Embed Size (px)

Citation preview

VERTEX SECURITIES LIMITED

VERTEX-COMPANY PROFILE

• VERTEX is a premier brokerage house in India on the fast growth track.• Vertex started functioning in the

stock market in 1993.• VERTEX Group, a leading financial

and investment service company in India. –Vertex Securities Ltd–Vertex Commodities &Finpro (P)Ltd.

VERTEX is a member of the National Stock Exchange of India (NSE), the Bombay Stock Exchange, the National Commodities Derivatives Exchange Ltd (NCDEX), and Multi Commodity Exchange of India (MCX). VERTEX is a full-fledged depository participant of the National Securities Depository Ltd.

VARIOUS DEPARTMENTS

• BACKOFFICE DEPARTMENT• TRADING DEPARTMENT• ADMIN DEPARTMENT

BACKOFFICE DEAPRTMENT

• FUNDAMENTAL NEEDS TO PARTICIPATE– DEMAT ACCOUNT– TRADING ACCOUNT

• QUERIES REGARDING PARTICIPATING IN STOCK EXCHANGE

• HANDLING THE ACCOUNTS OF A COMPANY

• KYC

TRADING DEPARTMENT

• ACTUAL TRADING TAKES PLACE• TRADING – EQUITIES AND

COMMODITIES• OPTION : STOP LOSS• ODIN CLIENT SOFTWARE

ADMIN DEPARTMENT

• Client transaction management • Brokerage • Client management

AVENUES OF INVESTMENT

• STOCK MARKET FUNDAMENTAL ANALYSIS TECHNICAL ANALYSIS• COMMODITIES MARKET

9

FUNDAMENTAL

ANALYSIS

10

• Fundamental analysis is the technique of applying the tenets of the firm foundation theory to the selection of individual stocks

11

About company

• TCS • HCL• Infosys• Tech mahindra• Wipro

12

Parameters used

• EPS• P/E ratio• PEG ratio• P/s ratio• P/b Ratio• Return on net worth• Dividend pay-out ratio

13

• EPS = Earnings/(No of shares)• P/E ratio = Martketprice/(EPS)• PEG ratio= P/E / (projected growth in

earnings• p/s ratio = Market Cap / Revenues• P/B ratio = Marketprice/(book value)• ReturnNetworth = Net income aftertax

/(networth)• DYR = Divident/(share price)

FORMULAS

14

Company

EPS p/e ratio

Book value

p/b ratio

Peg ratio

p/s ratio

Dividend payout ratio (in %)

Return on net worth

Market price( in july)

TCS 102.6 24.51 224.90

11.19 1.39 5.37 1.27 48.2 2516.45

Wipro 32.8 16.35 118.98

4.50 1.18 3.08 1.31 27.6 536

Infosys

185.7 17.99 733.03

4.56 1.25 252.94

1.89 26.1 3341.3

HCL 85.44 17.74 146.09

10.37 1.28 191.22

0.79 44 1515.55

Tech mahindra

111.28

19.12 365.81

5.81 1.06 2.74 0.94 42.1 2127.25

15

OBSERVATION

• Infosys Earnings capabilities more then Tech mahindra and TCS.

• High P/B ratio determine the price premium– TCS>HCL>Tech Mahindra

• ROE : TCS> HCL> Techmahindra• Low dividend pay-out – HCL , Tech mahindra• Industrial P/E -> 22.13– TCS is more– Tech Mahindra is close to

Industrial P/E

16

Compay EPS p/eratio

Bookvalue

p/bratio

Dividentpayoutratio(%)

Returnon networth

Marketprice( injul)

BAJAJ AUTO

112.1618.90

332.046.38

450%38.51

2121.65

MARUTI SUZUKI INDIA

96.4527.15

707.163.70 160%

12.87 2622.60

MRF 1803.9512.99

8594.712.73

250%20.02

23434.35

BOSCH 302.94

44.73

2004.62 6.74 550%14.05 13630.45

FUNDAMENTAL ANALYSIS OF AUTOMOBILE INDUSTRY

17

TECHNICAL ANALYSIS

18

PARAMETERS USED

• Value at Risk• Relative Strength Index

19

COMPANIES

• MRF• TIDE WATER OIL• STRIDES AROCLAB• LASKHMI MILL• BOSCH• JK BANK• SHREE CEMENT• GODREY PHILIP• UB HOLDINGS• INFOSYS

20

VALUEAT

RISK

21

What is value at risk?

• Value-at-Risk analyses provide the risk manager with a single measurement of the risk faced by that institution at a particular time.

• The Value-at-Risk is the maximum loss that the institution is likely to face within a given time period with (usually) a 95% probability.

22

Methods of calculating VaR

• Variance – covariance• Historic • Monte Carlo simulation

23

Formula

VaR(95%) = p * σ * z

P=price of the shareσ=standard deviation

Z=Z value

24

For example

An MRF stock is trading at Rs.23050 with a one-year standard deviation of 20%

In the normal distribution, 95% confidence level is 1.645standard deviations away from the mean.

Therefore, our VaR at 95% confidence level will be:

VaR(95%) = 23050*0.20*1.645 = 7583.45

25

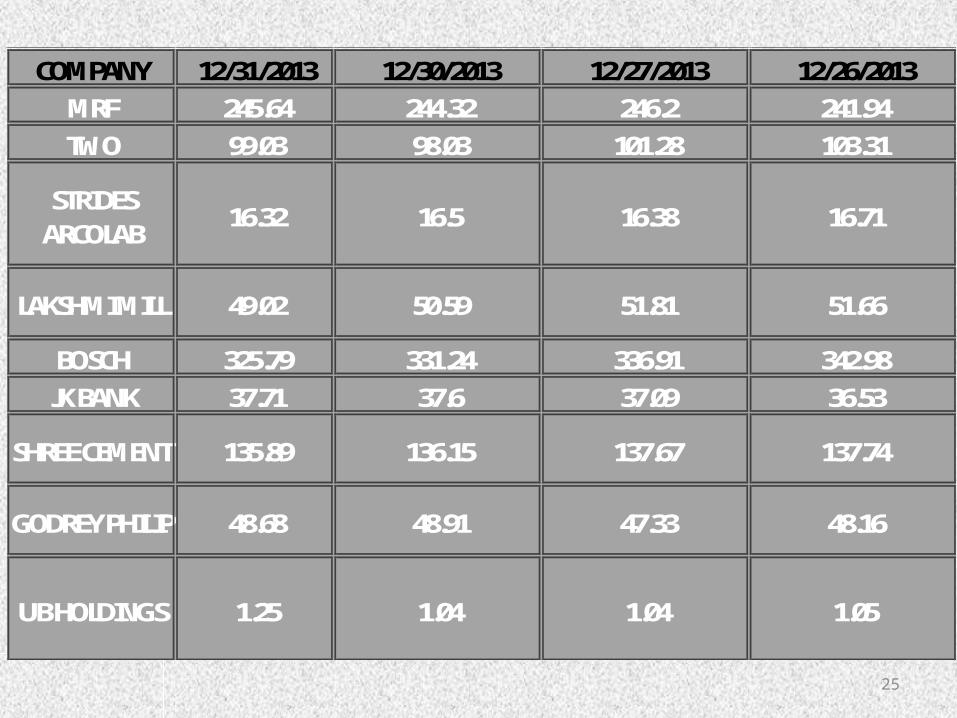

COMPANY 12/31/2013 12/30/2013 12/27/2013 12/26/2013MRF 245.64 244.32 246.2 241.94TWO 99.03 98.03 101.28 103.31

STRIDES ARCOLAB

16.32 16.5 16.38 16.71

LAKSHMI MILL 49.02 50.59 51.81 51.66

BOSCH 325.79 331.24 336.91 342.98JK BANK 37.71 37.6 37.09 36.53

SHREE CEMENT 135.89 136.15 137.67 137.74

GODREY PHILIP 48.68 48.91 47.33 48.16

UB HOLDINGS 1.25 1.04 1.04 1.05

26

RELATIVE STRENGTH

INDEX

27

RELATIVE STRENGTH INDEX

• It is an oscillator used to identify the inherent technical strength and weakness of a particular scrip or market.

• A technical momentum indicator that compares the magnitude of recent gains to recent losses in an attempt to determine overbought and oversold conditions of an asset.

28

• The RSI can be calculated for any number of days depending on the wish of the technical analyst and the time frame trading adopted in a particular stock market.

• RSI is calculated for 5, 7, 9 and 14 days. If the time period taken for calculation is more, the possibility of getting wrong signals is reduced.

29

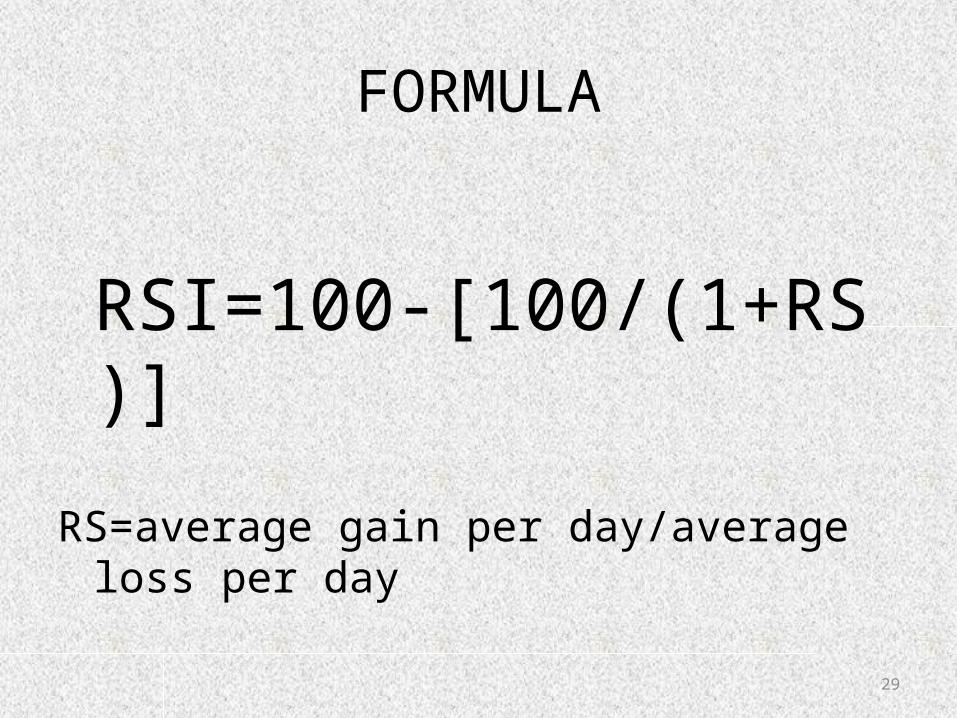

FORMULA

RSI=100-[100/(1+RS)]

RS=average gain per day/average loss per day

ExampleDATE PRICE CHANGE

1/3/2011 7356.4 01/4/2011 7406.8 50.41/5/2011 7326.85 -79.951/6/2011 7179.95 -146.91/7/2011 7059.65 -120.31/10/2011 6670.5 -389.151/11/2011 6596.85 -73.651/12/2011 6684.3 87.451/13/2011 6675.7 -8.61/14/2011 6579 -96.7

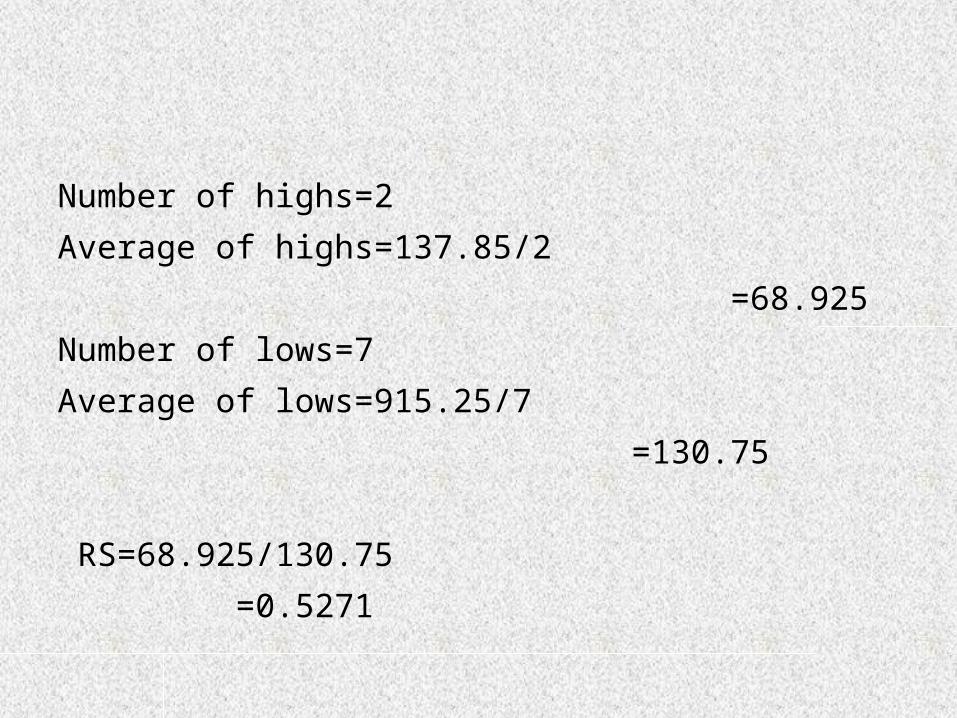

Number of highs=2 Average of highs=137.85/2 =68.925Number of lows=7Average of lows=915.25/7 =130.75

RS=68.925/130.75 =0.5271

• RSI=100-[100/(1+0.5271)] =34.5164

33

SERIAL NUMBER COMPANIES RELATIVE STRENGTH INDEX

1 MRF 44.20

2 TIDE WATER OIL 42.89

3 STRIDES ARCOLAB 49.94

4 LAKSHMI MILL 48.01

5 BOSCH 42.43

6 JK BANK 48.54

7 SHREE CEMENT 44.03

8 GODREY PHILIP 41.55

9 UB HOLDINGS 48.33

10 INFOSYS 49.22

34

INTERPRETATIONS

• 0-30 Buy mode• 40-70 (mean + standard deviation) above the mean – sell mode below the mean – buy mode• 70-100 Sell mode

35

GOLD INVESTMENT

S

36

OBJECTIVES OF THE STUDY

PRIMARY OBJECTIVE

To analyze the performance of the GOLD-ETF in national stock exchange (NSE) with reference to vertex securities.

SECONDARY OBJECTIVES

To find out the risk and correlation in between the gold ETF and commodity,spot market.To find out the best performing gold avenues in the capital market.To find out the long (buy) and short (sell) signal of the GOLD-ETF in NSE.To give suggestion to the investors regarding the investment of money in GOLD-ETF.

37

SAMPLING DESIGNA sample design is a definite plan for obtaining a sample from a given population. It refers to the technique of the procedure the researcher would adopt in selecting items for the sample. Sample design may as well lay down the number of items to be included in the sample i.e., the size of the sample. Sample size:The population of the study is 5 companies which involves in issuing of Gold ETF. Sample size is also 5.

SAMPLING METHOD Census Sampling is the sampling method used here. When the entire population is enumerated for sampling its known as census sampling.

PERIOD OF STUDY The period of the study is confined from 23rd June to 22nd july 2014 (4 weeks)

SAMPLING FRAME Gold Exchange Traded Fund.•SBI Mutual Fund - SBI Gold Exchange Traded Scheme – Growth Option•Kotak Mutual Fund - Gold Exchange Traded Fund•Axis Mutual Fund - Axis Gold ETF•Religare Mutual Fund - Religare Gold Exchange Traded Fund•Birla sunlife exchange traded fund

38

DEFINITION

EXCHANGE-TRADED FUND - ETFA security that tracks an index, a commodity or a basket of assets like an index fund, but trades like a stock on an exchange. ETFs experience price changes throughout the day as they are bought and sold.

Structure of ETF:

39

MCXMulti Commodity Exchange of India is a de-mutualised online commodity exchange of India promoted by Financial Technologies (I) Ltd, SBI, Fidelity International, NSE, NABARD, HDFC Bk, SBI Life Insurance Co., Union Bank of India, Canara Bank, Bank of India, Bank of Baroda and Corporation Bank.

Products

BullionsMetalsenergyOil & oil seedspulsesCerealsFibersPlantationsothers

40

S. No Parameter Jewellery Bank Gold ETF MCX-GOLD

1How Gold is held

Physical (Bars / Coins)

Physical (Bars / Coins)

Dematerialized (Electronic Form)

Dematerialized (Electronic Form)

2 Pricing

Differs from one to another. Neither transparent nor standard.

Differs from bank to bank. Not Standard.

Linked to International Gold Prices and very transparent.

Linked to International Gold Prices and very transparent.

3

Buying Premium above gold price

Likely to be more

Likely to be more Likely to be less

More in case of Physical delivery

4 Making ChargesCharges are incurred

Charges are incurred

No Charges are incurred

No Charges are incurred

5 Impurity Risk High Nil Nil Nil

6Storage Requirement Locker / Safe Locker / Safe Demat Account Demat Account

7Security of Asset

Investor is responsible

Investor is responsible

Fund House takes the responsibility

Fund House takes the responsibility

8 ResaleConditional and uneconomical

Banks do not buy back

At Secondary Market Prices

Not applicable after physical delivery

Overall comparison of means of Gold investment:

41

9Convenience in Buying / Selling

Less convenient, as Gold needs to be moved physically

Less convenient, as Gold needs to be moved physically

More Convenient, as held in electronic form under the demat account

More Convenient, as held in electronic form under the demat account

10Quantity to Buy / Sell

Available in standard denomination

Available in standard denomination

Minimum is ½ or 1 gram according to the fund

Minimum 10 grams

11 Bid Ask Spread Very High Can’t Sell Back Very Low

12 Risk of Theft Yes, possible Yes, possible No, Not possible No, Not possible

13 Wealth Tax Yes Yes No

14

Long Term Capital Gains Tax

Only after 3 years

Only after 3 years After 1 year

15 Delivery Centre Single Single Single Multiple

16 Market timings 10 AM-7AM 10 AM- 5PM 9 AM-3.30 PM 10 AM-11.55PM

42

Advantages of ETFs

•Tradable and Diversifiable•Low Cost•Transparency•Multiple Trading Strategies•Best during Bear markets•Convenience•Option Strategies•Passively Managed

Disadvantages of ETFs

•A new Market Concept•Large Investments•Brokerage Charges•Premiums and Discounts•Costly in Certain Situations

43

THANK YOU!!!