Embed Size (px)

Citation preview

Consolidatequarterlyreportas at 30 september 2016

Hera Group – Consolidated quarterly report as at 30 September 2016

1

Approved by Hera Spa’s Board of Directors in the meeting of 09 November 2016

TABLE OF CONTENTS

Introduction

Governance and control bodies 002

Mission 003

Management Report

1.01 Economic and financial performance overview and alternative performance measures

definitions 004

1.01.01 Operating results 007

1.01.02 Analysis of the Group’s financial structure and investments 011

1.01.03 Analysis of net cash (net borrowings) 013

1.02 Analysis by business area 014

1.02.01 Gas 015

1.02.02 Electricity 018

1.02.03 Integrated Water Cycle 021

1.02.04 Waste Management 026

1.02.05 Other services 030

1.03 Share performance and investor relations 033

1.04 Reference scenario and strategic approach 036

1.05 Human resources 039

Abbreviated consolidated financial statements

2.01 Financial statements 040

2.01.01 Income statement 040

2.01.02 Statement of comprehensive income 041

2.01.03 Statement of financial position 042

2.01.04 Cash flow statement 044

2.01.05 Statement of changes in equity 045

2.02 Explanatory notes 046

2.03 Net Borrowings 049

2.04 Equity investments 050

introduction

Hera Group – Consolidated quarterly report as at 30 September 2016

2

Approved by Hera Spa’s Board of Directors in the meeting of 09 November 2016

GOVERNANCE AND CONTROL BODIES

Board of Directors

Chairman Tomaso Tommasi di Vignano CEO Stefano Venier Vice-Chairman Giovanni Basile Director Mara Bernardini Director Forte Clò Director Giorgia Gagliardi Director Massimo Giusti Director Riccardo Illy Director Stefano Manara Director Luca Mandrioli Director Danilo Manfredi Director Cesare Pillon Director Tiziana Primori Director Bruno Tani

Board of Statutory Auditors

Chairman Sergio Santi Standing Auditor Antonio Gaiani Standing Auditor Marianna Girolomini

Control and Risk Committee

Chairman Giovanni Basile Member Massimo Giusti Member Stefano Manara Member Danilo Manfredi

Remuneration Committee

Chairman Giovanni Basile Member Mara Bernardini Member Luca Mandrioli Member Cesare Pillon

Executive Committee

Chairman Tomaso Tommasi di Vignano Vice-Chairman Giovanni Basile Member Stefano Venier Member Riccardo Illy

Ethics Committee

Chairman Massimo Giusti Member Mario Viviani Member Filippo Maria Bocchi

Independent auditing firm

Deloitte & Touche

Hera Group – Consolidated quarterly report as at 30 September 2016

3

Approved by Hera Spa’s Board of Directors in the meeting of 09 November 2016

MISSION

“Hera’s goal is to be the best multi‐utility in Italy for its customers, workforce and shareholders. It

aims to achieve this through further development of an original corporate model capable of

innovation and of forging strong links with the areas in which it operates by respecting the local

environment".

“For Hera to be the best means to represent a reason for pride and trust for: customers, who

receive, thanks to Hera’s constant responsiveness to their needs, quality services that satisfy their

expectations. The women and men who work at Hera, whose skills, engagement and passion are

the foundation of the company’s success; shareholders, confident that the economic value of the

company will continue to be generated in full respect of the principles of social responsibility; the

reference areas, because economic, social and environmental health represent the promise of a

sustainable future; and suppliers, key elements in the value chain and partners for growth".

chapter 1

report on operations

Hera Group – Consolidated quarterly report as at 30 September 2016

4

Approved by Hera Spa’s Board of Directors in the meeting of 09 November 2016

1.01 ECONOMIC AND FINANCIAL PERFORMANCE OVERVIEW AND ALTERNATIVE

PERFORMANCE MEASURES DEFINITIONS

The Hera Group uses Alternative Performance Measures (APM) to more effectively convey

information about the profitability of the business in which it operates as well as its financial

situation. In accordance with the guidelines published 5 October 2015 by the European Securities

and Markets Authority (ESMA/2015/1415) and in keeping with the provisions of Consob

communication no. 92543 of 12/3/2015, the content and criterion for determining the

Alternative Performance Indicators used in this financial statement are explained below.

The EBITDA is an operating performance indicator and is calculated as “EBIT” plus “Depreciation,

amortization and provisions.” This measure is used as the financial target in internal

presentations (business plans) and external presentations (to analysts and investors), and is a

useful measure for evaluating the operating performance of the Group (as a whole, and at the

level of each Business Unit), including by comparing the operating profitability of the reporting

period with that of previous periods. In this way it is possible to analyze trends and compare the

efficiency achieved in different periods.

The EBITDA on revenues, EBIT on revenues and Net profit on revenues are used as the financial

target in internal presentations (business plans) and external presentations (to analysts and

investors) and they measure the Group’s operating performance by representing a proportion, in

Economic indicators and investments (€/mln)

Sept 2016 Sept 2015 Abs. change % change

Revenues 3,104.8 3,246.4 -141.6 -4.4%

EBITDA 650.6 640.2 +10.4 +1.6%

EBITDA/Revenues 21.0% 19.7% -1.3 p.p.

EBIT 329.2 317.3 +11.9 +3.8%

EBIT/Revenues 10.6% 9.8% -0.8 p.p.

Net profit 151.8 134.9 +16.9 +12.5%

Net profit/Revenues 4.9% 4.2% -0.7 p.p.

Net investments 241.2 220.6 +20.6 +9.3%

Economic and financial indicators(€/mln)

Sept 2016 Dec 2015 Abs. change % change

Net fixed assets 5,521.2 5,511.3 +9.9 +0.2%

Net working capital 82.1 157.0 -74.9 -47.7%

Provisions (535.8) (513.5) -22.3 -4.3%

Net invested capital 5,067.5 5,154.8 -87.3 -1.7%

Net financial debt (2,567.0) (2,651.7) +84.7 +3.2%

Economic indicators and investments

Economic and financial indicators

Definition of Alternative Performance Measures (APM)

Economic APMs and Investments

Hera Group – Consolidated quarterly report as at 30 September 2016

5

Approved by Hera Spa’s Board of Directors in the meeting of 09 November 2016

terms of percentage, of the gross operating margin, operating profit and net profit divided by the

value of Revenues.

Net investments are calculated as investments in property, plant and equipment, intangible

assets and non‐controlling interests net of capital contributions. This measure is used as the

financial target in internal presentations (business plans) and external presentations (to analysts

and investors), and is a useful measure for evaluating the spending capacity in terms of

investments in maintenance and development of the Group (as a whole and at the level of each

Business Unit), including through comparison with previous periods. In this way it is possible to

analyze trends and compare the efficiency achieved in different periods.

Net non‐current assets are calculated as the sum of: property, plant and equipment; Intangible

assets and goodwill; non‐controlling interests; and Deferred tax assets and liabilities. This

measure is used as the financial target in internal presentations (business plans) and external

presentations (to analysts and investors), and is a useful measure for evaluating the Group’s net

assets as a whole, including through comparison with previous periods. In this way it is possible

to analyze trends and compare the efficiency achieved in different periods.

Net working capital is calculated as the sum of: Inventories; Trade receivables and payables;

Current tax assets and liabilities; Other current assets and liabilities; and Current assets and

liabilities for commodity derivatives. This measure is used as the financial target in internal

presentations (business plans) and external presentations (to analysts and investors), and is a

useful measure for evaluating the Group’s ability to generate cash flow through operating

activities over a period of 12 months, including through comparison with previous periods. In this

way it is possible to analyze trends and compare the efficiency achieved in different periods.

Funds includes the sum of the items “Post‐employment and other benefits” and “Provisions for

risks and charges”. This measure is used as the financial target in internal presentations (business

plans) and external presentations (to analysts and investors), and is a useful measure for

evaluating the Group’s ability to cope with possible future liabilities, including through

comparison with previous periods. In this way it is possible to analyze trends and compare the

efficiency achieved in different periods.

Net invested capital is determined by the sum of “Net non‐current assets”, “Net working capital”

and “Funds”. This measure is used as the financial target in internal presentations (business

plans) and external presentations (to analysts and investors), and is a useful measure for

evaluating all of the Group’s current and non‐current operating assets and liabilities, as specified

above.

Net borrowings is a measure of the company’s financial structure determined in accordance with

Consob communication 15519/2006, adding the value of non‐current financial assets. This

measure is therefore calculated by adding together the following items: Current and non‐current

financial assets; Cash and cash equivalents; Current and non‐current financial liabilities; current

Economic and financial APMs

Hera Group – Consolidated quarterly report as at 30 September 2016

6

Approved by Hera Spa’s Board of Directors in the meeting of 09 November 2016

and non‐current assets and liabilities for Derivative financial instruments on interest and

exchange rates. This measure is used as the financial target in internal presentations (business

plans) and external presentations (to analysts and investors), and is a useful measure for

evaluating the Group's financial debt, including through comparison with prior periods. In this

way it is possible to analyze trends and compare the efficiency achieved in different periods.

The item source of financing is calculated as the sum of “net borrowings” and “equity”. This

measure is used as the financial target in internal presentations (business plans) and external

presentations (to analysts and investors) and represents the breakdown of funding sources

distinguishing between the company’s own equity and that of third parties; this is an indicator of

the Group’s financial autonomy and solidity.

Hera Group – Consolidated quarterly report as at 30 September 2016

7

Approved by Hera Spa’s Board of Directors in the meeting of 09 November 2016

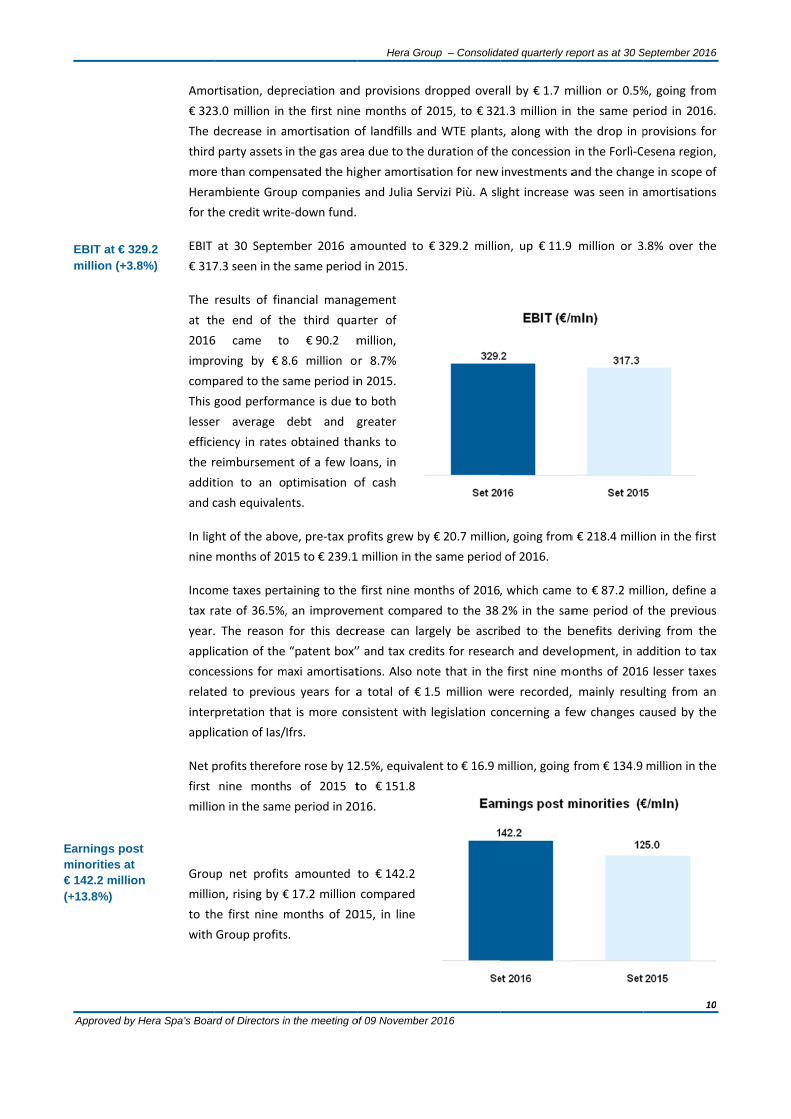

1.01.01 OPERATING RESULTS

At the end of the first nine months of 2016, the Hera Group shows growth in all economic

indicators, even when faced with an increasingly challenging context as defined by various

competitive and regulatory factors. The Hera Group has proved able to manage this scenario and

operate in a balanced and dynamic way: a comparison with the previous year, in fact, shows

EBITDA rising by 1.6%, operating income by 3.8% and net profits by 12.5%.

The main corporate and business operations that led to changes in the Group’s corporate

structure as of 30 September 2016 were as follows:

As of 1 November 2015, Biogas 2015 became part of the Group’s corporate structure.

This company’s activities include energy recovery and energy production from waste

recycling, as well as constructing, installing and managing the plants involved.

On 23 December 2015 Herambiente acquired 100% of shareholding in Waste Recycling

Spa, which is involved in special waste treatment and recovery in the province of Pisa

and in turn holds shares in Rew Trasporti Srl and Neweco Srl. During the second half of

2016 the two controlled companies were merged into Waste Recycling Spa.

As of 1 December 2015 Herambiente acquired effective control of a number of business

branches from Geo Nova Spa, taking over in particular the dangerous and non‐

dangerous waste storage plant in San Vito al Tagliamento (Pordenone) and the active

landfills for non‐dangerous waste located in Loria (Treviso) and Sommacampagna

(Verona).

On 29 December 2015 Hera Spa transferred 90% of the company Hera Energie

Rinnovabili to third parties; subsequently renamed Aloe Spa, it is no longer part of the

Group’s consolidated scope.

On 30 December 2015, AcegasApsAmga Spa divested its shares held in Trieste Onoranze

e Trasporti Funebri.

On 8 April 2016 Hera Comm Srl was definitively awarded the tender announced by the

Municipality of Giulianova for the acquisition of 100% of the share capital of Julia Servizi

Più, a gas and electricity sales company operating in the area surrounding Teramo.

Effective as of 1 July 2016, Hera Spa conferred its business branch dedicated to activities

in the sector of electricity and gas distribution to Inrete Distribuzione Energia Spa. This

company was established to manage activities in natural gas and electricity distribution

coherently with the requirements concerning functional and accounting unbundling

foreseen by the regulations of the Authority fo Electricity, Gas and Water System

(Aeegsi) for enterprises operating in the electricity and gas sectors, aimed at improving

competitiveness, efficiency and quality in providing energy services.

Constant results maintained

Approved by H

Constant anexpanding increases

Revenues a€ 3.1 billion

Hera Spa’s Boar

This

“Serv

unch

servi

The t

In the

roug

are r

by ro

and w

roug

chan

inves

class

e

amou

been

show

volum

€ 4.1

pass‐

reven

roug

Incom

Reven

Other

Raw m

Servic

Other

Perso

Capita

EBITD

Amort

Opera

Finan

Pre-ta

Taxes

Net p

AttribuShareNon-c

nd

at

rd of Directors in

consolidated

vice concessio

anged, is that

ces, are ackno

table below sh

e first nine mo

hly 4.4% com

esponsible fo

oughly € 180 m

water cycle s

hly € 25.6 m

ge in the

sted capital;

ification in th

“other op

unting to roug

n included. Th

w growth: re

mes of gas sol

1 million; a

‐through reve

nues from the

hly € 48 millio

me statement (€/m

nues

r operating revenue

materials

ce costs

r operating costs

onnel costs

alised costs

DA

t. & Prov.

ating profit

ncial operations

ax profit

s

profit for the perio

utable to:eholders of the Pacontrolling interests

n the meeting o

income stat

on arrangeme

t investments

owledged in t

hows the econ

onths of 2016

pared to the

r this decreas

million followi

ervices, the d

illion is due

rate of retu

lastly, a di

he items “rev

perating in

ghly € 15 milli

he following

venues for g

ld coming to r

greater port

enue related

e environmen

on and, lastly,

mln)

es

od

arent Companys

Hera Gro

of 09 November

tement reflec

ents”. The effe

s made in goo

he income sta

nomic results

6, revenues am

€ 3,246.4 mil

se: revenues f

ing a drop in t

drop of

to the

urn on

ifferent

venues”

ncome”

ion has

figures

greater

roughly

tion of

to non‐netw

nt area, owing

larger revenu

Sept 2016

3,104.8

259.9

(1,437.4)

(872.0)

(34.7)

(390.1)

20.0

650.6

(321.3)

329.2

(90.2)

239.1

(87.2)

151.8

142.29.6

oup – Consolida

2016

cts the applic

ect of applying

ods granted un

atement.

as at 30 Sept

mounted to €

lion seen in th

from electricit

the price of ra

work distribut

g to both an i

ues covering g

% Inc. S

8.4%

-46.3%

-28.1%

-1.1%

-12.6%

0.6%

21.0%

-10.3%

10.6%

-2.9%

7.7%

-2.8%

4.9%

4.6%0.3%

ated quarterly re

cation of acc

g this principl

nder concessio

ember 2016 a

3,104.8 millio

he same perio

ty and gas sal

w materials; i

ion, coming

ncrease in wa

greater service

Sept 2015 %

3,246.4

226.0

(1,613.2) -49

(815.4) -25

(40.9) -

(380.5) -1

17.9 0

640.2 1

(323.0) -9

317.3

(98.8) -3

218.4

(83.5) -2

134.9

125.09.9 0

eport as at 30 S

counting prin

le, which leav

on, only inclu

and 2015:

on, down € 14

od in 2015. Va

les and tradin

in regulated g

to roughly €

aste disposed

es in regulate

% Inc. Abs. chang

-14

7.0% +3

9.7% -17

5.1% +5

1.3% -

1.7% +

0.6% +

9.7% +1

9.9% -

9.8% +1

3.0% -

6.7% +2

2.6% +

4.2% +1

3.9% +10.3% -

September 2016

8

ciple IFRIC12

ves the results

uding network

41.6 million or

arious factors

ng were down

gas, electricity

12.0 million,

of coming to

d businesses.

ge % change

1.6 -4.4%

3.9 +15.0%

5.8 -10.9%

6.6 +6.9%

6.2 -15.1%

9.6 +2.5%

2.1 +11.8%

0.4 +1.6%

1.7 -0.5%

1.9 +3.8%

8.6 -8.7%

0.7 +9.5%

3.7 +4.4%

6.9 +12.5%

7.2 +13.8%0.3 -2.8%

6

8

2

s

k

r

s

n

y

,

o

e

%

%

%

%

%

%

%

%

%

%

%

%

%

%

%%

Approved by H

EBITDA at € 650.6 millio(+1.6%)

Hera Spa’s Boar

For f

Othe

grow

incre

(€ 2.8

differ

from

The

mont

of ga

mate

Othe

and €

scope

distri

highe

The c

2015

provi

Envir

prese

Capit

year.

EBITD

perio

great

busin

from

parti

that

suffe

elect

total

€ 8.5

€ 14.

redu

capit

inflat

on

rd of Directors in

urther details

er operating i

wth is mainly d

ease in the ex

8 million), a

rent classifica

“revenues” t

cost of raw

ths of 2015, s

as purchased

erials and a dif

er operating c

€ 6.2 million

e of consolida

ibution, large

er costs of dis

cost of person

5 to € 390.1 m

ided for by th

ronment area

ence.

talised costs g

.

DA settled at

od in 2015. Th

ter EBITDA re

ness and the c

distribution

cularly sign

the first nine

ered from less

tricity and

ling € 25.6 m

in gas, € 2.

9 in wate

ction in re

tal in regul

tion.

n the meeting o

, see the anal

ncome grew

due to a larger

xchange price

greater contr

ation, amount

o “other oper

and other m

showing a cha

and lesser tr

fferent accou

osts grew by

in lesser ope

ation (€ 20.0

ly attributable

posal for the

nnel rose by €

illion in the sa

e National lab

a and Julia Se

grew by € 2.1

t € 650.6 mill

he growth in e

sulting from p

contribution c

n. This res

ificant cons

months of th

ser revenues

water distr

million (respe

2 in electrici

er) following

eturn on in

lated sector

Hera Gro

of 09 November

yses of the sin

compared to

r contribution

e (roughly € 1

ribution com

ting to rough

rating income

materials drop

ange of 10.9%

rading activity

nting mechan

€ 50.4 million

erating expen

million), a ris

e to the pass‐

rise in volume

€ 9.6 million o

ame period of

bour agreeme

ervizi Più is p

1 million or 1

ion, recordin

electricity com

power plants,

coming

sult is

sidering

he year

in gas,

ribution

ctively:

ity and

g the

nvested

rs and

oup – Consolida

2016

ngle business

o September

n coming from

13 million), h

ing from sort

ly € 15 million

e”.

pped by € 175

%. As with rev

y, as well as a

nism used for

n overall (€ 56

ses), which is

se in the cost

‐through reve

es treated and

or 2.5%, going

f 2016. This in

ent. The entra

artially comp

1.8% at Sept

g a growth o

mpensates the

, the good pe

ated quarterly re

areas.

2015 by € 33

m energy savin

higher revenu

ted waste (€

n, of certifica

5.8 million co

enues, this fa

an overall dec

energy incent

6.6 million in

s mainly attri

of electricity

enues mention

d greater IFRIC

g from € 380.

ncrease is mai

nce of resour

ensated by a

ember 2016 c

of € 10.4 milli

e drop in othe

rformance see

eport as at 30 S

3.9 million, o

ngs certificate

ues ensuing f

€ 3.5 million),

ate sales reve

ompared to t

all is due to le

crease in the

tives.

greater costs

butable to ch

y and gas tran

ned above (€

C 12 costs (€ 5

.5 million at 3

nly due to the

rces from com

a reduction in

compared to

ion, or 1.6%

er business are

en in the sale

September 2016

9

r 15.0%. This

es owing to an

rom IFRIC 12

as well as a

nues, passing

the first nine

esser volumes

e price of raw

s for services,

hanges in the

nsmission and

12.0 million),

5 million).

30 September

e salary raises

mpanies in the

n the average

the previous

on the same

eas, thanks to

es and trading

6

9

s

n

2

a

g

e

s

w

,

e

d

,

r

s

e

e

s

e

o

g

Em€ (+

Approved by H

EBIT at € 329million (+3.8

arnings postminorities at

142.2 million+13.8%)

Hera Spa’s Boar

Amo

€ 323

The d

third

more

Hera

for th

EBIT

€ 317

The

at th

2016

impr

comp

This g

lesse

effici

the r

addit

and c

In lig

nine

Incom

tax r

year.

appli

conc

relate

inter

appli

Net p

first

millio

Grou

millio

to th

with

9.2 %)

t

n

rd of Directors in

rtisation, dep

3.0 million in

decrease in a

party assets

e than compe

mbiente Grou

he credit write

at 30 Septem

7.3 seen in the

results of fin

he end of th

6 came to

oving by € 8

pared to the s

good perform

er average

ency in rates

reimbursemen

tion to an o

cash equivalen

ht of the abo

months of 20

me taxes pert

ate of 36.5%,

. The reason

cation of the

essions for m

ed to previou

pretation tha

cation of Ias/

profits therefo

nine month

on in the same

up net profits

on, rising by €

he first nine m

Group profits

n the meeting o

preciation and

the first nine

mortisation o

in the gas are

nsated the hig

up companies

e‐down fund.

mber 2016 am

e same period

ancial manag

he third qua

o € 90.2 m

8.6 million o

same period in

mance is due t

debt and g

obtained tha

nt of a few lo

ptimisation o

nts.

ve, pre‐tax pr

015 to € 239.1

taining to the

, an improvem

for this decr

“patent box”

maxi amortisat

us years for a

t is more con

Ifrs.

ore rose by 12

s of 2015 t

e period in 20

s amounted t

€ 17.2 million

months of 20

s.

Hera Gro

of 09 November

d provisions d

e months of 2

of landfills an

ea due to the d

gher amortisa

s and Julia Se

mounted to

d in 2015.

gement

rter of

million,

r 8.7%

n 2015.

to both

greater

anks to

oans, in

of cash

rofits grew by

1 million in the

first nine mo

ment compar

rease can lar

” and tax cred

tions. Also no

a total of € 1

nsistent with

2.5%, equivale

to € 151.8

016.

to € 142.2

compared

015, in line

oup – Consolida

2016

dropped overa

2015, to € 32

d WTE plants

duration of th

ation for new

rvizi Più. A sli

€ 329.2 millio

y € 20.7 millio

e same period

onths of 2016,

ed to the 38.

gely be ascri

dits for resear

ote that in the

1.5 million we

legislation co

ent to € 16.9 m

ated quarterly re

all by € 1.7 m

1.3 million in

s, along with

he concession

investments a

ight increase

on, up € 11.9

n, going from

d of 2016.

, which came

2% in the sam

bed to the b

rch and devel

e first nine mo

ere recorded,

oncerning a fe

million, going

eport as at 30 S

million or 0.5%

the same pe

the drop in p

in the Forlì‐C

and the chang

was seen in a

9 million or 3

m € 218.4 milli

e to € 87.2 mil

me period of

benefits deriv

opment, in ad

onths of 2016

, mainly resu

ew changes c

from € 134.9

September 2016

10

%, going from

eriod in 2016.

provisions for

esena region,

ge in scope of

amortisations

.8% over the

on in the first

llion, define a

the previous

ving from the

ddition to tax

6 lesser taxes

lting from an

caused by the

million in the

6

0

m

.

r

,

f

s

e

t

a

s

e

x

s

n

e

e

Hera Group – Consolidated quarterly report as at 30 September 2016

11

Approved by Hera Spa’s Board of Directors in the meeting of 09 November 2016

1.01.02 ANALYSIS OF THE GROUP’S FINANCIAL STRUCTURE AND INVESTMENTS

The table below shows changes in the Group’s net invested capital and sources of financing for

the period ended 30 September 2016:

At 30 September 2016, net invested

capital dropped compared to 31

December 2015 by € 87.3 million. This

change is related to the good

performance of net working capital,

which recorded a considerable

decrease due to the good performance

of trade receivables.

Group investments came to € 241.2 million in the first three quarters of 2016, with a further

€ 10.5 million in capital grants, of which € 4.2 million for the New Investments Fund (FoNI), as

provided for by the tariff method for the Integrated water service. Including capital grants, the

Group’s overall investments amounted to € 251.5 million. Net investments rose by € 20.6 million,

going from € 220.6 million in September 2015 to € 241.2 million in September 2016.

Invested capital and sources of financing (€/mln)

30 Sep 2016 Inc. % 31 Dec 2015 Inc. % Abs. change % change

Net non-current assets 5,523.2 108.9% 5,511.3 106.9% +11.9 +0.2%

Net working capital 82.1 1.6% 157.0 3.0% (74.9) (47.7%)

(Funds) (535.8) -10.6% (513.5) -10.0% (22.3) +4.3%

Net invested capital 5,069.5 100.0% 5,154.8 100.0% (85.3) (1.7%)

Equity (2,502.5) 49.4% (2,503.1) 48.6% +0.6 (0.0%)

Long-term borrowings (2,729.0) 53.8% (2,743.6) 53.2% +14.6 (0.5%)

Net cash/short term borrowings 162.0 -3.2% 91.9 -1.8% +70.1 +76.3%

Net financial debt (2,567.0) 50.6% (2,651.7) 51.4% +84.7 (3.2%)

Total sources of financing (5,069.5) -100.0% (5,154.8) 100.0% +85.3 (1.7%)

The Group’s magnitude increases

Net invested capital: € 5.1 billion

Net investments rise to € 241.2 million

5,1 5,15,2

5,1

Dec 2014 Sep 2015 Dec 2015 Sep 2016

Net invested capital (€/bln)

Hera Group – Consolidated quarterly report as at 30 September 2016

12

Approved by Hera Spa’s Board of Directors in the meeting of 09 November 2016

The following table shows a subdivision by sector, with separate mention of capital grants:

Capital expenditure totalled € 251.5 million, up 9.6% over September 2015, and mainly

concerned interventions on plants, networks and infrastructures. In addition, updating activities

were performed as required by new regulations, mainly concerning gas distribution, with a large‐

scale metre substitution, and the purification and sewerage area.

Remarks on investments in each single area are included in the analysis by business area.

At the Group’s headquarters, investments concerned interventions on corporate buildings, IT

systems and the vehicle fleet, as well as laboratories and remote control structures. Overall

investments in structures rose by € 3.3 million compared to the same period in the previous year,

an increase mainly due to substitutions of vehicles and equipment as well as work on corporate

buildings.

At September 2016, provisions amounted to € 535.8 million, growing compared to December

2015 thanks to provisions for the period in question, which covered usage expenses and the

effects of the adjustment of the TFR fund, calculated according to actuarial criteria, and

provisions following the enlargement of the Ravenna landfill.

Equity was essentially in line with the figures seen at 31 December of the previous year, passing

from € 2,503.1 million at 31 December 2015 to € 2,500.5 million at 30 September 2016, following

a dividend payment totalling roughly € 144.0 million, more than compensated for by the results

for the period, coming to € 151.8 million.

Total investments (€/mln)

Sept 2016 Sept 2015 Abs.change % change

Gas area 64.1 57.6 +6.5 +11.3%

Electricity area 16.7 15.1 +1.6 +10.6%

Water cycle area 93.1 91.6 +1.5 +1.6%

Waste management area 32.2 21.8 +10.4 +47.7%

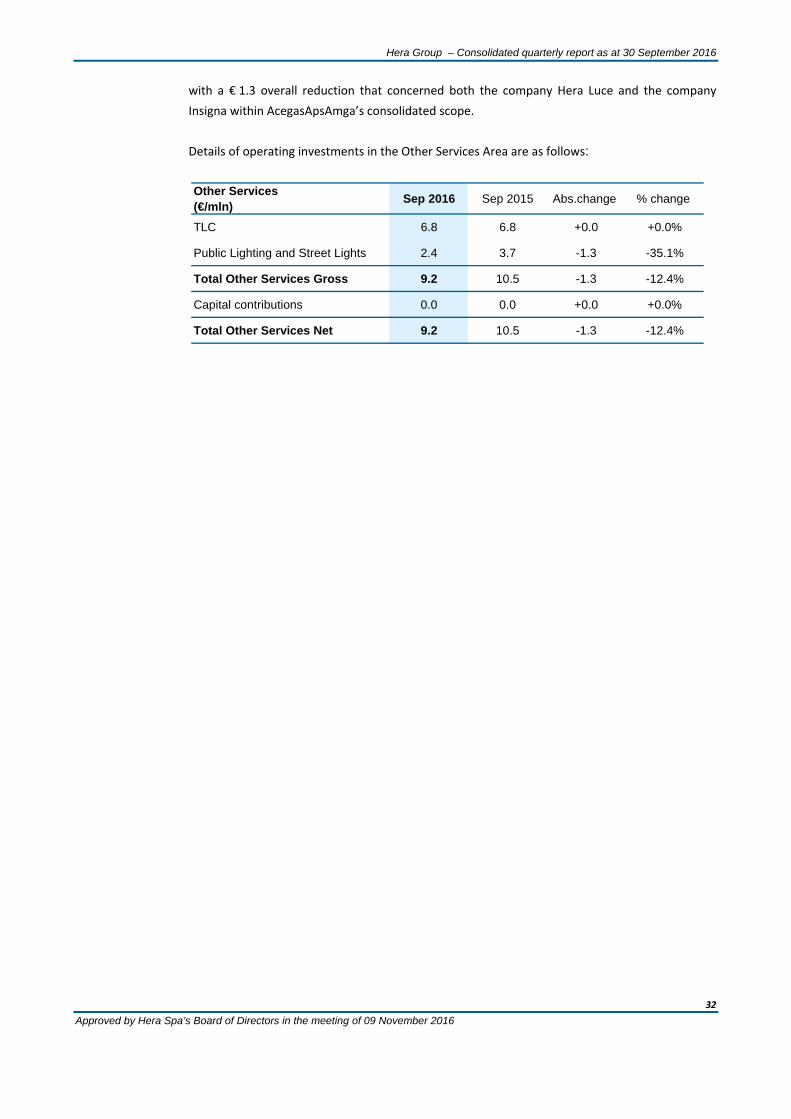

Other services area 9.2 10.5 -1.3 -12.4%

Headquarters 36.3 33.0 +3.3 +10.0%

Total operating investments 251.5 229.5 +22.0 +9.6%

Total financial investments 0.2 0.4 -0.2 -50.0%

Total gross investments 251.7 230.0 +21.7 +9.4%

Capital contributions 10.5 9.3 +1.2 +12.9%

of which FoNI (New Investment Fund) 4.2 7.3 -3.1 -42.5%

Total net investments 241.2 220.6 +20.6 +9.3%

Provisions come to € 535.8 million

€ 2.5 billion in equity

Strong commitment continues in operating investments in plants and infrastructures

Investments at headquarters in buildings, IT systems and vehicle fleet

Hera Group – Consolidated quarterly report as at 30 September 2016

13

Approved by Hera Spa’s Board of Directors in the meeting of 09 November 2016

1.01.03 ANALYSIS OF NET CASH (NET BORROWINGS)

An analysis of net borrowings is provided in the following table:

Current borrowings consist mainly in shares of bank loans reaching maturity for roughly € 85.4

million, accrued interest for roughly € 67 million and usage of current credit lines for roughly € 29

million. The amount of bank loans reaching maturity has fallen since 31 December 2015, as a

consequence of the reimbursement of a € 195.4 million bond in February 2016. The amount

related to non‐current bank debt and bonds is prevalently made up of bonds issued on the

European market and listed on the Luxembourg Stock Exchange (78% of the total) with

repayment at maturity.

As a whole, borrowings show an average term to maturity of over 8 years, with 73% maturing

after more than 5 years.

Net financial debt went down from

€ 2,651.7 at 31 December 2015 to

€ 2,567.0 at 30 September 2016. This

positive result, which is due to the cash

flow generated by operational

management, allowed dividends to be

entirely financed and net borrowings to

be reduced by over € 84 million.

An important contribution came from

the good performance of trade receivables and the ensuing optimisation of net working capital

(€/mln) 30 Sep 2016 31 Dec 2015

a Cash and cash equivalents 379.3 541.6

b Other current financial receivables 28.8 34.6

Current financial debt (96.3) (129.2)

Current bank debt (86.2) (284.9)

Other current financial liabilities (62.0) (68.2)

Finance lease payments maturing within 12 months (1.6) (2.0)

c Current financial debt (246.1) (484.3)

d=a+b+c Net current financial debt 162.0 91.9

Non-current bank debt and bonds issued (2,821.5) (2,845.4)

Other non-current financial liabilities (5.2) (5.8)

Finance lease payments maturing after 12 months (15.5) (17.6)

e Non-current financial debt (2,842.2) (2,868.8)

f=d+e Net borrowings - Consob communication n° 15519/2006 (2,680.2) (2,776.9)

g Non-current financial receivables 113.2 125.2

h=f+g Net financial debt (2,567.0) (2,651.7)

A strong financial position

Net financial debt drops to € 2.6 billion

2,6 2,62,7

2,6

Dec 2014 Sep 2015 Dec 2015 Sep 2016

Net financial debt (€/bln)

Hera Group – Consolidated quarterly report as at 30 September 2016

14

Approved by Hera Spa’s Board of Directors in the meeting of 09 November 2016

1.02 ANALYSIS BY BUSINESS AREA

An analysis of the results achieved by management in the various business areas in which the

Group operates is provided below, including: the gas area, which covers services in natural gas

and LPG distribution and sales, district heating and heat management; the electricity area, which

covers services in electricity production, distribution and sales; the integrated water cycle area,

which covers aqueduct, purification and sewerage services; the waste management area, which

covers services in waste collection, treatment, recovery and disposal; the other services area,

which covers services in public lighting and telecommunications, as well as other minor services.

As of September 2016, the Hera Group has revised the layout of its own multi‐business portfolio

in order to improve and simplify the process of financial reporting concerning its own industrial

structures: the business of industrial cogeneration has been transferred from the electricity area

to the gas business area, uniting it with heat management, which also respects the Group’s

organisational vision. Pertinent data from 2015 has been restated in line with this change.

The Group’s income statements include corporate headquarter costs and reflect intercompany

transactions accounted for at arm’s length.

The following analyses of each single business area take into account all increased revenues and

costs, with no impact on EBITDA, related to the application of IFRIC 12, as shown in the Group's

consolidated income statement. The business areas affected by IFRIC 12 are: natural gas

distribution services, electricity distribution services, all integrated water cycle services and

public lighting services.

28,7%

16,0%26,7%

26,5%

2,1%

September 2016 EBITDA

Gas Electricity IWC Waste Other Services

The contributions to EBITDA coming from the Group’s different areas show a balanced mix, coherent with the Group’s multi-business strategy

Approved by H

Contributionoverall EBITdecreases

Gas area EBfalls by 9.3%

1.3 million gcustomers

Gas: EBITDA

Hera Spa’s Boar

1.02

The g

Thes

in wh

the m

in the

resol

nine

recla

as fu

EBITD

perso

The f

Total

Septe

comm

set in

wide

parti

Più,

contr

custo

(€/m

Area

Grou

Perc

n to TDA

BITDA %

as

A falls

rd of Directors in

.01 GAS

gas area saw a

e results mus

hich resolutio

methods used

e gas sector, w

ution’s negat

months of the

ssification of

rther specifie

DA, made up

onnel costs; re

following tabl

l gas custome

ember 2015

mercial and c

n place to co

r customer

cular with the

which occu

ributed with

omers to the o

mln)

a EBITDA

up EBITDA

centage weigh

n the meeting o

a decrease as

st be consider

on 583/2015/R

d in calculating

with the aim o

tive impact o

e year. Note t

the business o

d in paragrap

of € 10 millio

egarding inves

e shows the c

ers rose by 1

5, owing to

customer loya

ontrast compe

base, in cen

e acquisition o

rred in June

h roughly 1

overall numbe

t

Hera Gro

of 09 November

at 30 Septem

red within a r

R/com of 2 D

g the rate of

of introducing

n revenues a

that a pro form

of industrial c

ph 1.02. The e

on in revenues

stments, the

changes occur

1.8% over 30

o both the

alty initiatives

etition, and a

ntral Italy in

of Julia Servizi

e 2016 and

13 thousand

er.

Se

oup – Consolida

2016

mber compare

egulatory con

December 201

return for inv

g greater stab

nd EBITDA am

ma version of

cogeneration f

effect of this r

s, € 7.5 millio

reclassificatio

rred in terms o

0

e

s

a

n

i

d

d

ep 2016

186.5

650.6

28.7%

ated quarterly re

d to the same

ntext that def

15 took effect

vested capital

ility into the r

mounted to €

the 2015 dat

from the elect

eclassification

n in operating

n comes to €

of EBITDA:

Sep 2015 A

205.6

640.2

32.1%

eport as at 30 S

e date in the p

fined 2016 as

t. This resolut

for infrastruc

regulatory fra

€ 8.5 million

ta is provided

tricity area to

n amounts to

g costs and €

1.5 million.

Abs. change

-19.1

+10.4

-3.4 p.p.

September 2016

15

previous year.

the first year

tion modified

cture services

mework. This

over the first

as part of the

o the gas area,

€ 2 million in

0.5 million in

% change

-9.3%

+1.6%

6

5

.

r

d

s

s

t

e

,

n

n

Approved by H

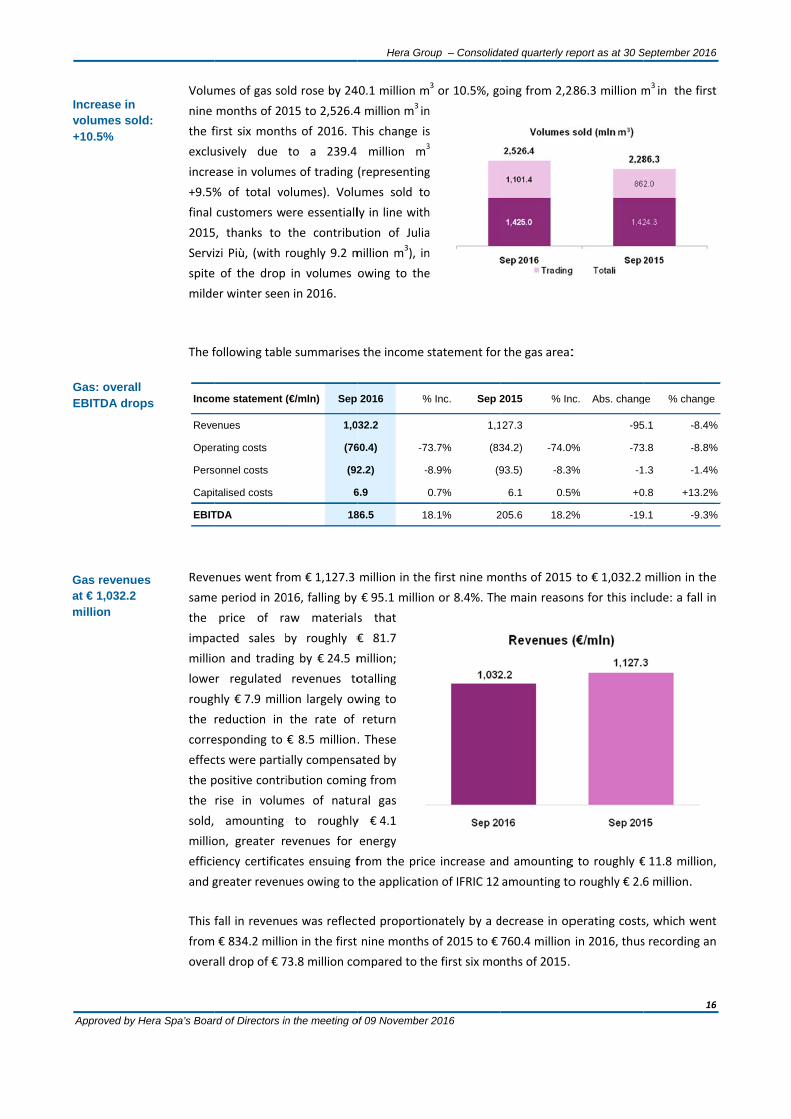

Increase in volumes sold+10.5%

Gas revenueat € 1,032.2 million

Gas: overall EBITDA drop

Hera Spa’s Boar

Volum

nine

the f

exclu

incre

+9.5%

final

2015

Servi

spite

milde

The f

Reve

same

the

impa

millio

lowe

roug

the

corre

effec

the p

the

sold,

millio

effici

and g

This f

from

overa

Inco

Reve

Oper

Pers

Capi

EBIT

d:

es

ps

rd of Directors in

mes of gas so

months of 20

first six month

usively due

ease in volume

% of total vo

customers w

5, thanks to

zi Più, (with

of the drop

er winter seen

following tabl

enues went fro

e period in 20

price of ra

acted sales b

on and tradin

r regulated

hly € 7.9 milli

reduction in

esponding to

cts were partia

positive contri

rise in volum

amounting

on, greater r

ency certifica

greater reven

fall in revenu

€ 834.2 millio

all drop of € 7

me statement (

enues

rating costs

onnel costs

talised costs

TDA

n the meeting o

old rose by 24

015 to 2,526.4

hs of 2016. T

to a 239.4

es of trading

olumes). Volu

ere essentiall

the contribu

roughly 9.2 m

in volumes o

n in 2016.

e summarises

om € 1,127.3

016, falling by

aw materials

by roughly €

ng by € 24.5 m

revenues to

ion largely ow

the rate of

€ 8.5 million.

ally compensa

ibution comin

mes of natur

to roughly

evenues for

ates ensuing f

ues owing to t

es was reflect

on in the first

73.8 million co

(€/mln) Sep

1,0

(76

(92

6

18

Hera Gro

of 09 November

40.1 million m

4 million m3 in

This change is

million m3

(representing

umes sold to

ly in line with

ution of Julia

million m3), in

owing to the

s the income s

million in the

€ 95.1 million

s that

€ 81.7

million;

otalling

wing to

return

. These

ated by

ng from

ral gas

y € 4.1

energy

from the pric

the applicatio

ted proportio

nine months

ompared to th

2016 %

32.2

60.4) -73

2.2) -8

6.9 0

86.5 18

oup – Consolida

2016

3 or 10.5%, go

n

s 3

g

o

h

a

n

e

statement for

e first nine mo

n or 8.4%. Th

e increase an

on of IFRIC 12

onately by a d

of 2015 to €

he first six mo

% Inc. Sep 2

1,1

3.7% (83

8.9% (9

0.7%

8.1% 2

ated quarterly re

oing from 2,2

r the gas area:

onths of 2015

e main reason

nd amounting

amounting to

decrease in op

760.4 million

nths of 2015.

2015 % In

27.3

34.2) -74.0%

93.5) -8.3%

6.1 0.5%

205.6 18.2%

eport as at 30 S

286.3 million m

:

5 to € 1,032.2

ns for this inc

g to roughly €

o roughly € 2.6

perating costs

in 2016, thus

c. Abs. chang

-95

% -73

% -1

% +0

% -19

September 2016

16

m3 in the first

million in the

clude: a fall in

€ 11.8 million,

6 million.

s, which went

s recording an

ge % change

5.1 -8.4%

3.8 -8.8%

.3 -1.4%

0.8 +13.2%

9.1 -9.3%

6

6

t

e

n

,

t

n

%

%

%

%

%

G€

In

Nin€

Approved by H

Gas EBITDA: € 186.5 millio

nvestments r

Net investmenn the Gas Are64.1 million

Hera Spa’s Boar

EBITD

passi

mont

perio

tradi

servi

had a

At 30

area

gas

recor

regul

554/

a la

invol

to hi

and

netw

first

seen

to th

situa

Inves

€ 2.8

plant

Deta

Gas(€/m

Netw

RH/

Tota

Cap

Tota

n

ise

nts ea:

rd of Directors in

DA was down

ing from € 20

ths of 2015 to

od in 2016,

ng and lesse

ces, in which

an € 8.5 millio

0 September 2

amounted to

distribution,

rded, mainly

latory upgra

15 (priorly re

rge‐scale me

ved lower‐cla

gher non‐rou

plants, and

works in the P

three quarte

in requests f

he previous y

tion.

stments increa

8 million in re

t. New connec

ils of operatin

smln)

works and pla

Heat manage

al Gas Gross

pital contributio

al Gas Net

n the meeting o

n by € 19.1 m

05.6 million in

o € 186.5 milli

due to lesse

er revenues f

the reduced

on impact.

2016, investm

o € 64.1 millio

a € 4.3 milli

y caused b

ding pursuan

esolution 631

etre substitu

ass devices (G

tine maintena

cathodic p

Padua and Tri

ers of 2016 a

for new conne

year, an activ

ased by € 2.2

mote heating

ctions in remo

ng investment

nts

ment

ons

Hera Gro

of 09 November

million or 9.3%

n the first nin

ion in the sam

er earnings

from regulate

d rate of retu

ments in the g

on, up € 6.6 m

ion increase

by activities

nt to resolu

/13) consistin

ution which

G4‐G6), in add

ance on netw

rotection in

este areas. In

a slight drop

ections comp

vity which con

million in rem

g mainly invol

ote heating w

ts in the Gas A

Sep

4

1

6

6

oup – Consolida

2016

%,

ne

me

in

ed

rn

as

million over th

was

s in

ution

ng in

also

dition

works

gas

n the

was

pared

ntinues to fe

mote heating

ving the reva

ere in line wit

Area are as fol

p 2016 Se

48.9

15.2

64.1

0.0

64.1

ated quarterly re

he same perio

el the effects

and heat man

mping of Bolo

th the figures

llows:

ep 2015 Ab

44.6

13.0

57.6

0.1

57.5

eport as at 30 S

od in the prev

s of the over

nagement as w

ogna’s Barca

seen in the p

bs. change

+4.3

+2.2

+6.5

-0.1

+6.6

September 2016

17

vious year. In

rall economic

well, of which

cogeneration

revious year.

% change

+9.6%

+16.9%

+11.3%

-100.0%

+11.5%

6

7

n

c

h

n

EE4

Ec8

Approved by H

Electricity: increase in EBITDA

Contributionoverall EBIT+4.6%

Electricity areEBITDA grow43.4%

Electricity customers rea863.8 thousan

Hera Spa’s Boar

1.02

In th

perce

defin

imple

capit

on re

nine

tariff

Note

busin

in pa

€ 10

regar

The f

The

2.3%

grow

confi

main

activ

(€/m

Area

Grou

Perc

n to TDA:

ea ws by

ach nd

rd of Directors in

.02 ELECTR

he first nine m

entage of Gro

ned 2016 as

emented, wh

tal for infrastr

evenues and

months of th

fary adjustme

e that a pro fo

ness of indust

ragraph 1.02.

million in rev

rding investm

following tabl

number of e

% (19.4 thous

wth in the fre

irming the gro

nly due to a

ities.

mln)

a EBITDA

up EBITDA

centage weight

n the meeting o

RICITY

months of 20

oup EBITDA. T

the first ye

ich modified

ructure servic

EBITDA, owin

e year. Reven

nt return and

orma version

trial cogenera

. The effect of

venues, € 7.5

ents, the recla

e shows the c

electricity cus

sand) increas

ee market, w

owth trend se

a reinforceme

t

Hera Gro

of 09 November

016, the Elec

These results a

ear in which

the method

ces in the elec

ng solely to th

nues as at 30

amortisation

of the 2015 d

ation from the

f this reclassif

5 million in o

assification co

changes occur

stomers reco

se, mainly d

which came to

een in recent

ent of comm

Sep

oup – Consolida

2016

ctricity Area g

are to be cons

h resolution

used in calc

ctricity sector

he rate of ret

September 2

n of investmen

data is provid

e electricity ar

fication amou

perating cost

omes to € 1.5

rred in terms o

rded a

due to

o 9.3%

t years,

mercial

p 2016

104.3

650.6

16.0%

ated quarterly re

grew in both

sidered within

583/2015/R/

ulating the ra

. The negative

turn, came to

016 furtherm

nts, in light of

ded as part of

rea to the gas

nts to € 2 mil

s and € 0.5 m

million.

of EBITDA:

Sep 2015 A

72.7

640.2

11.4%

eport as at 30 S

absolute ter

n a regulatory

/com of 02/1

ate of return

e impact of t

o € 2.2 million

more include t

resolution 65

f the reclassif

s area, as furt

lion in EBITDA

million in per

Abs. change

+31.6

+10.4

+4.6 p.p.

September 2016

18

rms and as a

y context that

12/2015 was

n on invested

his resolution

n for the first

he effect of a

54/15/R/eel.

ication of the

ther specified

A, made up of

rsonnel costs;

% chang

+43.4

+1.6

6

8

a

t

s

d

n

t

a

e

d

f

;

ge

4%

6%

Vs

€ inre

EleEBinc43.

Approved by H

Volumes soldslightly, by 0.

1,075.5 millioelectricity

evenues

ectricity: ITDA

creases by 4%

Hera Spa’s Boar

Volum

7,245

2015

perio

0.2%

due

activ

acqu

in o

activ

last r

The f

Reve

€ 1,0

millio

are:

Natio

avera

whic

reven

reven

regul

servi

rate

conta

price

therm

Oper

decre

Inco

Reve

Ope

Pers

Cap

EBIT

d drop .2%

on

rd of Directors in

mes of electr

5.6 GWh in th

5 to 7,233.7

od of 2016, w

%. This trend

to a red

ities, com

isitions on th

order to re

ities and incr

resort custom

following tabl

enues decreas

075.5 million i

on. The main

a fall in the

onwide Price

age compare

h caused € 4

nues, € 64 m

nues and €

lated reven

ces, an effect

of return. Th

ained by both

e increase, fo

moelectric pla

rating costs fe

ease in revenu

ome statement

enues

rating costs

sonnel costs

italised costs

TDA

n the meeting o

ricity sold we

he first nine m

GWh in th

with a slight

in volumes is

uction in

mpensated

e free market

einforce com

ease volumes

ers.

e summarises

sed by 6.3%, p

in the same p

reasons for t

e price of e

e) coming to

d to the pre

40 million in

million in les

€ 2.2 million

nues for

t of the reduc

ese effects w

h higher reve

or roughly € 2

ants, coming t

ell by € 107.8

ues for the low

t (€/mln) Se

1

(

Hera Gro

of 09 November

ent from

months of

he same

drop of

s mainly

reselling

greater

t, mainly

mmercial

s sold to

s the income s

passing from

period in 201

this decrease

energy (Pun,

o 27.6% on

evious year,

lesser sales

sser trading

n in lesser

distribution

ction of the

were partially

enues for ene

2.1 million, a

to roughly € 4

8 million or 1

wer cost of ra

ep 2016 %

1,075.5

(939.0) -87

(37.5) -3

5.3 0

104.3 9

oup – Consolida

2016

statement for

€ 1,147.8 mil

16, and thus s

ergy efficiency

and by great

million.

10.3%; this fi

aw materials.

% Inc. Sep

1,

7.3% (1,0

3.5% (

0.5%

9.7%

ated quarterly re

r the area:

lion in the fir

showing an ov

y certificates,

er revenues

gure is propo

2015 % Inc

147.8

046.8) -91.2%

(33.9) -3.0%

5.5 0.5%

72.7 6.3%

eport as at 30 S

rst nine mont

verall reducti

, mainly ensu

for energy p

ortionally hig

. Abs.change

-72.

% -107.

% +3.

% -0.2

% +31.

September 2016

19

hs of 2015 to

ion of € 72.3

uing from the

production in

gher than the

e % change

3 -6.3%

8 -10.3%

6 +10.6%

2 -3.6%

6 +43.4%

6

9

o

3

e

n

e

%

%

%

%

%

EleEBmil

A

Approved by H

ectricity ITDA at € 104llion

Net investmein the ElectriArea: € 16.6 million

Hera Spa’s Boar

At th

EBITD

going

2015

highe

highe

due

dispa

parti

reven

Inves

€ 1.5

seen

carrie

main

surro

Goriz

previ

routi

conc

in Im

Requ

comp

year.

The

Elet(€/m

Netw

Tota

Cap

Tota

4.3

ents city

rd of Directors in

he end of the f

DA rose by

g from € 72.7

5 to € 104.3 m

er margins

er margins i

to the po

atching servic

ally reduced

nues in the re

stments made

million com

in the previo

ed out ma

ntenance of p

ounding Mod

zia. Compared

ious year, a

ne mainten

erning interve

mola.

uests for new

pared of the s

.

details of op

ricity mln)

works and plan

al Electricty Gr

ital contribution

al Electricity N

n the meeting o

first nine mon

€ 31.6 million

7 million at 30

million in 201

on sales ac

n electricity

ositive perfo

ces. These e

by € 2.2 mill

gulated distri

e in the Elect

pared to the

ous year. The

inly concern

lants and grid

dena, Imola,

d to the same

higher amo

ance was

entions on th

w connections

same period i

perating inves

ts

ross

ns

Net

Hera Gro

of 09 November

nths of 2016,

n or 43.4%,

0 September

16, thanks to

ctivities and

production,

ormance of

effects were

ion in lesser

bution service

tricity Area ca

€ 15.1 millio

e intervention

n non‐routin

ds in the area

, Trieste an

e period in th

ount of non

seen, main

he Cogen plan

s grew slight

in the previou

stments in th

oup – Consolida

2016

e, owing to th

ame to € 16.6

on

ns

ne

as

nd

he

n‐

ly

nt

ly

us

he electricity

Sep 2016

16.7

16.7

0.0

16.6

ated quarterly re

he fall in the ra

6 million at S

area are as

Sep 2015

15.1

15.1

0.0

15.1

eport as at 30 S

ate of return.

September 20

follows:

Abs. change

+1.6

+1.6

+0.0

+1.5

September 2016

20

016, rising by

% change

+10.6%

+10.6%

+0.0%

+9.9%

6

0

y

Approved by H

Integrated WCycle: slight

Water CycleEBITDA falls0.6%

ContributionEBITDA: dow0.6%

Hera Spa’s Boar

1.02

Over

drop

as th

meth

invo

reve

amo

The f

Area

Grou

Perc

Water t drop

e Area s by

n to wn

rd of Directors in

.03 INTEGR

r the first nin

p compared t

he absolute v

hod defined

lving in a red

nues and EB

unts to € 14

following tab

a EBITDA

up EBITDA

centage weight

n the meeting o

RATED WAT

ne months of

to the same

value of this

by the AEEG

duction in th

BITDA, resulti

.9 million for

ble shows th

(€/mln

Hera Gro

of 09 November

TER CYCLE

f 2016, the in

period in 20

single busine

GSI for 2016‐

e rate of ret

ing from the

r the first nin

he changes o

n) Sep 2

1

6

26

oup – Consolida

2016

E

ntegrated wa

15, both as a

ess area. 201

2019 (resolu

urn. The reso

e rate of retu

ne months o

ccurred in te

2016 Se

173.7

650.6

6.7%

ated quarterly re

ater cycle ar

a contributio

16 is the first

ution 664/20

olution’s neg

rn and the re

f 2016.

erms of EBIT

ep 2015 A

174.7

640.2

27.3%

eport as at 30 S

rea recorded

on to Group

t year in whi

015) takes eff

gative impac

estriction on

DA:

bs.change

(1.0)

+10.4

-0.6 p.p.

September 2016

21

a slight

EBITDA and

ch the tariff

fect, largely

ct on

n revenues,

% change

(0.6%)

+1.6%

6

1

Approved by H

1.5 million WCycle custo

228.1 milliomanaged inaqueduct

Hera Spa’s Boar

The

settl

by 4

com

mon

the t

seen

the G

area

resp

this g

The

Volu

purif

trend

with

cons

indic

equa

inde

Water mers

on m3 n the

rd of Directors in

number of w

ed at 1.5 mi

.2 thousand

pared to the

nths of 2015

trend of orga

n across the a

Group. The E

managed by

onsible for t

growth, than

main quantit

umes dispens

fication, show

d is tied to c

respect to s

sumption. Vo

cator of activ

alisation purs

pendently o

n the meeting o

water custom

llion, increas

(+0.3%)

e first nine

and confirm

anic growth

areas served

Emilia Romag

y Hera Spa is

he majority

nks to a sligh

tative indica

sed through

wed a slight

limatic facto

seasonal ave

olumes distri

vities in the g

suant to regu

f volumes di

Hera Gro

of 09 November

mers

sing

ing

d by

gna

s

of

ht recovery in

tors of the a

the aqueduc

decline com

ors in early su

rages, and a

ibuted, follow

geographical

ulations that

stributed.

oup – Consolida

2016

n the numbe

area are as fo

ct, along with

mpared to the

ummer 2016

minor decre

wing AEEGSI

l areas serve

t call for a re

ated quarterly re

er of new con

ollows:

h volumes of

e first nine m

6, i.e. particu

ease in both

resolution 6

d by the Gro

gulated reve

eport as at 30 S

nnections.

f sewerage a

months of 20

larly heavy p

industrial an

664/2015, ar

oup and are s

enue to be re

September 2016

22

and

15; this

precipitation

nd domestic

re an

subject to

ecognised

6

2

InCyin

Em

Wr€

Approved by H

tegrated Watycle: slight fa EBITDA

EBITDA at € 1million

Water Cycle revenues at € 594.4 million

Hera Spa’s Boar

The t

Reve

2016

0.8%

in 20

2015

main

millio

distr

in th

millio

the r

costs

millio

from

cont

Oper

elect

EBIT

€ 1.0

€ 17

mon

in 20

in les

caus

of re

restr

com

high

Inco

Reve

Oper

Pers

Capi

EBIT

ter all

73.7

n

rd of Directors in

table below

enues for the

6 showed a s

% with respec

015, going fro

5 to € 594.4 m

n reasons for

on in lower r

ribution, owi

e rate of ret

on, due to th

restriction on

s acknowled

on in higher

m connection

tributed with

rating costs f

tricity for pla

DA saw a slig

0 million, or 0

4.7 million in

nths of 2015 t

016. This is d

sser revenue

sed by the de

eturn and the

riction on rev

pensated by

er revenues

me statement (

enues

rating costs

onnel costs

talised costs

TDA

n the meeting o

synthesises

e first nine m

slight decrea

ct to the sam

om € 599.1 m

million in 20

r this include

revenues for

ng to the red

urn, and € 1

he reformula

n revenues, o

ged by the A

revenues fo

s and from t

h € 1.8 millio

fell by € 6.2

ants, lower o

ght decrease

0.6%, passin

n the first nin

to € 173.7 m

ue to € 10.9

es for dispen

ecrease in th

e newly defin

venues, large

y lower opera

from new co

(€/mln) Sep

5

(3

(1

1

Hera Gro

of 09 November

the income

months of

se, down

me period

million in

016. The

e € 10.9

r

duction

4.9

ation of

only partially

Authority. Th

or subcontrac

the applicatio

n.

million or 2.0

operating cos

e of

g from

ne

million

million

nsing

e rate

ned

ely

ating and str

onnections.

p 2016 % I

94.4 -

06.0) -51.

17.2) -19.

2.6 0.4

73.7 29.2

oup – Consolida

2016

statement fo

y compensat

his drop was

cted works, a

on of accoun

0%, largely o

sts and lesse

ructural costs

nc. Sep 20

- 599.1

5% (312.2

7% (114.7

4% 2.5

2% 174.7

ated quarterly re

or the water

ted by highe

partially com

as well as hig

nting princip

on account o

r expenses e

s, subcontra

015 % Inc.

1 -

2) -52.1%

7) -19.2%

0.4%

7 29.2%

eport as at 30 S

r area:

r revenues c

mpensated b

gher revenue

le IFRIC 12, w

of the lower c

employed fo

cting activiti

Abs. change

(4.7)

(6.2)

+2.5

+0.1

(1.0)

September 2016

23

covering

by € 1.6

es coming

which

cost of

r structures.

es and

e % change

(0.8%)

(2.0%)

+2.2%

+4.0%

(0.6%)

6

3

NinW€

Approved by H

Net investmenn the Integrat

Water Cycle A82.7 million

Hera Spa’s Boar

Inves

Cycle

millio

year

inves

€ 93

main

recla

upgr

upgr

purif

Inves

€ 20

Amo

netw

trans

wate

Prot

in pu

on th

purif

work

Requ

prev

in th

Capi

com

prev

nts ted Area:

rd of Directors in

stments in th

e Area amou

on, in line w

. Including ca

stments in th

.1 million. Th

nly concerne

amations and

rading, in add

rades which

fication and

stments tota

.9 million in

ong the more

works in the h

sportation ro

er system; in

ection Plan,

urification, th

he Cattolica

fication plan

ks in upgradi

uests for new

vious year, re

e constructi

tal grants am

ponent of th

vious year by

n the meeting o

he Integrate

unted to € 82

ith the previ

apital grants

his area cam

he interventi

d extensions

d network an

dition to reg

largely involv

sewerage.

alled € 44.9 m

purification.

e significant w

historical cen

oute “Crealis

sewerage, c

in addition t

he creation o

purifier, reva

t in Bologna

ing the large

w water and

emaining rath

on sector.

mounting to €

he New Inves

y € 1.6 million

Hera Gro

of 09 November

d Water

2.7

ious

s,

me to

ions

s,

nd plant

gulatory

ved

million in the

.

works, note:

ntre of Bolog

s”, and an up

continued pr

to redevelop

of the head t

amping of th

and, in the a

e purification

sewerage co

her low none

€ 10.4 millio

stments Fun

n, in spite of

oup – Consolida

2016

e aqueduct, €

: in the aque

gna which ac

pgrading of in

rogress in wo

pment of the

tank of the R

he oxygen pr

areas served

plants in Se

onnections r

etheless, com

on included €

d (FoNI), and

a reduced a

ated quarterly re

€ 27.3 millio

duct, an upg

ccompanied

nterconnecti

orks for the R

sewerage ne

Riccione purif

oduction fac

d by AcegasA

rvola, Cà No

ose by € 1.3

mpared to th

€ 4.2 million

d increased o

mount comi

eport as at 30 S

n in sewerag

grading of wa

the creation

ions in the M

Rimini Seawa

etwork in ot

fication plan

cility in the Id

ApsAmga, con

ordio and Aba

million over

he pre‐crisis

pertaining to

overall comp

ing from the

September 2016

24

ge and

ater

n of the

Modena

ater

her areas;

nt, upgrading

dar

ntinued

ano Terme.

r the

conditions

o the tariff

pared to the

FoNI.

6

4

g

Hera Group – Consolidated quarterly report as at 30 September 2016

25

Approved by Hera Spa’s Board of Directors in the meeting of 09 November 2016

Details of operating investments in the Integrated Water Cycle Area are as follows:

Water Cycle Area(€/mln)

Sep 2016 Sep 2015 Abs.change % change

Aqueduct 44.9 43.3 +1.6 +3.7%

Purification 20.9 22.6 -1.7 -7.5%

Sewage 27.3 25.7 +1.6 +6.2%

Total Water Cycle Gross 93.1 91.6 +1.5 +1.6%

Capital contributions 10.4 8.8 +1.6 +18.2%

of which FoNI (New Investment Fund) 4.2 7.3 -3.1 -42.5%

Total Water Cycle Net 82.7 82.8 -0.1 -0.1%

WasManArestab

Approved by H

ste nagement

ea: EBITDA ble

Market wast+18.4%

Hera Spa’s Boar

1.02

In th

came

2015

The f

Volum

An an

in co

acqu

mana

in so

tonn

(€/m

Area

Grou

Perc

Quan

Urba

Mark

Wast

Plant

Wast

te:

rd of Directors in

.04 WASTE

e first nine m

e to 26.5%, wi

5.

following tabl

mes markete

nalysis of the

ommercial wa

isitions of W

agement of in

rted waste w

es. The increa

mln)

a EBITDA

up EBITDA

centage weight

ntitative data (th

n waste

ket waste

te marketed

t by-products

te treated by typ

n the meeting o

E MANAGEM

months of 201

ith a sector EB

e shows the c

d and treated

volumes trea

ste coming to

aste Recyclin

ndustrial wast

which compens

ase in by‐prod

t

housand of tonn

pe

Hera Gro

of 09 November

MENT

16, the waste

BITDA that rem

changes occur

d by the Gro

ted shows a 9

o 18.4%. This

g and the Ge

te. Urban was

sated for the

ducts is mainly

nes)

oup – Consolida

2016

e managemen

mained funda

rred in terms o

up in the firs

9.0% increase

s growth is ac

eonova plants

ste remained

drop in stran

y due to the co

Sep 201

172.

650.

26.5%

Sep 2016

1,533.4

1,747.6

3,281.0

1,869.8

5,150.9

ated quarterly re

nt area’s cont

amentally in lin

of EBITDA:

st nine month

in waste mar

ccounted for a

s, which gave

in line with 2

nd waste, whi

ompany merg

6 Sep 2015

2 172.5

6 640.2

% 26.9%

Sep 2015

1,533.0

1,476.2

3,009.2

1,717.2

4,726.4

eport as at 30 S

tribution to G

ne with the sa

hs of 2016 ar

rketed, mainly

above all by t

e a significant

2015 thanks t

ich came to 1

gers mentione

Abs. change

-0.3

+10.4

-0.4 p.p

Abs. change

+0.4

+271.4

+271.8

+152.6

+424.5

September 2016

26

Group EBITDA

ame period in

re as follows:

y due to a rise

the late‐2015

t impetus to

o an increase

12.3 thousand

ed above.

e %change

3 -0.2%

4 +1.6%

p.

% change

+0.0%

+18.4%

+9.0%

+8.9%

+9.0%

6

6

A

n

:

e

5

o

e

d

Shus

+w

Approved by H

harp drop in tse of landfills

+0.9% in sortwaste

Hera Spa’s Boar

Sorte

furth

to 5

expa

perce

to e

first

wast

by H

by

confi

of st

the T

The H

and d

/dige

comp

conta

Quan

Land

Wast

Selec

Com

Stabi

Othe

Wast

the

ted

rd of Directors in

ed urban

her progress,

5.8% primari

nsion proje

entages of ov

nvironmental

nine months

e grew by 0.5

era Spa, by 2

Marche M

irmed in 2016

trong growth

Triveneto regio

Hera Group o

disposal plant

esters and 9

panies Biogas

aining a few p

ntitative data (tho

dfills

te-to-energy plan

cting plant and o

posting and stab

ilisation and che

er plants

te treated by plan

n the meeting o

waste reco

rising from 5

ly thanks to

cts. These

erall recovery

l benefits. In

s of 2016, s

5% in areas se

2% in areas se

Multiservizi

6 as well the t

seen in are

on, up 2.6%.

operates in th

ts, the most im

selecting pla

2015 and Wa

plants.

ousand of tonnes

nts

other

bilisation plants

mical-physical p

nt

Hera Gro

of 09 November

orded

54.9%

new

high

y lead

n the

orted

erved

erved

and

trend

eas of

he entire wast

mportant of w

nts. Note tha

ste Recycling

) Se

5

1

4

2

lants 8

2

5

oup – Consolida

2016

te cycle, with

which are: 10

at towards th

were purcha

ep 2016 Se

573.4 6

,009.8 1

406.1 3

291.7 3

849.5 9

,020.4 1

,150.9 4

ated quarterly re

83 urban an

waste to ene

he end of th

sed, along wit

ep 2015 Abs

685.3 -

,021.6

329.5

340.8

903.5

,445.7 +

4,726.4 +

eport as at 30 S

d special was

ergy plants, 1

e 2015 finan

th the branch

s.change %

-111.9 -

-11.8

+76.6 +

-49.1 -

-54.0

+574.7 +

+424.5

September 2016

27

ste treatment

1 composters

ncial year the

h of Geo Nova

%change

-16.3%

-1.2%

+23.2%

-14.4%

-6.0%

+39.8%

+9.0%

6

7

t

s

e

a

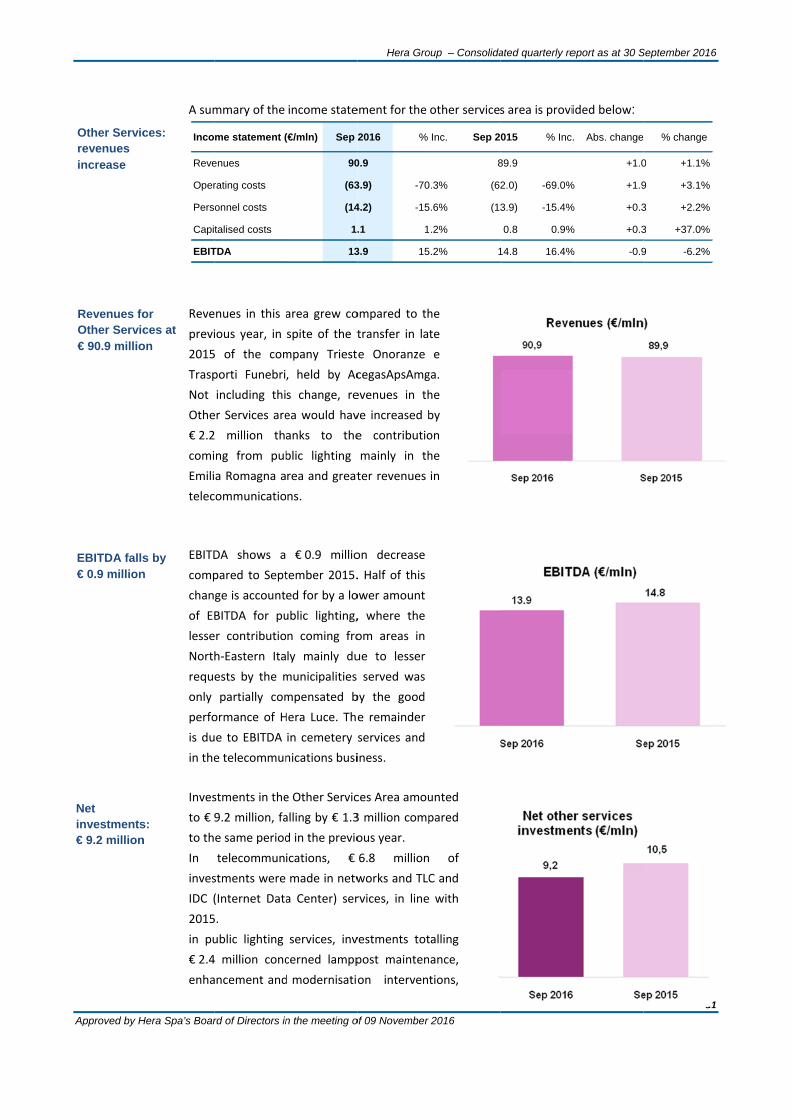

Approved by H

Waste managemenEBITDA stab

Waste Managemenrevenues at € 727.6 milli

Waste managemeEBITDA at € 172.2 mill

Hera Spa’s Boar

Wast

expla

Recy

had a

The

Reve

2016

€ 679

2015

2016

volum

statin

recor

in u

amou

effec

decre

plant

Oper

line w

of t

certif

EBITD

of 20

a fall

to th

and e

the h

enha

swee

Inco

Reve

Oper

Pers

Capi

EBIT

nt: ble

nt

on

ent

lion

rd of Directors in

te treatment

ained by the

cling, and an

already been s

table below

enues rose in

6 by 7.1% or

9.3 million in

5 to € 727.6 m

6. This growt

mes treated,

ng energy inc

rded as lesser

urban hygien

unt of service

cts were part

ease in the C

ts.

rating costs fo

with the rise i

the new m

ficated, as des

DA went from

015 to € 172.2

of € 0.3 millio

he lower price

energy certific

higher volum

ancing action

eping.

ome statement

enues

rating costs

sonnel costs

talised costs

TDA

n the meeting o

increased by

higher volum

increase in in

seen througho

w summarises

n the first ni

€ 48.3 millio