Embed Size (px)

Citation preview

01 02 03 04 05

Across Health is pleased to present you with the state of the multichannel landscape in life sciences in Europe, US and emerging markets – for the sixth year already. Find out whether multichannel has reached its full potential in life sciences or not… yet! Click for preface by CEO Fonny Schenck

KEY SURVEY STATISTICS

EXECUTIVE SUMMARY

ADOPTION OF MULTICHANNEL

KEY CHALLENGES

FUTURE OF DIGITAL LIFE SCIENCES

01 02 03 04 05

10/06/14 Across Health Multichannel Barometer 2014 2

302 LIFE SCIENCES LEADERS COMPLETED THE BAROMETER, MAKING IT THE LARGEST OF ITS KIND.

WHAT ARE THE KEY DYNAMICS? SATISFACTION, CHANNEL USE, HURDLES AND BUDGET TRENDS.

BUDGETS PLATEAU AT A LOW LEVEL; MIX OPTIMIZATION AND CUSTOMER ANALYTICS REMAIN AN ISSUE.

LEGAL-REGULATORY ISSUES REMAIN THE KEY HURDLE, BUT ROI AND LACK OF KNOWLEDGE MOVE UP.

MOBILE & CROSS-CHANNEL ON THE INCREASE… SEVERAL HIGH-IMPACT CHANNELS REMAIN UNDERUSED.

Preface Last year, we saw satisfaction, knowledge and spend levels in multichannel plateauing and suggested that pharma was entering the trough of disillusionment, as defined by Gartner. This hypothesis is confirmed by this year’s results... overall, satisfaction levels are down vs 2013, and the importance of ROI evidence and internal skills is rising. In addition, there is a clear mismatch between what respondents feel is very impactful vs what they do. Most strikingly, digital spend is plateauing vs last year, from 16 to 15.6% of marketing spend... while other industries are already over 20% and intend to up that by 10% or more in 2014. Setting up the right organization (companywide strategy, processes & technology, organization...), focusing on the right set of multichannel tactics, rolling them out at scale and measuring for performance are key steps to move beyond the trough of disillusionment. We are seeing an increasing focus on such strategic efforts – maybe 2015 will be the first year of the “plateau of productivity” ... and 2014 the last year of the long fuse?

Fonny Schenck Managing Partner, Across Group CEO, Across Health

KEY SURVEY

STATISTICS EXECUTIVE SUMMARY

ADOPTION OF MULTICHANNEL

KEY CHALLENGES

FUTURE OF DIGITAL

2011 2012 2013 2014

2015?

The long fuse?

01

10/06/14 Across Health Multichannel Barometer 2014 3

Key survey statistics

302 RESPONDENTS FROM 100 LIFE SCIENCE COMPANIES COMPLETED

THE ONLINE SURVEY BETWEEN FEB. 25 AND

APRIL 3, 2014

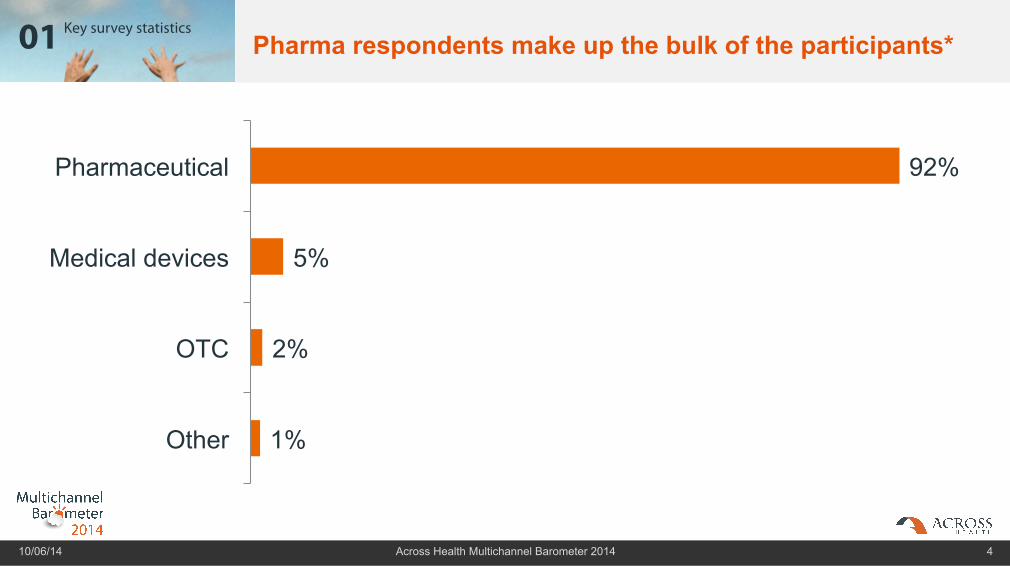

PHARMA RESPONDENTS MAKE UP THE BULK

GLOBAL SPREAD, BUT MOST RESPONDENTS FROM EUROPE

ONE THIRD HAVE INTERNATIONAL ROLE

MOST FUNCTIONS IN MARKETING & DIGITAL

01 Key survey statistics

1%

2%

5%

92%

Other

OTC

Medical devices

Pharmaceutical

Pharma respondents make up the bulk of the participants*

10/06/14 Across Health Multichannel Barometer 2014 4

KEY STATISTICS

01 Key survey statistics

4%

5%

6%

8%

9%

68%

Other

Japan

China

Latin-America

US

Europe

Most respondents come from the European region*

10/06/14 Across Health Multichannel Barometer 2014 5

KEY STATISTICS

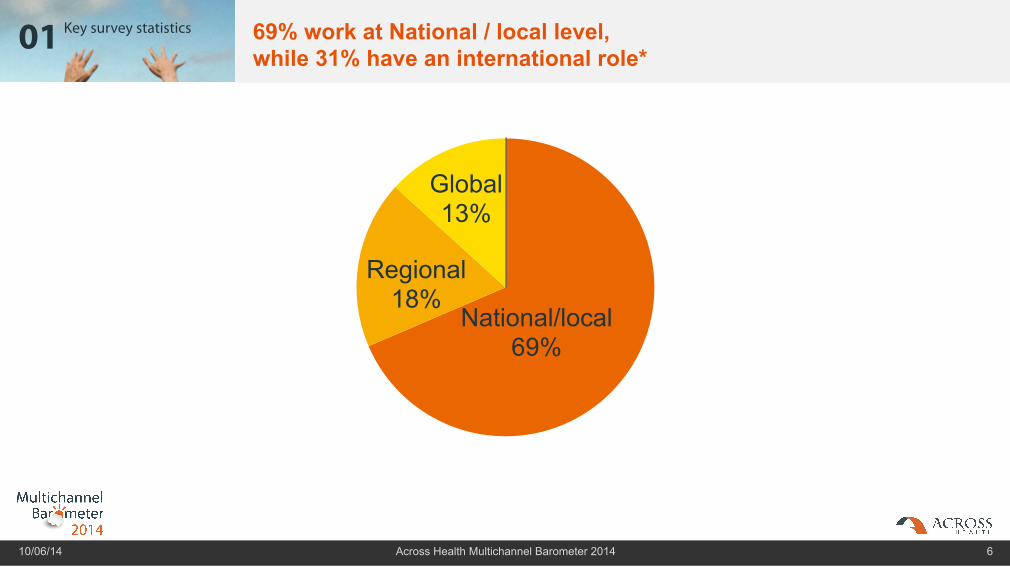

01 Key survey statistics 69% work at National / local level, while 31% have an international role*

10/06/14 Across Health Multichannel Barometer 2014 6

KEY STATISTICS

National/local 69%

Regional 18%

Global 13%

01 Key survey statistics Functional Spread

10/06/14 Across Health Multichannel Barometer 2014 7

KEY STATISTICS

7%

2%

3%

5%

6%

11%

21%

44%

Other

IT

Marketing Research

Medical

CRM

Sales

Digital

Marketing

02

LEGAL-REGULATORY ISSUES REMAIN THE TOP HURDLE, ROI &

LACK OF KNOWLEDGE RISING FAST

WEBSITES ARE MOST POPULAR TACTIC,

CROSS-CHANNEL AND MOBILE RISING FAST

SATISFACTION LEVELS REMAIN BELOW 20%

MULTICHANNEL BUDGETS HAVE

PLATEAUED

10/06/14 Across Health Multichannel Barometer 2014 8

Executive summary

02

Websites remain the top digital tactic. Tablet detailing is a strong second, and mobile and multichannel are rising quickly. In terms of impact vs use, there is clearly a mismatch, with several high-impact tactics just being piloted, while highly-used tactics receive a medium impact score.

Executive summary

REGULATORY ISSUES REMAIN TOP HURDLE, ROI & LACK OF KNOWLEDGE

ARE RISING

WEBSITES ARE MOST POPULAR TACTIC,

CROSS-CHANNEL AND MOBILE RISING FAST

SATISFACTION LEVELS REMAIN BELOW 20%

MULTICHANNEL BUDGETS HAVE

PLATEAUED

The top 4 bottlenecks for success are regulatory/legal/compliance issues, lack of digital strategy, ROI, and lack of internal knowledge. The latter two continue to rise fast.

Multichannel budgets seem to have plateaued – at least for now. Pharma continues to underspend on digital vs other industries and vs customer needs…as business pressures increase, we expect a strong growth in the next few years.

Satisfaction with multichannel edges higher in 2014 – but is still below 20%...although respondents continue to believe that their multichannel HCP efforts are on par with the competition…perhaps nobody is doing it really well?

10/06/14 Across Health Multichannel Barometer 2014 9

Full infograph

02 Executive summary

10/06/14 Across Health Multichannel Barometer 2014 10

03

DO WE STILL HAVE INSUFFICIENT

KNOWLEDGE & SKILLS IN DIGITAL?

IN THE MIX: WHAT IS HOT?

& WHAT IS NOT?

WE CAN’T GET NO SATISFACTION?

10/06/14 Across Health Multichannel Barometer 2014 11

Current adoption of multichannel

03 Current adoption of multichannel

STRATEGY, PEOPLE, SKILLS: ROOM FOR IMPROVEMENT!

SEVERAL HIGH-IMPACT CHANNELS ARE

UNDERUSED

RESPONDENTS DO NOT FEEL VERY CONFIDENT

• Around 60% of respondents has a multichannel brand/company strategy in place, but only around 25% of those consider it well executed (ie, 15% of all respondents)…

• More than 60% have a local and/or international team in place; but less than 50% of those feel it is very effective – local teams score significantly better than international ones

• Multichannel skill sets continue to be low – and are even lower vs 2009 (45% vs 37% with at least sufficient knowledge)

• Confidence in reaching patients & payers is even lower, and for patients too, confidence levels are dropping (Europe)... this correlates well with the limited use of high-impact patient channels (adherence, monitoring)

• As last year, multichannel initiatives targeted at HCPs are considered more competitive vs other customer groups....but only 24% feels this way...and in Europe, confidence is dropping. As in most other overviews, emerging markets score higher, but that may be due to the earlier stage of adoption (“hype” phase)

• Pilot focus continues to be on cross-channel & mobile mkt, while also patient adherence is rising through the ranks

• There is also limited use of third-party marketing & education opportunities (“fish where the fish are”) – less than 50% have included such channels so far.

• Pharma-owned websites still remain the most popular tactic, followed closely by tablet detailing. Mobile marketing is picking up, along with cross-channel

• Focused patient tactics are just emerging, with patient adherence tools scoring 26% standard use (quantified, self, social media and remote monitoring scoring much lower)

• Interestingly, the most used tactics are not always seen as the most effective… there is only 1 tactic in the high use/impact box, and highly effective tactics like multichannel and patient tools are hardly used.

10/06/14 Across Health Multichannel Barometer 2014 12

03 Current adoption of multichannel

20%

56%

24%

We have one, but its validity is questioned

We have one, but it is not implemented with rigour

We have one, and it is well executed

Most companies have issues with execution of their company-wide digital strategy or have not implemented one at all…

10/06/14 Across Health Multichannel Barometer 2014 13

Do you have a company-wide digital strategy in place (i.e. across all brands & functions)?

copyright © Across Health, 2014

57% 41%

2

No

No need

Yes

03 Current adoption of multichannel

26%

47%

27%

We have one, but its validity is questioned

We have one, but it is not implemented with rigour

We have one, and it is well executed

No

62%

36%

2

…the result is similar for digital brand strategies

10/06/14 Across Health Multichannel Barometer 2014 14

How robust is your digital brand strategy today (i.e. at the brand level – NOT the company level)?

copyright © Across Health, 2014

Don’t have one We have one

No need

03 Current adoption of multichannel

77%

16%

8%

Yes

Don’t know Not sure

No

25%

56%

19%

Yes, just being created Yes, but the impact is low Yes, and it is highly effective

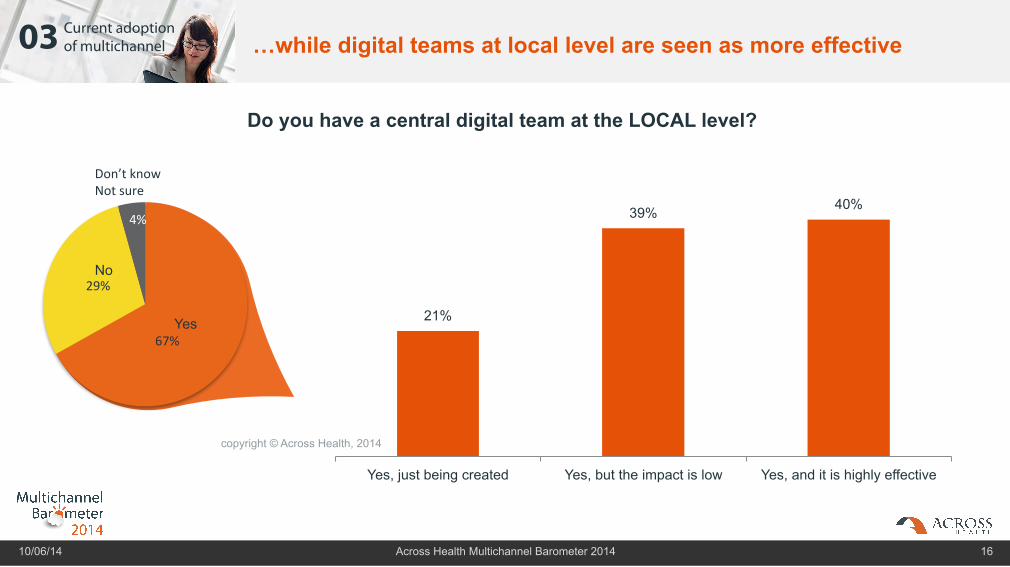

Most organizations have dedicated digital teams at international level but their effectiveness is questioned…

10/06/14 Across Health Multichannel Barometer 2014 15

Do you have a central digital team at the INTERNATIONAL level?

copyright © Across Health, 2014

03 Current adoption of multichannel

21%

39% 40%

Yes, just being created Yes, but the impact is low Yes, and it is highly effective

…while digital teams at local level are seen as more effective

10/06/14 Across Health Multichannel Barometer 2014 16

Do you have a central digital team at the LOCAL level?

copyright © Across Health, 2014

67%

29%

4%

No

Yes

Don’t know Not sure

03 Current adoption of multichannel

The level of internal expertise is dropping again – and arguably has not moved ahead since 2009

10/06/14 Across Health Multichannel Barometer 2014 17

Do you feel that you have sufficient knowledge of all opportunities offered by the internet for your business activities?

KEY CHALLENGES

Note: 2009-2011 data EMEA only

4%

4%

2%

1%

2%

4%

24%

20%

24%

18%

16%

21%

27%

31%

42%

44%

36%

38%

31%

34%

21%

30%

34%

25%

14%

10%

10%

8%

12%

12%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2009

2010

2011

2012

2013

2014

Totally insufficient

Insufficient

Between sufficient and insufficient

Sufficient

More than sufficient (expert)

copyright © Across Health, 2014

03 Current adoption of multichannel

80% 71%

62% 61%

59% 48%

46% 42% 41%

34% 33%

29% 26%

25% 23%

21% 20%

18% 11% 11% 11% 9%

8% 8% 7%

5%

11% 14%

21% 13% 17%

34% 33%

32% 22%

41% 25%

22% 36%

40% 28%

34% 35%

31% 12%

28% 18%

16% 22%

12% 19%

21%

4% 9%

11% 19% 16%

15% 16%

19% 26%

21% 30%

38% 25%

25% 40%

39% 39%

43% 54%

48% 60%

59% 47%

61% 54%

57%

5% 6% 6%

8% 9%

3% 5%

7% 11%

4% 12% 11%

12% 10% 9%

6% 6%

9% 23%

13% 11%

16% 23%

20% 20%

17%

Pharma-owned website* Tablet eDetailing Email marketing Direct marketing

Web Banners Web conference or virtual meeting

Online medical education HCP self-service portal

SEO Mobile marketing

SEA Outbound call centre

Patient adherence tools Integrated cross-channel campaigns

Virtual eDetailing Social media marketing

Social media monitoring eRep

e-sampling e-MSL

Mobile advertising e- or PHR** ad & promo services

Marketing automation software ePrescribing advertising & promo services

Quantified self / self-tracking devices Remote patient monitoring

Standard practice Pilot planned or ongoing Never Do not know / not applicable

Websites still remain the most popular tactic, followed closely by tablet detailing. Mobile marketing is picking up, along with cross-channel

10/06/14 Across Health Multichannel Barometer 2014 18

CURRENT ADOPTION *Company, product, or disease website. **electronic or personal health record.

copyright © Across Health, 2014

03 Current adoption of multichannel

80% 72%

63% 60% 59%

48% 48%

43% 41%

35% 33%

30% 25% 25%

22% 22%

21% 17%

11% 11% 10% 9% 8% 8% 8%

6%

11% 13%

21% 12%

17% 34%

33% 32%

23% 41%

26% 20%

41% 38%

34% 28%

36% 31%

29% 18%

16% 11%

20% 12%

20% 21%

4% 9%

10% 20%

15% 14%

14% 19%

25% 20%

30% 39%

23% 24% 39%

41% 38%

43% 47%

59% 59%

55% 47%

60% 52% 56%

5% 6% 5%

8% 9%

3% 5%

6% 11%

4% 12% 11% 10%

13% 5%

9% 6%

9% 13% 12%

16% 25% 24%

20% 20%

17%

Pharma-owned website* Tablet eDetailing Email marketing Direct marketing

Web Banners Web conference or virtual meeting

Online medical education HCP self-service portal

SEO Mobile marketing

SEA Outbound call centre

Integrated cross-channel campaigns Patient adherence tools Social media marketing

Virtual eDetailing Social media monitoring

eRep e-MSL

Mobile advertising e- or PHR** ad & promo services

e-sampling Marketing automation software

ePrescribing advertising & promo services Quantified self / self-tracking devices

Remote patient monitoring

Standard practice Pilot planned or ongoing Never Do not know / not applicable

Top tactics used in: Europe

10/06/14 Across Health Multichannel Barometer 2014 19

*Company, product, or disease website. **electronic or personal health record.

copyright © Across Health, 2014

03 Current adoption of multichannel

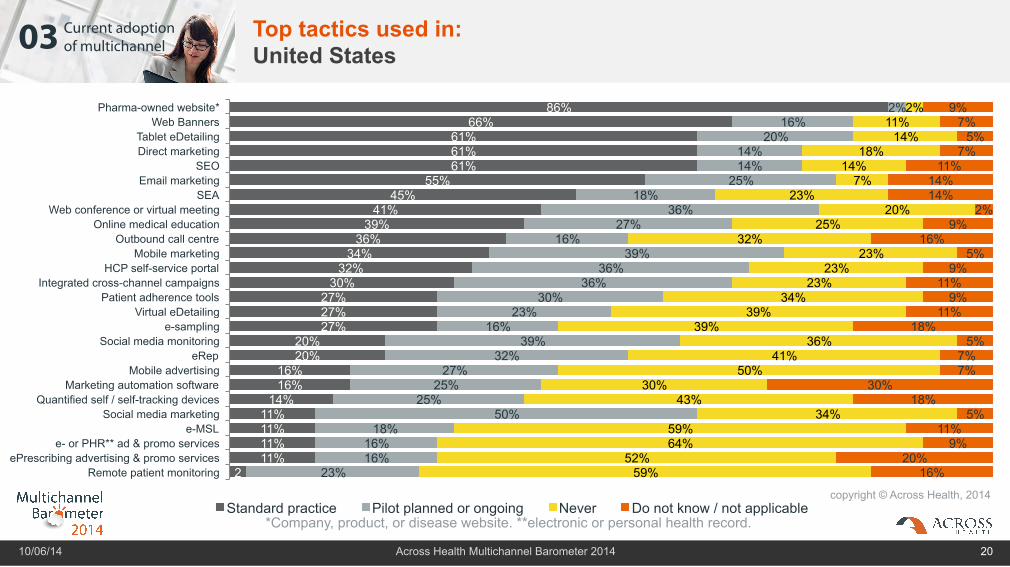

Top tactics used in: United States

10/06/14 Across Health Multichannel Barometer 2014 20

CURRENT ADOPTION

86% 66%

61% 61% 61%

55% 45%

41% 39%

36% 34%

32% 30%

27% 27% 27%

20% 20%

16% 16%

14% 11% 11% 11% 11%

2

2% 16%

20% 14% 14%

25% 18%

36% 27%

16% 39%

36% 36%

30% 23%

16% 39%

32% 27%

25% 25%

50% 18%

16% 16%

23%

2% 11%

14% 18%

14% 7%

23% 20%

25% 32%

23% 23%

23% 34%

39% 39%

36% 41%

50% 30%

43% 34%

59% 64%

52% 59%

9% 7%

5% 7%

11% 14% 14%

2% 9%

16% 5%

9% 11%

9% 11%

18% 5%

7% 7%

30% 18%

5% 11%

9% 20%

16%

Pharma-owned website* Web Banners

Tablet eDetailing Direct marketing

SEO Email marketing

SEA Web conference or virtual meeting

Online medical education Outbound call centre

Mobile marketing HCP self-service portal

Integrated cross-channel campaigns Patient adherence tools

Virtual eDetailing e-sampling

Social media monitoring eRep

Mobile advertising Marketing automation software

Quantified self / self-tracking devices Social media marketing

e-MSL e- or PHR** ad & promo services

ePrescribing advertising & promo services Remote patient monitoring

Standard practice Pilot planned or ongoing Never Do not know / not applicable *Company, product, or disease website. **electronic or personal health record.

copyright © Across Health, 2014

03 Current adoption of multichannel

82% 71% 71%

59% 59%

53% 47% 47%

41% 29% 29% 29% 29% 29%

24% 18% 18% 18%

12% 6% 6% 6% 6%

6% 24%

12% 29% 29%

18% 41%

29% 47%

47% 41%

35% 35%

29% 41%

71% 18%

6% 24%

24% 24%

12% 12%

18% 18%

12%

6% 6%

18% 12% 12%

24% 12%

18% 12%

18% 18% 29%

24% 35%

29% 6%

53% 65%

59% 59% 59%

65% 59%

65% 53%

71%

6%

6%

6%

6% 12%

6% 12%

6% 6% 6%

12% 12%

6% 12% 12%

18% 24%

18% 29%

18%

Pharma-owned website* Tablet eDetailing

Web Banners Web conference or virtual meeting

Email marketing Direct marketing

HCP self-service portal SEO

Online medical education Integrated cross-channel campaigns

SEA Outbound call centre

Patient adherence tools Virtual eDetailing

Social media monitoring Mobile marketing

Social media marketing Mobile advertising

eRep Marketing automation software

e-MSL ePrescribing advertising & promo services

e- or PHR** ad & promo services Quantified self / self-tracking devices

e-sampling Remote patient monitoring

Standard practice Pilot planned or ongoing Never Do not know / not applicable

Top tactics used in: Emerging countries

10/06/14 Across Health Multichannel Barometer 2014 21

CURRENT ADOPTION

*Company, product, or disease website. **electronic or personal health record.

copyright © Across Health, 2014

Emerging: Brazil, China, Colombia, Hungary, Mexico, Poland, Russian Federation, South Africa, Turkey, Uruguay

03 Current adoption of multichannel

11% 11% 12% 12%

13% 16%

17% 18%

20% 20% 20% 21% 21%

23% 26%

28% 29%

31% 32%

33% 34% 34%

36% 38%

41% 41%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

e-Sampling Pharma-owned website*

Direct Marketing ePrescribing advertising

Tablet eDetailing personal health records advertising

Web banners Mobile Advertising

Outbound Call Center Quantified self / self-tracking devices

Marketing automation software Remote patient monitoring

eMail marketing SEO SEA

Virtual eDetailing eMSL eRep

HCP self-service portal Online MedEd

Social media marketing Web conference

Social media monitoring Patient compliance/adherence

Mobile marketing Integrated cross-channel campaigns

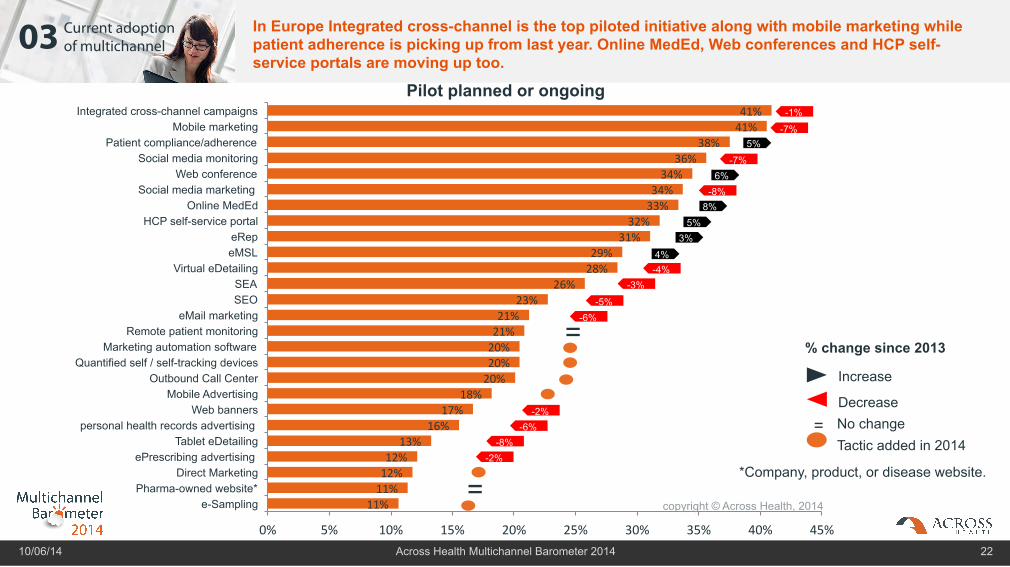

In Europe Integrated cross-channel is the top piloted initiative along with mobile marketing while patient adherence is picking up from last year. Online MedEd, Web conferences and HCP self-service portals are moving up too.

10/06/14 Across Health Multichannel Barometer 2014 22

Pilot planned or ongoing

*Company, product, or disease website.

copyright © Across Health, 2014

5%

-1%

-7%

-7% 6%

-8% 8%

5% 3%

-4% 4%

-3%

-5% -6%

= % change since 2013

Increase

Decrease No change = Tactic added in 2014

-2% -6%

-8% -2%

=

03 Current adoption of multichannel

27%

25%

21%

14%

16%

48%

47%

48%

27%

30%

25%

25%

27%

49%

44%

3

4

9%

9%

EPG

Mdlinx

Docguide

Medscape

Elsevier

Poor Neutral Good Excellent

Third-party offerings are less often used. Medscape and Elsevier are leading the pack.

10/06/14 Across Health Multichannel Barometer 2014 23

How would you rate the value for money of the following third-party digital channels to communicate

with your physicians?

copyright © Across Health, 2014 78%

75%

72%

49%

48%

22%

25%

28%

51%

52%

Never used it Used it

Have you worked with these third parties?

03 Current adoption of multichannel

Integrated cross-channel campaigns score the highest impact in all regions along with e-MSL and patient adherence tools yet they are all under utilized by pharma

10/06/14 Across Health Multichannel Barometer 2014 24

Impact scale from 0 (not impactful) to 10 (very impactful) *Company, product, or disease website. **electronic or personal health record.

*** Weighted Impact score based on results from previous question “How impactful do you feel these channels are?” **** Adoption is based on % of respondents who answered (Standard practice) to “How often do you use the following

multichannel Marketing tools TODAY?”

• Integrated cross-channel campaigns • Patient adherence tools • e-MSL • Remote patient monitoring

• Web conf/virtual meeting • Online MedEd • SEO

• HCP self-service portal • Mobile MKT • SEA

Adoption****

Perc

eive

d im

pact

***

10

0 0% 100% copyright © Across Health, 2014

• Tablet eDetailing

• Pharma-owned website* • Email MKT

• Web Banners • Direct MKT

4

• e/PHR** promotion

• e-sampling • MKT automation • ePrescribing

promo • Quantified self

• Call centre • Social media MKT • Virtual eDetailing • SM monitoring • eRep • Mobile Ad

6

30% 60%

Global

03 Current adoption of multichannel

Respondents are most confident in use of multichannel initiatives towards HCPs and least towards payors…

10/06/14 Across Health Multichannel Barometer 2014 25

How would you rank your company versus your competitors in using digital initiatives targeted at stakeholders?

copyright © Across Health, 2014

35%

53%

64%

41%

32%

28%

24%

15%

8%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

HCPs

Consumers/patients

Payors

Behind

Equal

Ahead

03 Current adoption of multichannel

2%

11%

0%

8% 7%

12%

25%

34%

18%

41%

32%

24% 21%

14%

41%

3% 2% 6%

Europe US Emerging

No opinion Far behind Behind Average Ahead Far ahead

…with the emerging markets showing most confidence

10/06/14 Across Health Multichannel Barometer 2014 26

How would you rank your company versus your competitors in using digital initiatives targeted at healthcare professionals?

HCPs

Emerging: Brazil, China, Colombia, Hungary, Mexico, Poland, Russian Federation, South Africa, Turkey, Uruguay

24%

47%

16%

copyright © Across Health, 2014

03 Current adoption of multichannel

0%

10%

20%

30%

40%

50%

60%

70%

2009 2010 2011 2012 2013 2014

Behind Equal Ahead

HCPs

…while a drop in confidence occurred in Europe vs. 2013

10/06/14 Across Health Multichannel Barometer 2014 27

CURRENT ADOPTION

How would you rank your company versus your competitors in using digital initiatives targeted at healthcare professionals?

copyright © Across Health, 2014

03 Current adoption of multichannel

3%

9% 12%

17%

9%

18%

34%

27% 29%

32%

36%

18%

11% 11%

18%

3%

7% 6%

Europe US Emerging

No opinion Far behind Behind Average Ahead Far ahead

Emerging markets also declare the greatest confidence in initiatives towards consumers/patients

10/06/14 Across Health Multichannel Barometer 2014 28

How would you rank your company versus your competitors in using digital initiatives targeted at consumers/patients?

14% 18%

CURRENT ADOPTION

Consumers/patients

24%

copyright © Across Health, 2014

Emerging: Brazil, China, Colombia, Hungary, Mexico, Poland, Russian Federation, South Africa, Turkey, Uruguay

03 Current adoption of multichannel

3%

12%

24%

44%

17%

1%

0 1 2 3 4 5

Overall, only 18% are satisfied with their current digital activities

10/06/14 Across Health Multichannel Barometer 2014 29

Extremely Satisfied

Extremely Dissatisfied

18%

CURRENT ADOPTION

On a scale from 0 to 5, how satisfied are you with your current digital activities?

copyright © Across Health, 2014

03 Current adoption of multichannel

38%

43%

29%

44%

41%

47%

19%

16%

24%

Europe

US

Emerging

Dissatisfied Neutral Satisfied

As last year, satisfaction rates were highest in emerging markets and lowest in US…

10/06/14 Across Health Multichannel Barometer 2014 30

CURRENT ADOPTION

On a scale from 0 to 5, how satisfied are you with your current digital activities?

copyright © Across Health, 2014

Emerging: Brazil, China, Colombia, Hungary, Mexico, Poland, Russian Federation, South Africa, Turkey, Uruguay

03 Current adoption of multichannel

0%

10%

20%

30%

40%

50%

60%

2009 2010 2011 2012 2013 2014

Dissatisfied Neutral Satisfied

…in Europe, satisfaction rates edged up slightly (but still less than 20%!!)

10/06/14 Across Health Multichannel Barometer 2014 31

On a scale from 0 to 5, how satisfied are you with your current digital activities?

copyright © Across Health, 2014

04

What are the key challenges in applying multichannel?

10/06/14 Across Health Multichannel Barometer 2014 32

KEY HURDLES ROI KNOWLEDGE

04 Key challenges

10/06/14 Across Health Multichannel Barometer 2014 33

KEY HURDLES ROI KNOWLEDGE

• As last year, regulatory, legal, and compliance issues, ROI, and lack of digital strategy remain the main challenges globally.

• In emerging markets, regulatory, legal, and compliance issues are by far the main concern (as opposed to ROI last year). In Europe, ROI issues are almost as important as regulatory concerns and in the US, the most advanced multichannel market, ROI has taken the top spot.

• Overall, ROI concerns and lack of internal knowledge have increased the most since 2010. Interestingly, also lack of management support is going up (perhaps they have been disappointed by the business impact of the current programs)

• Interestingly, only about 33% of respondents feel they have a poor understanding of ROI...so the framework is there...but the results are underwhelming?

04 Key challenges

3%

4%

4%

10%

12%

12%

18%

28%

31%

36%

42%

N/A

Other

No expert agencies with pharma background available

Customers are not ready

No budget

No headcount to support this

No senior management support

Not enough internal knowledge

No clear digital strategy

ROI questions

Regulatory / legal / healthcare compliance issues

Regulatory, legal and compliance issues remain the top bottlenecks, followed by ROI questions and unclear multichannel strategy

10/06/14 Across Health Multichannel Barometer 2014 34

KEY CHALLENGES

% of respondents indicating options as one of the top two main bottlenecks for digital in their organization.

copyright © Across Health, 2014

04 Key challenges

0%

10%

20%

30%

40%

50%

60%

70%

Regulatory / legal / healthcare compliance

issues

ROI questions No clear digital strategy Not enough internal knowledge

No senior management support

Europe

US

Emerging

Regulatory, legal and compliance issues are the largest bottlenecks in emerging countries and Europe, while US is mostly challenged by ROI questions

10/06/14 Across Health Multichannel Barometer 2014 35

KEY CHALLENGES

% of respondents indicating options as one of the top two main bottlenecks for digital in their organization. copyright © Across Health, 2014

Emerging: Brazil, China, Colombia, Hungary, Mexico, Poland, Russian Federation, South Africa, Turkey, Uruguay

04 Key challenges

6%

14%

16%

19%

28%

40%

51%

52%

61%

No expert agencies with pharma background available

Customers are not ready

No budget

No headcount to support this

No senior management support

Not enough internal knowledge in this area

No clear eBusiness strategy

ROI questions

Regulatory or legal issues

In Europe, ROI questions, lack of strategy and internal knowledge are rising in importance vs 2010…and even lack of senior support is on the increase.

10/06/14 Across Health Multichannel Barometer 2014 36

KEY CHALLENGES

% of respondents indicating main bottlenecks for digital in their organization.

* 2013 and 2014 data has been adjusted for comparability to previous years

copyright © Across Health, 2014

% change since 2010

High increase Low increase Decrease

-2%

5%

1%

-2%

10%

15%

6%

11%

4%

04 Key challenges

5%

28%

31%

23%

13%

4%

30% 28% 29%

9%

Very poor Poor OK Well Very well

2013 2014

More than 1/3 of all respondents state that they do not have sufficient understanding of ROI from their digital channels….

10/06/14 Across Health Multichannel Barometer 2014 37

How well do you understand the ROI from digital channels?

copyright © Across Health, 2014

34%

04 Key challenges

4% 7%

30% 32%

29% 28%

25%

41%

29% 30%

12%

8% 7%

18%

Europe US Emerging

Very poor

Poor

OK

Well

Very well

US and Europe feel they have an OK understanding of ROI; Emerging markets are behind

10/06/14 Across Health Multichannel Barometer 2014 38

How well do you understand the ROI from digital channels?

copyright © Across Health, 2014

Emerging: Brazil, China, Colombia, Hungary, Mexico, Poland, Russian Federation, South Africa, Turkey, Uruguay

05

10/06/14 Across Health Multichannel Barometer 2014 39

BUDGET CHANNEL MIX & CUSTOMER

INTELLIGENCE

What holds the future for digital in life sciences?

05 The future of digital in life sciences

10/06/14 Across Health Multichannel Barometer 2014 40

BUDGET

CHANNEL MIX & CUSTOMER

INTELLIGENCE

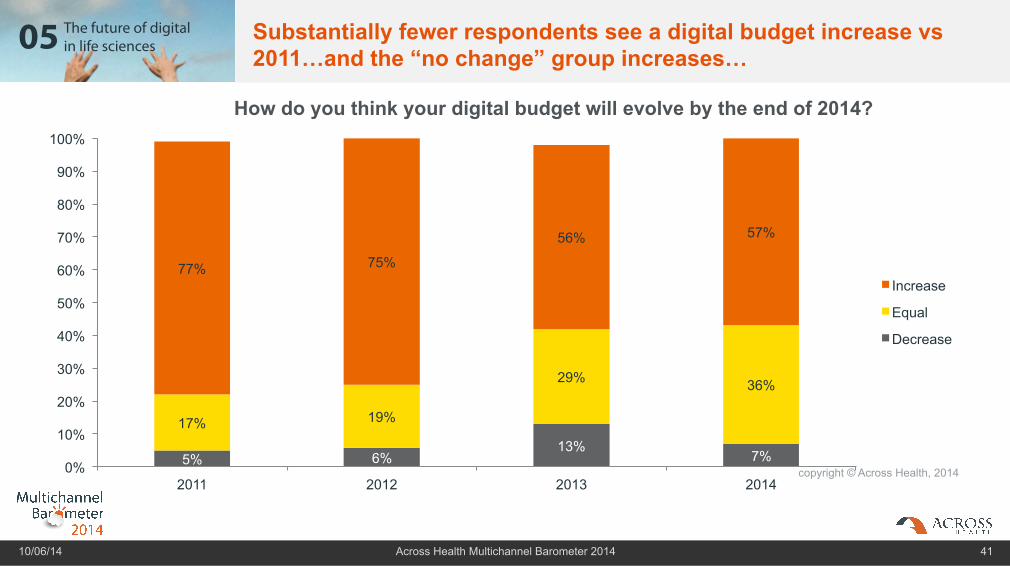

In view of the weak results on key parameters like strategic and organizational excellence, skill level, use of high-impact channels and overall satisfaction level, it should not come as a surprise that the investment in multichannel has plateaued vs last year – at a much earlier point than other industries.

Little progress is also being made on these 2 key areas

• Channel mix: For 9 out of 10 respondents, defining the optimal channel mix is not a simple task

• Customer intelligence: More than 4 of 5 respondents have not implemented a robust framework to leverage customer data for closed-loop marketing yet

05 The future of digital in life sciences

5% 6% 13%

7%

17% 19%

29% 36%

77% 75%

56% 57%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014

Increase

Equal

Decrease

Substantially fewer respondents see a digital budget increase vs 2011…and the “no change” group increases…

10/06/14 Across Health Multichannel Barometer 2014 41

How do you think your digital budget will evolve by the end of 2014?

copyright © Across Health, 2014

05 The future of digital in life sciences

9%

24%

19%

41%

16%

38%

17% 16% 19%

13%

20% 19%

12%

16%

6% 8% 8%

Europe US Emerging

less than 5% 5% to 10% 11% to 15% 16% to 20% 21% to 25% more than 25%

Average multichannel marketing budgets tend to be higher in the US and Europe than in emerging markets

10/06/14 Across Health Multichannel Barometer 2014 42

If you oversee a marketing budget, which percentage of it is allocated to digital initiatives THIS YEAR?

Average 10.9%

Average 15.8%

Average 15.6%

copyright © Across Health, 2014

Emerging: Brazil, China, Colombia, Hungary, Mexico, Poland, Russian Federation, South Africa, Turkey, Uruguay

05 The future of digital in life sciences

For the first time since 2010 in Europe, the average percentage allocated to digital marketing has plateaued – the average does not deviate a lot from 2012 figures…

10/06/14 Across Health Multichannel Barometer 2014 43

If you oversee a marketing budget, which percentage of it is allocated to digital initiatives THIS YEAR?

copyright © Across Health, 2014 0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2010 2011 2012 2013 2014

Average 5%

Average 8%

Average 15%

Average 16%

Δ +6% Δ -2.6%

Average 15.6%

05 The future of digital in life sciences

36% 36%

7%

14%

7%

If you oversee a MEDICAL* budget, which percentage of it is allocated to digital initiatives THIS YEAR?

46%

38%

8% 8%

less than 5%

5% to 10%

11% to 15%

16% to 20%

21% to 25%

more than 25%

Despite limited data, we can see an even lower average budget allocation to digital within sales and medical departments

10/06/14 Across Health Multichannel Barometer 2014 44

If you oversee a SALES* budget, which percentage of it is allocated to digital initiatives THIS YEAR?

Average

8.1% Average

6.2%

copyright © Across Health, 2014

*Limited data collected

copyright © Across Health, 2014

05 The future of digital in life sciences

2%

32%

51%

11% 4%

We do not see the need for collecting or using customer

data

We are not collecting useful customer data yet, but we

should

We have started doing some analysis on our multichannel

customer data

We have already implemented some robust

customer analytics frameworks

We leverage this data consistently

With little change from last year, more than 4 of 5 respondents have not implemented a robust framework to leverage customer data for closed-loop marketing yet

10/06/14 Across Health Multichannel Barometer 2014 45

Do you leverage customer data from your cross-channel initiatives for advanced customer analytics and closed-loop marketing?

15%

copyright © Across Health, 2014

% change since 2013

Increase Decrease

2%

-2%

-2%

3% -2%

05 The future of digital in life sciences

2% 2%

32% 27%

12%

52% 52% 59%

11% 14% 12% 4% 5%

18%

Europe US Emerging

We do not see the need for collecting or using customer data

We are not collecting useful customer data yet, but we should

We have started doing some analysis on our multichannel customer data

We have already implemented some robust customer analytics frameworks

We leverage this data consistently

The same can be observed in US while emerging countries show more focus at 30%

10/06/14 Across Health Multichannel Barometer 2014 46

Do you leverage customer data from your cross-channel initiatives for advanced customer analytics and closed-loop marketing?

copyright © Across Health, 2014

Emerging: Brazil, China, Colombia, Hungary, Mexico, Poland, Russian Federation, South Africa, Turkey, Uruguay

05 The future of digital in life sciences

24%

51%

16%

7% 2%

Very complicated Somewhat complicated Neither complicated nor simple

Relatively simple Very simple

For 9 out of 10 respondents, defining the optimal channel mix is not a simple task

10/06/14 Across Health Multichannel Barometer 2014 47

How complex is it to define the optimal channel mix*?

9%

*Allocating the right amount of budget to digital versus offline channels. copyright © Across Health, 2014

5%

-1%

1%

-6%

Emerging: Brazil, China, Colombia, Hungary, Mexico, Poland, Russian Federation, South Africa, Turkey, Uruguay

% change since 2013

Increase Decrease No change =

=

01 02 03 04 05

Final thoughts 2014… the long fuse? Digital will have a major impact on the outlook of healthcare, with empowered patients/caregivers, real-time clinical trials, the rise of the EHR & PHR 2.0, tight patient-physician connectivity and sophisticated payor programmes to name but a few key trends. Yet healthcare has traditionally been a slow adopter of new technologies at scale, which also reduces the business pressures on pharma to take the leap of faith. In life sciences, multichannel is very much evolutionary, rather than revolutionary. The comparison with the long fuse is therefore quite adequate…it may still take a while before the healthcare market “explodes”, but it is high time to start preparing for this transformational event and to jockey for position. As Marissa Meyer (Yahoo) puts it: Don't look for the "right" answer. There's a lot of good choices and then there's the one you pick, commit to, and make great.”… We hope we have given you some handles to improve your multichannel programme and wish you continued success in your journey!

Fonny Schenck Managing Partner, Across Group CEO, Across Health

LOREM IPSUM DOLOR SIT AMET, CONSECTETUR ADIPISCING ELIT. IN NIBH TELLUS, FRINGILLA AT

LOREM IPSUM DOLOR SIT AMET, CONSECTETUR ADIPISCING ELIT. IN NIBH TELLUS, FRINGILLA AT

LOREM IPSUM DOLOR SIT AMET, CONSECTETUR ADIPISCING ELIT. IN NIBH TELLUS, FRINGILLA AT

LOREM IPSUM DOLOR SIT AMET, CONSECTETUR ADIPISCING ELIT. IN NIBH TELLUS, FRINGILLA AT

LOREM IPSUM DOLOR SIT AMET, CONSECTETUR ADIPISCING ELIT. IN NIBH TELLUS, FRINGILLA AT

KEY SURVEY STATISTICS

EXECUTIVE SUMMARY

ADOPTION OF MULTICHANNEL

KEY CHALLENGES

FUTURE OF MULTICHANNEL

10/06/14 Across Health Multichannel Barometer 2014 48

2011 2012 2013 2014

2015?

“Chance favours the prepared mind”

Find us at

a-cross.com/health