Embed Size (px)

Citation preview

Fourth quarter and full year 2015 financial results February 10th, 2016

\ 2

Important notice

Forward-looking statements This presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the

Securities Exchange Act of 1934. All statements, other than statements of historical facts, included in this presentation that address activities,

events or developments that Markit Ltd. (“Markit” or the “Company”) expects, believes or anticipates will or may occur in the future are

forward-looking statements. Without limiting the generality of the foregoing, forward-looking statements contained in this presentation may

include the expectations of management regarding plans, strategies, objectives and anticipated financial and operating results of the

Company. Markit’s estimates and forward-looking statements are mainly based on its current expectations and estimates of future events and

trends, which affect or may affect its businesses and operations. Although Markit believes that these estimates and forward-looking

statements are based upon reasonable assumptions, they are subject to several risks and uncertainties and are made in light of information

currently available to Markit. When used in this presentation, the words “anticipate,” “believe,” “intend,” “expect,” “plan,” “will” or other similar

words are intended to identify forward-looking statements. Such statements are subject to a number of assumptions, risks and uncertainties,

many of which are beyond the control of Markit, which may cause actual results to differ materially from those implied or expressed by the

forward-looking statements. Further information on such assumptions, risks and uncertainties is available in Markit’s filings with the United

States Securities and Exchange Commission (“SEC”) including its annual report on Form 20-F. Markit’s SEC filings are available at

www.sec.gov or on the investor relations section of its website, www.markit.com. Markit undertakes no obligation and does not intend to

update these forward-looking statements to reflect events or circumstances occurring after the date of this presentation. You are cautioned not

to place undue reliance on these forward-looking statements, which speak only as of the date of this presentation. All forward-looking

statements are qualified in their entirety by this cautionary statement.

Non-IFRS financial measures

This presentation also includes measures defined by the SEC as non-IFRS financial measures. Markit believes that these non-IFRS

measures can provide useful supplemental information to securities analysts, investors and other interested parties regarding financial and

business trends relating to its financial condition and results of operations when read in conjunction with the company’s reported results.

Definitions and reconciliations of these non-IFRS measures to most directly comparable IFRS financial measures are available in the

Appendix of this presentation and in Markit’s earnings release dated February 10th, 2016.

Copyright ©2016, Markit Group Limited. All rights reserved and all intellectual property rights are retained by Markit.

\ 3

Agenda

Full year 2015 overview and outlook

Lance Uggla, CEO

Fourth quarter and full year 2015 financial results

Jeff Gooch, CFO

Appendix

\ 4

Full year 2015 overview and outlook

Lance Uggla

\ 5

Full year 2015 overview and outlook

2015 overview and outlook

• Organic revenue increased +3.6% (+7.4% constant currency)

• Proactive cost management resulted in adjusted EBITDA margins of 45%

Financial performance

• Disciplined capital management:

• Secondary offering of $650 million including $350 million buyback

• Entered into $200 million accelerated share repurchase agreement

• Refinanced debt through $500 million private placement

• Board authorized new $500m share repurchase program

Capital management

• Our leadership team is a key competitive advantage

• Strengthened this year through recruitment, acquisition and promotion

• Demonstrated ability to attract and promote top talent

Management team

• Developing products internally positions us to generate organic growth

• Expanded product offerings and solutions for customers across divisions

Product development

• Actively involved in the fixed income index market

• New technologies create opportunities (e.g. Blockchain)

• Leveraging enhanced account management structure

• Helping our customers respond to new regulations

Investing for growth

• Announced four acquisitions in 2015 with good momentum in 2016

• Acquisitions are integrated and contributing to adjusted earnings

• Pipeline remains strong Acquisitions

\ 6

Q4 and full year 2015 financial results

Jeff Gooch

\ 7

Q4 and FY 2015 financial results

Summary financial results

($ million)

Q4 2015 Q4 2014 YoY% FY 2015 FY 2014 YoY%

Revenue 291.5 271.4 7.4% 1,113.4 1,065.1 4.5%

Constant currency growth - - 9.4% - - 7.4%

Adjusted EBITDA (1) 131.8 124.7 5.7% 496.9 488.2 1.8%

Adjusted EBITDA margin (2) 45.6% 46.3% N/A 45.0% 46.0% N/A

Adjusted Earnings (3) 68.8 69.1 (0.4)% 273.9 279.0 (1.8)%

Adjusted EPS, diluted (4) $0.37 $0.37 - $1.44 $1.51 (4.6)%

Weighted average number of shares

used to compute earnings per share,

diluted (million)

188.1 187.3 0.4% 189.8 184.5 2.9%

1. Adjusted EBITDA is defined as profit for the period from continuing operations before income taxes, net finance costs, depreciation and amortisation on fixed assets and

intangible assets (including acquisition related intangible assets), acquisition related items, exceptional items, share based compensation and related items, net other

gains or losses, including Adjusted EBITDA attributable to joint ventures and excluding Adjusted EBITDA attributable to non-controlling interests.

2. Adjusted EBITDA margin is defined as Adjusted EBITDA divided by revenue, excluding revenue attributable to non-controlling interests.

3. Adjusted Earnings is defined as profit for the period from continuing operations before amortisation of acquired intangibles, acquisition related items, exceptional items,

share based compensation and related items, net other gains or losses and unwind of discount, less the tax effect of these adjustments and excluding Adjusted Earnings

attributable to non-controlling interests.

4. Adjusted EPS diluted is defined as Adjusted Earnings divided by the weighted average number of shares used to compute earnings per share diluted.

\ 8

Q4 and FY 2015 financial results

Revenue growth ($ million)

$271.4 $2.9

$22.6 $(5.4) $291.5

Q4 2014 revenue

Organic growth

Acquired growth

FX / Currency impact (1)

Q4 2015 revenue

+1.1%

(2.0)%

+8.3%

+7.4%

Q4 2014 vs. Q4 2015

$1,065.1

$38.3 $41.1 $(31.1)

$1,113.4

FY 2014 revenue

Organic growth

Acquired growth

FX / Currency impact (1)

FY 2015 revenue

+3.6%

+3.8% (2.9)%

+4.5%

FY 2014 vs. FY 2015

1) 10% movement in rates = $8m revenue impact & $7m opex impact in quarter

\ 9

53.8% 58.2%

40.9% 34.1%

5.3% 7.7%

Q4 2014 Q4 2015

Non-recurring revenue

Recurring variable revenue

Recurring fixed revenue

Q4 and FY 2015 financial results

Revenue mix

($ million) Q4 2015 % Q4 2014 % $ YoY FY 2015 % FY 2014 % $ YoY

Recurring fixed $169.6 58.2% $146.0 53.8% $23.6 $624.6 56.1% $559.2 52.5% $65.4

Recurring variable $99.3 34.1% $111.0 40.9% ($11.7) $418.8 37.6% $450.5 42.3% ($31.7)

Non-recurring $22.6 7.7% $14.4 5.3% $8.2 $70.0 6.3% $55.4 5.2% $14.6

Total Revenue $291.5 $271.4 $20.1 $1,113.4 $1,065.1 $48.3

Q4 overview:

─ Recurring fixed revenue

grew 16%, primarily due to

acquisitions and new

business wins in Information

and Solutions

─ Recurring variable revenue

decrease driven by

Processing

─ Q4 renewal rate ~90%

\ 10

Q4 and FY 2015 financial results

Operating and exceptional expenses

($ million)

Q4 2015 Q4 2014 YoY% FY 2015 FY 2014 YoY%

Personnel

costs (90.7) (85.2) 6.5% (362.3) (350.4) 3.4%

Non

personnel

costs

(64.7) (54.1) 19.6% (238.1) (218.8) 8.8%

Total

operating

expenses

(155.4) (139.3) 11.6% (600.4) (569.2) 5.5%

Exceptional

items - (33.1) n/a (48.7) (84.9) (42.6%)

Q4 overview:

─ Operating expenses

increased primarily due to

acquisitions

─ Continued investment in

new product development,

such as KYC, KY3P and

hosted service Solutions

offerings

\ 11

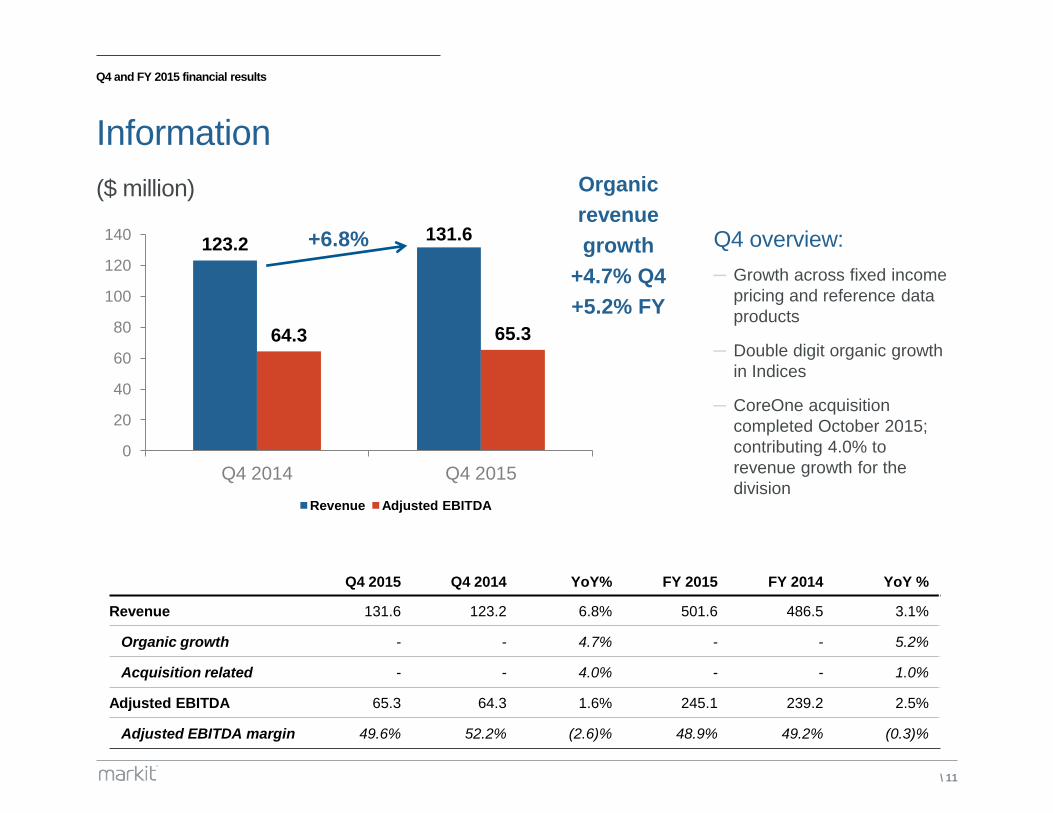

Q4 and FY 2015 financial results

Information

($ million)

123.2 131.6

64.3 65.3

0

20

40

60

80

100

120

140

Q4 2014 Q4 2015

Revenue Adjusted EBITDA

+6.8% Q4 overview:

─ Growth across fixed income

pricing and reference data

products

─ Double digit organic growth

in Indices

─ CoreOne acquisition

completed October 2015;

contributing 4.0% to

revenue growth for the

division

Organic

revenue

growth

+4.7% Q4

+5.2% FY

Q4 2015 Q4 2014 YoY% FY 2015 FY 2014 YoY %

Revenue 131.6 123.2 6.8% 501.6 486.5 3.1%

Organic growth - - 4.7% - - 5.2%

Acquisition related - - 4.0% - - 1.0%

Adjusted EBITDA 65.3 64.3 1.6% 245.1 239.2 2.5%

Adjusted EBITDA margin 49.6% 52.2% (2.6)% 48.9% 49.2% (0.3)%

\ 12

Q4 and FY 2015 financial results

Processing

($ million)

Q4 overview:

─ Strong rates volumes offset by price

changes implemented in Q2 and

adverse FX movements

─ Continued weakness in credit

volumes, along with one-off regulatory

reporting revenue in prior year

─ Loans secondary volumes maintained,

continued weakness in primary loan

issuance volumes

─ DealHub acquisition completed

September 2015; contributing 3.9% to

revenue growth for the division

68.5

59.8

36.5 30.9

0

10

20

30

40

50

60

70

80

Q4 2014 Q4 2015

Revenue Adjusted EBITDA

(12.7)%

Q4 2015 Q4 2014 YoY% FY 2015 FY 2014 YoY %

Revenue 59.8 68.5 (12.7)% 256.0 284.9 (10.1)%

Organic growth - - (14.7%) - - (8.2)%

Acquisition related - - 3.9% - - 1.3%

Adjusted EBITDA 30.9 36.5 (15.3)% 133.9 156.6 (14.5)%

Adjusted EBITDA margin 51.7% 53.3% (1.6)% 52.3% 55.0% (2.7)%

Organic

revenue

growth

(14.7)% Q4

(8.2)% FY

\ 13

Q4 and FY 2015 financial results

Solutions

($ million)

79.7

100.1

24.3 36.0

0

20

40

60

80

100

120

Q4 2014 Q4 2015

Revenue Adjusted EBITDA

+25.6%

Q4 2015 Q4 2014 YoY% FY 2015 FY 2014 YoY%

Revenue 100.1 79.7 25.6% 355.8 293.7 21.1%

Organic growth - - 9.0% - - 12.3%

Acquisition related - - 18.8% - - 11.1%

Adjusted EBITDA 36.0 24.3 48.1% 120.0 93.1 28.9%

Adjusted EBITDA margin 36.0% 30.5% 5.5% 33.7% 31.7% 2.0%

Q4 overview:

─ Growth across Managed Services

and Enterprise Software driven by

new business and increased

customer assets under

management

─ EDM, On Demand, Corporate

Actions, WSO Services achieved

double digit organic growth

─ Acquisition related revenue

growth of 18.8% for the division

was driven by Information Mosaic,

CoreOne, Tax Solutions and

thinkFolio

Organic

revenue

growth

+9.0% Q4

+12.3% FY

\ 14

Q4 and FY 2015 financial results

Net debt / leverage & free cash flow

($ million) December

31st, 2015

December

31st, 2014

Bank borrowings 197.4 224.5

Share buyback 128.6 211.1

Private placement 498.0 -

Total borrowings 824.0 435.6

Cash and cash equivalents (146.0) (117.7)

Net debt 678.0 317.9

LTM Adjusted EBITDA (1) 496.9 488.2

Leverage (2) 1.36x 0.65x

Net cash generated by operating

activities 405.6 369.9

Purchases of property, plant and

equipment (16.6) (23.5)

Purchases of intangible assets (100.5) (101.4)

Free cash flow 288.5 245.0

Overview:

─ On November 4, 2015, we

completed a $500m private

placement of debt with $210m at

3.73% (due 2022) and $290m at

4.05% (due 2025)

─ Free cash flow up 17.8% to

$288.5m

─ Working capital showed a net

inflow of ~$30m during 2015

─ Capex under control, at $117m for

the year at 10.5% of revenues

(2014: $125m or 11.7% of

revenues)

1) LTM Adjusted EBITDA is defined as Adjusted EBITDA for the previous twelve month period to date reported

2) Leverage is defined as net debt divided by LTM Adjusted EBITDA

\ 15

187.3

191.7 190.8

185.4

188.1

184.9

4.4

2.3 5.4

4.0

3.2 10.8

1.3

Q4 2014 Dilution Q1 2015 Dilution Share repurchase

Q2 2015 Dilution Share repurchase

Q3 2015 Dilution Share repurchase

Q4 2015 At 01.01.16

In-period weighted average number of shares, diluted

Managing diluted shares outstanding ─ $350 million share repurchase (~14m shares) completed June 2015

─ ~5.1 million shares repurchased in December 2015 representing $150 million of aggregate $200 million

accelerated share repurchase program

─ New share repurchase programme of up to $500 million over two years was authorised in February 2016 by the

Board of directors

(million)

Dilution refers to dilutive impact of employee options and restricted stock.

Diluted share count as of January 1, 2016 (184.9m) removes the impact of time-weighting on the 2015 share count and includes expected vesting of restricted stock

Q4 and FY 2015 financial results

\ 16

Long term financial objectives and commentary

LONG TERM FINANCIAL OBJECTIVES

Organic revenue growth 5-7%

Total revenue growth (constant currency) Double digits through acquisitions

Adjusted EBITDA margins Mid 40%’s

MANAGEMENT COMMENTARY

Adjusted effective tax rate 26-29%

Leverage ratio Target range of 1.5 – 2.0x

Capital expenditures1 9-11% of revenues

Depreciation / Amortisation 8-10% of revenues

Share capital management Aim to use cash proceeds from option exercises to offset dilution

Aim to use buybacks to offset dilution from annual compensation awards

Information – organic revenue growth 4-6%

Processing – adjusted EBITDA margin ~50%

Solutions – organic revenue growth 10-15%

Q4 and FY 2015 financial results

1 Excluding significant office related capex (e.g. 2016 New York City office consolidation).

\ 17

Appendix

\ 18

Acquired revenue calculation method comparison

Impact of revised treatment of acquired revenue

─ At Q3 2015, we disclosed a change to our organic growth methodology to be in line with peers

─ Commencing Q1 2016, new methodology treats acquisitions as organic growth twelve months post acquisition

─ Only our Solutions division was impacted in 2014 and 2015

FY 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 FY 2015

Reported:

Information 4.4% 6.3% 4.9% 5.1% 4.7% 5.2%

Processing 5.1% (2.4)% (2.5)% (13.6)% (14.7)% (8.2)%

Solutions 17.8% 14.4% 13.2% 13.1% 9.0% 12.3%

Group 7.8% 6.1% 5.1% 2.3% 1.1% 3.6%

New methodology:

Information 4.4% 6.3% 4.9% 5.1% 4.7% 5.2%

Processing 5.1% (2.4)% (2.5)% (13.6)% (14.7)% (8.2)%

Solutions 18.2% 15.6% 13.8% 15.9% 10.9% 14.0%

Group 7.8% 6.4% 5.3% 3.1% 1.7% 4.1%

Organic revenue growth comparison

\ 19

70 75 99 131 125 117

242

67

381 224

129

317

183

52

6191

551

2010 2011 2012 2013 2014 2015

($ million)

Annual capital allocation

Share repurchase Acquisitions Internal investments

Acquisitions 39%

Internal investments

19%

Share repurchase

42%

Balanced and flexible capital allocation framework

1 Includes $495m in share repurchases conducted in August 2012, 55% of which from related-party customers, payable in quarterly installments through to May 2017.

Capital allocation

495

194

1,099

355

254

985

2010 – 2015 cumulative capital allocation

Total: $3,380m

\ 20

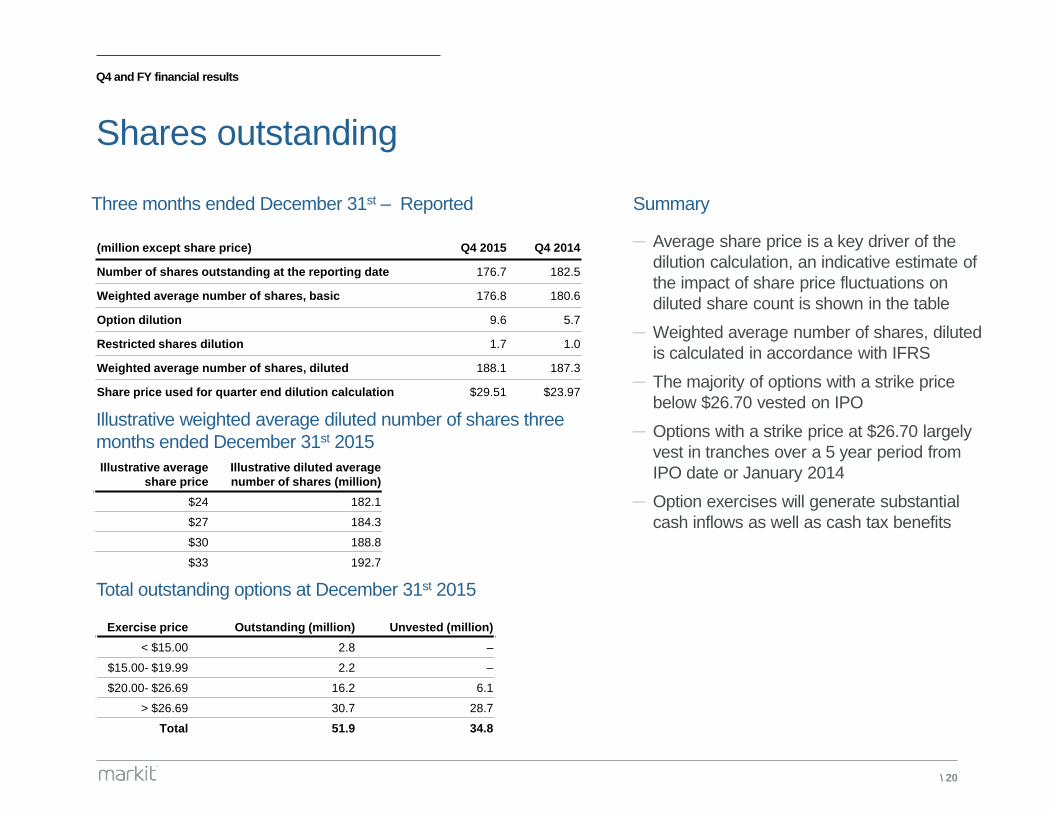

Q4 and FY financial results

Shares outstanding

Summary

─ Average share price is a key driver of the

dilution calculation, an indicative estimate of

the impact of share price fluctuations on

diluted share count is shown in the table

─ Weighted average number of shares, diluted

is calculated in accordance with IFRS

─ The majority of options with a strike price

below $26.70 vested on IPO

─ Options with a strike price at $26.70 largely

vest in tranches over a 5 year period from

IPO date or January 2014

─ Option exercises will generate substantial

cash inflows as well as cash tax benefits

(million except share price) Q4 2015 Q4 2014

Number of shares outstanding at the reporting date 176.7 182.5

Weighted average number of shares, basic 176.8 180.6

Option dilution 9.6 5.7

Restricted shares dilution 1.7 1.0

Weighted average number of shares, diluted 188.1 187.3

Share price used for quarter end dilution calculation $29.51 $23.97

Illustrative average

share price

Illustrative diluted average

number of shares (million)

$24 182.1

$27 184.3

$30 188.8

$33 192.7

Exercise price Outstanding (million) Unvested (million)

< $15.00 2.8 –

$15.00- $19.99 2.2 –

$20.00- $26.69 16.2 6.1

> $26.69 30.7 28.7

Total 51.9 34.8

Three months ended December 31st – Reported

Illustrative weighted average diluted number of shares three

months ended December 31st 2015

Total outstanding options at December 31st 2015

\ 21

Sub-segment revenue summary

Sub-segment revenue – 3 year summary

($ million)

Segments FY 2013 FY 2014 FY 2015 CAGR %

FY2013 – 2015

Pricing and Reference Data 182.8 199.8 210.8 7.4%

Indices 86.6 91.5 99.1 7.0%

Valuation and Trading Services 190.2 195.2 191.7 0.4%

Information 459.6 486.5 501.6 4.5%

Processing 265.3 284.9 256.0 (1.8)%

Managed Services 131.6 167.6 202.1 23.9%

Enterprise Software 91.4 126.1 153.7 29.7%

Solutions 223.0 293.7 355.8 26.3%

Group 947.9 1,065.1 1,113.4 8.4%

Note: We reorganised certain products within our Information segment between the Pricing and Reference Data, Indices and Valuation and Trading Services sub-segments in 2014.

For comparability purposes, all prior year figures above have been presented to reflect this change.

\ 22

Q4 and FY 2015 financial results

Reconciliation to Adjusted EBITDA

($ million)

Q4 2015 Q4 2014 FY 2015 FY2014

Profit for the period 46.6 15.7 152.1 164.1

Income tax expense 19.9 19.7 70.0 56.5

Finance costs – net 7.2 4.1 18.9 16.9

Depreciation and amortisation - other 28.8 28.2 107.0 100.1

Amortisation – acquisition related 18.4 14.6 63.7 57.9

Acquisition related items 2.0 (1.4) 4.2 (12.4)

Exceptional items - 33.1 48.7 84.9

Share based compensation and related items 14.6 9.2 50.8 16.0

Other (gains) / losses – net (4.6) 3.0 (13.7) 6.0

Share of results from joint venture not attributable to

Adjusted EBITDA (0.4) (1.1) (2.4) (1.1)

Adjusted EBITDA attributable to non-controlling interests (0.7) -(0.4) (2.4) (0.7)

Adjusted EBITDA 131.8 124.7 496.9 488.2

\ 23

Q4 and FY 2015 financial results

Reconciliation to Adjusted Earnings

($ million)

Q4 2015 Q4 2014 FY 2015 FY 2014

Profit for the period 46.6 15.7 152.1 164.1

Amortisation – acquisition related 18.4 14.6 63.7 57.9

Acquisition related items 2.0 (1.4) 4.2 (12.4)

Exceptional items - 33.1 48.7 84.9

Share based compensation and related items 14.6 9.2 50.8 16.0

Other (gains) / losses – net (4.6) 3.0 (13.7) 6.0

Unwind of discount(1)

2.2 2.7 9.2 10.5

Tax effect of above adjustments (9.7) (6.9) (38.7) (47.4)

Adjusted Earnings attributable to non-controlling interests (0.7) (0.9) (2.4) (0.6)

Adjusted Earnings 68.8 69.1 273.9 279.0

Weighted average number of shares for computation of

earnings per share, diluted 188,093,760 187,335,924 189,796,719 184,467,540

1. Unwind of discount represents the non-cash unwinding of discount, recorded through finance costs – net in the income statement, primarily in relation to our share buyback liability.

\ 24

Q4 and FY 2015 financial results

Reconciliation to Adjusted earnings effective tax rate

($ million)

Q4 2015 Q4 2014 FY 2015 FY 2014

Income tax expense 19.9 19.7 70.0 56.5

Tax effect of adjusted earnings adjustments(1)

9.7 6.9 38.7 47.4

Tax on adjusted earnings (A) 29.6 26.6 108.7 103.9

Adjusted earnings(1)

68.8 69.1 273.9 279.0

Share of results from joint venture 3.2 5.9 11.3 5.9

Tax on adjusted earnings 29.6 26.6 108.7 103.9

Adjusted profit before tax (B) 101.6 101.6 393.9 388.8

Adjusted earnings effective tax rate (A divided by B) 29.1% 26.2% 27.6% 26.7%

1. See “Reconciliation to adjusted earnings”

\ 25

Q4 and FY 2015 financial results

Definitions

Revenue growth

We measure revenue growth in terms of organic revenue growth, acquisition related revenue growth, foreign currency impact on revenue growth and constant currency revenue growth. We

define these components as follows:

Organic – Revenue growth from continuing operations from factors other than acquisitions and foreign currency fluctuations. We derive organic revenue growth from the development of new

products and services, increased penetration of existing products and services to new and existing customers, price changes for our products and services and market driven factors such as

increased trading volumes or changes in customer assets under management.

Acquisition related – Revenue growth from acquired businesses through the end of the fiscal year following the fiscal year in which the acquisition was completed. This growth results from our

strategy of making targeted acquisitions that facilitate growth by complementing our existing products and services and addressing market opportunities.

Foreign currency – The impact on revenue growth resulting from the difference between current revenue at current exchange rates and current revenue at the corresponding prior period

exchange rates.

Constant currency – Total revenue growth, excluding the impact of exchange rate movements from the prior period to the current period. This is equal to the combination of organic and

acquisition related revenue growth, as described above.

Revenue by type

Revenue by type is how we classify the income recognised from the sale of our products and services into three groups as defined below:

Recurring fixed revenue – Revenue generated from contracts specifying a fixed fee for services delivered over the life of the contract. The fixed fee is typically paid annually, semiannually or

quarterly in advance. These contracts are typically subscription contracts where the revenue is recognised across the life of the contract. The initial term of these contracts can range from one to

five years and usually includes auto-renewal clauses.

Recurring variable revenue – Revenue derived from contracts that specify a fee for services which is typically not fixed. The variable fee is typically paid monthly in arrears. Recurring variable

revenue is based on, among other factors, the number of trades processed, assets under management or the number of positions we value. Many of these contracts do not have a maturity

date while the remainder have an initial term ranging from one to five years.

Non-recurring revenue – Revenue that relates to certain software license sales and the associated consulting revenue.

Other Non-IFRS Measures

Adjusted EBITDA is defined as profit for the period from continuing operations before income taxes, net finance costs, depreciation and amortisation on fixed assets and intangible assets

(including acquisition related intangible assets), acquisition related items, exceptional items, share based compensation and related items, net other gains or losses, including Adjusted EBITDA

attributable to joint ventures and excluding Adjusted EBITDA attributable to non-controlling interests.

Adjusted EBITDA margin is defined as Adjusted EBITDA divided by revenue, excluding revenue attributable to non-controlling interests.

LTM Adjusted EBITDA is defined as Adjusted EBITDA for the previous twelve month period from date reported.

Adjusted Earnings is defined as profit for the period from continuing operations before amortisation of acquired intangibles, acquisition related items, exceptional items, share based

compensation and related items, net other gains or losses and unwind of discount, less the tax effect of these adjustments and excluding Adjusted Earnings attributable to non-controlling

interests.

Adjusted EPS diluted is defined as Adjusted Earnings divided by the weighted average number of shares used to compute earnings per share, diluted.

Adjusted earnings effective tax rate is a rate calculated using income tax for the period adjusted for the tax effect of Adjusted earnings adjustments, divided by Adjusted earnings excluding

tax and excluding share of results from joint venture.

Leverage is defined as net debt divided by Adjusted EBITDA for the previous twelve month period from date reported.

Free cash flow is defined as net cash generated by or used in operating activities, less capital expenditure, purchases of property, plant and equipment and intangible assets.