Embed Size (px)

Citation preview

Fire Assessment Fee

Understanding How It May Affect You

Kevin Cook Director of Communications / City of Lakeland

Public Outreach Schedule

January – February = Educate public on what a Fire Assessment Fee is and how you may effected March = Evaluate public feedback so City Commission can make policy decisions April – May = Inform public on Commission policy directives - report back with fee amounts and implementation decisions

• The Lakeland Fire Department provides comprehensive and quality fire, emergency medical and special operations emergency response services to the City of Lakeland and portions of unincorporated Polk County

• The Department also provides fire prevention education, inspection, plan review and code enforcement services

Lakeland Fire Department

• LFD operates seven Fire Stations • LFD’s response area is approximately 84-square miles • LFD’s services include heavy rescue, technical

rescue, fire prevention, fire code enforcement, fire investigation, aircraft rescue/firefighting and in-house fleet maintenance

Lakeland Fire Department

• LFD has 170 personnel with 67 serving as certified paramedics

• In 2013, LFD responded to 20,393 incidents

• In 2014, the Department responded to 21,600

• With the addition of Station 7, Lakeland residents now benefit from an ISO rating of 2

• Lower ISO rating=lower home owner’s insurance

Lakeland Fire Department

• Background of Fire Assessment Fees • Lakeland’s Fire Assessment Fee Study • Policy Decisions

Fire Assessment Fee Overview

• Lakeland Fire Department currently funded through the General Fund

• Public Safety budget is $56 Million and the City collects only $21.9 in property taxes

• City Commission is seeking more diverse revenues to support fire operations

• Polk County, Haines City & Bartow have implemented Fire Assessment Fees

• Over 30% of the 410 municipalities in Florida administer a Fire Assessment Fee

Background

Taxable Residential Property Values 28,500 Parcels

56%$of$all$residen/al$proper/es$pay$less$than$$200$in$City$taxes$

• Assessment Methodology – Determine Assessable Budget • Fire Suppression & Basic

Medical Response

– Benefits to Property • Resource Based • Land Use Based

– Equity for Property Owners

Background

• Assessable Budget • Demand by Land Use • Budget Allocations by Land Use • Calculated Assessment

Technical Study

• Measure Eligible Portion of Budget that can be funded with Fire Assessment Fee

• Per case law, a Fire Assessment Fee must exclude expenses associated with certain Fire Department medical runs

• LFD FY2015 Budget = $18.5 Million (includes $1.5 Million capital)

• Assessable LFD Budget = $17.1 Million

Assessable Budget

• Basic Life Support (BLS) is an emergency transport provided by certified Emergency Medical Technicians (EMTs).

• Advanced Life Support (ALS) is provided when a patient is in more critical condition and a Paramedic is required to assist in the treatment of the patient before and/or during transport to the emergency facility.

ALS vs BLS

✚ BLS services included in FAF calculation - ALS services are not

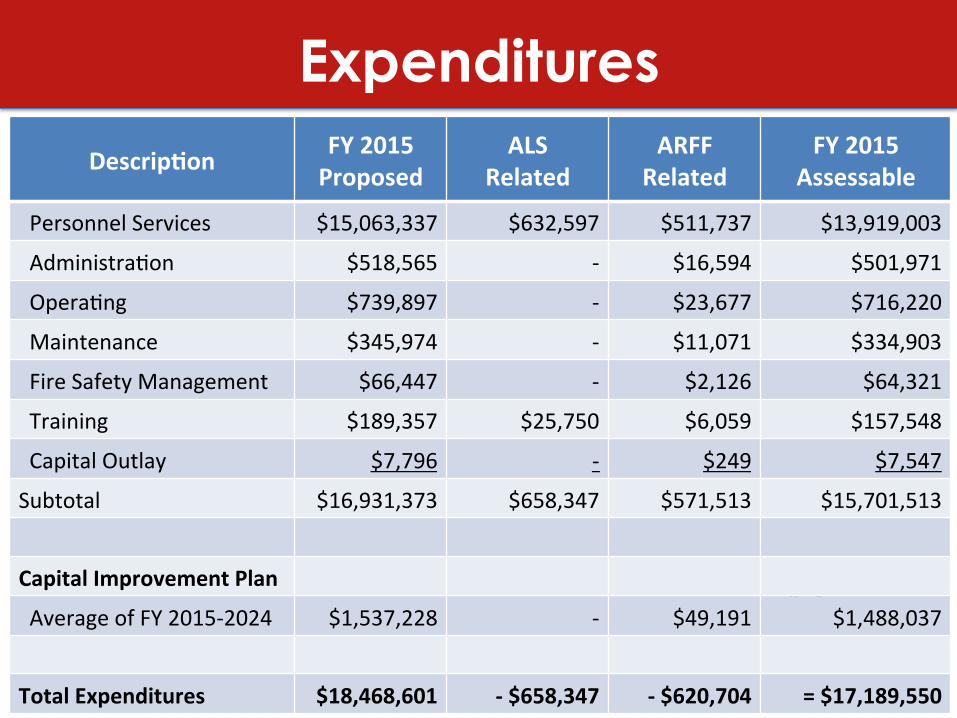

Assessable Budget = $17.1 Million • Review of Expenses • Net Dedicated Revenues & Expenses

Assessable Budget

$18.5M' ($1.4M' =$17.1M'

Expenditures Descrip/on$ FY$2015$

Proposed$ALS$$

Related$ARFF$

Related$FY$2015$$

Assessable$

''Personnel'Services' $15,063,337' $632,597' $511,737' $13,919,003'

''AdministraBon' $518,565' (' $16,594' $501,971'

''OperaBng' $739,897' (' $23,677' $716,220'

''Maintenance' $345,974' (' $11,071' $334,903'

''Fire'Safety'Management' $66,447' (' $2,126' $64,321'

''Training' $189,357' $25,750' $6,059' $157,548'

''Capital'Outlay' $7,796' (' $249' $7,547'

Subtotal' $16,931,373' $658,347' $571,513' $15,701,513'

Capital$Improvement$Plan$

''Average'of'FY'2015(2024' $1,537,228' (' $49,191' $1,488,037'

Total$Expenditures$ $18,468,601$ M$$658,347$ M$$620,704$ =$$17,189,550$

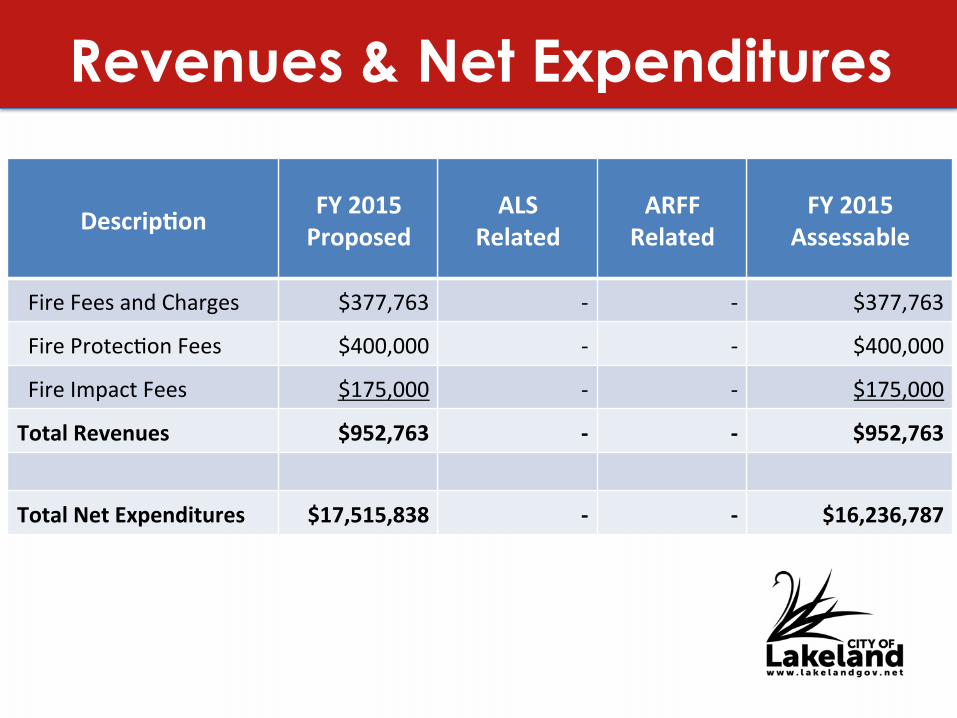

Revenues & Net Expenditures

Descrip/on$ FY$2015$Proposed$

ALS$$Related$

ARFF$Related$

FY$2015$Assessable$

''Fire'Fees'and'Charges' $377,763' (' (' $377,763'

''Fire'ProtecBon'Fees' $400,000' (' (' $400,000'

''Fire'Impact'Fees' $175,000' (' (' $175,000'

Total$Revenues$ $952,763$ M$ M$ $952,763$

Total$Net$Expenditures$ $17,515,838$ M$ M$ $16,236,787$

Assessment Funding Requirement

Descrip/on$ FY$2015$Proposed$

ALS$$Related$

ARFF$Related$

FY$2015$Assessable$

Miscellaneous$Assessment$Expenditures$

''Study'Reimbursement' (' (' (' $17,000'

''Statutory'Discount' (' (' (' $568,883'

''Assessment'CollecBon'''''' (' (' (' $325,076'

Total$Misc.$Expenditures$ M$ M$ M$ $910,959$

Total$Fire$Assessment$Funding$Requirements$ $17,147,746$

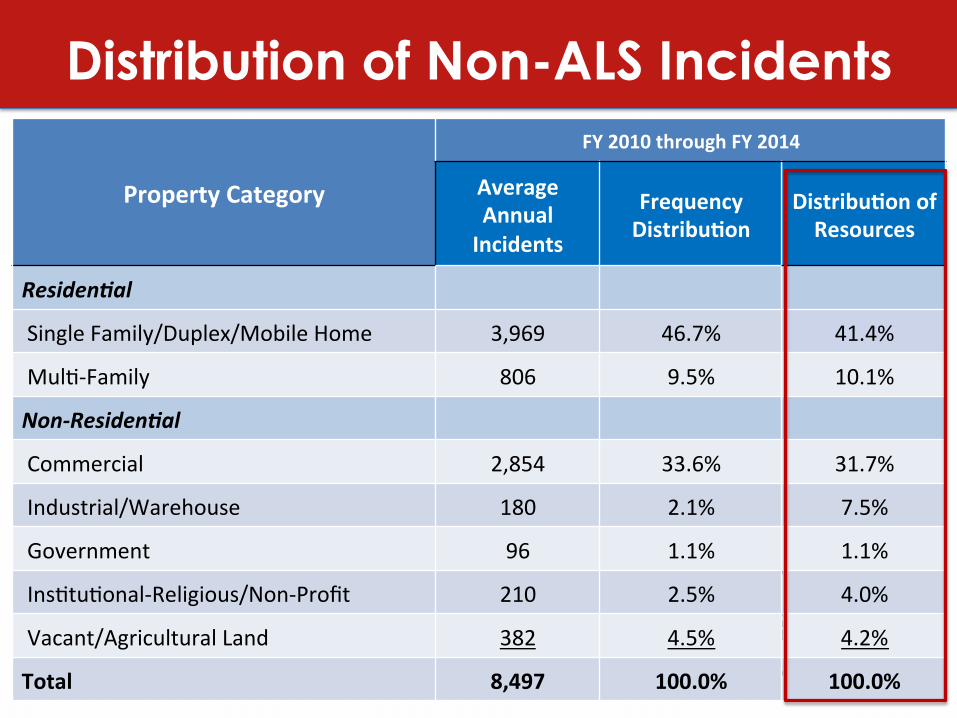

• Calls for Service Averaged (2010-2014) to define demand by land use

• Multiple Variables • Exclusion of ALS Related Incidents • Based on LFD Reports

Demand By Land Use

• Staff Time – Number of incidents X average

duration X staff

• Vehicle Time – Number of incidents X average

duration X units

• Total Resources – Staff time plus vehicle time

Demand By Land Use

Distribution of Non-ALS Incidents

Property$Category$

FY$2010$through$FY$2014$

Average$Annual$Incidents$

Frequency$Distribu/on$

Distribu/on$of$Resources$

Residen'al*

'Single'Family/Duplex/Mobile'Home' 3,969' 46.7%' 41.4%'

'MulB(Family' 806' 9.5%' 10.1%'

Non-Residen'al*

'Commercial' 2,854' 33.6%' 31.7%'

'Industrial/Warehouse' 180' 2.1%' 7.5%'

'Government' 96' 1.1%' 1.1%'

'InsBtuBonal(Religious/Non(Profit' 210' 2.5%' 4.0%'

'Vacant/Agricultural'Land' 382' 4.5%' 4.2%'

Total$ 8,497$ 100.0%$ 100.0%$

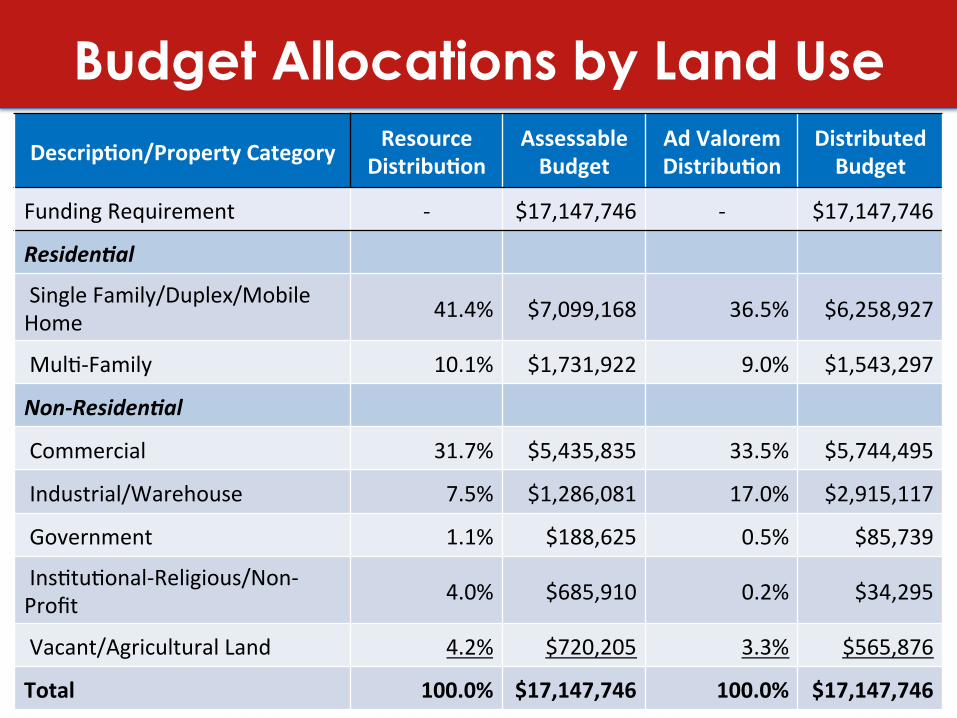

Budget Allocations by Land Use

Descrip/on/Property$Category$ Resource$Distribu/on$ Assessable$Budget$

Funding'Requirement' (' $17,147,746'

Residen'al*

'Single'Family/Duplex/Mobile'''Home' 41.4%' $7,099,168'

'MulB(Family' 10.1%' $1,731,922'

Non-Residen'al*

'Commercial' 31.7%' $5,435,835'

'Industrial/Warehouse' 7.5%' $1,286,081'

'Government' 1.1%' $188,625'

'InsBtuBonal(Religious/Non(Profit' 4.0%' $685,910'

'Vacant/Agricultural'Land' 4.2%' $720,205'

Total$ 100.0%$ $17,147,746$

Budget Allocations by Land Use

Descrip/on/Property$Category$ Resource$Distribu/on$

Assessable$Budget$

Ad$Valorem$Distribu/on$

Distributed$Budget$

Funding'Requirement' (' $17,147,746' (' $17,147,746'

Residen'al*

'Single'Family/Duplex/Mobile'''Home' 41.4%' $7,099,168' 36.5%' $6,258,927'

'MulB(Family' 10.1%' $1,731,922' 9.0%' $1,543,297'

Non-Residen'al*

'Commercial' 31.7%' $5,435,835' 33.5%' $5,744,495'

'Industrial/Warehouse' 7.5%' $1,286,081' 17.0%' $2,915,117'

'Government' 1.1%' $188,625' 0.5%' $85,739'

'InsBtuBonal(Religious/Non(Profit' 4.0%' $685,910' 0.2%' $34,295'

'Vacant/Agricultural'Land' 4.2%' $720,205' 3.3%' $565,876'

Total$ 100.0%$ $17,147,746$ 100.0%$ $17,147,746$

Calculated Rates

Property$Category$ Dwelling$Unit$

Fire$Assessment$Alloca/on$

Number$of$Units$

Rate$per$Unit$

Residen'al*

'Single'Family/Duplex/Mobile'Home' unit/site' $7,099,168' 34,512' $205.70'

'MulB(Family' unit/site' $1,731,922' 11,664' $148.48'

Non-Residen'al*

'Commercial' Sq']' $5,435,835' 20,050,214' $0.2711'

'Industrial/Warehouse' Sq']' $1,286,081' 19,821,309' $0.0649'

'Vacant/Agricultural'Land' Parcel' $720,205' 5,575' $129.18'

'InsBtuBonal(Religious/Non(Profit' Sq']' $685,910' 4,503,636' $0.1523'

'Government' Sq']' $188,625' 2,829,680' $0.0667'

Residential Tiering Example

Property$Size$ Dwelling$Unit$ Calculated$Rates$ Count$

Single*Family*/*Duplex*/*Mobile*Home*

''0(1,400'sf' Du'/'site' $181' 11,946'

''1,401'to'2,100'sf' Du'/'site' $225' 9,392'

''Greater'than'2,100'sf' Du'/'site' $264' 4,581'

Fee Comparison

Property$Category$ Dwelling$Unit$

City$of$Lakeland$Calcula/on$

Polk$County$ FL$Jurisdic/ons$

Calc.$ Adopted$ Adopted$

%'of'Calculated'Rate' (' 100%' 100%' 94%' 40%'to'100%'

Residen'al*

'SFR/Duplex/Mobile'Home' Du/site' $205.70' $180.00' $168.00' $25'to'$305'

'MulB(Family' Du/site' $148.48' $132.00' $124.00' $25'to'$305'

Non-Residen'al*

'Commercial' Sq']' $0.27' $0.22' $0.21' $0.19'to'$0.59''

'Industrial/Warehouse' Sq']' $0.06' $0.11' $0.10' $0.01'to'$0.11'

'Vacant/Agricultural'Land' Parcel' $129.18' $0' $0' $0'to'$78'

'Inst.(Religious/Non(Profit' Sq']' $0.15' $0.53' $0.49' $0'to'$1.04'

'Government' Sq']' $0.06' $0' $0' $0'

• Do we implement a Fire Assessment Fee? • At what implementation level? • Are there exemptions and caps? • Do we implement residential tiering? • What do we do about vacant land? • What is the millage impact?

Policy Decisions

• Implementation Level – Surveyed jurisdictions range from 40% - 100% of

assessable budget (before exemptions and caps)

Policy Decisions

• Federal Government is exempt • Some state owned property such as schools

are exempt • Do we exempt institutional, religious and

non-profits?

Exemptions

• Residential Tiering - based on size of home and service demand

• Similar to non-residential fee structure (sf. based)

• Need to consider as part of implementation plan

Residential Tiering

• LFD can handle fires up to 1 million sf. with current resources

• Polk County has a cap of 1 million sf. • If capped at 1 million, there is a revenue

impact of $160,000 to the General Fund

Non-Residential Cap

• If assessed, there is a benefit to surrounding structures

• Fire services do add value to vacant land owner

• City Commission must decide if they will reduce Fire Assessment Fee for vacant land

• A reduced Fire Assessment Fee for vacant land must be subsidized by other property owners or through other sources

Vacant Land

• If implemented, Fire Assessment Fee amount would be included on annual property tax bill distributed by the Polk County Tax Collector

Billing Approach

• Policy decisions must be made regarding the final level of a Fire Assessment Fee

• Property taxes could decrease depending on the level of implementation decided by the City Commission coupled with any land use exemptions

Ad Valorem Impact

• Jan 15 – Kiwanis • Jan 20 – Coleman Bush – NW Neighborhoods • Jan 22 – Family Fundamentals – NE

Neighborhoods • Jan 23 – Lakeland Business Leaders • Jan 27 – LMNA - SE Neighborhoods • Feb 17 – Interdenominational Ministers’ Alliance • Feb 17 – Dixieland NA - SW Neighborhoods

Upcoming Public Outreach

![Fire Prevention Fee Schedule - Phoenix, Arizona Prevention Fee Sch… · Development Fire Prevention section will be indicated with [P]. Perm its that are issued by Fire Prevention](https://img.pdfslide.net/doc/110x75/60134634a33dce13b219e2e4/fire-prevention-fee-schedule-phoenix-arizona-prevention-fee-sch-development.jpg)