

10%

growth

13M Hispanic

53%

growth

4M Black

16% growth

4M Asian

15% growth

1M Other

5% growth

Hispanics(will(account(for((53%%of%popula\on%growth%

334M USA Population 2020

3

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PLAYERS%HAVE%CHANGED%]%%More(people(working(and(not(re&ring(at(65(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Consumers(want(to(consume(fresher((foods(as(part(of(their(wellness(goals(

Source:(Na&onal(Consumer(Panel(Survey:(Total(US:(CY(2013(

Health and Wellness Trends Being physically fit & active Consuming fresher foods Consuming more Gluten-free foods Feeling good about yourself Portion control Buying organic / natural products Not being overweight Cooking at home / eating with family

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

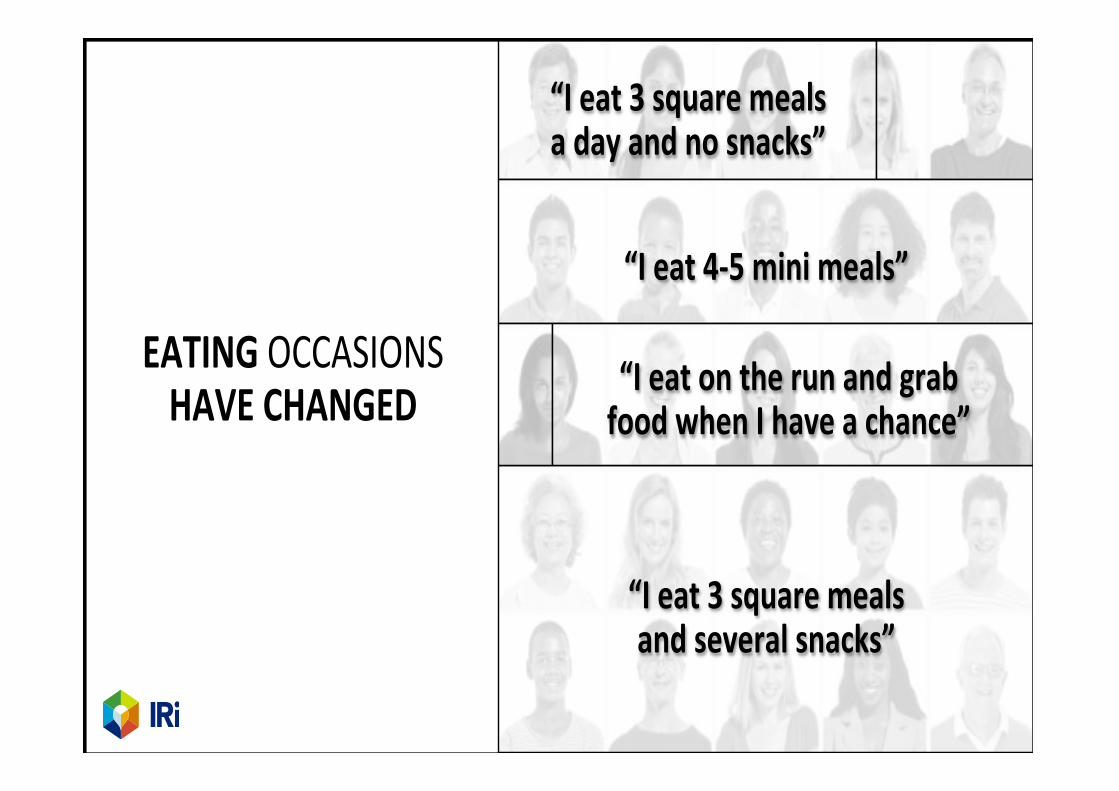

EATING%OCCASIONS(HAVE%CHANGED%

“I%eat%3%square%meals%%a%day%and%no%snacks”%

“I%eat%3%square%meals%and%several%snacks”%

“I%eat%4]5%mini%meals”%

“I%eat%on%the%run%and%grab%food%when%I%have%a%chance”%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

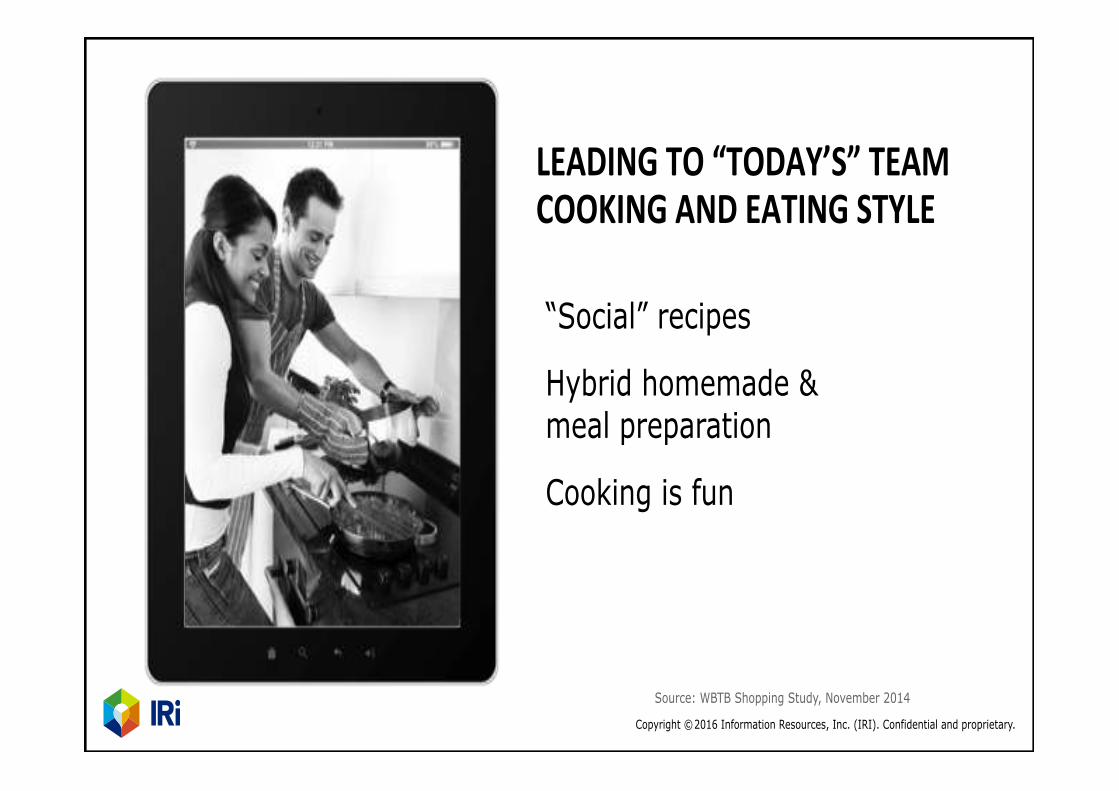

LEADING%TO%“TODAY’S”%TEAM%COOKING%AND%EATING%STYLE%

“Social” recipes

Hybrid homemade & meal preparation

Cooking is fun

Source: WBTB Shopping Study, November 2014

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

We are obsessed with food

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

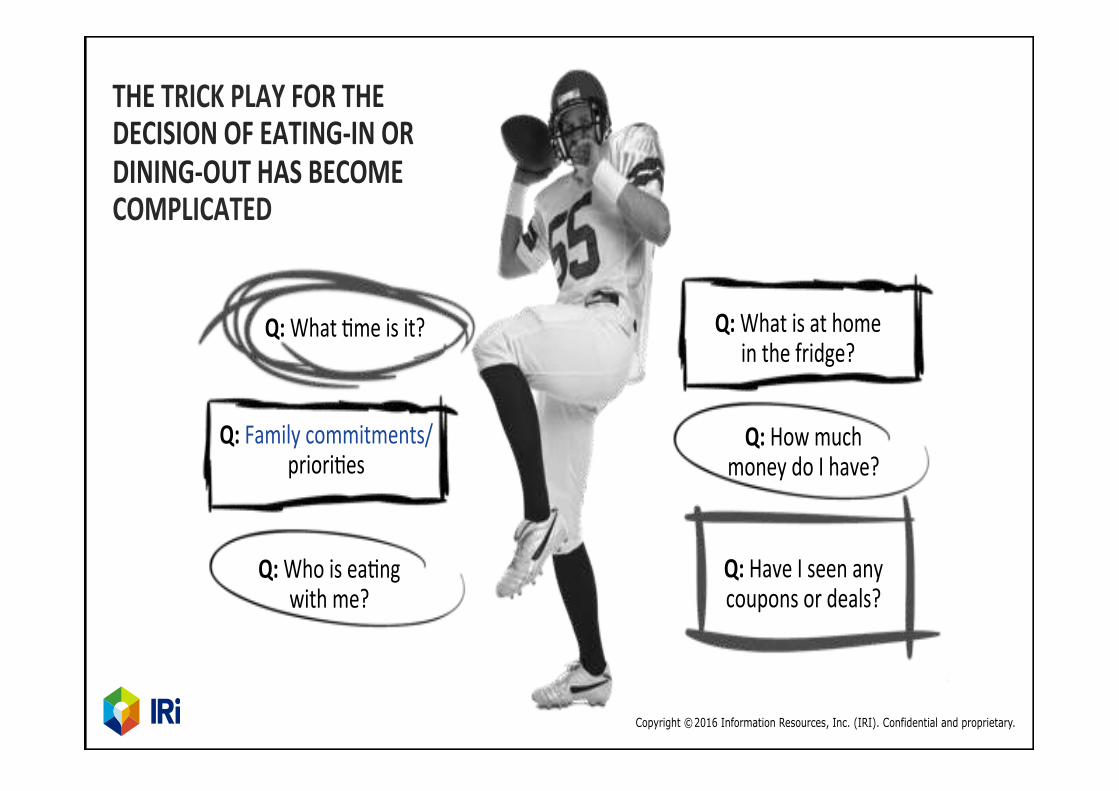

Q:%Family(commitments/(priori&es%

Q:%What(&me(is(it?%

Q:%Who(is(ea&ng((with(me?%

Q:%Have(I(seen(any((coupons(or(deals?%

Q:%What(is(at(home((in(the(fridge?%

Q:%How(much((money(do(I(have?%

THE%TRICK%PLAY%FOR%THE%DECISION%OF%EATING]IN%OR%DINING]OUT%HAS%BECOME%COMPLICATED%

3

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PLAYERS%HAVE%CHANGED%]%%More(people(working(and(not(re&ring(at(65(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Consumers(want(to(consume(fresher((foods(as(part(of(their(wellness(goals(

Source:(Na&onal(Consumer(Panel(Survey:(Total(US:(CY(2013(

Health and Wellness Trends Being physically fit & active Consuming fresher foods Consuming more Gluten-free foods Feeling good about yourself Portion control Buying organic / natural products Not being overweight Cooking at home / eating with family

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

EATING%OCCASIONS(HAVE%CHANGED%

“I%eat%3%square%meals%%a%day%and%no%snacks”%

“I%eat%3%square%meals%and%several%snacks”%

“I%eat%4]5%mini%meals”%

“I%eat%on%the%run%and%grab%food%when%I%have%a%chance”%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

LEADING%TO%“TODAY’S”%TEAM%COOKING%AND%EATING%STYLE%

“Social” recipes

Hybrid homemade & meal preparation

Cooking is fun

Source: WBTB Shopping Study, November 2014

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

We are obsessed with food

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Q:%Family(commitments/(priori&es%

Q:%What(&me(is(it?%

Q:%Who(is(ea&ng((with(me?%

Q:%Have(I(seen(any((coupons(or(deals?%

Q:%What(is(at(home((in(the(fridge?%

Q:%How(much((money(do(I(have?%

THE%TRICK%PLAY%FOR%THE%DECISION%OF%EATING]IN%OR%DINING]OUT%HAS%BECOME%COMPLICATED%

3

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PLAYERS%HAVE%CHANGED%]%%More(people(working(and(not(re&ring(at(65(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Consumers(want(to(consume(fresher((foods(as(part(of(their(wellness(goals(

Source:(Na&onal(Consumer(Panel(Survey:(Total(US:(CY(2013(

Health and Wellness Trends Being physically fit & active Consuming fresher foods Consuming more Gluten-free foods Feeling good about yourself Portion control Buying organic / natural products Not being overweight Cooking at home / eating with family

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

EATING%OCCASIONS(HAVE%CHANGED%

“I%eat%3%square%meals%%a%day%and%no%snacks”%

“I%eat%3%square%meals%and%several%snacks”%

“I%eat%4]5%mini%meals”%

“I%eat%on%the%run%and%grab%food%when%I%have%a%chance”%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

LEADING%TO%“TODAY’S”%TEAM%COOKING%AND%EATING%STYLE%

“Social” recipes

Hybrid homemade & meal preparation

Cooking is fun

Source: WBTB Shopping Study, November 2014

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

We are obsessed with food

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Q:%Family(commitments/(priori&es%

Q:%What(&me(is(it?%

Q:%Who(is(ea&ng((with(me?%

Q:%Have(I(seen(any((coupons(or(deals?%

Q:%What(is(at(home((in(the(fridge?%

Q:%How(much((money(do(I(have?%

THE%TRICK%PLAY%FOR%THE%DECISION%OF%EATING]IN%OR%DINING]OUT%HAS%BECOME%COMPLICATED%

3

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PLAYERS%HAVE%CHANGED%]%%More(people(working(and(not(re&ring(at(65(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Consumers(want(to(consume(fresher((foods(as(part(of(their(wellness(goals(

Source:(Na&onal(Consumer(Panel(Survey:(Total(US:(CY(2013(

Health and Wellness Trends Being physically fit & active Consuming fresher foods Consuming more Gluten-free foods Feeling good about yourself Portion control Buying organic / natural products Not being overweight Cooking at home / eating with family

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

EATING%OCCASIONS(HAVE%CHANGED%

“I%eat%3%square%meals%%a%day%and%no%snacks”%

“I%eat%3%square%meals%and%several%snacks”%

“I%eat%4]5%mini%meals”%

“I%eat%on%the%run%and%grab%food%when%I%have%a%chance”%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

LEADING%TO%“TODAY’S”%TEAM%COOKING%AND%EATING%STYLE%

“Social” recipes

Hybrid homemade & meal preparation

Cooking is fun

Source: WBTB Shopping Study, November 2014

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

We are obsessed with food

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Q:%Family(commitments/(priori&es%

Q:%What(&me(is(it?%

Q:%Who(is(ea&ng((with(me?%

Q:%Have(I(seen(any((coupons(or(deals?%

Q:%What(is(at(home((in(the(fridge?%

Q:%How(much((money(do(I(have?%

THE%TRICK%PLAY%FOR%THE%DECISION%OF%EATING]IN%OR%DINING]OUT%HAS%BECOME%COMPLICATED%

3

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PLAYERS%HAVE%CHANGED%]%%More(people(working(and(not(re&ring(at(65(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Consumers(want(to(consume(fresher((foods(as(part(of(their(wellness(goals(

Source:(Na&onal(Consumer(Panel(Survey:(Total(US:(CY(2013(

Health and Wellness Trends Being physically fit & active Consuming fresher foods Consuming more Gluten-free foods Feeling good about yourself Portion control Buying organic / natural products Not being overweight Cooking at home / eating with family

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

EATING%OCCASIONS(HAVE%CHANGED%

“I%eat%3%square%meals%%a%day%and%no%snacks”%

“I%eat%3%square%meals%and%several%snacks”%

“I%eat%4]5%mini%meals”%

“I%eat%on%the%run%and%grab%food%when%I%have%a%chance”%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

LEADING%TO%“TODAY’S”%TEAM%COOKING%AND%EATING%STYLE%

“Social” recipes

Hybrid homemade & meal preparation

Cooking is fun

Source: WBTB Shopping Study, November 2014

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

We are obsessed with food

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Q:%Family(commitments/(priori&es%

Q:%What(&me(is(it?%

Q:%Who(is(ea&ng((with(me?%

Q:%Have(I(seen(any((coupons(or(deals?%

Q:%What(is(at(home((in(the(fridge?%

Q:%How(much((money(do(I(have?%

THE%TRICK%PLAY%FOR%THE%DECISION%OF%EATING]IN%OR%DINING]OUT%HAS%BECOME%COMPLICATED%

3

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PLAYERS%HAVE%CHANGED%]%%More(people(working(and(not(re&ring(at(65(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Consumers(want(to(consume(fresher((foods(as(part(of(their(wellness(goals(

Source:(Na&onal(Consumer(Panel(Survey:(Total(US:(CY(2013(

Health and Wellness Trends Being physically fit & active Consuming fresher foods Consuming more Gluten-free foods Feeling good about yourself Portion control Buying organic / natural products Not being overweight Cooking at home / eating with family

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

EATING%OCCASIONS(HAVE%CHANGED%

“I%eat%3%square%meals%%a%day%and%no%snacks”%

“I%eat%3%square%meals%and%several%snacks”%

“I%eat%4]5%mini%meals”%

“I%eat%on%the%run%and%grab%food%when%I%have%a%chance”%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

LEADING%TO%“TODAY’S”%TEAM%COOKING%AND%EATING%STYLE%

“Social” recipes

Hybrid homemade & meal preparation

Cooking is fun

Source: WBTB Shopping Study, November 2014

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

We are obsessed with food

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Q:%Family(commitments/(priori&es%

Q:%What(&me(is(it?%

Q:%Who(is(ea&ng((with(me?%

Q:%Have(I(seen(any((coupons(or(deals?%

Q:%What(is(at(home((in(the(fridge?%

Q:%How(much((money(do(I(have?%

THE%TRICK%PLAY%FOR%THE%DECISION%OF%EATING]IN%OR%DINING]OUT%HAS%BECOME%COMPLICATED%

4

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

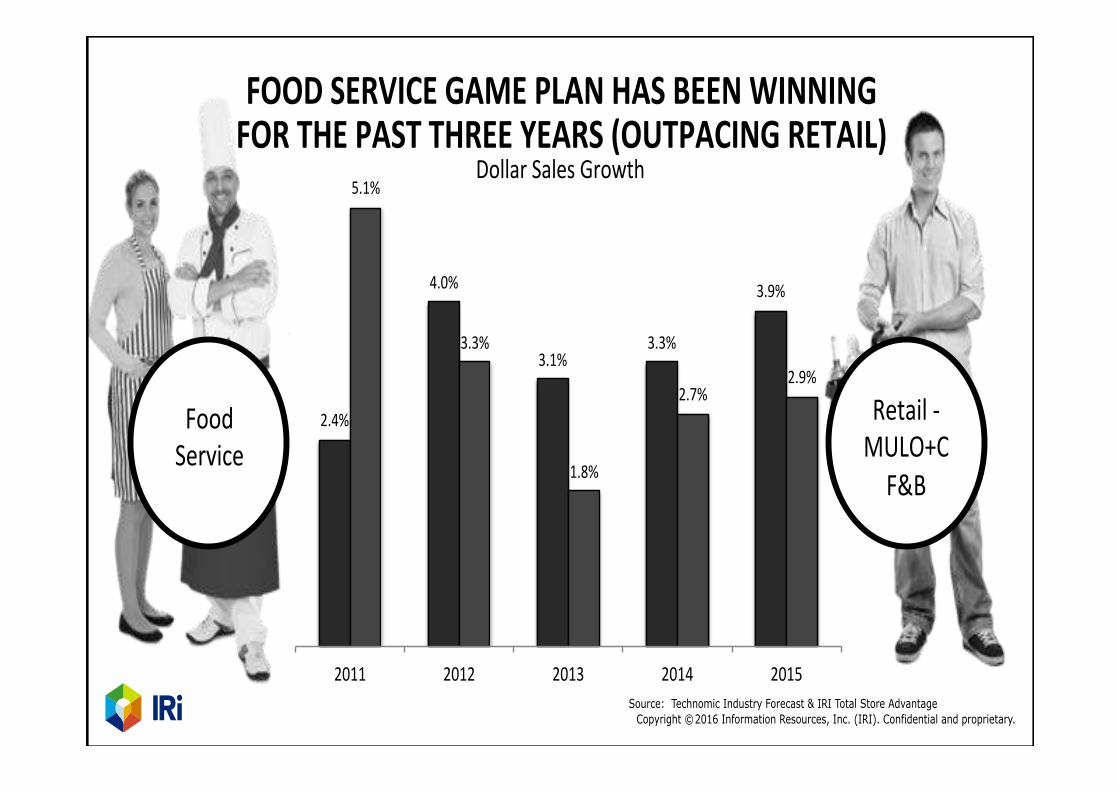

FOOD%SERVICE%GAME%PLAN%HAS%BEEN%WINNING%%FOR%THE%PAST%THREE%YEARS%(OUTPACING%RETAIL)%

Food((Service% Retail(f((

MULO+C(F&B(

2.4%(

4.0%(

3.1%(3.3%(

3.9%(

5.1%(

3.3%(

1.8%(

2.7%(2.9%(

2011( 2012( 2013( 2014( 2015(

Dollar(Sales(Growth(

Source: Technomic Industry Forecast & IRI Total Store Advantage Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

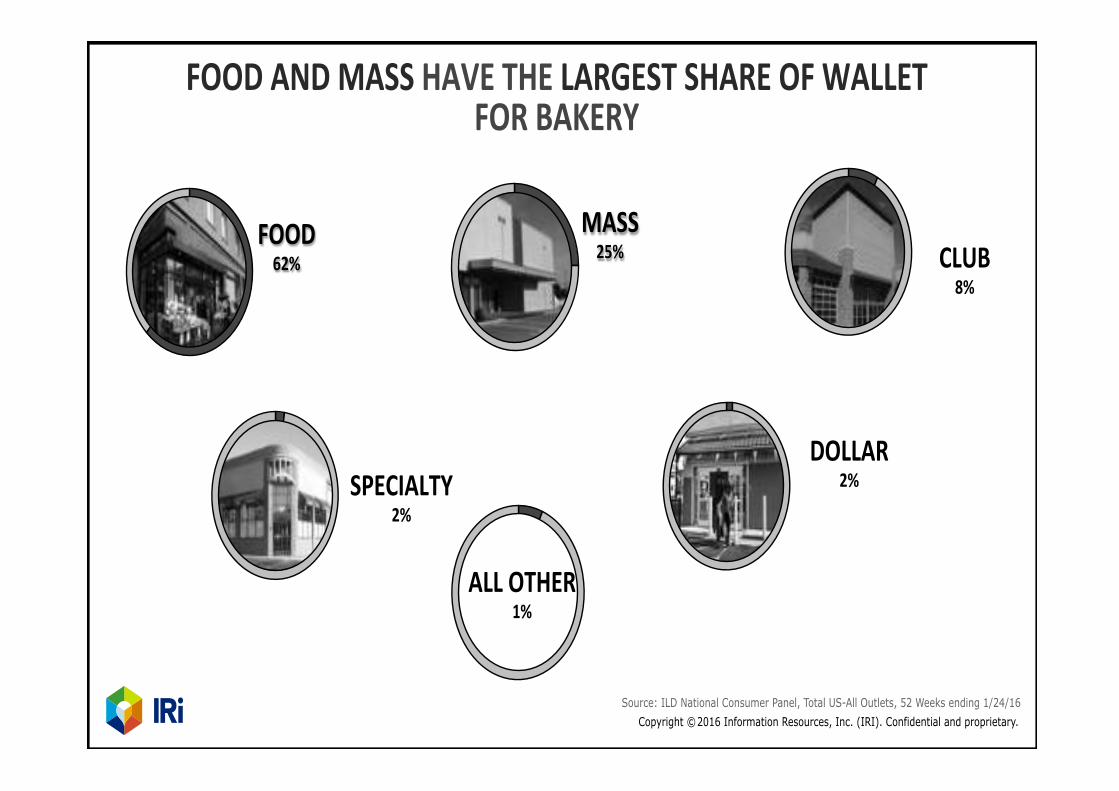

AT%RETAIL,%THE%PERIMETER%IS%BECOMING:%The(fulcrum(point(for(maximum(retail(differen&a&on((Base(for(deeper(and(more(engaging(customer(experiences((Focus(for(space(expansion(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

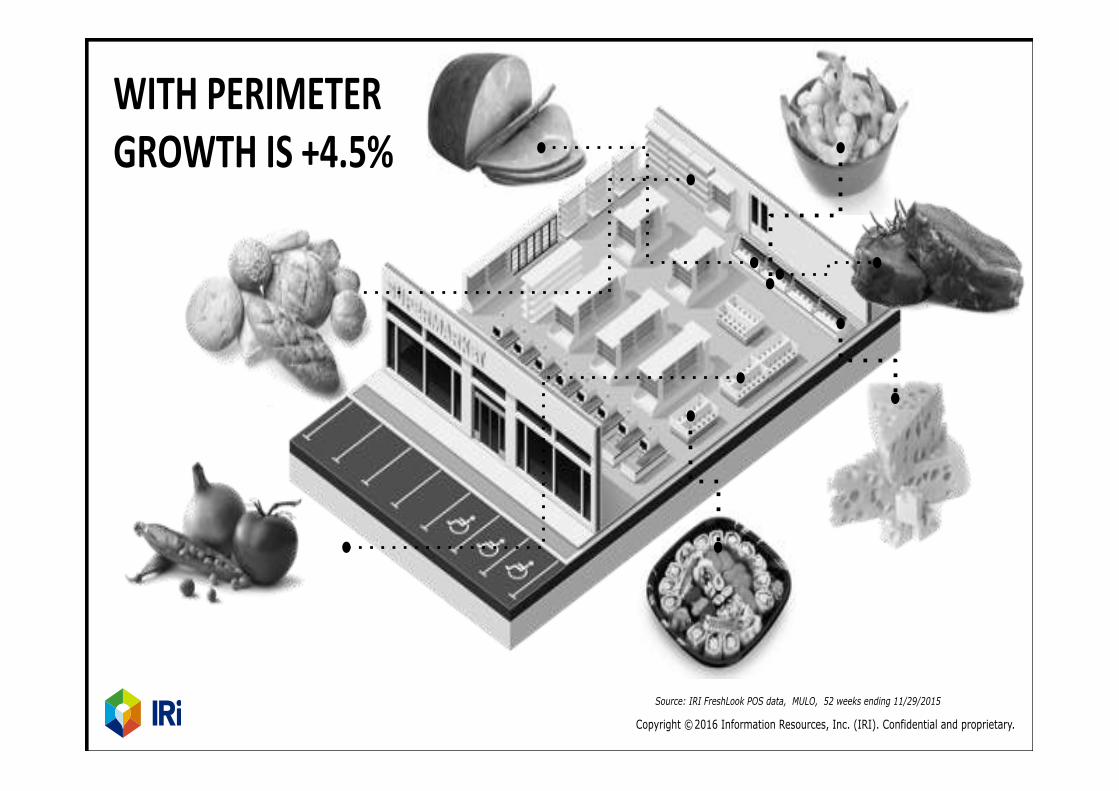

WITH%PERIMETER%GROWTH%IS%+4.5%%

Source: IRI FreshLook POS data, MULO, 52 weeks ending 11/29/2015

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

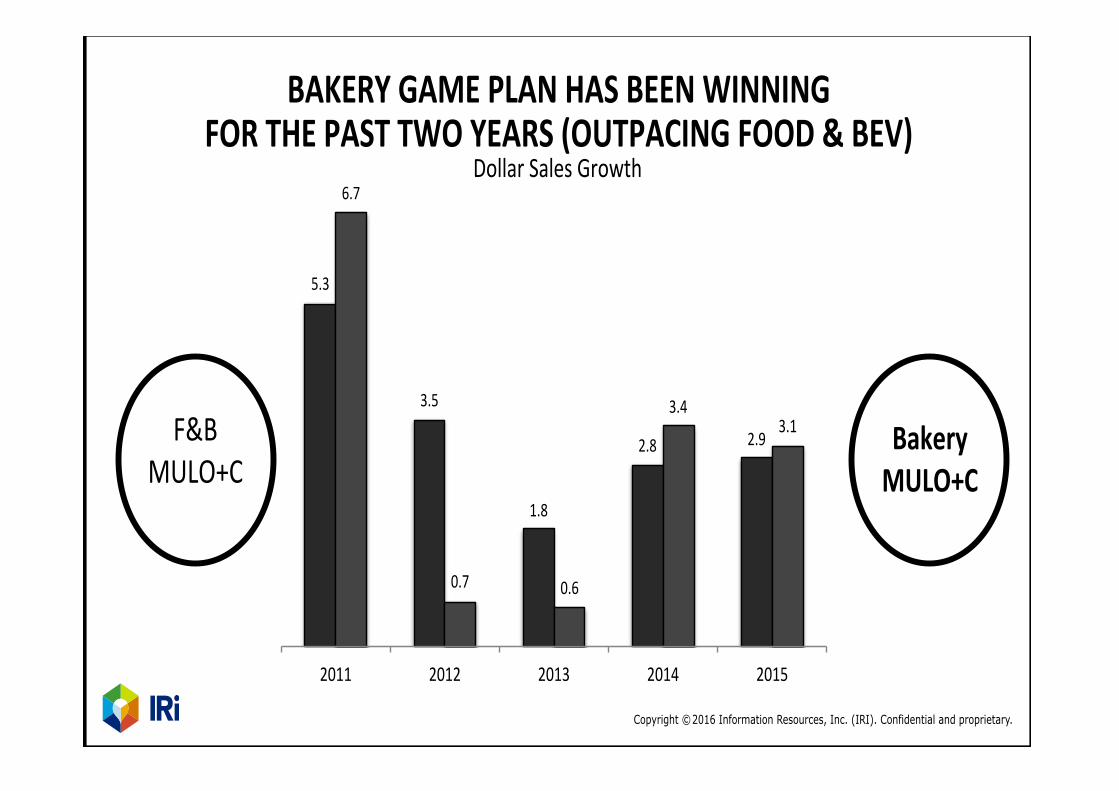

BAKERY%GAME%PLAN%HAS%BEEN%WINNING%%FOR%THE%PAST%TWO%YEARS%(OUTPACING%FOOD%&%BEV)%

Bakery%MULO+C%

F&B(MULO+C(

5.3(

3.5(

1.8(

2.8( 2.9(

6.7(

0.7( 0.6(

3.4(3.1(

2011( 2012( 2013( 2014( 2015(

Dollar(Sales(Growth(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

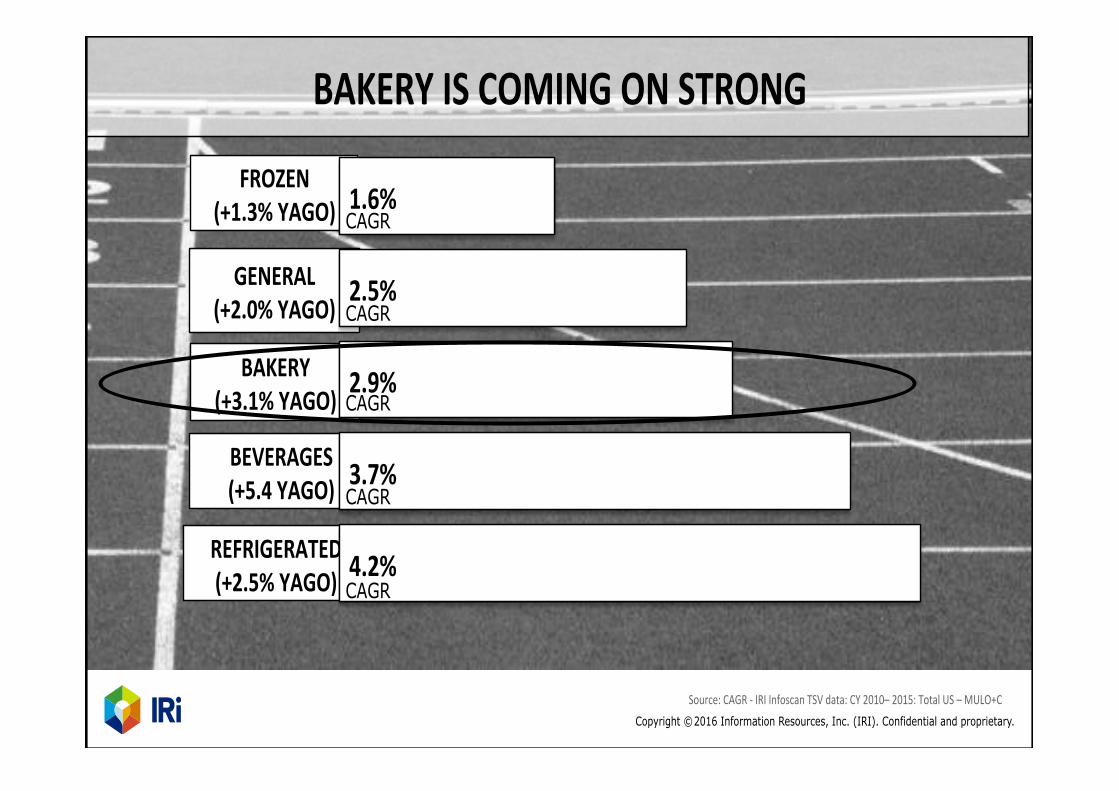

GENERAL%%(+2.0%%YAGO)%

BEVERAGES%(+5.4%YAGO)%

FROZEN%(+1.3%%YAGO)%

REFRIGERATED%(+2.5%%YAGO)%

BAKERY%IS%COMING%ON%STRONG%

Source:(CAGR(f(IRI(Infoscan(TSV(data:(CY(2010–(2015:(Total(US(–(MULO+C(

BAKERY%(+3.1%%YAGO)%

4.2%%

3.7%%

2.9%%

2.5%%

1.6%%CAGR

CAGR

CAGR

CAGR

CAGR

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

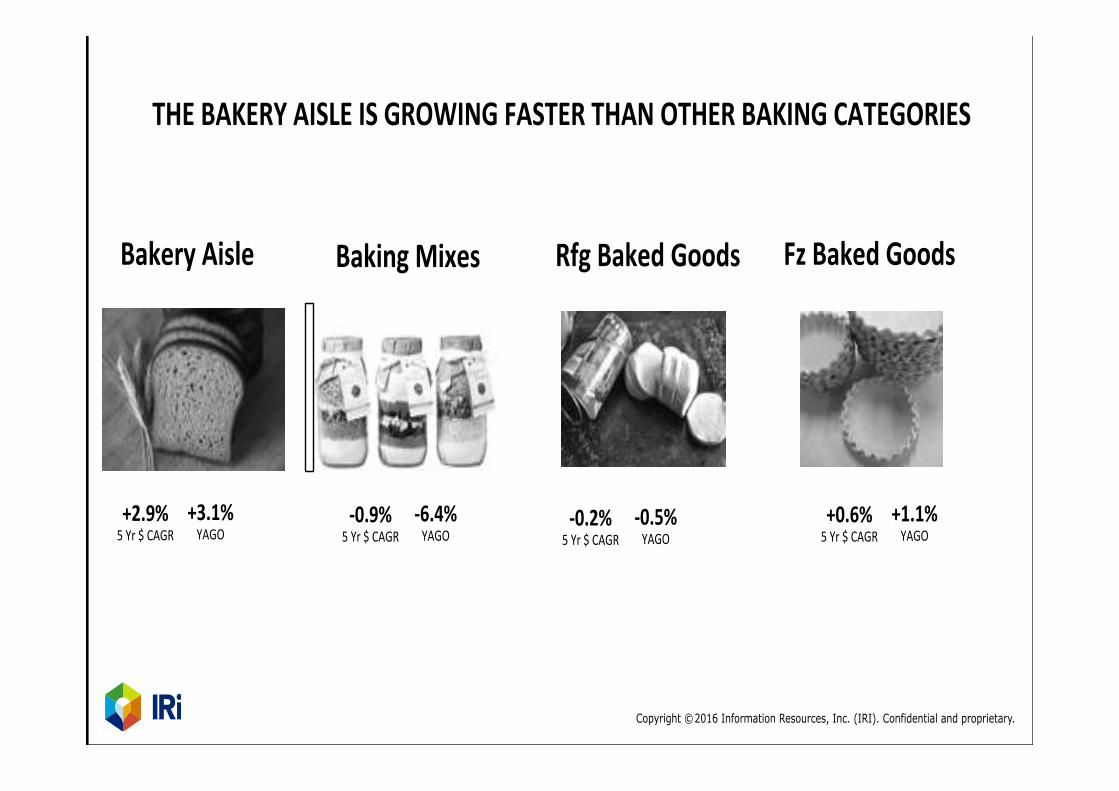

THE%BAKERY%AISLE%IS%GROWING%FASTER%THAN%OTHER%BAKING%CATEGORIES%

Bakery%Aisle%

+2.9%%5(Yr($(CAGR(

Baking%Mixes%

+3.1%%YAGO(

Rfg%Baked%Goods% Fz%Baked%Goods%

]0.9%%5(Yr($(CAGR(

]6.4%%YAGO(

]0.2%%5(Yr($(CAGR(

]0.5%%YAGO(

+0.6%%5(Yr($(CAGR(

+1.1%%YAGO(

4

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

FOOD%SERVICE%GAME%PLAN%HAS%BEEN%WINNING%%FOR%THE%PAST%THREE%YEARS%(OUTPACING%RETAIL)%

Food((Service% Retail(f((

MULO+C(F&B(

2.4%(

4.0%(

3.1%(3.3%(

3.9%(

5.1%(

3.3%(

1.8%(

2.7%(2.9%(

2011( 2012( 2013( 2014( 2015(

Dollar(Sales(Growth(

Source: Technomic Industry Forecast & IRI Total Store Advantage Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

AT%RETAIL,%THE%PERIMETER%IS%BECOMING:%The(fulcrum(point(for(maximum(retail(differen&a&on((Base(for(deeper(and(more(engaging(customer(experiences((Focus(for(space(expansion(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

WITH%PERIMETER%GROWTH%IS%+4.5%%

Source: IRI FreshLook POS data, MULO, 52 weeks ending 11/29/2015

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

BAKERY%GAME%PLAN%HAS%BEEN%WINNING%%FOR%THE%PAST%TWO%YEARS%(OUTPACING%FOOD%&%BEV)%

Bakery%MULO+C%

F&B(MULO+C(

5.3(

3.5(

1.8(

2.8( 2.9(

6.7(

0.7( 0.6(

3.4(3.1(

2011( 2012( 2013( 2014( 2015(

Dollar(Sales(Growth(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

GENERAL%%(+2.0%%YAGO)%

BEVERAGES%(+5.4%YAGO)%

FROZEN%(+1.3%%YAGO)%

REFRIGERATED%(+2.5%%YAGO)%

BAKERY%IS%COMING%ON%STRONG%

Source:(CAGR(f(IRI(Infoscan(TSV(data:(CY(2010–(2015:(Total(US(–(MULO+C(

BAKERY%(+3.1%%YAGO)%

4.2%%

3.7%%

2.9%%

2.5%%

1.6%%CAGR

CAGR

CAGR

CAGR

CAGR

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%BAKERY%AISLE%IS%GROWING%FASTER%THAN%OTHER%BAKING%CATEGORIES%

Bakery%Aisle%

+2.9%%5(Yr($(CAGR(

Baking%Mixes%

+3.1%%YAGO(

Rfg%Baked%Goods% Fz%Baked%Goods%

]0.9%%5(Yr($(CAGR(

]6.4%%YAGO(

]0.2%%5(Yr($(CAGR(

]0.5%%YAGO(

+0.6%%5(Yr($(CAGR(

+1.1%%YAGO(

4

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

FOOD%SERVICE%GAME%PLAN%HAS%BEEN%WINNING%%FOR%THE%PAST%THREE%YEARS%(OUTPACING%RETAIL)%

Food((Service% Retail(f((

MULO+C(F&B(

2.4%(

4.0%(

3.1%(3.3%(

3.9%(

5.1%(

3.3%(

1.8%(

2.7%(2.9%(

2011( 2012( 2013( 2014( 2015(

Dollar(Sales(Growth(

Source: Technomic Industry Forecast & IRI Total Store Advantage Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

AT%RETAIL,%THE%PERIMETER%IS%BECOMING:%The(fulcrum(point(for(maximum(retail(differen&a&on((Base(for(deeper(and(more(engaging(customer(experiences((Focus(for(space(expansion(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

WITH%PERIMETER%GROWTH%IS%+4.5%%

Source: IRI FreshLook POS data, MULO, 52 weeks ending 11/29/2015

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

BAKERY%GAME%PLAN%HAS%BEEN%WINNING%%FOR%THE%PAST%TWO%YEARS%(OUTPACING%FOOD%&%BEV)%

Bakery%MULO+C%

F&B(MULO+C(

5.3(

3.5(

1.8(

2.8( 2.9(

6.7(

0.7( 0.6(

3.4(3.1(

2011( 2012( 2013( 2014( 2015(

Dollar(Sales(Growth(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

GENERAL%%(+2.0%%YAGO)%

BEVERAGES%(+5.4%YAGO)%

FROZEN%(+1.3%%YAGO)%

REFRIGERATED%(+2.5%%YAGO)%

BAKERY%IS%COMING%ON%STRONG%

Source:(CAGR(f(IRI(Infoscan(TSV(data:(CY(2010–(2015:(Total(US(–(MULO+C(

BAKERY%(+3.1%%YAGO)%

4.2%%

3.7%%

2.9%%

2.5%%

1.6%%CAGR

CAGR

CAGR

CAGR

CAGR

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%BAKERY%AISLE%IS%GROWING%FASTER%THAN%OTHER%BAKING%CATEGORIES%

Bakery%Aisle%

+2.9%%5(Yr($(CAGR(

Baking%Mixes%

+3.1%%YAGO(

Rfg%Baked%Goods% Fz%Baked%Goods%

]0.9%%5(Yr($(CAGR(

]6.4%%YAGO(

]0.2%%5(Yr($(CAGR(

]0.5%%YAGO(

+0.6%%5(Yr($(CAGR(

+1.1%%YAGO(

4

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

FOOD%SERVICE%GAME%PLAN%HAS%BEEN%WINNING%%FOR%THE%PAST%THREE%YEARS%(OUTPACING%RETAIL)%

Food((Service% Retail(f((

MULO+C(F&B(

2.4%(

4.0%(

3.1%(3.3%(

3.9%(

5.1%(

3.3%(

1.8%(

2.7%(2.9%(

2011( 2012( 2013( 2014( 2015(

Dollar(Sales(Growth(

Source: Technomic Industry Forecast & IRI Total Store Advantage Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

AT%RETAIL,%THE%PERIMETER%IS%BECOMING:%The(fulcrum(point(for(maximum(retail(differen&a&on((Base(for(deeper(and(more(engaging(customer(experiences((Focus(for(space(expansion(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

WITH%PERIMETER%GROWTH%IS%+4.5%%

Source: IRI FreshLook POS data, MULO, 52 weeks ending 11/29/2015

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

BAKERY%GAME%PLAN%HAS%BEEN%WINNING%%FOR%THE%PAST%TWO%YEARS%(OUTPACING%FOOD%&%BEV)%

Bakery%MULO+C%

F&B(MULO+C(

5.3(

3.5(

1.8(

2.8( 2.9(

6.7(

0.7( 0.6(

3.4(3.1(

2011( 2012( 2013( 2014( 2015(

Dollar(Sales(Growth(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

GENERAL%%(+2.0%%YAGO)%

BEVERAGES%(+5.4%YAGO)%

FROZEN%(+1.3%%YAGO)%

REFRIGERATED%(+2.5%%YAGO)%

BAKERY%IS%COMING%ON%STRONG%

Source:(CAGR(f(IRI(Infoscan(TSV(data:(CY(2010–(2015:(Total(US(–(MULO+C(

BAKERY%(+3.1%%YAGO)%

4.2%%

3.7%%

2.9%%

2.5%%

1.6%%CAGR

CAGR

CAGR

CAGR

CAGR

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%BAKERY%AISLE%IS%GROWING%FASTER%THAN%OTHER%BAKING%CATEGORIES%

Bakery%Aisle%

+2.9%%5(Yr($(CAGR(

Baking%Mixes%

+3.1%%YAGO(

Rfg%Baked%Goods% Fz%Baked%Goods%

]0.9%%5(Yr($(CAGR(

]6.4%%YAGO(

]0.2%%5(Yr($(CAGR(

]0.5%%YAGO(

+0.6%%5(Yr($(CAGR(

+1.1%%YAGO(

4

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

FOOD%SERVICE%GAME%PLAN%HAS%BEEN%WINNING%%FOR%THE%PAST%THREE%YEARS%(OUTPACING%RETAIL)%

Food((Service% Retail(f((

MULO+C(F&B(

2.4%(

4.0%(

3.1%(3.3%(

3.9%(

5.1%(

3.3%(

1.8%(

2.7%(2.9%(

2011( 2012( 2013( 2014( 2015(

Dollar(Sales(Growth(

Source: Technomic Industry Forecast & IRI Total Store Advantage Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

AT%RETAIL,%THE%PERIMETER%IS%BECOMING:%The(fulcrum(point(for(maximum(retail(differen&a&on((Base(for(deeper(and(more(engaging(customer(experiences((Focus(for(space(expansion(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

WITH%PERIMETER%GROWTH%IS%+4.5%%

Source: IRI FreshLook POS data, MULO, 52 weeks ending 11/29/2015

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

BAKERY%GAME%PLAN%HAS%BEEN%WINNING%%FOR%THE%PAST%TWO%YEARS%(OUTPACING%FOOD%&%BEV)%

Bakery%MULO+C%

F&B(MULO+C(

5.3(

3.5(

1.8(

2.8( 2.9(

6.7(

0.7( 0.6(

3.4(3.1(

2011( 2012( 2013( 2014( 2015(

Dollar(Sales(Growth(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

GENERAL%%(+2.0%%YAGO)%

BEVERAGES%(+5.4%YAGO)%

FROZEN%(+1.3%%YAGO)%

REFRIGERATED%(+2.5%%YAGO)%

BAKERY%IS%COMING%ON%STRONG%

Source:(CAGR(f(IRI(Infoscan(TSV(data:(CY(2010–(2015:(Total(US(–(MULO+C(

BAKERY%(+3.1%%YAGO)%

4.2%%

3.7%%

2.9%%

2.5%%

1.6%%CAGR

CAGR

CAGR

CAGR

CAGR

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%BAKERY%AISLE%IS%GROWING%FASTER%THAN%OTHER%BAKING%CATEGORIES%

Bakery%Aisle%

+2.9%%5(Yr($(CAGR(

Baking%Mixes%

+3.1%%YAGO(

Rfg%Baked%Goods% Fz%Baked%Goods%

]0.9%%5(Yr($(CAGR(

]6.4%%YAGO(

]0.2%%5(Yr($(CAGR(

]0.5%%YAGO(

+0.6%%5(Yr($(CAGR(

+1.1%%YAGO(

4

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

FOOD%SERVICE%GAME%PLAN%HAS%BEEN%WINNING%%FOR%THE%PAST%THREE%YEARS%(OUTPACING%RETAIL)%

Food((Service% Retail(f((

MULO+C(F&B(

2.4%(

4.0%(

3.1%(3.3%(

3.9%(

5.1%(

3.3%(

1.8%(

2.7%(2.9%(

2011( 2012( 2013( 2014( 2015(

Dollar(Sales(Growth(

Source: Technomic Industry Forecast & IRI Total Store Advantage Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

AT%RETAIL,%THE%PERIMETER%IS%BECOMING:%The(fulcrum(point(for(maximum(retail(differen&a&on((Base(for(deeper(and(more(engaging(customer(experiences((Focus(for(space(expansion(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

WITH%PERIMETER%GROWTH%IS%+4.5%%

Source: IRI FreshLook POS data, MULO, 52 weeks ending 11/29/2015

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

BAKERY%GAME%PLAN%HAS%BEEN%WINNING%%FOR%THE%PAST%TWO%YEARS%(OUTPACING%FOOD%&%BEV)%

Bakery%MULO+C%

F&B(MULO+C(

5.3(

3.5(

1.8(

2.8( 2.9(

6.7(

0.7( 0.6(

3.4(3.1(

2011( 2012( 2013( 2014( 2015(

Dollar(Sales(Growth(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

GENERAL%%(+2.0%%YAGO)%

BEVERAGES%(+5.4%YAGO)%

FROZEN%(+1.3%%YAGO)%

REFRIGERATED%(+2.5%%YAGO)%

BAKERY%IS%COMING%ON%STRONG%

Source:(CAGR(f(IRI(Infoscan(TSV(data:(CY(2010–(2015:(Total(US(–(MULO+C(

BAKERY%(+3.1%%YAGO)%

4.2%%

3.7%%

2.9%%

2.5%%

1.6%%CAGR

CAGR

CAGR

CAGR

CAGR

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

THE%BAKERY%AISLE%IS%GROWING%FASTER%THAN%OTHER%BAKING%CATEGORIES%

Bakery%Aisle%

+2.9%%5(Yr($(CAGR(

Baking%Mixes%

+3.1%%YAGO(

Rfg%Baked%Goods% Fz%Baked%Goods%

]0.9%%5(Yr($(CAGR(

]6.4%%YAGO(

]0.2%%5(Yr($(CAGR(

]0.5%%YAGO(

+0.6%%5(Yr($(CAGR(

+1.1%%YAGO(

5

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

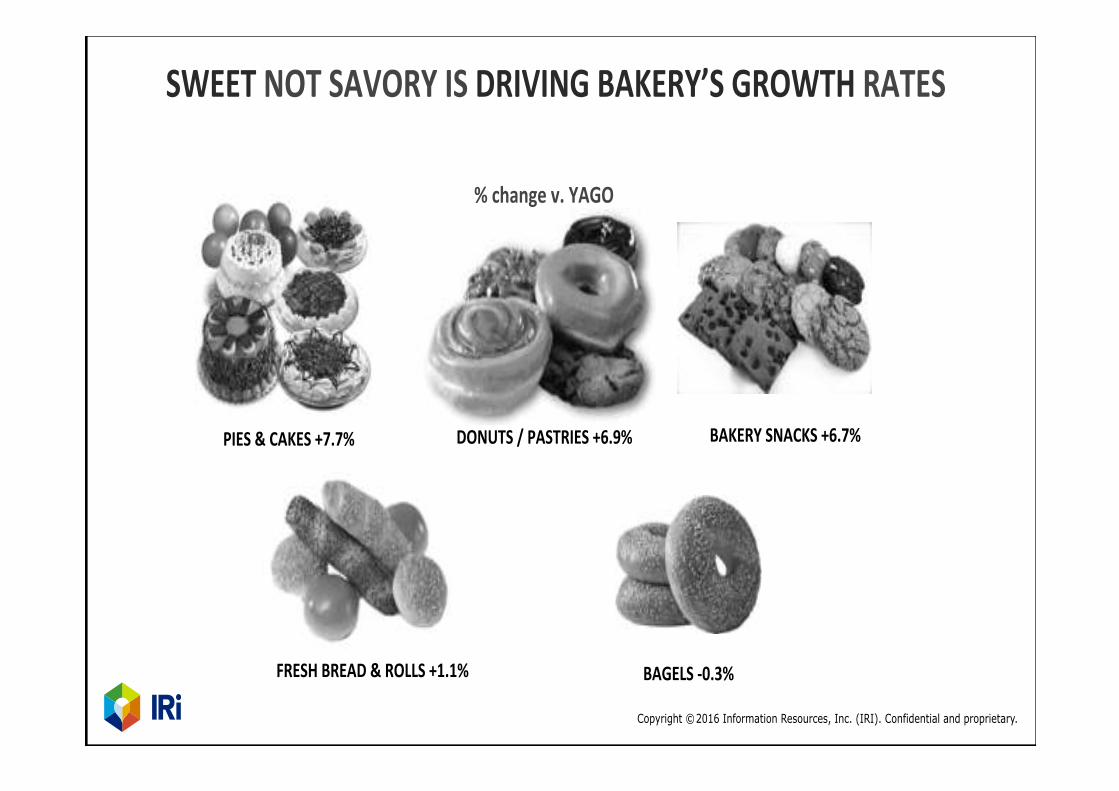

%%change%v.%YAGO(

SWEET%NOT%SAVORY%IS%DRIVING%BAKERY’S%GROWTH%RATES%

PIES%&%CAKES%+7.7%%

FRESH%BREAD%&%ROLLS%+1.1%% BAGELS%]0.3%%

DONUTS%/%PASTRIES%+6.9%% BAKERY%SNACKS%+6.7%%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

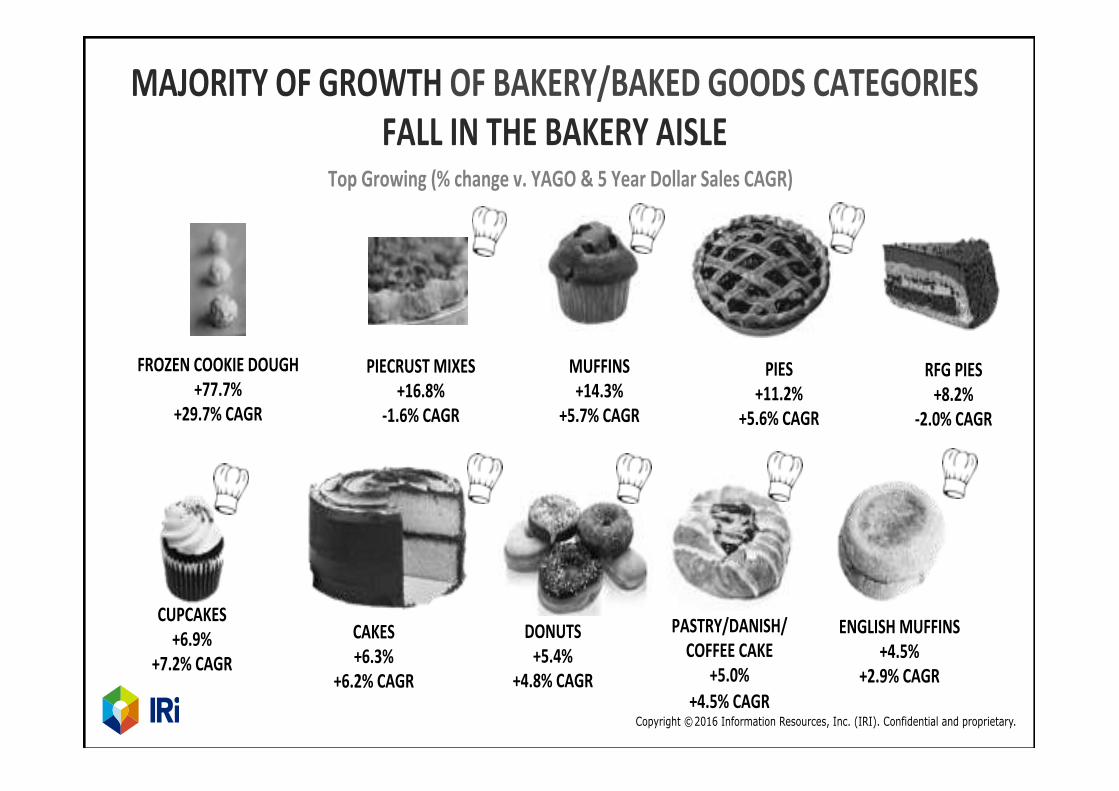

Top%Growing%(%%change%v.%YAGO%&%5%Year%Dollar%Sales%CAGR)(

MAJORITY%OF%GROWTH%OF%BAKERY/BAKED%GOODS%CATEGORIES%FALL%IN%THE%BAKERY%AISLE%

PASTRY/DANISH/%%%%%COFFEE%CAKE%

+5.0%%+4.5%%CAGR%

PIECRUST%MIXES%+16.8%%%

]1.6%%CAGR%

FROZEN%COOKIE%DOUGH%+77.7%%%

+29.7%%CAGR%

RFG%PIES%+8.2%%

]2.0%%CAGR%

PIES%+11.2%%%

+5.6%%CAGR%

CUPCAKES%+6.9%%

+7.2%%CAGR%CAKES%+6.3%%

+6.2%%CAGR%

DONUTS%+5.4%%

+4.8%%CAGR%

MUFFINS%+14.3%%

+5.7%%CAGR%

ENGLISH%MUFFINS%+4.5%%

+2.9%%CAGR%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PLAYS%OF%THE%DAY:%Millennials(&(Hispanics(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

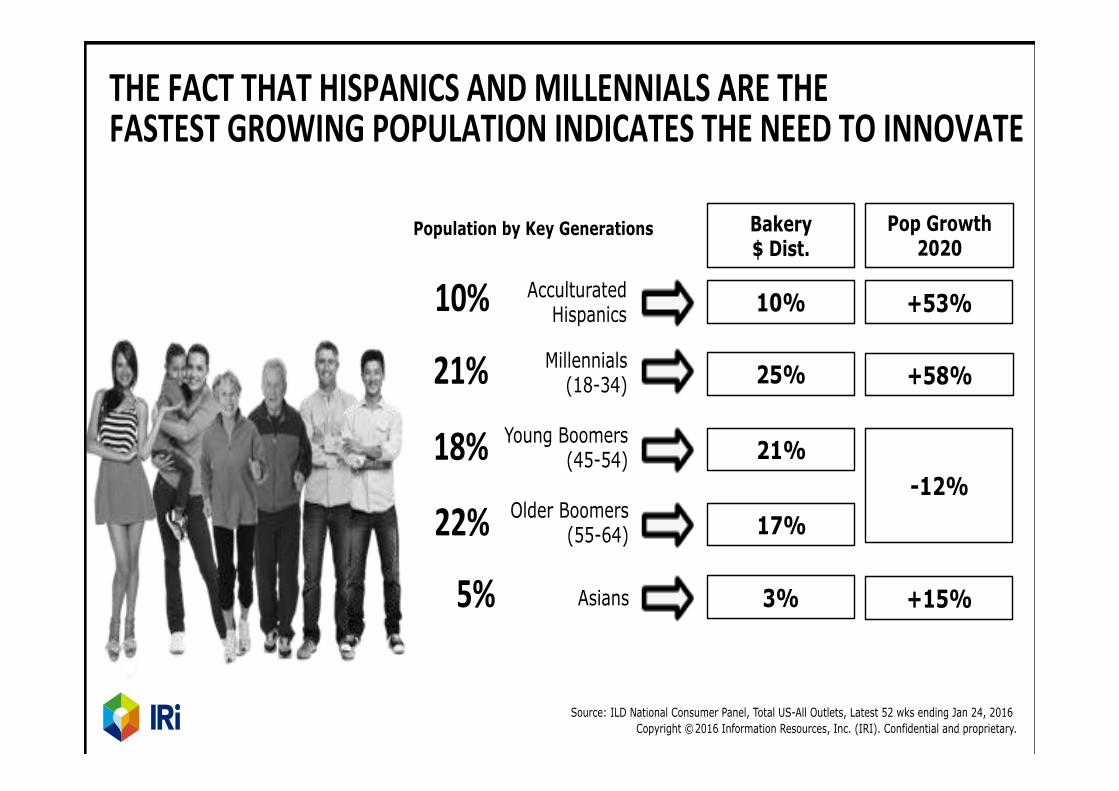

Acculturated Hispanics 10% +53%

THE%FACT%THAT%HISPANICS%AND%MILLENNIALS%ARE%THE%%FASTEST%GROWING%POPULATION%INDICATES%THE%NEED%TO%INNOVATE%

Population by Key Generations%

Source: ILD National Consumer Panel, Total US-All Outlets, Latest 52 wks ending Jan 24, 2016

10%%

21%%

18%%

22%%

5%%

25% +58%

21%

17%

3% +15%

Millennials (18-34)

Young Boomers (45-54)

Older Boomers (55-64)

Asians

Bakery $ Dist.

Pop Growth 2020

-12%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

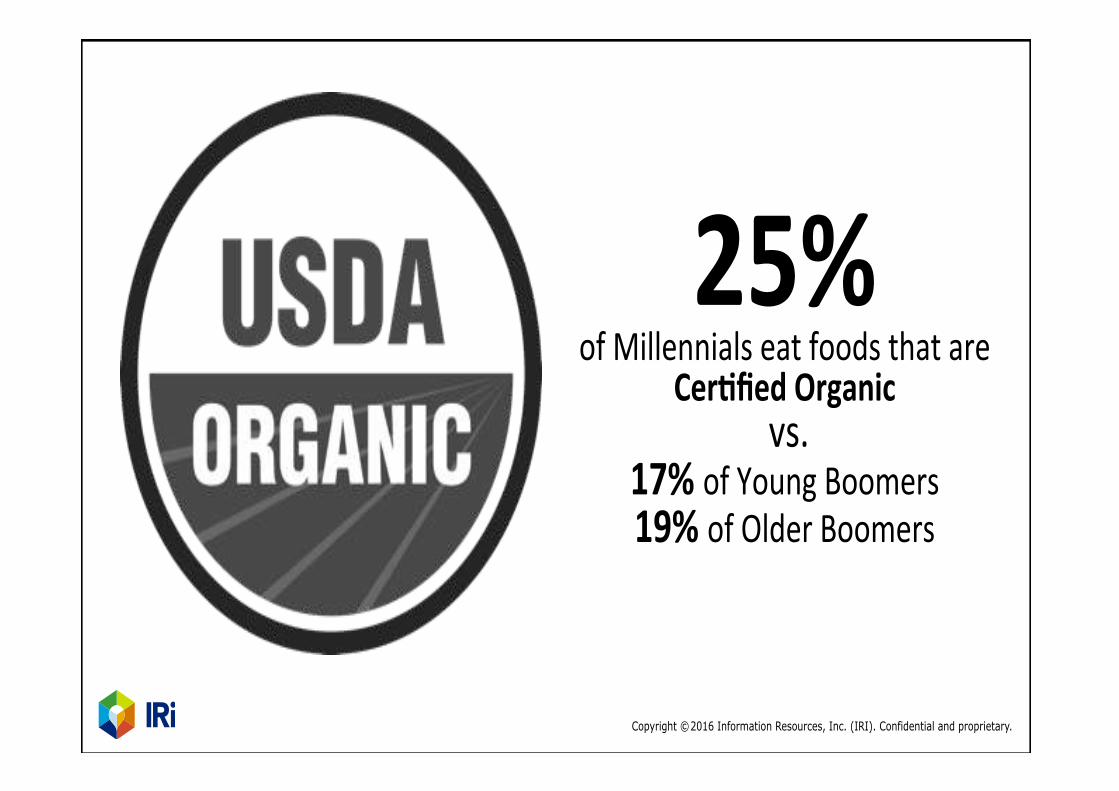

25%%of(Millennials(eat(foods(that(are((

Cer\fied%Organic%%vs.((

17%%of(Young(Boomers(%19%%of(Older(Boomers(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

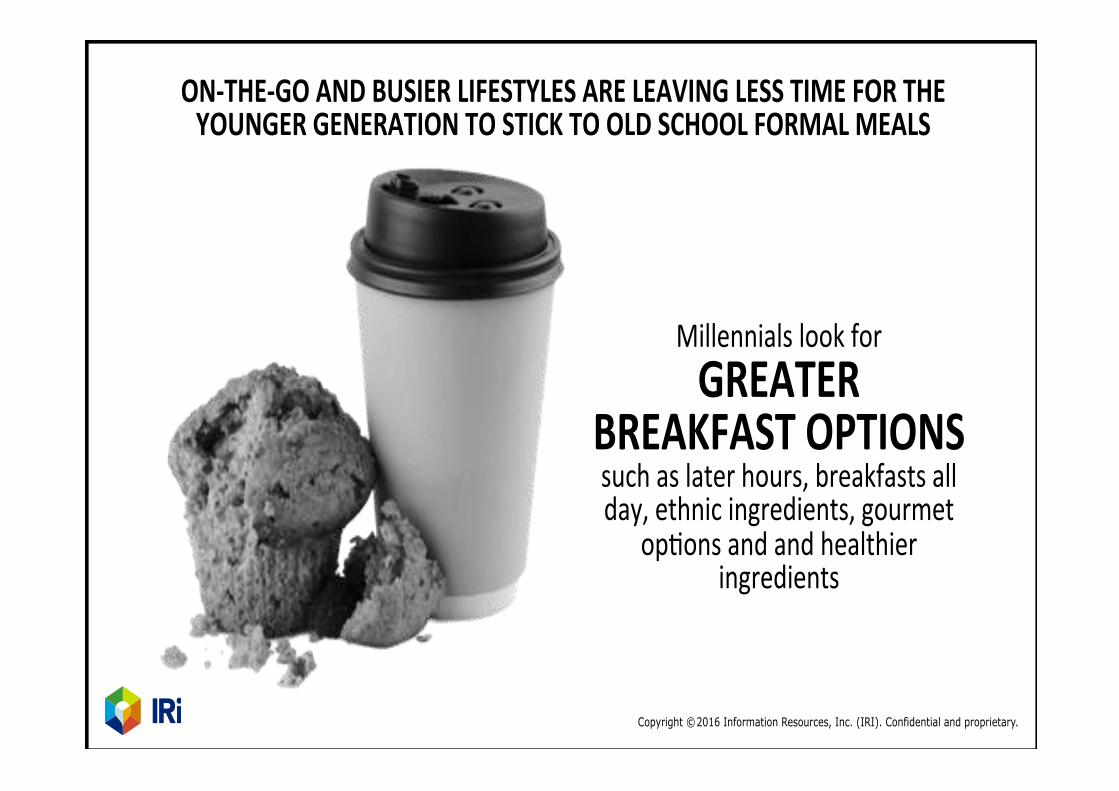

ON]THE]GO%AND%BUSIER%LIFESTYLES%ARE%LEAVING%LESS%TIME%FOR%THE%%YOUNGER%GENERATION%TO%STICK%TO%OLD%SCHOOL%FORMAL%MEALS%

Millennials(look(for((GREATER%%

BREAKFAST%OPTIONS%%such(as(later(hours,(breakfasts(all(day,(ethnic(ingredients,(gourmet(

op&ons(and(and(healthier(ingredients(

5

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

%%change%v.%YAGO(

SWEET%NOT%SAVORY%IS%DRIVING%BAKERY’S%GROWTH%RATES%

PIES%&%CAKES%+7.7%%

FRESH%BREAD%&%ROLLS%+1.1%% BAGELS%]0.3%%

DONUTS%/%PASTRIES%+6.9%% BAKERY%SNACKS%+6.7%%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Top%Growing%(%%change%v.%YAGO%&%5%Year%Dollar%Sales%CAGR)(

MAJORITY%OF%GROWTH%OF%BAKERY/BAKED%GOODS%CATEGORIES%FALL%IN%THE%BAKERY%AISLE%

PASTRY/DANISH/%%%%%COFFEE%CAKE%

+5.0%%+4.5%%CAGR%

PIECRUST%MIXES%+16.8%%%

]1.6%%CAGR%

FROZEN%COOKIE%DOUGH%+77.7%%%

+29.7%%CAGR%

RFG%PIES%+8.2%%

]2.0%%CAGR%

PIES%+11.2%%%

+5.6%%CAGR%

CUPCAKES%+6.9%%

+7.2%%CAGR%CAKES%+6.3%%

+6.2%%CAGR%

DONUTS%+5.4%%

+4.8%%CAGR%

MUFFINS%+14.3%%

+5.7%%CAGR%

ENGLISH%MUFFINS%+4.5%%

+2.9%%CAGR%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PLAYS%OF%THE%DAY:%Millennials(&(Hispanics(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Acculturated Hispanics 10% +53%

THE%FACT%THAT%HISPANICS%AND%MILLENNIALS%ARE%THE%%FASTEST%GROWING%POPULATION%INDICATES%THE%NEED%TO%INNOVATE%

Population by Key Generations%

Source: ILD National Consumer Panel, Total US-All Outlets, Latest 52 wks ending Jan 24, 2016

10%%

21%%

18%%

22%%

5%%

25% +58%

21%

17%

3% +15%

Millennials (18-34)

Young Boomers (45-54)

Older Boomers (55-64)

Asians

Bakery $ Dist.

Pop Growth 2020

-12%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

25%%of(Millennials(eat(foods(that(are((

Cer\fied%Organic%%vs.((

17%%of(Young(Boomers(%19%%of(Older(Boomers(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

ON]THE]GO%AND%BUSIER%LIFESTYLES%ARE%LEAVING%LESS%TIME%FOR%THE%%YOUNGER%GENERATION%TO%STICK%TO%OLD%SCHOOL%FORMAL%MEALS%

Millennials(look(for((GREATER%%

BREAKFAST%OPTIONS%%such(as(later(hours,(breakfasts(all(day,(ethnic(ingredients,(gourmet(

op&ons(and(and(healthier(ingredients(

5

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

%%change%v.%YAGO(

SWEET%NOT%SAVORY%IS%DRIVING%BAKERY’S%GROWTH%RATES%

PIES%&%CAKES%+7.7%%

FRESH%BREAD%&%ROLLS%+1.1%% BAGELS%]0.3%%

DONUTS%/%PASTRIES%+6.9%% BAKERY%SNACKS%+6.7%%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Top%Growing%(%%change%v.%YAGO%&%5%Year%Dollar%Sales%CAGR)(

MAJORITY%OF%GROWTH%OF%BAKERY/BAKED%GOODS%CATEGORIES%FALL%IN%THE%BAKERY%AISLE%

PASTRY/DANISH/%%%%%COFFEE%CAKE%

+5.0%%+4.5%%CAGR%

PIECRUST%MIXES%+16.8%%%

]1.6%%CAGR%

FROZEN%COOKIE%DOUGH%+77.7%%%

+29.7%%CAGR%

RFG%PIES%+8.2%%

]2.0%%CAGR%

PIES%+11.2%%%

+5.6%%CAGR%

CUPCAKES%+6.9%%

+7.2%%CAGR%CAKES%+6.3%%

+6.2%%CAGR%

DONUTS%+5.4%%

+4.8%%CAGR%

MUFFINS%+14.3%%

+5.7%%CAGR%

ENGLISH%MUFFINS%+4.5%%

+2.9%%CAGR%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PLAYS%OF%THE%DAY:%Millennials(&(Hispanics(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Acculturated Hispanics 10% +53%

THE%FACT%THAT%HISPANICS%AND%MILLENNIALS%ARE%THE%%FASTEST%GROWING%POPULATION%INDICATES%THE%NEED%TO%INNOVATE%

Population by Key Generations%

Source: ILD National Consumer Panel, Total US-All Outlets, Latest 52 wks ending Jan 24, 2016

10%%

21%%

18%%

22%%

5%%

25% +58%

21%

17%

3% +15%

Millennials (18-34)

Young Boomers (45-54)

Older Boomers (55-64)

Asians

Bakery $ Dist.

Pop Growth 2020

-12%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

25%%of(Millennials(eat(foods(that(are((

Cer\fied%Organic%%vs.((

17%%of(Young(Boomers(%19%%of(Older(Boomers(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

ON]THE]GO%AND%BUSIER%LIFESTYLES%ARE%LEAVING%LESS%TIME%FOR%THE%%YOUNGER%GENERATION%TO%STICK%TO%OLD%SCHOOL%FORMAL%MEALS%

Millennials(look(for((GREATER%%

BREAKFAST%OPTIONS%%such(as(later(hours,(breakfasts(all(day,(ethnic(ingredients,(gourmet(

op&ons(and(and(healthier(ingredients(

5

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

%%change%v.%YAGO(

SWEET%NOT%SAVORY%IS%DRIVING%BAKERY’S%GROWTH%RATES%

PIES%&%CAKES%+7.7%%

FRESH%BREAD%&%ROLLS%+1.1%% BAGELS%]0.3%%

DONUTS%/%PASTRIES%+6.9%% BAKERY%SNACKS%+6.7%%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Top%Growing%(%%change%v.%YAGO%&%5%Year%Dollar%Sales%CAGR)(

MAJORITY%OF%GROWTH%OF%BAKERY/BAKED%GOODS%CATEGORIES%FALL%IN%THE%BAKERY%AISLE%

PASTRY/DANISH/%%%%%COFFEE%CAKE%

+5.0%%+4.5%%CAGR%

PIECRUST%MIXES%+16.8%%%

]1.6%%CAGR%

FROZEN%COOKIE%DOUGH%+77.7%%%

+29.7%%CAGR%

RFG%PIES%+8.2%%

]2.0%%CAGR%

PIES%+11.2%%%

+5.6%%CAGR%

CUPCAKES%+6.9%%

+7.2%%CAGR%CAKES%+6.3%%

+6.2%%CAGR%

DONUTS%+5.4%%

+4.8%%CAGR%

MUFFINS%+14.3%%

+5.7%%CAGR%

ENGLISH%MUFFINS%+4.5%%

+2.9%%CAGR%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PLAYS%OF%THE%DAY:%Millennials(&(Hispanics(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Acculturated Hispanics 10% +53%

THE%FACT%THAT%HISPANICS%AND%MILLENNIALS%ARE%THE%%FASTEST%GROWING%POPULATION%INDICATES%THE%NEED%TO%INNOVATE%

Population by Key Generations%

Source: ILD National Consumer Panel, Total US-All Outlets, Latest 52 wks ending Jan 24, 2016

10%%

21%%

18%%

22%%

5%%

25% +58%

21%

17%

3% +15%

Millennials (18-34)

Young Boomers (45-54)

Older Boomers (55-64)

Asians

Bakery $ Dist.

Pop Growth 2020

-12%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

25%%of(Millennials(eat(foods(that(are((

Cer\fied%Organic%%vs.((

17%%of(Young(Boomers(%19%%of(Older(Boomers(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

ON]THE]GO%AND%BUSIER%LIFESTYLES%ARE%LEAVING%LESS%TIME%FOR%THE%%YOUNGER%GENERATION%TO%STICK%TO%OLD%SCHOOL%FORMAL%MEALS%

Millennials(look(for((GREATER%%

BREAKFAST%OPTIONS%%such(as(later(hours,(breakfasts(all(day,(ethnic(ingredients,(gourmet(

op&ons(and(and(healthier(ingredients(

5

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

%%change%v.%YAGO(

SWEET%NOT%SAVORY%IS%DRIVING%BAKERY’S%GROWTH%RATES%

PIES%&%CAKES%+7.7%%

FRESH%BREAD%&%ROLLS%+1.1%% BAGELS%]0.3%%

DONUTS%/%PASTRIES%+6.9%% BAKERY%SNACKS%+6.7%%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Top%Growing%(%%change%v.%YAGO%&%5%Year%Dollar%Sales%CAGR)(

MAJORITY%OF%GROWTH%OF%BAKERY/BAKED%GOODS%CATEGORIES%FALL%IN%THE%BAKERY%AISLE%

PASTRY/DANISH/%%%%%COFFEE%CAKE%

+5.0%%+4.5%%CAGR%

PIECRUST%MIXES%+16.8%%%

]1.6%%CAGR%

FROZEN%COOKIE%DOUGH%+77.7%%%

+29.7%%CAGR%

RFG%PIES%+8.2%%

]2.0%%CAGR%

PIES%+11.2%%%

+5.6%%CAGR%

CUPCAKES%+6.9%%

+7.2%%CAGR%CAKES%+6.3%%

+6.2%%CAGR%

DONUTS%+5.4%%

+4.8%%CAGR%

MUFFINS%+14.3%%

+5.7%%CAGR%

ENGLISH%MUFFINS%+4.5%%

+2.9%%CAGR%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PLAYS%OF%THE%DAY:%Millennials(&(Hispanics(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Acculturated Hispanics 10% +53%

THE%FACT%THAT%HISPANICS%AND%MILLENNIALS%ARE%THE%%FASTEST%GROWING%POPULATION%INDICATES%THE%NEED%TO%INNOVATE%

Population by Key Generations%

Source: ILD National Consumer Panel, Total US-All Outlets, Latest 52 wks ending Jan 24, 2016

10%%

21%%

18%%

22%%

5%%

25% +58%

21%

17%

3% +15%

Millennials (18-34)

Young Boomers (45-54)

Older Boomers (55-64)

Asians

Bakery $ Dist.

Pop Growth 2020

-12%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

25%%of(Millennials(eat(foods(that(are((

Cer\fied%Organic%%vs.((

17%%of(Young(Boomers(%19%%of(Older(Boomers(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

ON]THE]GO%AND%BUSIER%LIFESTYLES%ARE%LEAVING%LESS%TIME%FOR%THE%%YOUNGER%GENERATION%TO%STICK%TO%OLD%SCHOOL%FORMAL%MEALS%

Millennials(look(for((GREATER%%

BREAKFAST%OPTIONS%%such(as(later(hours,(breakfasts(all(day,(ethnic(ingredients,(gourmet(

op&ons(and(and(healthier(ingredients(

5

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

%%change%v.%YAGO(

SWEET%NOT%SAVORY%IS%DRIVING%BAKERY’S%GROWTH%RATES%

PIES%&%CAKES%+7.7%%

FRESH%BREAD%&%ROLLS%+1.1%% BAGELS%]0.3%%

DONUTS%/%PASTRIES%+6.9%% BAKERY%SNACKS%+6.7%%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Top%Growing%(%%change%v.%YAGO%&%5%Year%Dollar%Sales%CAGR)(

MAJORITY%OF%GROWTH%OF%BAKERY/BAKED%GOODS%CATEGORIES%FALL%IN%THE%BAKERY%AISLE%

PASTRY/DANISH/%%%%%COFFEE%CAKE%

+5.0%%+4.5%%CAGR%

PIECRUST%MIXES%+16.8%%%

]1.6%%CAGR%

FROZEN%COOKIE%DOUGH%+77.7%%%

+29.7%%CAGR%

RFG%PIES%+8.2%%

]2.0%%CAGR%

PIES%+11.2%%%

+5.6%%CAGR%

CUPCAKES%+6.9%%

+7.2%%CAGR%CAKES%+6.3%%

+6.2%%CAGR%

DONUTS%+5.4%%

+4.8%%CAGR%

MUFFINS%+14.3%%

+5.7%%CAGR%

ENGLISH%MUFFINS%+4.5%%

+2.9%%CAGR%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PLAYS%OF%THE%DAY:%Millennials(&(Hispanics(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Acculturated Hispanics 10% +53%

THE%FACT%THAT%HISPANICS%AND%MILLENNIALS%ARE%THE%%FASTEST%GROWING%POPULATION%INDICATES%THE%NEED%TO%INNOVATE%

Population by Key Generations%

Source: ILD National Consumer Panel, Total US-All Outlets, Latest 52 wks ending Jan 24, 2016

10%%

21%%

18%%

22%%

5%%

25% +58%

21%

17%

3% +15%

Millennials (18-34)

Young Boomers (45-54)

Older Boomers (55-64)

Asians

Bakery $ Dist.

Pop Growth 2020

-12%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

25%%of(Millennials(eat(foods(that(are((

Cer\fied%Organic%%vs.((

17%%of(Young(Boomers(%19%%of(Older(Boomers(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

ON]THE]GO%AND%BUSIER%LIFESTYLES%ARE%LEAVING%LESS%TIME%FOR%THE%%YOUNGER%GENERATION%TO%STICK%TO%OLD%SCHOOL%FORMAL%MEALS%

Millennials(look(for((GREATER%%

BREAKFAST%OPTIONS%%such(as(later(hours,(breakfasts(all(day,(ethnic(ingredients,(gourmet(

op&ons(and(and(healthier(ingredients(

6

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

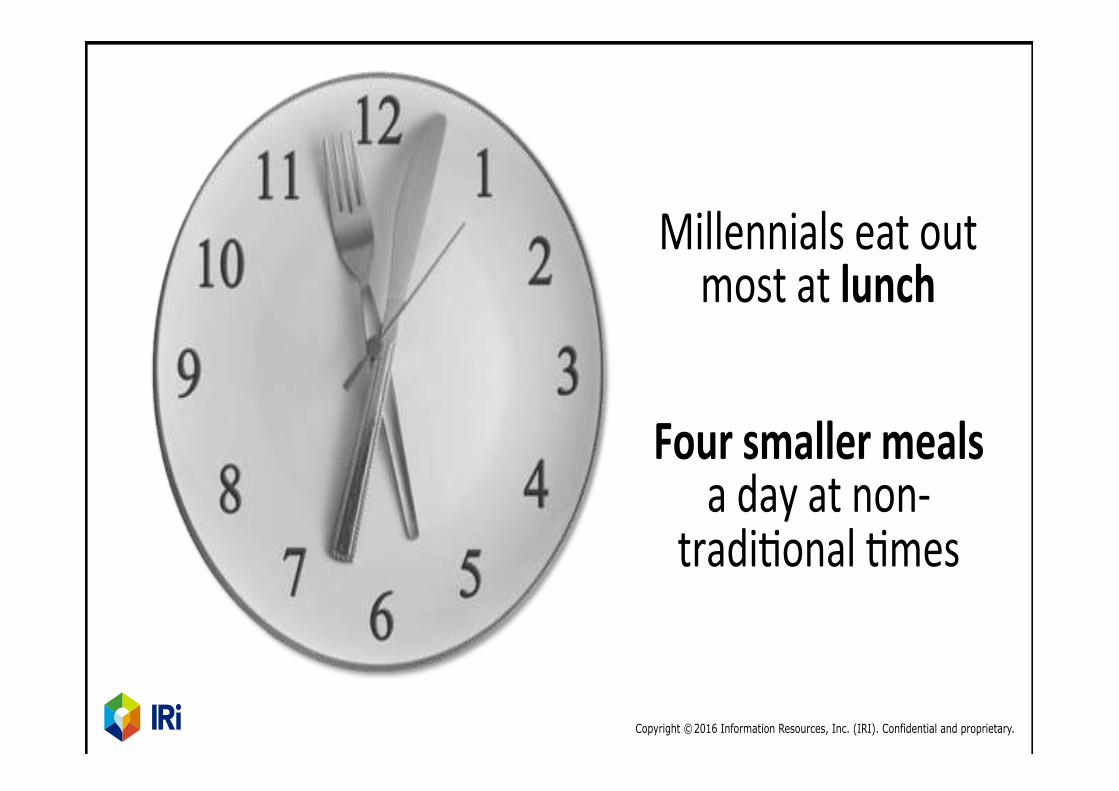

Millennials(eat(out((most(at(lunch%

Four%smaller%meals%%a(day(at(nonf(

tradi&onal(&mes%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary. Source: ILD National Consumer Panel, Total US-MULO, Rolling 52 wks ending Mar 22, 2015, NBD Aligned

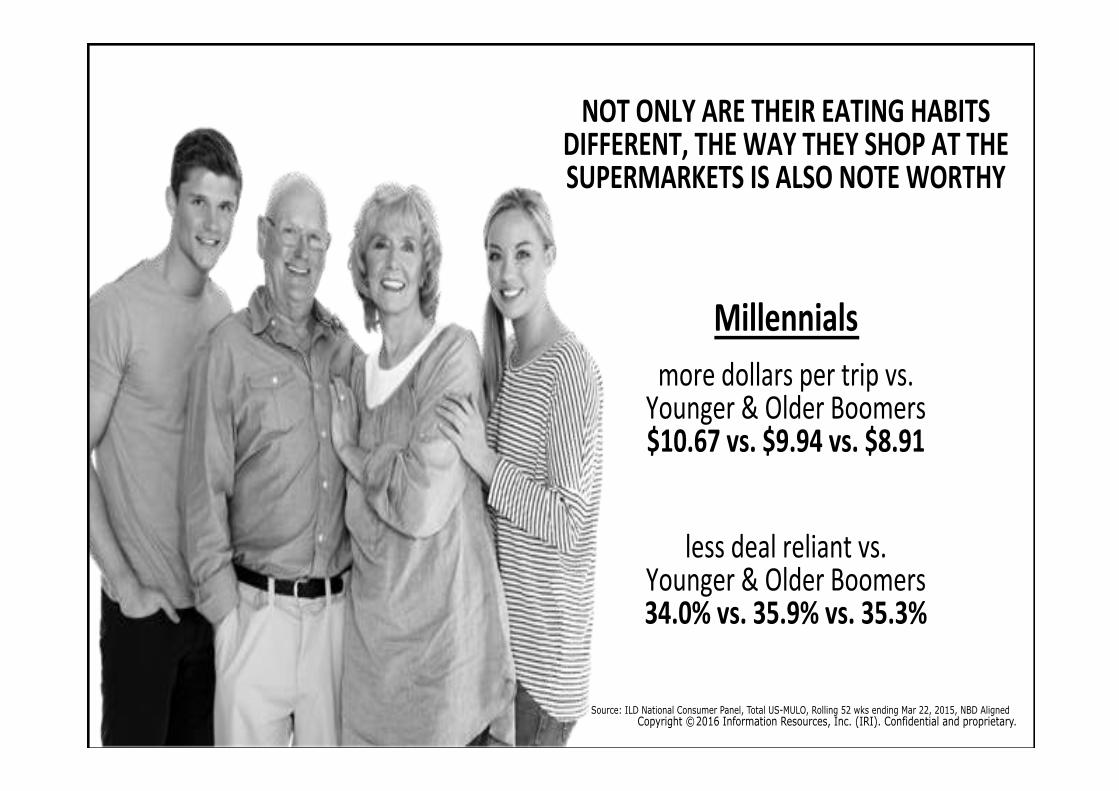

more(dollars(per(trip(vs.((Younger(&(Older(Boomers(($10.67%vs.%$9.94%vs.%$8.91%

Millennials%

less(deal(reliant(vs.((Younger(&(Older(Boomers((34.0%%vs.%35.9%%vs.%35.3%%

NOT%ONLY%ARE%THEIR%EATING%HABITS%DIFFERENT,%THE%WAY%THEY%SHOP%AT%THE%SUPERMARKETS%IS%ALSO%NOTE%WORTHY%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary. Source: ILD National Consumer Panel, Total US-MULO, Rolling 52 wks ending Mar 22, 2015, NBD Aligned

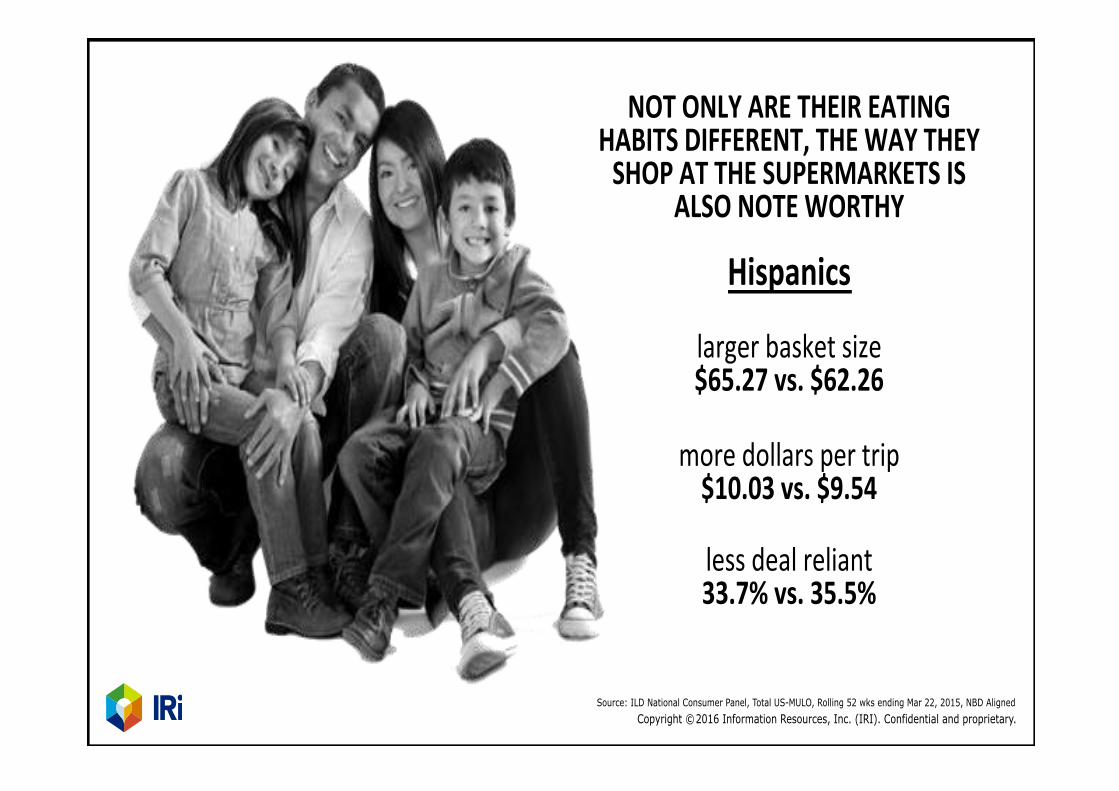

NOT%ONLY%ARE%THEIR%EATING%HABITS%DIFFERENT,%THE%WAY%THEY%SHOP%AT%THE%SUPERMARKETS%IS%

ALSO%NOTE%WORTHY%

larger(basket(size($65.27%vs.%$62.26%

more(dollars(per(trip(($10.03%vs.%$9.54%

less(deal(reliant(33.7%%vs.%35.5%%

Hispanics%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

LIFESTYLES%ARE%%FAST%CHANGING%%WITH%EVOLUTION%%OF%TECHNOLOGY%

of(BifCultural(Hispanic(Millennials(look(for(recipes(

online((

75%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PLAYS%OF%THE%DAY:%Health(&(Wellness(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

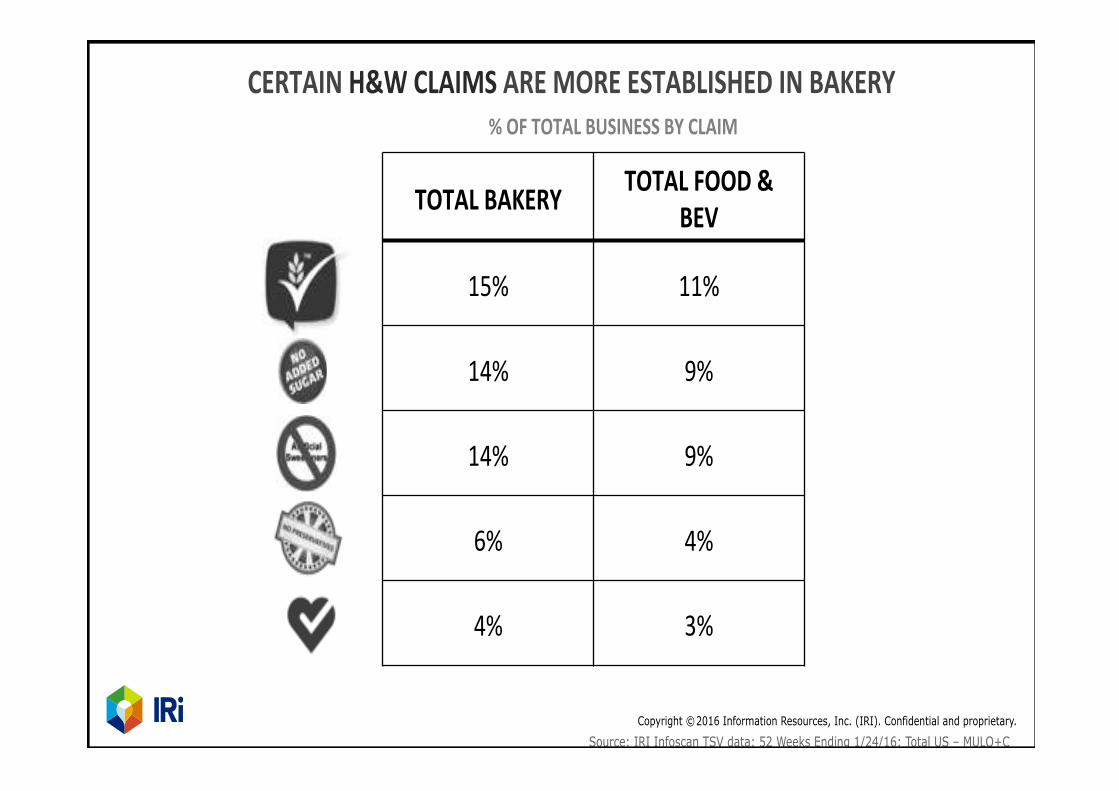

Source: IRI Infoscan TSV data: 52 Weeks Ending 1/24/16: Total US – MULO+C

%%OF%TOTAL%BUSINESS%BY%CLAIM%

CERTAIN%H&W%CLAIMS%ARE%MORE%ESTABLISHED%IN%BAKERY%

TOTAL%BAKERY% TOTAL%FOOD%&%BEV%

15%( 11%(

14%( 9%(

14%( 9%(

6%( 4%(

4%( 3%(

6

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Millennials(eat(out((most(at(lunch%

Four%smaller%meals%%a(day(at(nonf(

tradi&onal(&mes%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary. Source: ILD National Consumer Panel, Total US-MULO, Rolling 52 wks ending Mar 22, 2015, NBD Aligned

more(dollars(per(trip(vs.((Younger(&(Older(Boomers(($10.67%vs.%$9.94%vs.%$8.91%

Millennials%

less(deal(reliant(vs.((Younger(&(Older(Boomers((34.0%%vs.%35.9%%vs.%35.3%%

NOT%ONLY%ARE%THEIR%EATING%HABITS%DIFFERENT,%THE%WAY%THEY%SHOP%AT%THE%SUPERMARKETS%IS%ALSO%NOTE%WORTHY%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary. Source: ILD National Consumer Panel, Total US-MULO, Rolling 52 wks ending Mar 22, 2015, NBD Aligned

NOT%ONLY%ARE%THEIR%EATING%HABITS%DIFFERENT,%THE%WAY%THEY%SHOP%AT%THE%SUPERMARKETS%IS%

ALSO%NOTE%WORTHY%

larger(basket(size($65.27%vs.%$62.26%

more(dollars(per(trip(($10.03%vs.%$9.54%

less(deal(reliant(33.7%%vs.%35.5%%

Hispanics%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

LIFESTYLES%ARE%%FAST%CHANGING%%WITH%EVOLUTION%%OF%TECHNOLOGY%

of(BifCultural(Hispanic(Millennials(look(for(recipes(

online((

75%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PLAYS%OF%THE%DAY:%Health(&(Wellness(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Source: IRI Infoscan TSV data: 52 Weeks Ending 1/24/16: Total US – MULO+C

%%OF%TOTAL%BUSINESS%BY%CLAIM%

CERTAIN%H&W%CLAIMS%ARE%MORE%ESTABLISHED%IN%BAKERY%

TOTAL%BAKERY% TOTAL%FOOD%&%BEV%

15%( 11%(

14%( 9%(

14%( 9%(

6%( 4%(

4%( 3%(

6

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Millennials(eat(out((most(at(lunch%

Four%smaller%meals%%a(day(at(nonf(

tradi&onal(&mes%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary. Source: ILD National Consumer Panel, Total US-MULO, Rolling 52 wks ending Mar 22, 2015, NBD Aligned

more(dollars(per(trip(vs.((Younger(&(Older(Boomers(($10.67%vs.%$9.94%vs.%$8.91%

Millennials%

less(deal(reliant(vs.((Younger(&(Older(Boomers((34.0%%vs.%35.9%%vs.%35.3%%

NOT%ONLY%ARE%THEIR%EATING%HABITS%DIFFERENT,%THE%WAY%THEY%SHOP%AT%THE%SUPERMARKETS%IS%ALSO%NOTE%WORTHY%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary. Source: ILD National Consumer Panel, Total US-MULO, Rolling 52 wks ending Mar 22, 2015, NBD Aligned

NOT%ONLY%ARE%THEIR%EATING%HABITS%DIFFERENT,%THE%WAY%THEY%SHOP%AT%THE%SUPERMARKETS%IS%

ALSO%NOTE%WORTHY%

larger(basket(size($65.27%vs.%$62.26%

more(dollars(per(trip(($10.03%vs.%$9.54%

less(deal(reliant(33.7%%vs.%35.5%%

Hispanics%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

LIFESTYLES%ARE%%FAST%CHANGING%%WITH%EVOLUTION%%OF%TECHNOLOGY%

of(BifCultural(Hispanic(Millennials(look(for(recipes(

online((

75%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PLAYS%OF%THE%DAY:%Health(&(Wellness(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Source: IRI Infoscan TSV data: 52 Weeks Ending 1/24/16: Total US – MULO+C

%%OF%TOTAL%BUSINESS%BY%CLAIM%

CERTAIN%H&W%CLAIMS%ARE%MORE%ESTABLISHED%IN%BAKERY%

TOTAL%BAKERY% TOTAL%FOOD%&%BEV%

15%( 11%(

14%( 9%(

14%( 9%(

6%( 4%(

4%( 3%(

6

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Millennials(eat(out((most(at(lunch%

Four%smaller%meals%%a(day(at(nonf(

tradi&onal(&mes%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary. Source: ILD National Consumer Panel, Total US-MULO, Rolling 52 wks ending Mar 22, 2015, NBD Aligned

more(dollars(per(trip(vs.((Younger(&(Older(Boomers(($10.67%vs.%$9.94%vs.%$8.91%

Millennials%

less(deal(reliant(vs.((Younger(&(Older(Boomers((34.0%%vs.%35.9%%vs.%35.3%%

NOT%ONLY%ARE%THEIR%EATING%HABITS%DIFFERENT,%THE%WAY%THEY%SHOP%AT%THE%SUPERMARKETS%IS%ALSO%NOTE%WORTHY%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary. Source: ILD National Consumer Panel, Total US-MULO, Rolling 52 wks ending Mar 22, 2015, NBD Aligned

NOT%ONLY%ARE%THEIR%EATING%HABITS%DIFFERENT,%THE%WAY%THEY%SHOP%AT%THE%SUPERMARKETS%IS%

ALSO%NOTE%WORTHY%

larger(basket(size($65.27%vs.%$62.26%

more(dollars(per(trip(($10.03%vs.%$9.54%

less(deal(reliant(33.7%%vs.%35.5%%

Hispanics%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

LIFESTYLES%ARE%%FAST%CHANGING%%WITH%EVOLUTION%%OF%TECHNOLOGY%

of(BifCultural(Hispanic(Millennials(look(for(recipes(

online((

75%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PLAYS%OF%THE%DAY:%Health(&(Wellness(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Source: IRI Infoscan TSV data: 52 Weeks Ending 1/24/16: Total US – MULO+C

%%OF%TOTAL%BUSINESS%BY%CLAIM%

CERTAIN%H&W%CLAIMS%ARE%MORE%ESTABLISHED%IN%BAKERY%

TOTAL%BAKERY% TOTAL%FOOD%&%BEV%

15%( 11%(

14%( 9%(

14%( 9%(

6%( 4%(

4%( 3%(

6

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Millennials(eat(out((most(at(lunch%

Four%smaller%meals%%a(day(at(nonf(

tradi&onal(&mes%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary. Source: ILD National Consumer Panel, Total US-MULO, Rolling 52 wks ending Mar 22, 2015, NBD Aligned

more(dollars(per(trip(vs.((Younger(&(Older(Boomers(($10.67%vs.%$9.94%vs.%$8.91%

Millennials%

less(deal(reliant(vs.((Younger(&(Older(Boomers((34.0%%vs.%35.9%%vs.%35.3%%

NOT%ONLY%ARE%THEIR%EATING%HABITS%DIFFERENT,%THE%WAY%THEY%SHOP%AT%THE%SUPERMARKETS%IS%ALSO%NOTE%WORTHY%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary. Source: ILD National Consumer Panel, Total US-MULO, Rolling 52 wks ending Mar 22, 2015, NBD Aligned

NOT%ONLY%ARE%THEIR%EATING%HABITS%DIFFERENT,%THE%WAY%THEY%SHOP%AT%THE%SUPERMARKETS%IS%

ALSO%NOTE%WORTHY%

larger(basket(size($65.27%vs.%$62.26%

more(dollars(per(trip(($10.03%vs.%$9.54%

less(deal(reliant(33.7%%vs.%35.5%%

Hispanics%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

LIFESTYLES%ARE%%FAST%CHANGING%%WITH%EVOLUTION%%OF%TECHNOLOGY%

of(BifCultural(Hispanic(Millennials(look(for(recipes(

online((

75%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PLAYS%OF%THE%DAY:%Health(&(Wellness(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Source: IRI Infoscan TSV data: 52 Weeks Ending 1/24/16: Total US – MULO+C

%%OF%TOTAL%BUSINESS%BY%CLAIM%

CERTAIN%H&W%CLAIMS%ARE%MORE%ESTABLISHED%IN%BAKERY%

TOTAL%BAKERY% TOTAL%FOOD%&%BEV%

15%( 11%(

14%( 9%(

14%( 9%(

6%( 4%(

4%( 3%(

6

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Millennials(eat(out((most(at(lunch%

Four%smaller%meals%%a(day(at(nonf(

tradi&onal(&mes%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary. Source: ILD National Consumer Panel, Total US-MULO, Rolling 52 wks ending Mar 22, 2015, NBD Aligned

more(dollars(per(trip(vs.((Younger(&(Older(Boomers(($10.67%vs.%$9.94%vs.%$8.91%

Millennials%

less(deal(reliant(vs.((Younger(&(Older(Boomers((34.0%%vs.%35.9%%vs.%35.3%%

NOT%ONLY%ARE%THEIR%EATING%HABITS%DIFFERENT,%THE%WAY%THEY%SHOP%AT%THE%SUPERMARKETS%IS%ALSO%NOTE%WORTHY%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary. Source: ILD National Consumer Panel, Total US-MULO, Rolling 52 wks ending Mar 22, 2015, NBD Aligned

NOT%ONLY%ARE%THEIR%EATING%HABITS%DIFFERENT,%THE%WAY%THEY%SHOP%AT%THE%SUPERMARKETS%IS%

ALSO%NOTE%WORTHY%

larger(basket(size($65.27%vs.%$62.26%

more(dollars(per(trip(($10.03%vs.%$9.54%

less(deal(reliant(33.7%%vs.%35.5%%

Hispanics%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

LIFESTYLES%ARE%%FAST%CHANGING%%WITH%EVOLUTION%%OF%TECHNOLOGY%

of(BifCultural(Hispanic(Millennials(look(for(recipes(

online((

75%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

PLAYS%OF%THE%DAY:%Health(&(Wellness(

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Source: IRI Infoscan TSV data: 52 Weeks Ending 1/24/16: Total US – MULO+C

%%OF%TOTAL%BUSINESS%BY%CLAIM%

CERTAIN%H&W%CLAIMS%ARE%MORE%ESTABLISHED%IN%BAKERY%

TOTAL%BAKERY% TOTAL%FOOD%&%BEV%

15%( 11%(

14%( 9%(

14%( 9%(

6%( 4%(

4%( 3%(

7

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

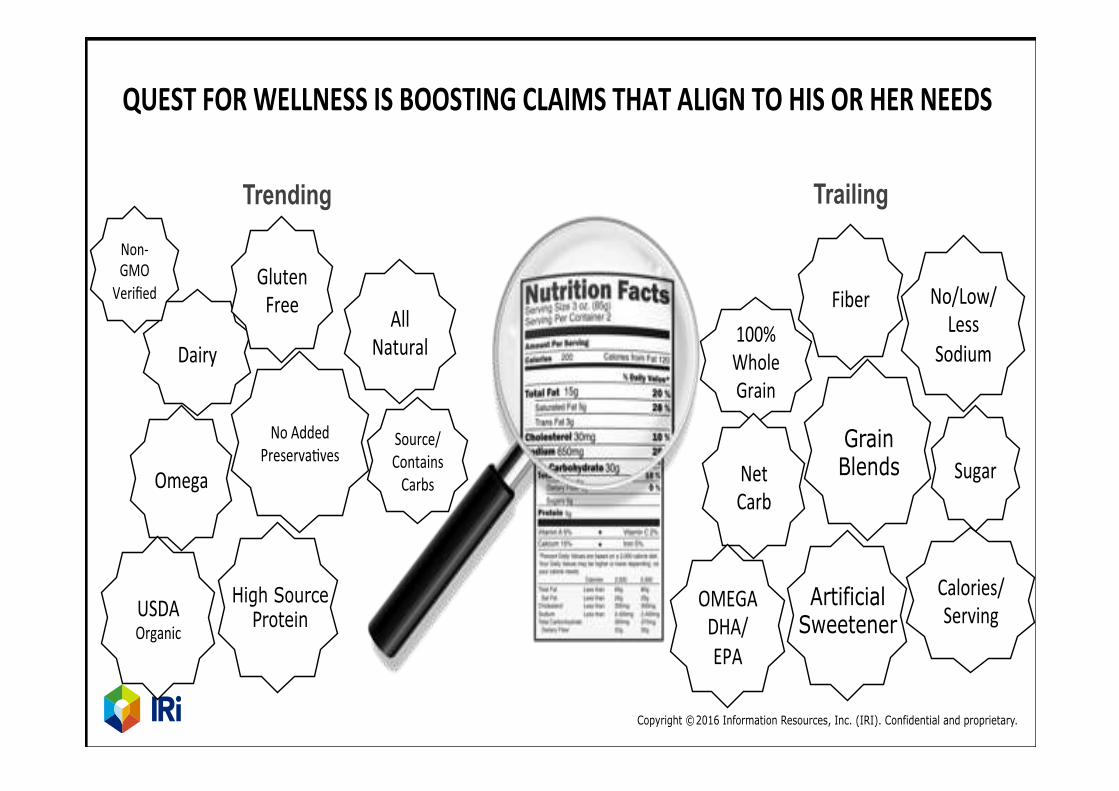

Trending

QUEST%FOR%WELLNESS%IS%BOOSTING%CLAIMS%THAT%ALIGN%TO%HIS%OR%HER%NEEDS%

Trailing

Dairy(

Omega(

Gluten(Free((

No(Added(Preserva&ves((

USDA(Organic(

All(Natural(

High Source Protein

Source/(Contains(Carbs(

NonfGMO(

Verified(

100%(Whole(Grain(

Net(Carb(

Fiber(

OMEGA(DHA/(EPA(

No/Low/Less(

Sodium(

Sugar(

Calories/(Serving(

Grain Blends

Artificial Sweetener

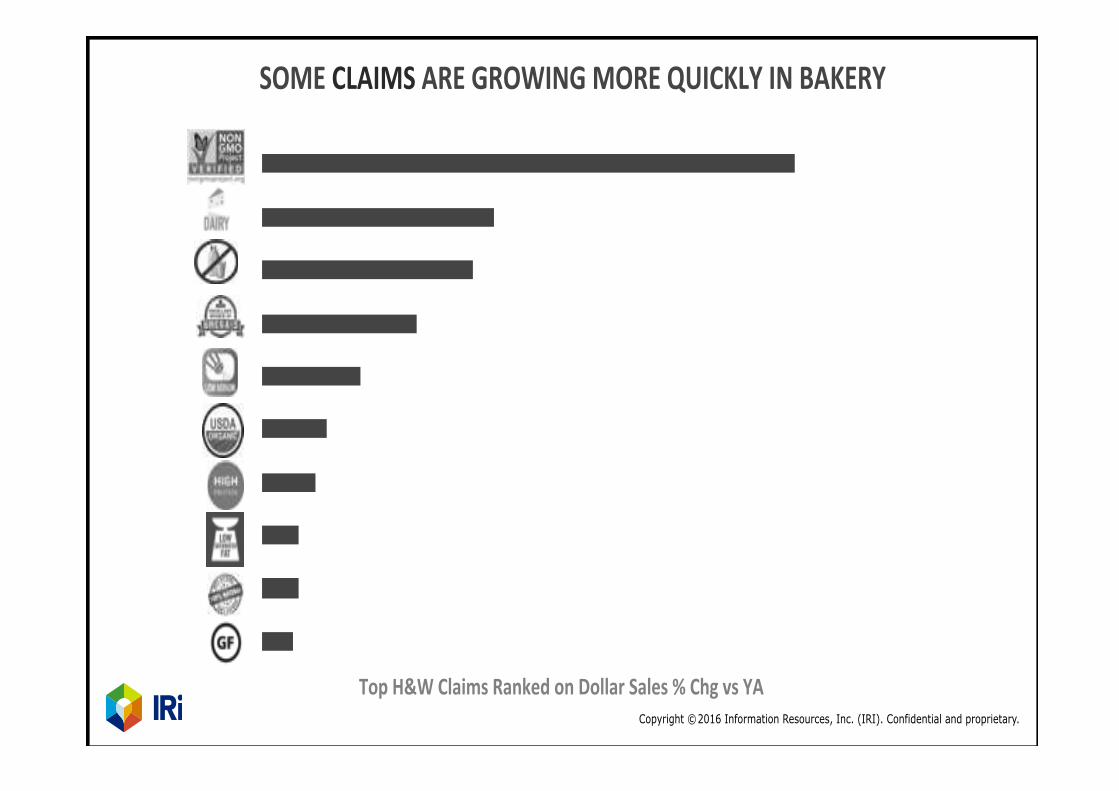

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

Top%H&W%Claims%Ranked%on%Dollar%Sales%%%Chg%vs%YA%

SOME%CLAIMS%ARE%GROWING%MORE%QUICKLY%IN%BAKERY%

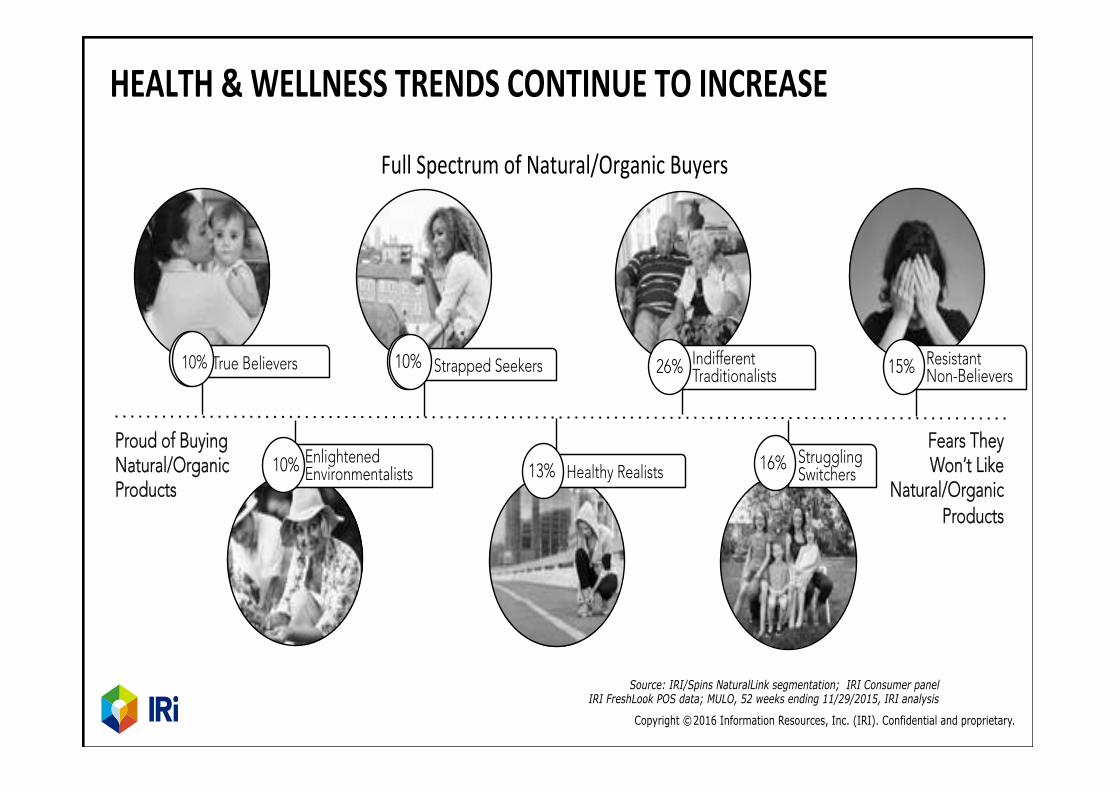

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

HEALTH%&%WELLNESS%TRENDS%CONTINUE%TO%INCREASE%

Fears They Won’t Like

Natural/Organic Products

Proud of Buying Natural/Organic Products

True Believers

Enlightened Environmentalists

Strapped Seekers Indifferent Traditionalists

Healthy Realists

Resistant Non-Believers

Struggling Switchers

10% 10% 26% 15%

16%13%10%

Full(Spectrum(of(Natural/Organic(Buyers(

Source: IRI/Spins NaturalLink segmentation; IRI Consumer panel IRI FreshLook POS data; MULO, 52 weeks ending 11/29/2015, IRI analysis

10% 10%

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

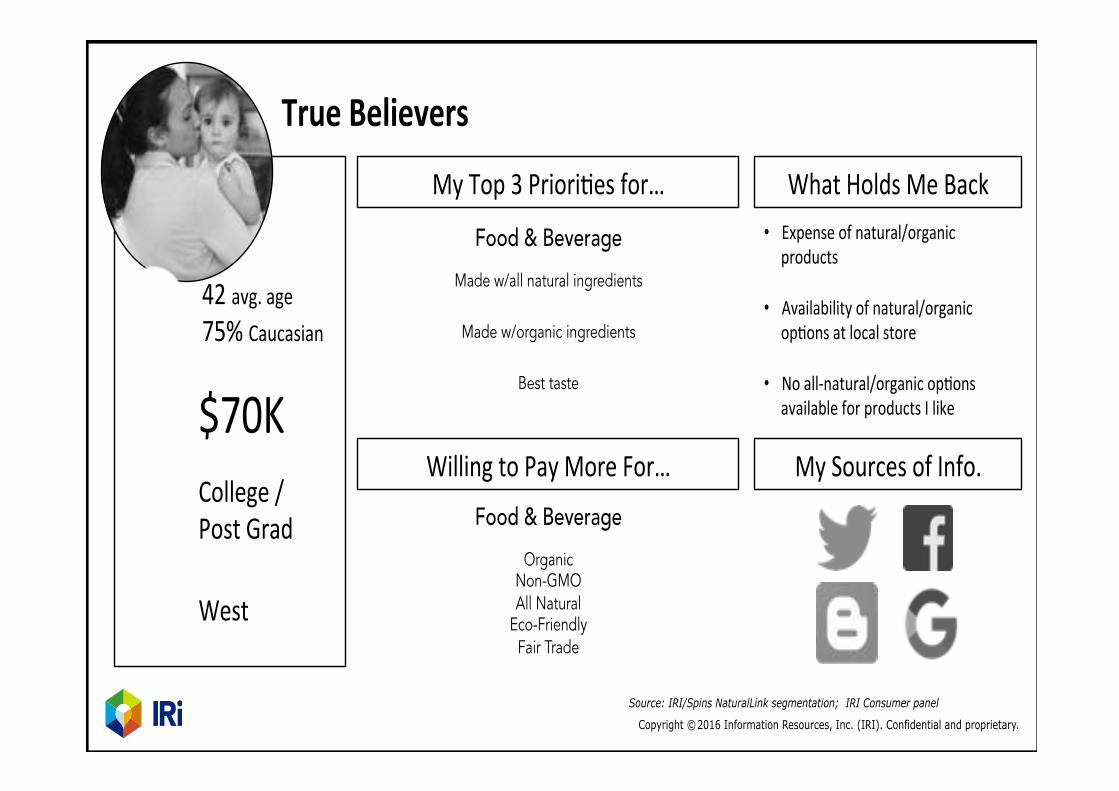

True%Believers%

$70K(College(/((Post(Grad(

West(

42(avg.(age(75%(Caucasian(

My(Top(3(Priori&es(for…(

Willing(to(Pay(More(For…(

What(Holds(Me(Back(

My(Sources(of(Info.(Food & Beverage

Organic Non-GMO All Natural

Eco-Friendly Fair Trade

• Expense(of(natural/organic(products(

• Availability(of(natural/organic(op&ons(at(local(store(

• No(allfnatural/organic(op&ons(available(for(products(I(like(

Source: IRI/Spins NaturalLink segmentation; IRI Consumer panel

Food & Beverage Made w/all natural ingredients

Made w/organic ingredients

Best taste

Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

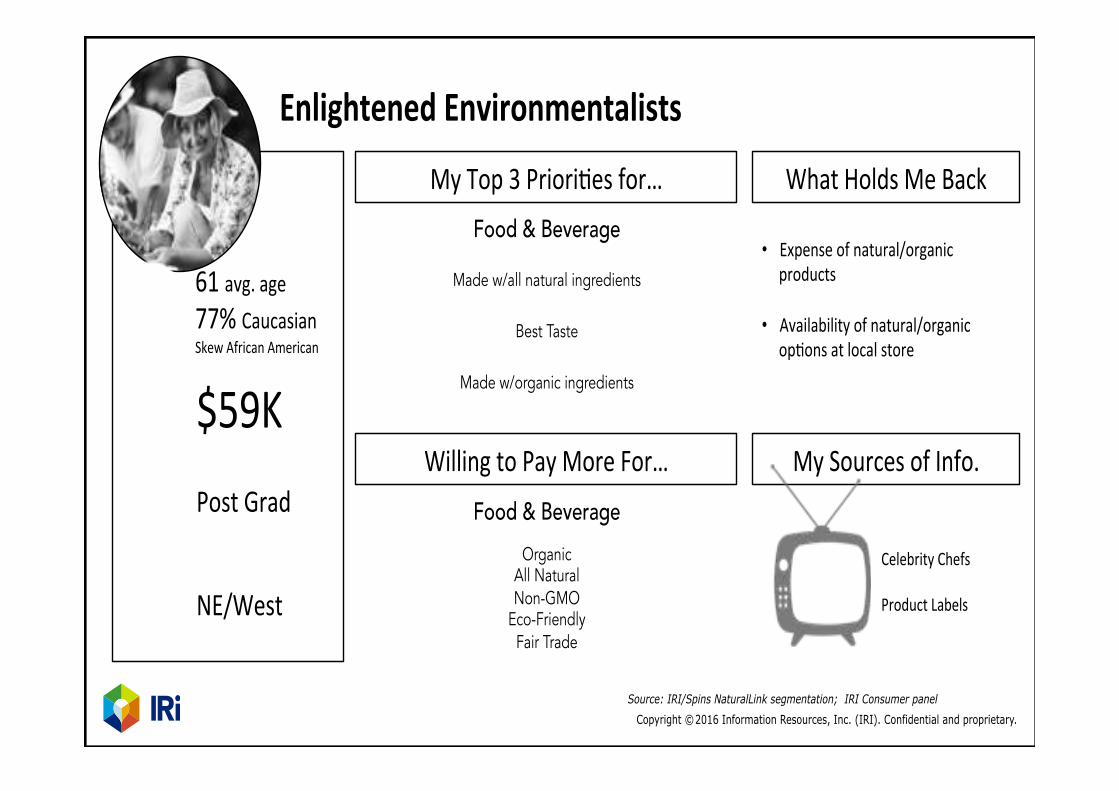

Enlightened%Environmentalists%

$59K(Post(Grad(

NE/West(

61(avg.(age(77%(Caucasian(Skew(African(American(

My(Top(3(Priori&es(for…(

Willing(to(Pay(More(For…(

What(Holds(Me(Back(

My(Sources(of(Info.(

Food & Beverage

Made w/all natural ingredients

Best Taste

Made w/organic ingredients

Food & Beverage Organic

All Natural Non-GMO

Eco-Friendly Fair Trade

• Expense(of(natural/organic(products(

• Availability(of(natural/organic(op&ons(at(local(store(

Celebrity(Chefs((Product(Labels(

Source: IRI/Spins NaturalLink segmentation; IRI Consumer panel Copyright ©�2016 Information Resources, Inc. (IRI). Confidential and proprietary.

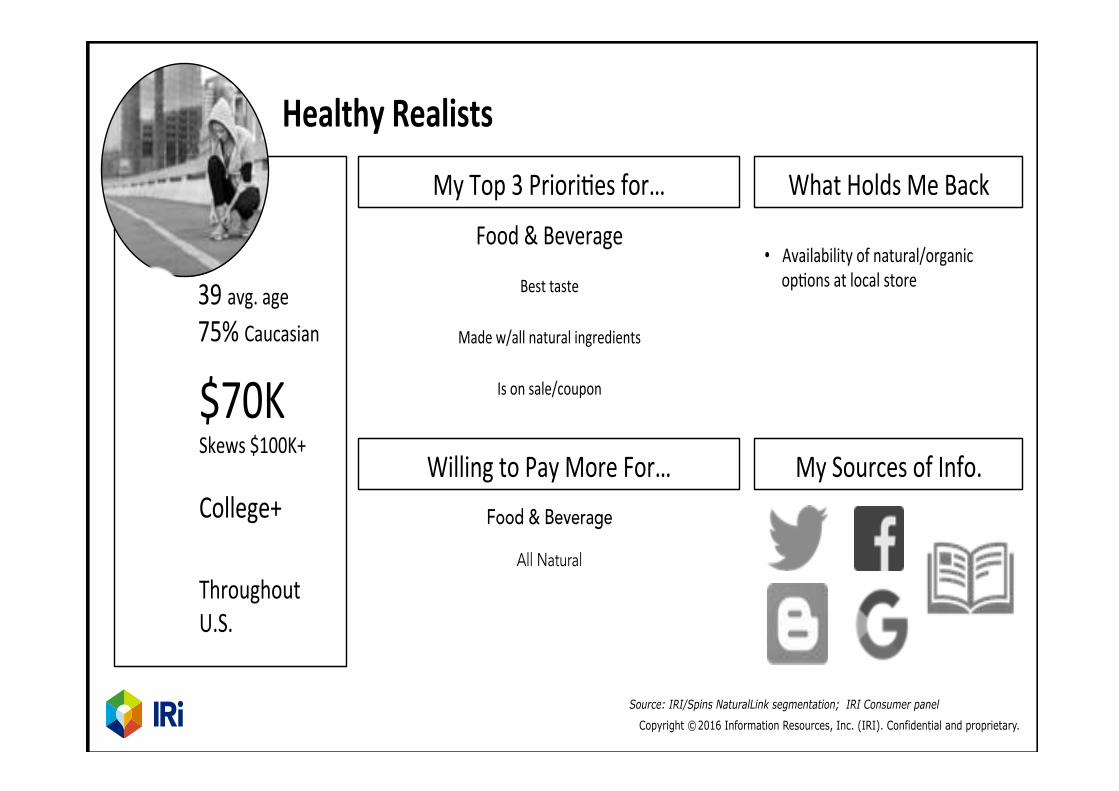

Healthy%Realists%

$70K(Skews($100K+(College+(

Throughout(U.S.(

39(avg.(age(75%(Caucasian(