Embed Size (px)

Citation preview

Governmental Accounting

from Easy Street to Life in the Fast

Lane

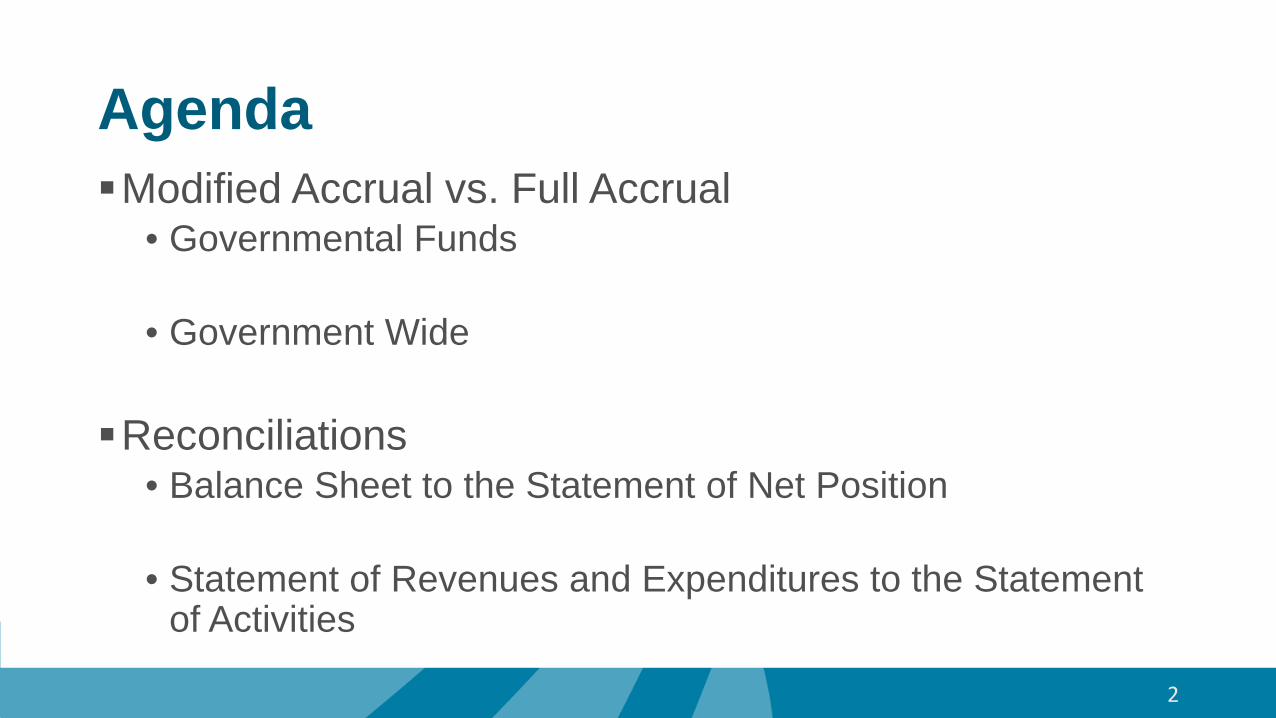

AgendaModified Accrual vs. Full Accrual

• Governmental Funds

• Government Wide

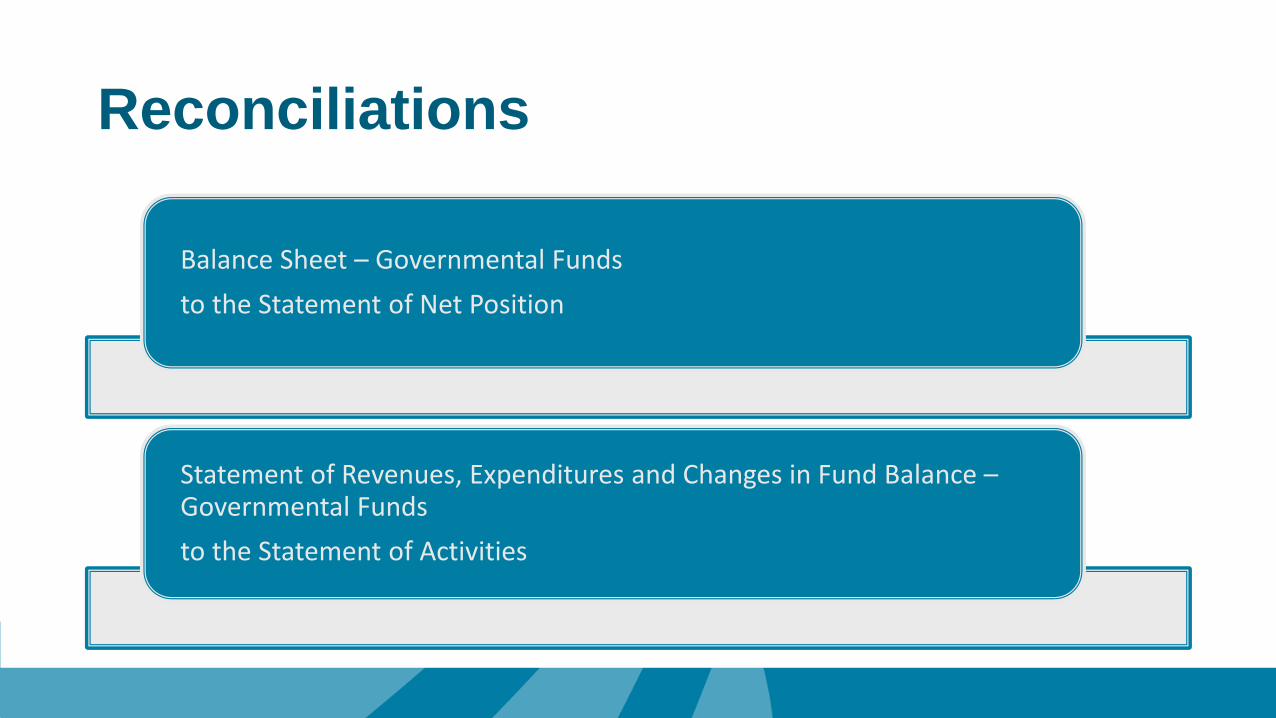

Reconciliations• Balance Sheet to the Statement of Net Position

• Statement of Revenues and Expenditures to the Statement of Activities

2

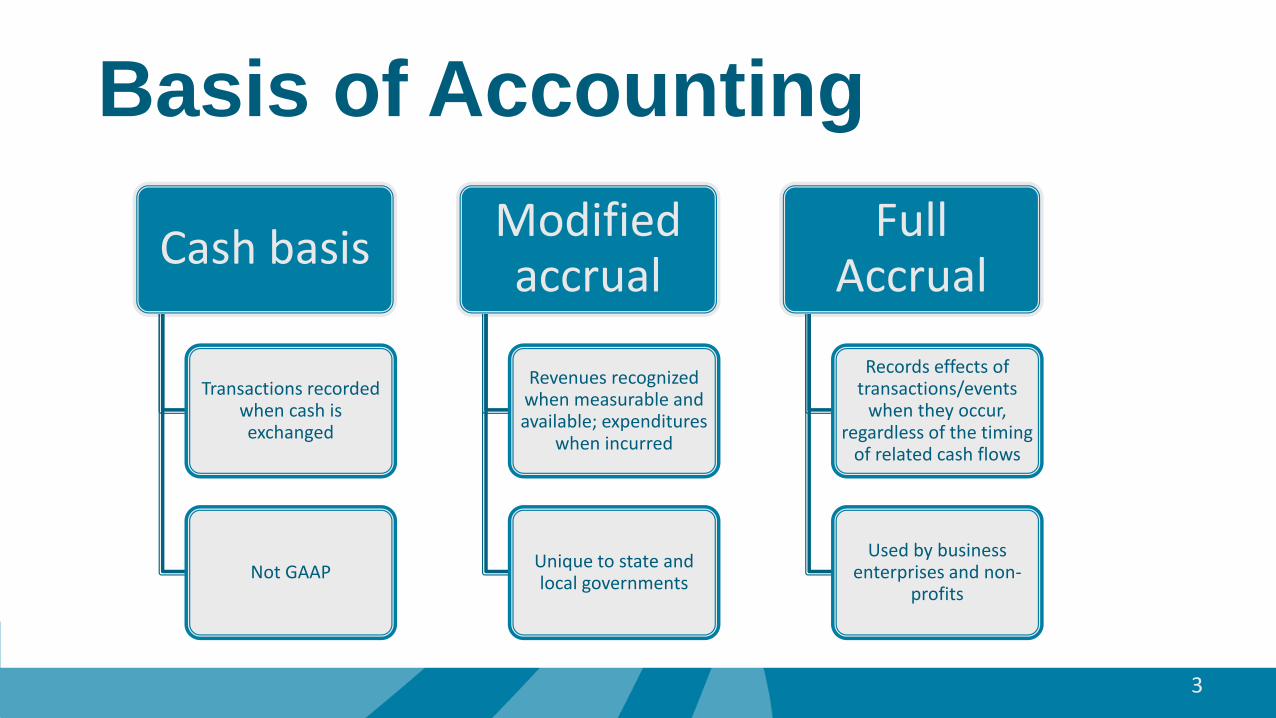

Basis of Accounting

3

Cash basis

Transactions recorded when cash is exchanged

Not GAAP

Modified accrual

Revenues recognized when measurable and available; expenditures

when incurred

Unique to state and local governments

Full Accrual

Records effects of transactions/events

when they occur, regardless of the timing

of related cash flows

Used by business enterprises and non-

profits

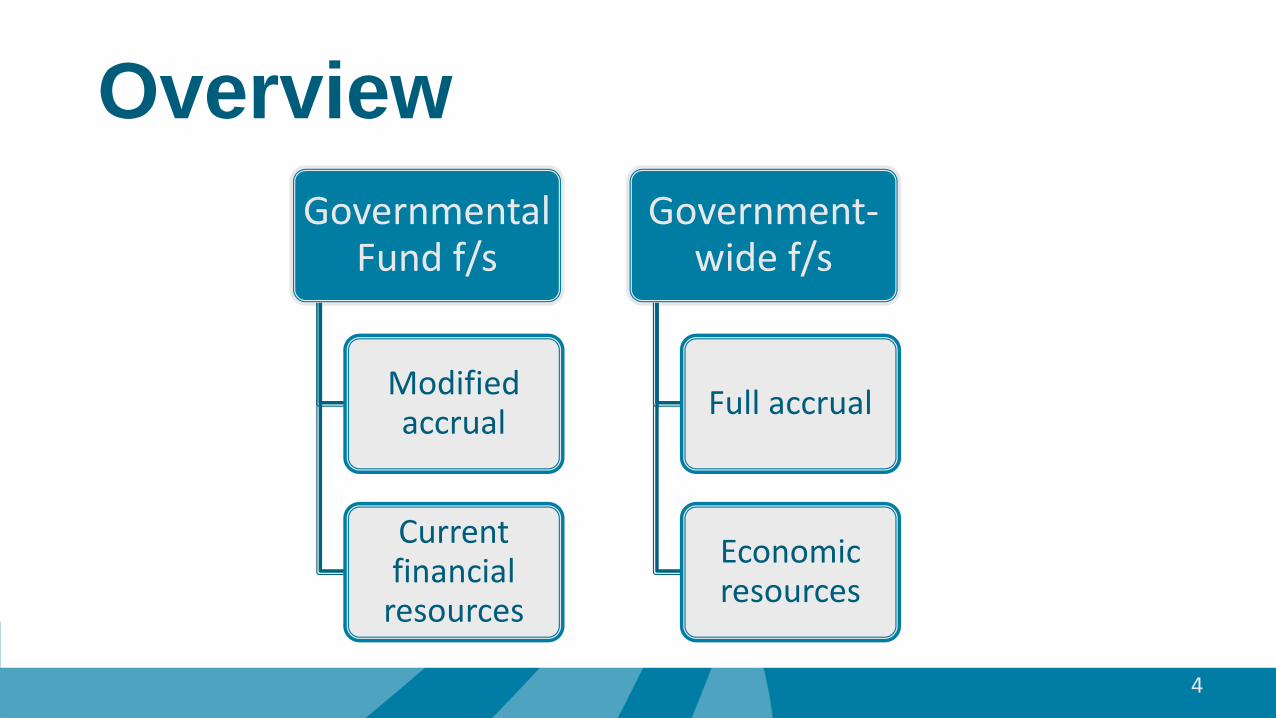

Overview

4

Governmental Fund f/s

Modified accrual

Current financial

resources

Government-wide f/s

Full accrual

Economic resources

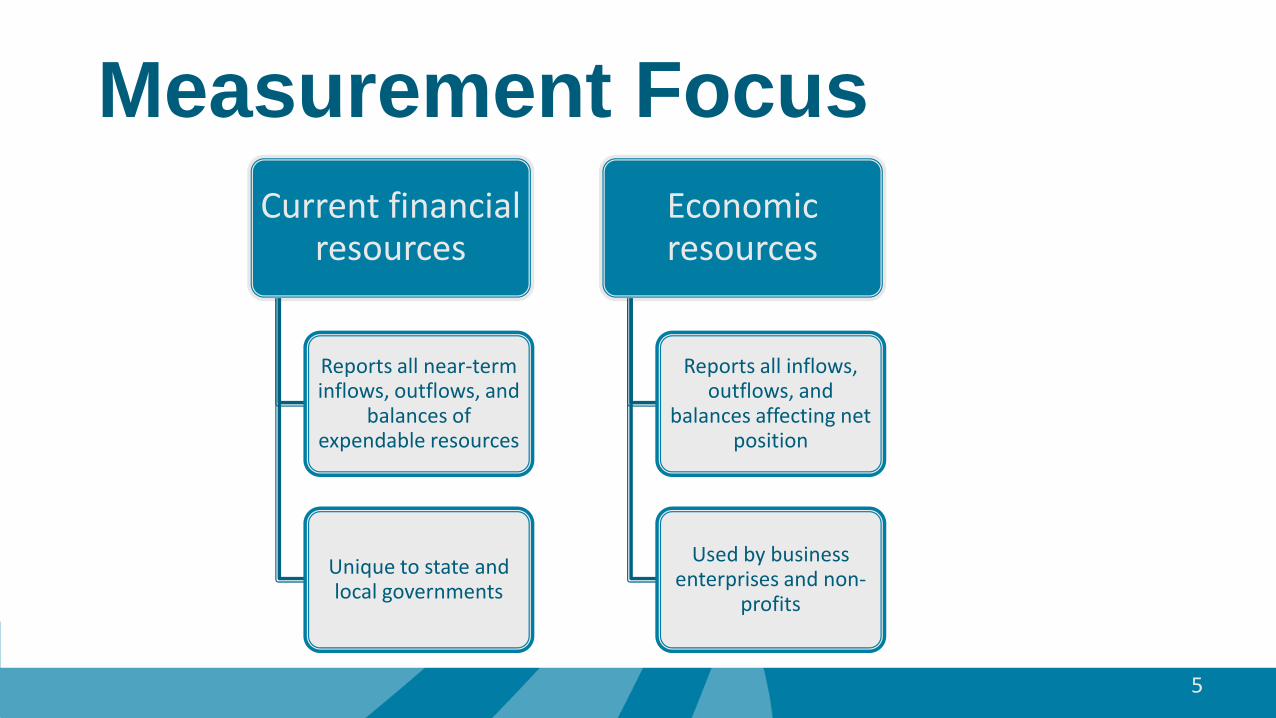

Measurement Focus

5

Current financial resources

Reports all near-term inflows, outflows, and

balances of expendable resources

Unique to state and local governments

Economic resources

Reports all inflows, outflows, and

balances affecting net position

Used by business enterprises and non-

profits

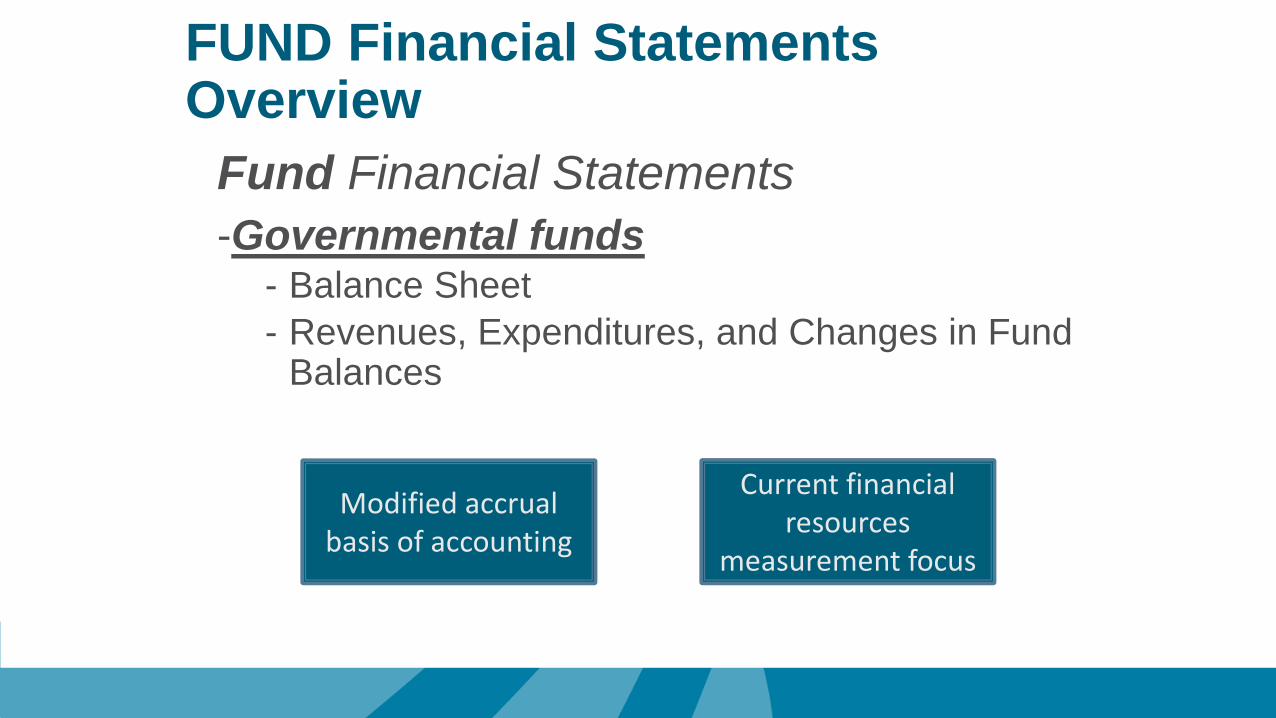

FUND Financial Statements Overview

Fund Financial Statements-Governmental funds

- Balance Sheet- Revenues, Expenditures, and Changes in Fund

Balances

Modified accrual basis of accounting

Current financial resources

measurement focus

FUND Financial Statements Overview

The fund financial statements focus on near-term inflows of spendable resources and are useful in evaluating the government’s near-term financing requirements.

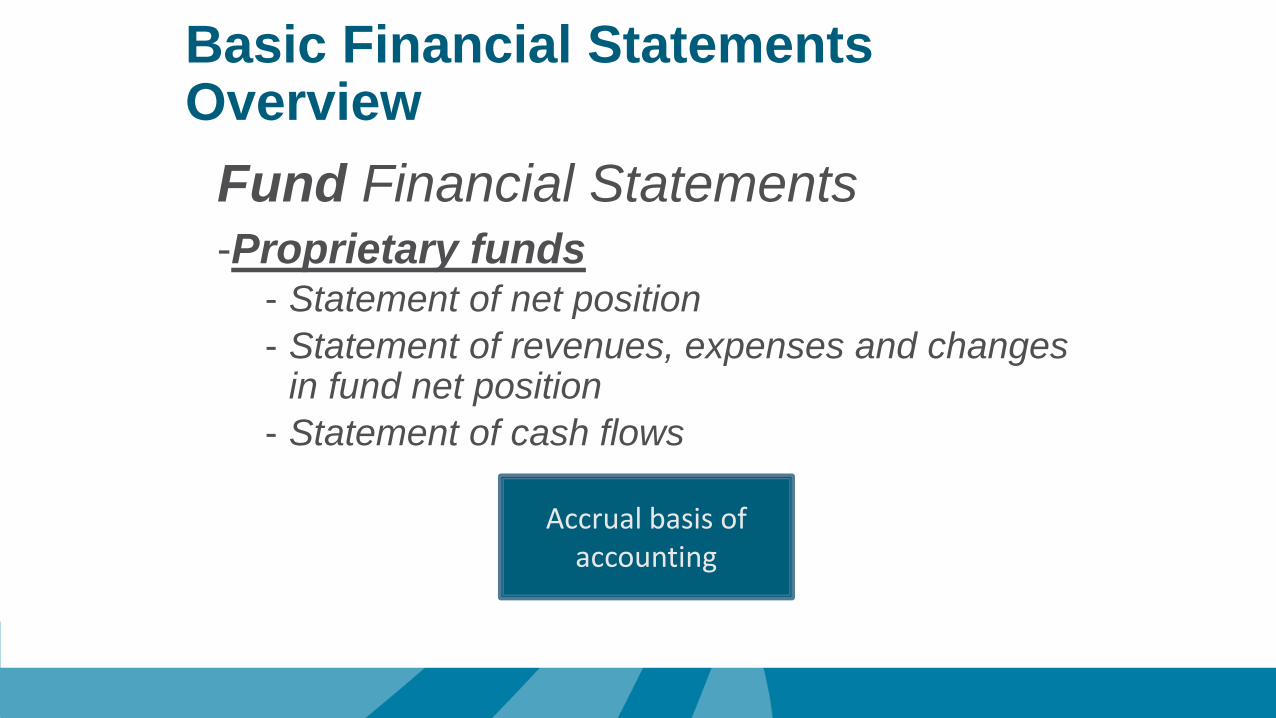

Basic Financial Statements Overview

Fund Financial Statements-Proprietary funds

- Statement of net position- Statement of revenues, expenses and changes

in fund net position- Statement of cash flows

Accrual basis of accounting

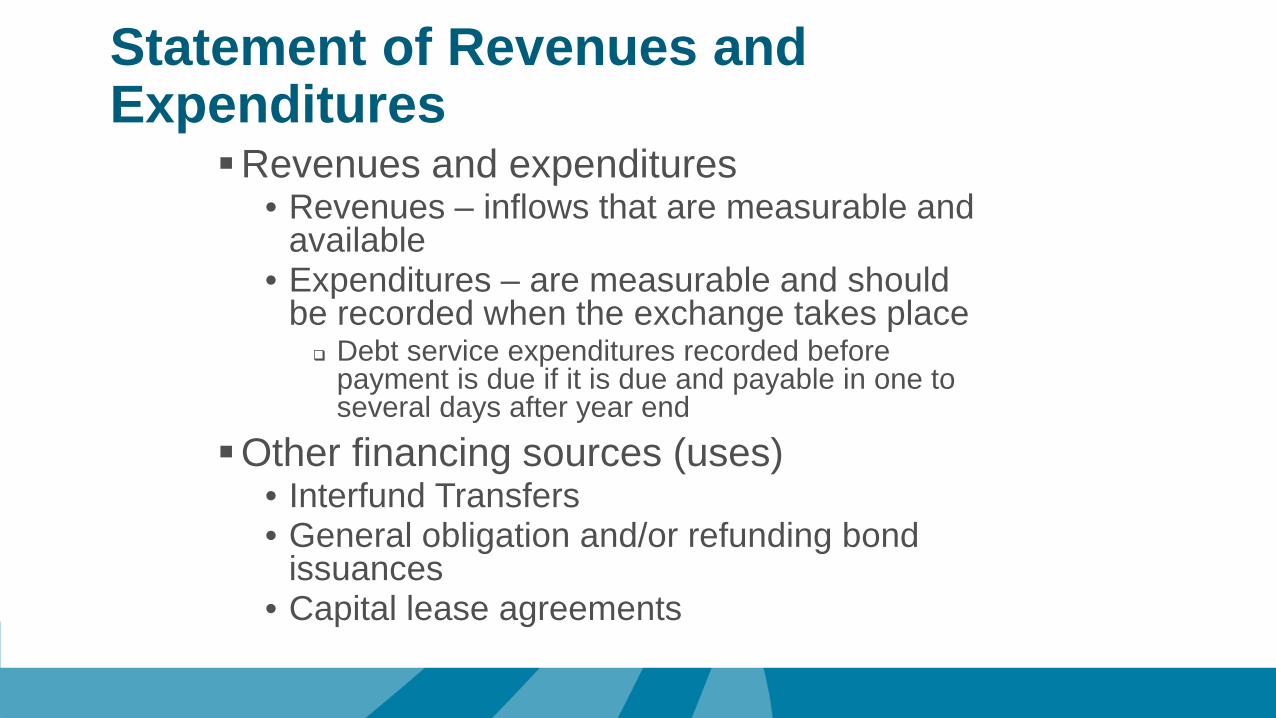

Statement of Revenues and Expenditures

Revenues and expenditures• Revenues – inflows that are measurable and

available• Expenditures – are measurable and should

be recorded when the exchange takes place Debt service expenditures recorded before

payment is due if it is due and payable in one to several days after year end

Other financing sources (uses)• Interfund Transfers• General obligation and/or refunding bond

issuances• Capital lease agreements

Basic Financial Statements Overview

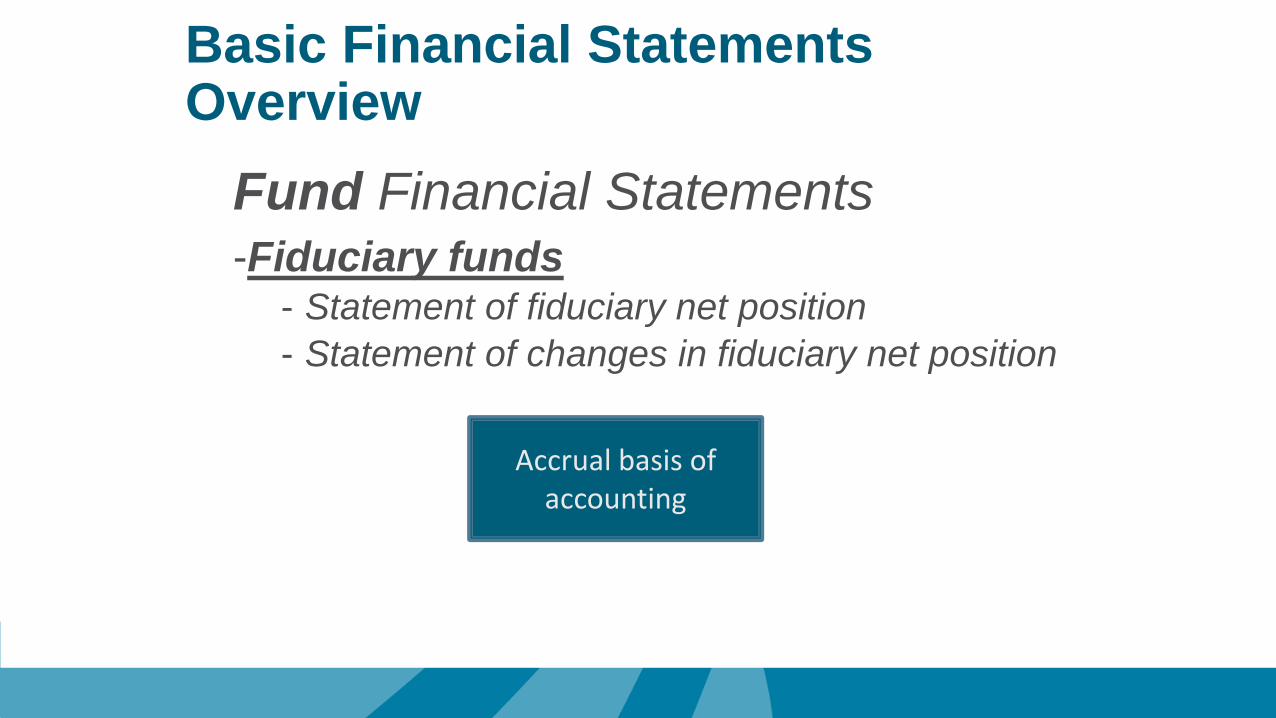

Fund Financial Statements-Fiduciary funds

- Statement of fiduciary net position- Statement of changes in fiduciary net position

Accrual basis of accounting

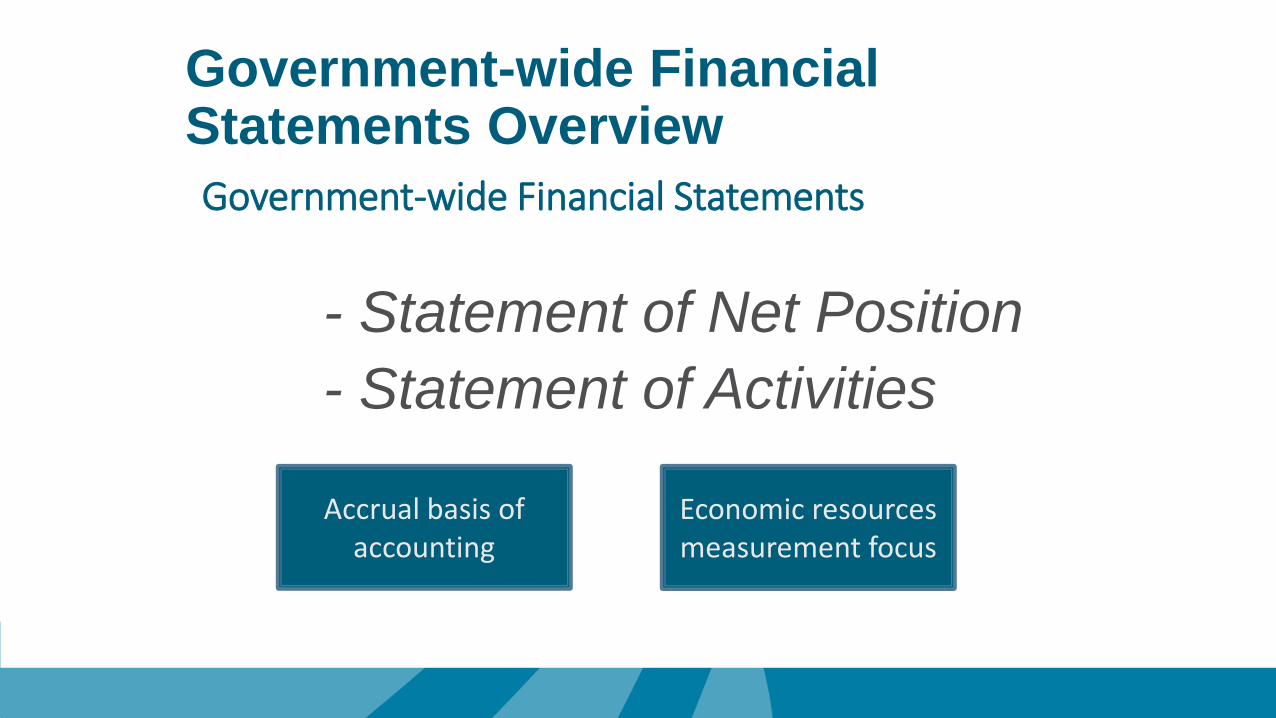

Government-wide Financial Statements Overview

- Statement of Net Position- Statement of Activities

Government-wide Financial Statements

Accrual basis of accounting

Economic resources measurement focus

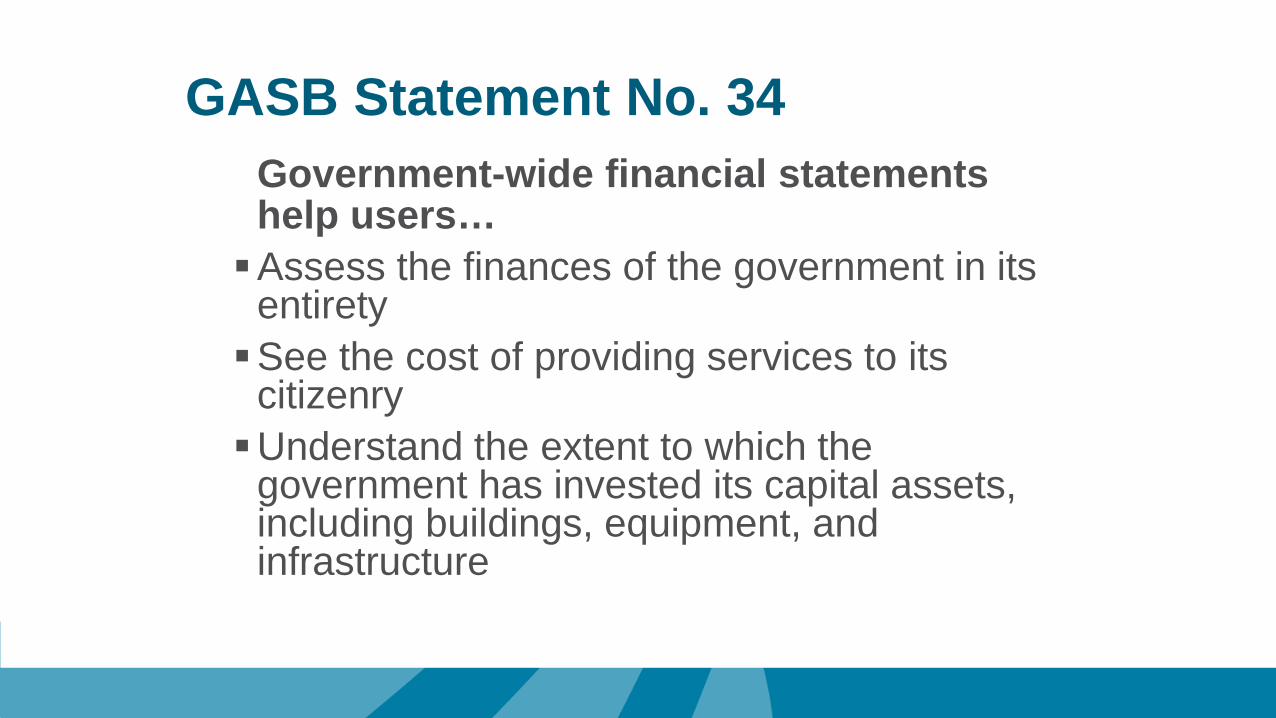

GASB Statement No. 34Government-wide financial statements help users…Assess the finances of the government in its

entiretySee the cost of providing services to its

citizenryUnderstand the extent to which the

government has invested its capital assets, including buildings, equipment, and infrastructure

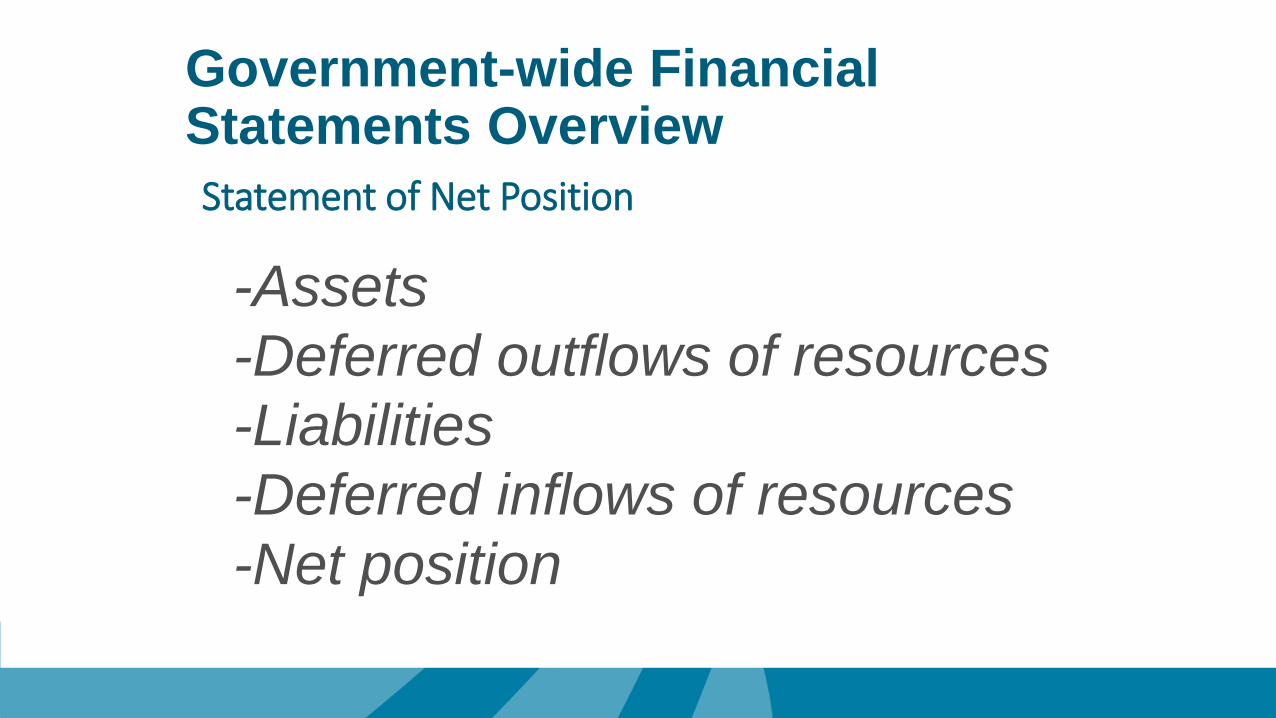

Government-wide Financial Statements Overview

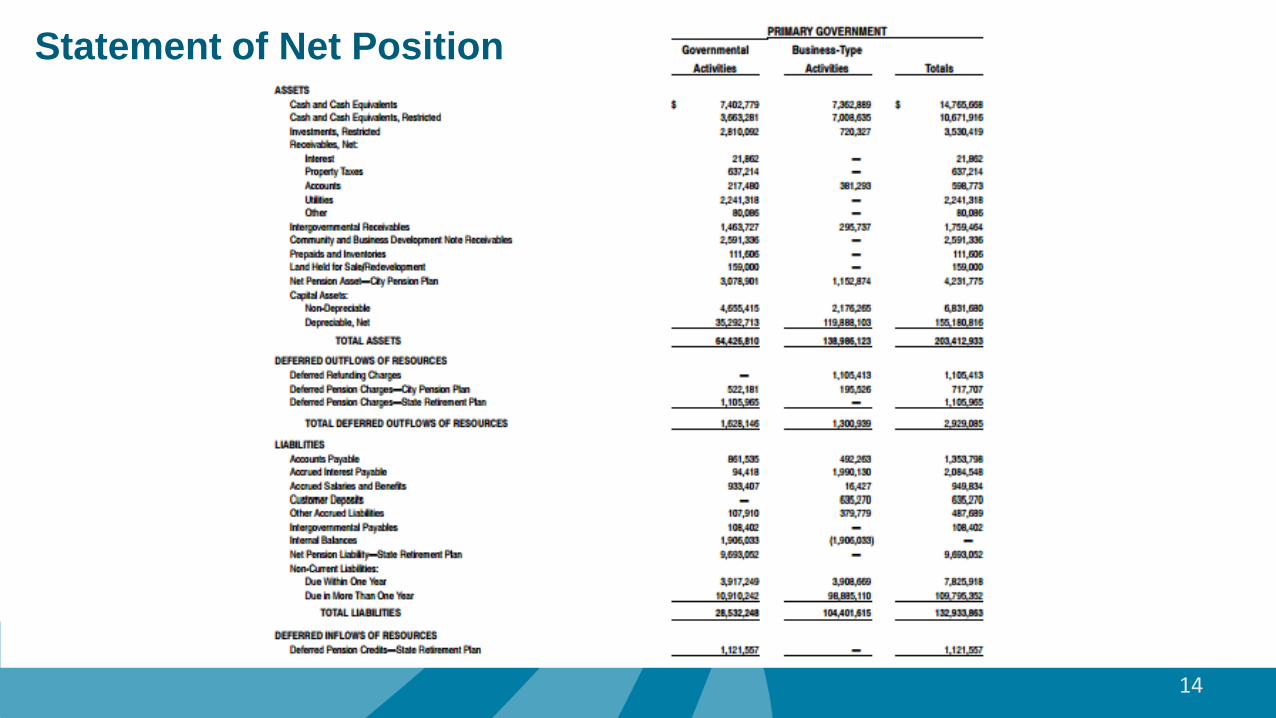

-Assets-Deferred outflows of resources-Liabilities-Deferred inflows of resources-Net position

Statement of Net Position

14

Statement of Net Position

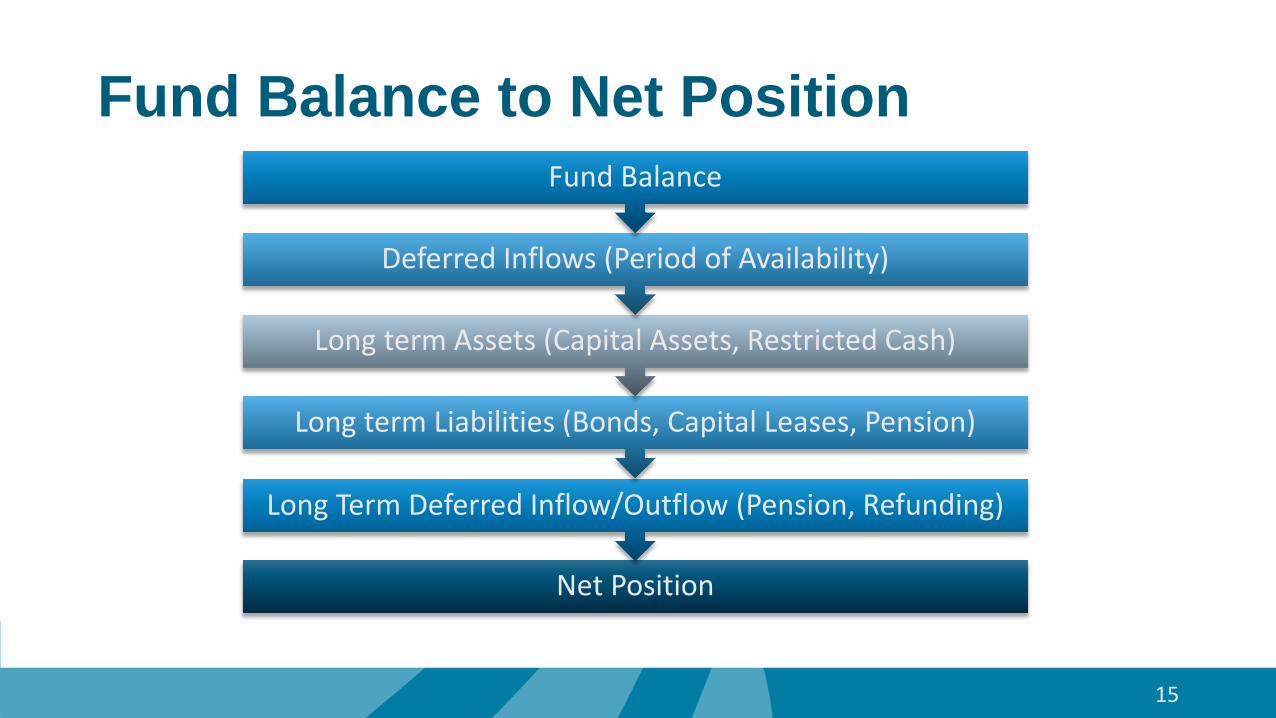

Fund Balance to Net Position

15

Net Position

Long Term Deferred Inflow/Outflow (Pension, Refunding)

Long term Liabilities (Bonds, Capital Leases, Pension)

Long term Assets (Capital Assets, Restricted Cash)

Deferred Inflows (Period of Availability)

Fund Balance

16

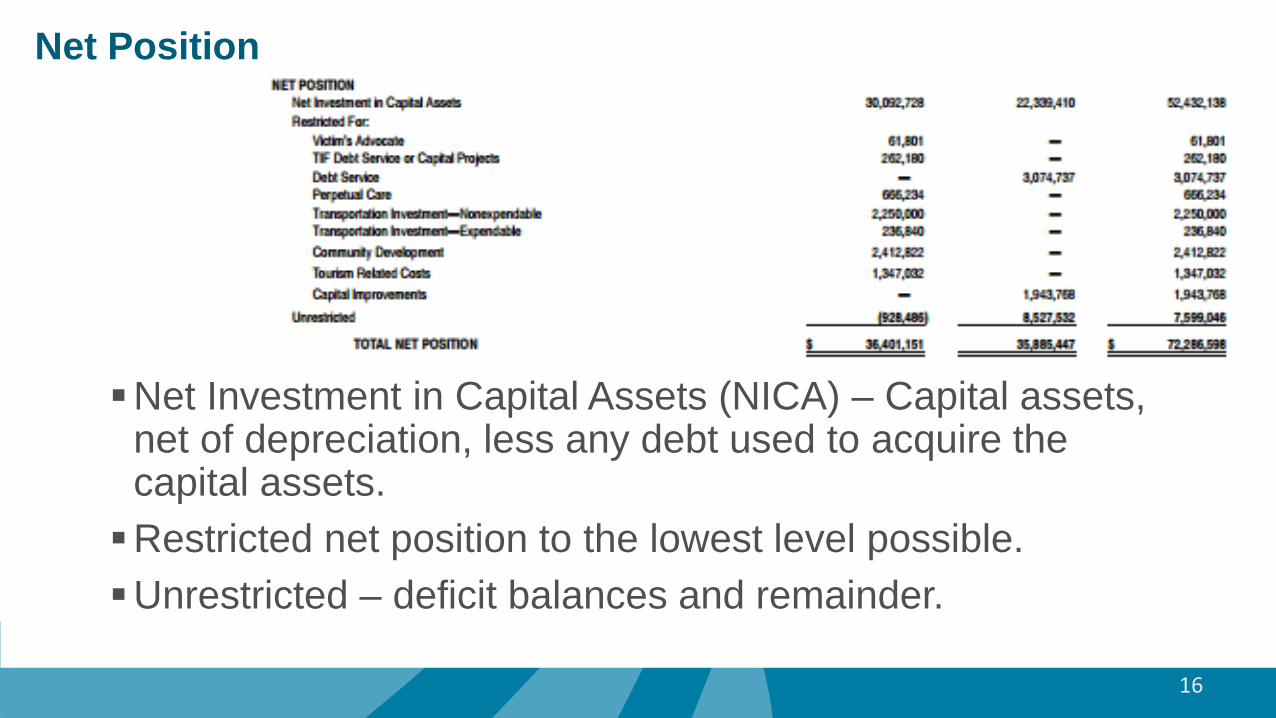

Net Investment in Capital Assets (NICA) – Capital assets, net of depreciation, less any debt used to acquire the capital assets.Restricted net position to the lowest level possible.Unrestricted – deficit balances and remainder.

Net Position

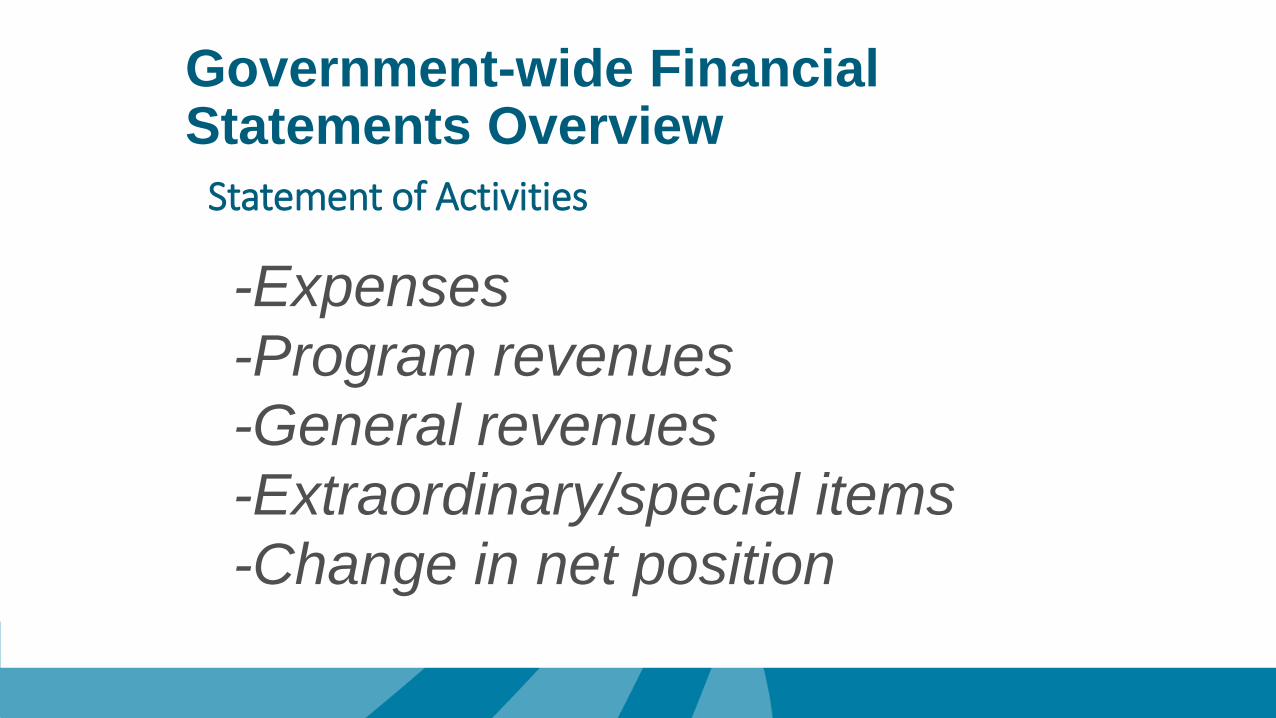

Government-wide Financial Statements Overview

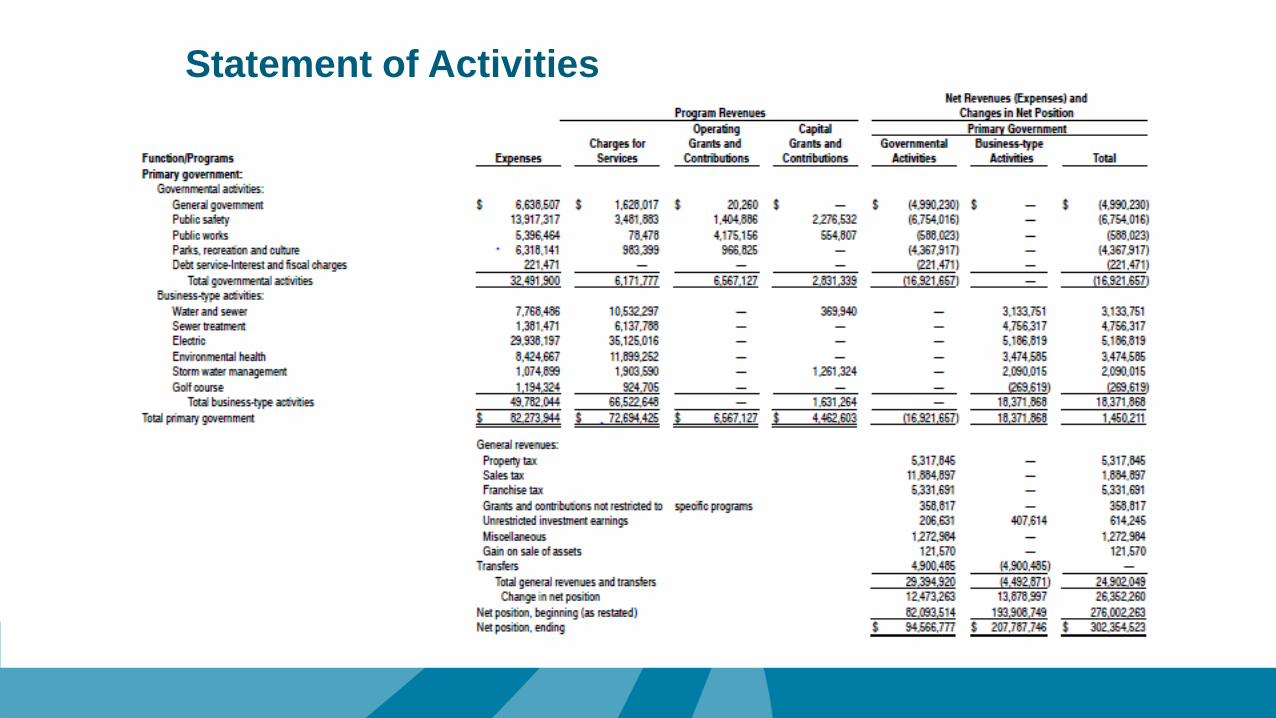

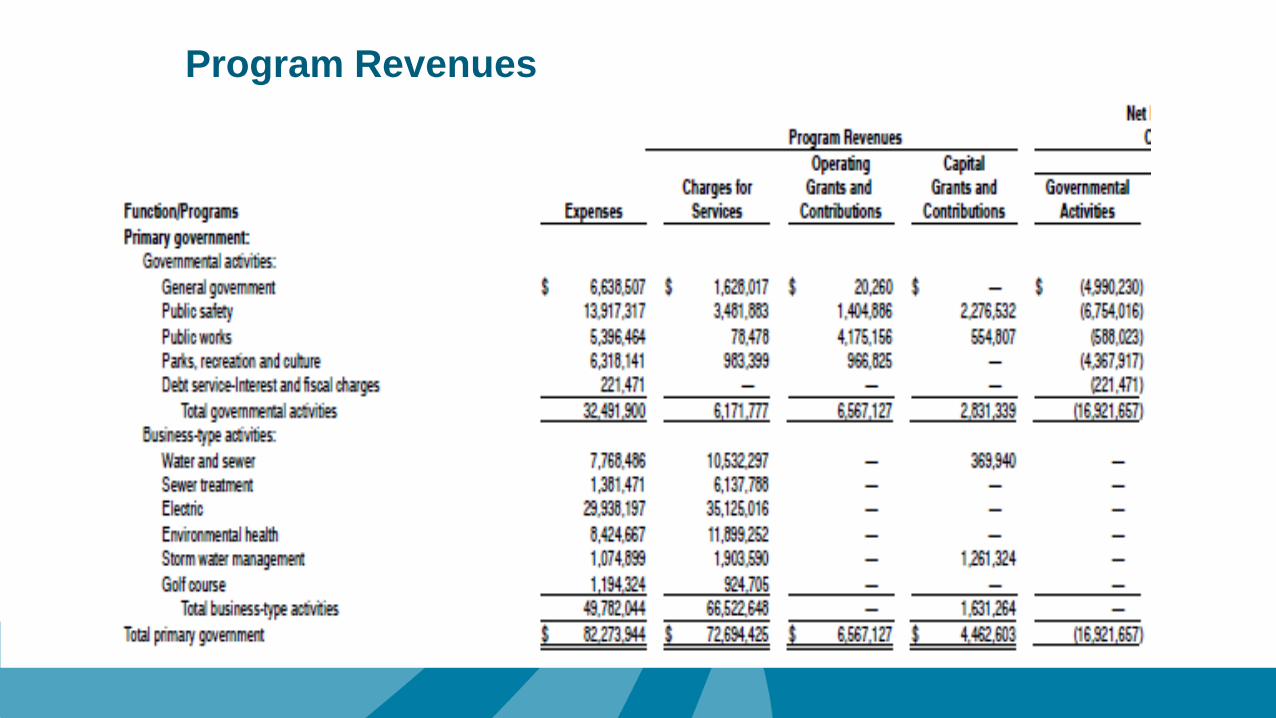

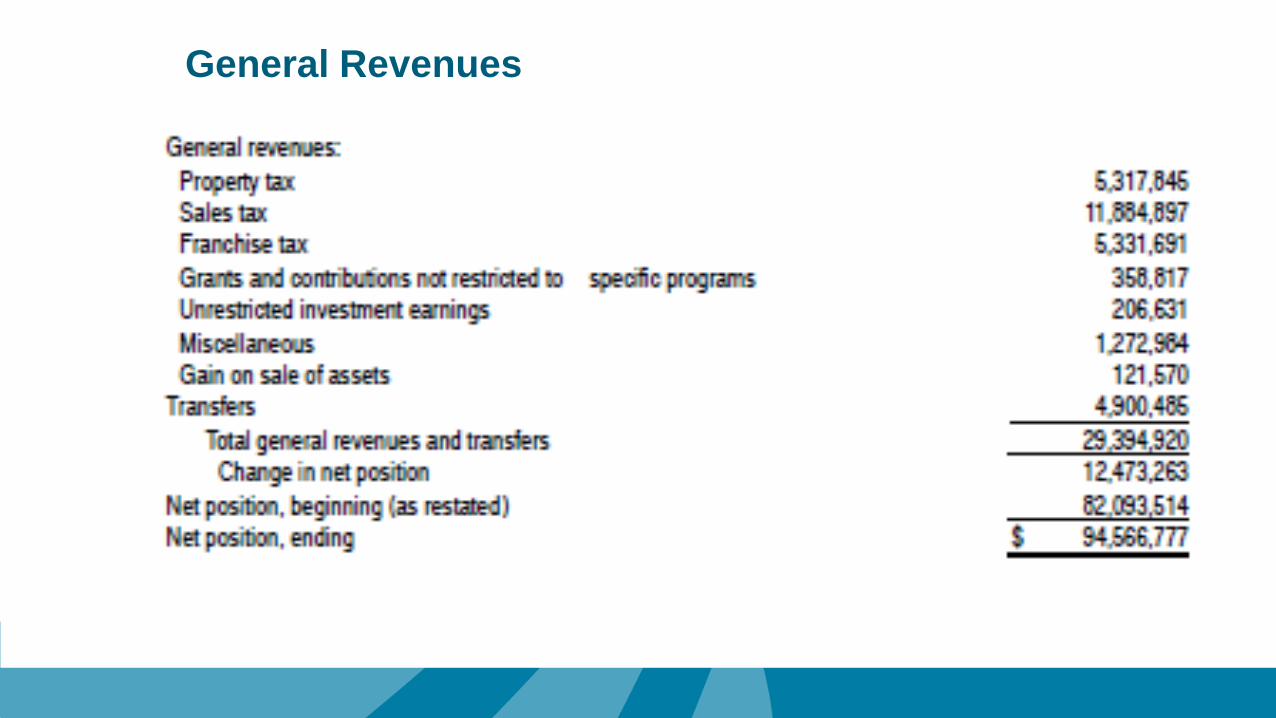

-Expenses-Program revenues-General revenues-Extraordinary/special items-Change in net position

Statement of Activities

Statement of Activities

Program Revenues

General Revenues

Reconciliations

Balance Sheet – Governmental Fundsto the Statement of Net Position

Statement of Revenues, Expenditures and Changes in Fund Balance –Governmental Fundsto the Statement of Activities

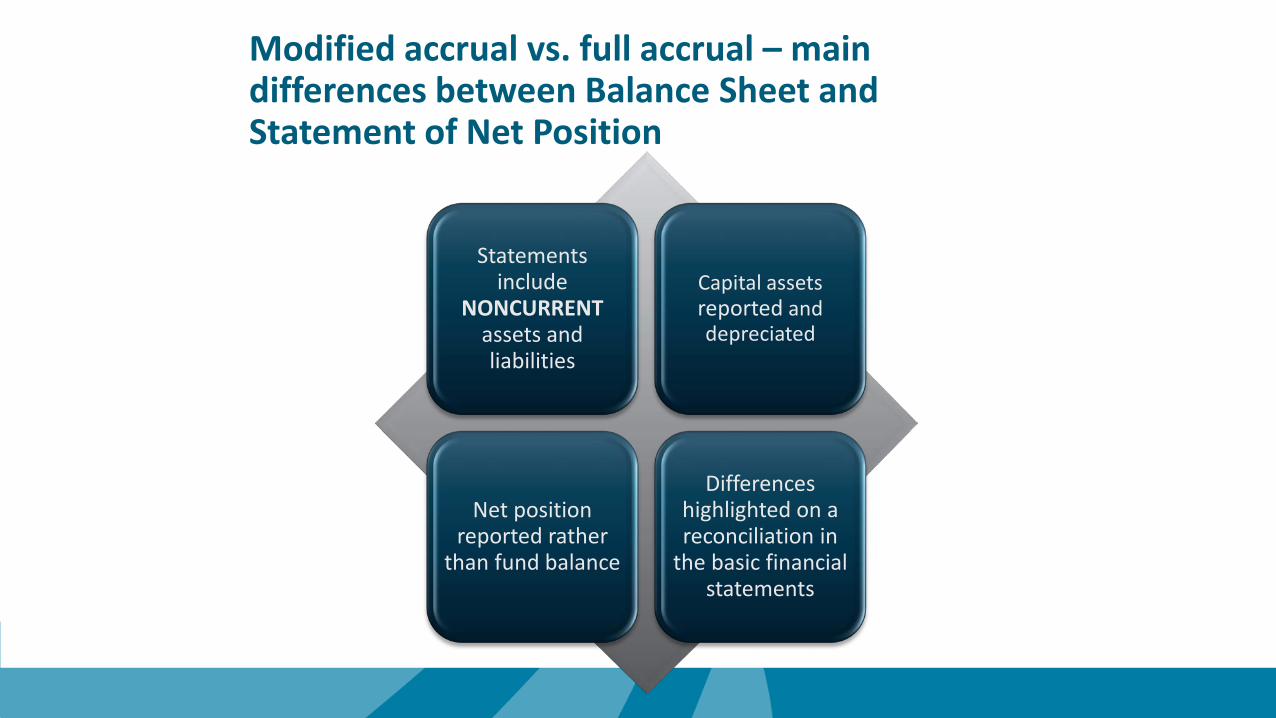

Modified accrual vs. full accrual – main differences between Balance Sheet and Statement of Net Position

Statements include

NONCURRENT assets and liabilities

Capital assets reported and depreciated

Net position reported rather

than fund balance

Differences highlighted on a reconciliation in

the basic financial statements

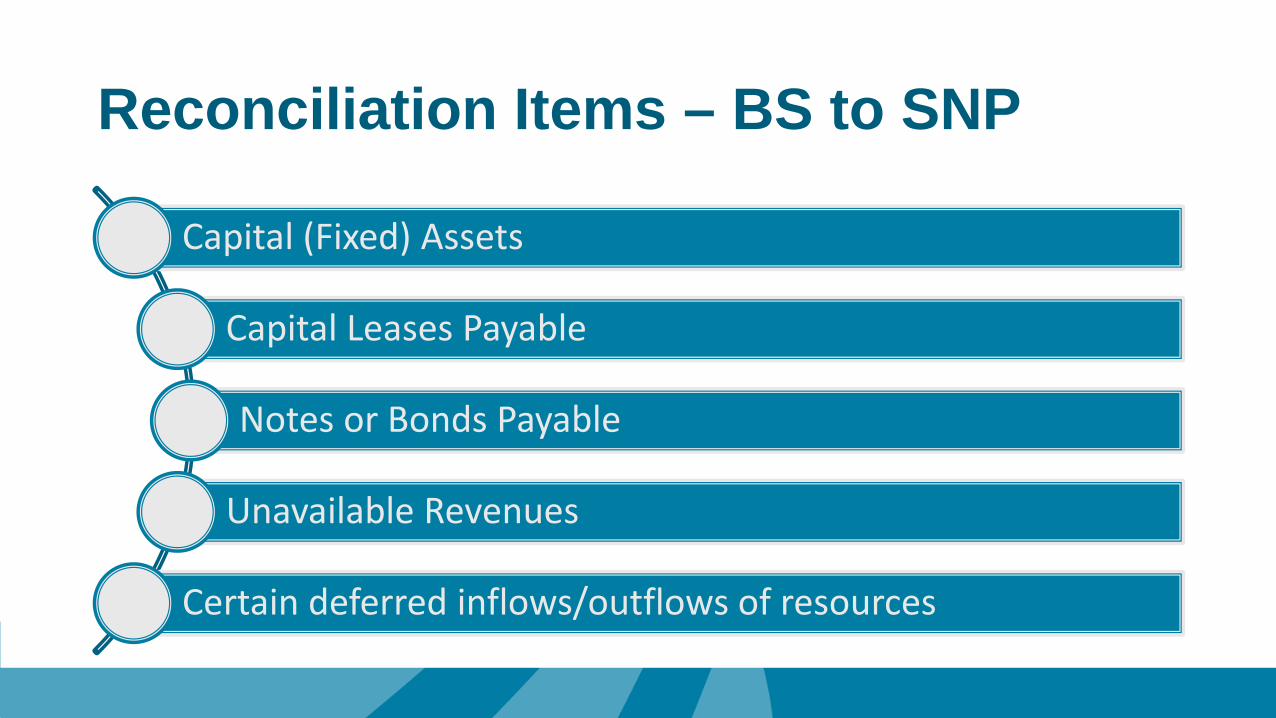

Reconciliation Items – BS to SNP

Capital (Fixed) Assets

Capital Leases Payable

Notes or Bonds Payable

Unavailable Revenues

Certain deferred inflows/outflows of resources

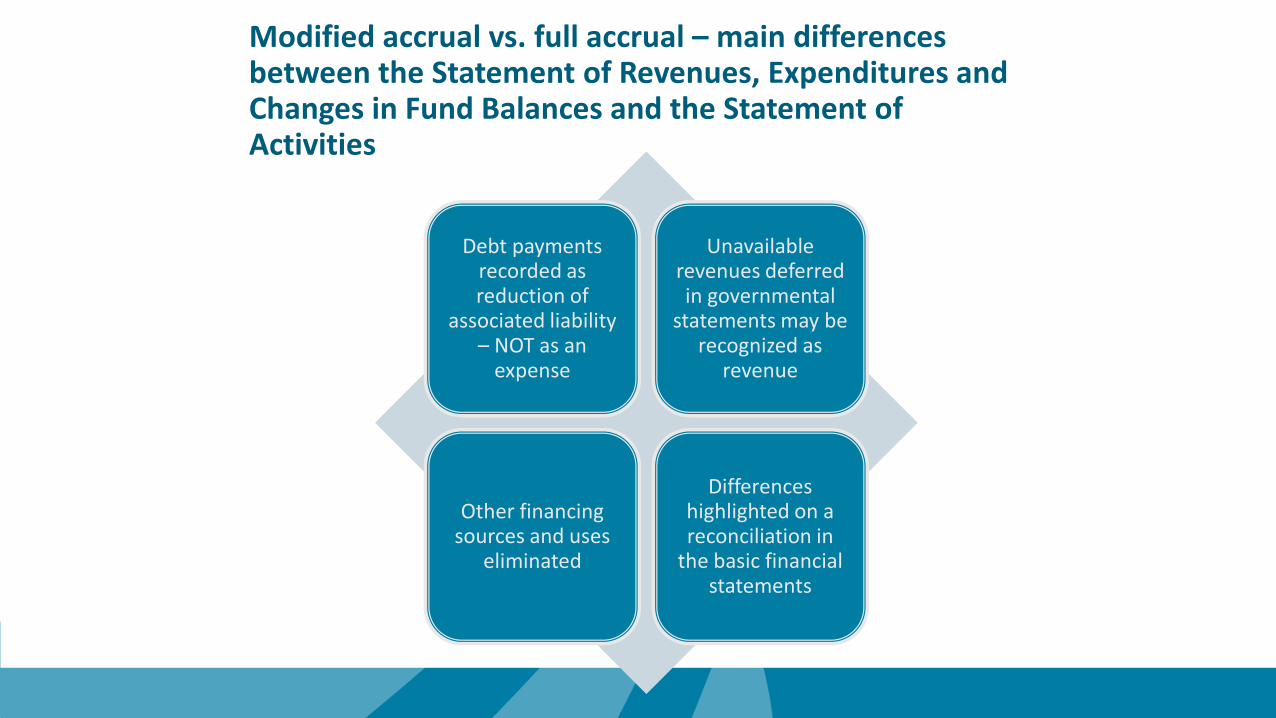

Modified accrual vs. full accrual – main differences between the Statement of Revenues, Expenditures and Changes in Fund Balances and the Statement of Activities

Debt payments recorded as reduction of

associated liability – NOT as an

expense

Unavailable revenues deferred in governmental

statements may be recognized as

revenue

Other financing sources and uses

eliminated

Differences highlighted on a reconciliation in

the basic financial statements

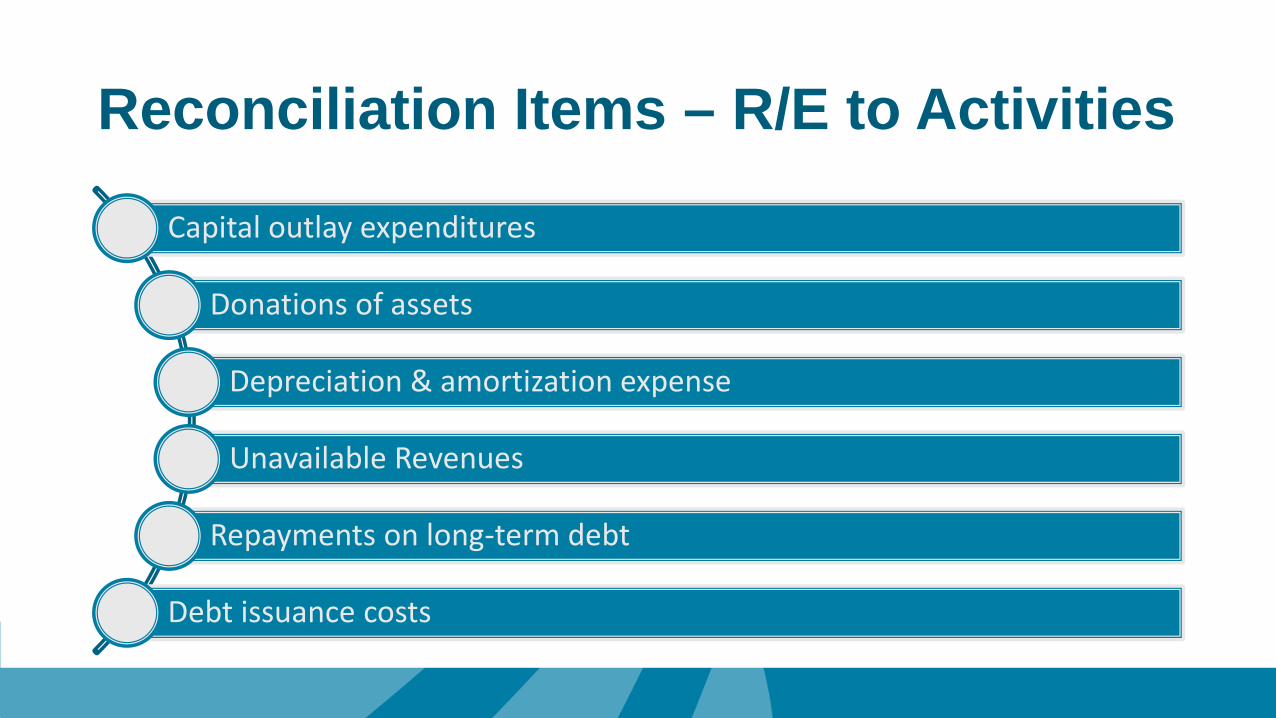

Reconciliation Items – R/E to Activities

Capital outlay expenditures

Donations of assets

Depreciation & amortization expense

Unavailable Revenues

Repayments on long-term debt

Debt issuance costs

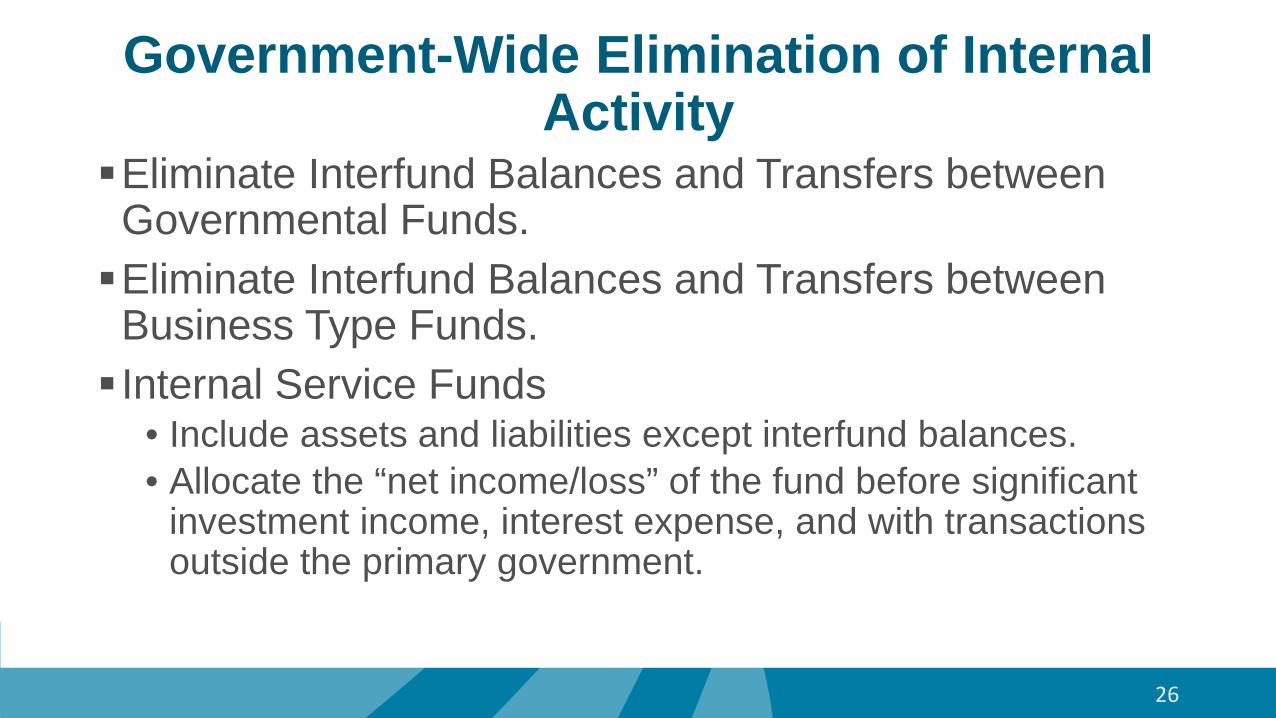

Government-Wide Elimination of Internal Activity

Eliminate Interfund Balances and Transfers between Governmental Funds.Eliminate Interfund Balances and Transfers between

Business Type Funds. Internal Service Funds

• Include assets and liabilities except interfund balances.• Allocate the “net income/loss” of the fund before significant

investment income, interest expense, and with transactions outside the primary government.

26

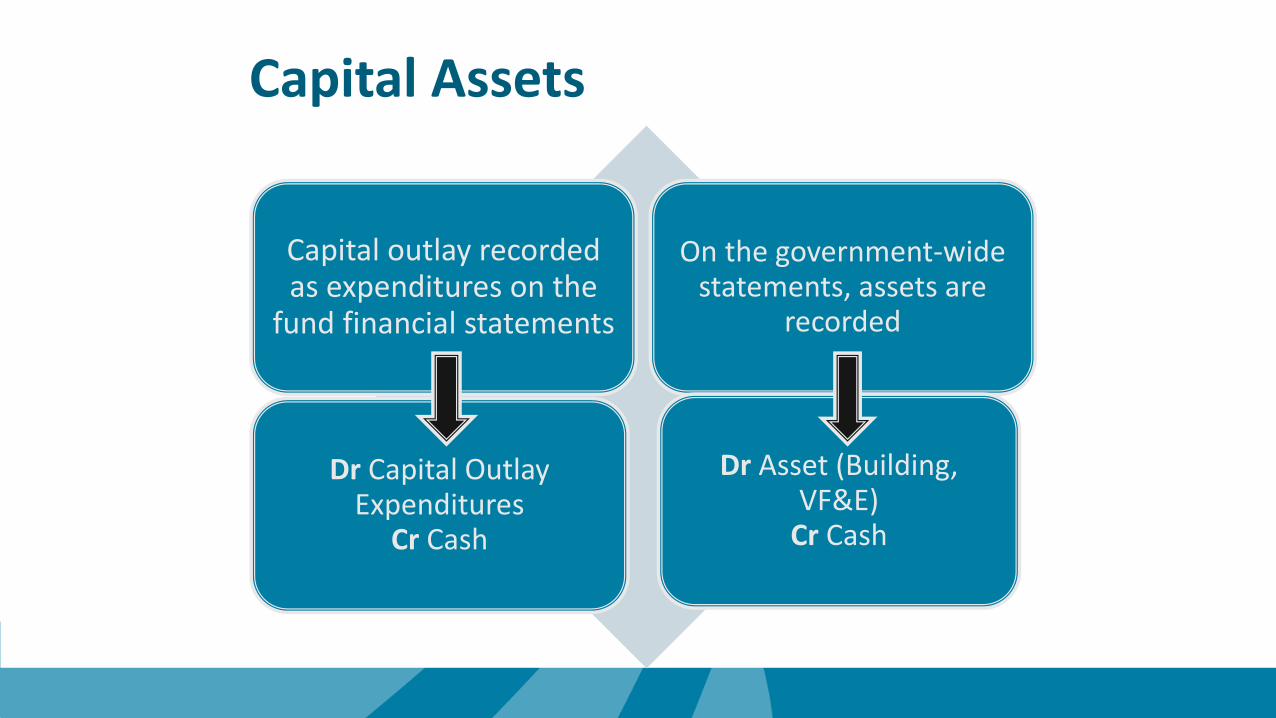

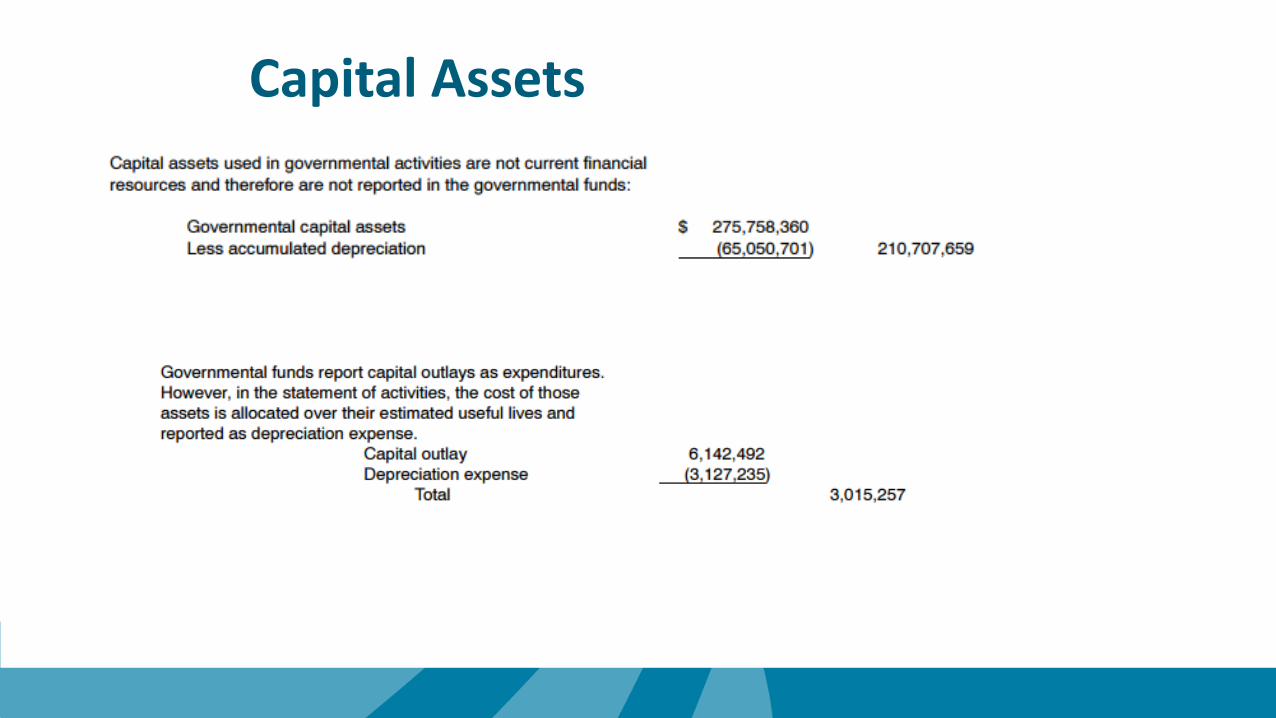

Capital Assets

Capital outlay recorded as expenditures on the

fund financial statements

On the government-wide statements, assets are

recorded

Dr Capital Outlay Expenditures

Cr Cash

Dr Asset (Building, VF&E)

Cr Cash

Capital Assets

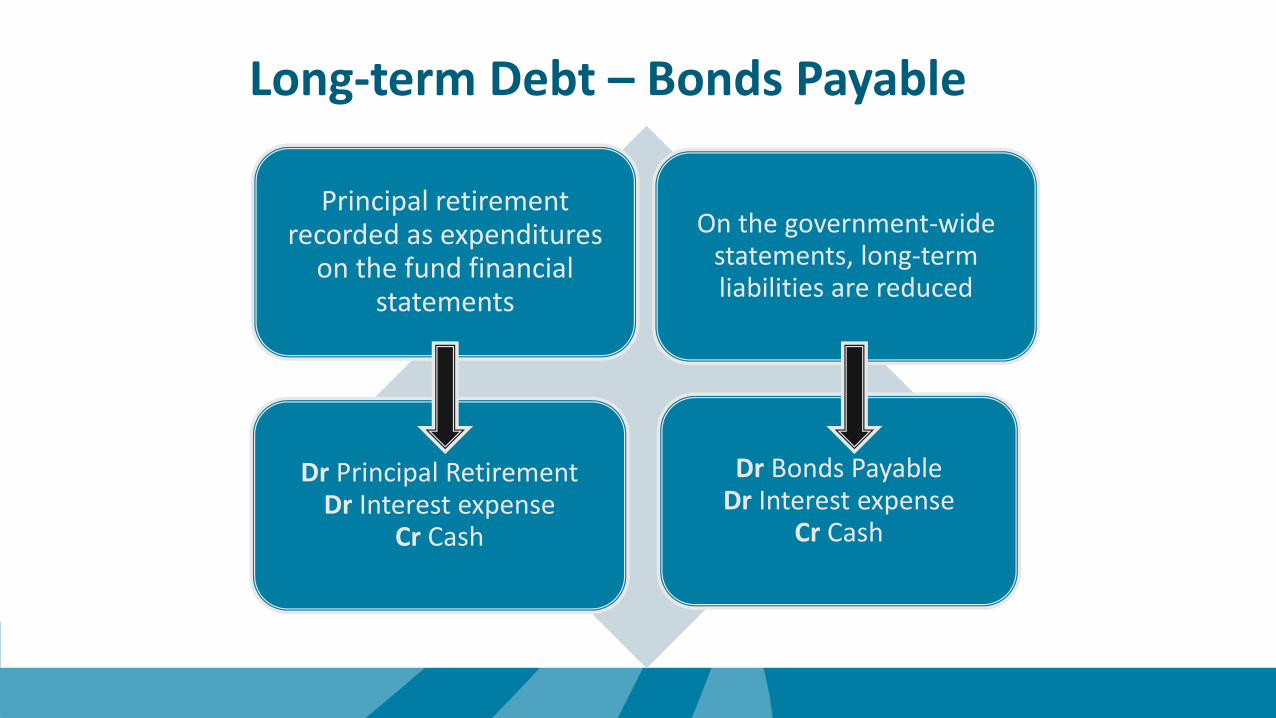

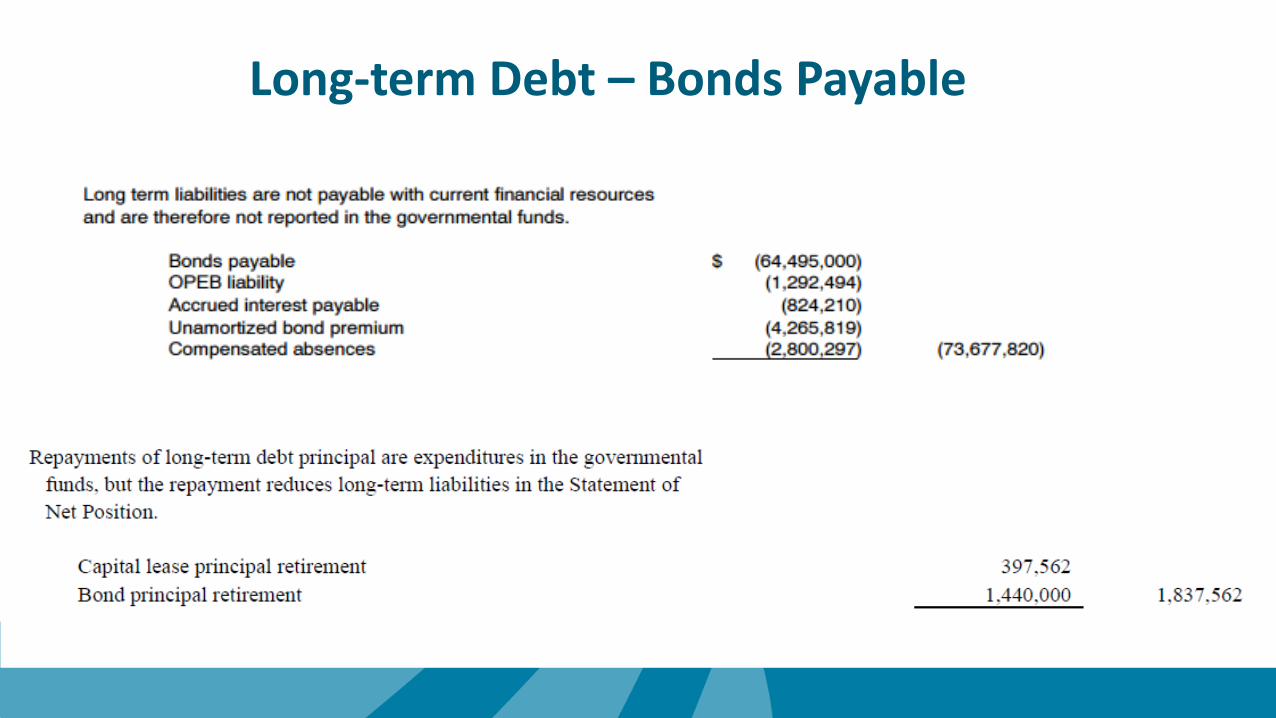

Long-term Debt – Bonds Payable

Principal retirement recorded as expenditures

on the fund financial statements

On the government-wide statements, long-term liabilities are reduced

Dr Principal RetirementDr Interest expense

Cr Cash

Dr Bonds PayableDr Interest expense

Cr Cash

Long-term Debt – Bonds Payable

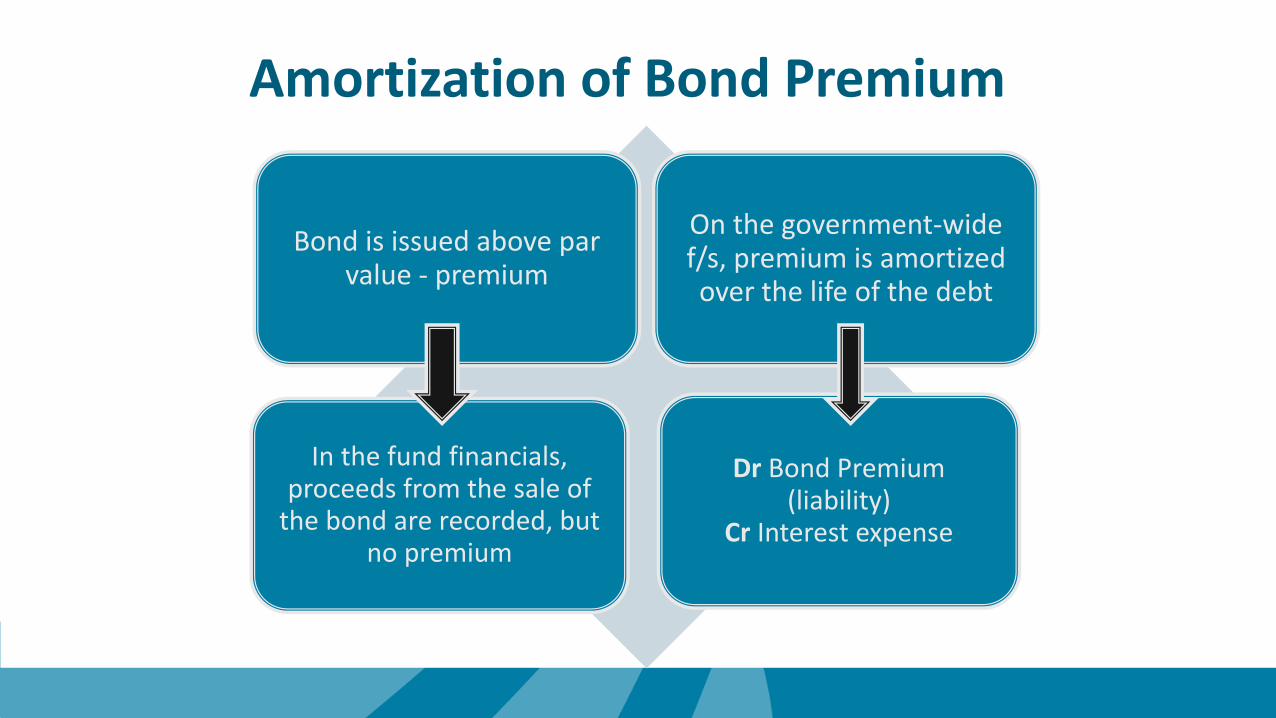

Amortization of Bond Premium

Bond is issued above par value - premium

On the government-wide f/s, premium is amortized over the life of the debt

In the fund financials, proceeds from the sale of

the bond are recorded, but no premium

Dr Bond Premium (liability)

Cr Interest expense

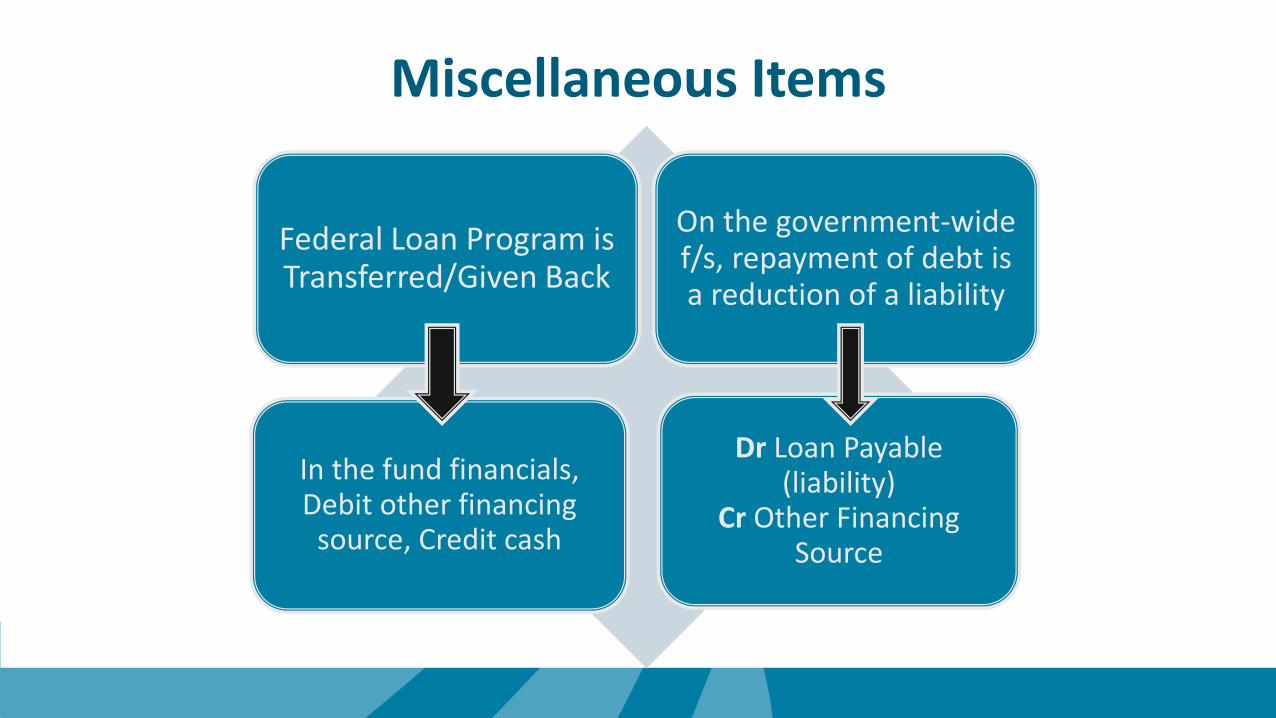

Miscellaneous Items

Federal Loan Program is Transferred/Given Back

On the government-wide f/s, repayment of debt is a reduction of a liability

In the fund financials, Debit other financing

source, Credit cash

Dr Loan Payable (liability)

Cr Other Financing Source

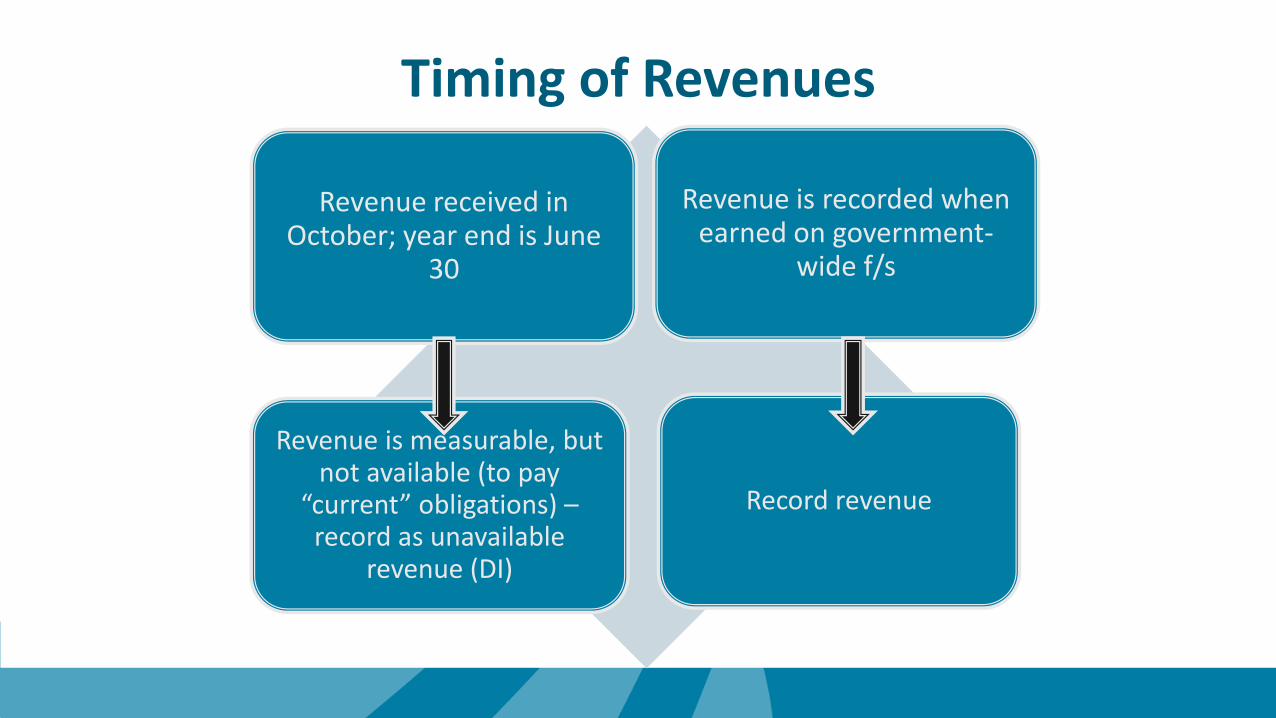

Timing of Revenues

Revenue received in October; year end is June

30

Revenue is recorded when earned on government-

wide f/s

Revenue is measurable, but not available (to pay

“current” obligations) –record as unavailable

revenue (DI)

Record revenue

Are we done yet?Not quite……..

Governmental Accounting: A Dive Into Revenues

Agenda1. Exchange vs. Nonexchange revenues2. Revenue Recognition 3. Revenue Sources

1. Accounting2. Financial Statement Presentation3. Reporting Complexities

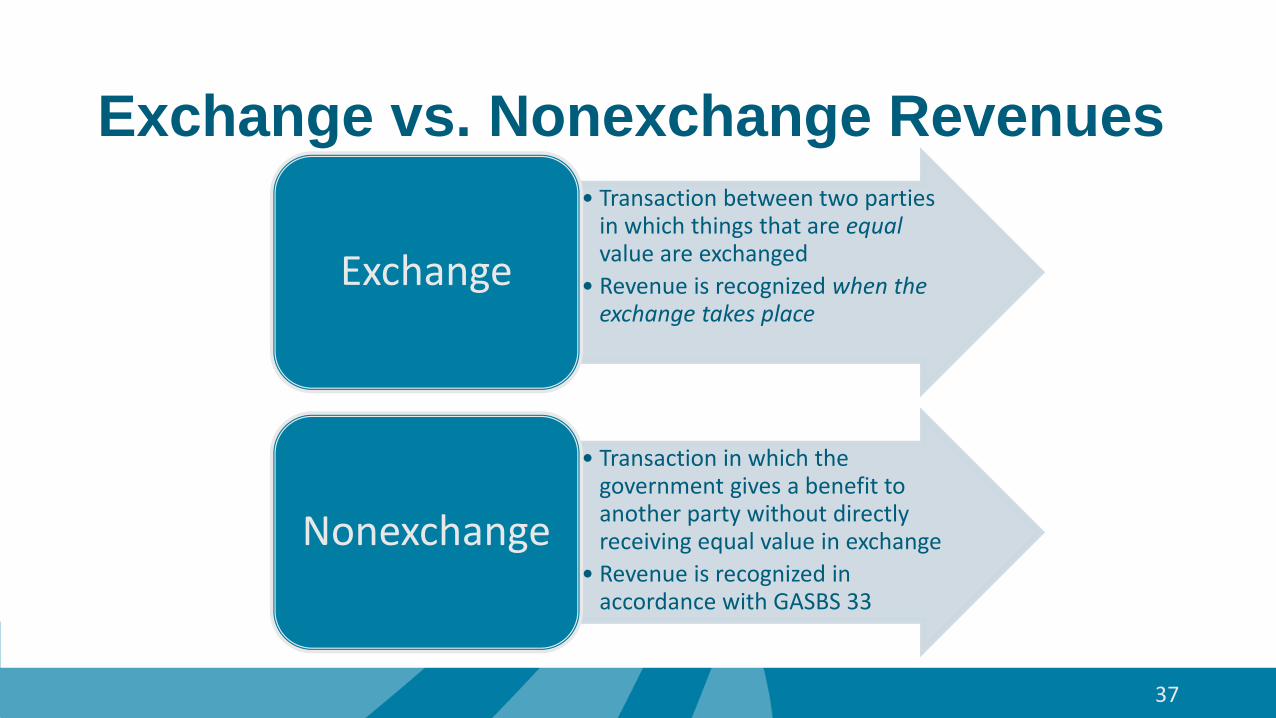

Exchange vs. Nonexchange Revenues

37

• Transaction between two parties in which things that are equalvalue are exchanged

• Revenue is recognized when the exchange takes place

Exchange

• Transaction in which the government gives a benefit to another party without directly receiving equal value in exchange

• Revenue is recognized in accordance with GASBS 33

Nonexchange

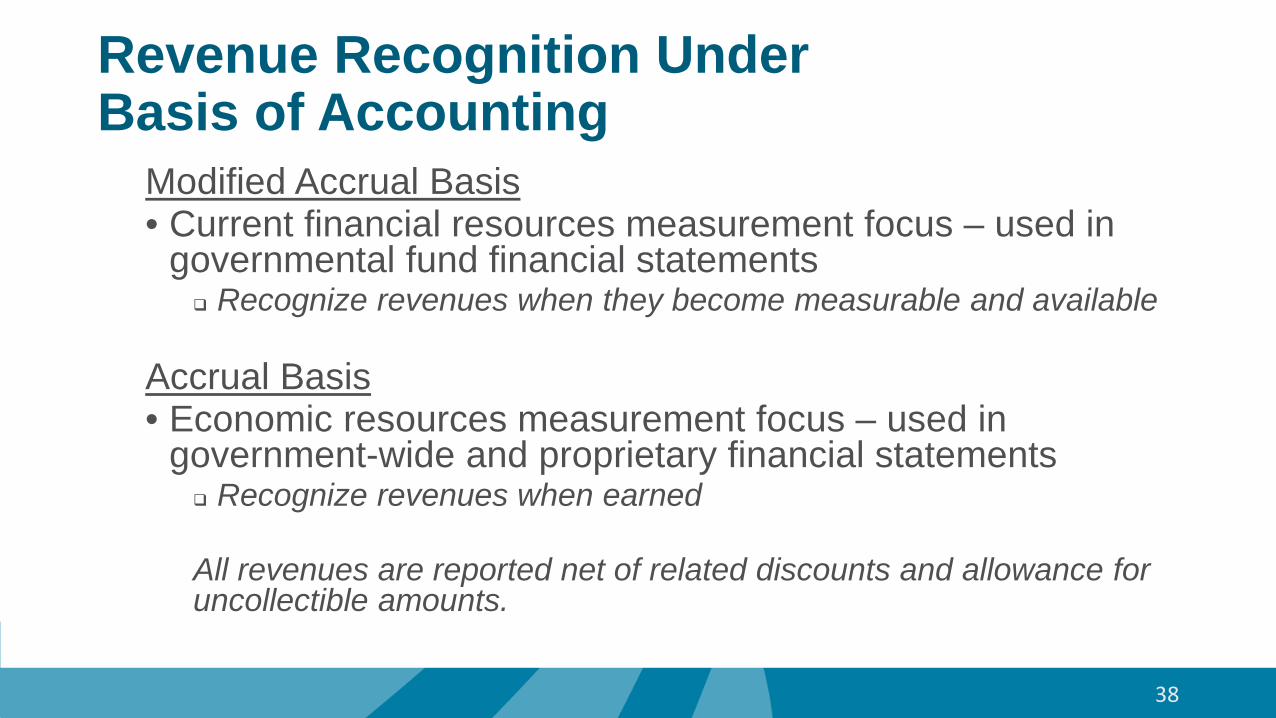

Revenue Recognition Under Basis of Accounting

Modified Accrual Basis• Current financial resources measurement focus – used in

governmental fund financial statements Recognize revenues when they become measurable and available

Accrual Basis• Economic resources measurement focus – used in

government-wide and proprietary financial statements Recognize revenues when earned

All revenues are reported net of related discounts and allowance for uncollectible amounts.

38

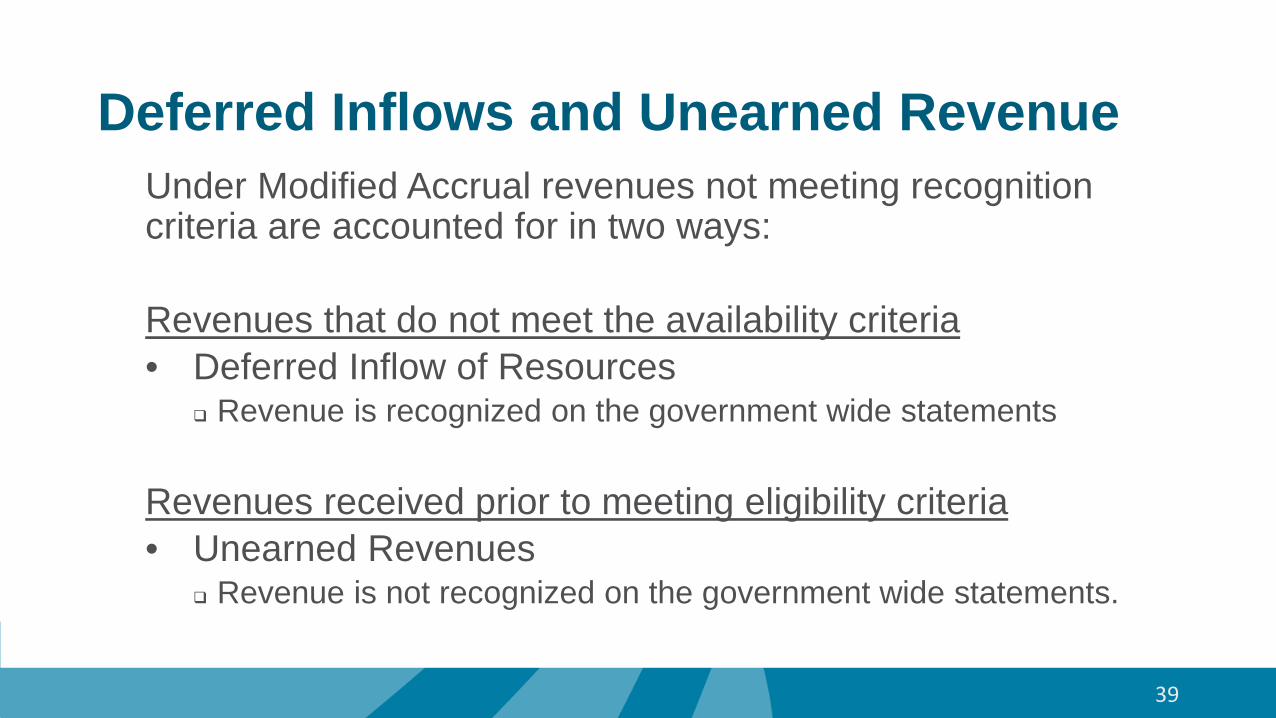

Deferred Inflows and Unearned RevenueUnder Modified Accrual revenues not meeting recognition criteria are accounted for in two ways:

Revenues that do not meet the availability criteria • Deferred Inflow of Resources

Revenue is recognized on the government wide statements

Revenues received prior to meeting eligibility criteria• Unearned Revenues

Revenue is not recognized on the government wide statements.

39

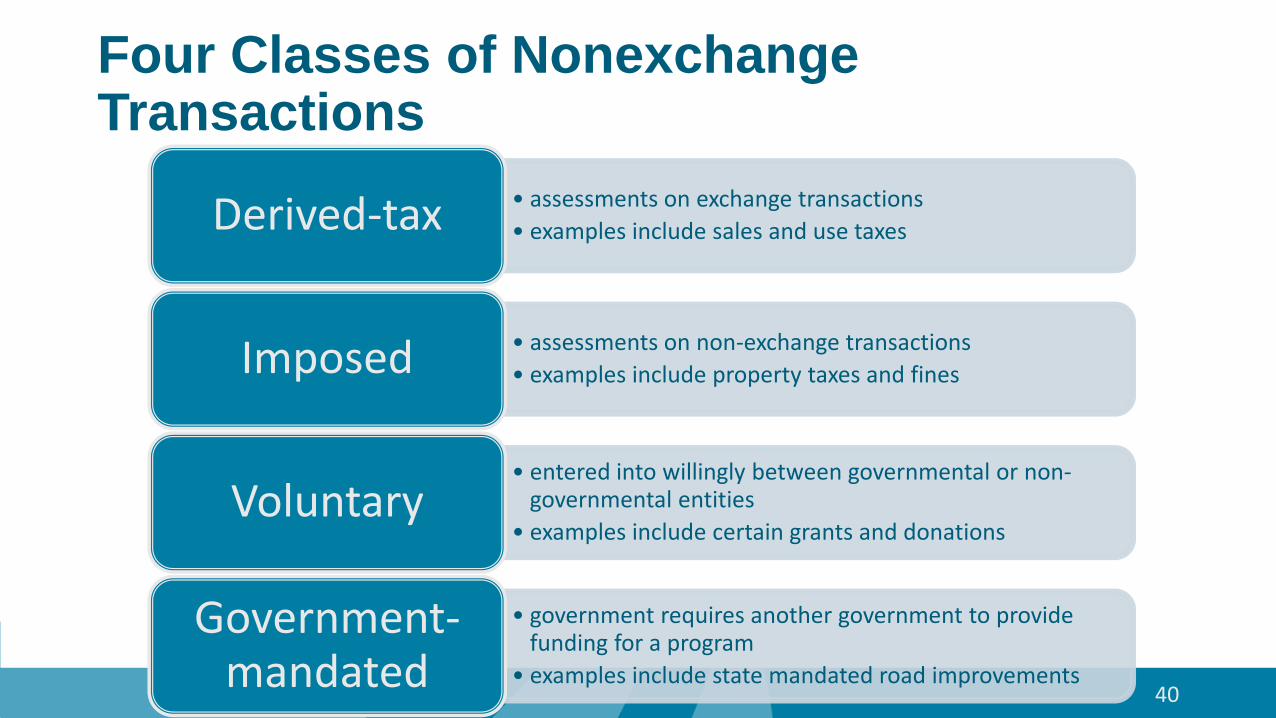

Four Classes of NonexchangeTransactions

40

• assessments on exchange transactions• examples include sales and use taxesDerived-tax

• assessments on non-exchange transactions• examples include property taxes and finesImposed

• entered into willingly between governmental or non-governmental entities

• examples include certain grants and donationsVoluntary

• government requires another government to provide funding for a program

• examples include state mandated road improvements

Government-mandated

41

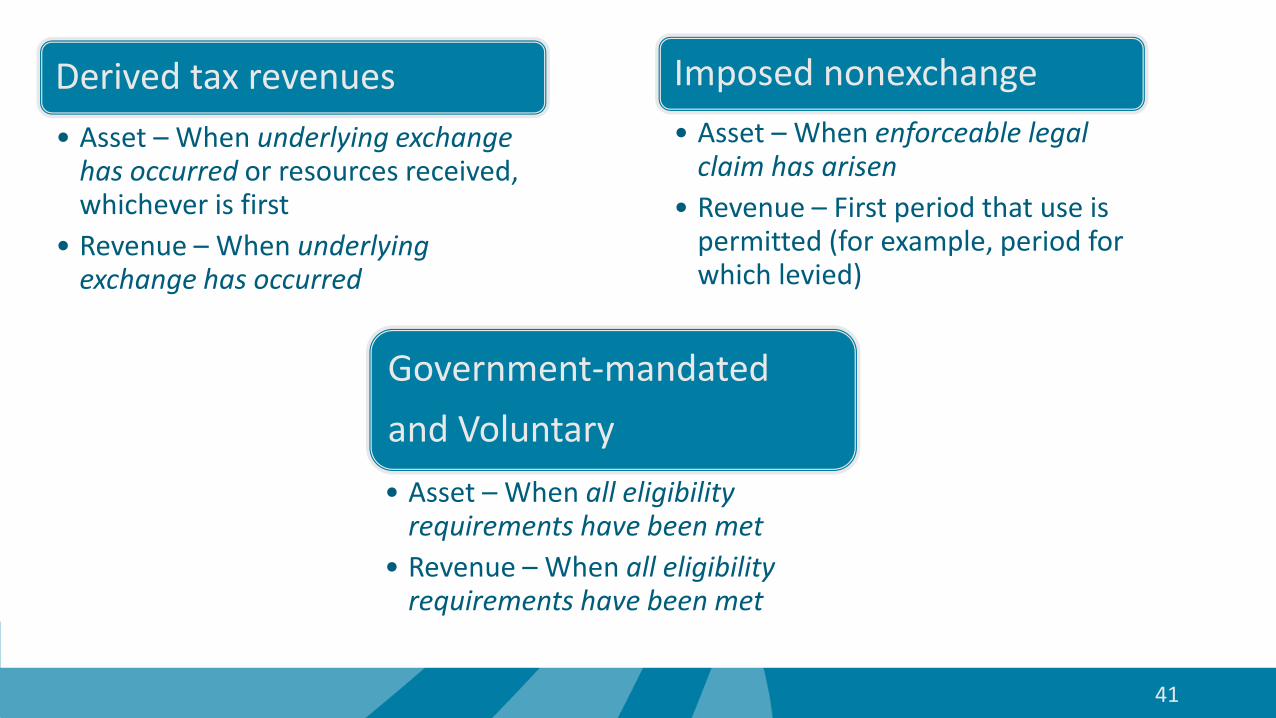

Derived tax revenues• Asset – When underlying exchange

has occurred or resources received, whichever is first

• Revenue – When underlying exchange has occurred

Imposed nonexchange• Asset – When enforceable legal

claim has arisen• Revenue – First period that use is

permitted (for example, period for which levied)

Government-mandatedand Voluntary• Asset – When all eligibility

requirements have been met• Revenue – When all eligibility

requirements have been met

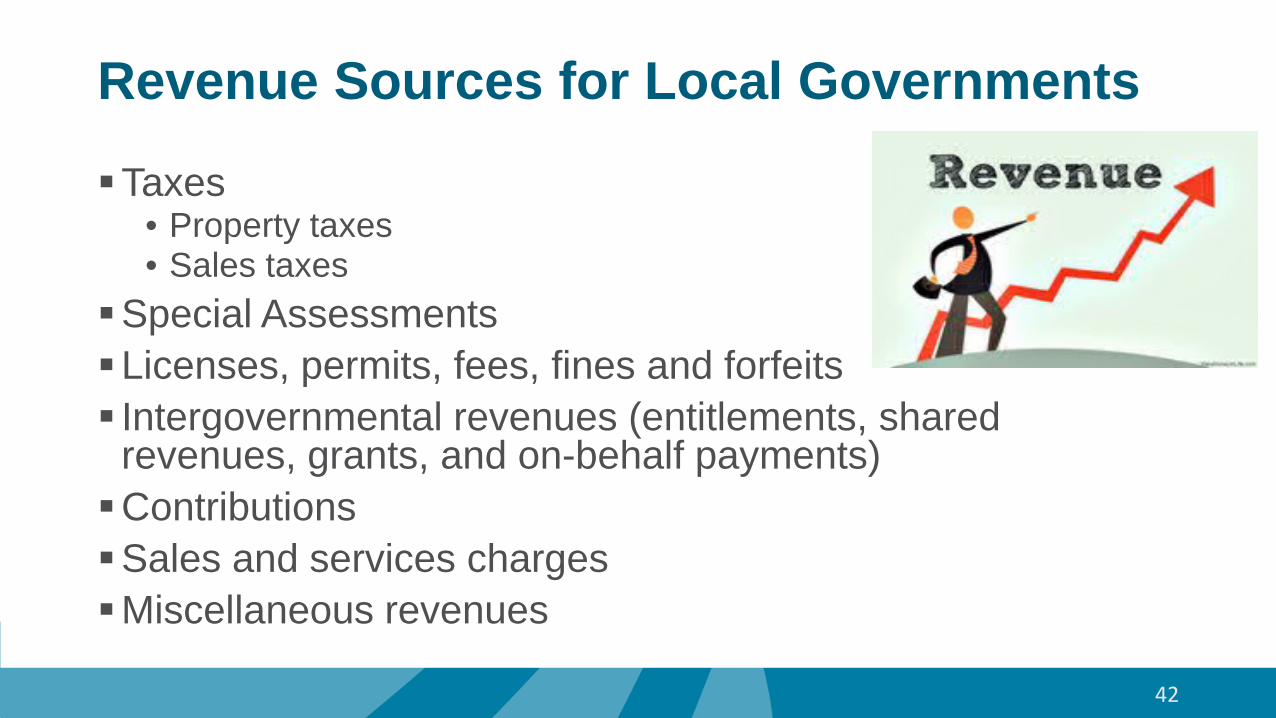

Revenue Sources for Local Governments

Taxes• Property taxes• Sales taxes

Special AssessmentsLicenses, permits, fees, fines and forfeits Intergovernmental revenues (entitlements, shared

revenues, grants, and on-behalf payments)ContributionsSales and services chargesMiscellaneous revenues

42

Property Taxes Imposed nonexchange revenueAlso called ad valorem taxesLevied on real (land, buildings) or

personal property (vehicles, machinery)Property is subject to a lienAllowances are generally minimal

43

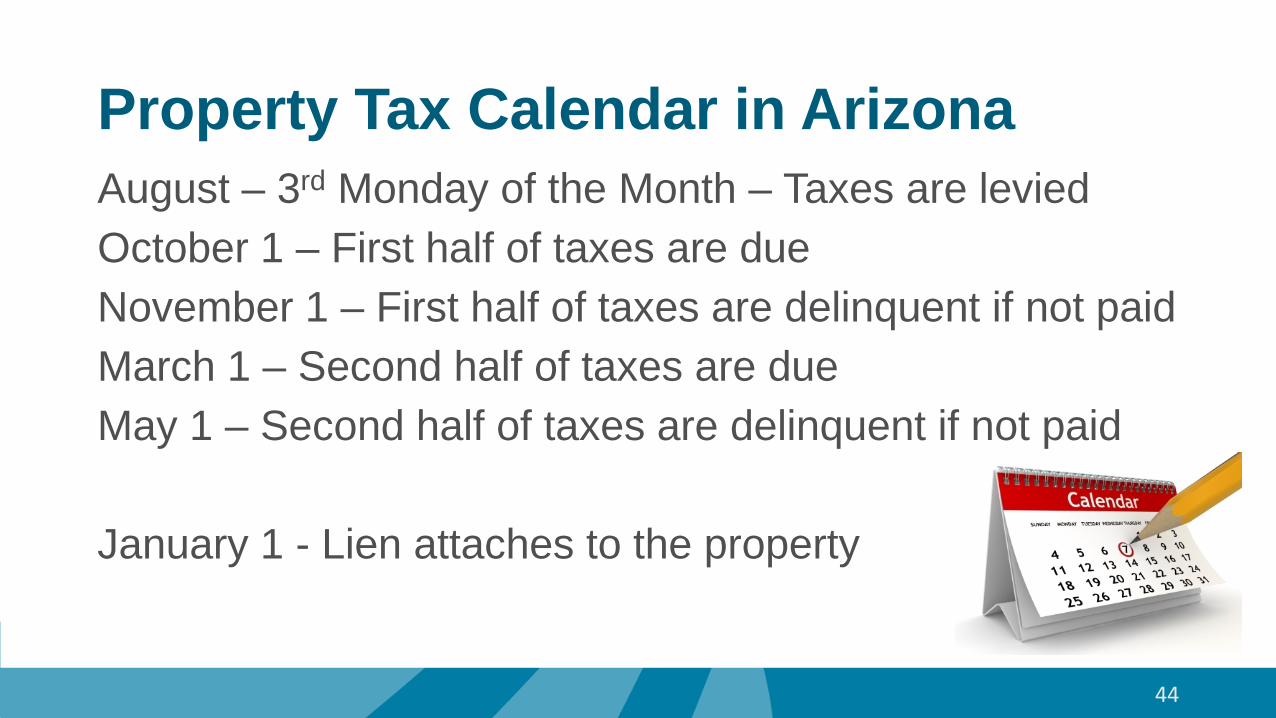

Property Tax Calendar in Arizona

44

August – 3rd Monday of the Month – Taxes are leviedOctober 1 – First half of taxes are dueNovember 1 – First half of taxes are delinquent if not paidMarch 1 – Second half of taxes are dueMay 1 – Second half of taxes are delinquent if not paid

January 1 - Lien attaches to the property

Accounting for Property TaxesModified Accrual basisReceivable should be recognized in the period for which

it is leviedRevenue recognized when levied provided they are also

availableGASB Cod. Sec. P70 defines availability period –

should not exceed 60 days after year-endReport deferred inflows for assets not received within

period of availability

45

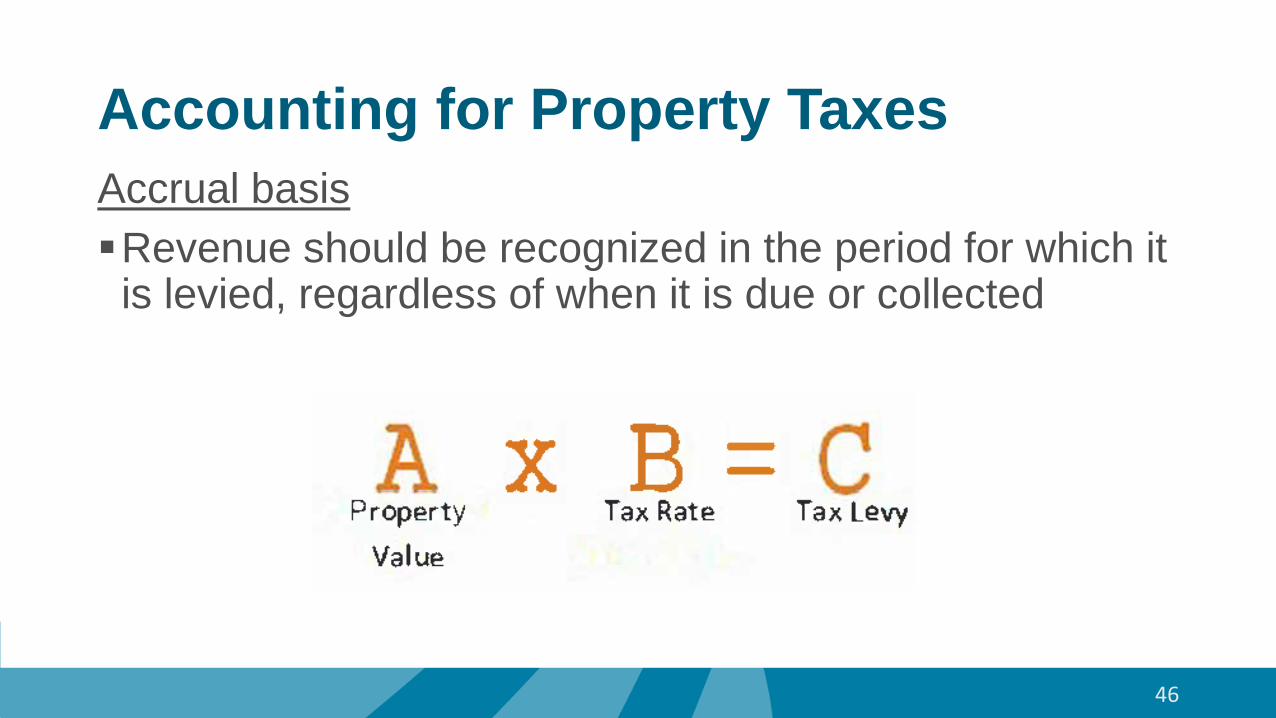

Accounting for Property TaxesAccrual basisRevenue should be recognized in the period for which it

is levied, regardless of when it is due or collected

46

Presentation of Property Taxes in the Financial StatementsGovernment-wide Financial Statements

• General Revenues

Proprietary Fund Financial Statements• Nonoperating Revenues

Governmental Fund Financial Statements• May be reported within Tax Revenues or broken out into a

separate line item.

47

Property Tax Financial Reporting Considerations1. Since property taxes are collected by the County,

there is a lag in receipt of the revenues.2. Receivable and unavailable should be reported for

revenues not received within the period of availability.3. Review receivable to ensure it is adjusted when the

County adjusts the levy.

48

Sales TaxesDerived: Imposed by government based

on underlying exchange transaction (such as sale of retail items)May be imposed on all good or services

sold (except those that are exempt) May be imposed on specific items (ex.

hotel occupancy)

49

Accounting for Sales TaxesModified Accrual basisShould be recognized when the underlying exchange

(sale of goods) takes place and the resources are availablePurpose restrictions do not affect revenue recognition,

but may require reporting in a specific fundReport revenues net of estimated refunds and

uncollectible amounts

50

Accounting for Sales TaxesAccrual basisShould be recognized when the underlying exchange

(sale of goods) takes place

51

Presentation of Sales Taxes in the Financial StatementsGovernment-wide Financial Statements

• General Revenues

Proprietary Fund Financial Statements• Nonoperating Revenues

Governmental Fund Financial Statements• May be reported within Tax Revenues or broken out into a

separate line item

52

Sales Tax Financial Reporting Considerations1. Receivable and unavailable should be reported for

revenues not received within the period of availability. This may require consultation with sales tax department regarding delinquent accounts/tax audits.

2. Review lag schedule of sales taxes receivable to determine if allowance is reasonable

53

Special AssessmentsService-type – Exchange Transactions

• Examples include: charges for street cleaning, snow removal, landscape maintenance

Capital – May be Exchange or Imposed Nonexchange• Improve or add infrastructure related to specific properties• Examples include: roads, sidewalks, curbs

54

Accounting for Service-Type Special AssessmentsModified Accrual basisReport revenue when the service is provided and

amounts are availableReport deferred inflows for revenues not received

during period of availability

55

Accounting for Service-Type Special AssessmentsAccrual basisReport revenue when the service is providedGASB Implementation Guide No 2015-1, Question

7.36.1, report with charges for services on Government-Wide Statements

56

Accounting for Capital Special AssessmentsModified Accrual basis If debt is issued and government is obligated in some

manner for the debt – record receivable and unavailable revenue/revenue If government is not obligated – no receivable is

recorded, activity is recorded in an agency fund If capital improvements are financed with existing funds

– record receivable and unavailable revenue/revenue in the fund that provided the resources

Recognize prepayments as revenue when collected

57

Accounting for CapitalSpecial AssessmentsGovernment-Wide ReportingWhen government is obligated: Recognize revenue

when the government has an enforceable legal claim When government is not obligated: Report a capital

contribution equal to the debt proceeds

58

Presentation of Special Assessments in the Financial StatementsGovernment-wide Financial Statements

• Capital Contributions

Proprietary Fund Financial Statements• Capital Contributions

Governmental Fund Financial Statements• Typically reported as a separate line item

59

Intergovernmental RevenuesGovernment mandated or voluntary nonexchange

transactions

Revenues should be recognized when all four types of eligibility requirements specified in GASBS No. 33

• Required characteristics of recipients• Time requirements• Reimbursements• Contingencies

60

Intergovernmental Revenue TypesShared Revenues

• Example – Highway User Revenues, State Shared Sales TaxEntitlement

• Payment based on an allocation formula Grants and Other Financial Assistance

• Usually restricted• Generally must be applied for• Example – federal grant for police equipment

61

Shared RevenuesConsidered continuing appropriations “once established, are automatically renewed without further legislative action, period after period, until altered or revoked”.

• The time eligibility is continuously (automatically) met and revenues are reported in the period in which the sales take place.

62

Accounting for Intergovernmental RevenuesModified accrualReport revenue when all eligibility requirements have

been met and amounts are availableReport unearned revenues for resources received prior

to meeting eligibility requirementsGASB No. 33 provides that governments should not

delay revenue recognition pending completion of purely routine requirements such as filing of claims for allowable costs for reimbursement-type grants

63

Accounting for Intergovernmental RevenuesAccrualReport revenue when all eligibility requirements have

been metReport unearned revenues for resources received prior

to meeting eligibility requirements

64

Presentation of Intergovernmental Revenues in the Financial StatementsGovernment-wide Financial Statements

• If restricted – Operating or Capital Grants• If not restricted - General Revenue

Proprietary Fund Financial Statements• Nonoperating Revenues

Governmental Fund Financial Statements• Typically reported as a separate line item and the various types of

intergovernmental revenues are broken out Taxes - Intergovernmental Federal Grants State Grants

65

Intergovernmental Revenue Financial Reporting Considerations1. Review receivables at year end to ensure all are

included even if the revenues did not come in by FYE or shortly thereafter• Unrecorded receivables have unfortunate side effects on

recognition of federal awards2. Investigate funds with deficit balances at fiscal year

end to ensure that no receivable exists.

66

Licenses, Permits, Fees, Fines and ForfeitsRevenue can be reported on the cash basis in the

governmental fund financial statementsTypically not a significant source of revenues

• Exception could be courtsFines – GASB Implementation Guide No. 2015-1

• Undisputed fines should be recognized when they are paid or when the statutory time allowed for dispute lapses, whichever occurs first.

67

Presentation of Licenses, Permits, Fines in the Financial StatementsGovernment-wide Financial Statements

• Charges for Services

Governmental Fund Financial Statements• Typically reported as a separate line item

68

ContributionsMost are voluntary nonexchange transactions

Revenues should be recognized when all eligibility requirements are met (and available in governmental funds)

69

Presentation of Contribution Revenues in the Financial StatementsGovernment-wide Financial Statements

• If restricted – Operating or Capital Grants• If not restricted - General Revenue

Proprietary Fund Financial Statements• Nonoperating Revenues

Governmental Fund Financial Statements• Either miscellaneous line item or separately classified as

contributions, gifts or donations

70

Sales and Service ChargesExchange TransactionsRecognize revenue when the exchange takes placeReport revenues net of discounts and allowancesPrimary source of revenue for proprietary fundsUnbilled services charges require accrual

71

GASB ProjectsFinancial Reporting Model

• Invitation to Comment issued December 2016• Presents potential improvements to recognition approaches

(measurement focus and basis of accounting)

Revenue and Expense Recognition• Currently in Initial Deliberations• Addresses exchange transactions not specifically addressed

in existing statements• Post-implementation review of Statements 33 and 36

72