Embed Size (px)

Citation preview

D I G I TA L T R A D E R E S T R I C T I O N S I N S O U T H A F R I C AM A R T I N A F. F E R R A C A N E R E S E A R C H A S S O C I A T E A T E C I P E

R O U N D TA B L E D I S C U S S I O N : E - C O M M E R C E I N A F R I C A 3 1 J A N U A R Y 2 0 1 7

D E F I N I T I O N A L I S S U E S

- “An e-commerce transaction is the sale or purchase of goods

or services, conducted over computer networks by methods

specifically designed for the purpose of receiving or placing

of orders.“ - UNCTAD

- “Cross-border provision of goods, products, services and

solutions that are instrumental to or avail themselves of

internet connectivity.”- Huawei

E - C O M M E R C E :

D I G I TA L T R A D E :

D I G I TA L T R A D E E S T I M A T E S : T H E D A TA B A S E

13 main areas:

1. Tariffs and trade defence

2. Taxation and subsidies

3. Public procurement

4. Foreign investment

5. IPR

6. Competition policy

7. Business mobility

8. Data policies

9. Intermediary liability

10. Content access

11. Quantitative trade restrictions

12. Standards

13. Online sales and transactions

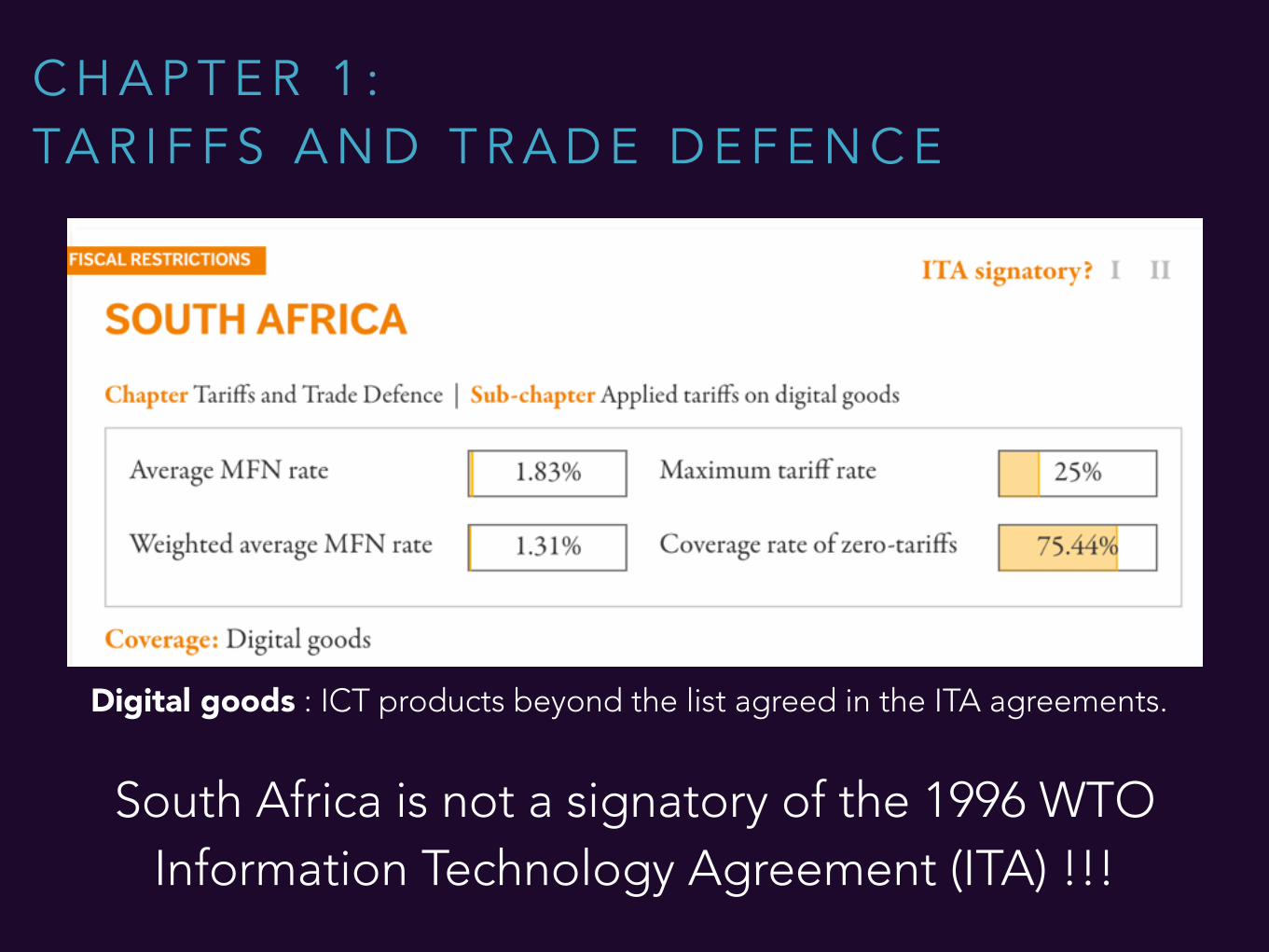

1. Applied tariffs on digital goods

2. Antidumping, CVD & Safeguards on digital goods

C H A P T E R 1 : TA R I F F S A N D T R A D E D E F E N C E

Digital goods : ICT products beyond the list agreed in the ITA agreements.

C H A P T E R 1 : TA R I F F S A N D T R A D E D E F E N C E

South Africa is not a signatory of the 1996 WTO Information Technology Agreement (ITA) !!!

C H A P T E R 2 : TA X A T I O N A N D S U B S I D I E S

1. Discriminatory tax regime on digital goods and products

2. Discriminatory tax regime on online services

3. Taxation on data usage

4. Subsidies and discriminatory tax regime

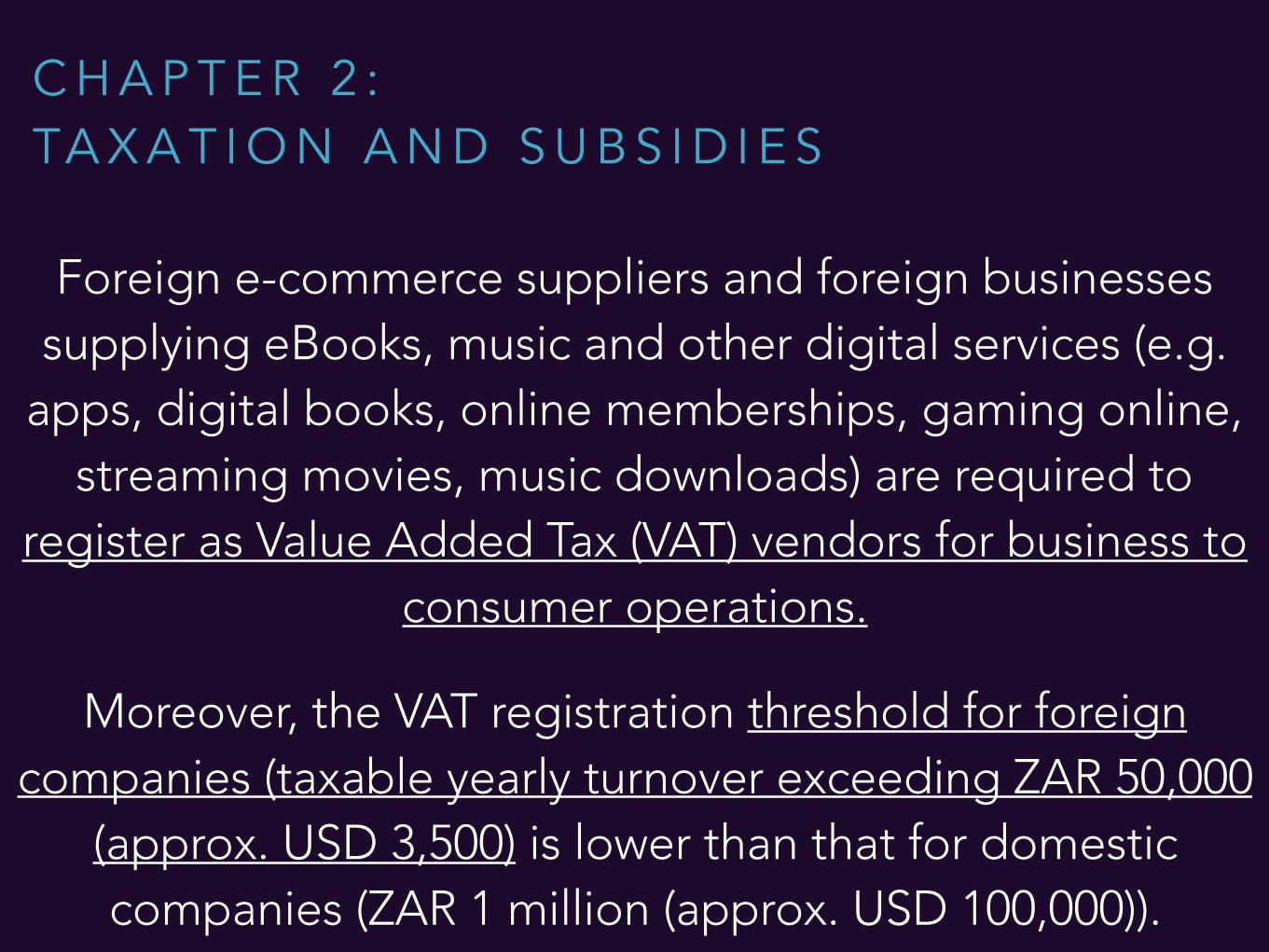

Foreign e-commerce suppliers and foreign businesses supplying eBooks, music and other digital services (e.g.

apps, digital books, online memberships, gaming online, streaming movies, music downloads) are required to

register as Value Added Tax (VAT) vendors for business to consumer operations.

C H A P T E R 2 : TA X A T I O N A N D S U B S I D I E S

Moreover, the VAT registration threshold for foreign companies (taxable yearly turnover exceeding ZAR 50,000

(approx. USD 3,500) is lower than that for domestic companies (ZAR 1 million (approx. USD 100,000)).

C H A P T E R 2 : TA X A T I O N A N D S U B S I D I E S

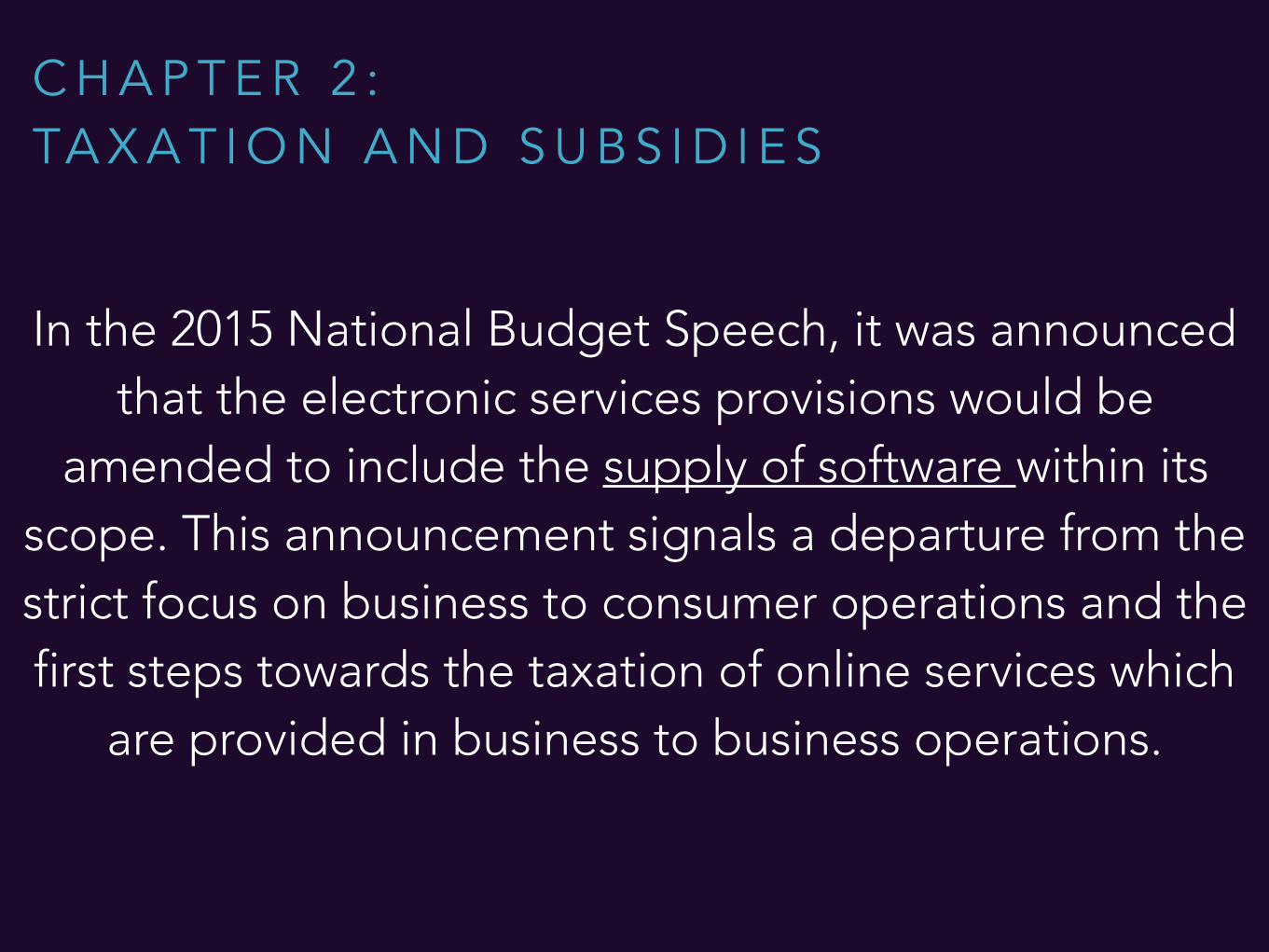

In the 2015 National Budget Speech, it was announced that the electronic services provisions would be

amended to include the supply of software within its scope. This announcement signals a departure from the strict focus on business to consumer operations and the first steps towards the taxation of online services which

are provided in business to business operations.

C H A P T E R 3 : P U B L I C P R O C U R E M E N T

1. Preferential purchase schemes covering ICT products, services

2. Surrendering of patents, source code etc.

3. Technology mandate (encryption, formats)

C H A P T E R 3 : P U B L I C P R O C U R E M E N T

In the case of designated sectors where local production and content is deemed “of critical importance”, the

tendering procedure must be restricted to locally produced goods, services or works only. As of April 2014,

these designated sectors include set-top boxes for digital TV and telecom cables.

C H A P T E R 3 : P U B L I C P R O C U R E M E N T

South Africa is not a party to the WTO Agreement on Government Procurement.

C H A P T E R 4 . F O R E I G N I N V E S T M E N T

1. Restrictions on ownership

2. Restrictions on board of directors and managers

3. Screening and restrictions on cross-border mergers

and acquisitions

1. Patents

2. Copyright

3. Trade secrets

C H A P T E R 5 . I N T E L L E C T U A L P R O P E R T Y R I G H T S

The Copyright Act provides for a copyright exception based on the notion of fair dealing. When the source as well as the name of the author are mentioned, literary or musical work can be used for the purposes of research,

private study, criticism, review and reporting current events.

C H A P T E R 5 : I N T E L L E C T U A L P R O P E R T Y R I G H T S

M A I N A R E A S : 6 . C O M P E T I T I O N P O L I C Y

Mainly related to the telecom sector….

M A I N A R E A S : 6 . C O M P E T I T I O N P O L I C Y

Despite deregulation in February 2005, it is reported that local loop unboundling has not been implemented.

M A I N A R E A S : 6 . C O M P E T I T I O N P O L I C Y

Telkom, the telecommunications incumbent in South Africa, is 51% state-owned.

M A I N A R E A S : 6 . C O M P E T I T I O N P O L I C Y

It is reported that several factors limite competition and the effects of liberalisation in the South Africa telecommunications market. These include:

interconnection, tariff regulation, access to scarce resources and anti-competitive practices.

In 2013, Orange (France) complained that mobile termination rates in South Africa were very high and that

the wholesale prices are not capped by the regulator.

M A I N A R E A S : 7 . B U S I N E S S M O B I L I T Y

Measures include quotas, labour

market regulations and limits of stay,

inter alia.

M A I N A R E A S : 8 . D A TA P O L I C I E S

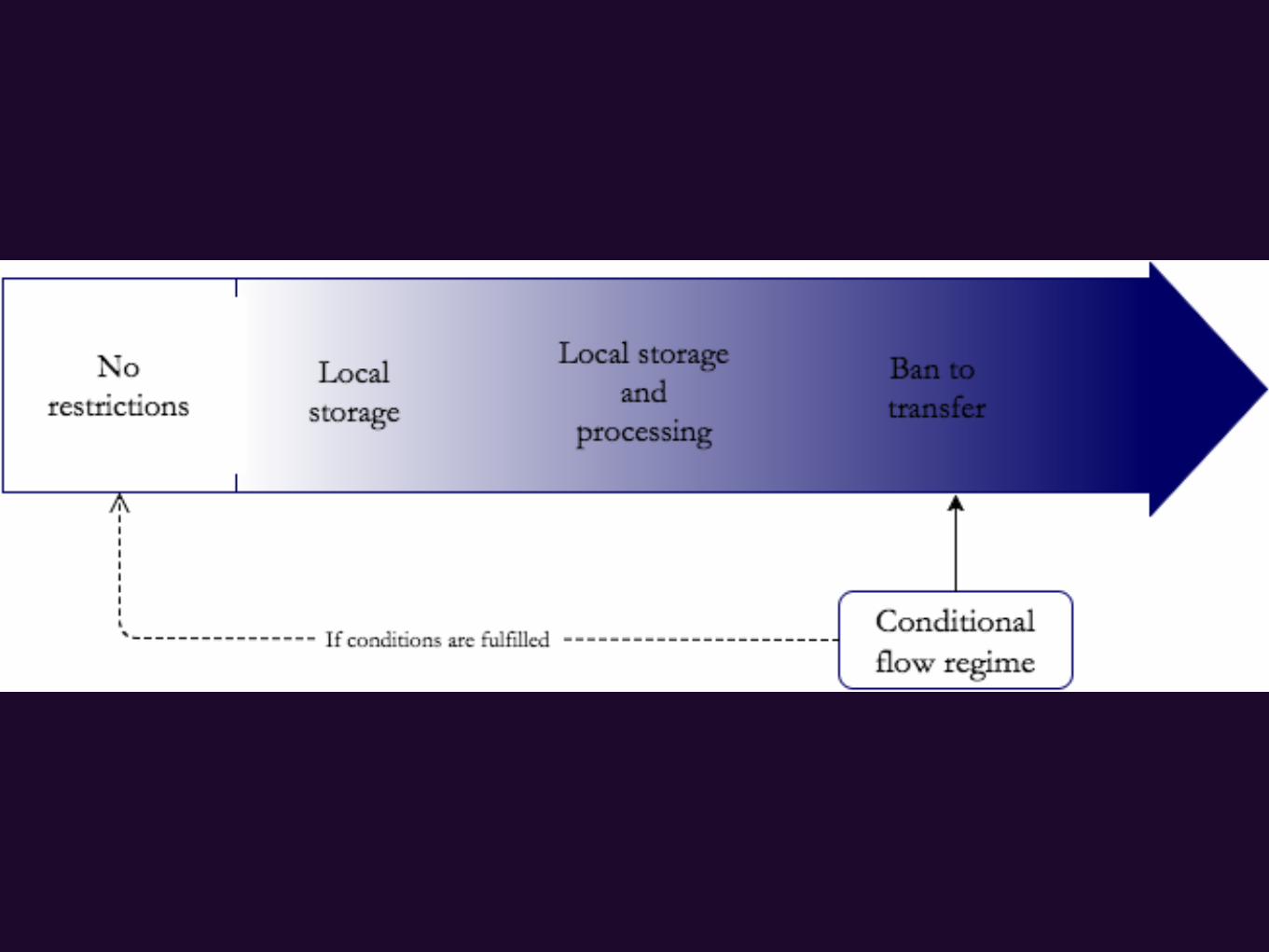

1. Restrictions cross-border on data flows (data localisation)

2. Data retention

3. Subject rights on data privacy

4. Administrative requirements on data privacy

5. Sanctions for non-compliance

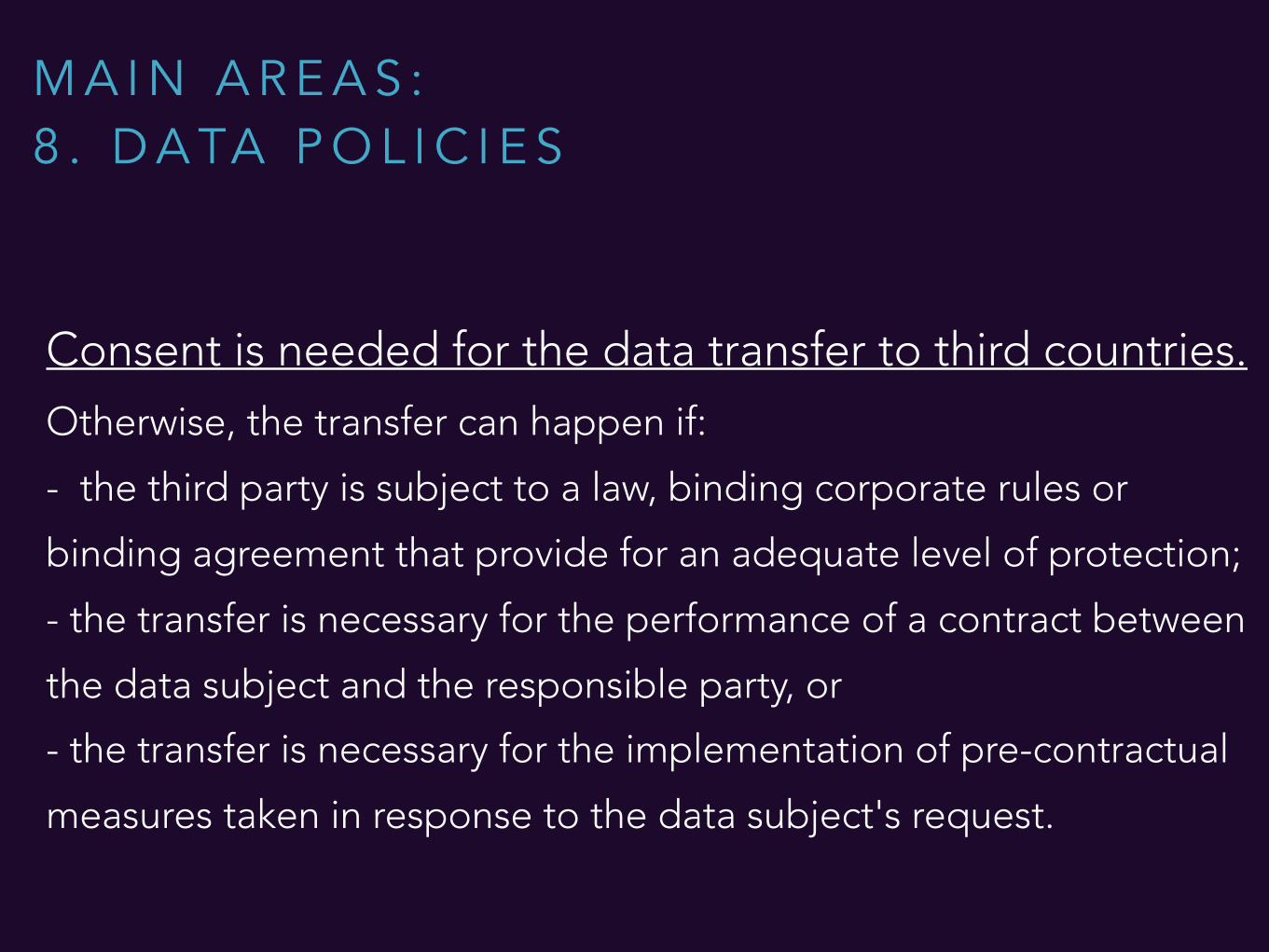

M A I N A R E A S : 8 . D A TA P O L I C I E S

Consent is needed for the data transfer to third countries. Otherwise, the transfer can happen if:

- the third party is subject to a law, binding corporate rules or

binding agreement that provide for an adequate level of protection;

- the transfer is necessary for the performance of a contract between

the data subject and the responsible party, or

- the transfer is necessary for the implementation of pre-contractual

measures taken in response to the data subject's request.

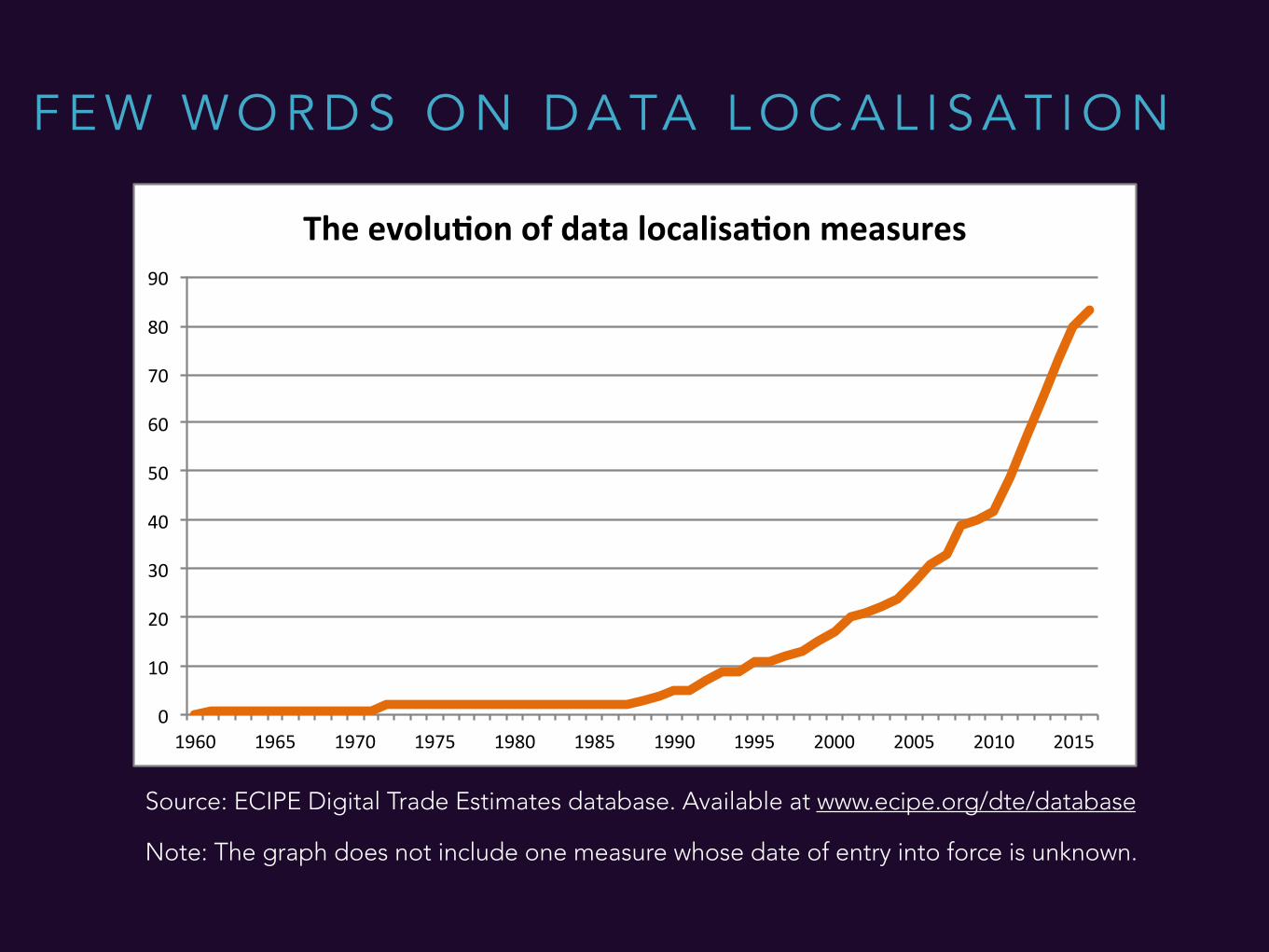

Source: ECIPE Digital Trade Estimates database. Available at www.ecipe.org/dte/database

Note: The graph does not include one measure whose date of entry into force is unknown.

0"

10"

20"

30"

40"

50"

60"

70"

80"

90"

1960" 1965" 1970" 1975" 1980" 1985" 1990" 1995" 2000" 2005" 2010" 2015"

The$evolu)on$of$data$localisa)on$measures$

F E W W O R D S O N D A TA L O C A L I S A T I O N

M A I N A R E A S : 9 . I N T E R M E D I A R Y L I A B I L I T Y

1. Framework that provides a safe harbor

2. Notice and takedown requirement

1 0 . C O N T E N T A C C E S S

1. Censorship, filtering

2. Bandwidth, net neutrality

M A I N A R E A S : 9 . I N T E R M E D I A R Y L I A B I L I T Y

The most distinctive feature of South African safe harbor regime for intermediaries is the conditioning of any liability limitation to the membership of an industry representative body recognised by the Minister of

Communications. Membership is subject to specific criteria, which are reported to be quite lengthy and

burdensome. At the same time, the representative body should assess compliance over all members.

M A I N A R E A S : 1 1 . Q U A N T I TA T I V E T R A D E R E S T R I C T I O N S

1. Import restrictions

2. Local Content Requirements for commercial market

3. Export restrictions

M A I N A R E A S : 1 2 . S TA N D A R D S

1. Telecom network and base standards (Non-international

broadband, mobile, and ICT product standards)

2. Product safety certification (EMC/EMI, radio transmission)

3. Product screening and testing requirements

4. Encryption

M A I N A R E A S : 1 2 . S TA N D A R D S

South Africa's National Regulator for Compulsory Specifications (NRCS) requires a Letter of Authority for product

safety and Certificate of Conformity for Electromagnetic Compatibility for some telecommunications equipment, some

radio equipment and information technology equipment.

Approval is typically issued based on foreign standard test reports that demonstrate compliance with South African

technical standards.Telecommunication line terminal equipment (TLTE) is subject to type approval by ICASA (the

regulator for the South African communications sector.)

M A I N A R E A S : 1 3 . O N L I N E S A L E S A N D T R A N S A C T I O N S

1. Barriers to fulfilment

2. Domain name (DNS) registration requirements

3. Ban to online sales

4. Discriminatory/disproportionate consumer protection

M A I N A R E A S : 1 3 . O N L I N E S A L E S A N D T R A N S A C T I O N S

South Africa has no de minimis rule, which means that there is no minimum value of a good below which the good is exempted from duties and taxes collected by

the customs.

W W W. E C I P E . O R G / D T E

M A R T I N A F R A N C E S C A F E R R A C A N E E M A I L : M A R T I N A . F E R R A C A N E @ E C I P E . O R G

THANK YOU!