Embed Size (px)

Citation preview

Governance Best Practices

welchllp.com

www.welchllp.com

• Audit Committee - Committee of the Board of Directors that ensures audit quality

• Publication in January 2014 entitled “Oversight of the External Auditor – Guidance for Audit Committees”

o Chartered Professional Accountants Canada

o Canadian Public Accountability Board (CPAB)

o Institute of Corporate Directors

• Summarizes responsibilities of audit committees with best practices

Audit Committee Best Practices

www.welchllp.com

• Some of their responsibilities:

o Oversee the work of the external auditor

o Recommend to the Board the nomination of auditor

With the primary objective to ensure audit quality

Responsibilities

www.welchllp.com

At least 3 members, all must be:

• Independent

• Financially literate

• Director of entity

Composition of Committee

www.welchllp.com

Likely to be achieved by an audit team that:

• Exhibits appropriate values, ethics and attitudes

• Has the requisite knowledge, skills, experience and sufficient time allocated to perform the audit work

• Applies a rigorous audit process and quality control procedures that complies with law, regulation and applicable standards

• Provides useful and timely reports

• Interacts appropriately with relevant stakeholders

Audit Quality

www.welchllp.com

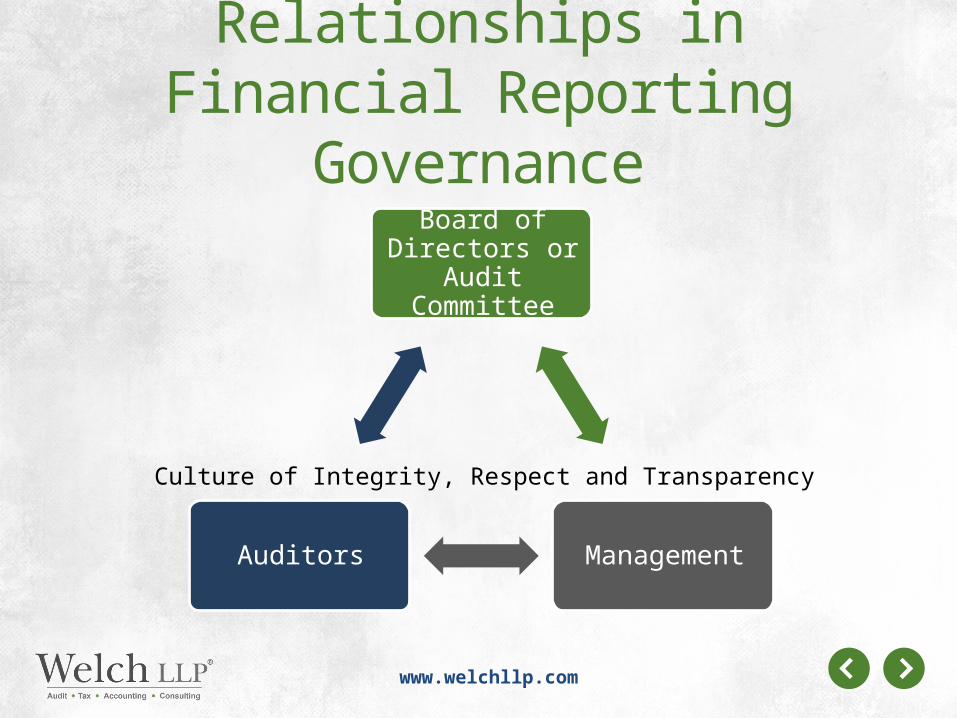

Relationships in Financial Reporting Governance

Board of Directors or Audit

Committee

ManagementAuditors

Culture of Integrity, Respect and Transparency

www.welchllp.com

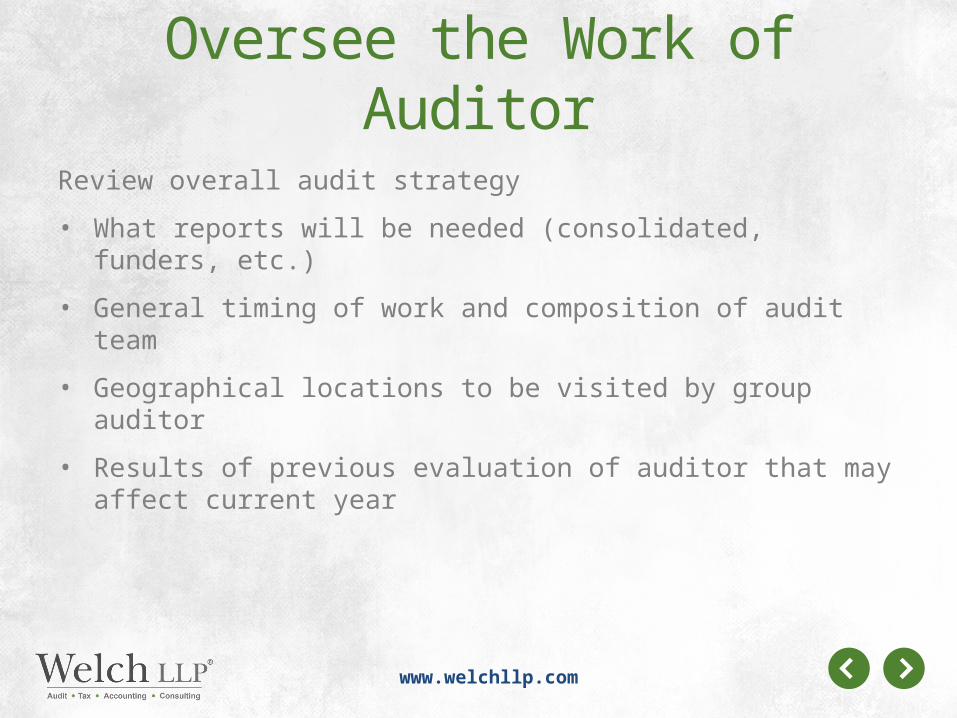

Review overall audit strategy

• What reports will be needed (consolidated, funders, etc.)

• General timing of work and composition of audit team

• Geographical locations to be visited by group auditor

• Results of previous evaluation of auditor that may affect current year

Oversee the Work of Auditor

www.welchllp.com

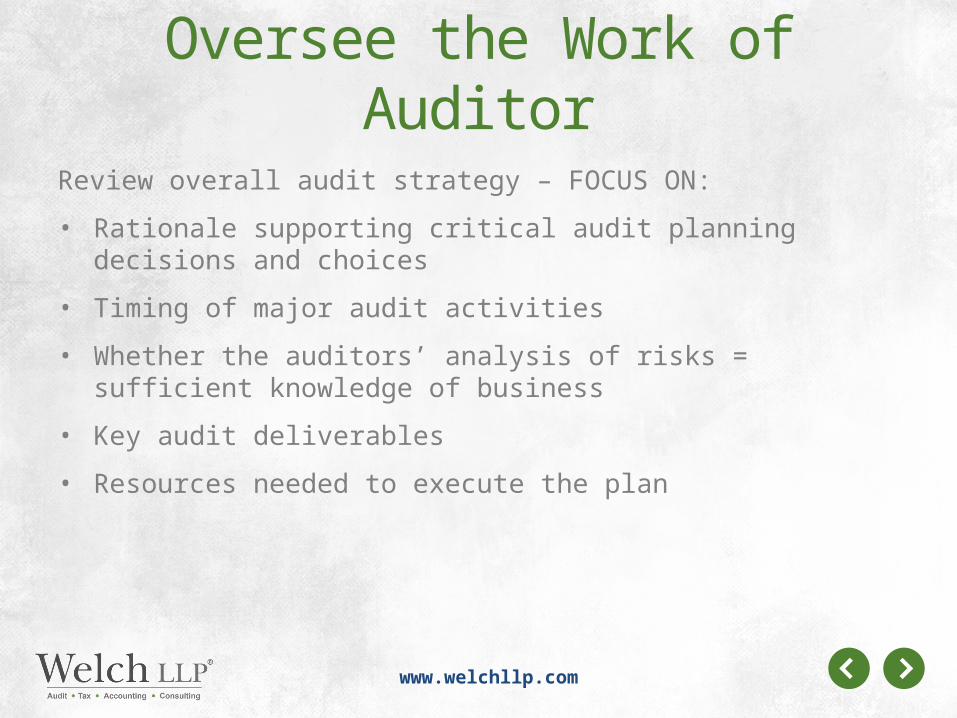

Review overall audit strategy – FOCUS ON:

• Rationale supporting critical audit planning decisions and choices

• Timing of major audit activities

• Whether the auditors’ analysis of risks = sufficient knowledge of business

• Key audit deliverables

• Resources needed to execute the plan

Oversee the Work of Auditor

www.welchllp.com

Auditor should report any difficulties in executing audit plan:

• Areas where audit was behind schedule and reasons

• Unexpected and extensive auditor effort to obtain evidence

• Changes in business conditions or circumstances

• Identification of unexpected audit results

Separately meet in camera with auditors and management

Oversee the Work of Auditor

www.welchllp.com

Evaluating Auditor’s Findings

• Primary focus of review of auditor’s communication

o Enough information to recommend approval of financial statements to board

o Auditors have exercised professional skepticism and performed a quality audit

Oversee the Work of Auditor

www.welchllp.com

Prompt communication and in-depth discussion with both management and auditors are required if findings could:

• Require auditors to modify their opinion

• Add an emphasis of matter paragraph to report

• Lead external auditors to question organization’s ability to continue to operate as a going concern

Oversee the Work of Auditor

www.welchllp.com

• Informed decision by doing annual assessment

o Audit quality considerations

Auditor independence, objectivity & professional skepticism

Quality of engagement team provided by auditor

Communication & interaction with auditor

o Quality of service considerations

• Review with auditors to continually improve effectiveness & performance

• Consider if there are actions that can improve committee’s own processes

Recommend Auditors to Board

www.welchllp.com

Periodic comprehensive review of auditor

o Fear of complacency & independence concerns

o Recommended every 5 years

o Outcome:

retain the firm or

put the audit out for tender

o Identify areas for improvement for both the auditors and committee

Recommend Auditors to Board

www.welchllp.com

Comprehensive review includes reviewing and evaluating:

• Significant trends and results identified in previous annual assessments

• Safeguards against independence & familiarity threats

• How the audit firm has responded to past evaluations

Recommend Auditors to Board

www.welchllp.com

Common reasons for audits going to tender:

• Lower fees

o Ensure RFP outlines all of the required services – avoids misunderstandings and surprise bills

o Evaluate firm’s performance on regular basis

• Complacency and independence

o Enquire about firm’s quality control procedures to address this risk

o Consider requesting a rotation of certain audit team members if this is a concern

Recommend Auditors to Board

www.welchllp.com

Contact Us!

Christa Casey, CPA, CAPartner & Director of the Not-for-Profit [email protected]