Embed Size (px)

Citation preview

www.medtecheurope.org 1

Yves Verboven

Director, Market Access & Economic Policies

Procurement, “the” cornerstone to access to novel Medical Technology in Europe.

www.medtecheurope.org 2

MedTech Industry Association

Alliance

Medical Devices

In-Vitro Diagnostics

MedTech Europe

3

THE EUROPEAN MEDTECH

INDUSTRY IN FIGURES

2014

www.medtecheurope.org

European MedTech Imports, Exports & Trade balance

www.medtecheurope.org 6

Medical devices and Imaging excluding in-vitro diagnostics. Europe refers to EU (excluding Cyprus, Luxembourg, Malta) +

Norway, Switzerland.

Data related to total exports and total imports include EU intra-trade. Trade balance refers to external trade balance.

Source: Espicom, Eucomed calculations.

6.0 7.1 8.0 7.3

13.2 14.6 15.8 15.2

55

58

63 64

74

78

84 80

49 51

55 57 61

64

68 65

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

2006 2007 2008 2009 2010 2011 2012 2013

bill

ion

EU

R

Trade balance

Exports

Imports

Employment comparison

www.medtecheurope.org 7

575,000

520,000

675,000

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

European MedTech industry US MedTech industry European pharmaceuticalindustry

num

ber

of people

em

plo

yed

Europe refers to EU + Norway, Switzerland. Latest year available.

Source: Eurostat, Eucomed calculations based on the data obtained from National Associations of 15 countries. Countries with

(partially) provided data: Belgium, Czech Republic, Denmark, France, Germany, Greece, Ireland, Italy, Netherlands, Poland,

Portugal, Spain, Sweden, UK, Switzerland.

EFPIA – The Pharmaceutical Industry in Figures. Key Data 2013.

S. Tripp, M. Grueber, R. Helwig - The Economic Impact of the U.S. Advanced Medical Technology Industry, Battelle Technology

Partnership Practice, March 2012.

Number of people employed in the MedTech industry

per 10,000 inhabitants

www.medtecheurope.org 8

Source: Eurostat, Eucomed calculations based on the data obtained from National Associations.

USA data source: S. Tripp, M. Grueber, R. Helwig - The Economic Impact of the U.S. Advanced Medical Technology Industry,

Battelle Technology Partnership Practice, March 2012.

Trade

Europe’s MedTech trade surplus in 2013 is estimated at €15 billion,

more than a twofold increase since 2006.

Countries with the highest trade surplus* are Germany, Ireland and Switzerland

www.medtecheurope.org 9

*including EU intra-trade

Medical technology excluding in vitro diagnostics. Europe refers to EU (excluding Cyprus, Luxembourg, Malta) + Norway, Switzerland.

Source: Espicom, Eucomed calculations.

MEDTECH

www.medtecheurope.org

www.medtecheurope.org 11

MedTech Industry - A Diverse Sector

There are more than 500,000 medical technologies registered ,

ranging from syringes, bandages, In-vitro diagnostics to eye

implants and artificial limbs (20,000 generic groups)

Source: Global Medical Devices Nomenclature (GMDN) Agency, 2010 www.medtecheurope.org

Diversity and classification of medical technology

www.medtecheurope.org 13

1The classification of medical devices is a ‘risk based’ system based on the vulnerability of the human body taking account of the

potential risks associated with the devices. The classification rules are based on different criteria such as the duration of contact with the

patient, the degree of invasiveness and the part of the body affected by the use of the device. 2IVD classification is based on the degree of health risk posed to an individual and public, and is related to the risk of an incorrect result

arising from the use of the IVD.

Source: European Commission.

Medical technology market estimates by area and sales growth

www.medtecheurope.org 14

World, 2013-2020

Source: World Preview 2013, Outlook to 2018: The Future of Medtech, EvaluateMedTech™, September 2013.

INNOVATION

www.medtecheurope.org

Top technical fields in patent applications

www.medtecheurope.org 16

Analysis based on European patent applications filed with the EPO in 2013 (Direct European applications filed in 2013 and

International (PCT) applications entering the European phase in 2013), including divisional applications filed during the year.

Based on the WIPO IPC-Technology concordance as revised in January 2013.

Source: European Patent Office

Number of patent applications filed, by field, 2013

41%

39%

20%

Evolution of European patent applications by technical field

2004-2013

www.medtecheurope.org 17

Analysis based on European patent applications filed with the EPO from 2004 to 2013 (Direct European applications filed and

International (PCT) applications entering the European phase in these years), including divisional applications filed during the year.

Based on the WIPO IPC-Technology concordance as revised in January 2013.

Source: European Patent Office

0

2 000

4 000

6 000

8 000

10 000

12 000

Nu

mb

er

of p

ate

nt a

pp

lica

tion

s f

iled w

ith

EP

O

Medical technology Pharmaceuticals Biotechnology

MedTech Companies in Europe

almost 25,000 medical technology companies

www.medtecheurope.org 18

Europe refers to EU + Norway, Switzerland. An enterprise is considered to be an SME if it employs fewer than 250 persons and has

an annual turnover not exceeding €50 million.

Source: Eucomed calculations based on the data obtained from National Associations of 15 countries for the latest year available.

Countries with (partially) provided data: Belgium, Czech Republic, Denmark, France, Germany, Greece, Ireland, Italy, Netherlands,

Poland, Portugal, Spain, Sweden, UK, Switzerland.

European MedTech market

Is estimated at roughly

www.medtecheurope.org 19

Europe refers to EU + Norway, Switzerland. Market size refers to the total annual value of products sold in Europe in the final

purchaser’s prices, i.e. the total amount spent from public and private sources on medical technology.

Source: WHO Global Health Expenditure Database, Eurostat, Eucomed calculations based on the data obtained from National

Associations of 15 countries for the latest year available. Countries with (partially) provided data: Belgium, Czech Republic,

Denmark, France, Germany, Greece, Ireland, Italy, Netherlands, Poland, Portugal, Spain, Sweden, UK, Switzerland.

Breakdown of total healthcare expenditure in Europe

www.medtecheurope.org 20

Europe refers to EU + Switzerland, Norway. MedTech data – latest year available, healthcare expenditure data – 2010.

Source: WHO, Eurostat, EFPIA, EDMA, Eucomed calculations.

Per capita investment in various fields in Europe

in EUR, latest year available

www.medtecheurope.org 21

Weighted European average. Europe refers to EU + Norway, Switzerland.

Source: WHO Global Health Expenditure Database, Eurostat, Eucomed calculations based on the data obtained from National

Associations.

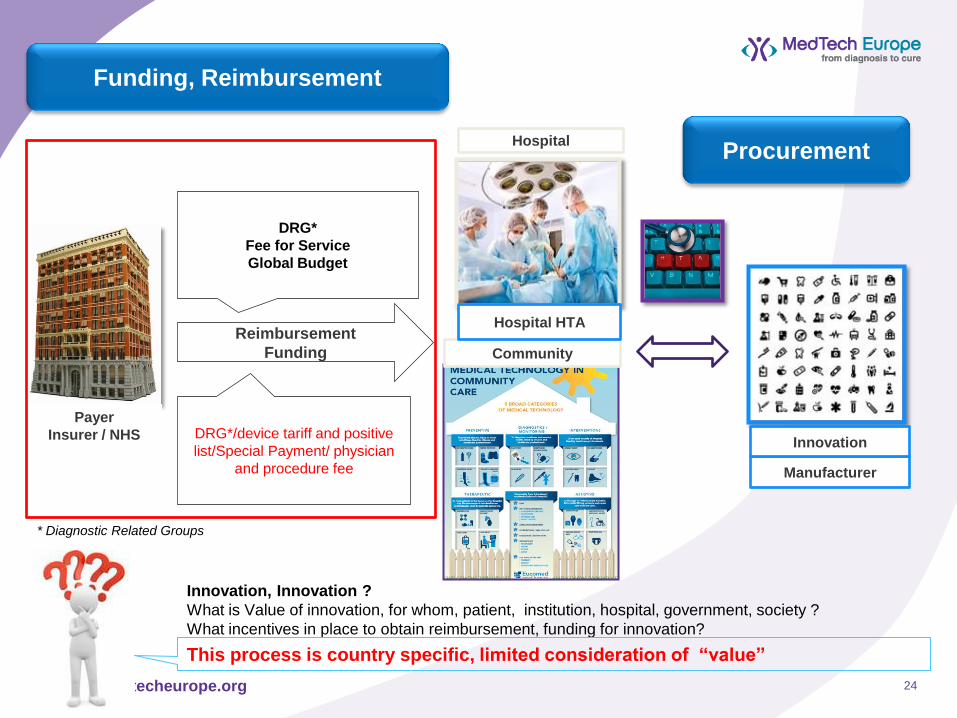

Market Access Model

www.medtecheurope.org 23

PROCUREMENT

FIRST ENTRY POINT

TO MARKET

Estimated

70% procured

www.medtecheurope.org 24

Hospital

Reimbursement

Funding

DRG*

Fee for Service

Global Budget

Innovation, Innovation ?

What is Value of innovation, for whom, patient, institution, hospital, government, society ?

What incentives in place to obtain reimbursement, funding for innovation?

This process is country specific, limited consideration of “value”

Payer

Insurer / NHS DRG*/device tariff and positive

list/Special Payment/ physician

and procedure fee Manufacturer

Innovation

Funding, Reimbursement

Community

* Diagnostic Related Groups

Procurement

Hospital HTA

Procurement of medtech innovations

Impact of procurement in the EU on the innovation

strength of the medical technology sector

Joint study, University of Twente and Simon-Kucher &

Partners commissioned by Eucomed

innovations are differentiated according to three key dimensions

Definitions

Number of substitutes

Signifies a market/product category dimension

Number of interchangeable products in the market

Level of clinician influence

Signifies a stakeholder dimension

Degree of influence of clinicians on product selection

and procurement

Influence depends on the therapeutic specialty, the

unmet need and the perceived improvement of

patient outcomes

Product conformity

Signifies a process dimension

High product conformity, i.e. fit with existing

procurement processes and demand specifications

Low product conformity, i.e. requires time and effort to

learn and process/specification adaptations and

developments on the procurement side

Low

Leve

l o

f c

lin

icia

n in

flu

en

ce

High

Low

Innovation classification cube

61 interviews with procurement bodies and industry reps were held and

systematic literature research was done

Source: Simon-Kucher & Partners; *Spain was excluded due to major changes in the healthcare system and a strong focus on cost reductions, Switzerland as a non-EU country

was included due to market relevance

30 interviews with:

Regional procurement bodies

GPOs

Individual (university) hospitals

Countries* and procurement

bodies

Sweden

Switzerland

Austria Czech Rep

Netherlands

UK

France

Poland

Italy Germany

31 interviews with:

Major medical device

companies

SMEs

Eucomed SME expert

Medtech industry

representatives

Scopus and Pubmed

databases

General studies on

procurement centralization

Product specific procurement

studies for selected products

Cost-effectiveness studies for

selected studies

Systematic literature research

A total of 11 medtech case studies were selected and analyzed which

covered all areas of the innovation classification cube

High Number of substitutes

Leve

l o

f c

lin

icia

n in

flu

en

ce

Low product conformity

High product conformity

High

1

4

11

9

8

7

10b 2a 2b

2c 3 6

Low

1 Customized OR procedure trays

2 Drug-eluting

stents

a) 1st generation

b) 2nd generation

c) 3rd generation

3 Endoprosthetics – Mobile-bearing knee

implants

4 High-end radiology equipment

5 Incontinence pants

6 Insulin pumps with CGM

7 Integrated patient monitoring systems

8 Negative pressure wound therapy

9 Safety medical devices

10 Spinal

implants

a) Cervical plates

b) Artificial disc replacement

11 Transcatheter aortic valve implantation

10a

5

Low

Mo

de

rate

Innovation classification “cube”*

Innovations

Hypotheses

DES 3rd generation

Endoprosthetics: MB knee implants*

Spinal implants: Cervical plates

High-end radiology equipment --

Customized OR procedure trays ()

Incontinence pants ()

Integrated patient monitoring systems ()

Safety medical devices ()

DES 1st / 2nd generation -- / ** -- / **

Insulin pumps with CGM

Negative pressure wound therapy

Spinal implants: Artificial disc replacement -- --

Transcatheter aortic valve implants --*** --***

Case study analysis reveals that the impact of procurement varies

29

*Latest generation **1st gen: not applicable, 2nd gen: no impact ***Predominantly not purchased through centralized/coop. procurement

Confirmed () Partly confirmed Not confirmed -- No exposure to PC

Group 1:

impact

Group 2:

Impact

depends

Group 3:

No

exposure

Increasing

procurement

centralization

Reduced short-

term price level

Reduced

innovation

adoption

Increasing

procurement

centralization

Reduced

innovation

adoption

implications of Procurement on adoption and price

level of product categories were assessed

Source: Simon-Kucher & Partners

Subject

to PC? Insights and impact

Drug-eluting

stents 3rd

generation

Procurement centralization of DES started in 2004/2005

This and other factors such as increasing competition and a study revealing

potential safety issues of DES in 2007, drove price erosion in the DES market

Today, 2nd-generation products are often considered “sufficient”. Centralized and

cooperative procurement bodies often use them as their standard products

In addition, PC’s strong focus on price leads to further price erosion and limited

opportunities to achieve price premiums for next-generation products

Endopros-

thetics: MB

knee implants

PC of mobile-bearing knee implants started in ~2002

PC drove price erosion of fixed-bearing implants and made it impossible to sustain

a price premium for mobile bearing implants, despite regular launch of new

products/next-generation products

This has led to reduced adoption of next-generation MB implants priced at a

premium over FB implants

Spinal

implants:

Cervical plates

PC of cervical plates started in ~2002/2003

Today, PC limits adoption and price potential of next-generation cervical plates due

to strong demand standardization

High-end

radiology

equipment ~

High-end equipment not yet in the focus of centralized procurement

PC (among other factors such as increasing competition) drives price erosion in

low- to mid-end radiology equipment thereby increasing the price differential to

high-end equipment

This affects adoption of high-end equipment indirectly as price premiums vs. low-

to mid-end equipment can get prohibitively high

yes ~ to limited extent no

Expenditure on MedTech

It is estimated that only around 7.5 % of

total European healthcare expenditure

is attributed to MedTech.

Procurement - >

Price only not the solution as MedTech not “the” cost-driver

www.medtecheurope.org 31

Source: WHO, Eurostat, EFPIA, EDMA, Eucomed calculations,

EU Semester – FISCAL STABILITY

www.medtecheurope.org 32

Source: European Commission

5.4 6.0

7.3

2.4

6.0

4.9

1.8

4.1

3.3

4.1 3.9 3.5

4.7

2.2

7.1

2.0

4.0

1.5

6.9

2.1

3.4 4.0

5.6

11.2

7.3

3.3

8.6

7.4

3.4

-11.6

-4.4

-6.5

-2.8

-4.6

-0.8

1.0

-0.1

-2.3

-0.6

-2.3

-1.0 -0.5

0.5 0.4

2.4

0.1

2.1

-3.7

0.7 1.3

0.5

2.6 2.4

-5.0

2.9

4.5

5.9

4.8

-11.0

-0.6

1.7

-1.4

0.9

-2.7

-4.1

-1.5

0.8

-0.7

1.3 0.6

0.1

-0.7 -0.4

-1.3

1.3

-0.6

5.2

0.9 0.5

1.4

-0.6

0.2

8.1

2.0

0.6 0.2

4.0

-12.0

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2000-2009 2010 2011

Austerity

www.medtecheurope.org 33

Annual average growth rate in health expenditure per capita, in real terms, 2000 to 2011

Source: WHO Global Health Expenditure Database, Eurostat, Eucomed calculations.

A changing environment ….

Non Communicable – Chronic Disease

Ageing

Demographic

Austerity – reduced per capita

Or Healthcare System Reform

And Investment in Health, in Medtech

Ageing … Other factors Public healthcare expenditure projections

35

AWG - Ageing Working Group of Economic Policy Committee

Source: European Commission, The 2012 Ageing Report Economic and budgetary projections for the 27 EU Member States (2010-2060)

www.medtecheurope.org

8.3%

8.9%

The burden of chronic diseases in Europe

www.medtecheurope.org 36

Source: European Chronic Disease Alliance

Demographics Driving Demand for Healthcare

www.medtecheurope.org

1.7

1.8

1.8

2.2

1.7

2.3

2.1

2.0

1,9

2.1

1.7

2.3

1.5

1.8

2.4

1.8

1.7

1.7

1.8 2.1

1.8

1.8

1.5

2.2

1.5

2.1

2.7

1.6

3.2

3.2

3.5

3.6

3.7

3.8

3.8

3.8

3.8

3.9

3.9

4.0

4.0

4.0

4.0

4.0

4.1

4.2

4.3

4.3

4.6

4.6

4.7

4.9

5.3

5.3

5.8

5.9

0.0 2.0 4.0 6.0

Germany

Italy

Greece

Sweden

Portugal

Belgium

Finland

Austria

EU27

France

Bulgaria

Denmark

Latvia

Estonia

UK

Spain

Hungary

Slovenia

Lithuania

Netherlands

Czech Republik

Malta

Romania

Luxembourg

Poland

Cyprus

Ireland

Slovakia

2060 ← 2010

2060

Difference 2010-2060

Weighted EU average.

Source: European Commission Services, Eurostat, EUROPOP2010.

Old age support ratio 2010 and 2060 (projections):

Number of people working age (15-64)

per person of pension age (65+)

Economic Growth Health Care Expenditure

Evolution of GDP vs. HC expenditure - EU28, 1995-2011

www.medtecheurope.org 38

Source: WHO Global Health Expenditure Database, Eurostat, Eucomed calculations

1.0

1.2

1.4

1.6

1.8

2.0

2.2

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

index

Healthcareexpenditure

GDP8.8%

10.4%

% - the percentage of

GDP spent on healthcare

.

www.medtecheurope.org 39

More sustainable health system

Health as human capital

Reducing Inequalities

COST -> ”INVESTING IN HEALTH”

Health a Value in itself

Health a pre-requisite for economic growth

Improving cost efficiency and reconciling fiscal consolidation targets with

the continued provision of sufficient levels of public services

improving the health of the population in general and reinforcing

employability, thus making active employment policies more effective,

helping to secure adequate livelihoods and contributing to growth.

contributing to social cohesion and breaking the vicious spiral of

poor health contributing to, and resulting from, poverty and

exclusion.

EU Public Health Strategy

40

MEDTECH – TIME TO CHANGE HOW TO DO BUSINESS

www.medtecheurope.org

CONTRACT FOR A

HEALTHY FUTURE

www.medtecheurope.org 41

M

The role of medical technology in steering

healthcare system onto a sustainable path

5 year Strategy

1 - Build and engage stakeholder networks to collectively

establish the opportunity and value of medical technology

and innovation

2 - Collect, develop and share, evidence-based cases of

medical technology supporting effective personalised care, a

sustainable healthcare system and healthy ageing

3 - – Demonstrate cost-effectiveness incl. cost-

containment, Tx lifelong cost-saving, lifecycle cost

(product), and the (socio-)economic value for patient,

healthcare system and society of medical technology,

while improving healt and economic outcomes and quality of

care

4 – Enable care processes to address labour shortages

HEALTH ECONOMIC

VALUE

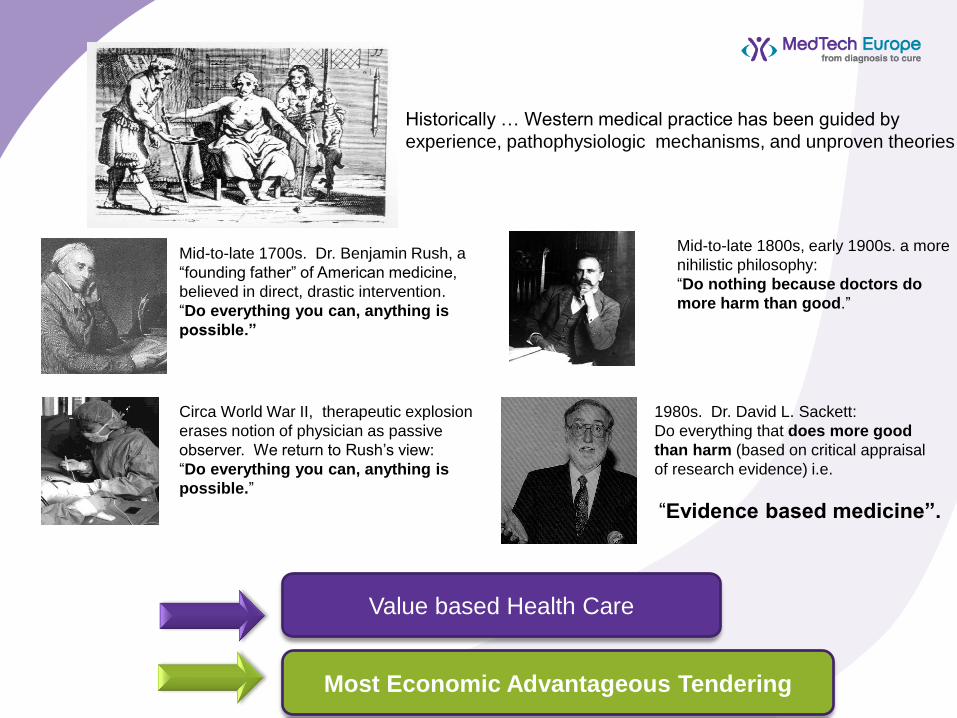

Mid-to-late 1700s. Dr. Benjamin Rush, a

“founding father” of American medicine,

believed in direct, drastic intervention.

“Do everything you can, anything is

possible.”

Mid-to-late 1800s, early 1900s. a more

nihilistic philosophy:

“Do nothing because doctors do

more harm than good.”

Circa World War II, therapeutic explosion

erases notion of physician as passive

observer. We return to Rush’s view:

“Do everything you can, anything is

possible.”

1980s. Dr. David L. Sackett:

Do everything that does more good

than harm (based on critical appraisal

of research evidence) i.e.

“Evidence based medicine”.

Historically … Western medical practice has been guided by

experience, pathophysiologic mechanisms, and unproven theories

Most Economic Advantageous Tendering

Value based Health Care

www.medtecheurope.org 43

Cost - Containment

• Avoid disease progression

• Avoid hospitalizations

• Avoid disease

• Avoid complication

• Avoid waste

• Avoid costly set-up of Tx

• Optimize most costly resources

• Product life-cycle cost

• Offer Procurement Innovation –

“Solutions”

• => “ Bleu Economy “

European Semester

the growing importance of health care and long-term care

The CSRs are related to the need to improve the fiscal sustainability of healthcare and/or long-term care systems:

BE, DE, ES, FR, MT, NL, AT, PL, PT, SI, SK;

…the need to increase their (cost-)efficiency and/or (cost-)effectiveness:

BE, BG, CZ, DE, IE, ES, HR, LV, MT, AT, PL, PT, RO, SK, FI ;

…and more specific recommendations in the areas of…

44

6

15

19

15

7

2012 2013 2014 Healthcare

Long-termcare

Graph, Table: Number of EU Member

States with country-specific

recommendations in

healthcare/long-term care

Enable Reforms

VALUE OF INVESTING IN MEDTECH

Healthcare systems

Efficient & effective

contribute to fiscal

stability and “Bleu

Economy

“Economic”

Advantageous

Patient’s/ Citizen

Income reduces

inequality

(wealth <-> health)

(Economic Growth)

Silver Economy

(Economic Growth)

Productivity

(workforce, carers)

( Economic Growth)

Public Procurement : From Cost to Value & Investment

www.medtecheurope.org 46

Tender preparation : Preliminary Market Consultation, Prior

involvement of candidates or tenderers, labels

Flexible procedures : Choice of procedures, Open

procedure, competitive procedure with negotiation,

competitive dialogue, innovation partnership

Art. 67: Contract Award Criteria

Most Economic Advantageous Tendering

Art. 68 : Life Cycle cost, Cost-Effectiveness

(incl. environmental, social, economic) – method tbd

47

MEDTECH

www.medtecheurope.org

CONTRACT FOR A

HEALTHY FUTURE

MOST ECONOMIC

ADVANTAGEOUS

TENDERING

www.medtecheurope.org 48

Procurement, “the” cornerstone to access to novel Medical Technology in Europe.