Embed Size (px)

Citation preview

Investor and Analyst DayMarch 30, 2016

Forward Looking Information

Both these slides that you will be presented today and the accompanying oral presentations contain certain forward-looking statements within themeaning of the United States Private Securities Litigation Reform Act of 1995 and forward-looking information within the meaning of the Securities Act(Ontario). Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results,performance or achievements of Teck to be materially different from any future results, performance or achievements expressed or implied by theforward-looking statements. These forward-looking statements include statements relating to management’s expectations with respect to Teck’s costs,production, expenditures, financial projections and guidance, production targets and guidance and those other statements identified in the slides titled“Forward Looking Information” in each of the individual presentations. The “Forward Looking Information” slide in each individual presentation isincorporated by reference and please refer to each of those slides for further information.

These forward-looking statements involve numerous assumptions, risks and uncertainties and actual results may vary materially. These statements arebased on a number of assumptions, including, but not limited to, assumptions regarding general business and economic conditions, interest rates, thesupply and demand for, inventories of, and the level and volatility of prices of our products, the timing of receipt of regulatory and governmental approvalsfor Teck’s expansions, Teck’s costs of production and production and productivity levels, as well as those of its competitors, market competition, theaccuracy of Teck’s reserve and resources estimates and the geological, operational and price assumptions on which these are based, tax benefits, theresolution of environmental and other proceedings, our ongoing relations with our employees and partners and joint venturers, performance by customersand counterparties of their contractual obligations, and the future operational and financial performance of the company generally. Each of the slidestitled “Forward Looking Information” in the individual presentations describe additional assumptions for the forward-looking statements included in thatpresentation.

Events or circumstances could cause actual results to differ materially. Factors that may cause actual results to vary include, but are not limited to:unanticipated developments in business and economic conditions in the principal markets for Teck’s products or in the supply, demand, and prices formetals and other commodities to be produced, changes in interest or currency exchange rates, inaccurate geological assumptions (including with respectto the size, grade and recoverability of reserves and resources), legal disputes or unanticipated outcomes of legal proceedings, unanticipated operationaldifficulties (including failure of plant, equipment or processes to operate in accordance with specifications or expectations, cost escalation, unavailabilityof materials and equipment, government action or delays in the receipt of permits or government approvals, industrial disturbances or other job action,and unanticipated events related to health, safety and environmental matters), decisions made by our partners or co-venturers, social unrest, failure ofsuppliers to meet their contractual commitments and changes in general economic conditions or conditions in the financial markets. Each of the slidestitled “Forward Looking Information” in the individual presentations describe events and uncertainties that could cause actual results to differ materially.

Certain of these risks and the risks described in the slides titled “Forward Looking Information” in each of the individual presentations are described inmore detail in Teck’s annual information form available under Teck’s corporate profile at www.sedar.com and www.sec.gov. Teck does not assume theobligation to revise or update these forward-looking statements after the date of this document or to revise them to reflect the occurrence of futureunanticipated events, except as may be required under applicable securities laws.

Overview and StrategyMarch 30, 2016Don Lindsay, President & Chief Executive Officer

Top ten copper miner in the Americas

#3 zinc miner in the world

Building an energy business

# 1 Producer of steelmaking coal in North America

# 2 Seaborne exporter of steelmaking coal globally

Safety is a core value

Implementing a comprehensive sustainability strategy

Overview and Strategy

Canada’s Largest Diversified Resources Company

3

Overview and Strategy

Senior Management Planned Retirements

Ray ReipasSenior Vice President, Energy

Tim WatsonSenior Vice President, Project Development

Rob ScottSenior Vice President, Zinc

Ian KilgourExecutive Vice President & Chief Operating Officer

4

Overview and Strategy

Senior Management Update

• Continued strong leadership• Closer reporting relationship between GMs and senior executives• Further aligned to current business environment

Dale AndresSVP, Base Metals

Robin Sheremeta

SVP, Coal

Andrew StonkusSVP, Sales & Marketing

Copper Operations

Zinc Operations

Coal Operations

Energy Sales &

Marketing

Base Metals Sales &

Marketing

CoalSales &

Marketing

Alex ChristopherSVP, Exploration, Projects

& Technical Services

ExplorationEngineering & Related Activities

5

Diversification to expand opportunity set

Long life assets

Low half of the cost curve

Appropriate scale

Low risk jurisdictions

Overview and Strategy

Consistent Long-Term Strategy

6

• Based in Vancouver, Canada, with operations in the Americas

• Strategy focused on long life assets in stable jurisdictions

• Sustainability: Key to managing risks and developing opportunities

Strong Resource Position1

With Sustainable Long-Life AssetsCoal Resources ~100 years

Copper Resources ~30 years

Zinc Resources ~15 years

Energy Resources ~50 years

Overview and Strategy

Attractive Portfolio of Long-Life Assets

1. Reserve and resource life estimates refer to the mine life of the longest lived resource in the relevant commodity assuming production at planned rates and in some cases development of as yet undeveloped projects. See the reserve and resource disclosure in our most recent Annual Information Form, available on SEDAR and EDGAR, for additional detail regarding underlying assumptions.

7

Overview and Strategy

Plan to Navigate an Extended Low Price Environment & Emerge Stronger

Strength of our diversified portfolio of long-life assets & resources

Strong operating execution

Target for positive cash flow from core business

Finish building Fort Hills

Protect our strong financial position

8

Overview and Strategy

Core Business Free Cash Flow vs. Development Project Cash Flow

Cost management delivering improvements in Free Cash Flow2, despite weakening prices

Target for positive cash flow

Funding from internal sources in 2016; Current cash balance > remaining capital1

Fort Hills Development Project Core Business

Potential future free cash flow

Teck’s total share of capital $2.94B

Remaining capital (as of February 10th, 2016)

$1.2 B

Teck cash balance(as of February 10th, 2016)

~$1.8 B(100)

-

100

200

Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15C

$ M

illion

s

Free Cash Flow, Before Fort Hills Capex

1. As of February 10, 2016. Based on Suncor’s planned project spending. Sanction capital is the go-forward amount from the date of the Fort Hills sanction decision (October 30, 2013), denominated in Canadian dollars and on a fully-escalated basis.

2. Free Cash Flow is Net Cash from Operations, before changes in Working Capital, less Investing activity excluding Fort Hills capital expenditures, not including proceeds from sales of investments, less interest paid and distributions to minority interests.

9

Overview and Strategy

Near-Term Priorities

10 1. Assumes current commodity prices and exchange rates, Teck’s 2016 guidance for production, costs and capital expenditures, existing US$ debt levels and no unusual transactions.

• Target for positive cash flow from core business

• Fund Fort Hills from internal sources in 2016

• Protect our strong financial position− Target for US$3B credit facility

to remain undrawn in 2016− Expect year-end cash balance

of >$500M1

− Evaluating opportunities to further strengthen liquidity

Overview and Strategy

Options to Strengthen Liquidity

• Further cost & capital reductions

• Asset value realization opportunities− Infrastructure assets−Non-operating assets−Additional precious metal

streaming transactions−Minority interests in assets−Royalties on future cash flows

11

FinanceMarch 30, 2016Ron Millos, Senior Vice President, Finance & Chief Financial Officer

Finance

Agenda

2015 Overview

Balance Sheet & Liquidity

2016 Guidance & Overview

Summary

3

Diversified gross profit

Focus on costs has delivered improvements in free cash flow

Strong balance sheet and liquidity

Extended debt maturities consistent with long-life assets

Well positioned to finance capital spending plans

4

Finance

Navigating Difficult Market Conditions

Guidance Results

Steelmaking CoalProduction1 25-26 Mt 25.3 Mt

Site costs C$49-53/t C$45/t

Transportation costs C$37-40/t C$36/t

Combined costs2 C$86-93 /t C$83/tUS$64/t Lower unit costs at all mines

CopperProduction 340-360 kt 358 kt Record mill throughput at Antamina

Cash unit costs3 US$1.45-1.55 /lb US$1.45/lb Lower unit costs at all mines

ZincMetal in concentrate production4 635-665 kt 658 kt

Refined production 280–290 kt 307 kt Record production at Trail

Capital Expenditures5 $2.3B $2.2B Lower capex

Finance

Solid Delivery Against 2015 Guidance

1. Reflects mid-year revision for temporary shutdowns.2. Combined coal costs are site costs, inventory adjustments and transportation costs.3. Net of by-product credits.4. Including co-product zinc production from our copper business unit.5. Including capitalized stripping.

5

0%

25%

50%

75%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Coal Copper Zinc

Gross Profit Before Depreciation and Amortization

Finance

Diversified Gross Profit (before depreciation & amortization)

6

Teck has good leverage to stronger zinc and copper markets, and benefits from the weaker Canadian dollar

Finance

The Value of Our Diversified Business Model

Cash Operating Profit 2015

Production Guidance1

Unit of Change

Estimated Profit 2

EstimatedEBITDA2

$C/$US C$0.01 $22M /$.01∆ $34M /$.01∆

Coal 25.5 Mt US$1/tonne $23M /$1∆ $35M /$1∆

Copper 312 kt US$0.01/lb $6M /$.01∆ $9M /$.01∆

Zinc 940 kt US$0.01/lb $9M /$.01∆ $14M /$.01∆

2016 Leverage to Commodities & FX

1. Based on mid-point of 2016 guidance ranges. Zinc includes 645 kt of zinc in concentrate and 295 kt of refined zinc.2. Based on budgeted commodity prices and a 1.40 CAD/USD exchange rate. The effect on our profit and EBITDA will vary with

commodity price and exchange rate movements, and sales volumes.

Coal~30%

Copper 35%

Zinc35%

Base Metals~70%

7

Finance

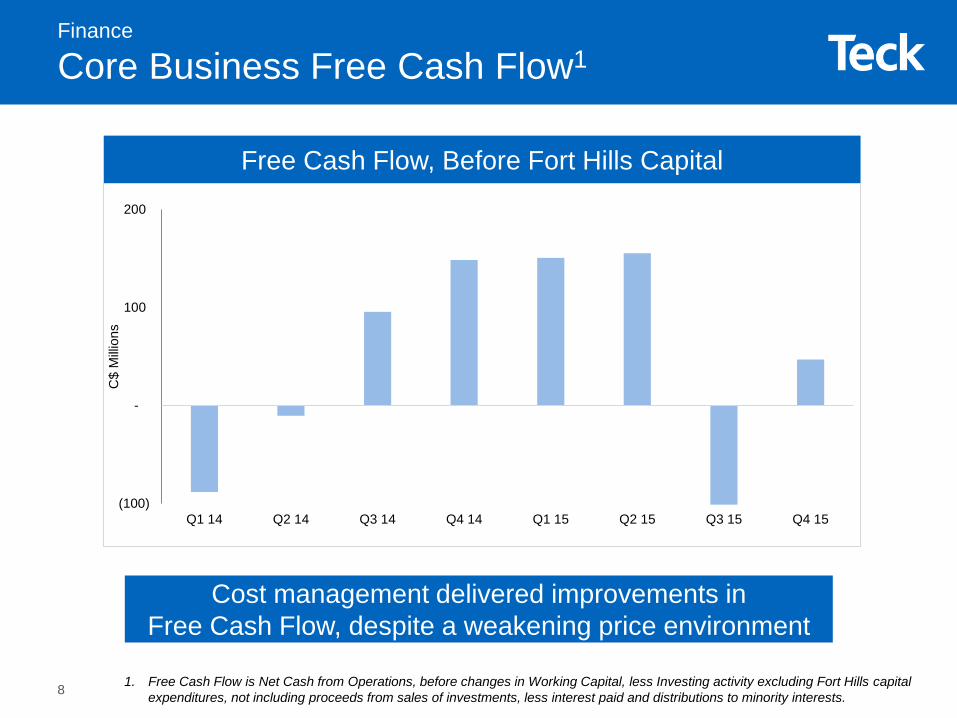

Core Business Free Cash Flow1

Free Cash Flow, Before Fort Hills Capital

(100)

-

100

200

Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15

C$

Milli

ons

Cost management delivered improvements in Free Cash Flow, despite a weakening price environment

1. Free Cash Flow is Net Cash from Operations, before changes in Working Capital, less Investing activity excluding Fort Hills capital expenditures, not including proceeds from sales of investments, less interest paid and distributions to minority interests.8

Finance

Agenda

2015 Overview

Balance Sheet & Liquidity

2016 Guidance & Overview

Summary

9

0

500

1000

1500

2000

2500

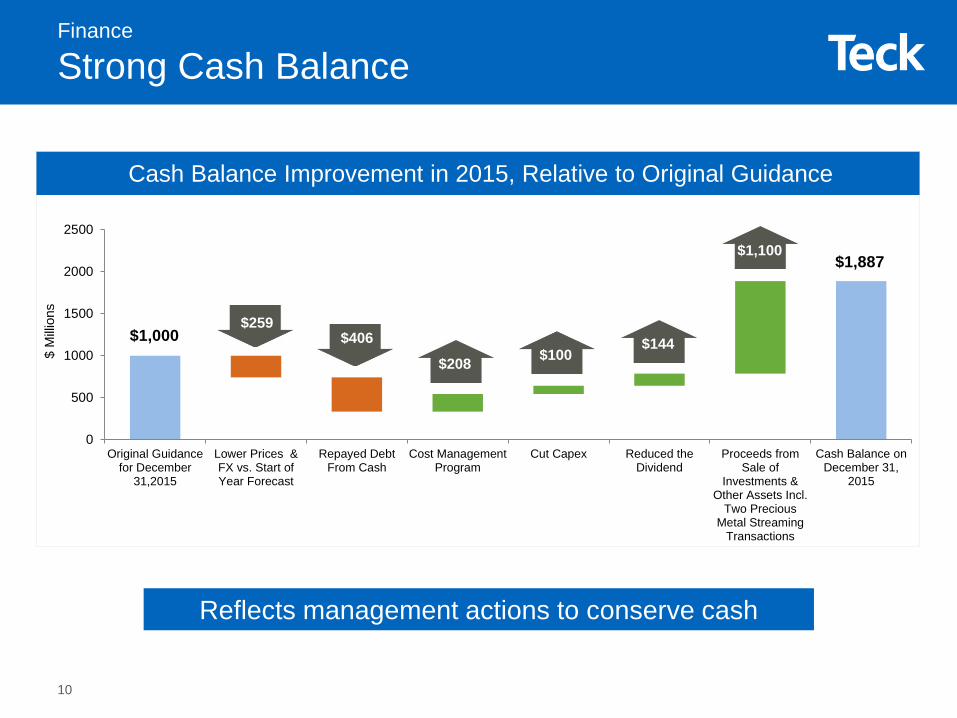

Original Guidancefor December

31,2015

Lower Prices &FX vs. Start ofYear Forecast

Repayed DebtFrom Cash

Cost ManagementProgram

Cut Capex Reduced theDividend

Proceeds fromSale of

Investments &Other Assets Incl.

Two PreciousMetal Streaming

Transactions

Cash Balance onDecember 31,

2015

Cash Balance Improvement in 2015, Relative to Original Guidance

Finance

Strong Cash Balance$

Milli

ons

$1,000

$1,887

$208 $100

$1,100

$259$406 $144

Reflects management actions to conserve cash

10

$0

$250

$500

$750

$1,000

$1,250

$1,500

$1,750

$2,000

$2,250

$2,500

$2,750

$3,00020

16

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

US$

M

11

• No debt due until 2017− Weighted average maturity ~14 years− Weighted average coupon (interest rate) ~4.8%− Average maturity <US$600M

• Debt to debt-plus-equity ratio 37%1

2017Q1: US$300MQ3: US$300M

Repaid US$300M in notes in Q4 2015

As at December 31, 2015.

Finance

Long-Dated Debt Maturity Profile

Amount (M) Commitment Maturity

Letters of Credit Limit

($M)

Letters of Credit Drawn

($M)

Total Available

($M)

US$3,000 Committed July 2020 US$1,000 Undrawn US$3,000

US$1,200 Committed June 2017 None US$740 US$460Expect to keep available for letter of credit requirements

~C$1,700 Uncommitted n/a n/a ~C$1,500 ~C$200

• Unsecured; any borrowings rank pari passu with outstanding public notes• Only financial covenant is debt to debt-plus-equity of <50%; excludes issued letters of credit• Availability not affected by commodity price changes or credit rating actions• Available for general corporate purposes

Ample liquidity for remaining Fort Hills capital expenditure of ~C$1.2B

Current cash balance of C$1.5B (3/4/16) and substantial credit facilities1:

1. As of December 31, 2015. Assumes a 1.38 CAD/USD exchange rate.

Finance

Strong Liquidity

12

Finance

US$1.2B Committed Credit Facility

US$740M drawn for letters of credit at Dec 31st• US$672M for power purchase agreements for QB2

− Requirements decrease: • If/when QB2 is sanctioned and certain project milestones are reached

− Requirements go away: • If/when QB2 reaches commercial production, regardless of credit rating; or• When Teck regains an investment grade credit rating

− Actively reviewing options to onsell power

• C$93M for transport service agreements related to Fort Hills− If all counterparties request financial assurances, aggregate requirement could

increase up to C$550M by year end 2016 and C$650M by year end 2017− Aggregate maximum requirement decreases to C$450M post the relevant

in-service date (late 2017 and beyond)− Requirements go away when Teck regains an investment grade credit rating

13

Finance

C$1.7B Uncommitted Credit Facilities

• C$1.5B drawn for letters of credit, mostly for reclamation obligations− Export Development Canada

facility renewed annually− Other facilities are uncommitted

• Assessing surety bonds to reduce bank exposure

Canadian Banks

EDC

Others

Uncommitted credit facilities are with relationship banks that have been supportive of Teck through the industry cycles

14

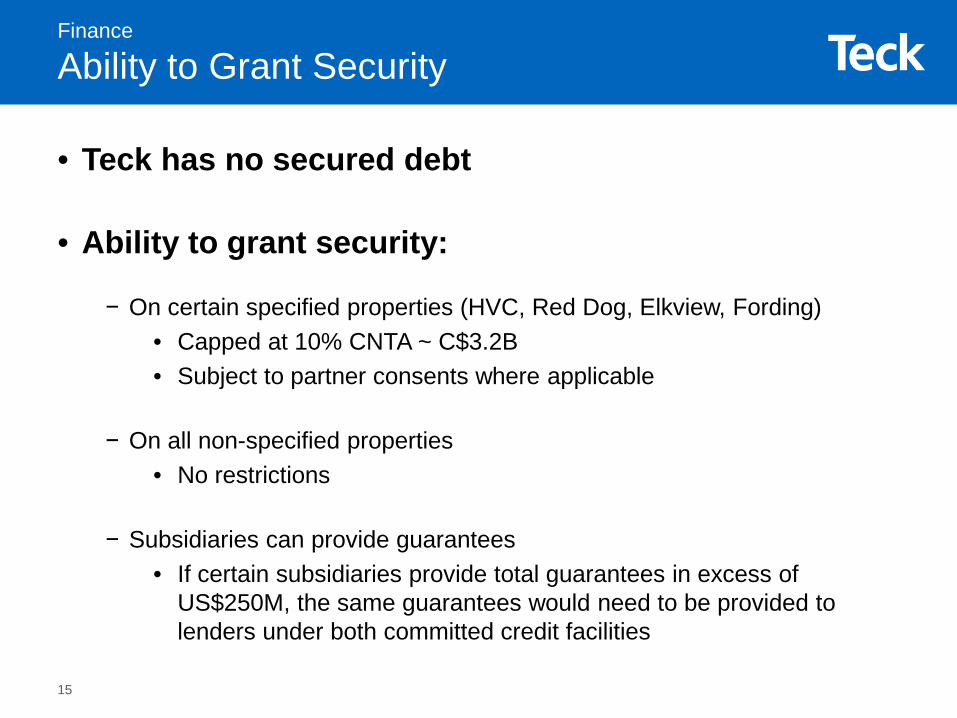

• Teck has no secured debt

• Ability to grant security:

− On certain specified properties (HVC, Red Dog, Elkview, Fording) • Capped at 10% CNTA ~ C$3.2B• Subject to partner consents where applicable

− On all non-specified properties• No restrictions

− Subsidiaries can provide guarantees• If certain subsidiaries provide total guarantees in excess of

US$250M, the same guarantees would need to be provided to lenders under both committed credit facilities

Finance

Ability to Grant Security

15

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000Ja

n-05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

14

Jan-

15

Jan-

16

Moody's S&P Fitch DBRS London Metal Exchange Index (Right Axis)

BBB/Baa2

BBB-/Baa3

BB+/Ba1

BB/Ba2

BB-/Ba3

BBB+/Baa1

B+/B1

B/B2

B-/B3

A+/A1

A/A2

A-/A3

Inve

stm

ent G

rade

Non

-Inve

stm

ent G

rade

Teck Credit Ratings vs. London Metal Exchange Index

Finance

Credit Ratings Reflect Commodity Prices

16

Finance

Agenda

2015 Overview

Balance Sheet & Liquidity

2016 Guidance

Summary

17

2015 Results 2016 GuidanceSteelmaking Coal

Production 25.3 Mt 25-26 MtSite costs $45/t $45-49/tCapitalized stripping $16/t $11/t1

Transportation costs $36/t $35-37/tTotal cash costs2 $99/t

(US$76/t)$91-97/t

(US$65-69/t)Copper

Production 358 kt 305-320 ktC1 unit costs3 US$1.45/lb US$1.50-1.60/lbCapitalized stripping US$0.21/lb US$0.21/lb1

Total cash costs4 US$1.66/lb US$1.71-1.81/lbZinc

Metal in concentrate production5 658 kt 630-665 ktRefined production 307 kt 290-300 kt

Finance

2016 Production & Site Cost Guidance

1. Approximate, based on capitalized stripping guidance and mid-point of production guidance range.2. Steelmaking coal unit cost of sales include site costs, inventory adjustments and transport costs. Total cash costs

are unit cost of sales plus capitalized stripping. 3. Net of by-product credits.4. Copper total cash costs include cash C1 unit costs (after by-product margins) and capitalized stripping. 5. Including co-product zinc production from our copper business unit.

18

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2012 2013 2014 2015 2016Guidance

New MineDevelopment

MajorEnhancements

Sustaining Capital

CapitalizedStripping

$M

Finance

Achieved Capital Spending Reductions

Total Capital Expenditures 2012-2016F

19

Finance

Agenda

2015 Overview

Balance Sheet & Liquidity

2016 Guidance & Overview

Summary

20

• Core business to remain cash flow positive1

• All operations to generate positive cash flow2

• Achieve sustainable cost savings and capital reductions / deferrals

• C$500M minimum cash balance at year end, with no new debt

• Maintain sufficient liquidity

Finance

2016 Financial Objectives

1. Core business excludes the Fort Hills development project.2. After sustaining capital and capitalized stripping.21

OperationsMarch 30, 2016Ian Kilgour, Executive Vice President & Chief Operating OfficerRobin Sheremeta, Vice President, Coal OperationsDale Andres, Senior Vice President, CopperRob Scott, Senior Vice President, Zinc

Operations

Agenda

Overview

Steelmaking Coal

Copper

Zinc

Summary

3

Staying true to Teck’s values

Delivering results

Building operational excellence

Disciplined capital spending

Focused growth pipeline

4

Operations

Meeting the Challenge

Operations

Staying True to Teck’s Values

Safety

Sustainability

Integrity

Respect

Excellence

Courage

5

Operations

Safety is a Core Value

Courageous Safety LeadershipVisible Felt Leadership

Frontline Leadership Development

Incident InvestigationHealth & Safety BenchmarkingControl Effectiveness Reviews

Risk ManagementStandards & Best Practices

Technology Enablers

6

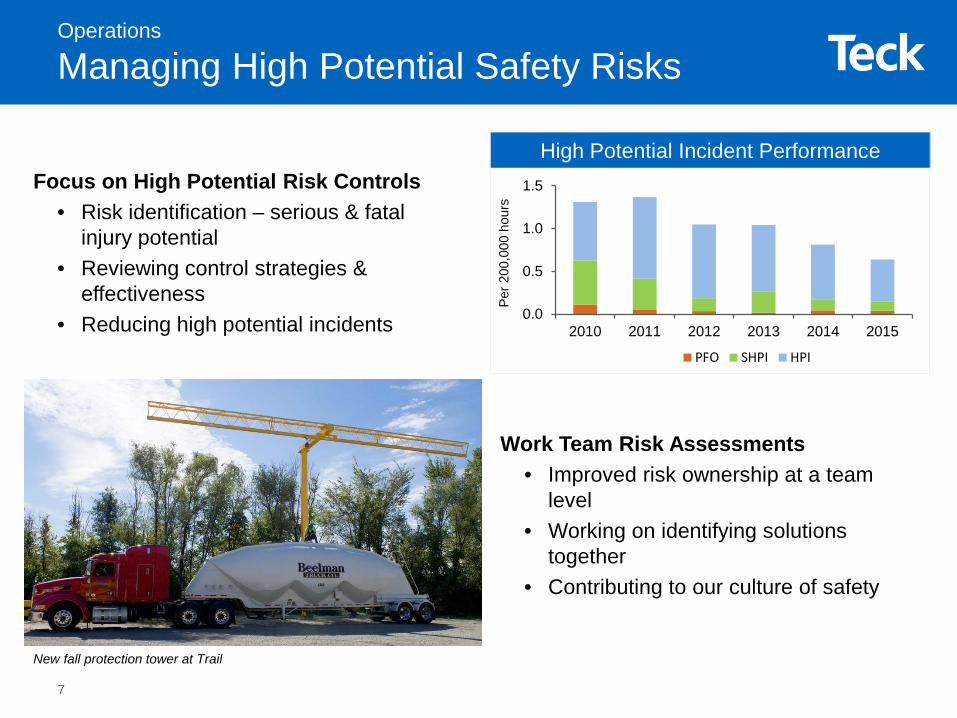

Operations

Managing High Potential Safety Risks

Focus on High Potential Risk Controls• Risk identification – serious & fatal

injury potential• Reviewing control strategies &

effectiveness• Reducing high potential incidents

High Potential Incident Performance

0.0

0.5

1.0

1.5

2010 2011 2012 2013 2014 2015

PFO SHPI HPI

Per 2

00,0

00 h

ours

Work Team Risk Assessments• Improved risk ownership at a team

level• Working on identifying solutions

together• Contributing to our culture of safety

New fall protection tower at Trail

7

Operations

Sustainability Incorporated in Operations

Sustainable practices are the “right thing to do” and have a solid business case

Formalizing our commitment to working with Indigenous Peoples

Enhancing air quality in areas near our operations

Reducing GHG remissions and energy costs through haul truck efficiency

Strengthening diversity at operations

8

Operations

LNG Haul Trucks – Status Update

9

• Six pilot trucks have been converted to “dual-fuel” - LNG and diesel (four 830E’s, two 930E’s); first in Canada

• Current substitution rates achieved: 25 – 40% (target >35%)• Pilot objective is to confirm the business case (cost and sustainability) for a Teck

wide application; focus is on safety, sustainability and operability• Establishing reliability of the LNG systems • Optimizing LNG substitution rates and monitoring GHG emissions

9

0.00

0.50

1.00

1.50

2.00

2.50

2012 2013 2014 2015 2016F*

Before by-product credits

After by-product credits

US$

/lb

0

50

100

150

200

250

300

350

400

2012 2013 2014 2015

US$

per t

onne

of p

rodu

ctio

n

0

10

20

30

40

50

60

70

80

90

2012 2013 2014 2015 2016F*

OperatingCapitalized Stripping

C$/

tOperations

Delivering Results in Unit Cost Management

Copper Cash Costs3

Achieved significant unit cost reductions, and expect further reductions in 2016

Steelmaking Coal Total Site Costs1

2

1. Total site costs are site costs, inventory write-downs and capitalized stripping, excluding depreciation. 2. Operating costs include site costs and inventory write-downs.3. By-product credits reduced cash costs by US$0.19/lb in 2015. Assumes US$0.19/lb in 2016.4. Zinc cash costs are Red Dog site costs per tonne of combined zinc and lead production.* 2016F based on mid-point of guidance range.

Zinc Cash Costs4

10

- $50 $100 $150 $200 $250 $300

Other ($1M)Productivity - Utilization (e.g Op Delays) ($5M)

Components (life/cost) ($7M)Freight savings ($7M)

Over time reduction ($12M)Productivity - Enablers, multiple levers ($16M)

Plan optimization ($21M)Pricing Improvements ($20M)

Equipment Rental Savings ($20M)Mining Productivity - Availability ($23M)

Admin savings ($55M)Idling & Energy Savings ($64M)

Consumables ($64M)Employee Cost Reduction ($134M)

Contractors/Consultants Reduction ($160M)Mining Productivity - Throughput ($215M)

2013 Initiatives 2014 Initiatives 2015 Initiatives

CAD$ millions(all USD savings translated using CAD/USD rate of 1.384)

~$820M of Annualized Savings in 2015, from Major Cost Reduction Initiatives in 2013-2015

Annualized 2015 Savings from Major Cost Reduction Program Initiatives

Targeting an additional $300M in operating cost reductions in 2016; A total of >$1B of annualized savings identified and included in 2016 plan

Operations

Embedding Sustainable, Ongoing Operating Cost Reductions in the Organization

11

Planning

Blasting

Loading and Hauling

CrushingStockpiling

Geology and Metallurgy

Grinding

Optimizing value across the production process to breakdown silos and drive continuous improvement

Operations

One Teck: Mine to Mill Optimization

Increased Margin

Lower Unit Costs

More Product

Sharing Best Practices

12

Operations

Disciplined Project Execution

Our project delivery framework strengthens our ability to deliver projects on time and on budget

Highland Valley Crusher Relocation Project

Teck Project Delivery Framework • Significant progress in

permitting practices

• Tight alignment between permitting and engineering

• Integrating sustainability into project framework

Pend Oreille Restart

West Line Creek Water Treatment Plant

13

Robust People Development Systems are Key• Performance management systems that

align organizational goals and objectives with personal goals

• Company-wide development programs for all levels of supervision and management, including operational based leadership development - To address the demand on increasing leadership

competence to drive business results

• Internal career opportunities- Ensuring ‘the best people in the right jobs’ at the

right time

14

Operations

People Achieve Excellence

We attract, engage and develop people whose passion, skills and motivation lead our journey in safety, sustainability and productivity

ProgramBegan

# of Cohorts

# of Participants

Leading for the Future (LFF) 2011 40 844

~70% of eligible population

Leading for Excellence (LFX) 2011 33

462~70% of eligible population;Includes 30 senior leaders

The LeadershipChallenge (LC) 2014 16 271

~15% of eligible population

0

200

400

600

800

1000

1200

1400

2010 2011 2012 2013 2014 2015 2016F

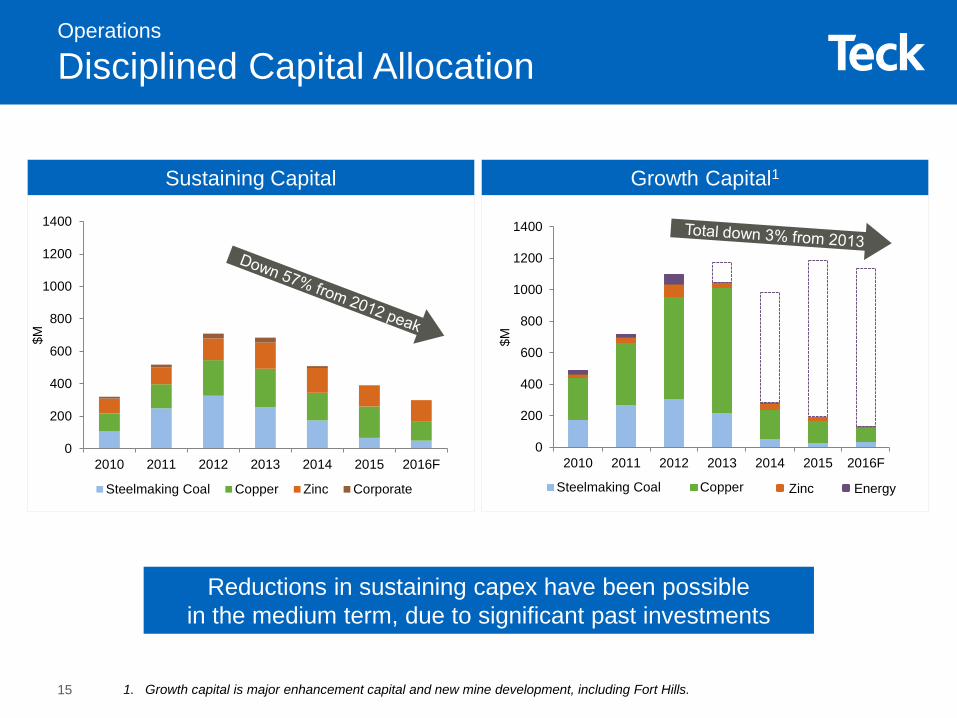

$M

Steelmaking Coal Copper Zinc Corporate

15

Operations

Disciplined Capital Allocation

Reductions in sustaining capex have been possible in the medium term, due to significant past investments

Growth Capital1Sustaining Capital

1. Growth capital is major enhancement capital and new mine development, including Fort Hills.

0

200

400

600

800

1000

1200

1400

2010 2011 2012 2013 2014 2015 2016F

$MSteelmaking Coal Copper Zinc Energy

CoalWell established with capital efficient growth options

Strong platform combined with diverse portfolio of options allows us to be selective in terms of commodity and timing

Completed In Construction Pre-Sanction

CopperStrong platform with substantial growth options

ZincWorld-class resource combined with integrated assets

EnergyBuilding a new business through partnership

Trail #1 Acid Plant

HVC Mill Optimization

Pend Oreille Restart

Fort Hills

Elk Valley Brownfield (4 Mpta)

Operations

Staged Growth/Value Pipeline

Red Dog Satellite Deposit – Anarraaq

San Nicolas (Cu-Zn)

Elk Valley Brownfield (Replacement 4Mpta) Quintette/Mt. Duke

Frontier

Lease 421

QB Phase 2

Corridor

Mesaba

ZafranalHVC Brownfield

Galore/Schaft Creek

Cirque

Future Options

Trail #2 Acid Plant

Medium-term Growth Options

Elk Valley Brownfield

Antamina Brownfield

Red Dog Satellite Deposits

Neptune Terminals to 18Mtpa

16

Staying true to Teck’s values

Delivering results

Building operational excellence

Disciplined capital spending

Focused growth pipeline

17

Operations

Meeting the Challenge

Operations

Agenda

Overview

Steelmaking Coal

Copper

Zinc

Summary

18

Steelmaking Coal

Focused on Today; Prepared for Tomorrow

19

Improving efficiency

Continuing to lower costs

Maintaining future potential

Steelmaking Coal

An Integrated Long Life Coal Business

20

Prince Rupert

Ridley Terminal

Vancouver

Prince George Edmonton

Calgary

Westshore Terminal

Quintette

Cardinal River

Elk Valley

Kamloops

British Columbia

Alberta

Seattle

Elkford

Sparwood

Hosmer

Fernie

Fording River

Greenhills

Line Creek

Elkview

Coal Mountain

ElcoElk Valley

1,150 km

• >1 billion tonnes of reserves support 26 Mt of production for many years• Geographically concentrated in the Elk Valley• Established infrastructure and capacity with mines, railways and terminals• Only steelmaking coal mines still operating in Canada; competitive globally

Neptune Terminal

20

Coal MountainPhase 2

20

Ongoing improvement in safety performance

Achieving top quartile truck and shovel productivities

Maintaining cash positive operations

Targeting opportunities to lower maintenance and procurement costs

21

Steelmaking Coal

Continued Operational Excellence

80%

87%88%

97%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015

% o

f Ben

chm

ark

Teck Coal Truck Productivities

Significant annualized value in truck productivity improvements

1. All-in sustaining costs are in inclusive of cost of sales, capitalized stripping and sustaining capital expenditures.

50

75

100

125

150

175

200

2012 2013 2014 2015 2016F

$/to

nne

(CDN

)

All-in Sustaining Costs Transport Coal Price

25% cost reduction from 2012 to 2016

Cost management delivers positive cash margin despite weakening i

1

197

125

76

81

0

50

100

150

200

250

300

350

400

450

500

2013 2014 2015 2016

$ (m

illion

s)

2013 Savings 2014 Savings 2015 Savings 2016 Target

Highlights:• Truck productivity improvements achieved

$145M in sustainable savings • Labour improvements resulted in $90M

savings• $74M savings in contractor management

initiatives

Highlights:• Reduction of 587 employees since

December 2013• Reduction of 360 employees since the May

2015 hiring freeze• Additional planned reduction of 99

employees in 2016

Steelmaking Coal

Cost Reduction & Workforce 2013-2015

~$400M of sustainable annual cost reductions to date; targeting >$81M of additional savings in 2016

Coa

l Hiri

ng F

reez

e

Achieving balanced workforce profile to manage production to market conditions

Total Annualized Savings ~$400M

4,711

4,463

4,124 4,025

5,000

5,400

5,800

6,200

6,600

7,000

3,000

3,400

3,800

4,200

4,600

5,000

Dec-13 Dec-14 Dec-15 2016

Tonn

es/E

mpl

oyee

# Em

ploy

ees

Workforce Productivity

22

5635 34

1

37

28 26

21

128

2012 2015 2016F

Total cash costs down US$46/t from 2012 to 2016F2

Total Cash Costs2

23

US$/t 20123 2015 2016F4 Change

Site $56 $35 $34 -39%

Inventory Adjustments $0 $1 $0 n/a

Transportation $37 $28 $26 -29%

Unit Cost of Sales (IFRS) $93 $64 $60 -35%

Capitalized Stripping $21 $12 $84 -61%

Total Cash Costs2 $114 $76 $68 -40%

Sustaining Capital $14 $2 $15 -90%

All In Sustaining Costs $128 $78 $69 -45%

1. In US dollars per tonne. Assumes a Canadian dollar to US dollar exchange rate of 1.00 in 2012, 1.28 in 2015 and 1.38 in 2016.2. Steelmaking coal unit cost of sales include site costs, inventory adjustments and transport costs. Total cash costs are unit cost

of sales plus capitalized stripping. All in sustaining costs are total cash costs plus sustaining capital.3. Assumes that capitalized stripping was reported from January 1, 2012.4. Based on the mid-point of guidance ranges.5. Approximate, based on capital expenditures guidance and mid-point of production guidance ranges.

IFRS

$114

$76

IFRS IFRS

$68

Site

Inventory

Transport

Capitalized Stripping

Steelmaking Coal

Highly Competitive Costs1

West Line Creek Treatment Plant• First of the water treatment facilities planned for the

Elk Valley; total cost $120M• Operating at design flowrate (7,500 m3 per day) and

achieving design selenium and nitrate reductionsFording River South Treatment Plant• Facility to be operational by 2019, using learnings

from West Line Creek • Project capital estimate of <$150M

Elk Valley Water Quality Plan Costs• Capex as per previous guidance for both plants,

and expectation that this will continue as design and construction improvements are incorporated

• Costs included in sustaining capital• Continuing research and development into

alternative processes which have potential to further reduce costs

24

Steelmaking Coal

Achieving the Elk Valley Water Quality Plan

Overview of FROAWTF-S Location and Streams

Steelmaking Coal

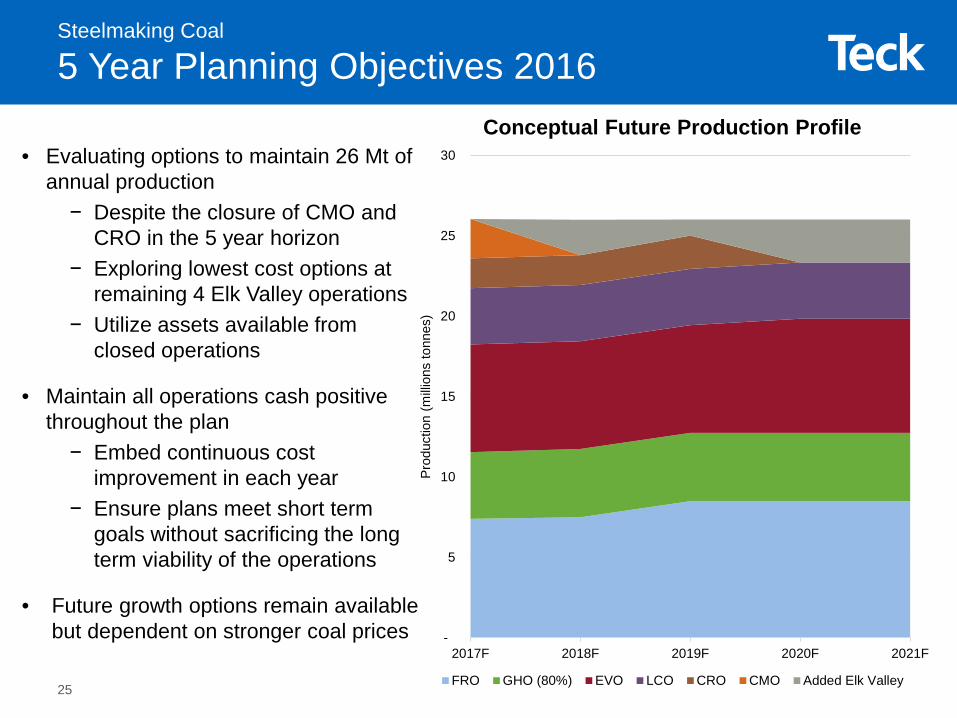

5 Year Planning Objectives 2016

• Evaluating options to maintain 26 Mt of annual production− Despite the closure of CMO and

CRO in the 5 year horizon− Exploring lowest cost options at

remaining 4 Elk Valley operations− Utilize assets available from

closed operations

• Maintain all operations cash positive throughout the plan− Embed continuous cost

improvement in each year− Ensure plans meet short term

goals without sacrificing the long term viability of the operations

• Future growth options remain available but dependent on stronger coal prices -

5

10

15

20

25

30

2017F 2018F 2019F 2020F 2021F

Prod

uctio

n (m

illion

s to

nnes

)

Conceptual Future Production Profile

FRO GHO (80%) EVO LCO CRO CMO Added Elk Valley25

Steelmaking Coal

Focused on Today; Prepared for Tomorrow

26

Improving efficiency

Continuing to lower costs

Maintaining future potential

Operations

Agenda

Overview

Steelmaking Coal

Copper

Zinc

Summary

27

28

Solid assets in low-risk jurisdictions

Cost reduction

Productivity and throughput improvements

Advancing best project opportunities

Copper

Finding Opportunity in Challenges

• Operating assets with long lives capable of multiple price cycles

• Strong resource base to leverage- Opportunities at existing operations

to extend mine lives significantly- Disciplined approach to greenfield

project portfolio

0

100

200

300

400

500

2012 2013 2014 2015 2016E* 2017-2019E

Tonn

es(0

00’s

)

Cu Cathode Cu in Concentrate

Copper Production

* 2016E represents the mid-point of 2016 guidance.

Copper

Long-Life Assets Focused on the Americas

29

0.2

0.3

0.4

100

125

150

175

200

2012 2013 2014 2015 2016E* 2017-2019E

2020+

Grade (%

)

Tonn

es p

er d

ay (0

00’s

)

Mill Throughput Copper Grade R&R Grade

Lower Near-Term Copper Production

Focusing on sustainable cost reduction strategies to unlock potential expansion and extension options

* 2016E represents the mid-point of 2016 guidance.

• High-grade phase ends late-2016• Aggressive cost reduction plans• Options to expand production & mine life

Copper

Highland Valley Grade Decline in the Short-Term

30

0.60

0.80

1.00

1.20

50

100

150

200

2011 2012 2013 2014 2015 2016E* 2017-2019E

Grade (%

)

Tonn

espe

r day

(000

s)

Mill Throughput Copper Grade

Record Throughput in 2015Strong Cost Position

* 2016E represents the mid-point of 2016 guidance.

Antamina

• New three-year collective agreement signed• Increasing zinc production over the next 5 years• Copper and zinc grades rising• Strong cost position; driving further improvements

Copper

Antamina’s Resources Support a Long Mine Life

31

Copper

Removing Barriers to Unlocking Value at Andacollo

0.2

0.4

0.6

30

45

60

2012 2013 2014 2015 2016E* 2017-2019E

Grade (%

)

Tonn

es p

er d

ay (0

00’s

)

Mill Throughput Copper Grade

Throughput Offsets Grade Decline1

30

60

90

2012 2013 2014 2015 2016E* 2017-2019EC

oppe

r pro

duct

ion,

t (0

00’s

)

Copper in Concentrate Copper Cathode

Extending Cathode Production Creates Value

1. Grade represents total copper grade of ore sent to the mill only, excluding the cathode operation.* 2016E represents the mid-point of 2016 guidance.

• Four-year labour agreements settled• Throughput improvement projects underway• Further cost reductions in progress• Extending cathode production to 2020

32

Copper Cutting Costs & Evaluating Options at Quebrada Blanca

RIPIOS

RIPIOS

DUMP

• Labour agreements settled through 2017• Geotechnical issues mitigated• Implementing aggressive cost reduction initiatives• Evaluating options to supplement production

-

20

40

60

80

2012 2013 2014 2015 2016E*

Unit C

osts ($/lb)Tonn

es (0

00’s

)

Cu Production Unit Costs

2

Cash Costs Maintained Against Declining Production

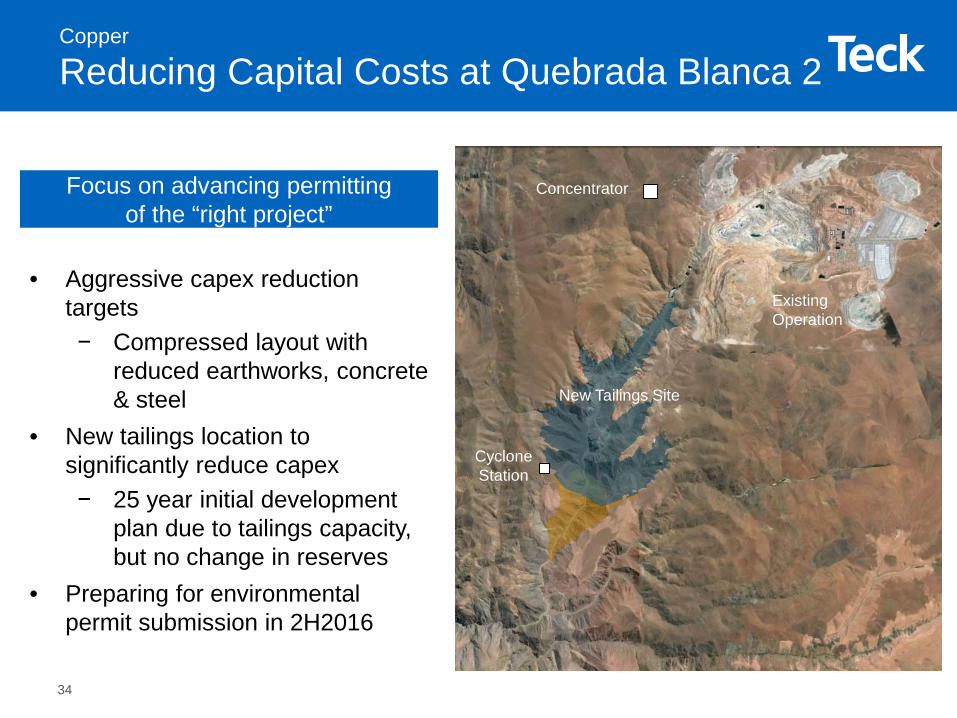

* 2016E represents the mid-point of 2016 guidance.33

• Aggressive capex reduction targets− Compressed layout with

reduced earthworks, concrete & steel

• New tailings location to significantly reduce capex− 25 year initial development

plan due to tailings capacity, but no change in reserves

• Preparing for environmental permit submission in 2H2016

Copper

Reducing Capital Costs at Quebrada Blanca 2

Concentrator

CycloneStation

New Tailings Site

Existing Operation

Focus on advancing permitting of the “right project”

34

35

• Committed to building strong, mutually beneficial relationships with stakeholders and communities

• Capital smart partnership- Common infrastructure- Longer mine life- Reduced environmental footprint- Enhanced community benefits

• Short term priorities- Community engagement &

participatory planning- Evaluate strategic options &

prefeasibility study

35

Before: Duplicate Infrastructure

After: Common Infrastructure

Copper

Building Partnerships: Project Corridor

• Absolute cost reduction• Productivity improvements• Labour force reduction• Contractor reduction• Managing supply contracts and usage

Copper

Intense Focus on Costs & Productivity

36

37

Solid assets in low-risk jurisdictions

Cost reduction

Productivity and throughput improvements

Advancing best project opportunities

Copper

Finding Opportunity in Challenges

Operations

Agenda

Overview

Steelmaking Coal

Copper

Zinc

Summary

38

• Red Dog has stable zinc production despite declining grade• Pend Oreille moving to a higher proportion of secondary mining,

which improves selectivity and ore availability• Increased refined zinc production at Trail with enhanced process

stability of a new acid plant • Value creating roadmaps for Red Dog and Pend Oreille

39

ZincPoised to Capitalize on Improving Fundamentals

Mill Throughput vs. Grade

40

Stable zinc metal production despite declining grade

• Declining zinc grade offset by increasing mill throughput

• Increasing mill throughput has resulted in reduced unit cost

• Exploring opportunities to further increase mill throughput

ZincRed Dog: Maintaining Zinc Metal Production

Expected Production 2017-2019

• 500,000-550,000 tonnes of zinc

• 100,000-110,000 tonnes of lead10

15

20

25

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Gra

de %

Mill

Thro

ughp

ut (k

t)

Grade

Throughput

41

Su-LikAktigirukAnarraaq

Red Dog Mine

NANA Lease100% Teck

Red Dog District Drilling 2004-2015

Significant regional land position

• 350 km2 of highly prospective NANA and State lands with identified exploration targets

• Ongoing drilling programs to enhance resource certainty and define future developments

ZincRed Dog: Significant Exploration Potential

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Mine Regional Exploration

41

1980 – Red Dog Main and Qanaiyaq drilled

1989 – First ore from Main

1995 – Aqqaluk and Paalaaqdiscovered

2012 - First ore from Aqqaluk

2016 – First ore from Qanaiyaq

35 years of discovery and development42

ZincRed Dog: Mine Area Deposits

1999 Discovery: Anarraaq

2001 Discovery: Aktigiruk

Underground targets

Plan & section at same scale as previous slide

43

Anarraaq–Aktigiruk corridor

ZincRed Dog: Regional Exploration Discoveries

2cm

1.1 m @ 42.2% Zn, 14.7 % Pb, 558g/t Ag

2cm

1.9 m @ 24.6% Zn, 6.3 % Pb, 53g/t Ag

Zinc

Red Dog: Anarraaq High Grade Intercepts Demonstrate Significant Resource Potential1

DDH171854.7m @ 15.7%Zn, 4.0% Pb, 106g/t AgIncl. 11.2m @ 34.2% Zn, 11.5% Pb, 382g/t Ag

DDH1714 42m @ 18.3% Zn, 4.5% Pb, 82g/t AgIncl. 23.4m @ 23.2% Zn, 5.2% Pb, 74g/t Ag44

Industry Average Zinc Grades Falling

High Grade Anarraaq Intercepts

Red Dog zinc grades are much higher than industry average

0

5

10

15

20

25

2009 2010 2011 2012 2013 2014 2015

Gra

de %

Weighted Average Industry Grade

Red Dog

1. The scientific and technical information disclosed has been reviewed and approved by Rodrigo Marinho, P.Geo., Technical Director, Reserve Evaluation, Teck who is a Qualified Person under NI 43-101. For further information, please see Teck’s most recent Annual Information Form.

• Underground mine• Road access• Power generation

• Access to Aktigurik• Resource upside

• Resource drilling• Development schedule

and capital

• SAG motor upgrades• Fine grinding• Additional flotation

• Lower ore cut-off• Further throughput

increase

• Mill space• Generator capacity

Components

Opportunities

Challenges

• Crushing & sorting equipment

• Reactive ore

• Higher metal recovery• Lower cut-off• Increase throughput

• Screening technology

• Underground mine• Access from Anarraaq

• Resource upside

• Resource drilling• Development schedule

and capital

Creating value through long-term planning45

Mill Throughput Increase

AnarraaqUnderground

Ore Sorting

AktigirukUnderground

Current Life of Mine Plan

Legend

Zinc

Red Dog: Value Creating Road Map

Ore Production from Secondary Mining

46

Stabilizes ore production, which will result in reduced unit costs

• Room and pillar stopes developed by drift mining

• Initial ore supply entirely from primary mining of stopes – limited broken ore inventory

• Secondary mining increases as stopes established and pillars can be removed as the mining front retreats – larger broken inventory

0

100

200

300

400

500

600

700

800

900

2004 2005 2006 2007 2008 2015 2016F

Ore

Min

ed (

ooo’

ston

nes)

Primary Mining (Drift)

Secondary Mining (Pillar)

Zinc

Pend Oreille: Increasing Secondary Mining

• Tailings back fill• Resource in adjacent

to existing workings

• Higher grades• Additional life

• Resource drilling• Development schedule

and capital

• Dry stack tailings• Resources in YH1

• Higher grades and recovery

• Additional mine life

• Drilling required• Permitting of tailings

Components

Opportunities

Challenges

Creating value through long-term planning47

Possible Life Extension

to 2028

Ongoing Exploration to Define Future

ResourcesOre Sorting

Current Life of Mine Plan

Legend

Zinc

Pend Oreille: Value Creating Road Map

Acid Plant Reliability –Unplanned Downtime and Refined Zinc Production

260

265

270

275

280

285

290

295

300

305

310

0%

1%

2%

3%

4%

5%

6%

7%

8%

2010 2011 2012 2013 2014 2015

Ref

ined

Zin

c Pr

oduc

tion

(000

's t)

Unp

lann

ed D

ownt

ime

(%)

48

Increased refined zinc production with enhanced process stability of a new acid plant

New Acid Plant

• Commissioned May 2014; first full year 2015

• Removes SO2 gas created from roasting sulphideconcentrates.

• Replaced unreliable 40-year old acid plants

Focus on Cost Reduction

• Personnel utilization

• Zinc production

Zinc

Trail: More Reliable Acid Plant

Unplanned Downtime

• Red Dog has stable zinc production despite declining grade• Pend Oreille moving to a higher proportion of secondary mining,

which improves selectivity and ore availability• Increased refined zinc production at Trail with enhanced process

stability of a new acid plant • Value creating roadmaps for Red Dog and Pend Oreille

49

ZincPoised to Capitalize on Improving Fundamentals

Operations

Agenda

Overview

Steelmaking Coal

Copper

Zinc

Summary

50

Staying true to Teck’s values

Delivering results

Building operational excellence

Disciplined capital spending

Focused growth pipeline

51

Operations

Meeting the Challenge

MarketingMarch 30, 2016Andrew Stonkus, Senior Vice President, Marketing & SalesRéal Foley, Vice President, Coal MarketingMike Doma, Managing Director, Lee & Doma Energy Group

Marketing

Agenda

Overview

Steelmaking Coal

Base Metals

Energy

Summary

3

Marketing

World Economy in 2016

Global growth expected to increase to 2.8% in 2016, vs. 2.6% in 2015

• India will be the fastest-growing economy at 7.6%1

• China is determined to keep growth >6.5%, per the 13th Five Year Plan

− Focusing on further urbanization as a key growth driver

− Accelerating supply-side reforms, including reduction of overcapacity in coal and steel

− Taking a more expansionary fiscal policy and monetary policy stance

− Moving towards a more consumer/service based economy, whichshould provide positive fundamental support to later stage metals

Global GDP is still growing

1. CRISIL’s estimate of real GDP growth.4

Marketing

Prolonged Deep Cycle

Prices starting to improveSource: LME, BEA, LBMA, Teck

Relative Price Changes

0.0

0.2

0.4

0.6

0.8

1.0

1.2

ZN CU Au WTI HC Coal

plotted to March 15, 2016

Peak2014-2016

ChangeFrom Peak

Change FromDecember 2015

Oil $108/bbl -66% -3%

Zinc $1.10/lb -28% +10%

Copper $3.37/lb -34% +5%

Gold $1,385/oz -8% +16%

HC Coal $135/Mt -39% +8%

5

• Up cycles in green and down cycles in orange; plotted against duration in years on the right scale• Peak-to-trough price moves during the cycle in blue; plotted against the left axis• Up cycles tend to be longer, with higher percentage gains

Marketing

Price Cycles Deepest since 1920’sYears

Pea

k to

Tro

ugh

Cyc

le %

Cha

nge

Source: Wood Mackenzie, USGS, WBMS, Teck* Copper prices were fixed in the 1932-1937 period.

72%

-37%

132%

-57%

3%41%

-68%

130%

-10%

86%

-13%

115%

-37%

23%

-6%

92%

-12%

50%

-15%

54%

-28%

5%

-13%

97%

-30%

51%

-45%

16%

-14%

333%

-26%

68%

-49%

54

6

4

6

23

5

8*

3

1

7

2 21

9

2 2

4

2 21 1

54

2

4

12

5

2 2

5

0

2

4

6

8

10

12

14

16

18

20

-600%

-500%

-400%

-300%

-200%

-100%

0%

100%

200%

300%

400% Example: Copper Cycle

6

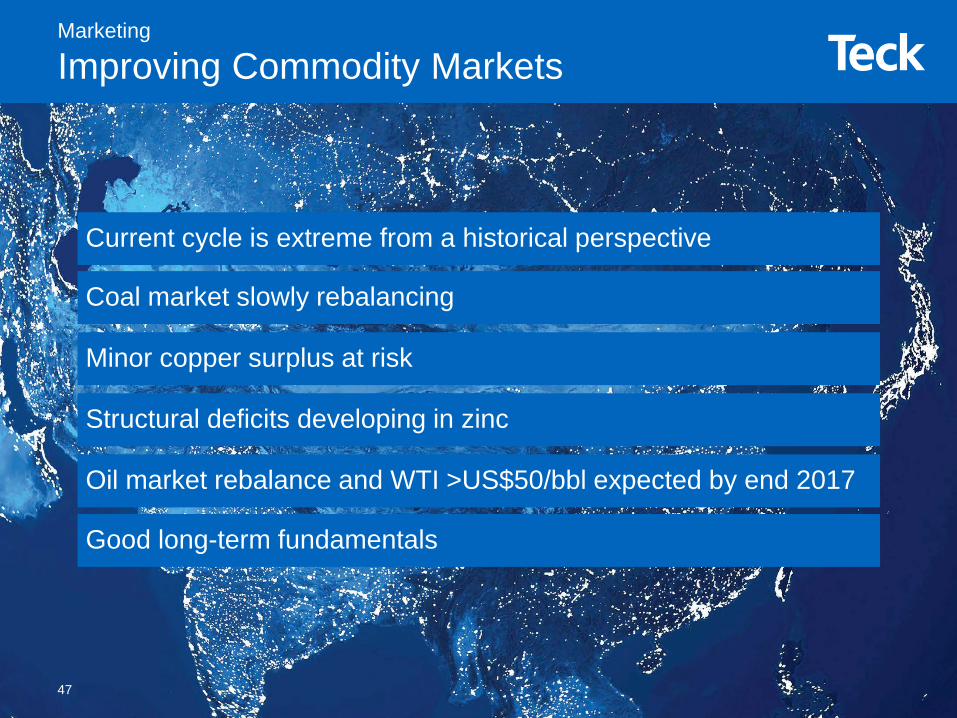

Current cycle is extreme from a historical perspective

Coal market slowly rebalancing

Minor copper surplus at risk

Structural deficits developing in zinc

Oil market rebalance and WTI >US$50/bbl expected by end 2017

Good long-term fundamentals

Marketing

Improving Commodity Markets

7

Marketing

Agenda

Overview

Steelmaking Coal

Base Metals

Energy

Summary

8

9

Steelmaking Coal Marketing

Market Slowly Rebalancing

• Steelmaking coal in longest and deepest cycle

• Pricing at unsustainably low levels

• USA supply reduced and remains under most pressure

• Good demand outside China

• Higher pricing required to incent future production

Our Market - Seaborne Hard Coking Coal2: ~200 million tonnes

1. Source: International Energy Agency 2014 data2. Source: CRU

Global Coal Production1: 7.9 billion tonnesSteelmaking Coal Production2: ~1,185 million tonnes

Export Steelmaking Coal2: ~325 million tonnesSeaborne Steelmaking Coal2: ~290 million tonnes

Steelmaking Coal Marketing

High Grade Hard Coking Coal Is A Niche Market

10

60

80

100

120

140

160

$ / to

nne

Quarterly Contract Settlement Argus FOB Australia

Steelmaking Coal Marketing

Largest Uptick in Spot Prices Since Q3 2013

Source: Argus

Coal Prices: Quarterly Benchmark Prices and Spot Assessments

Q2 Benchmark Price?11

Steelmaking Coal Marketing

Mixed Views on China Coking Coal Imports

2020

F

China's Coking Coal Imports & Stock Changes

Stocks at ports and end users reaching low levels

China Rolling 12-Month Coking Coal Imports

2020 Forecast: 30~70 Mt

Source: GTIS, Wood Mackenzie, CRU, UBS, Mysteel

0

10

20

30

40

50

60

70

80

2009

2010

2011

2012

2013

2014

2015

Milli

on to

nnes

Seaborne imports rolling 12moMongolia imports rolling 12mo

60.0

15.413.2 13.1

35.3

12.7

3.48.0

0

10

20

30

40

50

60

70

Seaborne Landborne Stock at ports Stock at sampleend users

Milli

on to

nnes

2013 2015

12

0

200

400

600

800

1000

1200

1400

Mt

Estimated Crude Steel Capacity Crude Steel Production

Source: Teck, Fenwei, NBS, CISA, MIIT, State Administration of Work Safety

Steelmaking Coal Marketing

China Reducing Overcapacity

Raw CoalCrude Steel

13th 5-Year Plan: Eliminate 100-150 Mt of capacity

13th 5-Year Plan: Eliminate 500 Mt of capacity

0

1000

2000

3000

4000

5000

Mt

Estimated Raw Coal Capacity Raw Coal Production

13

0

200

400

600

800

1000

2010 2015 2020 2025 2030 2035

Crude Steel and Hot Metal Production

Source: WSA, China Association of Metalscrap Utilization, Wood Mackenzie

Crude Steel

Steelmaking Coal Marketing

China Scrap Use to Increase Slowly

China’s Scrap Ratio Low vs. Other Countries

73%54%

33%

88%

28%

50%

11%

36%

0%

20%

40%

60%

80%

100%

UnitedStates

Europe Japan Turkey Russia Korea China WorldAverage China

Steel Use By Sector(2000-14)

Electric Arc Furnace

Hot Metal

Hot metal / crude steel ratio to remain >90% and EAF share of crude steel production <10% until ~2028

14

Steelmaking Coal Marketing

Growing India Steelmaking Coal Imports

India’s Hot Metal Capacity; Projects and Operations

Seaborne Steelmaking Coal ImportsRequired to Meet India Hot Metal Production

0

10

20

30

40

50

60

70

80

0

10

20

30

40

50

60

70

80

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

HMP forecast by Wood MackenzieHMP forecast by CRUSeaborne Steelmaking Coal Imports (average Wood Mackenzie and CRU)

Mt

Seaborne steelmaking coal imports forecasted to increase by >20%

Source: WSA, Wood Mackenzie, CRU15

Source: CRU, Wood Mackenzie

Steelmaking Coal Marketing

Stronger Fundamentals in Rest of the World

Seaborne Steelmaking Coal Imports (Average Wood Mackenzie and CRU; Change 2020 vs. 2015)

16

Steelmaking Coal Marketing

Cash Margins Under Pressure

Seaborne HCC Cash Margins US Steelmaking Seaborne Coal Exports

38 Mt

0

10

20

30

40

50

60

70

Mt 2000-2009

average of 23 Mt

2010-2014average of 55 Mt

>90% of US HCC exports are cash negative

Source: GTIS, Wood Mackenzie17

Steelmaking Coal Marketing

Australian Production Peaking

Australian Steelmaking Coal Production

Higher pricing required to incent more production

Source: CRU

100

120

140

160

180

200

220

2016 2018 2020 2022 2024 2025

Existing & Committed Production

Mt

18

Steelmaking Coal Marketing

We Are a Leading Steelmaking Coal Supplier To Steel Producers Worldwide

North America~5%

Europe2015: ~20%2013: ~15%

China 2015: ~20%2013: ~30%

High quality, consistent, reliable, long-term supply

Asia excl. China2015: ~50%2013: ~45% Latin America

~5%

Proactively realigning sales with changing market19

20

Steelmaking Coal Marketing

Market Slowly Rebalancing

• Steelmaking coal in longest and deepest cycle

• Pricing at unsustainably low levels

• USA supply reduced and remains under most pressure

• Good demand outside China

• Higher pricing required to incent future production

Marketing

Agenda

Overview

Steelmaking Coal

Base Metals

Energy

Summary

21

22

Base Metals Marketing

Strong Fundamentals

Copper• Global mine production continues to underperform• Small surpluses but low global stocks

Zinc• Cutbacks/closures push market into significant deficit• Zinc metal market working off excess inventory • Consensus for metal deficits in 2016 & 2017

Base Metals Marketing

Slowing Copper Mine Production Growth

0

5,000

10,000

15,000

20,000

25,000

30,000

2010 2013 2016 2019 2022 2025

Thou

sand

Ton

nes

Mine Production SXEW Scrap Demand

Copper Mine Production Peaks in 2017 Uncommitted Projects Increasingly Delayed

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2016FLast Year

2016FToday

2018FLast Year

2018FToday

2020FLast Year

2020FToday

Thou

sand

Ton

nes

Highly Probable Probable Possible

Existing and Fully Committed Mines

Committed and operating mine production peaking & replacement projects delayed

Source: Wood Mackenzie, CRU, ICSG, Teck23

Base Metals Marketing

Copper Cathode Balances Trending Down

-950-859

-776-851

-945

-584

-839

-973

-831

-968

-1,315

-225

-1,400

-1,200

-1,000

-800

-600

-400

-200

0

Thou

sand

tonn

es

Analysts projecting weak fundamentals still don’t show massive stock builds

Source: Wood Mackenzie, Teck

Historic Disruptions 7-9% / Year

2015 Disruptions: 8.5%2016 YTD: 6.7%

-200

-100

0

100

200

300

400

500

WM

CR

U

JPM MS

Citi CS

UB

S

Mac

q

BNS

TD

Thou

sand

tonn

es

1% of Demand

Analyst 2016 & 2017 Cathode Balances

24

Base Metals Marketing

Significant Chinese Copper Demand Remains

…But Will Add Significantly in Additional Tonnage Terms

Annual Growth Rate of Chinese Copper Consumption to Slow Dramatically…

China expected to add almost as much to global demand in the next 15 years as the past 25 years

Source: Wood Mackenzie, Teck

-

200

400

600

800

1,000

1,200

1,400

1990 1994 1998 2002 2006 2010 2014 2018 2022 2026 2030

0%

5%

10%

15%

20%

25%

30%

1990 1994 1998 2002 2006 2010 2014 2018 2022 2026 2030

Annual Avg. 11.9%

Annual Avg. 2.8%

Annual Avg. Growth 356 kt Annual Avg. Growth

325 kt

Thou

sand

tonn

es

25

0

200

400

600

800

1,000

1,200

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Cathode Concs Scrap Blister/Semis

000’

s to

nnes

(con

tent

)

Net Copper Imports up ~5% in 2015

Source: NBS

Updated to January 2016

Total copper unit imports continue to climb

Base Metals Marketing

China Switching to Copper Concentrates

26

(2,000)

(1,500)

(1,000)

(500)

0

500

2012 2014 2016 2018 2020

Thou

sand

tonn

es

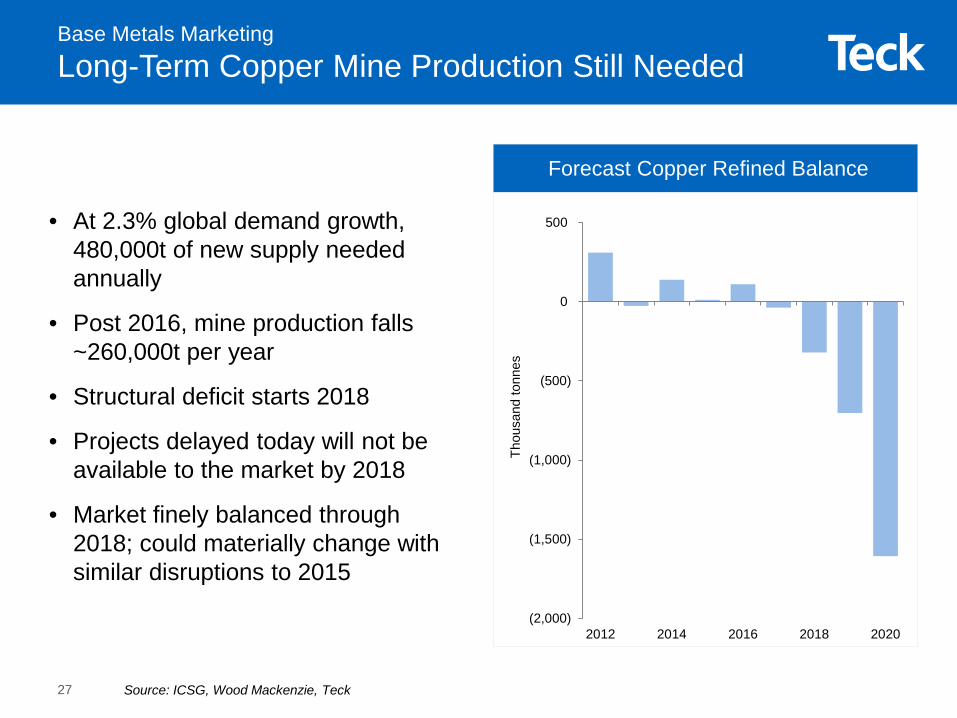

• At 2.3% global demand growth, 480,000t of new supply needed annually

• Post 2016, mine production falls ~260,000t per year

• Structural deficit starts 2018

• Projects delayed today will not be available to the market by 2018

• Market finely balanced through 2018; could materially change with similar disruptions to 2015

Forecast Copper Refined Balance

Base Metals Marketing

Long-Term Copper Mine Production Still Needed

Source: ICSG, Wood Mackenzie, Teck27

Base Metals Marketing

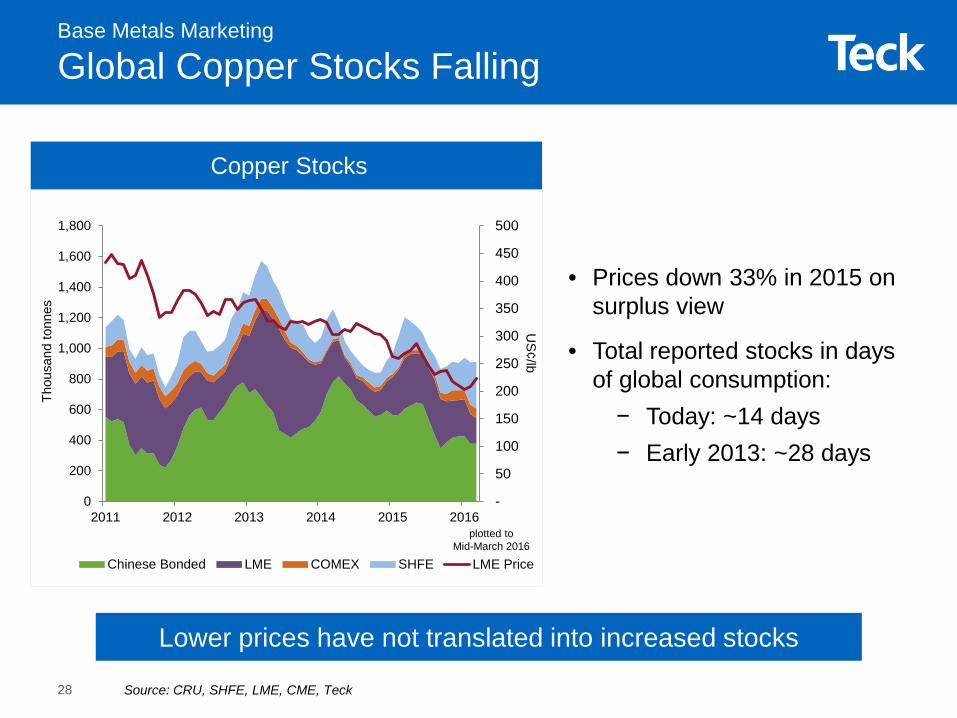

Global Copper Stocks Falling

-

50

100

150

200

250

300

350

400

450

500

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2011 2012 2013 2014 2015 2016

US¢/lb

Thou

sand

tonn

es

Chinese Bonded LME COMEX SHFE LME Price

• Prices down 33% in 2015 on surplus view

• Total reported stocks in days of global consumption:− Today: ~14 days − Early 2013: ~28 days

Copper Stocks

Source: CRU, SHFE, LME, CME, Teck

plotted to Mid-March 2016

Lower prices have not translated into increased stocks

28

29

• Mine production continues to underperform• Small forecast surpluses relative to market size• Production curtailments and project delays due low prices• Global stocks are low in days of consumption• Deficit if upside to demand or higher than forecast disruptions

Base Metals Marketing

Minor Copper Surpluses at Risk

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2016FLastYear

2016FToday

2018FLastYear

2018FToday

2020FLastYear

2020FToday

Thou

sand

Ton

nes

Highly Probable Probable Possible

Base Metals Marketing

Slowing Zinc Mine Production Growth

Zinc Mine Production Peaks in 2020 Uncommitted Projects Increasingly Delayed

Existing and Fully Committed Mines

Committed and operating mine production peaking & replacement projects delayed

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2010 2013 2016 2019 2022 2025

Thou

sand

Ton

nes

Mine Production Secondary Demand

Source: Wood Mackenzie, CRU, ILZSG, Teck30

4,000

4,500

5,000

5,500

6,000

6,500

7,000

2012 2013 2014 2015 2016F

Thou

sand

tonn

es

Mine Supply ROW Conc Imports Australia Conc Imports Metal Imports Demand 3%

Source: NBS, GTIS, Wood Mac, Teck

Chinese Zinc Supply, Including Trade & Demand

Base Metals Marketing

Chinese Zinc Spot Market is Short

• 2016 Australian mine production will fall 43%• Chinese concentrate imports: 40% Australia and 30% Peru in 2015• 2016 shortage of 1.0 Mt at 0% growth, and 1.3 Mt at 3% growth

Con

cent

rate

Sup

ply

Con

cent

rate

Sup

ply

Lower concentrate supply expected in 201631

Spot TCs Tighten

Base Metals Marketing

Market Consensus for Tightening Zinc Market

Source: BGRIMM/Antaike, Wood Mackenzie

-1,000

-800

-600

-400

-200

0

200

400

WM

CR

U

JPM MS

Citi CS

UB

S

Mac

q

BNS

TD

Thou

sand

tonn

es

2016 2017

Analyst Zinc Metal Balance Comparison

$0

$100

$200

$300

$400

$500

$600

Spot Annual

32

Base Metals Marketing

Committed Zinc Supply Insufficient for Demand

Forecast Zinc Refined Balance

Source: Teck

• We expect insufficient mine supply to constrain refined production− From 2014-2020, refined metal supply

increase of only 792 kt− Over the same period, refined demand

increase of 2.8 Mt

• Market was in deficit in 2014• Ongoing, large inventory that has

funded the deficit will continue in 2016• Metal market moving into significant

deficit with further mine closures and depleting inventories

(2,500)

(2,000)

(1,500)

(1,000)

(500)

0

500

2012 2013 2014 2015 2016 2017 2018 2019 2020

Thou

sand

tonn

es

33

-

20

40

60

80

100

120

0

500

1,000

1,500

2,000

2,500

2011 2012 2013 2014 2015 2016

US¢/lb

Thou

sand

tonn

es

Chinese Bonded LME SHFE LME Price

Base Metals Marketing

Global Zinc Stocks Falling

• Prices fell 27% in 2015

• Total reported stocks in days of global consumption:− Today: ~25 days − Early 2013: ~59 days

Zinc Stocks

Source: CRU, SHFE, LME, Teck

plotted to Mid-March 2016

34

35

Base Metals Marketing

Structural Deficits Developing in Zinc

• Mine closures have occurred

• Supply deficit magnified by production cuts

• Spot concentrate treatment charges falling

• Chinese metal imports must increase

• Stocks declining & insufficient to meet demand

36

Base Metals Marketing

Strong Fundamentals

Copper• Global mine production continues to underperform• Small surpluses but low global stocks

Zinc• Cutbacks/closures push market into significant deficit• Zinc metal market working off excess inventory • Consensus for metal deficits in 2016 & 2017

Marketing

Agenda

Overview

Steelmaking Coal

Base Metals

Energy

Summary

37

38

Energy Marketing

Near-Term Market Expectations

• Oil markets currently oversupplied

• Markets expected to rebalance in 2017

• >US$50/bbl WTI expected by end 2017

Energy Marketing

Market Rebalance Expected in 2017

$0

$50

$100

$150

$200

40

50

60

70

80

90

100

Nom

inal

$U

S/b

bl

MM

b/d

Oil Demand (left axis)

Source: IEA and EIA

Source: Wood Mackenzie Macro Oils Short-Term Outlook, February 2016

Long-Term Trend: Prices rose to create supply to meet demand growth• 2000–2015 demand up 16 MM b/d

− Growth from 74 to 90 MM b/d or 1.3%/yr

• 2000–2015 supply − Higher prices required to bring on incremental supply

to meet demand growth− Supply growth (16 MM b/d): U.S. 4.8, Russia 4.6,

Saudi Arabia 2.1, Canada 1.6, China 1.1, Brazil 1.0, Net Others 0.8

Short-Term: Low price due to oversupply & resultant inventory build• 2011–2015 liquids supply up 7.9 MM b/d

− U.S. tight oil growth and Saudi policies result in current oversupply and inventory build

− Supply growth (MM b/d): U.S. 4.8, Iraq 1.3, Saudi Arabia 1.1, Canada 0.9, Net Others -0.2

• Supply/demand expected to rebalance in 2017− Response to low price signals have begun− Key 2016 trends: Demand to grow, US tight oil

production to decline and Iranian production to grow

Long-Term Global Oil Demand and WTI Price

World Liquids Supply & Demand

-2

0

2

4

6

80

85

90

95

100

MM

b/d

MM

b/d

Stock Change (right axis)World Supply (left axis)World Demand (left axis)

WTI Price (right axis)

Forecast

39

Energy Marketing

>$US50/bbl WTI Expected by End 2017

$0$10$20$30$40$50$60

-2

0

2

4

6

Nom

inal

$U

S/b

bl

MM

b/d

Stock ChangeWoodMackenzie WTI ForecastConsensus Economics Avg. Forecast

Stock Change (left axis)

Forecast

02004006008001,0001,2001,4001,6001,800

4

5

6

7

8

9

10

# of

Oil

Rig

s

MM

b/d

U.S. Oil Rig Count (right axis)

U.S. Oil Production (left axis)

Rebalancing of supply and demand expected to raise WTI to >US$50/bbl by Q4/17• 2016/17 world liquids demand expected to rise by

2.7 MM b/d while supply decreases by 0.9 MM b/d• WTI price forecast for Q4/2017:

• WoodMackenzie: US$59/bbl• Consensus Economics Avg.: US$52/bbl

Lower investment leads to lower supply growth• U.S. oil rig count fell from a peak of 1,609 in Oct/14 to

a low of 392 in March/16 (76% drop). • U.S. oil production peaked in June/15 and expected

to decline by 0.6 MM b/d in 2016/17• Global oil capital expenditures dropped from

US$540B in 2014 to US$400B in 2015, and an expected US$330B in 2016 (40% drop in 2 years)

Source: Wood Mackenzie February 2016; Consensus Economics February 2016

WTI Price (right axis)

Source: EIA, Baker Hughes

World Liquids Balance and WTI Price Outlook

U.S. Oil Production and Oil Rig Count

40

Energy Marketing

Higher Prices Required For New Production Development

$0$20$40$60$80$100$120$140$160$180$200

50

60

70

80

90

100

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

Nom

inal

US

$/bb

l

MM

b/d

Actual WoodMac IEAActual WoodMac McD/Spr/GLJ

Source: IEA World Energy Outlook, December 2015

Demand growth continues and prices recover to ensure supply meets demand• Oil demand growth to continue

− Wood Mackenzie and IEA forecasting similar demand growth, increasing ~8 MM b/d by 2030 (0.7% growth/yr)

• Higher long-term prices required for new production development

− 2018 to 2030 avg. WTI price forecasts (2016 dollars):• Wood Mackenzie (Nov/15): US$80/bbl• McDaniel/Sproule/GLJ Avg.: US$73/bbl

36 MM b/d of new oil production required to meet demand growth & production declines • 28 MM b/d of declines plus 8 MM b/d of oil demand

growth implying 36 MM b/d of new production by 2030

• Key contributors to production growth (MM b/d):• Iraq 3.0, Brazil 2.3, Canada 1.5, Saudi Arabia 1.5, Iran

1.4

• US production peaks around 2022; 2030 US production similar to 2014 levels

Oil Demand (left axis)

WTI Price (right axis)

020406080

100120

MM

b/d

Forecast

Oil Demand and WTI Price Outlook

World Oil Supply Sources

41

• US/Canadian heavy refining capacity exceeds Canadian heavy crude oil production

• US Gulf Coast provides largest market for growth

• TMX and Energy East pipelines will provide access to deep water ports

Energy Marketing

Heavy Oil Refining Capacity Available

Estimated Disposition and Refining Capacity for Canadian Heavy (kbbls/day)

0600

12001800

2014 2019

Western Canada

0600

12001800

2014 2019

US Rockies0

60012001800

2014 2019

Eastern US/Canada0600

12001800

2014 2019

US West Coast

0600

12001800

2014 2019

US Midwest

0600

12001800

2014 2019

US Gulf Coast

0

1000

2000

3000

4000

2014 2019

kbbl

s/da

y

US/Canada Heavy Crude Refining Capacity

AdditionalCapacityAvailable forCanadian Heavy

Canadian HeavyUsage

Access to deep water ports will add market capacity and diversification

Source: CAPP, EIA, Lee & Doma Energy Group

Additional Capacity Available for Canadian Heavy

Canadian Heavy Usage

42

Energy Marketing

Sufficient Western Canadian Takeaway Capacity Expected

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

kbbl

s/da

y

Western Canada Crude Supply Forecast Pipeline & Local Refining Capacity

Pipeline, Local Refining & Rail Capacity

TMX & Energy East

Enbridge Expansions

Western Canadian Supply and Takeaway Capacity

Source: CAPP, Lee & Doma Energy Group

Fort Hills’ First Oil Sufficient takeaway capacity expected for forecast growth

• 2011–2014− Rapid production growth resulted in

takeaway capacity challenges− Industry added significant pipeline and

rail capacity during this time

• 2015–2030− Existing pipeline capacity, new pipelines

(TMX and Energy East) and existing rail capacity expected to provide sufficient takeaway capacity

43

WTI - WCS Annual Average Price Differentials

Sufficient takeaway capacity results in current WTI-WCS differentials

• 2011–2014− Takeaway capacity challenges drive

wider WTI - WCS differentials, averaging ~US$25/bbl in 2013

• 2015–2030− Sufficient takeaway capacity developed

and WTI - WCS differential narrowed to ~US$14/bbl in 2015

− Current differentials expected to persist with sufficient takeaway capacity available

$14.19

$17.09

$21.01

$25.12

$19.63

$13.69 $14.00

$0

$5

$10

$15

$20

$25

$30

2010 2011 2012 2013 2014 2015 2018-2030Real

Forecast*

Nom

inal

US

$/bb

l

* In 2016 real US dollars. Assumes US$75/bbl WTI.Source: GLJ (historicals), Lee & Doma Energy Group (forecast)

Average real price differential of US$14/bbl expected 2018-2030

Energy Marketing

Current Differentials Expected to Persist

44

45

Energy Marketing

Market Rebalance Expected in 2017

• 36 MM b/d of new oil production required by 2030• Higher prices required for new production development• US/Canadian heavy refining capacity can accommodate

growing Canadian heavy production• Sufficient Western Canadian takeaway capacity expected

Marketing

Agenda

Overview

Steelmaking Coal

Base Metals

Energy

Summary

46

Current cycle is extreme from a historical perspective

Coal market slowly rebalancing

Minor copper surplus at risk

Structural deficits developing in zinc

Oil market rebalance and WTI >US$50/bbl expected by end 2017

Good long-term fundamentals

Marketing

Improving Commodity Markets

47

Energy ProjectsMarch 30, 2016Ray Reipas, Senior Vice President, EnergyTim Watson, Senior Vice President, Project Development

Energy Projects

Agenda

Energy Business

Fort Hills

3

Energy Business

Building A Valuable Energy Business

4

Market strategy and market access are progressing

Fort Hills economics are robust

Significant free cash flow over 50 year project life at expected long term oil price

Energy Business

Progress in Implementing Our Diversified Marketing Strategy

Market Access Options for Teck’s 50 kbbls/day of Fort Hills Diluted Bitumen Blend

Cushing

Flanagan

Houston

Kitimat

Edmonton

US Gulf Coast

Europe

Asia

TransCanada Energy East (Proposed, Contract Carriage)Enbridge Northern Gateway (Proposed, Contract Carriage)

TransCanada Keystone/MarketLink (Existing, Contract Carriage)Enbridge Flanagan South (Existing, Contract Carriage)

Vancouver

TransMountain Pipeline Expansion (Proposed, Contract Carriage)

Asia

Agreements for pipelines to Hardisty in place

Agreement for Hardisty product storage in place

Monitoring production vs market access balance

Developing a portfolio of pipeline capacity opportunities, to enable access to diversified markets

Evaluating opportunities in the secondary market for pipeline capacity

Developing a diversified customer base

Hardisty

Chicago

Sarnia

Patoka

SuperiorGuernsey

MontrealSaint John

Enbridge Mainline System (Existing, Common Carriage)Spectra Express (Existing, Contract Carriage)

Teck can enter into long-term take or pay contracts

5

East Tank Farm Blending w/Condensate

Energy Business

Committed Logistics Solutions in Alberta

Pipeline/Terminal OperatorPipelineCapacity

(kbpd)

Teck Capacity

(kbpd)Status

Northern Courier Hot Bitumen TransCanada 202 40.4 Construction on schedule

East Tank Farm -Blending Suncor 292 58.4 Modules constructed and on site; tank construction

ahead of schedule

Wood Buffalo Blend Pipeline Enbridge 550 65.3 In service

Wood Buffalo Extension Enbridge 550 65.3 Pipeline 80% complete, beginning pump stationconstruction

Norlite Diluent Pipeline Enbridge 130 18.0 Construction on schedule: In service May 2017

Hardisty Blend Tankage Gibsons 425 kbbls 425 kbbls Construction ahead of schedule: In service Q4 2016

Wood BuffaloExtension

NorliteDiluent Pipeline

Cheecham Terminal

Hardisty Terminal

Wood Buffalo Pipeline

AthabascaPipeline

Edmonton Terminal

Fort HillsMine Terminal

Northern CourierHot Bitumen Pipeline

Teck

OptionsExport Pipeline

Rail

Local Market

Pipeline LegendBitumenBlendDiluentExistingNew

Kirby AthabascaTwin Pipeline

6

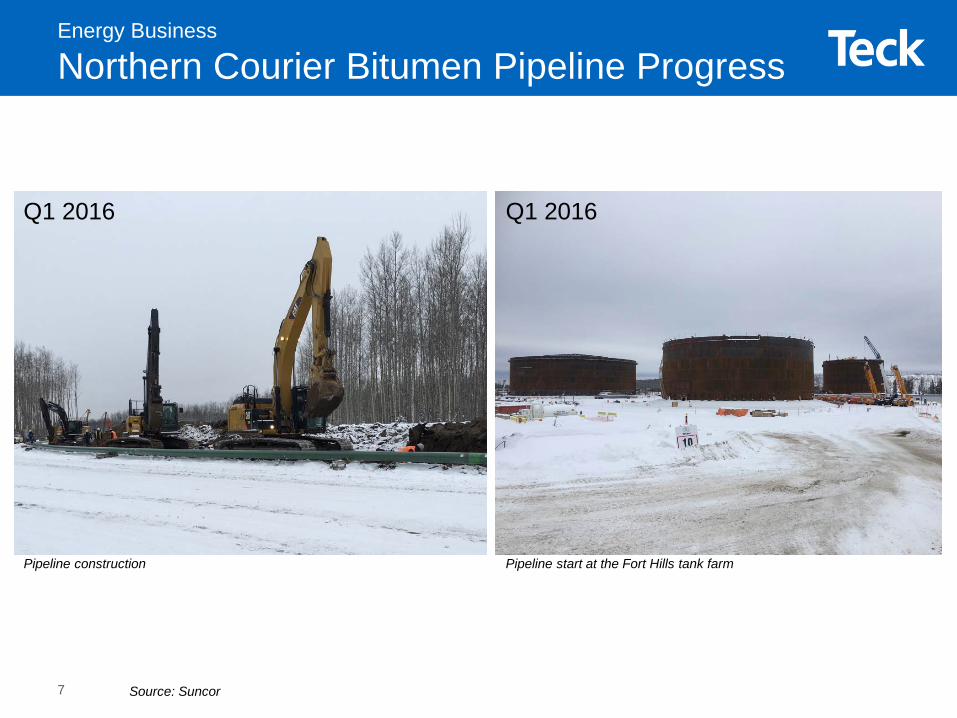

Source: Suncor

Energy Business

Northern Courier Bitumen Pipeline Progress

Q1 2016 Q1 2016