Embed Size (px)

Citation preview

Fourth Quarter 2014 February 11, 2015

Genworth MI Canada Inc.

Q4 2014 Genworth MI Canada Inc. 2

Forward-Looking and Non-IFRS Statements

This presentation relating to Genworth MI Canada Inc. (the “Company”, “Genworth Canada” or “MIC”) includes certain forward-looking statements. These forward-looking statements include, but are not limited to, statements with respect to the Company’s future operating and financial results, expectations regarding premiums written, losses on claims and investment income, the Canadian housing market, and other statements that are not historical facts. These forward-looking statements may be identified by their use of words such as “may”, “would”, “could”, “will,” “intend”, “plan”, “anticipate”, “believe”, “seek”, “propose”, “estimate”, “expect”, and similar expressions. These statements are based on the Company’s current assumptions, including assumptions regarding economic, global, political, business, competitive, market and regulatory matters. These forward-looking statements are inherently subject to significant risks, uncertainties and changes in circumstances, many of which are beyond the control of the Company. The Company’s actual results may differ materially from those expressed or implied by such forward-looking statements, including as a result of changes in the facts underlying the Company’s assumptions, and the other risks described in the Company’s Annual Information Form dated March 17, 2014, its Short Form Base Shelf Prospectus dated June 18, 2014, the Prospectus Supplements thereto, its most recently issued Management’s Discussion and Analysis and all documents incorporated by reference in such documents. Other than as required by applicable laws, the Company undertakes no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future developments or otherwise.

To supplement its financial statements, the Company uses select non-IFRS financial measures. Non-IFRS financial measures include net operating income, interest and dividend income (net of investment expenses), operating earnings per common share (basic), operating earnings per common share (diluted), shareholders’ equity excluding accumulated other comprehensive income (“AOCI”), operating return on equity and underwriting ratios such as loss ratio, expense ratio and combined ratio. The Company believes that these non-IFRS financial measures provide meaningful supplemental information regarding its performance and may be useful to investors because they allow for greater transparency with respect to key metrics used by management in its financial and operational decision making. Non-IFRS measures do not have standardized meanings and are unlikely to be comparable to any similar measures presented by other companies. These measures are defined in the Company’s glossary, which is posted on the Company’s website at http://investor.genworthmicanada.ca. A reconciliation from non-IFRS financial measures to the most readily comparable measures calculated in accordance with IFRS, where applicable can be found in the Company’s most recent management’s discussion and analysis, which is posted on the Company’s website and is also available at www.sedar.com.

Q4 2014 Genworth MI Canada Inc. 3

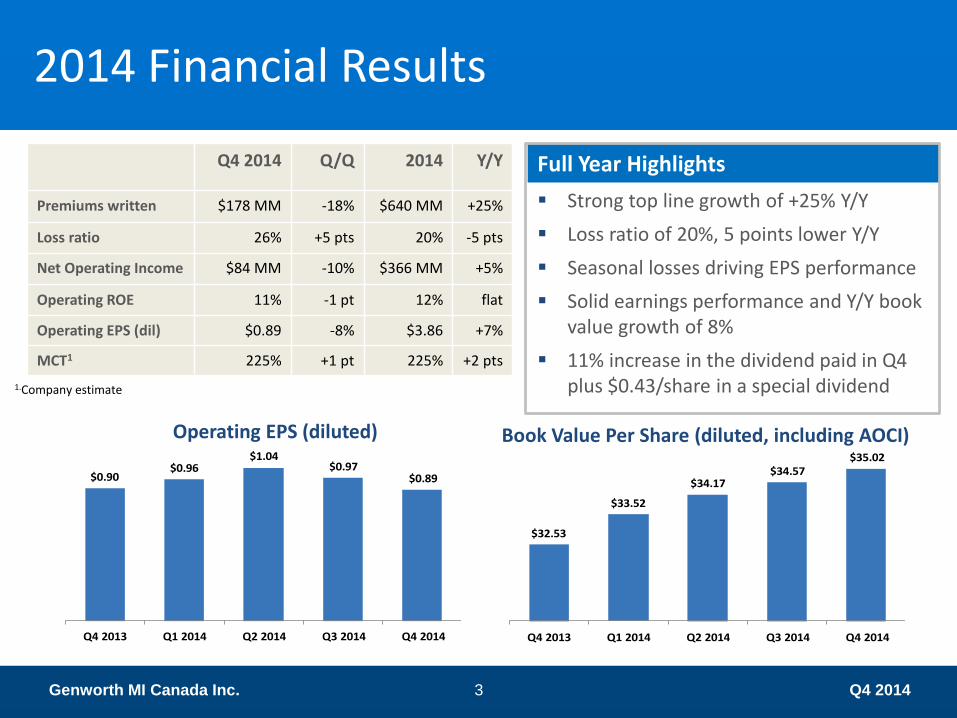

$32.53

$33.52

$34.17$34.57

$35.02

Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014

$0.90$0.96

$1.04$0.97

$0.89

Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014

2014 Financial Results

Q4 2014 Q/Q 2014 Y/Y

Premiums written $178 MM -18% $640 MM +25%

Loss ratio 26% +5 pts 20% -5 pts

Net Operating Income $84 MM -10% $366 MM +5%

Operating ROE 11% -1 pt 12% flat

Operating EPS (dil) $0.89 -8% $3.86 +7%

MCT1 225% +1 pt 225% +2 pts

Book Value Per Share (diluted, including AOCI)

Full Year Highlights

Strong top line growth of +25% Y/Y

Loss ratio of 20%, 5 points lower Y/Y

Seasonal losses driving EPS performance

Solid earnings performance and Y/Y book value growth of 8%

11% increase in the dividend paid in Q4 plus $0.43/share in a special dividend

Operating EPS (diluted)

1.Company estimate

Q4 2014 Genworth MI Canada Inc. 4

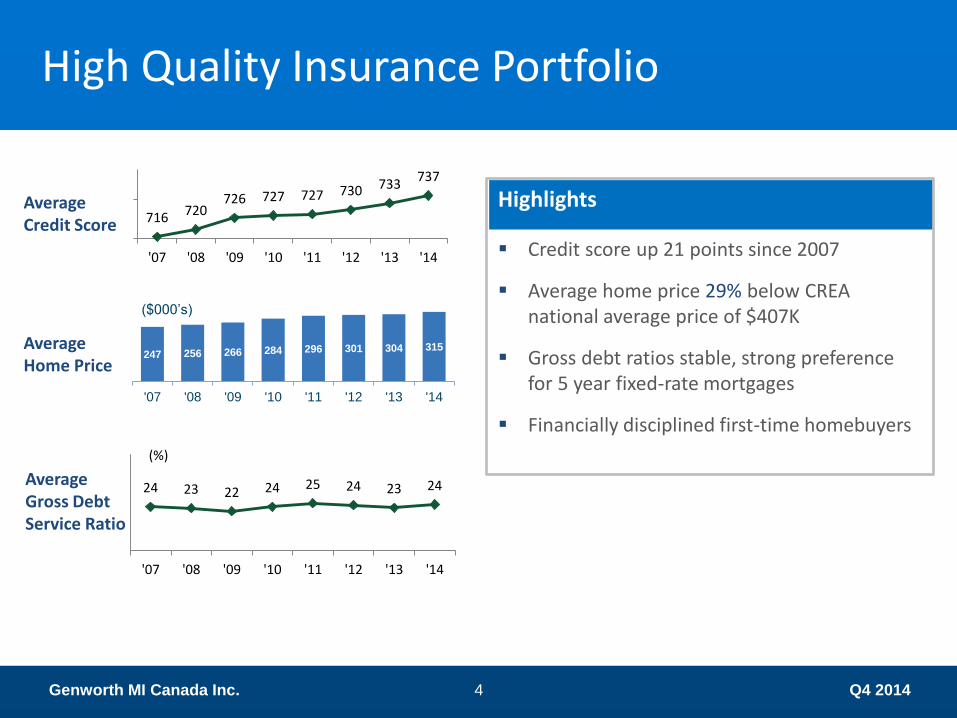

Highlights

Credit score up 21 points since 2007

Average home price 29% below CREA national average price of $407K

Gross debt ratios stable, strong preference for 5 year fixed-rate mortgages

Financially disciplined first-time homebuyers

High Quality Insurance Portfolio

Average Credit Score

Average Home Price

Average Gross Debt Service Ratio

716 720 726 727 727 730 733

737

'07 '08 '09 '10 '11 '12 '13 '14

247 256 266 284 296 301 304 315

'07 '08 '09 '10 '11 '12 '13 '14

($000’s)

24 23 22 24 25 24 23 24

'07 '08 '09 '10 '11 '12 '13 '14

(%)

Q4 2014 Genworth MI Canada Inc. 5

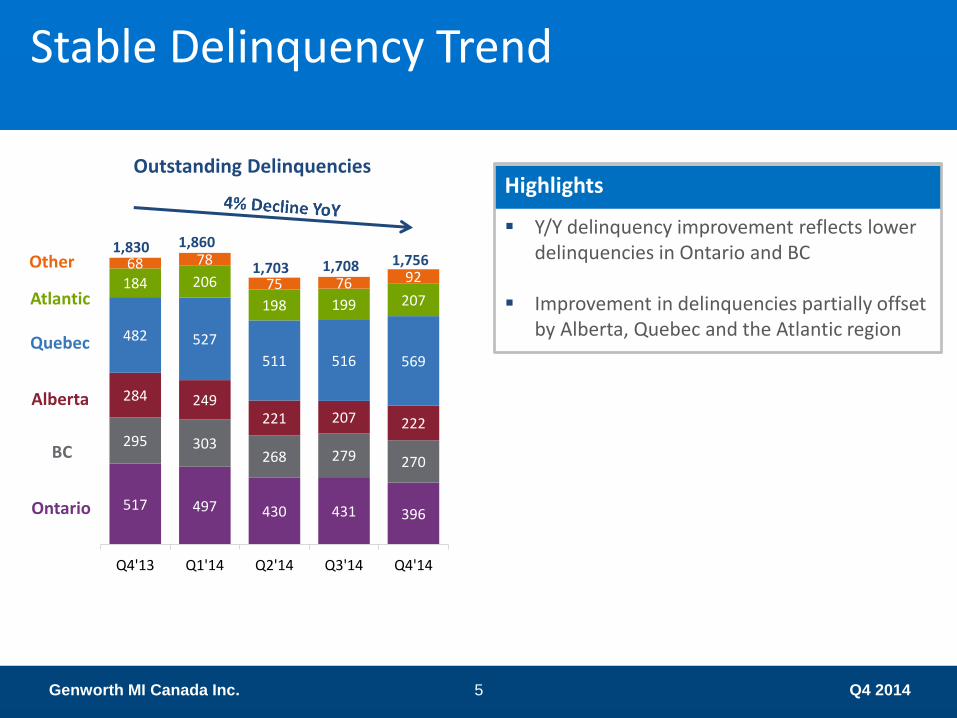

517 497 430 431 396

295 303 268 279 270

284 249 221 207 222

482 527

511 516 569

184 206

198 199 207

68 78

75 76 92

Q4'13 Q1'14 Q2'14 Q3'14 Q4'14

1,860 1,830

1,703 1,708 1,756

Outstanding Delinquencies

Stable Delinquency Trend

Ontario

BC

Alberta

Quebec

Atlantic

Highlights

Y/Y delinquency improvement reflects lower delinquencies in Ontario and BC

Improvement in delinquencies partially offset

by Alberta, Quebec and the Atlantic region

Other

Q4 2014 Genworth MI Canada Inc. 6

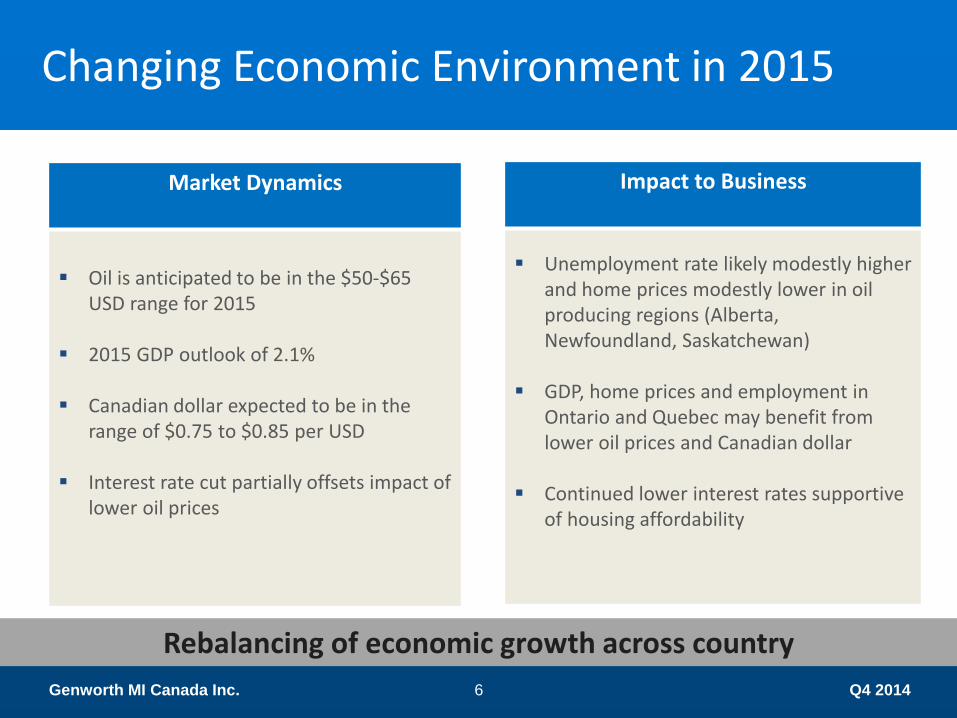

Changing Economic Environment in 2015

Market Dynamics

Oil is anticipated to be in the $50-$65 USD range for 2015

2015 GDP outlook of 2.1% Canadian dollar expected to be in the

range of $0.75 to $0.85 per USD Interest rate cut partially offsets impact of

lower oil prices

Impact to Business

Unemployment rate likely modestly higher and home prices modestly lower in oil producing regions (Alberta, Newfoundland, Saskatchewan)

GDP, home prices and employment in

Ontario and Quebec may benefit from lower oil prices and Canadian dollar

Continued lower interest rates supportive

of housing affordability

Rebalancing of economic growth across country

Q4 2014 Genworth MI Canada Inc. 7

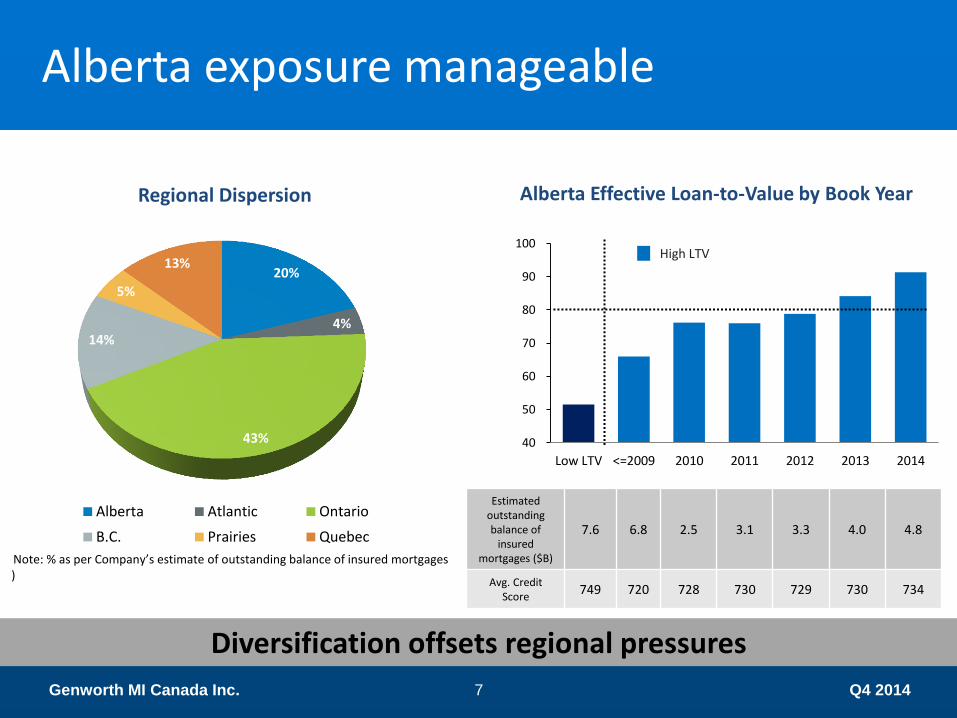

Alberta exposure manageable

20%

4%

43%

14%

5%

13%

Alberta Atlantic Ontario

B.C. Prairies Quebec

Regional Dispersion Alberta Effective Loan-to-Value by Book Year

Diversification offsets regional pressures

40

50

60

70

80

90

100

Low LTV <=2009 2010 2011 2012 2013 2014

High LTV

Estimated outstanding balance of

insured mortgages ($B)

7.6 6.8 2.5 3.1 3.3 4.0 4.8

Avg. Credit Score

749 720 728 730 729 730 734

Note: % as per Company’s estimate of outstanding balance of insured mortgages )

Q4 2014 Genworth MI Canada Inc. 8

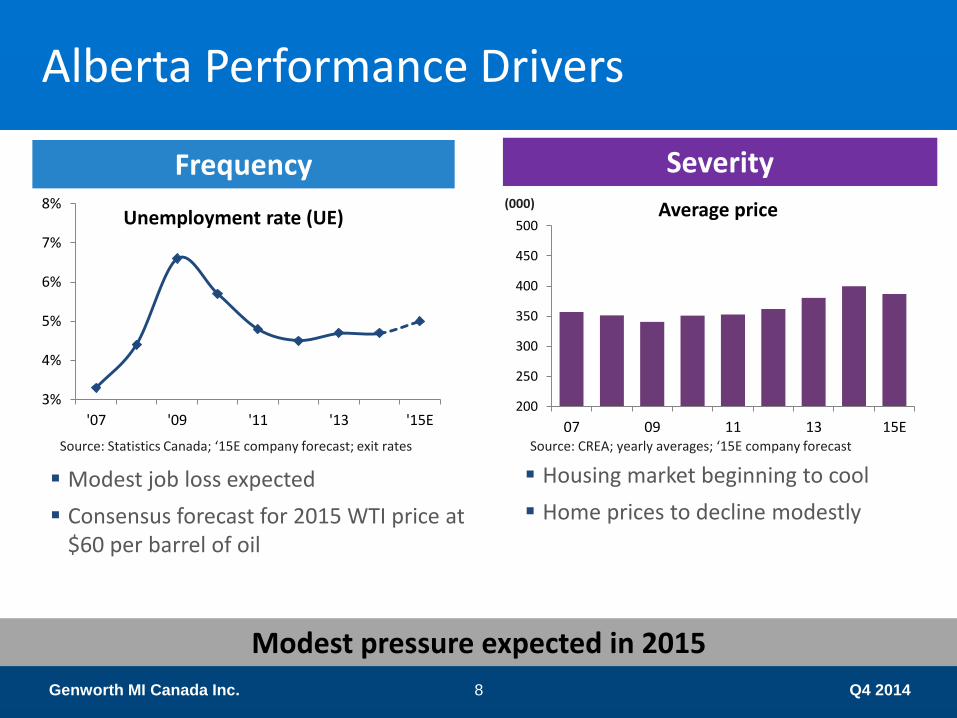

Alberta Performance Drivers

Frequency Severity

Modest job loss expected

Consensus forecast for 2015 WTI price at $60 per barrel of oil

Housing market beginning to cool

Home prices to decline modestly

3%

4%

5%

6%

7%

8%

'07 '09 '11 '13 '15E

Unemployment rate (UE)

200

250

300

350

400

450

500

07 09 11 13 15E

Average price (000)

Source: CREA; yearly averages; ‘15E company forecast Source: Statistics Canada; ‘15E company forecast; exit rates

Modest pressure expected in 2015

Q4 2014 Genworth MI Canada Inc. 9

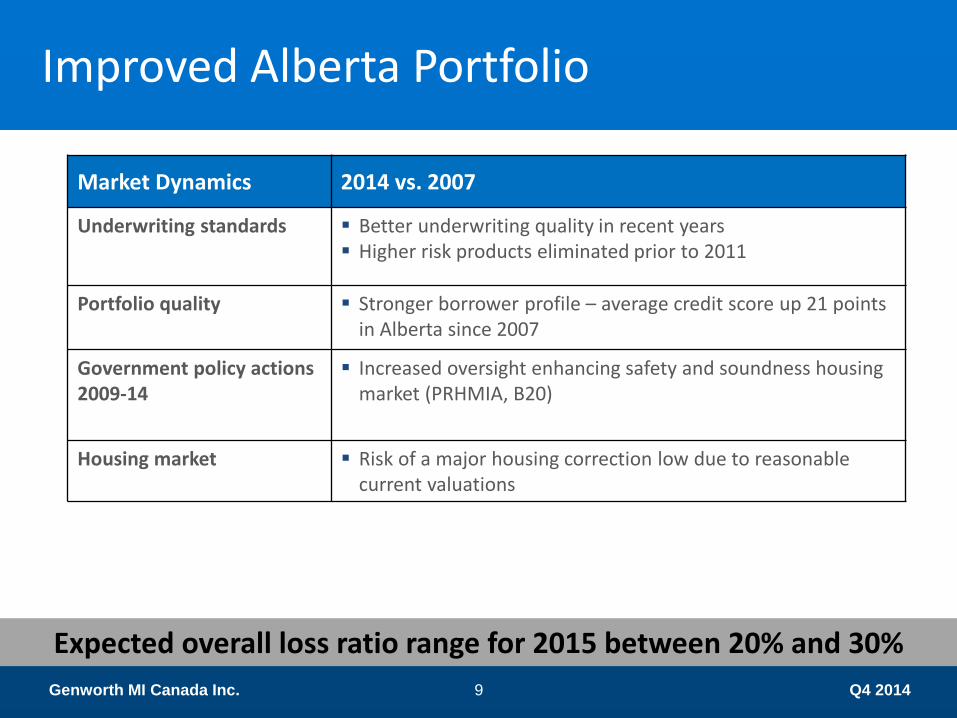

Improved Alberta Portfolio

Expected overall loss ratio range for 2015 between 20% and 30%

Market Dynamics 2014 vs. 2007

Underwriting standards Better underwriting quality in recent years Higher risk products eliminated prior to 2011

Portfolio quality Stronger borrower profile – average credit score up 21 points in Alberta since 2007

Government policy actions 2009-14

Increased oversight enhancing safety and soundness housing market (PRHMIA, B20)

Housing market Risk of a major housing correction low due to reasonable current valuations

Q4 2014 Genworth MI Canada Inc. 10

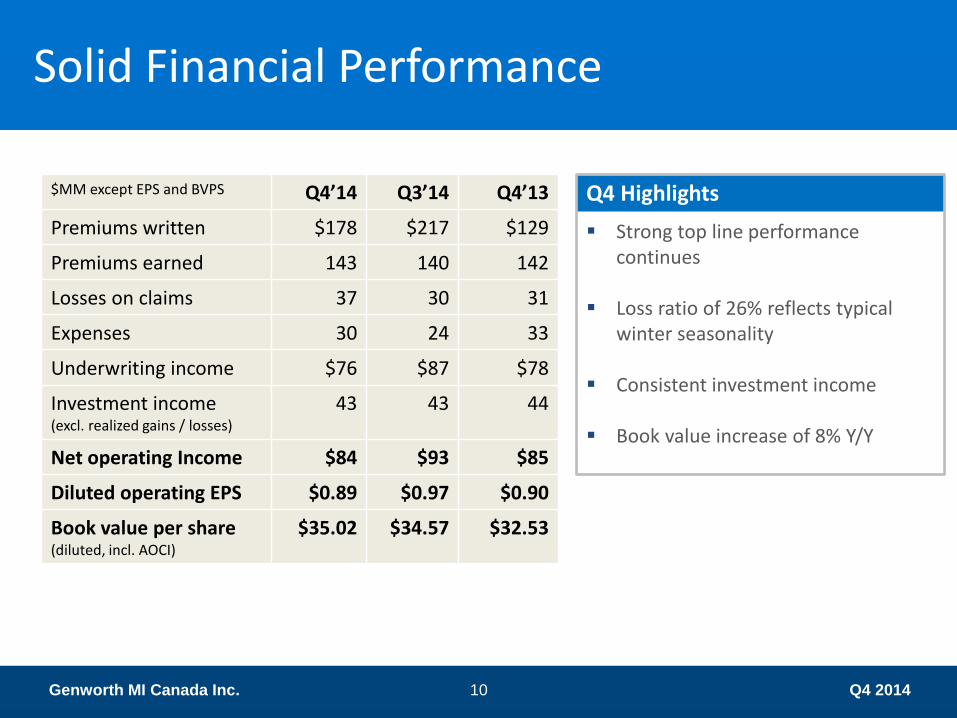

Solid Financial Performance

$MM except EPS and BVPS Q4’14 Q3’14 Q4’13

Premiums written $178 $217 $129

Premiums earned 143 140 142

Losses on claims 37 30 31

Expenses 30 24 33

Underwriting income $76 $87 $78

Investment income (excl. realized gains / losses)

43 43 44

Net operating Income $84 $93 $85

Diluted operating EPS $0.89 $0.97 $0.90

Book value per share (diluted, incl. AOCI)

$35.02 $34.57 $32.53

Q4 Highlights

Strong top line performance continues

Loss ratio of 26% reflects typical

winter seasonality Consistent investment income Book value increase of 8% Y/Y

Q4 2014 Genworth MI Canada Inc. 11

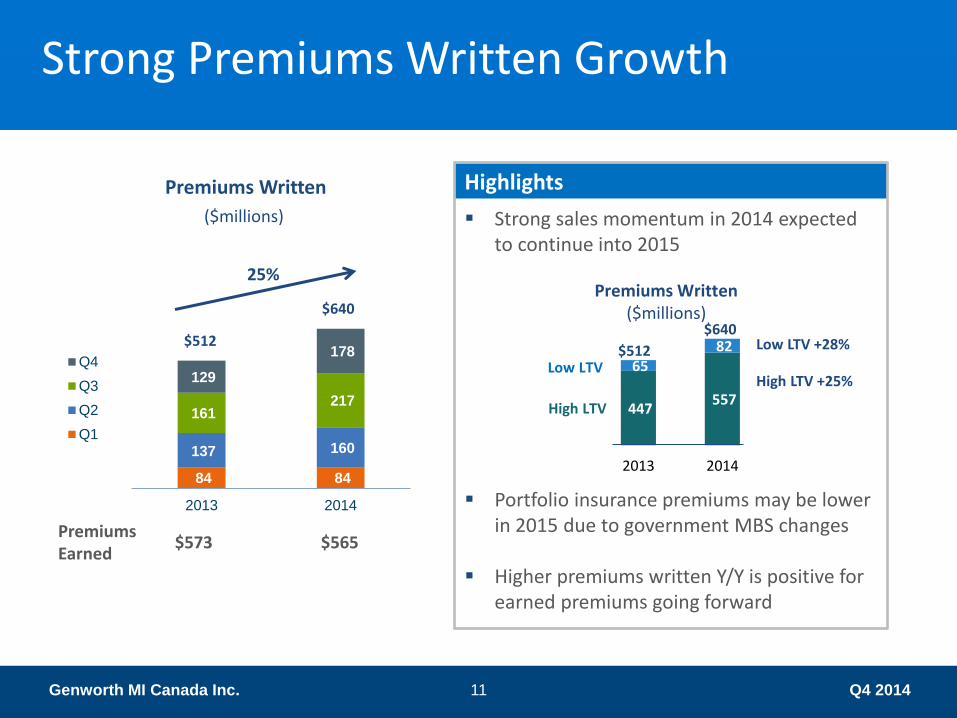

Strong Premiums Written Growth

Premiums Written

($millions)

Highlights

Strong sales momentum in 2014 expected to continue into 2015

Portfolio insurance premiums may be lower in 2015 due to government MBS changes

Higher premiums written Y/Y is positive for earned premiums going forward

84 84

137 160

161 217

129

178

2013 2014

Q4

Q3

Q2

Q1

25%

Premiums Earned

$573 $565

447 557

65 82

2013 2014

Premiums Written ($millions)

High LTV

Low LTV

Low LTV +28% $512

$640 $512

$640

High LTV +25%

Q4 2014 Genworth MI Canada Inc. 12

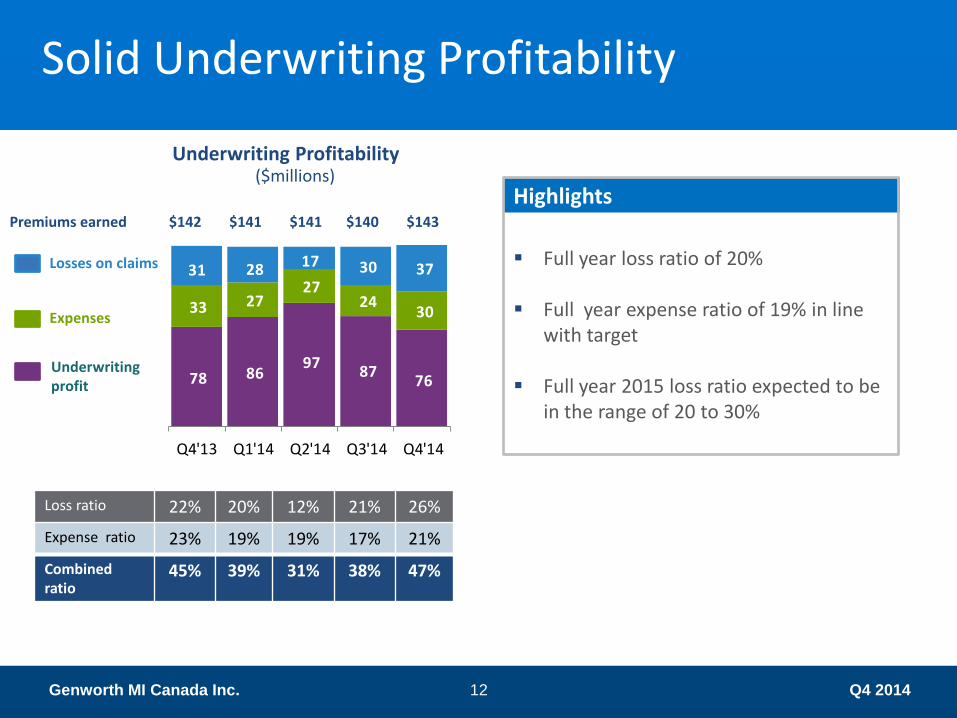

78 86 97

87 76

33 27 27

24 30

31 28 17 30 37

Q4'13 Q1'14 Q2'14 Q3'14 Q4'14

Solid Underwriting Profitability

Underwriting Profitability

Underwriting profit

Expenses

Losses on claims

Loss ratio 22% 20% 12% 21% 26%

Expense ratio 23% 19% 19% 17% 21%

Combined ratio

45% 39% 31% 38% 47%

($millions) Highlights

Full year loss ratio of 20% Full year expense ratio of 19% in line

with target

Full year 2015 loss ratio expected to be in the range of 20 to 30%

Premiums earned $142 $141 $141 $140 $143

Q4 2014 Genworth MI Canada Inc. 13

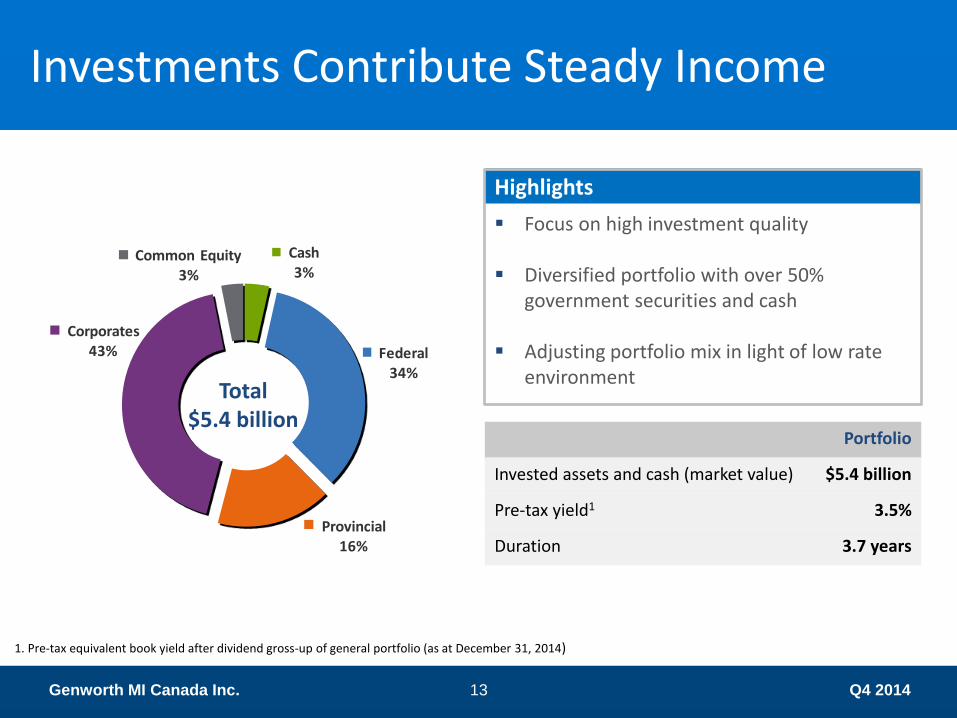

Cash3%

Federal34%

Provincial16%

Corporates 43%

Common Equity3%

Investments Contribute Steady Income

Total $5.4 billion

1. Pre-tax equivalent book yield after dividend gross-up of general portfolio (as at December 31, 2014)

Portfolio

Invested assets and cash (market value) $5.4 billion

Pre-tax yield1 3.5%

Duration 3.7 years

Highlights

Focus on high investment quality

Diversified portfolio with over 50% government securities and cash

Adjusting portfolio mix in light of low rate environment

Q4 2014 Genworth MI Canada Inc. 14

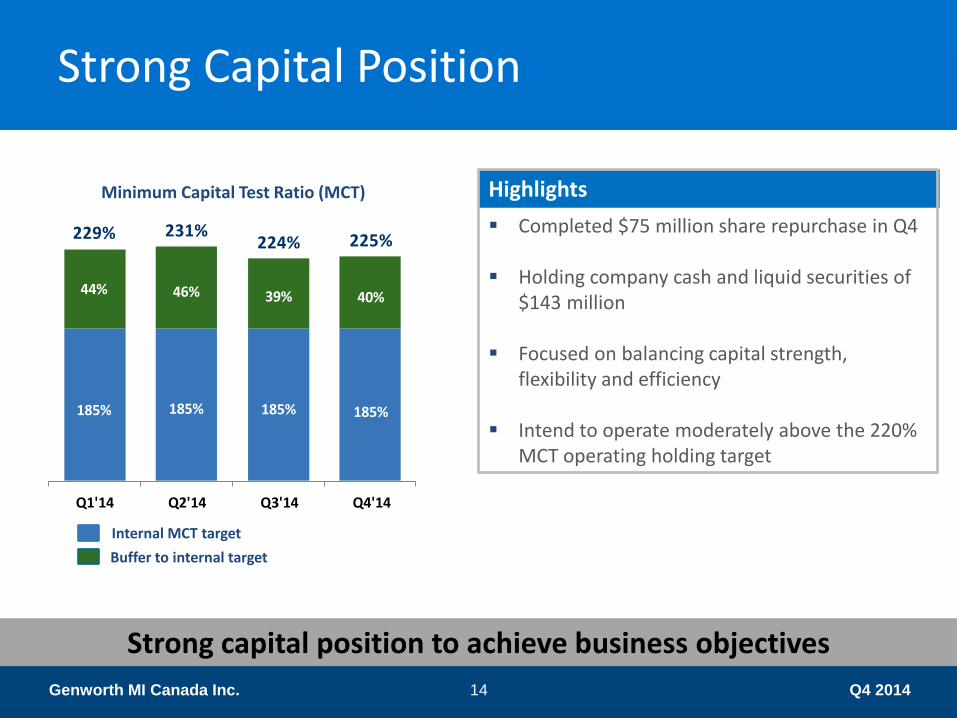

185% 185% 185% 185%

44% 46% 39% 40%

229% 231%224% 225%

Q1'14 Q2'14 Q3'14 Q4'14

Strong Capital Position

Minimum Capital Test Ratio (MCT)

Internal MCT target

Buffer to internal target

Highlights

Completed $75 million share repurchase in Q4

Holding company cash and liquid securities of $143 million

Focused on balancing capital strength,

flexibility and efficiency Intend to operate moderately above the 220%

MCT operating holding target

Strong capital position to achieve business objectives

Q4 2014 Genworth MI Canada Inc. 15

Building on Growth Momentum

Prudently expand market share

Proactive risk management and loss mitigation

Strong government relations

Efficient capital structure

Adjacent opportunities Employ and engage top talent

Well-positioned and remain focused on strategic course

Q4 2014 Genworth MI Canada Inc. 16

Question and Answer

Samantha Cheung Vice-President, Investor Relations 905.287.5482 [email protected] www.genworth.ca

Contact: