Embed Size (px)

Citation preview

1

Presented by

M.Nageswara Rao Sr.SO(A)/S.C.Rly

Indian Rly. Administration & Finance Code- Para 510 (Financial Ratios)

The financial efficiency of operating an enterprise can best be seen from the ' financial ratios ' which are worked out

from the Statement of Profit and Loss for the year and the Balance Sheet (of Assets and Liabilities) as at the end of the year.

The glossary of terms which should be used in Railway Estimates and Financial

statements is given in Para 308-F.

Indian Rly. Administration & Finance Code- Para 511 (Financial Ratios)

(a) Operating Ratio, i.e., percentage of gross working expenses (item (xiii) of Para 308-F.) to gross earnings (item

(v) of Para 308-F).

b) Return on Capital (i) percentage of (revenue) surplus (item xxi of para 308-F)

to Capital-at-charge (item xxii of para 308-F).(ii) percentage of net receipts (item xix of para 308-F) to

Capital-at-charge. c) Current Assets/Liabilities - (j) Stores in stock in terms of month's consumption,

(ii) work-in-process (workshops) as a percentage of the value of workshop outturn.

(iii) stores inventory (stores, ' purchases', 'sales', and miscellaneous advance- capital, etc.,) as percentage of the total issue of stores.

(iv) Unrealised earnings at the year-end in terms of number of days, earnings.

Operating Ratio

It is regarded as one of the Most Important financial statistics/ratios.

frequently been used as an Index of the operating efficiency of the Railways.

Operating Ratio – Definition (Para 434 of Finance code vol.I)

Percentage of Gross Working Expenses to Gross Earnings of any accounting year.

There is no ideal Operating Ratio for Indian Railways. In rail road sector, an operating ratio

of 80 % or lower is considered desirable

Advantage of better O.R

However lower O.R. helps in generating internal resources for meeting requirement of Plan Expenditure on Safety (RSF), Amenities to Passengers & Staff (D.F) and other Capital investments such as laying of new lines,

acquisition of Rolling Stock etc (Capital Fund).

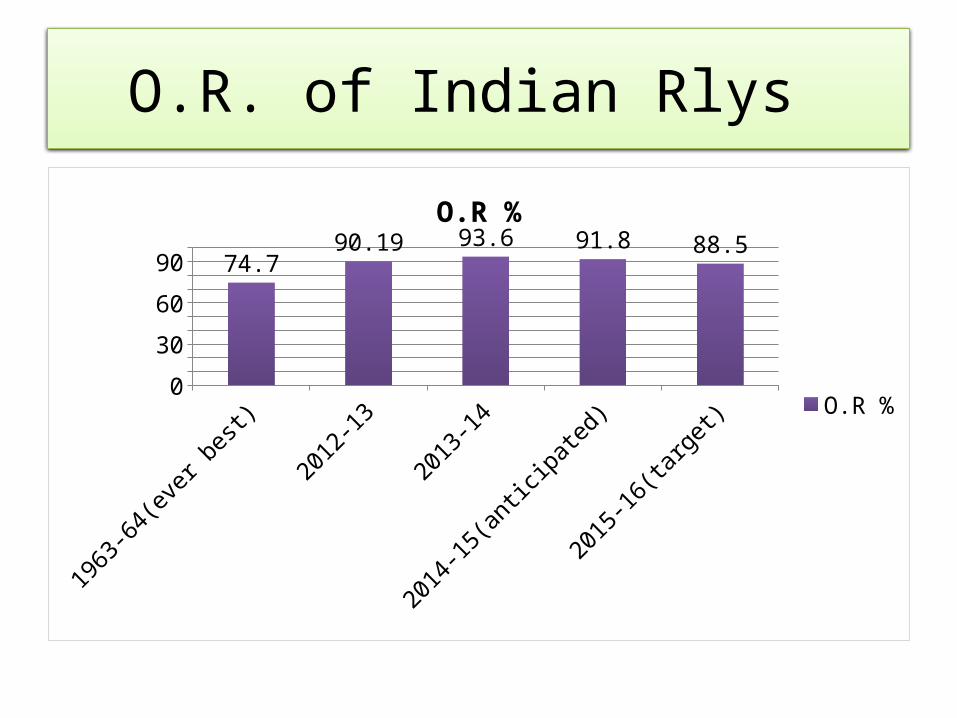

The Best ever O.R of Indian Railways was 74.7 % in 1963-64.

O.R. of Indian Rlys

1963-64(ever b

est)

2012-13

2013-14

2014-15(anticip

ated)

2015-16(targe

t)0

20

40

60

80

100

74.790.19 93.6 91.8 88.5

O.R %

O.R %

Comparing OR of I.Rly with other countries Rly. systems

Not possible due to different computation methodologies across

different countries thus reducing validity of comparison of such

statistical figures.

In the year 2005, Indian Railways, changed its accounting policy for the lease charges paid to IRFC. The lease charges have been broken into two parts – Principal part(capital) and Interest part (revenue).

This move has resulted in reduction of Working expenses from 2005 year onwards

Lease charges payable to IRFC

Principal component

New Plan Head 2200 – Leased

Assets

Interest Component

Revenue Demand No.

09 G

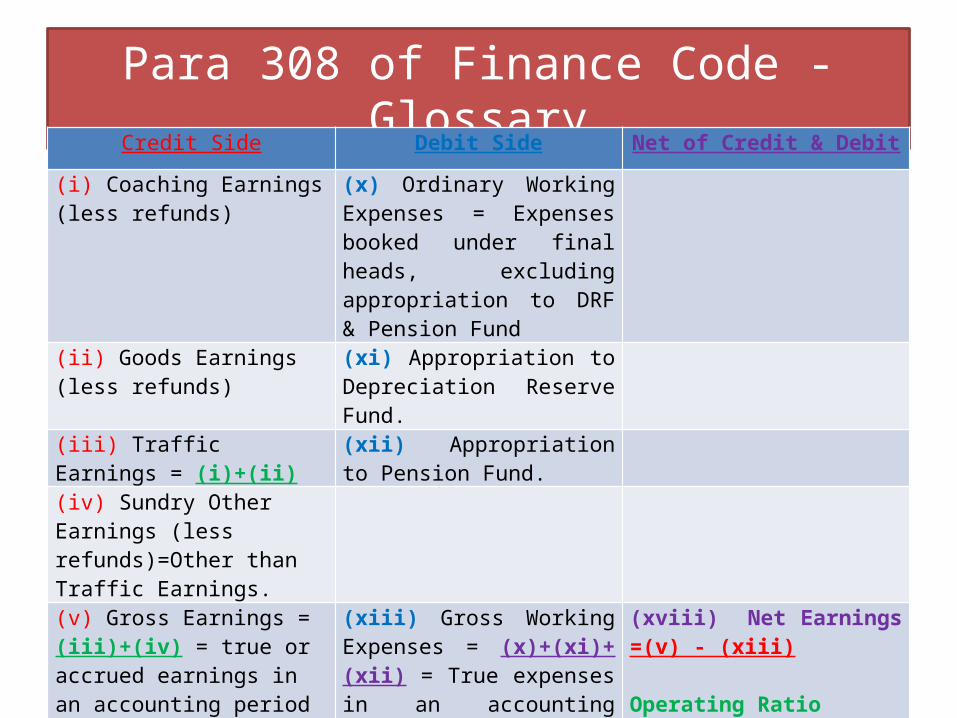

Para 308 of Finance Code - GlossaryCredit Side Debit Side Net of Credit & Debit

(i) Coaching Earnings (less refunds)

(x) Ordinary Working Expenses = Expenses booked under final heads, excluding appropriation to DRF & Pension Fund

(ii) Goods Earnings (less refunds)

(xi) Appropriation to Depreciation Reserve Fund.

(iii) Traffic Earnings = (i)+(ii)

(xii) Appropriation to Pension Fund.

(iv) Sundry Other Earnings (less refunds)=Other than Traffic Earnings.

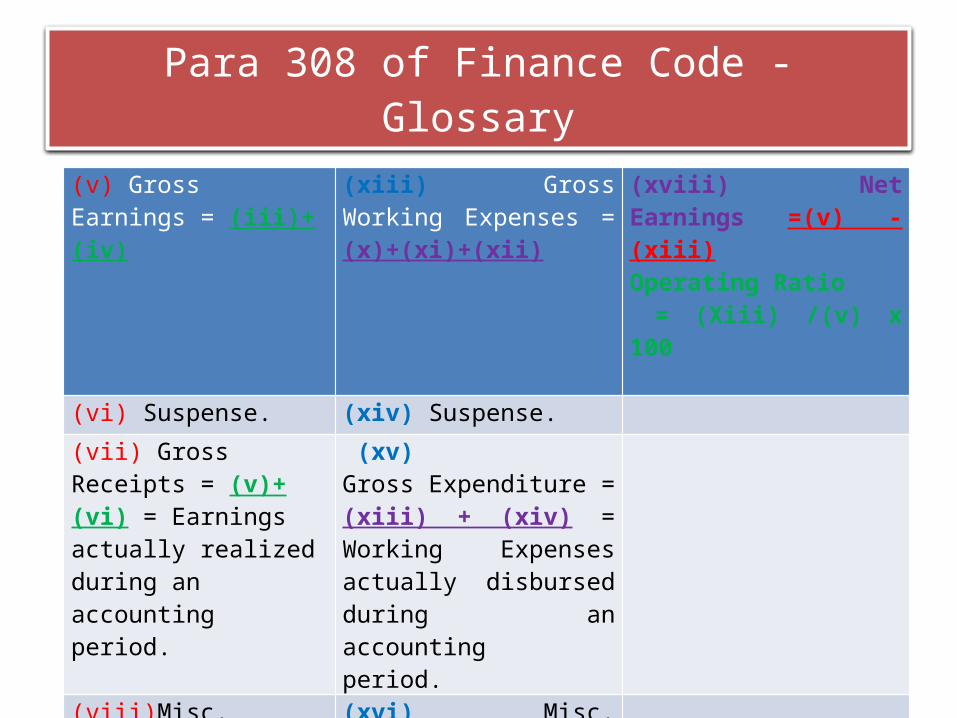

(v) Gross Earnings = (iii)+(iv) = true or accrued earnings in an accounting period whether or not actually realized.

(xiii) Gross Working Expenses = (x)+(xi)+(xii) = True expenses in an accounting period whether or not actually disbursed.

(xviii) Net Earnings =(v) - (xiii) Operating Ratio = (Xiii) /(v) x 100

Para 308 of Finance Code - Glossary

(v) Gross Earnings = (iii)+(iv)

(xiii) Gross Working Expenses = (x)+(xi)+(xii)

(xviii) Net Earnings =(v) - (xiii)Operating Ratio = (Xiii) /(v) x 100

(vi) Suspense. (xiv) Suspense.

(vii) Gross Receipts = (v)+(vi) = Earnings actually realized during an accounting period.

(xv) Gross Expenditure = (xiii) + (xiv) = Working Expenses actually disbursed during an accounting period.

(viii)Misc. Receipts (xvi) Misc. expenditure

(ix) Total Revenue Receipts = (vii)+(viii).

(xvii) Total Revenue Expenditure = (xv)+(xvi).

(xix) Net Receipts or Net Revenue = (ix) - (xvii).

Para 308 of Finance Code - Glossary

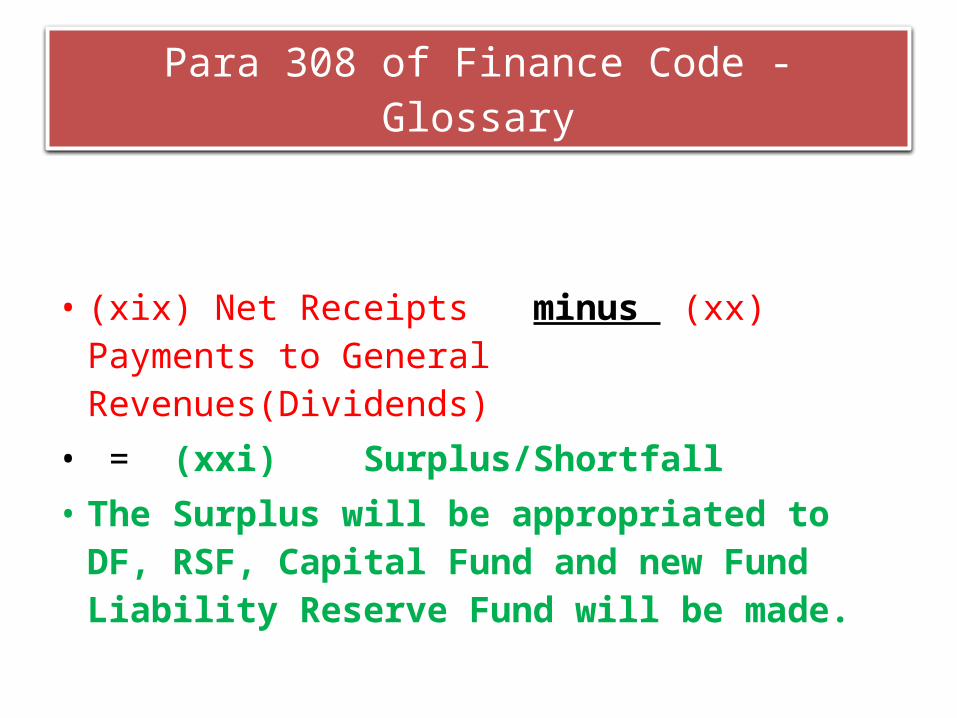

• (xix) Net Receipts minus (xx) Payments to General Revenues(Dividends)

• = (xxi) Surplus/Shortfall• The Surplus will be appropriated to DF, RSF,

Capital Fund and new Fund Liability Reserve Fund will be made.

O.R - Formulae

GWE - Gross Working Expenses---------------------------------------------- x100

Gross Earnings

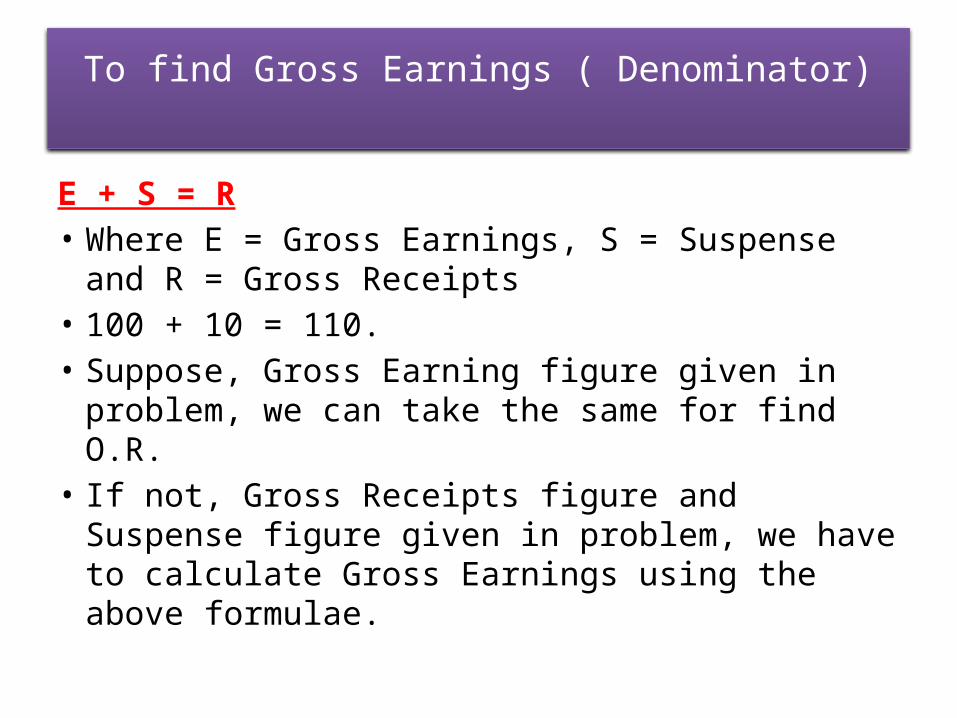

To find Gross Earnings ( Denominator)

E + S = R• Where E = Gross Earnings, S = Suspense and R =

Gross Receipts• 100 + 10 = 110.• Suppose, Gross Earning figure given in problem,

we can take the same for find O.R.• If not, Gross Receipts figure and Suspense figure

given in problem, we have to calculate Gross Earnings using the above formulae.

To find Gross Working Expenses (Numerator)

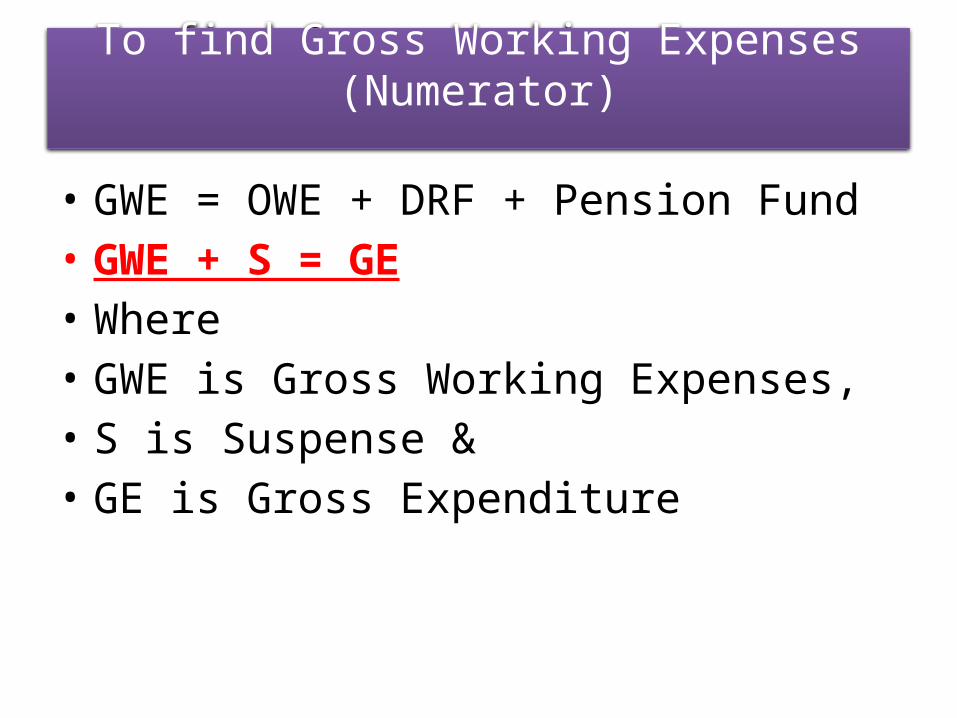

• GWE = OWE + DRF + Pension Fund• GWE + S = GE• Where • GWE is Gross Working Expenses, • S is Suspense & • GE is Gross Expenditure

O.R. - PracticalsDetails Amount(Rs.)

Gross Receipts 900Suspense (Earnings) 100

OWE 450Suspense (expenditure) 50

Appropriation to DRF 40Appropriation to Pension Fund 70Appropriation to Development Fund 100

Find the Operating Ratio

Finding Gross Earnings ( Denominator)

• Using formulae E + S = R,

• E + 100 = 900• E = 900-100• E = 800

Finding Gross Working Expenses ( Numerator)

• GWE = OWE + DRF + Pension Fund• GWE = 450 +40 +70 = 560• Hence GWE figure(numerator) is available,

there is no reason to apply formulae i.e., GWE + S = GE.

• Suspense – 50 is irrelevant for computation of GWE

• So O.R = 560/800 X 100 = 70 %

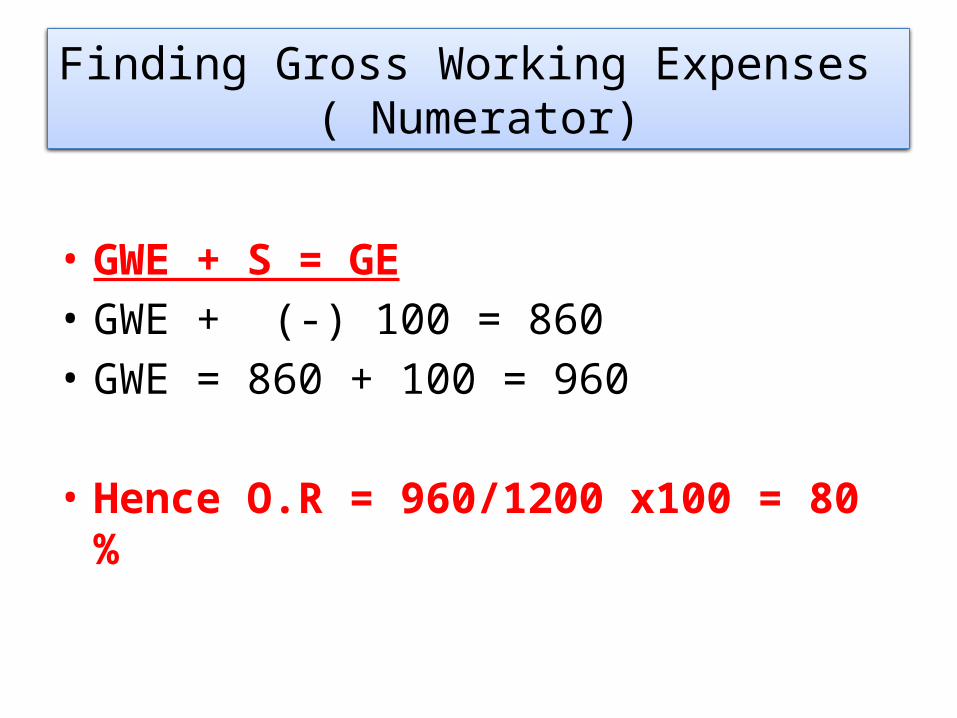

O.R. - PracticalsDetails Amount(Rs.)

Gross Earnings 1200Suspense (Earnings) (-) 100Gross Expenditure 860

Suspense (expenditure) (-) 100Appropriation to DRF 40

Appropriation to Pension Fund 80Misc. Receipts 50

Find the Operating Ratio

Finding Gross Earnings ( Denominator)

• Gross Earnings Figure -1200 given in problem itself. Here suspense - (-) 100 is irrelevant and ignored the same for calculation of O.R.

Finding Gross Working Expenses ( Numerator)

• GWE + S = GE• GWE + (-) 100 = 860• GWE = 860 + 100 = 960

• Hence O.R = 960/1200 x100 = 80 %

Saturday, April 15, 2023 25