Embed Size (px)

Citation preview

Q3 2015 results presentation

2015-10-21

Summary, Q3 2015

• Continued trend of improved earnings– Operating income up 22% to SEK 405m (332)

– Operating margin improved 0.6 p.p. to 5.5%

• High margin divisions growing net sales, and Consumer Brands

mitigated impact from lower volumes

• Accelerated Improvement Program continues to

deliver successfully

• Increasingly challenging currency headwind

• Additional measures defined to mitigate currency impact

and to fund growth investments beyond 2016

2

Financial highlights Q3 2015, Group

• Unchanged sales (currency adjusted)– Higher in all divisions, except for Consumer Brands

• EBIT rose by 22% to SEK 405m (332)– Favorable mix driven by growth in watering

– Direct material cost reductions

– Adverse impact from lower production volumes

– Unfavorable EBIT currency impact of approx. SEK -60m

• Operating margin improved 0.6 p.p. to 5.5%

3

SEKm

Q3

2015

Q3

2014

As

reported Adjusted1

Jan-Sep

2015

Jan-Sep

2014

As

reported Adjusted1 LTM2

FY

2014

Net sales 7,307 6,785 8 0 30,498 27,515 11 -2 35,821 32,838

Gross margin, % 28.4 29.0 - - 29.1 28.9 - - 28.7 28.5

EBIT 405 332 22 26 3,192 2,613 22 12 2,160 1,581

Excl. impairment 405 332 22 26 3,192 2,613 22 12 2,927 2,348

EBIT margin, % 5.5 4.9 - - 10.5 9.5 - - 6.0 4.8

Excl. impairment, % 5.5 4.9 - - 10.5 9.5 - - 8.2 7.2

1 Adjusted for currency translation effects. 2 Last tw elve months rolling

% change, Q3 % change, 9M

Husqvarna Division Q3 2015

• Sales increased 3% (currency adjusted)– Increase driven mainly by snow-blowers in

North America

• EBIT and margin declined– Unfavorable mix

– Lower production volumes

– Adverse FX impact approx. SEK -30m

• Year-to-date positive EBIT and margin

development

4

SEKm

Q3

2015

Q3

2014

As

reported Adjusted1

Jan-Sep

2015

Jan-Sep

2014

As

reported Adjusted1 LTM2

FY

2014

Net sales 3,519 3,264 8 3 14,588 12,660 15 5 17,377 15,449

EBIT 321 432 -26 -24 2,219 1,917 16 10 2,310 2,008

EBIT margin, % 9.1 13.2 - - 15.2 15.1 - - 13.3 13.0

1 Adjusted for currency translation effects. 2 Last tw elve months rolling

% change, Q3 % change, 9M

Gardena Division Q3 2015

5

• Favorable weather in Central/Southern Europe

• Sales increased 19% (currency adjusted)

related to strong growth in watering

• Favorable scale impact and mix driven by the

growth in watering

• EBIT and margin rose substantially

SEKm

Q3

2015

Q3

2014

As

reported Adjusted1

Jan-Sep

2015

Jan-Sep

2014

As

reported Adjusted1 LTM2

FY

2014

Net sales 1,060 879 21 19 4,174 3,743 12 8 4,643 4,212

EBIT 113 -7 n/a n/a 714 569 25 21 528 383

EBIT margin, % 10.7 -0.8 - - 17.1 15.2 - - 11.4 9.1

1 Adjusted for currency translation effects. 2 Last tw elve months rolling

% change, Q3 % change, 9M

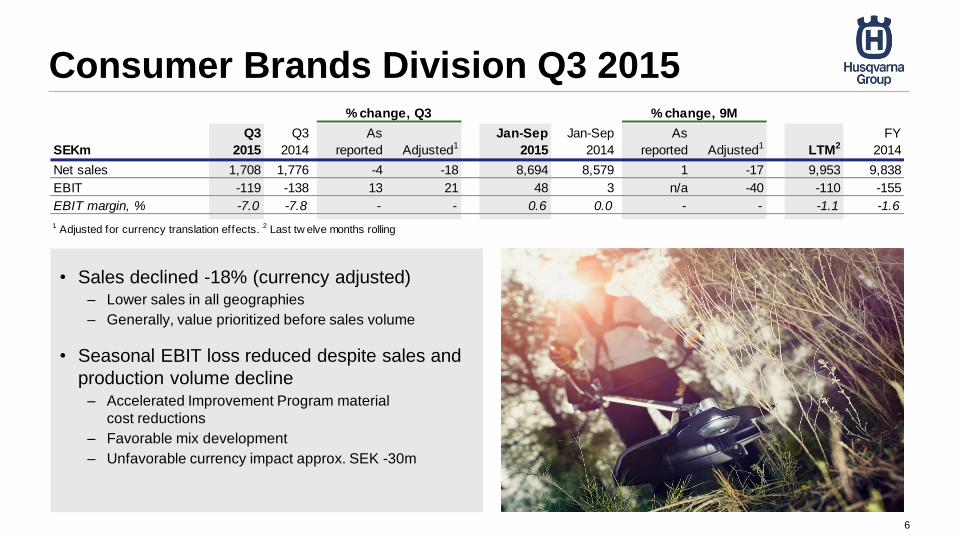

Consumer Brands Division Q3 2015

6

SEKm

Q3

2015

Q3

2014

As

reported Adjusted1

Jan-Sep

2015

Jan-Sep

2014

As

reported Adjusted1 LTM2

FY

2014

Net sales 1,708 1,776 -4 -18 8,694 8,579 1 -17 9,953 9,838

EBIT -119 -138 13 21 48 3 n/a -40 -110 -155

EBIT margin, % -7.0 -7.8 - - 0.6 0.0 - - -1.1 -1.6

1 Adjusted for currency translation effects. 2 Last tw elve months rolling

% change, Q3 % change, 9M

• Sales declined -18% (currency adjusted)– Lower sales in all geographies

– Generally, value prioritized before sales volume

• Seasonal EBIT loss reduced despite sales and

production volume decline– Accelerated Improvement Program material

cost reductions

– Favorable mix development

– Unfavorable currency impact approx. SEK -30m

Construction Division Q3 2015

7

• Sales increased 7% (currency adjusted)– Strong development in North America

– Slightly up, but mixed, in Europe

– Increase in rest of the world driven by Brazil and

Australia

• EBIT and margin increased– Sales volume impact

– Increased costs for sales and service resources

– Favorable currency impact

SEKm

Q3

2015

Q3

2014

As

reported Adjusted1

Jan-Sep

2015

Jan-Sep

2014

As

reported Adjusted1 LTM2

FY

2014

Net sales 1,020 866 18 7 3,042 2,533 20 6 3,848 3,339

EBIT 144 107 35 19 378 305 24 8 427 354

EBIT margin, % 14.1 12.4 - - 12.4 12.1 - - 11.1 10.6

1 Adjusted for currency translation effects. 2 Last tw elve months rolling

% change, Q3 % change, 9M

4%

5%

6%

7%

8%

9%

10%

0

500

1 000

1 500

2 000

2 500

3 000

3 500

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

EBIT rolling 12 months (SEKm)

EBIT margin rolling 12 months (%) as reported

EBIT margin rolling 12 months (%) FX adjusted*

SEKm

9.5%*

EBIT almost doubled since AIP launch

• The Accelerated Improvement Program; launched Q3

2013, activities ending in 2015 and full financial impact

realized 2016

• The program is delivering above expectations

– Purchasing, value engineering and SKU complexity reduction

– Selective growth in profit pool areas

• However, the Group faces ~1,3 p.p. margin headwind due

to changes in exchange rates since 2013

– So far, unfavorable FX translation impact on net sales

– In 2016 currency hedges will no longer offset unfavorable

transaction impact on EBIT

• Additional activities to secure cost reductions beyond the

AIP in 2016 and 2017

8* FX adjusted only for translation effect on sales.

8.2%

Main initiatives

• Continued direct material cost-out

• Indirect material costs, logistics costs

• Rightsizing of footprint

• SG&A efficiency

• Working capital improvements –Cash Conversion Cycle

Why?

• Mitigate FX headwind and support margin target

• Fund investments for future profitable growth

Further efficiency measures 2016-17

AIP

9

Gross profit development

10

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

Q1 Q2 Q3 Q4

Gross profit per quarter SEKm, Group

2013 2014 2015

Consolidated income statement

11

SEKm

Q3

2015

Q3

2014

Jan-Sep

2015

Jan-Sep

2014

FY

2014

Net sales 7,307 6,785 30,498 27,515 32,838

Cost of goods sold -5,232 -4,819 -21,630 -19,567 -23,488

Gross income 2,075 1,966 8,868 7,948 9,350

Gross margin, % 28.4 29.0 29.1 28.9 28.5

Selling expense -1,333 -1,306 -4,518 -4,344 -5,626

Administrative expense -350 -328 -1,171 -1,004 -1,392

Other operating income/expense 13 0 13 13 16

Impairment of goodwill - - - - -767

Operating income1 405 332 3,192 2,613 1,581

Operating margin, % 5.5 4.9 10.5 9.5 4.8

Financial items, net -83 -70 -277 -276 -325

Income after financial items 322 262 2,915 2,337 1,256

Margin, % 4.4 3.9 9.6 8.5 3.8

Income tax -126 -63 -788 -551 -432

Income for the period 196 199 2,127 1,786 824

Basic earnings per share, SEK 0.34 0.35 3.70 3.11 1.43

Diluted earnings per share, SEK 0.34 0.35 3.69 3.11 1.43

1Of which depreciation, amortization

and impairment-285 -238 -823 -707 -1,734

Consolidated balance sheet

12

SEKm

30 Sep

2015

30 Sep

2014

31 Dec

2014

Non-current assets 16,157 15,404 15,748

Inventories 7,188 6,577 7,709

Trade receivables 4,105 3,970 2,898

Other current assets 660 560 716

Liquid funds 2,231 2,316 2,105

Total assets 30,341 28,827 29,176

Total equity 13,229 12,816 12,088

Interest-bearing liabilities incl. dividend payable 7,151 7,167 7,504

Pension liabilities 1,746 1,599 1,835

Provisions 2,736 2,369 2,550

Trade payables 2,659 2,533 3,154

Other current liabilities 2,820 2,343 2,045

Total equity and liabilities 30,341 28,827 29,176

Operating cash flow

13

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

Q1 Q2 Q3 Q4

SEKm

2015

2014

2013

0.00

0.30

0.60

0.90

1.20

1.50

1.80

2.10

2.40

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

201

0 Q

3

201

0 Q

4

201

1 Q

1

201

1 Q

2

201

1 Q

3

201

1 Q

4

201

2 Q

1

201

2 Q

2

201

2 Q

3

201

2 Q

4

201

3 Q

1

201

3 Q

2

201

3 Q

3

201

3 Q

4

201

4 Q

1

201

4 Q

2

201

4 Q

3

201

4 Q

4

201

5 Q

1

201

5 Q

2

201

5 Q

3

Net Debt / EquitySEKm

Net debt

Equity

Net debt / equity

Net debt and equity

14

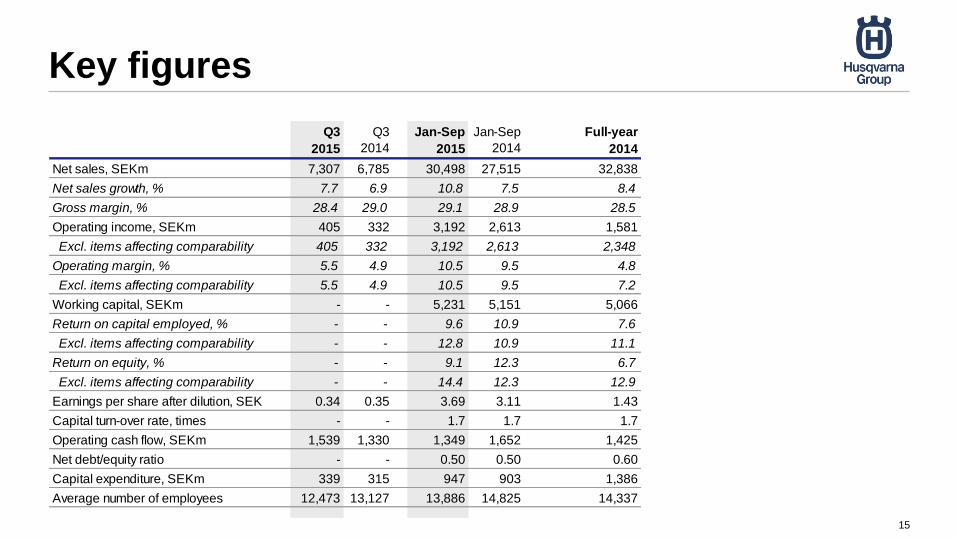

Key figures

15

Q3

2015

Q3

2014

Jan-Sep

2015

Jan-Sep

2014

Full-year

2014

Net sales, SEKm 7,307 6,785 30,498 27,515 32,838

Net sales growth, % 7.7 6.9 10.8 7.5 8.4

Gross margin, % 28.4 29.0 29.1 28.9 28.5

Operating income, SEKm 405 332 3,192 2,613 1,581

Excl. items affecting comparability 405 332 3,192 2,613 2,348

Operating margin, % 5.5 4.9 10.5 9.5 4.8

Excl. items affecting comparability 5.5 4.9 10.5 9.5 7.2

Working capital, SEKm - - 5,231 5,151 5,066

Return on capital employed, % - - 9.6 10.9 7.6

Excl. items affecting comparability - - 12.8 10.9 11.1

Return on equity, % - - 9.1 12.3 6.7

Excl. items affecting comparability - - 14.4 12.3 12.9

Earnings per share after dilution, SEK 0.34 0.35 3.69 3.11 1.43

Capital turn-over rate, times - - 1.7 1.7 1.7

Operating cash flow, SEKm 1,539 1,330 1,349 1,652 1,425

Net debt/equity ratio - - 0.50 0.50 0.60

Capital expenditure, SEKm 339 315 947 903 1,386

Average number of employees 12,473 13,127 13,886 14,825 14,337

Summary, Q3 2015

• Continued trend of improved earnings– Operating income up 22% to SEK 405m (332)

– Operating margin improved 0.6 p.p. to 5.5%

• High margin divisions growing net sales, and Consumer Brands

mitigated impact from lower volumes

• Accelerated Improvement Program continues to

deliver successfully

• Increasingly challenging currency headwind

• Additional measures defined to mitigate currency impact

and to fund growth investments beyond 2016

16

• Q4 2015: Increasing adverse impact from currency and lower production

rates will make it difficult for AIP to balance vs. last year result.

• In addition, SEK ~150m of restructuring cost as announced on October 7

www.husqvarnagroup.com

![Announces Q3 results [Result]](https://img.pdfslide.net/doc/110x75/577ca58e1a28abea748b9591/announces-q3-results-result.jpg)