Embed Size (px)

Citation preview

CIL “Non-negotiable” Tax

CIL is a locally set tax “levy” on land introduced under the Growth and Infrastructure Act 2008. The operation of the levy, including calculation of the levy payable, is prescribed by the Community Infrastructure Levy Regulations 2010 (as amended). The most recent regulatory changes were introduced in Amendment Regulations published in February 2014.

CIL does not replace S106 obligations: under CIL Regulation 122(2) these may still be payable in addition to CIL where the planning obligation is:

a) necessary to make the development acceptable in planning terms;

b) directly related to the development; and

c) fairly and reasonable related in scale and kind to the development

CIL is only paid on net increases in floor space provided that any building(s) on site remain “in-use” in accordance with Regulation 40; i.e. lawfully occupied for a continuous period of 6 months in the 36 months ending on the date planning permission is granted.

CIL- All Stages Map of England & Wales

Savills - http://www.savills.co.uk/promotions/cil-map.aspx

Source: Savills (as at 2nd March 2015)

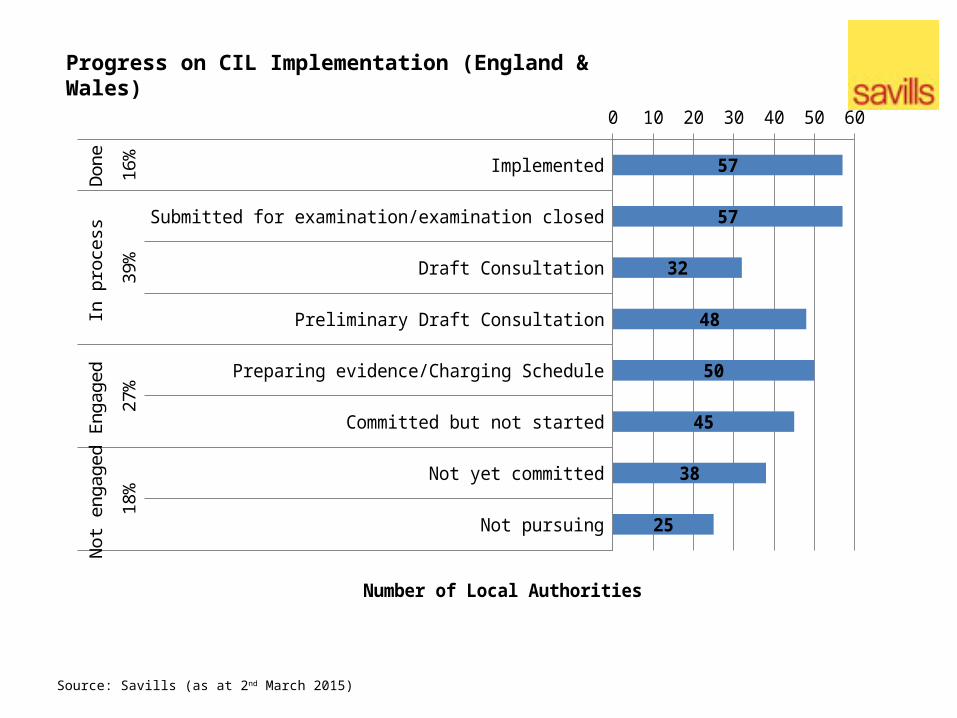

Progress on CIL Implementation (England & Wales)

Implemented

Submitted for examination/examination closed

Draft Consultation

Preliminary Draft Consultation

Preparing evidence/Charging Schedule

Committed but not started

Not yet committed

Not pursuing

16

%3

9%

27

%1

8%

Do

ne

In p

roce

ssE

ng

ag

ed

No

t en

ga

ge

d0 10 20 30 40 50 60

57

57

32

48

50

45

38

25

Number of Local Authorities

Projections on number of implemented CILs

April 2015 Deadline

Source: Savills (February 2015)

London- CIL Progress Map

Mayoral CIL- Facts & Figures

£70.2m collected since

April 2012

£300m target by

2019

Six London Boroughs made up

52% of CIL receipts

Source of funding for Crossrail, approximately 2%

of total costExceeded projections –

two years ahead of projections

Outperformed Section 106

contributions which have raised

less funds than forecast

There are trade-offs between the viability of CIL, Section 106 and affordable housing policy

Source: Savills

150 175 200 225 250 275 300 325 3500

10,000

20,000

30,000

40,000

50,000

0%

10%

20%

30%

40%

50%

New homes sales value (£ per sq.ft.)

Via

ble

leve

l of C

IL a

nd

Se

ctio

n 1

06

(£

pe

r p

lot)

Afford-able

housing policy

Local Context Needs to be Considered

• Historic delivery• Historic Section106 achievement• Local Plan policy costs• Benchmark land value• Land supply characteristics and profile

Viability Buffer

Local Market Evidence is Needed

Source: Savills

“competitive return”

Policy choices have a cumulative impact on viability

Source: Savills

Local policies must be assessed to establish an

appropriate Benchmark Land Value

Avoiding ‘Double Dipping’• Explicit policy on the balance between Section 106 and CIL

– Draft regulation 123 list – what will be excluded from Section 106 funding?

– Does the Regulation 123 list support the delivery of the Plan?

– The proposed changes to the regulations will tighten the restriction on pooling of Section 106

– Flexible to give Charging Authorities scope to change what CIL is spent on

• Must be allowed for within the viability appraisals

savills.com

Risk to Delivery?

Grampian Conditions – who will deliver?

Who will pay? When will infrastructure be delivered?

What are the implications?• LPAs need to consider the impact of the April

2015 restrictions on the delivery of infrastructure in their area

• Developers and housebuilders should work with LPAs to identify key pieces of infrastructure that are needed for the delivery of housing sites

• Section 106 agreements should refer to specific named projects

• Further guidance from Ministers is essential to ensure that LPAs have a sufficient Section 106 mechanism in place post-April 2015, as failure to do so will have a significant impact on the delivery of both infrastructure and housing.

CIL Checklist (Ten Key Points)

Source: Savills

CIL is a non-negotiable tax. This is very different to the provision of Section 106 obligations,which are a policy requirement and potentially subject to negotiation, particularly in respectof viability. It is therefore essential that the following is considered on all development siteswhere a Charging Schedule has been, or is about to be, implemented.

• Failure to pay is a criminal offence: Once a Liability Notice is served it is the responsibility of the landowner or appointed party to pay CIL.

• Off-setting is subject to the “lawful occupation” test: To be off-set, a part of each existing building must have been in continuous lawful occupation for a minimum of 6 months out of the 36 months preceding the grant of planning permission. The relevant buildings must therefore still be standing on the day that planning permission is granted.

• CIL is liable for chargeable development triggered by Planning Consent: The trigger for CIL is the grant of a planning permission. This means that schemes submitted for planning, prior to CIL implementation, may still be liable for CIL, dependent on the timing of the decision. This should be factored in scheme appraisals and valuations.

CIL Checklist

Source: Savills

• Failure to pay is a criminal offence: Once a Liability Notice is served it is the responsibility of the landowner or appointed party to pay CIL.

• CIL is index-linked: All CIL rates are index-linked from the date that the Charging Schedule is implemented. It is therefore important that the correct index figures are used when calculating CIL liability in accordance with Regulation 40. The Index date is 1st November. The CIL calculation is triggered on the date of planning permission.

• CIL is payable on commencement of development: The timing and amount of these CIL payments may be subject to the Charging Authority’s Instalments Policy. Where there is no instalments policy, CIL is payable in full 60 days after the commencement of development. For phased outline applications, each phase of a development may be charged separately.

• Exemptions and reliefs must be applied for and approved prior to commencement: A number of exceptions or reliefs are available which may reduce the CIL liability (for example social housing, self build housing, or charitable relief). Some are compulsory; others are offered at the Charging Authority’s discretion and you should check the Charging Schedule.

CIL Checklist

Source: Savills

• CIL does not replace Section 106: Affordable housing and site specific mitigation obligations remain matters that can be secured with planning obligations under Section 106. CIL Regulations 122 and 123 impose a restriction to limit the pooling of contributions in planning obligations in Section 106 when CIL is implemented, or from the 6th April 2015, whichever is the earlier. This should be considered when negotiating and agreeing Section 106 agreements with Local Authorities.

• Notice procedures must be followed: It is essential that the collection process is followed and relevant forms and notices are issued, both by the developer/owner and the Charging Authority. For developers and owners, it is essential that the Notice of Commencement of Development is served at least one day before development commences on site. Failure to do so will result in the loss of all reliefs, removal of the ability to pay by instalments and penalties and interest becoming liable. In addition there are penalties and surcharges for failing to comply with the notice procedures set out in the Regulations.

• CIL is non-negotiable: Section 106 requirements remain subject to negotiation whereas CIL is fixed. CIL Regulation 40 sets out the method for calculating CIL liability. At this stage it is important to consider whether off-setting of existing floorspace or mandatory reliefs are applicable (see Regulations 41 – 58).

Key Points to Remember• Office to residential permitted

development is CIL liable• Notice of Chargeable Development

should be served before a CIL charging schedule comes into force

• No statutory definition of “Gross Internal Area”

• Existing floorspace does not include parts of the building not part of the planning application site

• “Vacancy Test” – buildings in “lawful use for a continuous period of 6 in 36 months prior to “date which planning permission first permits development”