Embed Size (px)

Citation preview

K.VAITHEESWARAN ADVOCATE & TAX CONSULTANT

Flat No.3, First Floor,

No.9, Thanikachalam Road,

T. Nagar,

Chennai - 600 017, India

Tel.: 044 + 2433 1029 / 4048

402, Front Wing,

House of Lords,

15/16, St. Marks Road,

Bangalore – 560 001, India

Tel : 080 22244854/ 41120804

Mobile: 98400-96876

E-mail : [email protected] [email protected]

www.vaithilegal.com

"Let us not take this planet for granted. I do not take tonight for granted.“ – Acceptance speech by Leonardo on 29.02.2016 on receipt of the Oscar Award.

The Annual Budget is also an opportunity for the Government to outline its priorities for the year to come. The priority of our Government is clearly to provide additional resources for vulnerable sections, rural areas and social and physical infrastructure creation. Our agenda for the next year is, therefore, to ‘Transform India’ in this direction. My Budget proposals are, therefore, built on this transformative agenda with nine distinct pillars….Finance Minister Mr. Arun Jaitley on 29.02.2016

This entire presentation is linked with Oscar Awards and other film titles including Tamil Films.

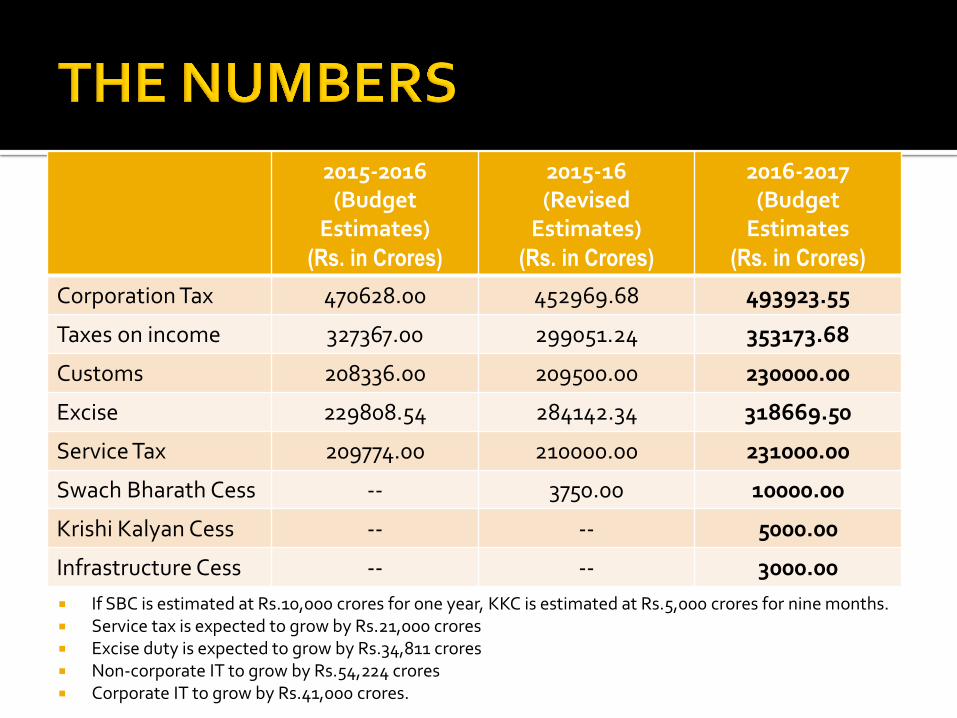

2015-2016 (Budget

Estimates) (Rs. in Crores)

2015-16 (Revised

Estimates) (Rs. in Crores)

2016-2017 (Budget

Estimates (Rs. in Crores)

Corporation Tax 470628.00 452969.68 493923.55

Taxes on income 327367.00 299051.24 353173.68

Customs 208336.00 209500.00 230000.00

Excise 229808.54 284142.34 318669.50

Service Tax 209774.00 210000.00 231000.00

Swach Bharath Cess -- 3750.00 10000.00

Krishi Kalyan Cess -- -- 5000.00

Infrastructure Cess -- -- 3000.00

If SBC is estimated at Rs.10,000 crores for one year, KKC is estimated at Rs.5,000 crores for nine months. Service tax is expected to grow by Rs.21,000 crores Excise duty is expected to grow by Rs.34,811 crores Non-corporate IT to grow by Rs.54,224 crores Corporate IT to grow by Rs.41,000 crores.

Excise duty of 1% without cenvat credit and 12.5% with cenvat credit on articles of jewellery (excluding articles of silver jewellery other than those studded with diamonds, ruby, emerald or sapphire).

2005 story. 2011 story. SSI exemption increased to Rs.6 crores in a year provided the clearances

did not exceed Rs.12 crores in the preceding financial year. Levy from 01.03.2016 and for month of March 2016 exemption

restricted to Rs.50 lakhs. Where manufacturer has centralized billing or accounting system in

respect of these goods manufactured by different factories or premises and opts for registering only the factory from where centralized billing or accounting is done and where the account / records showing receipt of raw materials / finished excisable goods manufactured or received back from job workers or kept.

Option to obtain separate registration.

No stock declaration required to be made to the Department but jewellery manufacturer is required to keep declaration of finished goods / goods in process / inputs as on 29.02.2016 duly certified by a CA.

Registration within two days. Records maintained for State VAT or BIS enough for excise. Simplified return. Job work. Practical problems.

Existing Section 37B of the Central Excise Act empowers CBEC to issue orders / instructions / directions to Central Excise Officers for the purpose of uniformity in the classification of excisable goods or with respect to levy of excise duty.

The Supreme Court in the case of UCO Bank Vs. Commissioner of Income Tax (1999) 111 ELT 673 has held that Departmental Circulars are not meant for contradicting or nullifying any provisions of the statute but are meant for ensuring proper and efficient administration of the statute.

The Constitution Bench of the Supreme Court in the case of CCE Vs. Ratan Melting and Wire Industries (2008) 231 ELT 22 has held that a Circular, which is contrary to the statutory provisions, has really no existence in law.

Section 37B being amended to expand the scope to cover for the implementation of any other provision of this Act.

Duty originally introduced on branded readymade garments from 01.03.2011 and made optional from 01.03.2013.

Excise duty introduced on readymade garments and made up articles of textiles falling under Chapter 61, 62 and 63 except those falling under 6309.

2% without Cenvat Credit and 12.5% with Cenvat Credit. The levy is restricted to articles which have RSP of Rs.1000/- and above

when they bear or are sold under a brand name. Tariff value shall be 60% of the RSP. Levy not applicable to retail tailoring establishments that stitch

garments in a customized manner. Brand name owner who gets manufactured on his own account on job

work shall pay the duty as if goods were manufactured by him. Brand owner is required to register under central excise.

Brand name owner can authorise the job worker to pay duty. Job worker to get registered.

Excisable goods manufactured on or before 29.02.2016 but lying in stock as on 29.02.2016 shall attract excise duty upon clearance.

Manufacturers to keep stock declaration of finished goods, goods in progress and inputs as on 29.02.2016 in their records duly certified by a CA so as to enable cenvat credit claim on inputs or inputs contained in goods lying in stock.

No stock declaration required to be made to the jurisdictional central excise authorities.

Previous instructions dated 28.02.2011 applicable.

BCD on golf cars increased from 10% to 60%. ED on waters including mineral waters and aerated waters

containing added sugar or other sweetening matter or flavoured increased from 18% to 21%.

Steep increase in ED on all lengths of non-filter and filter cigarettes.

ED on ATF increased from 8% to 14%. Clean energy cess renamed as Clean environment cess and

increased from Rs.300 to Rs.400 per ton. and effective rate increased from Rs.200 per ton. to Rs.400 per ton.

BCD of 10% on plans, drawings and designs.

BCD / CVD / SAD on charger / adapter / battery and wired headsets / speakers used in the manufacture of mobile handsets including cell phones.

BCD / ED / CVD / SAD exempted on inputs and parts for manufacture of charger / adapter / battery / wired headsets / speakers of mobile handsets including cell phones and inputs and sub-parts for use in manufacture these parts.

4% without cenvat and 12.5% with cenvat on routers, broadband modems, STP for gaining access to internet, CCTV camera, digital video recorder, network video recorder, reception apparatus for television not designed to incorporate video display.

BCD / ED / CVD / SAD exempt on parts components and accessories for use in the manufacture of routers, broadband modems, etc.

Normal period for issue of show cause notice

2 years for Central Excise and Customs

2 and half years for Service Tax.

Against concept of ease of doing business.

Services provided by a Senior Advocate to an Advocate or partnership firm of Advocates taxable from 01.04.2016.

Originally in respect of all legal services, reverse charge mechanism was applicable when the services are provided to business entities.

Service Tax Rules amended whereby in respect of service provided or agreed to be provided by a firm of advocates or an individual advocate other than a Senior Advocate by way of legal services, the business entity shall be liable to pay service tax.

Legal services of a senior advocate to a person other than a person ordinarily carrying out any activity relating to industry, commerce or any other business or profession is exempted.

Non-senior advocates / firms – services to law firms or advocate or any person other than a business entity or business entity upto Rs.10 lakhs turnover continues to be exempt.

Services of a person represented on an Arbitral Tribunal to an Arbitral Tribunal taxable.

Earlier exemption through Notification No.25/2012 withdrawn from 01.04.2016.

Section 2(d) of the Arbitration and Conciliation Act, 1996 defines ‘Arbitral Tribunal’ to mean a sole arbitrator or a panel of arbitrators.

Concept of service Under the new Section 11(14), High Court is to frame Rules for

determination of fees of the Arbitral Tribunal. Sole Arbitrator ?

Transportation of passengers with or without accompanied belongings by ropeway, cable car or aerial tramway is taxable.

Gulmarg Gondola, Manali Ropeway, Raigad Ropeway, Glenmorgan Ropeway, Srisailam Ropeway, etc.

Section 66D(o)(i) which refers to service of transportation of passengers with or without accompanied belongings by a stage carriage is deleted from 01.06.2016.

Services by a non-air-conditioned contract carriage continues to be exempt.

Service of transportation of passengers by air-conditioned stage carriage taxable with an abatement of 60% w.e.f. 01.06.2016.

Section 72 of the MV Act deals with ‘grant of stage carriage permit’ by an RTO and Section 74 deals with ‘grant of contract carriage permit’.

Construction, erection, commissioning or installation of original works pertaining to monorail or metro is withdrawn in respect of contracts entered into on or after 01.03.2016.

Where contracts have been entered into before 01.03.2016 on which appropriate stamp duty has been paid, exemption continues.

Similar exemption in respect of railway continues.

Is there a difference between railway and metro?

The Supreme Court in the case of Shahdara (Delhi) Sharanpur Light Railways Co. Ltd. Vs. Municipal Board (1967) AIR 1747 in the context of the Indian Railways Act, 1890 has held that when all the provisions of the Railways Act have been extended to the appellant and the appellant is a ‘railway’ as commonly understood then it would remain a railway notwithstanding the fact that it is registered as a tramway under the Tramways Act.

Section 2(p) of the Metro Railway (Operation and Maintenance) Act, 2002 defines ‘railway’ and provides that railway shall have the meaning assigned to it in Section 2(31) of the Railway Act, 1989.

Pre 01.07.2012 in respect of services provided by agent or distributors to MF or AMC, service tax was payable by MF or AMC.

Post 01.07.2012, services of agent or distributor to MF or AMC was exempted.

Exemption withdrawn from 01.04.2015 and MF or AMC made liable under reverse charge mechanism.

Services by mutual fund agents / distributors to MF or AMC taxable from 01.04.2016.

Section 66D(p)(ii) referring to services by way of transportation of goods by an aircraft or a vessel from a place outside India upto the customs station of clearance in India deleted w.e.f. 01.06.2016.

Services by way of transportation of goods by an aircraft from a place outside India upto the customs station of clearance in India exempted from 01.06.2016.

Similar exemption not available for shipping

TRU Circular dated 29.02.2016 states that domestic shipping line registered in

India shall pay service tax and if the services are availed from foreign shipping

line by a business entity located in India, reverse charge would apply.

Service received from foreign shipping line by a business entity located in India

taxable under RCM.

Under customs law, freight forms part of value for the purpose of customs duty.

Internationally, there is no GST or VAT on international transportation of goods.

Freight forwarding in imports.

Section 158 of the Finance Bill, 2016 provides for a levy of Krishi Kalyan Cess (KKC) as service tax on all or any of the taxable services at the rate of 0.5% on the value of such services for the purposes of the Union for financing and promoting initiatives to improve agriculture or for any other purpose relating thereto.

Levy in addition to service tax and other cess.

Proceeds to be credited to the consolidated fund of India and the Central

Government after due appropriation by Parliament by law use it for such

purposes as specified above.

Effective 01.06.2016.

Board Circular indicates availability of cenvat credit though there is no

amendment to CCR.

Section 66D(l) dealing with pre-school education; higher secondary; education as part of a curriculum for qualification recognized by law; education as part of an approved vocational educational course proposed to be deleted.

Board Circular states that these services are proposed to be omitted from the Negative List but the service tax exemption on them is being continued by incorporating them in Notification No.25/2012 as amended by Notification No.9/2016.

No such exemption in Notification No.9/2016 except IIM, etc.

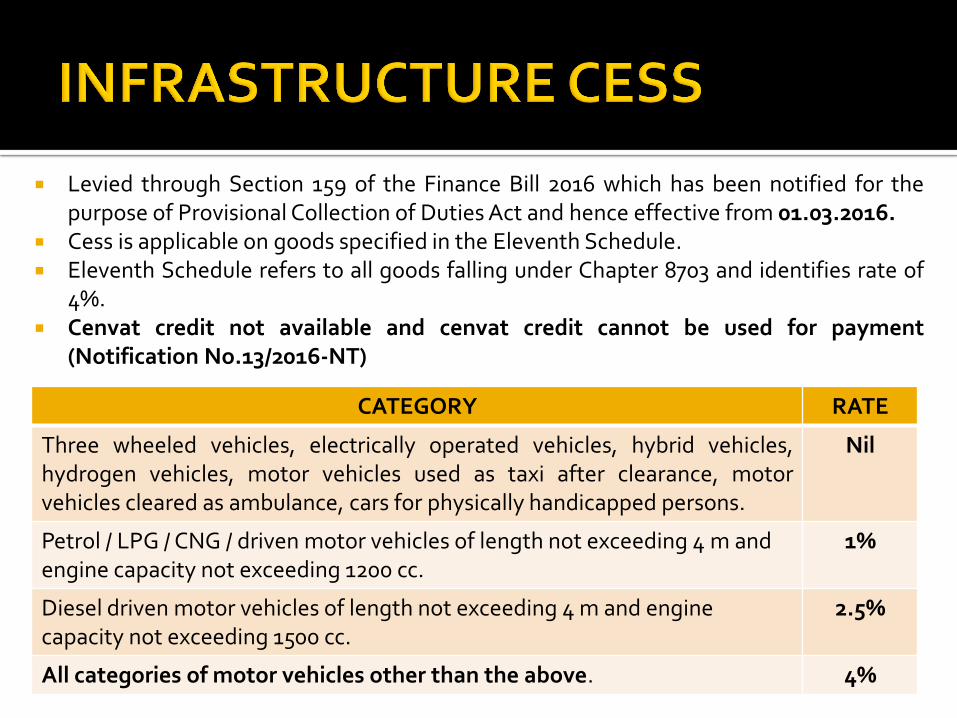

Levied through Section 159 of the Finance Bill 2016 which has been notified for the purpose of Provisional Collection of Duties Act and hence effective from 01.03.2016.

Cess is applicable on goods specified in the Eleventh Schedule. Eleventh Schedule refers to all goods falling under Chapter 8703 and identifies rate of

4%. Cenvat credit not available and cenvat credit cannot be used for payment

(Notification No.13/2016-NT)

CATEGORY RATE

Three wheeled vehicles, electrically operated vehicles, hybrid vehicles, hydrogen vehicles, motor vehicles used as taxi after clearance, motor vehicles cleared as ambulance, cars for physically handicapped persons.

Nil

Petrol / LPG / CNG / driven motor vehicles of length not exceeding 4 m and engine capacity not exceeding 1200 cc.

1%

Diesel driven motor vehicles of length not exceeding 4 m and engine capacity not exceeding 1500 cc.

2.5%

All categories of motor vehicles other than the above. 4%

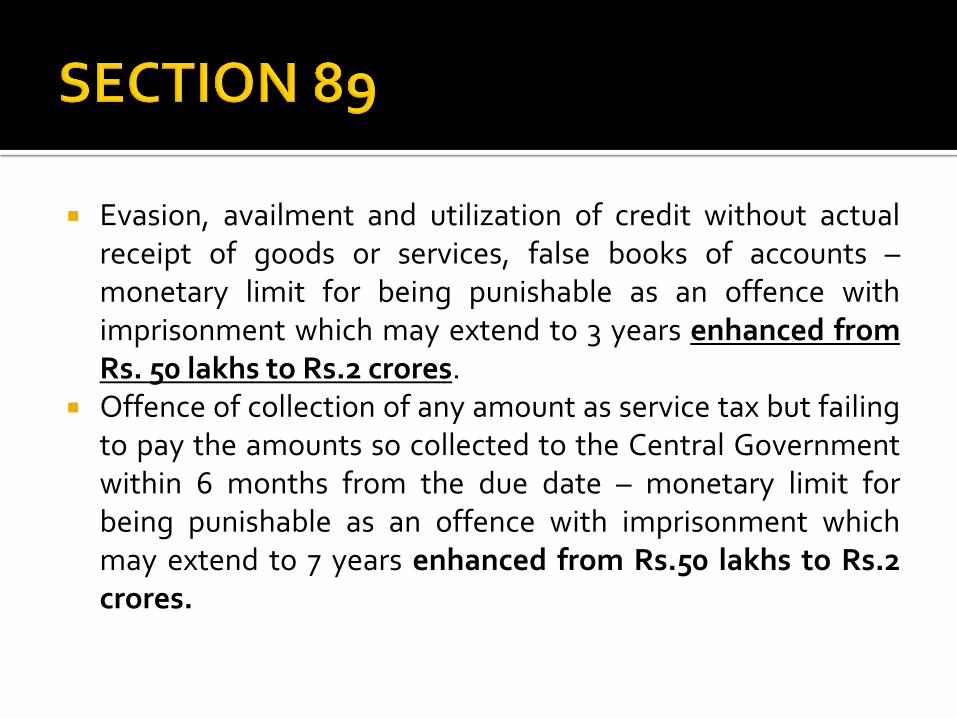

Evasion, availment and utilization of credit without actual receipt of goods or services, false books of accounts – monetary limit for being punishable as an offence with imprisonment which may extend to 3 years enhanced from Rs. 50 lakhs to Rs.2 crores.

Offence of collection of any amount as service tax but failing to pay the amounts so collected to the Central Government within 6 months from the due date – monetary limit for being punishable as an offence with imprisonment which may extend to 7 years enhanced from Rs.50 lakhs to Rs.2 crores.

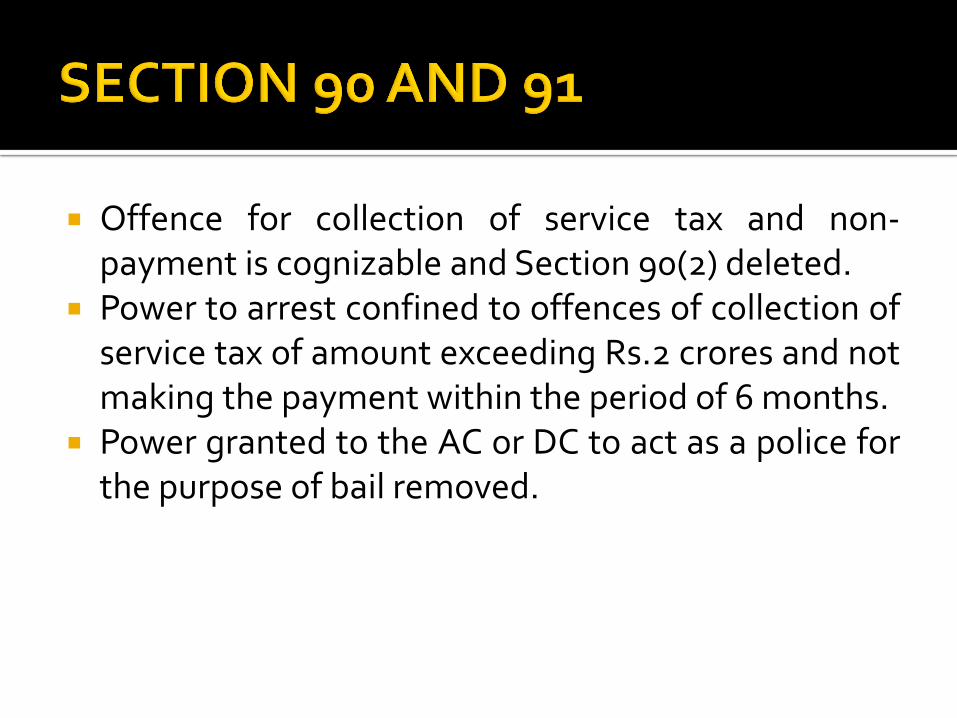

Offence for collection of service tax and non-payment is cognizable and Section 90(2) deleted.

Power to arrest confined to offences of collection of service tax of amount exceeding Rs.2 crores and not making the payment within the period of 6 months.

Power granted to the AC or DC to act as a police for the purpose of bail removed.

Originally, Notification No.4/1997, C.E. provided for exemption from excise duty in respect of certain goods through Serial No.51 and falling under Chapter 38 of the Central Excise Tariff Act. The Notification referred to

“Concrete mix manufactured at the site of construction for use in construction work at such site.”

In the case of Larsen & Toubro , the Company was constructing its own cement plant at Ananthapur and for the purpose of construction of civil structure, the concrete mix was prepared at site with the help of machinery and captively consumed in the construction of the plant.

The Company claimed the benefit of exemption from excise duty under Notification No.4/1997.

K.Vaitheeswaran - All Copyrights Reserved

Exemption was denied and ED was imposed on the ground that the way L&T produced the concrete mix by using machinery at site indicates that the product is ready mix concrete and not concrete mix.

What distinguishes ready mix concrete (RMC) from concrete mix (CM) is the manner in which it is manufactured, the high degree of precision, and the stringent quality control over the mix of ingredients.

The Tribunal observed that the facility put up by L&T involved various machines coupled with sophisticated process which was indicative of the fact that it was for the manufacture of RMC and the only reason for manufacture thereof at site was that the larger quantities of RMC which was required by L&T.

K.Vaitheeswaran - All Copyrights Reserved

The Tribunal held that it is a high degree of precision and stringent quality control observed in the selection and processing of ingredients namely aggregates, cement, sand, additives and water which made the product as RMC in contra distinction with CM.

The Supreme Court in the case of Larsen & Toubro Ltd. Vs. CCE vide judgment dated 06.10.2015 has held that (i) It is the process of mixing the concrete that differentiates between

Concrete Mix (CM) and Ready Mix Concrete (RMC).

(ii) RMC and CM are different and the exemption Notification exempts only CM.

(iii) It is only the process that would determine whether the produce could be termed as CM or RMC.

K.Vaitheeswaran - All Copyrights Reserved

(iv) RMC is an expression now well understood in the market and used to refer to a commodity bought and sold with clearly distinguishable features and characteristics as regards the plant and machinery required to be set up for its manufacture and the manufacturing process involved as well as its own properties and the manner of delivery.

(v) The earlier decision of the Supreme Court in the case of Simplex Infrastructures has not discussed whether RMC is different from CM.

The Supreme Court remanded the matter to the Assessing Officer to look into the matter afresh keeping the observations in the judgment.

K.Vaitheeswaran - All Copyrights Reserved

K.Vaitheeswaran - All Copyrights Reserved

K.Vaitheeswaran - All Copyrights Reserved

Sl. No.144 in Notification No.12/2012 provides for an exemption in respect of Chapter 38 being concrete mix manufactured at the site of construction for use in construction work at such site.

The industry has been availing exemption in respect of the mix that is manufactured at the site.

K.Vaitheeswaran - All Copyrights Reserved

Entry 144, Notification No.12/2012 substituted. Concrete Mix or Ready-mix Concrete (RMC), manufactured at the site of construction for use in construction work at such site. Explanation. – For the purpose of this entry, the expression “site” means any premises made available for the manufacture of goods by way of a specific mention in the contract or agreement for such construction work, provided that the goods manufactured at such premises are solely used in the said construction work only.

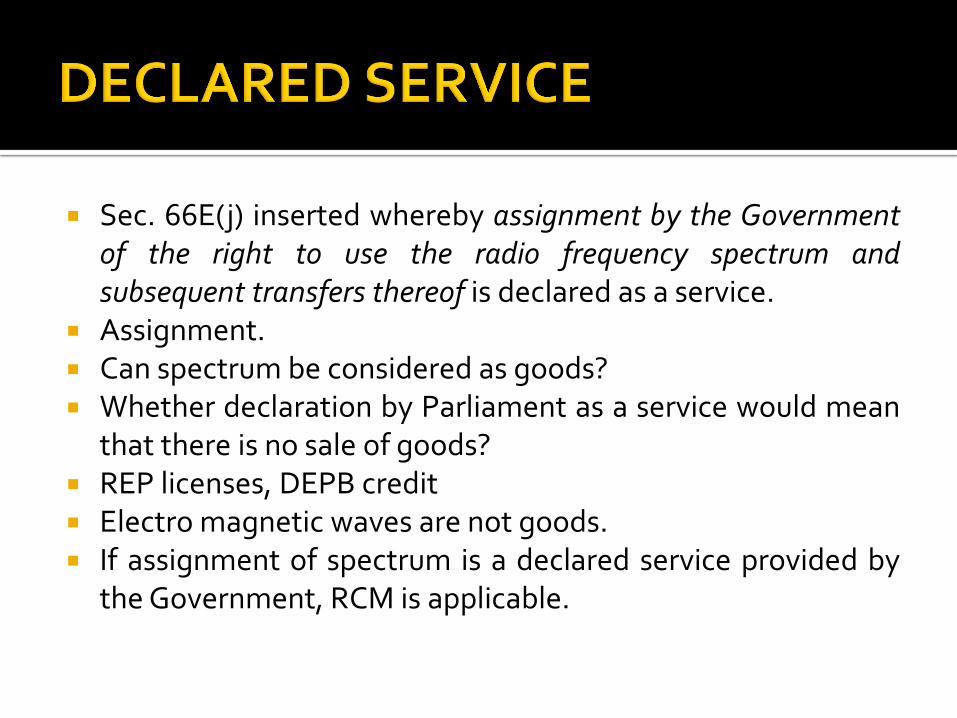

Sec. 66E(j) inserted whereby assignment by the Government of the right to use the radio frequency spectrum and subsequent transfers thereof is declared as a service.

Assignment. Can spectrum be considered as goods? Whether declaration by Parliament as a service would mean

that there is no sale of goods? REP licenses, DEPB credit Electro magnetic waves are not goods. If assignment of spectrum is a declared service provided by

the Government, RCM is applicable.

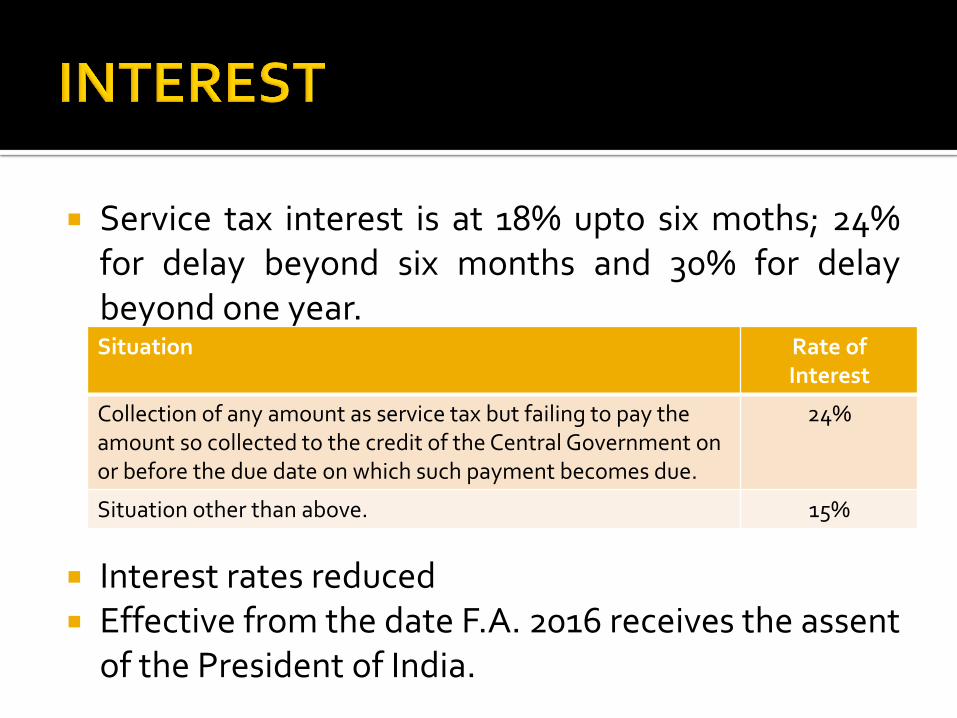

Service tax interest is at 18% upto six moths; 24% for delay beyond six months and 30% for delay beyond one year.

Interest rates reduced Effective from the date F.A. 2016 receives the assent

of the President of India.

Situation Rate of Interest

Collection of any amount as service tax but failing to pay the amount so collected to the credit of the Central Government on or before the due date on which such payment becomes due.

24%

Situation other than above. 15%

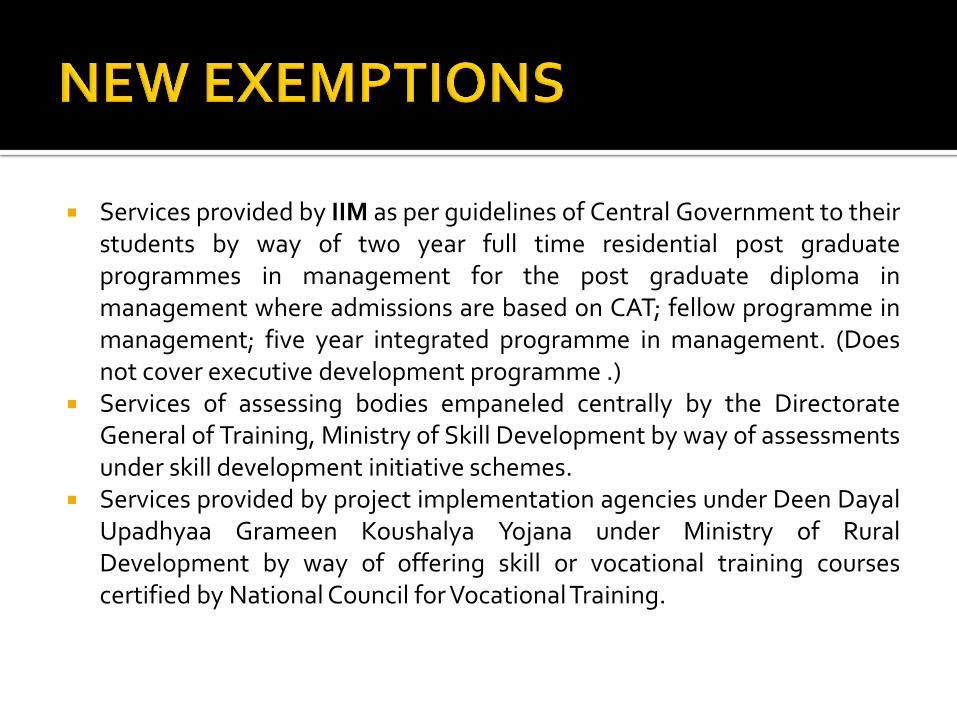

Services provided by IIM as per guidelines of Central Government to their students by way of two year full time residential post graduate programmes in management for the post graduate diploma in management where admissions are based on CAT; fellow programme in management; five year integrated programme in management. (Does not cover executive development programme .)

Services of assessing bodies empaneled centrally by the Directorate General of Training, Ministry of Skill Development by way of assessments under skill development initiative schemes.

Services provided by project implementation agencies under Deen Dayal Upadhyaa Grameen Koushalya Yojana under Ministry of Rural Development by way of offering skill or vocational training courses certified by National Council for Vocational Training.

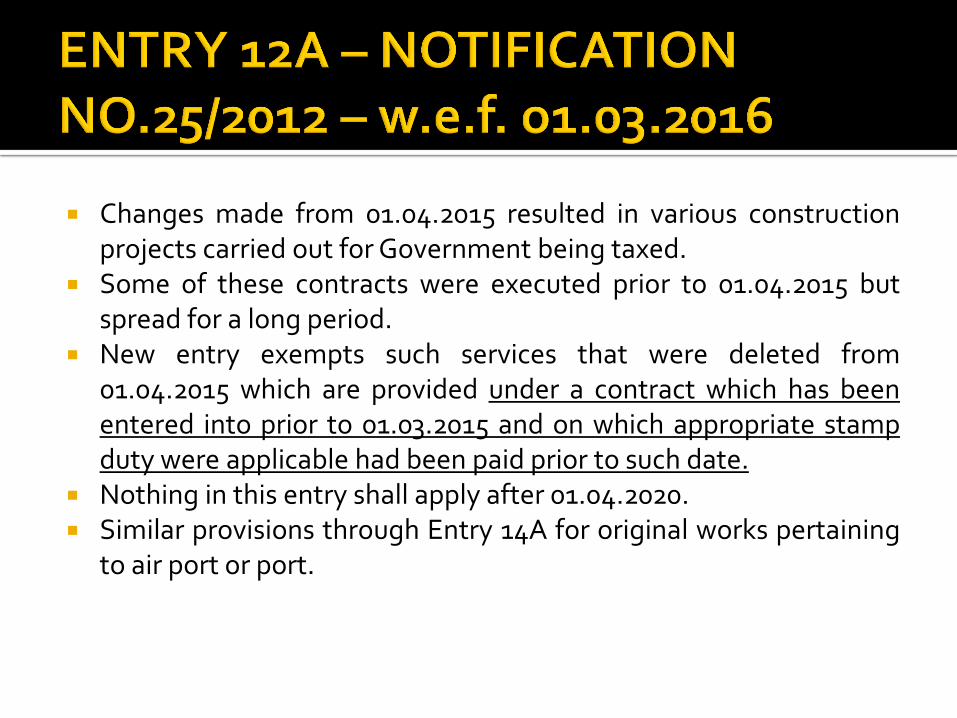

Changes made from 01.04.2015 resulted in various construction projects carried out for Government being taxed.

Some of these contracts were executed prior to 01.04.2015 but spread for a long period.

New entry exempts such services that were deleted from 01.04.2015 which are provided under a contract which has been entered into prior to 01.03.2015 and on which appropriate stamp duty were applicable had been paid prior to such date.

Nothing in this entry shall apply after 01.04.2020. Similar provisions through Entry 14A for original works pertaining

to air port or port.

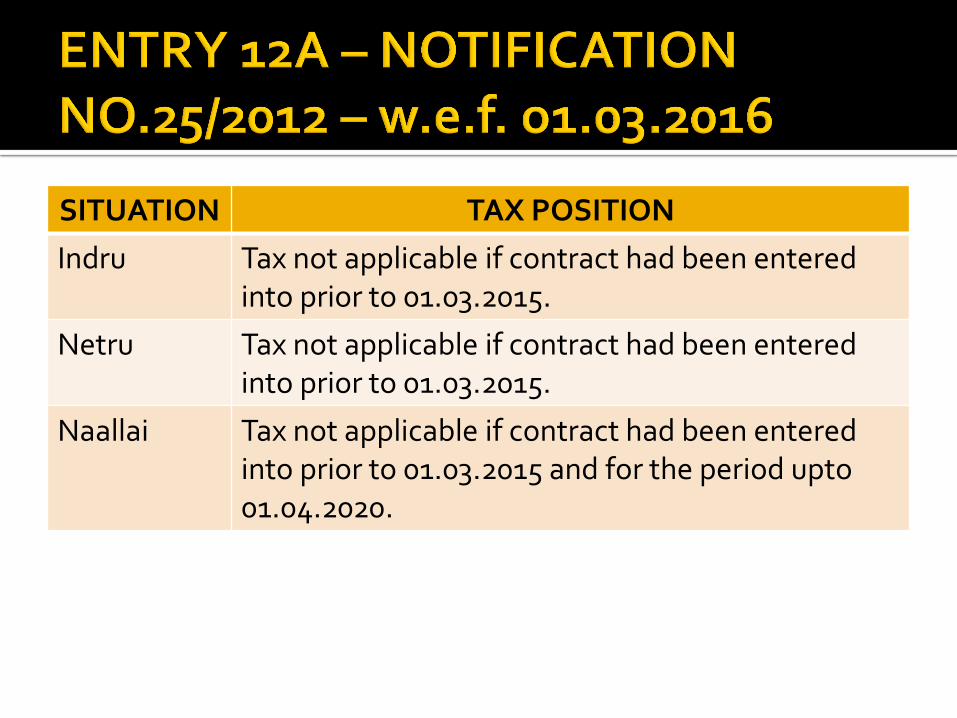

SITUATION TAX POSITION

Indru Tax not applicable if contract had been entered into prior to 01.03.2015.

Netru Tax not applicable if contract had been entered into prior to 01.03.2015.

Naallai Tax not applicable if contract had been entered into prior to 01.03.2015 and for the period upto 01.04.2020.

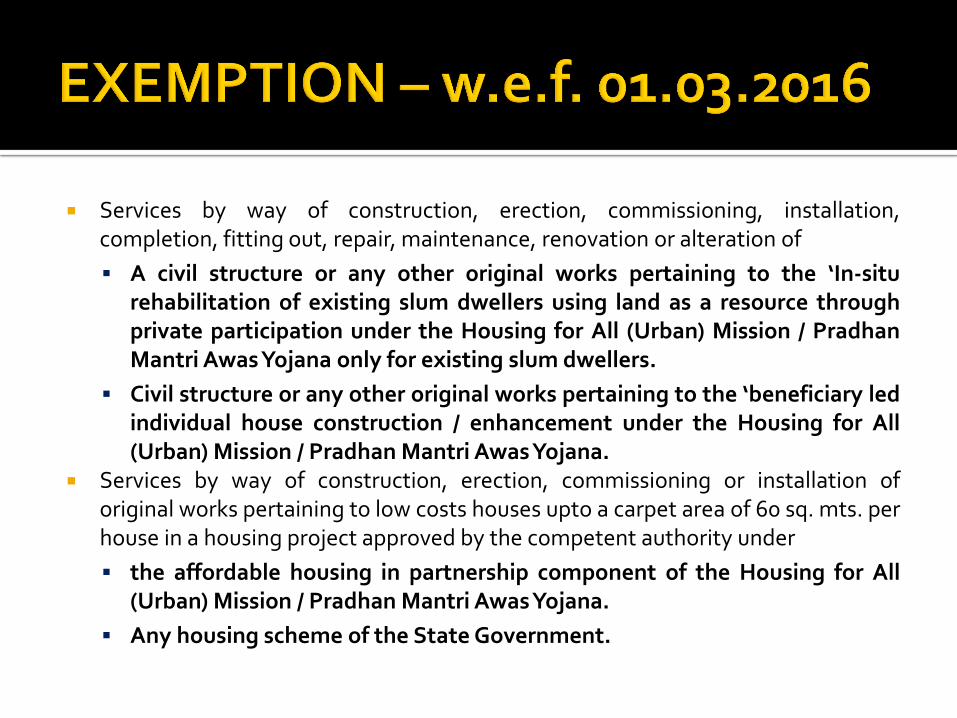

Services by way of construction, erection, commissioning, installation, completion, fitting out, repair, maintenance, renovation or alteration of

A civil structure or any other original works pertaining to the ‘In-situ rehabilitation of existing slum dwellers using land as a resource through private participation under the Housing for All (Urban) Mission / Pradhan Mantri Awas Yojana only for existing slum dwellers.

Civil structure or any other original works pertaining to the ‘beneficiary led individual house construction / enhancement under the Housing for All (Urban) Mission / Pradhan Mantri Awas Yojana.

Services by way of construction, erection, commissioning or installation of original works pertaining to low costs houses upto a carpet area of 60 sq. mts. per house in a housing project approved by the competent authority under

the affordable housing in partnership component of the Housing for All (Urban) Mission / Pradhan Mantri Awas Yojana.

Any housing scheme of the State Government.

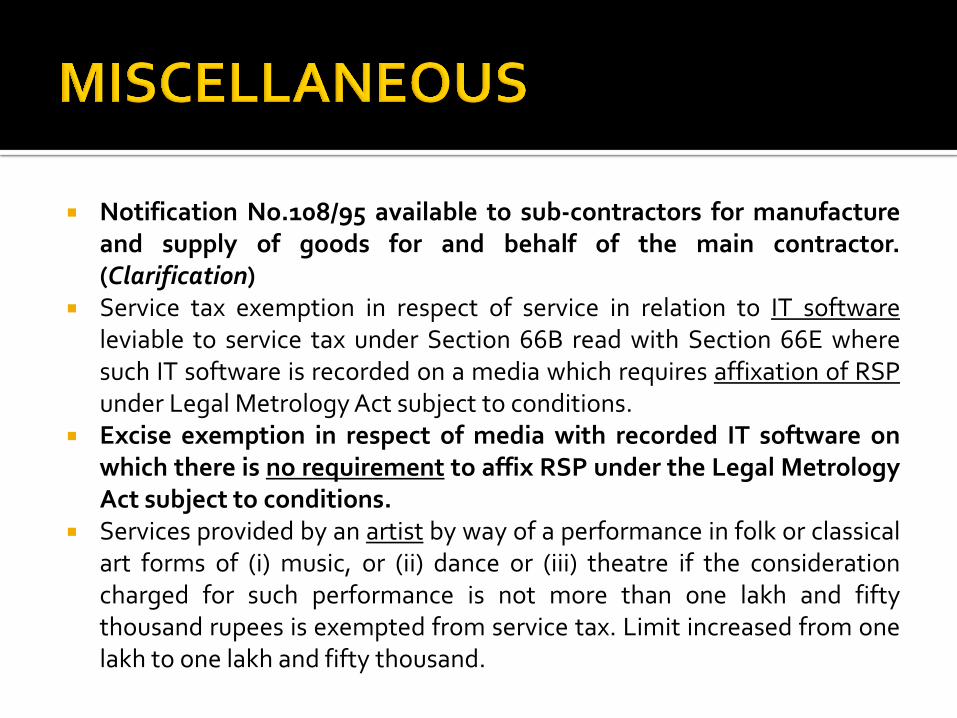

Notification No.108/95 available to sub-contractors for manufacture and supply of goods for and behalf of the main contractor. (Clarification)

Service tax exemption in respect of service in relation to IT software leviable to service tax under Section 66B read with Section 66E where such IT software is recorded on a media which requires affixation of RSP under Legal Metrology Act subject to conditions.

Excise exemption in respect of media with recorded IT software on which there is no requirement to affix RSP under the Legal Metrology Act subject to conditions.

Services provided by an artist by way of a performance in folk or classical art forms of (i) music, or (ii) dance or (iii) theatre if the consideration charged for such performance is not more than one lakh and fifty thousand rupees is exempted from service tax. Limit increased from one lakh to one lakh and fifty thousand.

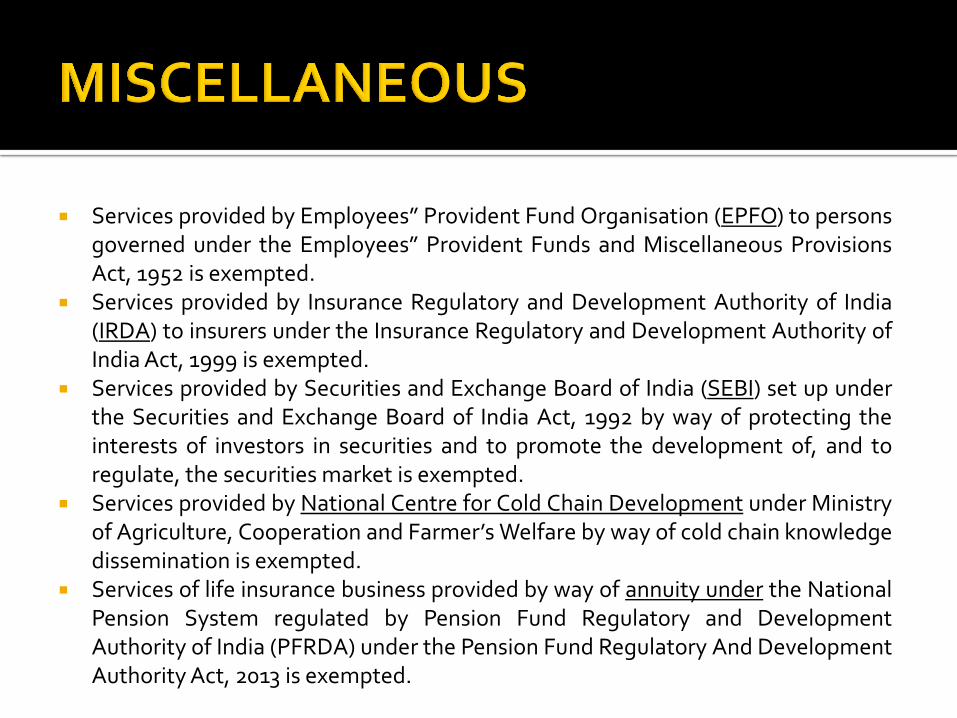

Services provided by Employees” Provident Fund Organisation (EPFO) to persons governed under the Employees” Provident Funds and Miscellaneous Provisions Act, 1952 is exempted.

Services provided by Insurance Regulatory and Development Authority of India (IRDA) to insurers under the Insurance Regulatory and Development Authority of India Act, 1999 is exempted.

Services provided by Securities and Exchange Board of India (SEBI) set up under the Securities and Exchange Board of India Act, 1992 by way of protecting the interests of investors in securities and to promote the development of, and to regulate, the securities market is exempted.

Services provided by National Centre for Cold Chain Development under Ministry of Agriculture, Cooperation and Farmer’s Welfare by way of cold chain knowledge dissemination is exempted.

Services of life insurance business provided by way of annuity under the National Pension System regulated by Pension Fund Regulatory and Development Authority of India (PFRDA) under the Pension Fund Regulatory And Development Authority Act, 2013 is exempted.

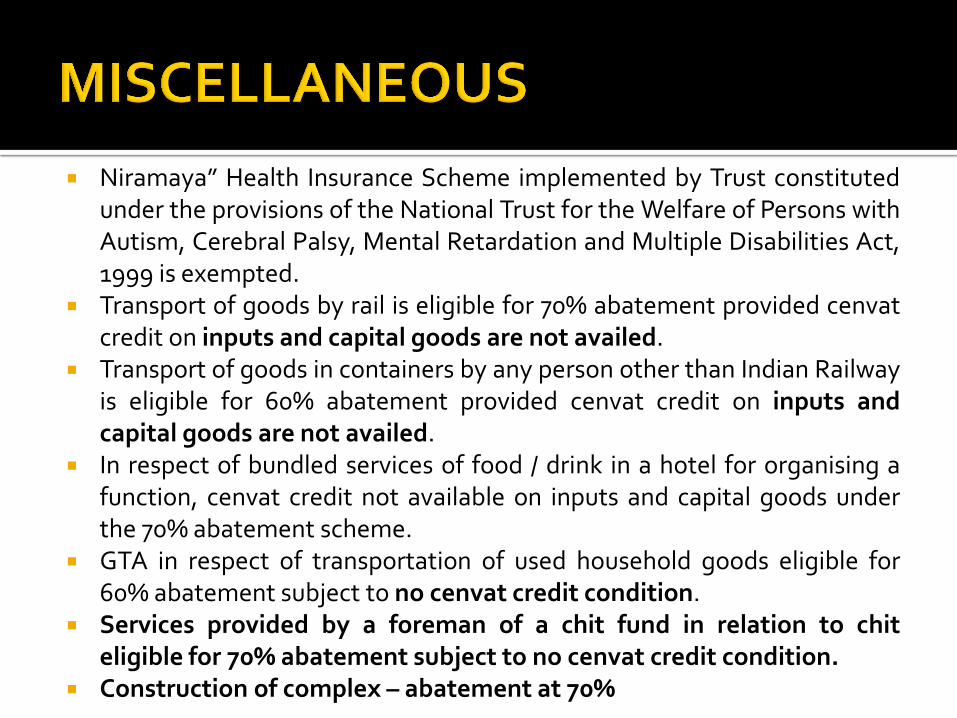

Niramaya” Health Insurance Scheme implemented by Trust constituted under the provisions of the National Trust for the Welfare of Persons with Autism, Cerebral Palsy, Mental Retardation and Multiple Disabilities Act, 1999 is exempted.

Transport of goods by rail is eligible for 70% abatement provided cenvat credit on inputs and capital goods are not availed.

Transport of goods in containers by any person other than Indian Railway is eligible for 60% abatement provided cenvat credit on inputs and capital goods are not availed.

In respect of bundled services of food / drink in a hotel for organising a function, cenvat credit not available on inputs and capital goods under the 70% abatement scheme.

GTA in respect of transportation of used household goods eligible for 60% abatement subject to no cenvat credit condition.

Services provided by a foreman of a chit fund in relation to chit eligible for 70% abatement subject to no cenvat credit condition.

Construction of complex – abatement at 70%

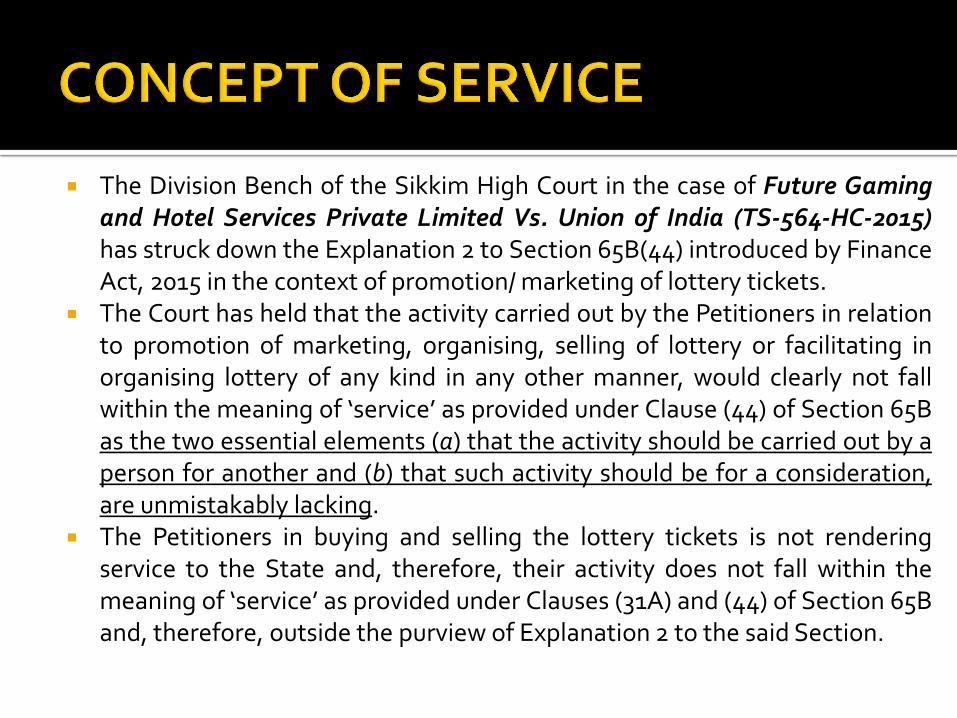

The Division Bench of the Sikkim High Court in the case of Future Gaming and Hotel Services Private Limited Vs. Union of India (TS-564-HC-2015) has struck down the Explanation 2 to Section 65B(44) introduced by Finance Act, 2015 in the context of promotion/ marketing of lottery tickets.

The Court has held that the activity carried out by the Petitioners in relation to promotion of marketing, organising, selling of lottery or facilitating in organising lottery of any kind in any other manner, would clearly not fall within the meaning of ‘service’ as provided under Clause (44) of Section 65B as the two essential elements (a) that the activity should be carried out by a person for another and (b) that such activity should be for a consideration, are unmistakably lacking.

The Petitioners in buying and selling the lottery tickets is not rendering service to the State and, therefore, their activity does not fall within the meaning of ‘service’ as provided under Clauses (31A) and (44) of Section 65B and, therefore, outside the purview of Explanation 2 to the said Section.

In Future Gaming Case (2015) and Future Gaming Case (2014) it has been held most unequivocally, inter alia, that the activity of the Petitioners comprising of promotion, organising, reselling or any other manner assisting in arranging the lottery tickets of a State Lottery does not establish the relationship of a principal and an agent but that of a buyer and a seller on principal to principal basis there being bulk purchase of lottery tickets by the Petitioners from the State Government on full payment on a discounted price as a natural business transaction and other related features and, of there being no privity of contract between the State Government and the Stockists, agents, sellers, etc., under the Petitioners.

In our view, in this case also the very same conclusion would be applicable as the nature of the relationship between the Petitioners and the State Government and the Petitioners and the Stockists, agents, resellers, etc., does not appear to have been altered. K.Vaitheeswaran - All Copyrights Reserved

The Court also held that since the selling and marketing agents purchase the tickets from the Petitioners/ Distributors as goods on payment of price, it cannot be considered as a service.

K.Vaitheeswaran - All Copyrights Reserved

Explanation 2 in section 65B(44) is proposed to be amended whereby Explanation 2(a) is substituted with by a lottery distributor or selling agent on behalf of the State Government in relation to promotion, marketing, organizing, selling of lottery or facilitating in organizing lottery of any kind in any other manner, in accordance with the provisions of the Lotteries (Regulation) Act, 1998.

Section 67A(2) inserted to provide that the time or the point in time with respect to the rate of service tax shall be such as may be prescribed.

Explanation-1 to Rule 5 of PoT Rules provides that the Rule shall apply mutatis mutandis in case of new levy on services.

Definition of capital goods now covers parts of wagon falling under sub-heading 8606 92.

Equipments or appliance used in an office in the factory is covered.

Usage outside the factory for pumping of water for captive use is permitted.

Effective from 01.04.2016.

Exempt service shall not include a service. which is exported in terms of Rule 6A by way of transportation of goods by a vessel from

customs station of clearance in India to a place outside India.

Effective from 01.03.2016.

Goods used for pumping of water are covered.

All capital goods which have value upto Rs.10,000/- per piece shall be treated as input.

The definition of inputs excludes capital good except when the value of capital goods is upto Rs.10,000/- per piece.

Effective from 01.03.2016

ISD amended to mean an office of a manufacturer of final products or service provider which receives invoices and issues invoice for the purpose of distributing credit to such manufacturer or service provider or outsourced manufacturing unit.

Effective 01.03.2016 Far reaching amendment. Section 4A Rule 10A

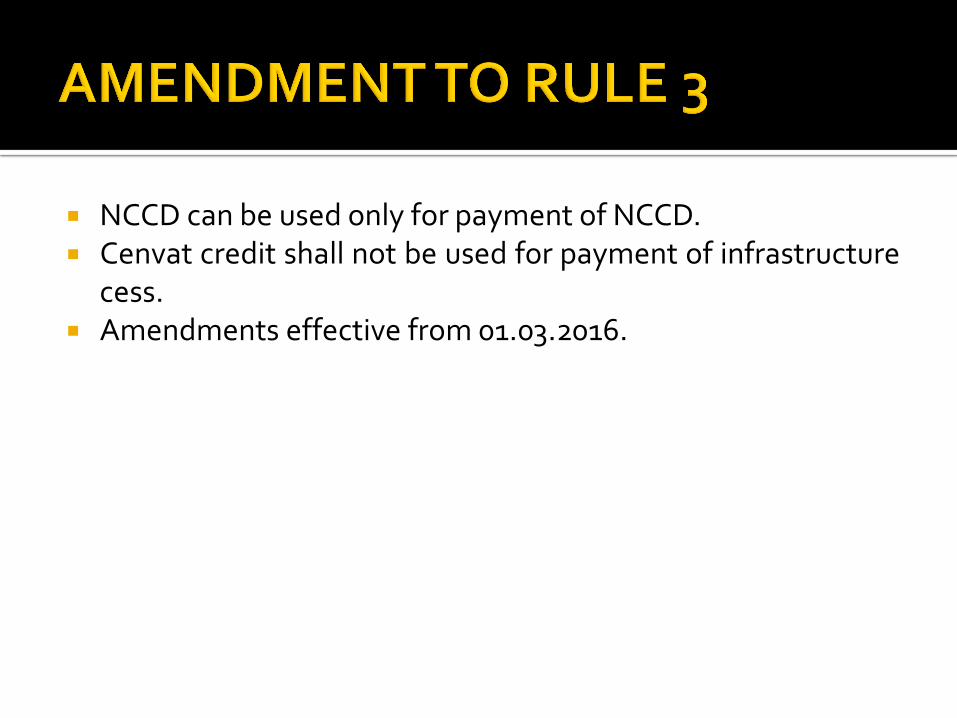

NCCD can be used only for payment of NCCD. Cenvat credit shall not be used for payment of infrastructure

cess. Amendments effective from 01.03.2016.

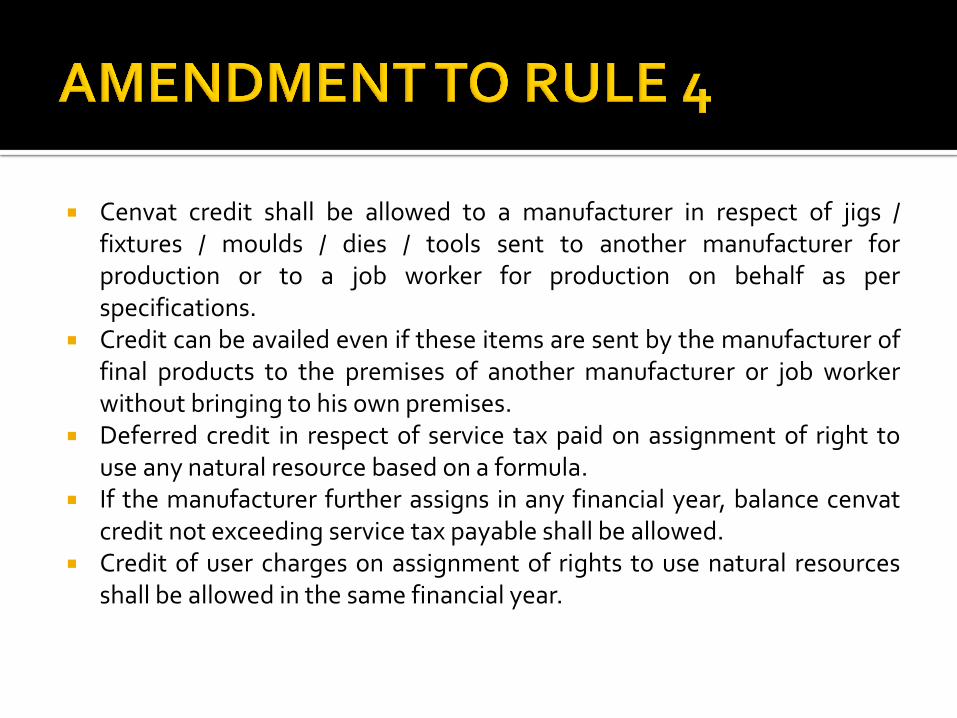

Cenvat credit shall be allowed to a manufacturer in respect of jigs / fixtures / moulds / dies / tools sent to another manufacturer for production or to a job worker for production on behalf as per specifications.

Credit can be availed even if these items are sent by the manufacturer of final products to the premises of another manufacturer or job worker without bringing to his own premises.

Deferred credit in respect of service tax paid on assignment of right to use any natural resource based on a formula.

If the manufacturer further assigns in any financial year, balance cenvat credit not exceeding service tax payable shall be allowed.

Credit of user charges on assignment of rights to use natural resources shall be allowed in the same financial year.

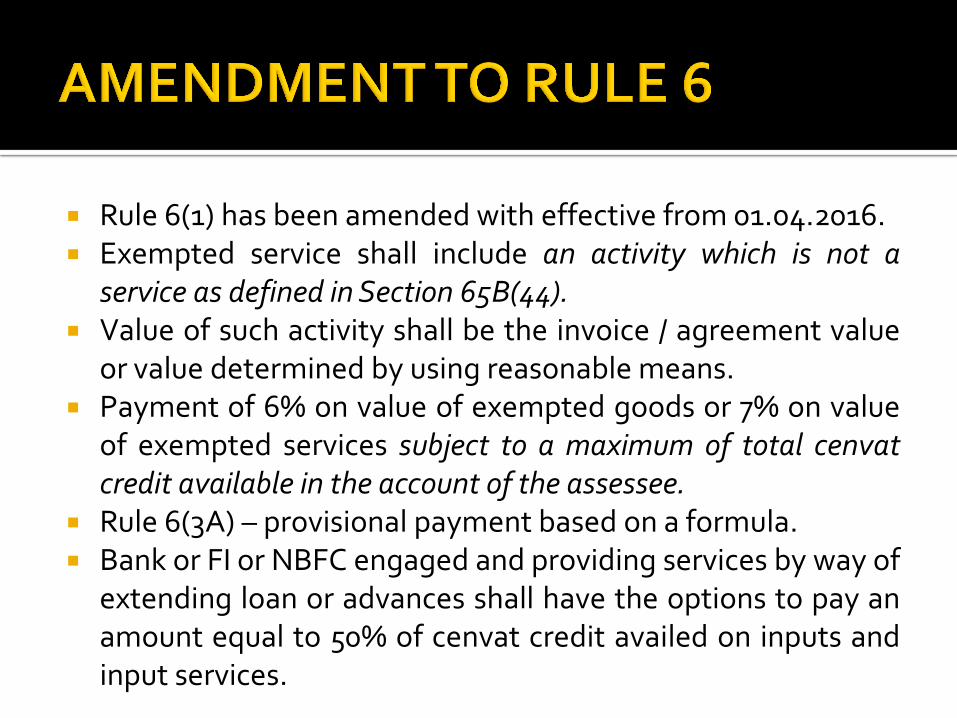

Rule 6(1) has been amended with effective from 01.04.2016. Exempted service shall include an activity which is not a

service as defined in Section 65B(44). Value of such activity shall be the invoice / agreement value

or value determined by using reasonable means. Payment of 6% on value of exempted goods or 7% on value

of exempted services subject to a maximum of total cenvat credit available in the account of the assessee.

Rule 6(3A) – provisional payment based on a formula. Bank or FI or NBFC engaged and providing services by way of

extending loan or advances shall have the options to pay an amount equal to 50% of cenvat credit availed on inputs and input services.

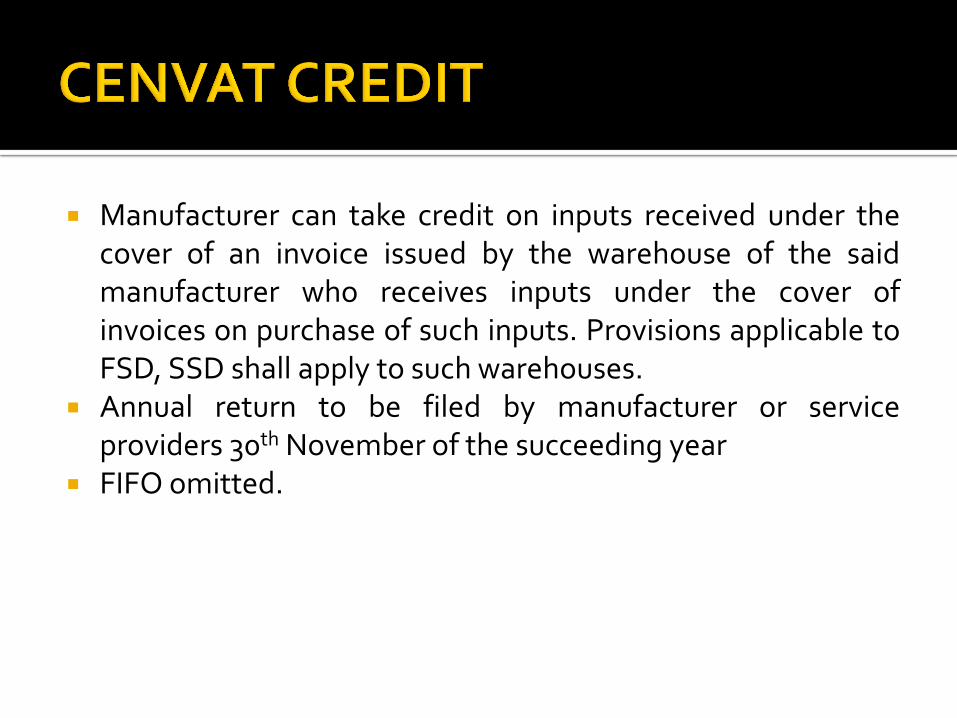

Manufacturer can take credit on inputs received under the cover of an invoice issued by the warehouse of the said manufacturer who receives inputs under the cover of invoices on purchase of such inputs. Provisions applicable to FSD, SSD shall apply to such warehouses.

Annual return to be filed by manufacturer or service providers 30th November of the succeeding year

FIFO omitted.

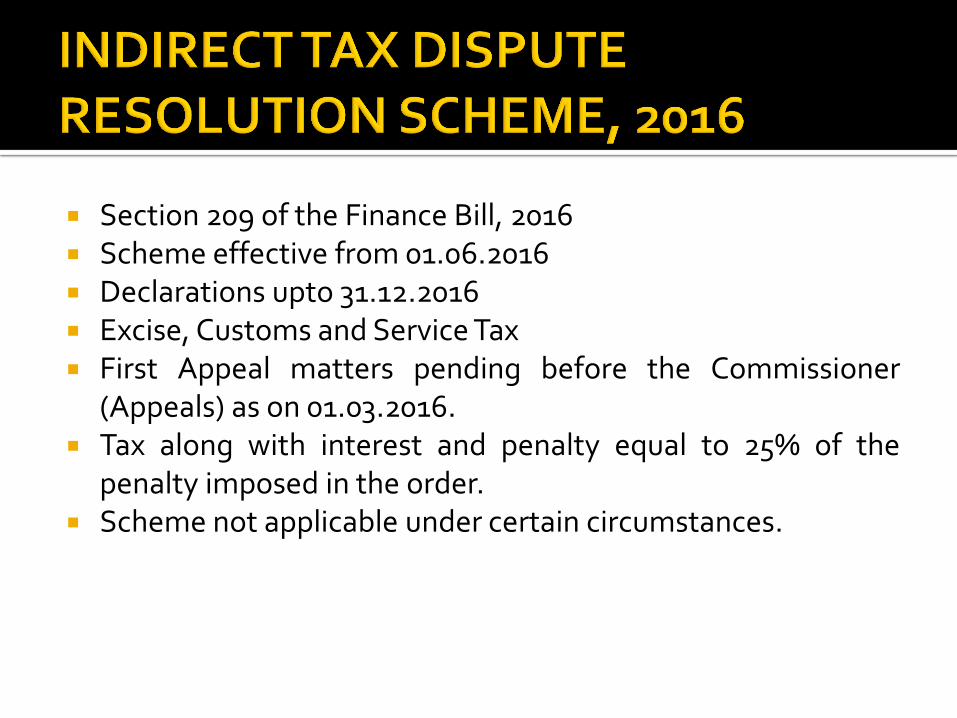

Section 209 of the Finance Bill, 2016 Scheme effective from 01.06.2016 Declarations upto 31.12.2016 Excise, Customs and Service Tax First Appeal matters pending before the Commissioner

(Appeals) as on 01.03.2016. Tax along with interest and penalty equal to 25% of the

penalty imposed in the order. Scheme not applicable under certain circumstances.

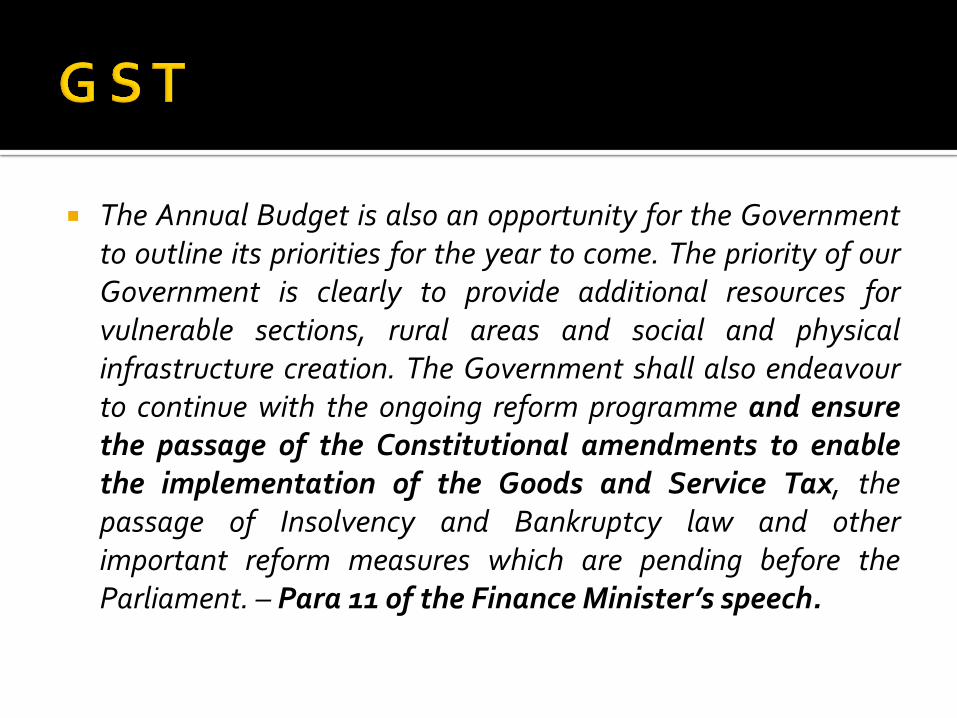

The Annual Budget is also an opportunity for the Government to outline its priorities for the year to come. The priority of our Government is clearly to provide additional resources for vulnerable sections, rural areas and social and physical infrastructure creation. The Government shall also endeavour to continue with the ongoing reform programme and ensure the passage of the Constitutional amendments to enable the implementation of the Goods and Service Tax, the passage of Insolvency and Bankruptcy law and other important reform measures which are pending before the Parliament. – Para 11 of the Finance Minister’s speech.

K.VAITHEESWARAN ADVOCATE & TAX CONSULTANT

Flat No.3, First Floor,

No.9, Thanikachalam Road,

T. Nagar,

Chennai - 600 017, India

Tel.: 044 + 2433 1029 / 4048

402, Front Wing,

House of Lords,

15/16, St. Marks Road,

Bangalore – 560 001, India

Tel : 080 22244854/ 41120804

Mobile: 98400-96876

E-mail : [email protected] [email protected]

www.vaithilegal.com