Embed Size (px)

Citation preview

Green Bonds – Deal Survey They've Arrived

Dentons Canada LLP

Bill Gilliland February 2015 #13180742

Introduction

2

• What are Green Bonds?

• History of Green Bonds.

• New Era of Green Bonds.

• Deals.

• Why Issue Green Bonds?

• Assurance/Verification.

• Appendices – Deal Analysis – Real Estate/Power/Other.

Key Points

3

• Market evolving quickly.

• The first "labeled" green bond was issued in 2007.

• Began with multilateral agencies.

• Next wave was commercial banks.

• First corporate (non-bank) bond issued in November 2013.

• Now corporate issuers with their own green use of proceeds. • Renewable Power Generation. • Energy Efficient Buildings. • Other energy efficiency/water projects.

Key Points

4

• Corporate issues are shifting the market away from AAA rated bonds from multilateral development banks.

• Recently more non-rated, high yield issues.

• Historical approach not model used by corporates.

• Terms lengthening.

• Pricing advantages? – short/longer term.

Key Points

5

• "Green" standards developing – flexible/practical approaches taken.

• Green Bond Principles (GBP) - voluntary process guidelines.

• Dentons first Canadian law firm member.

• Climate Bond Initiative. • Certification standards. • Deal commentary.

What are Green Bonds?

6

Green Bond Principles.

• Green bonds enable capital-raising and investment for new and existing project with environmental benefits.

• Currently four types: • Green Use of Proceeds Bond. • Green Use of Proceeds Revenue Bond. • Green Project Bond. • Green Securitized Bond.

• Not a closed set.

What are Green Bonds?

7

• Green Use of Proceeds Bond:

• A standard recourse-to-the-issuer debt obligation. • Proceeds moved to a sub-portfolio or otherwise tracked by the issuer. • Use of proceeds attested to by a formal internal process that will be linked to

the issuer’s lending and investment operations for projects.

What are Green Bonds? – Other Types

8

• Green Use of Proceeds Revenue Bond: a non-recourse-to-the-issuer debt obligation in which the credit exposure in the bond is to the pledged cash flows of the revenue streams, fees, taxes, etc., and the Use of Proceeds of the bond goes to related or unrelated Green Project(s). These proceeds shall be moved to a sub-portfolio or otherwise tracked by the issuer and attested to by a formal internal process that will be linked to the issuer’s lending and investment operations for projects.

• Green Project Bond: a project bond for a single or multiple Green Project(s) for which the investor has direct exposure to the risk of the project(s) with or without potential recourse to the issuer.

• Green Securitized Bond: a bond collateralized by one or more specific projects, including but not limited to covered bonds, ABS, and other structures. The first source of repayment is generally the cash flows of the assets.

What are Green Bonds?

9

• Proceeds are exclusively used to finance approved environmental projects.

• Not general corporate purposes.

• Assurance/verification steps. Transparency to confirm funds are being used appropriately and that the supported projects are yielding the intended environmental benefits.

• Issuers of green bonds usually maintain this transparency through formal monitoring and verification and, where sustainability/greening is promised, environmental specialists.

• Monitoring can be conducted by the issuer of a bond, or a third-party – market dependent.

What are Green Bonds? - Documentation

10

• General corporate obligations, or project obligations.

• No extra "green events of default" or covenants.

• No extra maintenance obligations.

• Standard trust indenture, prospectus supplements.

• Can be issued under MTN programs.

What are Green Bonds? - Documentation

11

• "Green" components currently are outside bond documentation. • Use of proceeds. • Website/public disclosure of business. • Social responsibility disclosure. • Reporting.

• Offering representations re: use of proceeds and reporting.

• Structuring of bond issuer and flow of proceeds can make them work better.

Climate Bond Initiative – A Certification Scheme

12

• The Climate Bonds Initiative ("CBI") is an investor-focused not-for-profit organization, promoting large-scale investments that will deliver a global low-carbon economy.

• Seeks to develop mechanisms to better align the interest of investors, industry and government so as to catalyze investments at a speed and scale sufficient to avoid dangerous climate change.

• The Certification Scheme allows investors, governments and other stakeholders to prioritize "low carbon" investments with confidence that the funds are being used to deliver a low-carbon economy.

• Pre-issue certification and verification of green criteria, tracking requirements.

• Deal commentary an effective guide to the market.

Green Bond Principles, 2014 – Voluntary Process Guidelines

13

• January 13, 2014.

• The Green Bond Principles (GBP) are voluntary process guidelines that recommend transparency and disclosure and promote integrity in the development of the Green Bond market by clarifying the approach for issuance of a Green Bond.

• No single gatekeeper.

• The GBP have four components: 1. Use of Proceeds.

2. Process for Project Evaluation and Selection.

3. Management of Proceeds.

4. Reporting.

Green Bond Principles, 2014 – Voluntary Process Guidelines

14

• The issuer of a Green Bond should outline the investment decision-making process it follows to determine the eligibility of an individual investment using Green Bond proceeds.

• Where applicable, the issuer should, as a first step, review the investments overall environmental profile.

• In all cases, the issuer should establish a well-defined process for determining how the investments fit within the eligible Green Project categories identified in the Use of Proceeds disclosure.

• If possible, issuer should work to establish impact objectives from the projects selected.

• The net proceeds of Green Bonds should be moved to a sub-portfolio or otherwise tracked by the issuer and Attested to by a formal internal process that will be linked to the issuer's lending and investment operations for projects.

• Depending on issuer's and investors' expectations, outside review of the internal tracking method may or may not be necessary.

Green Bond Principles - Voluntary Process Guidelines

15

• The GBP recognize several broad categories of potential eligible Green Projects for the Use of Proceeds including but not limited to: • Renewable energy. • Energy efficiency (including efficient buildings). • Sustainable waste management. • Sustainable land use (including sustainable forestry and agriculture). • Biodiversity conservation. • Clean transportation. • Clean water and/or drinking water.

• There is diversity of opinion on the definition of Green Projects; therefore it is not the intent of the GBP to opine on the eligible Green Project categories. The GBP recommend issuers communicate their Use of Proceeds categories clearly so that investors can determine the bond's consistency with their investment strategy.

Green Bond Principles, 2014 – Voluntary Process Guidelines

16

Reporting

• In addition to reporting on the Use of Proceeds and the eligible investments for unallocated proceeds, issuers should report at least annually, if not semi-annually, via newsletters, website updates or filed financial reports on the specific investments made from the Green Bond proceeds, detailing wherever possible the specific project and the dollars invested in the project.

• The GBP recommend the use of quantitative and/or qualitative performance indicates which measure, where feasible, the impact of the specific investments (e,g, reductions in greenhouse gas emissions, number of people provided with access to clean power or clean water, or avoided vehicle miles travelled, etc.).

Green Bond Principles, 2014 – Voluntary Process Guidelines

17

Assurance

• Attention will be paid to the accuracy and integrity of sustainability information and data whose disclosure is recommended by the GBP and which will be reported by issuers to stakeholders and used for strategic decision making by investors.

Green Bond Principles, 2014 – Voluntary Process Guidelines

18

• There are also several levels of independent assurance that can be provided to the market. Such guidance and assurance might include, in order of increasing rigor:

(i) Second party consultation: for example, an issuer ("first party") can hire an expert consultant ("second party") with climate expertise to help in the establishment of a Green Bond's eligible Green Project categories. The issuer may choose to keep the recommendations of the consultant private.

(ii) Publicly available reviews and audits: if an expert consultant or auditor and an issuer so choose, a consultant's recommendations or an auditor's evaluation may be put in the public domain by the issuer.

(iii) Third party, independent verification/certification: at the moment, at least one or more standards intended for use by accredited third parties to certify Green Bonds are in development. The GBP are supportive of certification of Green Bonds against fully developed and vetted standards. It is also the intention of the GB to allow for third party evaluation/audit of conformance with the guidelines recommended herein. (Further review of 2014 will refine this intended use and related communications.)

Market for Climate Themed Bonds - CBI

19

• CBI estimate $502.6 billion of climate themed bonds outstanding (to June, 2014).

• Proceeds must align with their criteria for a low carbon, climate-resilient economy, but not specifically labeled as green bonds.

• Bonds not required to be monitored, funds to be ring-fenced, or bonds to be tied to the financing of certain projects.

• Globally – 12% increase in issuances from 2012 to 2013 (25% increase 2011 to 2012).

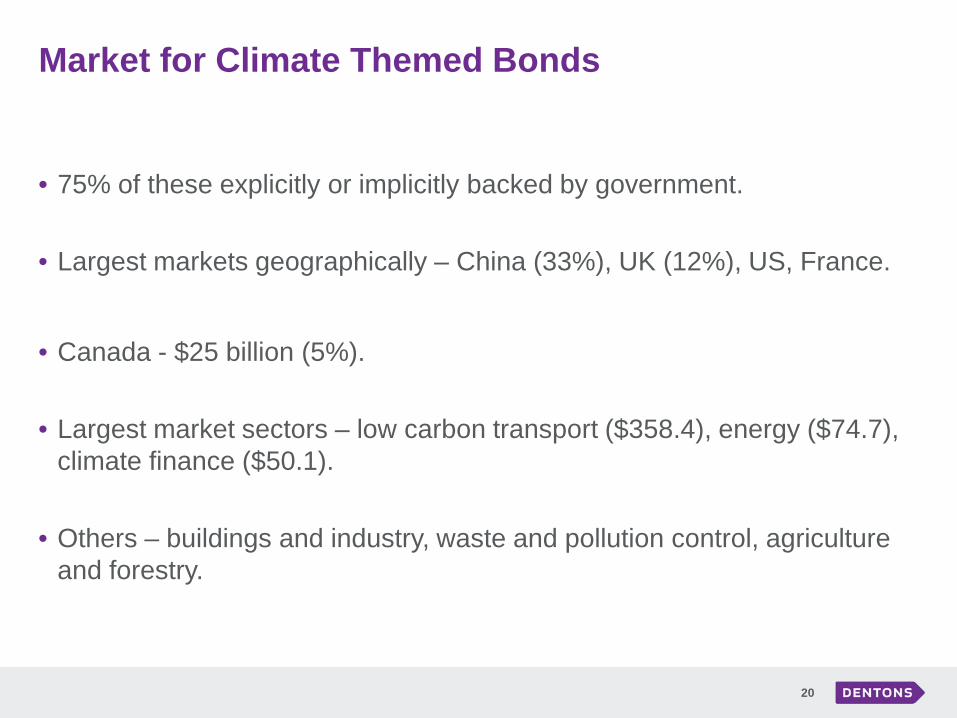

Market for Climate Themed Bonds

20

• 75% of these explicitly or implicitly backed by government.

• Largest markets geographically – China (33%), UK (12%), US, France.

• Canada - $25 billion (5%).

• Largest market sectors – low carbon transport ($358.4), energy ($74.7), climate finance ($50.1).

• Others – buildings and industry, waste and pollution control, agriculture and forestry.

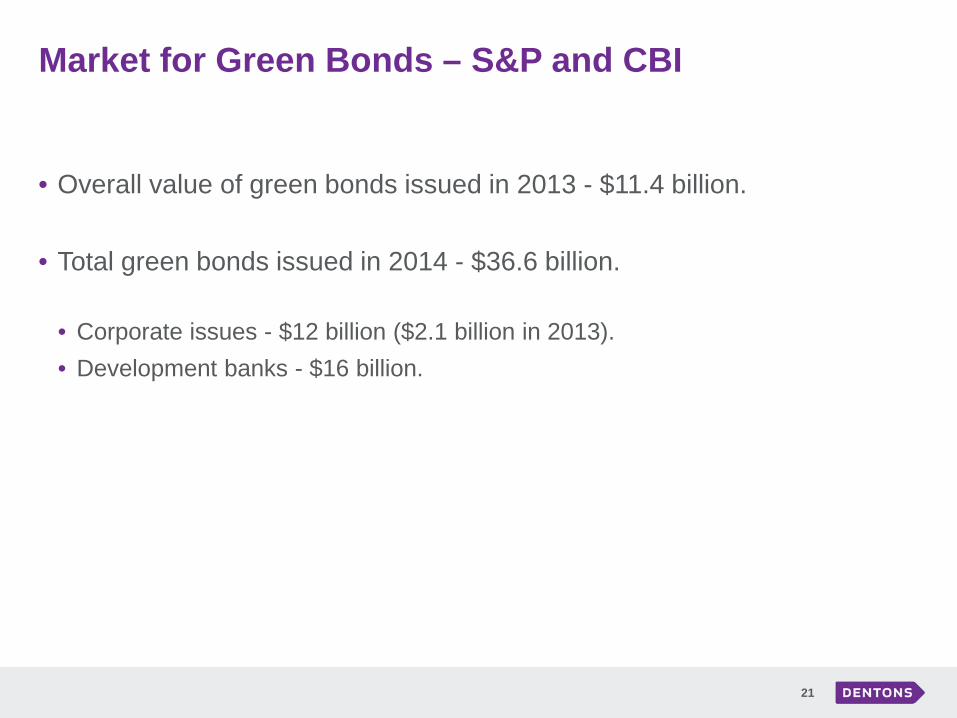

Market for Green Bonds – S&P and CBI

21

• Overall value of green bonds issued in 2013 - $11.4 billion.

• Total green bonds issued in 2014 - $36.6 billion. • Corporate issues - $12 billion ($2.1 billion in 2013). • Development banks - $16 billion.

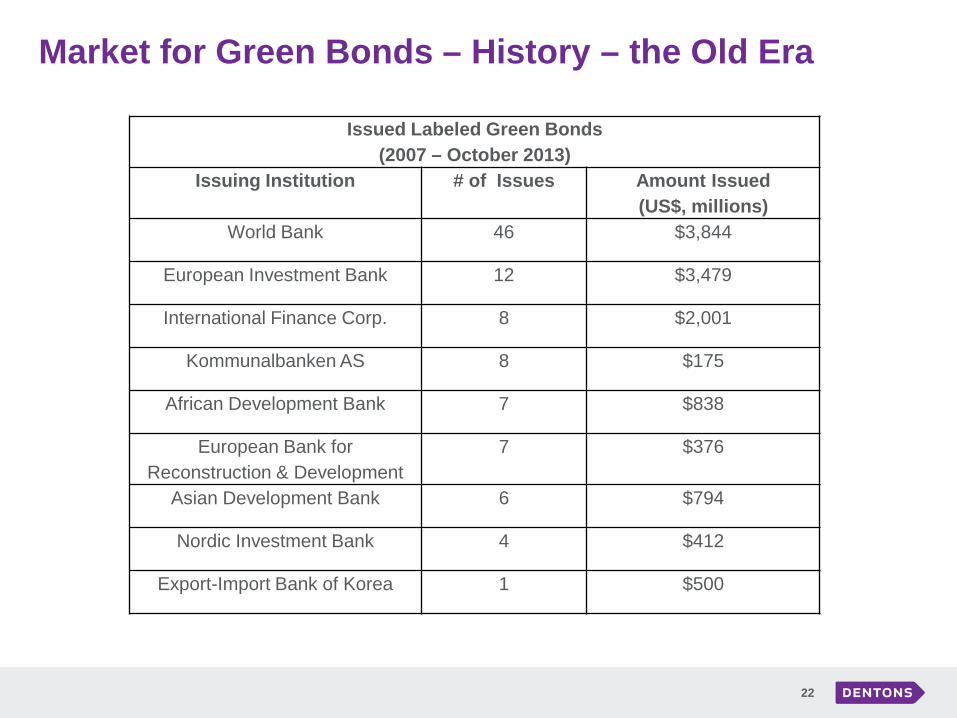

Market for Green Bonds – History – the Old Era

22

Issued Labeled Green Bonds (2007 – October 2013)

Issuing Institution # of Issues Amount Issued (US$, millions)

World Bank 46 $3,844

European Investment Bank 12 $3,479

International Finance Corp. 8 $2,001

Kommunalbanken AS 8 $175

African Development Bank 7 $838

European Bank for Reconstruction & Development

7 $376

Asian Development Bank 6 $794

Nordic Investment Bank 4 $412

Export-Import Bank of Korea 1 $500

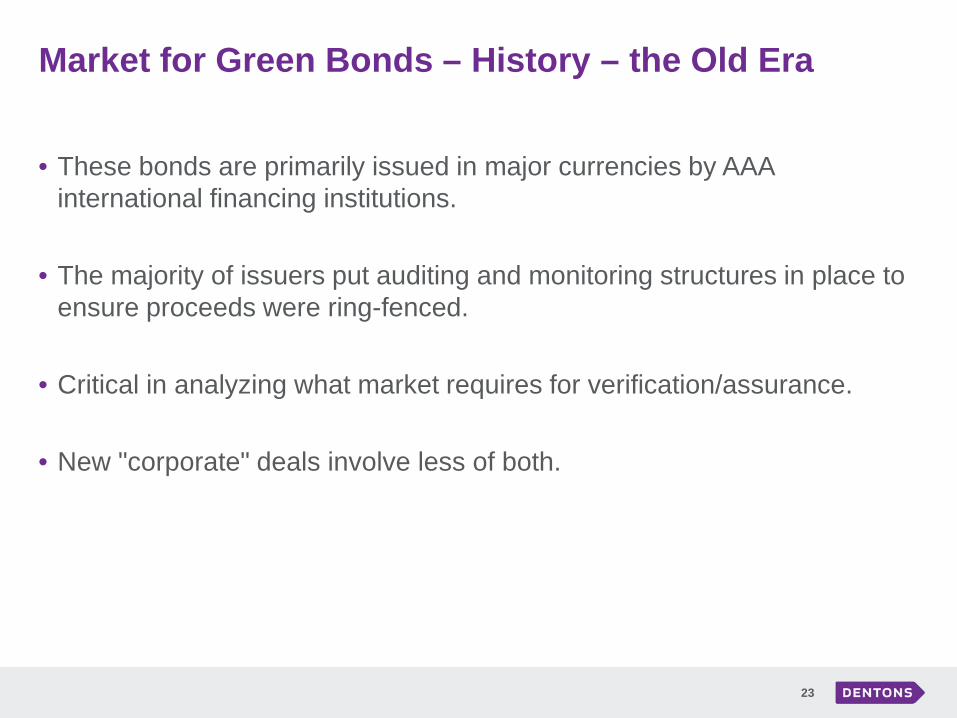

Market for Green Bonds – History – the Old Era

23

• These bonds are primarily issued in major currencies by AAA international financing institutions.

• The majority of issuers put auditing and monitoring structures in place to ensure proceeds were ring-fenced.

• Critical in analyzing what market requires for verification/assurance.

• New "corporate" deals involve less of both.

Market for Green Bonds – Term Trends

24

• Labeled green bonds by multi-lateral institutions tended to have terms in the 3 – 6 year range.

• 2014 – Started to see terms on bonds issued by multi-lateral institutions pushing out longer.

• Newer corporate deals tend to have longer terms. • Typical 6 – 10 yrs. • Real Estate bonds – 7 – 32 yrs. • One power generation bond – 20 yrs.

New Era Green Bonds (Phase 1) – Private Bank Issues

25

• Credit Agricole – 17 issues January 2013 – December 2014 (3 – 7 year term).

• Bank of America – November 2013 (3 year term).

• NRW Bank – November 2013 (4 year term).

• NRW Bank - November 2014 (4 year term).

• National Australian Bank – December 2014 (7 year term).

• TD Bank – March 2014 (3 year term).

• Export Development Corporation – January 2014 (3 year term).

• National Australian Bank – December 2014 (7 year term).

• Variety of currencies.

TD Bank – March 2014

26

• $500 million.

• 3 year term.

• Private placement.

• No up-front external review of green credentials, and very broad use of proceeds criteria.

TD Bank - March 2014 – Use of Proceeds

27

• The focus of the investments will be on projects that contribute to the low carbon economy through:

1. Renewable and low carbon energy and related infrastructure, such as hydroelectric, wind, solar and geothermal.

2. Energy efficiency and management, with a focus on green buildings. 3. Green infrastructure and sustainable land use management. This category of

projects will include municipal and regional infrastructure projects that contribute to energy reduction as well as projects that involve certified sustainable agricultural and forestry practices.

• The TD Green Bond will fund new projects or refinance continuing business operations.

• Pending the allocation to finance the above projects, the proceeds of the TD Green Bond will be segregated and invested in short term financial instruments. Details of the allocation of proceeds will be reported on annually and assured by an independent third party.

TD Bank – March 2014 – Use of Proceeds

28

• TD Bank have subsequently confirmed that gas and biofuel are not included.

• TD Bank subsequently confirmed that fossil fuels are generally not included.

Export Development Corporation – January 2014

29

• $300 million.

• 3 year term.

• Prospectus supplement, standard trust indenture.

• CICERO endorsed EDC’s green bond framework that sets out eligible transactions and provides guidance on internal selection process.

Export Development Corporation – January 2014

30

Use of Proceeds:

• Upon issuance, an amount equal to the net proceeds of this inaugural issue of the bonds (which proceeds may be converted into other currencies) will be credited by EDC to an account that will support EDC’s existing and future lending operations for Eligible Transactions (as defined below). After issuance of the inaugural bonds, the net proceeds will be deducted from the account and added to EDC’s lending pool for disbursements made from that pool in respect of Eligible Transactions.

• "Eligible Transactions" means all transactions (loans) funded in whole or in part by EDC in support of goods, services or projects that are beneficial to the environment, as determined by EDC.

Export Development Corporation – January 2014

31

• Eligible Transactions will include, without limitation, those that are aimed at the preservation, protection or remediation of air, water or soil or the mitigation of climate change. For example:

1. Water Management.

2. Remediation & Soil Treatment.

3. Recycling & Recovery.

4. Water Management.

5. Sustainable Forests Management.

6. Sustainable Agriculture Management.

7. Renewable Energy.

8. Biofuel & Bioenergy.

9. Smart Grid Energy Infrastructure.

10. Alternative Energy Transportation and Public Ground Transport.

11. Industrial Process Improvements.

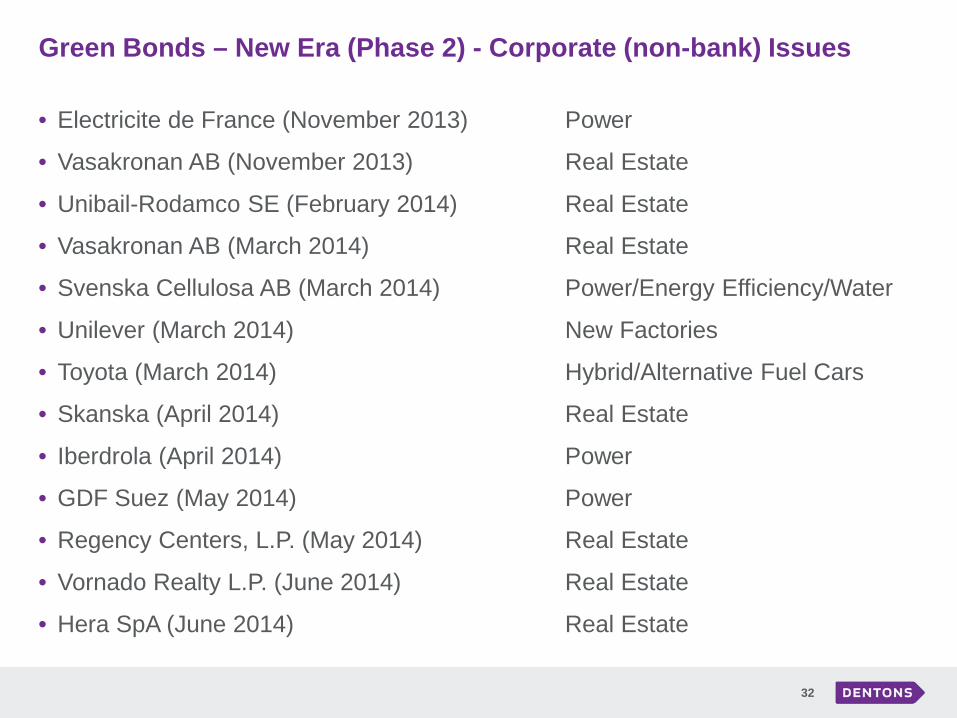

Green Bonds – New Era (Phase 2) - Corporate (non-bank) Issues

32

• Electricite de France (November 2013) Power

• Vasakronan AB (November 2013) Real Estate

• Unibail-Rodamco SE (February 2014) Real Estate

• Vasakronan AB (March 2014) Real Estate

• Svenska Cellulosa AB (March 2014) Power/Energy Efficiency/Water

• Unilever (March 2014) New Factories

• Toyota (March 2014) Hybrid/Alternative Fuel Cars

• Skanska (April 2014) Real Estate

• Iberdrola (April 2014) Power

• GDF Suez (May 2014) Power

• Regency Centers, L.P. (May 2014) Real Estate

• Vornado Realty L.P. (June 2014) Real Estate

• Hera SpA (June 2014) Real Estate

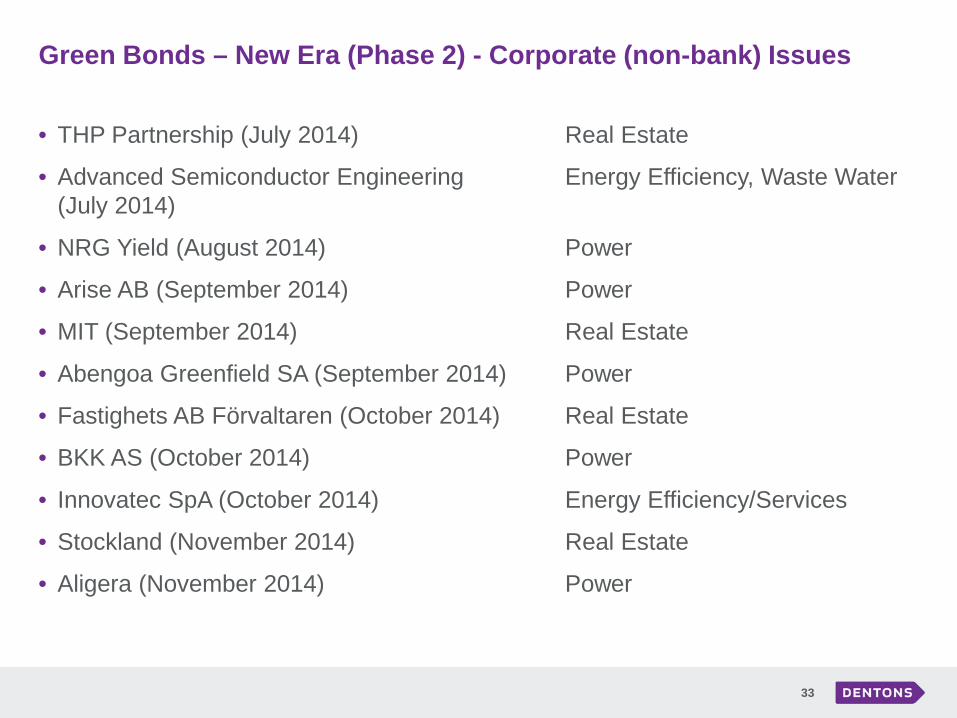

Green Bonds – New Era (Phase 2) - Corporate (non-bank) Issues

33

• THP Partnership (July 2014) Real Estate

• Advanced Semiconductor Engineering Energy Efficiency, Waste Water (July 2014)

• NRG Yield (August 2014) Power

• Arise AB (September 2014) Power

• MIT (September 2014) Real Estate

• Abengoa Greenfield SA (September 2014) Power

• Fastighets AB Förvaltaren (October 2014) Real Estate

• BKK AS (October 2014) Power

• Innovatec SpA (October 2014) Energy Efficiency/Services

• Stockland (November 2014) Real Estate

• Aligera (November 2014) Power

Green Bonds – New Era (Phase 2) - Corporate (non-bank) Issues

34

• Nord-Trondelag Elektrisitetsverk Power (November 2014)

• Verbund AG (November 2014) Power

• Vasakronan AB (November 2014) Real Estate

• Rikshem AB (December 2014) Power

• Rikshem AB (December 2014) Power

• Vardar AS (December 2014) Power

• Massachusetts State College (December 2014) Real Estate

• Energia Eolica (December 2014) Power

• University of Cincinnati (December 2014) Real Estate

• Indiana University (January 2015) Real Estate

• Terraform Power (January 2015) Power

• Variety of local government agencies Various

Green Bonds New Era

Dentons Canada LLP 35

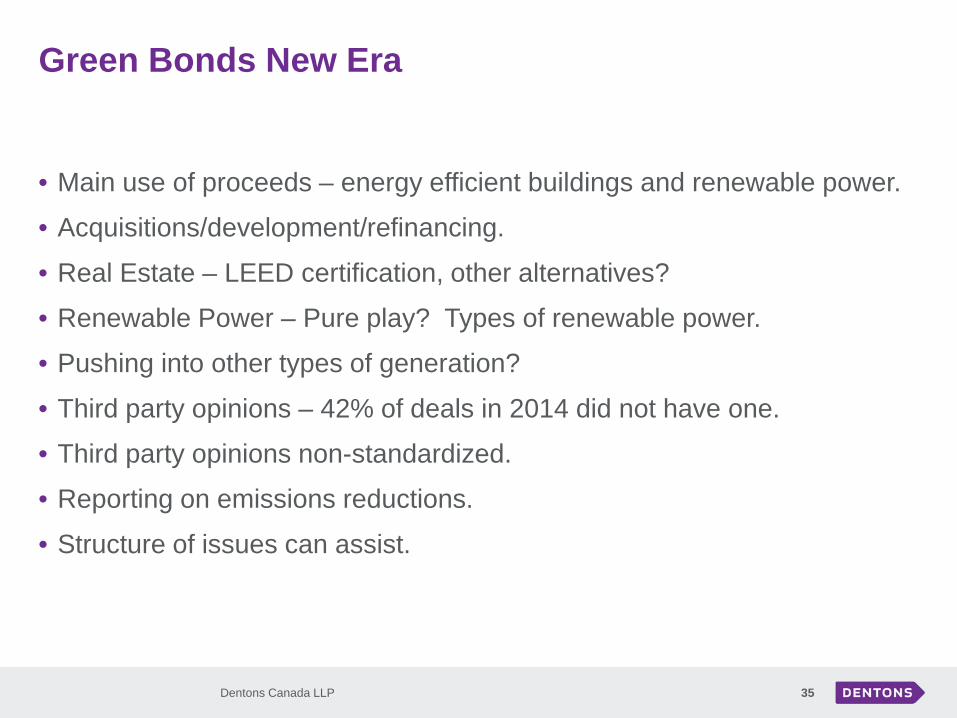

• Main use of proceeds – energy efficient buildings and renewable power.

• Acquisitions/development/refinancing.

• Real Estate – LEED certification, other alternatives?

• Renewable Power – Pure play? Types of renewable power.

• Pushing into other types of generation?

• Third party opinions – 42% of deals in 2014 did not have one.

• Third party opinions non-standardized.

• Reporting on emissions reductions.

• Structure of issues can assist.

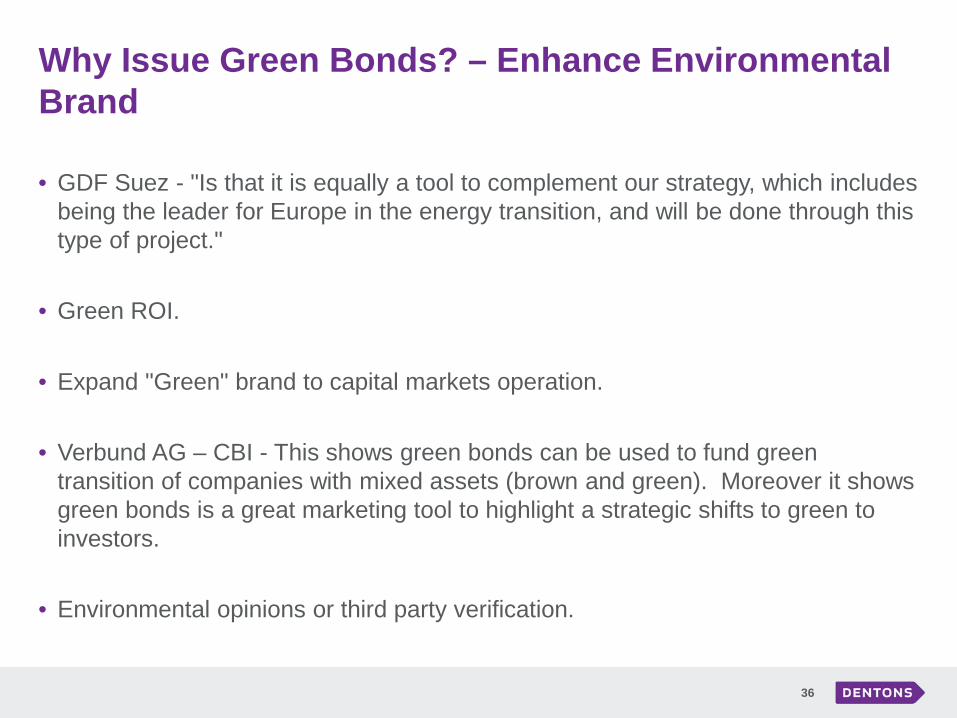

Why Issue Green Bonds? – Enhance Environmental Brand

36

• GDF Suez - "Is that it is equally a tool to complement our strategy, which includes being the leader for Europe in the energy transition, and will be done through this type of project."

• Green ROI.

• Expand "Green" brand to capital markets operation.

• Verbund AG – CBI - This shows green bonds can be used to fund green transition of companies with mixed assets (brown and green). Moreover it shows green bonds is a great marketing tool to highlight a strategic shifts to green to investors.

• Environmental opinions or third party verification.

Why Issue Green Bonds? – Attract New Investors

37

• TD Bank - Attract new investors - long term this will lower prices - either by bigger demand or same amount for lower price.

• TD Bank had 40 purchasers, 12 new to TD. Of the 12 one would not have invested if not a green bid, other 11 tucked investment into sub portfolios devoted to sustainable in investments.

• GDF Suez – "We noticed clearly that there is more and more appetite for this type of transaction, so we are diversifying our investor base."

• Vasakronan – Diversify borrowings "which over time, will result in lower borrowing costs".

Why Issue Green Bonds? - Pricing

38

• TD Bank does not think pricing of its green bonds influenced by being "green".

• TD Bank looking for longer term pricing advantage in green market from broader investor base.

• Observers looking at Regency and Vornado deals and seeing price advantage.

• Vornado – negative new issue premium – 10bps – 15 bps.

• Global Capital – "a degree of negative new issue premium that is hard to imagine being possible without the deal’s green allure".

• Fitch – Regency REIT – issue had more favorable pricing from new investors.

Why Issue Green Bonds? – Pricing

39

• Maintain pricing as defensive measure in sectors facing environmental challenges.

• e.g. Barclays downgrade of US power utility bonds due to solar generation.

• e.g. US GHG emissions reduction requirements for coal power producers.

• Differentiate renewable power play issuers.

Why Issue Green Bonds? – Other Reasons

40

• Green bonds can fit into existing investor portfolios due to their similarity to existing bonds.

• Green attributes – slight competitive advantage most investors will choose.

• Driving management improvement, a green "rating", operating efficiencies, reducing contingent liabilities.

• Less market volatility?

Verification/Assurance

41

• CBI vs. GBP evolution.

• Current man environmental consultancies: • CICERO. • Vigeo. • DNV GL. • Oekom.

• Oekom – green rating.

Verification/Assurance

42

• 42% of issuers chose not to get a 2nd opinion in 2014.

• CBI - Second opinions are included because they provide investors with additional transparency into the bonds' planned use of proceeds or green assets. However not all bonds have second opinions.

• CBI - Although not strictly required they are a great tool for investors and key for market confidence.

• CBI - Of course not all bonds need a second opinion; those issued by a wind farm are going to be green. However that does not apply to most use of proceeds bonds. These need a second opinion.

• Green Bond Principles – market approach to the issue.

• CBI List (Includes 2nd opinion).

• Oslo Exchange List (Requires 2nd opinion).

• Alternative standards. e.g. LEED, others?

Verification/Assurance

43

What do they do?

• Advice re: developing criteria for use of proceeds – are they green? Or issuer can do it itself?

• Initial verification of the bond issue – confirm that assets or projects meet criteria established for use of proceeds.

• Tracing use of proceeds – ensure a process is in place.

• Annual verification – reporting to ensure that the projects comply with criteria.

• Road show attendance by verifiers.

• Pricing/time a function of criteria, number of projects, road show attendance, sustainability.

• Role of auditors.

Verification/Assurance

44

• There are two types of assurance available in the green bond space:

• Third-party verification against the Climate Bonds Standard. • Second-party opinions that do not involve a standard and instead rely on the

credentials of the institution issuing the opinion to provide integrity to the opinion.

Verification/Assurance

45

• Recently the market has become less focused on the third-party approach and more on bespoke second-party opinions, which can go beyond "green" and into sustainability more broadly.

• The publication of the GBPs has helped provide a more robust assurance environment by defining a set of guidelines for issuers and investors which, while not being a standard, nonetheless provide guidance for giving an "opinion".

• The second-party opinion is especially important to socially responsible investors: • When the bond issuer is not a large well-known institution with transparent

environmental, social and governance credentials; • When the activities being financed are not obviously "green" and, hence, require

additional scrutiny and performance indicators; and • When the issuer is pureplay "green" but is issuing a corporate bond and investors would

like to know that their funds are deployed in projects and not for general corporate purposes.

• Not always significant assurance requirements.

Green Bonds - Appendix Real Estate

Vasakronan AB – November 2013

48

• 200 million SEK.

• 3 year term.

• Issued under Vasakronan's MTN program.

• Use of proceeds for construction and renovation of real estate portfolio with high environmental certification requirements.

• CICERO provided framework for selection of green projects.

Unibail – Rodamco SE – February 2014

49

• 1.025 billion Euros.

• 10 year term.

• Energy efficient real estate portfolio.

Vasakronan AB – March 2014

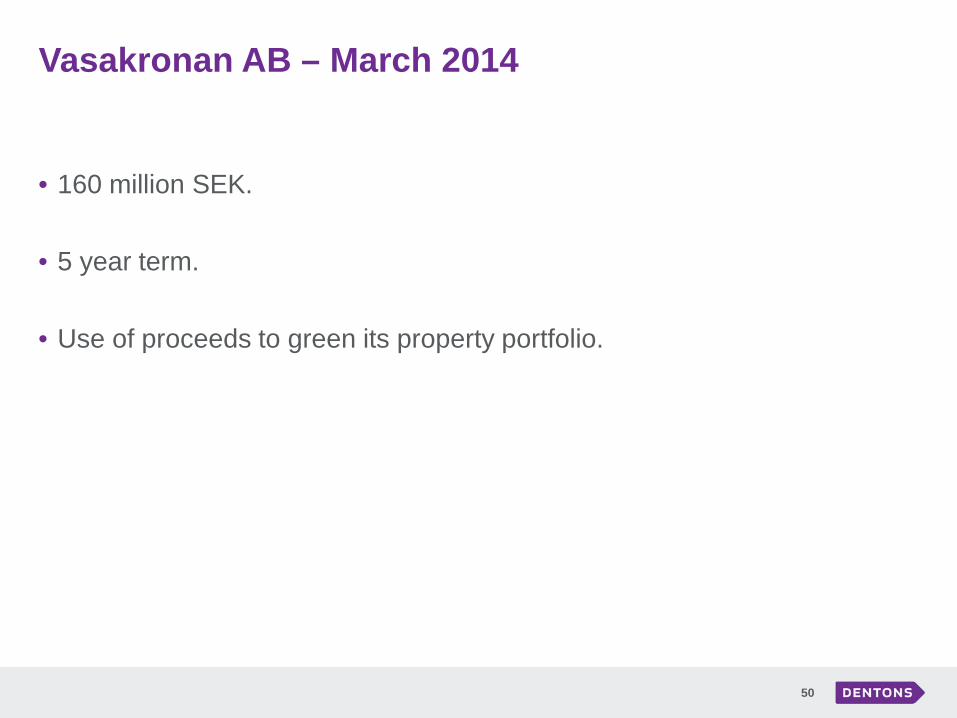

50

• 160 million SEK.

• 5 year term.

• Use of proceeds to green its property portfolio.

Skanska – April 2014

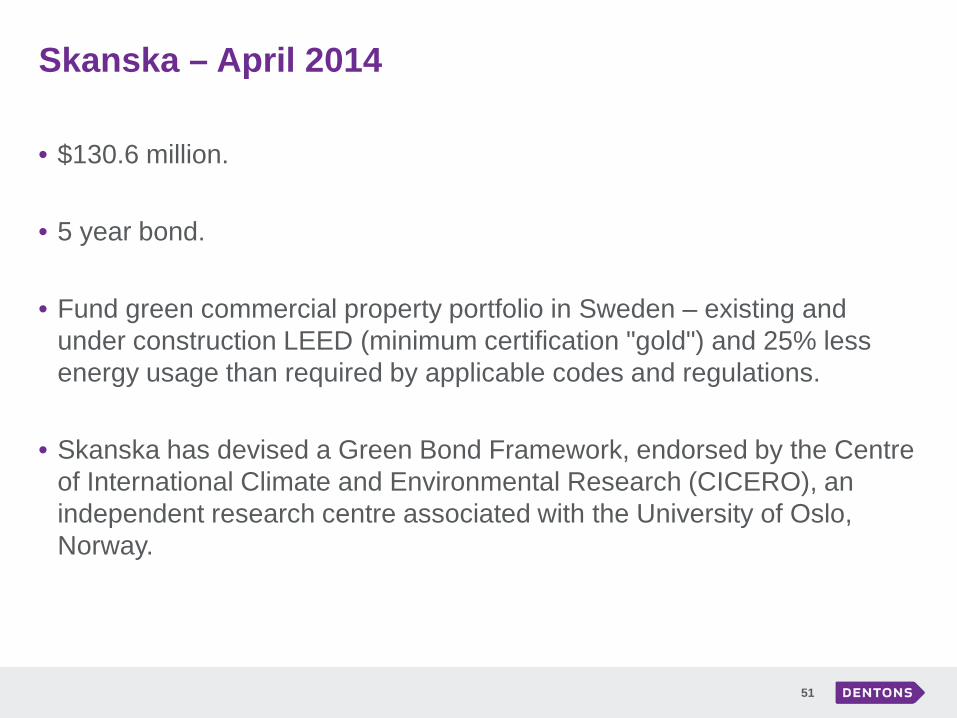

51

• $130.6 million.

• 5 year bond.

• Fund green commercial property portfolio in Sweden – existing and under construction LEED (minimum certification "gold") and 25% less energy usage than required by applicable codes and regulations.

• Skanska has devised a Green Bond Framework, endorsed by the Centre of International Climate and Environmental Research (CICERO), an independent research centre associated with the University of Oslo, Norway.

Regency Centers, L.P. – May 2014

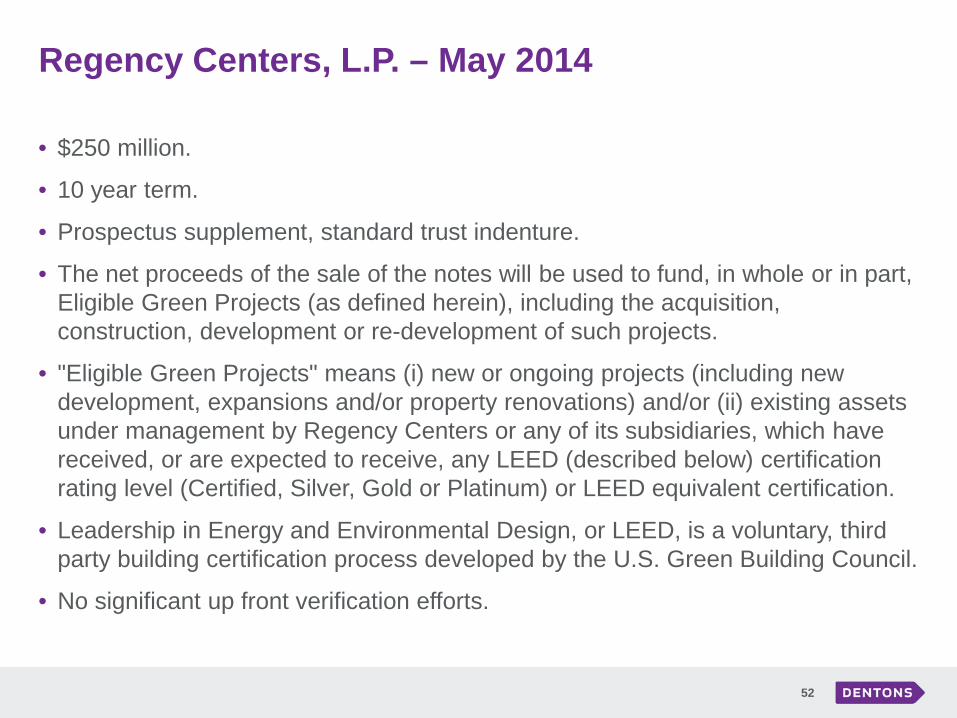

52

• $250 million.

• 10 year term.

• Prospectus supplement, standard trust indenture.

• The net proceeds of the sale of the notes will be used to fund, in whole or in part, Eligible Green Projects (as defined herein), including the acquisition, construction, development or re-development of such projects.

• "Eligible Green Projects" means (i) new or ongoing projects (including new development, expansions and/or property renovations) and/or (ii) existing assets under management by Regency Centers or any of its subsidiaries, which have received, or are expected to receive, any LEED (described below) certification rating level (Certified, Silver, Gold or Platinum) or LEED equivalent certification.

• Leadership in Energy and Environmental Design, or LEED, is a voluntary, third party building certification process developed by the U.S. Green Building Council.

• No significant up front verification efforts.

Regency Centers, L.P. – May 2014

53

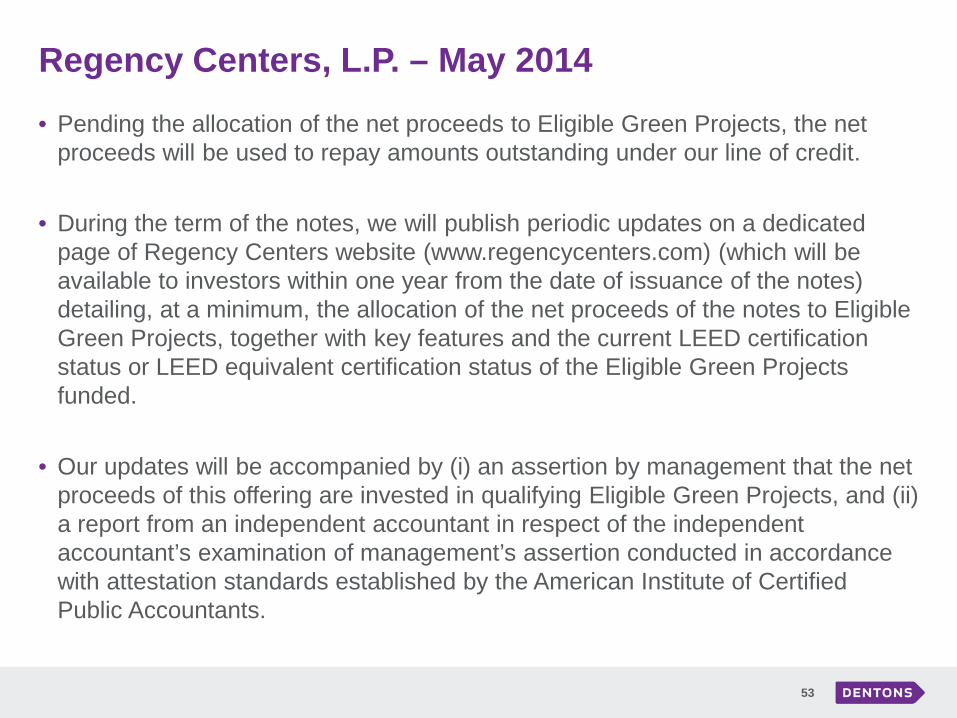

• Pending the allocation of the net proceeds to Eligible Green Projects, the net proceeds will be used to repay amounts outstanding under our line of credit.

• During the term of the notes, we will publish periodic updates on a dedicated page of Regency Centers website (www.regencycenters.com) (which will be available to investors within one year from the date of issuance of the notes) detailing, at a minimum, the allocation of the net proceeds of the notes to Eligible Green Projects, together with key features and the current LEED certification status or LEED equivalent certification status of the Eligible Green Projects funded.

• Our updates will be accompanied by (i) an assertion by management that the net proceeds of this offering are invested in qualifying Eligible Green Projects, and (ii) a report from an independent accountant in respect of the independent accountant’s examination of management’s assertion conducted in accordance with attestation standards established by the American Institute of Certified Public Accountants.

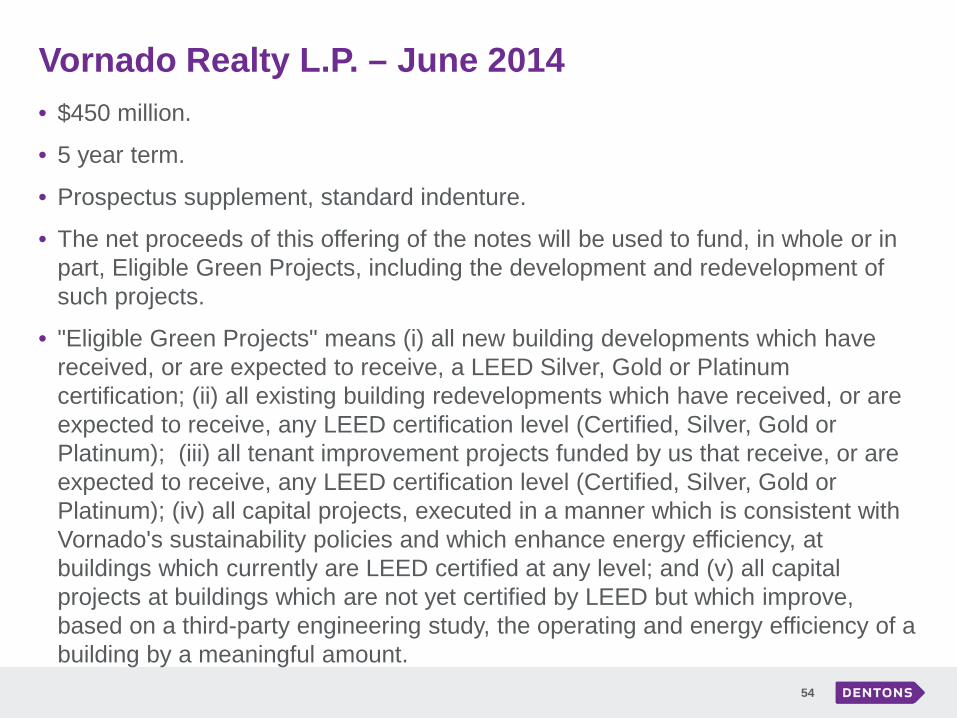

Vornado Realty L.P. – June 2014

54

• $450 million.

• 5 year term.

• Prospectus supplement, standard indenture.

• The net proceeds of this offering of the notes will be used to fund, in whole or in part, Eligible Green Projects, including the development and redevelopment of such projects.

• "Eligible Green Projects" means (i) all new building developments which have received, or are expected to receive, a LEED Silver, Gold or Platinum certification; (ii) all existing building redevelopments which have received, or are expected to receive, any LEED certification level (Certified, Silver, Gold or Platinum); (iii) all tenant improvement projects funded by us that receive, or are expected to receive, any LEED certification level (Certified, Silver, Gold or Platinum); (iv) all capital projects, executed in a manner which is consistent with Vornado's sustainability policies and which enhance energy efficiency, at buildings which currently are LEED certified at any level; and (v) all capital projects at buildings which are not yet certified by LEED but which improve, based on a third-party engineering study, the operating and energy efficiency of a building by a meaningful amount.

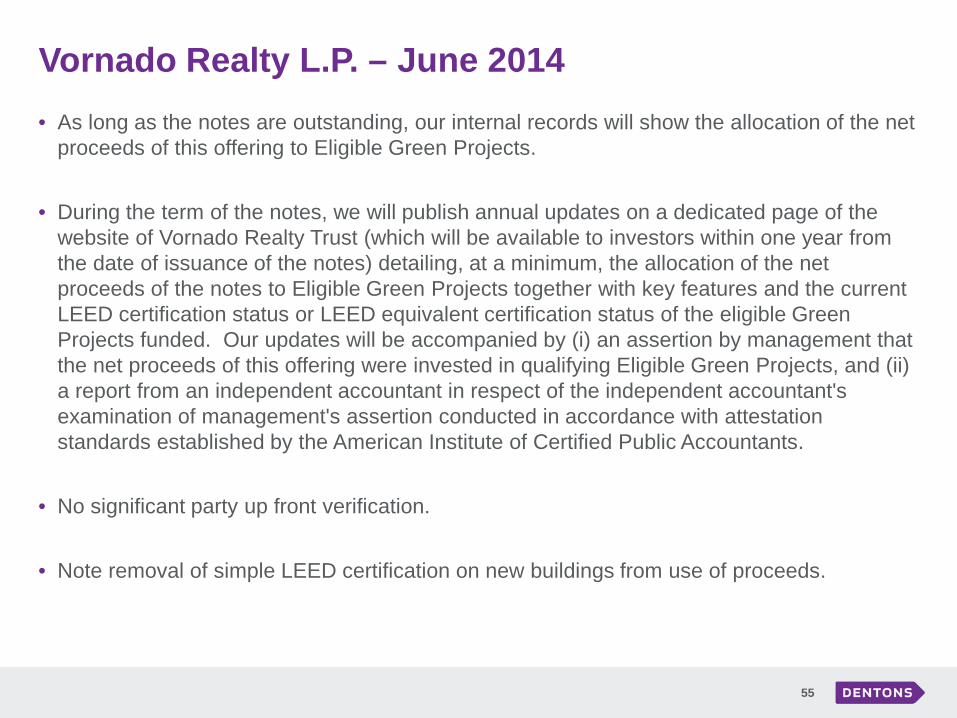

Vornado Realty L.P. – June 2014

55

• As long as the notes are outstanding, our internal records will show the allocation of the net proceeds of this offering to Eligible Green Projects.

• During the term of the notes, we will publish annual updates on a dedicated page of the website of Vornado Realty Trust (which will be available to investors within one year from the date of issuance of the notes) detailing, at a minimum, the allocation of the net proceeds of the notes to Eligible Green Projects together with key features and the current LEED certification status or LEED equivalent certification status of the eligible Green Projects funded. Our updates will be accompanied by (i) an assertion by management that the net proceeds of this offering were invested in qualifying Eligible Green Projects, and (ii) a report from an independent accountant in respect of the independent accountant's examination of management's assertion conducted in accordance with attestation standards established by the American Institute of Certified Public Accountants.

• No significant party up front verification.

• Note removal of simple LEED certification on new buildings from use of proceeds.

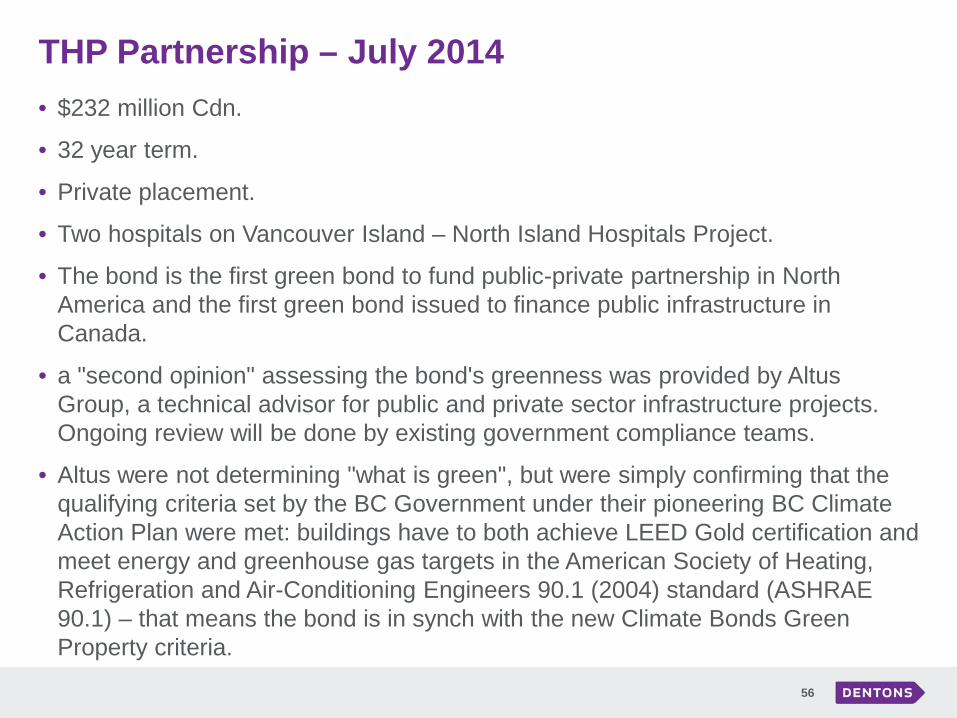

THP Partnership – July 2014

56

• $232 million Cdn.

• 32 year term.

• Private placement.

• Two hospitals on Vancouver Island – North Island Hospitals Project.

• The bond is the first green bond to fund public-private partnership in North America and the first green bond issued to finance public infrastructure in Canada.

• a "second opinion" assessing the bond's greenness was provided by Altus Group, a technical advisor for public and private sector infrastructure projects. Ongoing review will be done by existing government compliance teams.

• Altus were not determining "what is green", but were simply confirming that the qualifying criteria set by the BC Government under their pioneering BC Climate Action Plan were met: buildings have to both achieve LEED Gold certification and meet energy and greenhouse gas targets in the American Society of Heating, Refrigeration and Air-Conditioning Engineers 90.1 (2004) standard (ASHRAE 90.1) – that means the bond is in synch with the new Climate Bonds Green Property criteria.

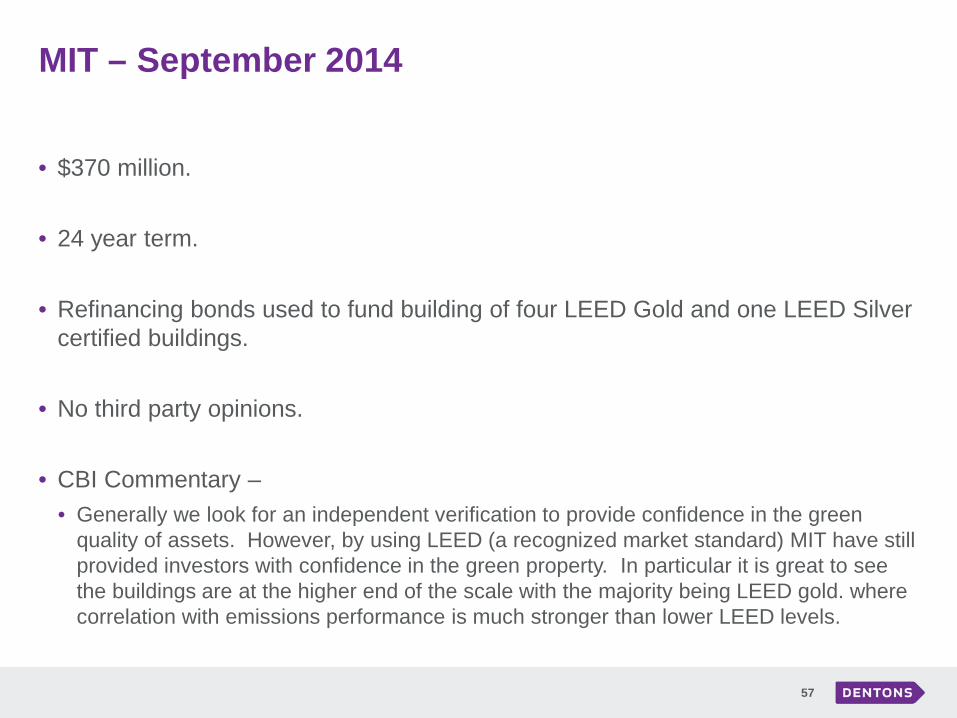

MIT – September 2014

57

• $370 million.

• 24 year term.

• Refinancing bonds used to fund building of four LEED Gold and one LEED Silver certified buildings.

• No third party opinions.

• CBI Commentary – • Generally we look for an independent verification to provide confidence in the green

quality of assets. However, by using LEED (a recognized market standard) MIT have still provided investors with confidence in the green property. In particular it is great to see the buildings are at the higher end of the scale with the majority being LEED gold. where correlation with emissions performance is much stronger than lower LEED levels.

Fastghets AB Forvaltaven – October 2014

58

• 400 million SEK.

• 7 year term.

• Eligible green building projects – framework reviewed by Cicero.

• Residential and commercial buildings, new or refurbished, must meet a recognised green building standard. The level required is: • Miljöbyggnad (a Swedish green building standard) – minimum “silver”. • LEED – minimum “gold”. • BREEAM SE (operated by the Swedish Green Building Council under licence

from BRE Global) – minimum “very good”.

• CBI Commentary - • While it’s good to see recognized standards being used for green buildings, the

view of our international expert panel is that it’s the performance of the building in relation to a local baseline [that] matters.

Fastghets AB Forvaltaven – October 2014

59

• Highly rated LEED is a reasonable proxy while emissions reporting is being developed; but it’s important to understand the issue. As John H. Scofield found in his recent ScienceDirect paper “Efficacy of LEED-certification in reducing energy consumption and greenhouse gas emission for large New York city office buildings, there is little correlation between building emissions performance and Silver or Basic LEED; but there is some correlation for Gold LEED. This is not a new finding. LEED of course addresses all sorts of very useful issues in relation to environmental performance; but wearing our climate change urgency glasses, we are concerned that ambitious emission reductions are part of any inclusion as green – that leads us to be generally supportive of LEED Gold and Platinum buildings being included – for example last week’s MIT bond and this bond – although we will be pushing hard for emissions reporting hurdles to be met to ensure the buildings contribute emission reductions.

Fastghets AB Forvaltaven – October 2014

60

• Förvaltaren have covered performance issues by including a caveat that buildings must also achieve “25% less energy usage than required by applicable codes and regulations” (CICERO report). The hurdle rate is a good addition to the criteria.

• Förvaltaren have committed to reporting through annual newsletters. Included in the report will be a list of projects financed and examples of projects. This transparency allows investors to see how proceeds are allocated. We hope there will also be details of each property energy performance in the newsletter.

Stockland – November 2014

61

• 300 million Euros.

• 7 year term.

• The green bond framework was reviewed by KPMG.

• Proceeds will go to investment in the development, redevelopment or tenant improvements that have, or expected to receive, Green Star ratings of 4, 5 or 6 or equivalent. Additionally, proceeds can be allocated to capital projects that have a third party verify that any reductions in energy, water and/or waste will be achieved. Stockland will also apply their own sustainability policies to select projects within these categories.

Stockland – November 2014

62

• CBI Commentary – • Green Star scheme rates on a scale from 4 to 6, which implies any Green Star

rating is included in Stockland’s eligibility criteria. Okay. As for what that means in terms of specific environmental impacts, such as energy and emissions, this is more difficult to tease out. The Green Star ratings, like other green buildings standards such as LEED and BREEAM, is not a rating system that is focused on energy or greenhouse gas emissions – it uses a broader definition of green buildings. The lowest standard of 4 Green Star is understood to be able to be achieved [without] any specific credits awarded in the Energy category.

• It’s worth emphasising that we do think rating tools have a role to play in markets where reliable baselines can’t be established and therefore taking a robust approach to evaluate emissions reductions is not possible. However, the ambition should be to include buildings that will perform at the higher end of the ratings scale.

Stockland – November 2014

63

• In the case of Stockland and Australia, data on baselines is readily available, and so green property bonds do not have to rely on design and construction rating tools, such as Green Star.

• We would also like to see some more details from Stockland around post-issuance reporting. The company has committed to public annual reporting, which is in line with best practice. Great! Reporting will include disclosure on allocation of proceeds to eligible projects, and where applicable, disclosure of the Green Star rating or equivalent. Good to see reporting commitments on a specific indicator - but again, this does not provide information on the energy or emissions improvements associated with the bond over time.

University of Cincinnati – December 2014

64

• $30 million.

• 7 – 27 year term.

• Renovation of a 50 year old student hall.

• No third party opinions.

• Expect to achieve of LEED Silver certification.

• Provides estimate of energy use reduction (based on similar renovation) – 46% target.

• CBI Commentary – • Now, a key difference between the MIT bond and [this] bond is that MIT was re-financing

existing green buildings. Investors knew that the buildings in the MIT bond had achieved either LEED Gold or Silver certification. Cincinnati and Indiana are using proceeds for new projects with and are aiming to achieve LEED Silver. The outcome of the projects is not guaranteed. This is where reporting on the environmental outcomes of green property is important. At a minimum we would expect reporting on certification and energy performance achieved (like Cincinnati has done for Morgens Hall). [The university has] committed to reporting the allocation of proceeds (which is great) fingers crossed they will report on LEED rating and subsequent energy performance of the buildings at the same time.

University of Indiana – December 2014

65

• $59 million.

• 1 – 19 year term.

• Student hall renovation and new art and science building.

• No third party opinions.

• Expect to earn a LEED Silver certification.

Mass. State College – December 2014

66

• $92 million.

• 2 – 20 year term.

• New building, a renovation and a car park.

• Buildings expected to be LEED Silver rated.

• CBI questions “Green Garage Certification” – energy efficiency?

Green Bonds - Appendix Power Generation

Electricite de France (EDF) – November 2013

68

• €1.4 billion (Euros).

• 7 year term.

• Issued under EDF's MTN program.

• Net proceeds to a sub-portfolio of issuer to be used for financing green projects – renewable energy power plants in Europe and North America - either its own or third parties’.

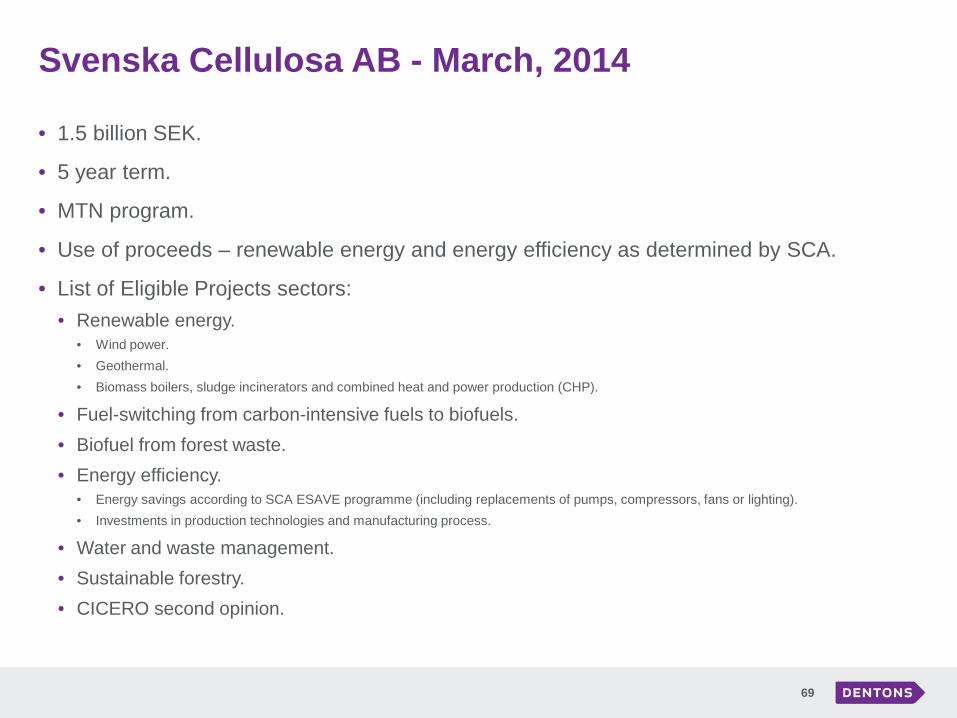

Svenska Cellulosa AB - March, 2014

69

• 1.5 billion SEK.

• 5 year term.

• MTN program.

• Use of proceeds – renewable energy and energy efficiency as determined by SCA.

• List of Eligible Projects sectors: • Renewable energy.

• Wind power. • Geothermal. • Biomass boilers, sludge incinerators and combined heat and power production (CHP).

• Fuel-switching from carbon-intensive fuels to biofuels. • Biofuel from forest waste. • Energy efficiency.

• Energy savings according to SCA ESAVE programme (including replacements of pumps, compressors, fans or lighting). • Investments in production technologies and manufacturing process.

• Water and waste management. • Sustainable forestry. • CICERO second opinion.

Iberdrola - April, 2014

70

• €750 million (Euros).

• 8 year term.

• Use of Proceeds – renewable energy production, electric power distribution and transmission networks that contribute to connect renewable energy production to network and improve networks in terms of energy demand-side management, energy efficiency and access to electricity.

GDF Suez – May 2014

71

• €2.5 billion.

• 6 – 12 year term.

• Use of Proceeds - "projects that contribute to fighting climate change".

• Renewable non-fossil energy technologies, mainly wind and solar but also including geothermal and biomass and energy efficiency projects – projects that contribute to a reduction of energy consumption per unit of output, e.g. heating and cooling network, optimization of building or plant efficiency, systems for energy management (smart monitoring), co-generation, combined heat and power production.

GDF Suez – May 2014

72

• Does not include fossil fuel or nuclear facilities.

• Vigeo, the ethical rating agency based in Paris, has validated the criteria GDF uses to select eligible projects.

• Entire proceeds will be held in its treasury in money market investments until they can be disbursed on green projects.

• The use of proceeds is checked by GDF’s auditor, but the actual compliance with environmental targets is up to GDF and will be reported on by itself.

NRG Yield Operating LLC – August 2014

73

• Funds raised to buy Alta Wind facility, and for equipment and systems that generate or facilitate the generation of energy from renewable sources, such as solar, wind and geothermal energy.

• No independent review.

• 43% of assets of issuer “green”.

• Periodic reporting on use of proceeds available to investors within one year.

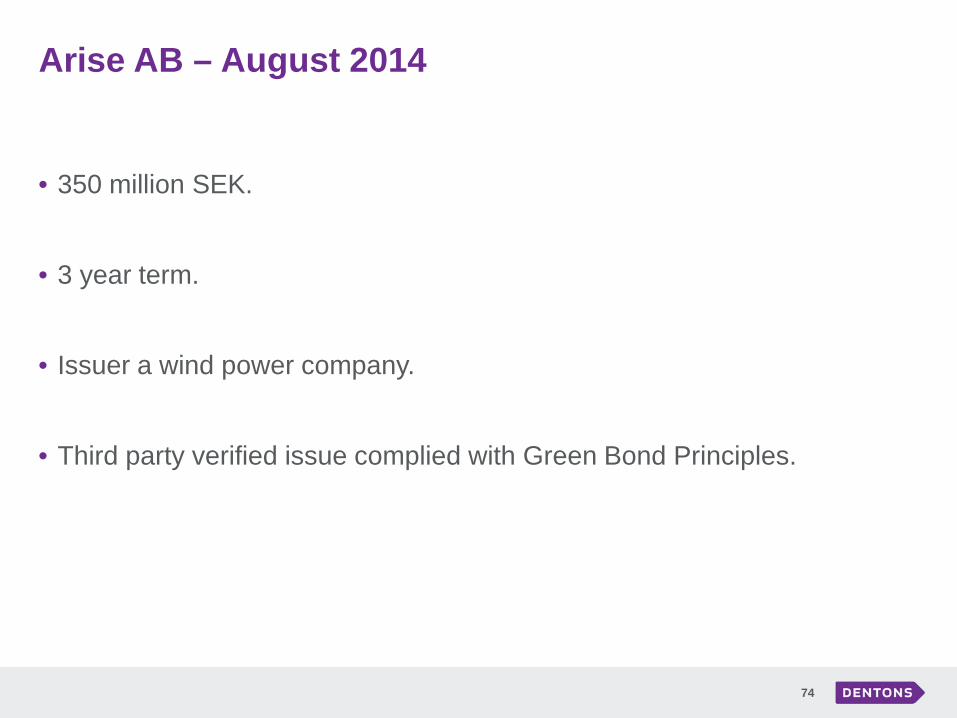

Arise AB – August 2014

74

• 350 million SEK.

• 3 year term.

• Issuer a wind power company.

• Third party verified issue complied with Green Bond Principles.

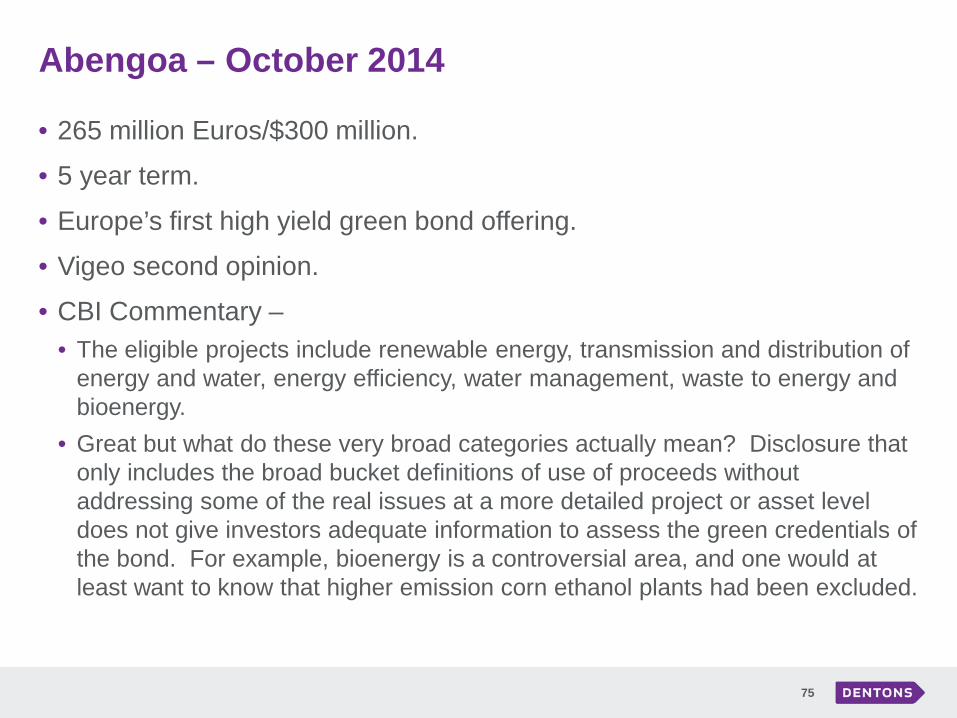

Abengoa – October 2014

75

• 265 million Euros/$300 million.

• 5 year term.

• Europe’s first high yield green bond offering.

• Vigeo second opinion.

• CBI Commentary – • The eligible projects include renewable energy, transmission and distribution of

energy and water, energy efficiency, water management, waste to energy and bioenergy.

• Great but what do these very broad categories actually mean? Disclosure that only includes the broad bucket definitions of use of proceeds without addressing some of the real issues at a more detailed project or asset level does not give investors adequate information to assess the green credentials of the bond. For example, bioenergy is a controversial area, and one would at least want to know that higher emission corn ethanol plants had been excluded.

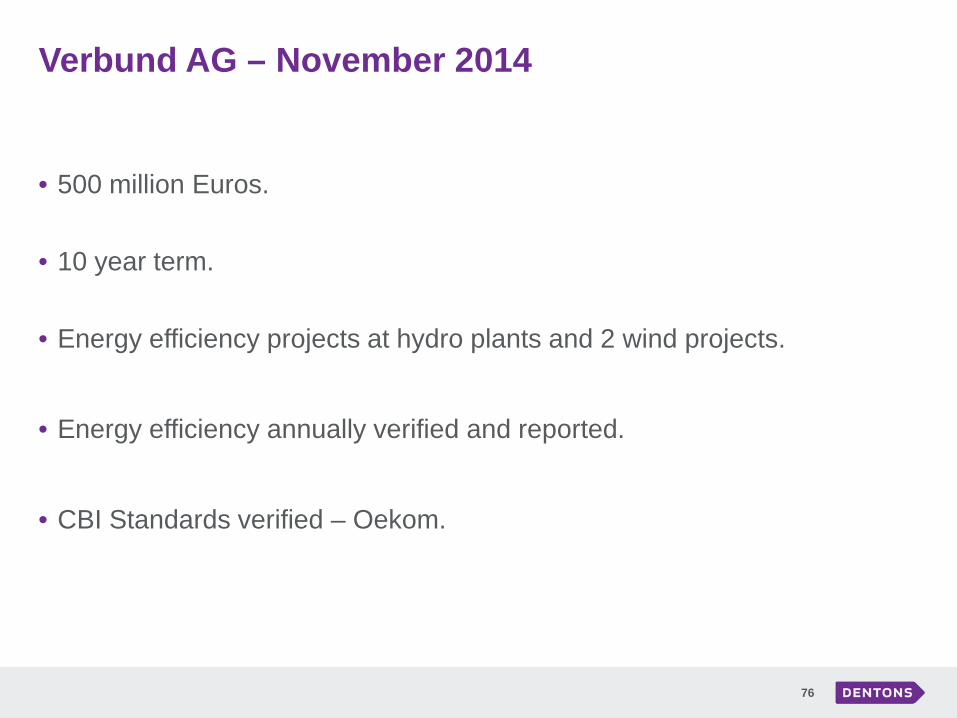

Verbund AG – November 2014

76

• 500 million Euros.

• 10 year term.

• Energy efficiency projects at hydro plants and 2 wind projects.

• Energy efficiency annually verified and reported.

• CBI Standards verified – Oekom.

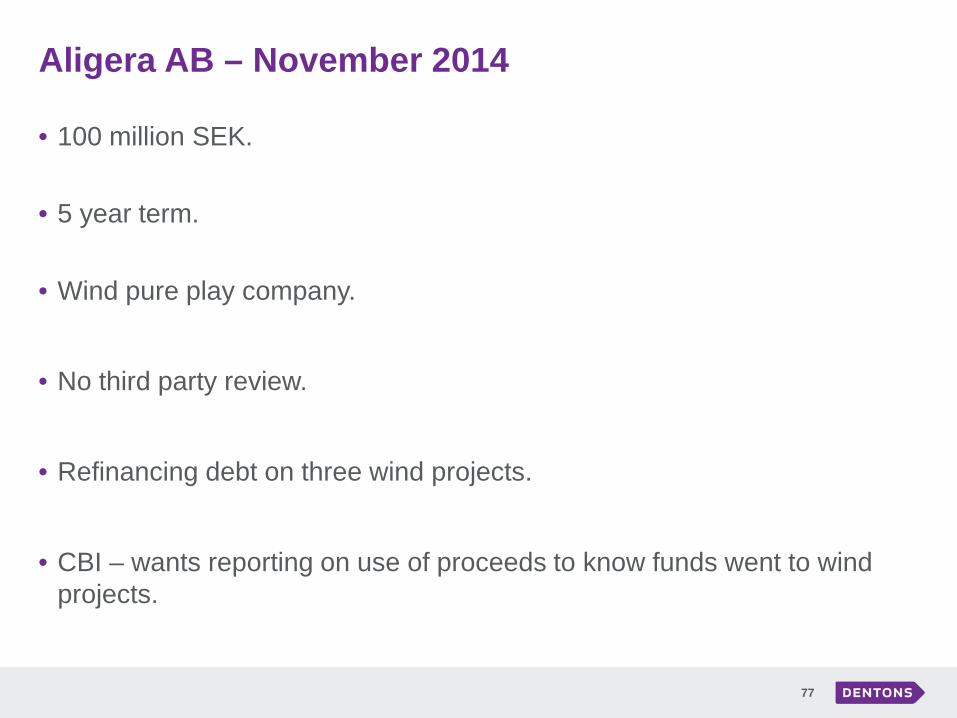

Aligera AB – November 2014

77

• 100 million SEK.

• 5 year term.

• Wind pure play company.

• No third party review.

• Refinancing debt on three wind projects.

• CBI – wants reporting on use of proceeds to know funds went to wind projects.

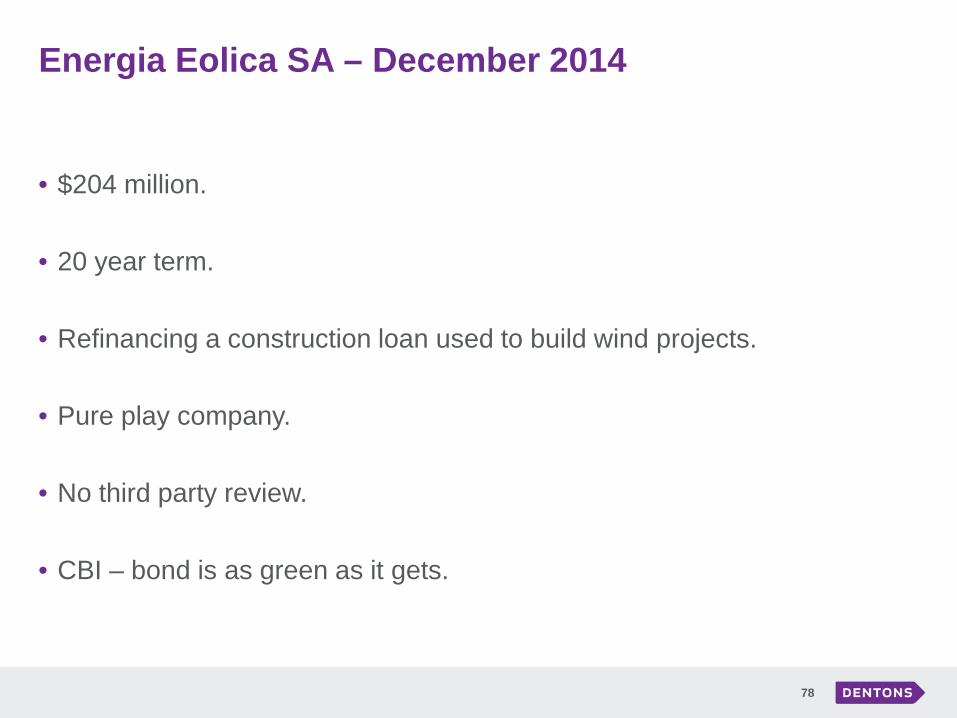

Energia Eolica SA – December 2014

78

• $204 million.

• 20 year term.

• Refinancing a construction loan used to build wind projects.

• Pure play company.

• No third party review.

• CBI – bond is as green as it gets.

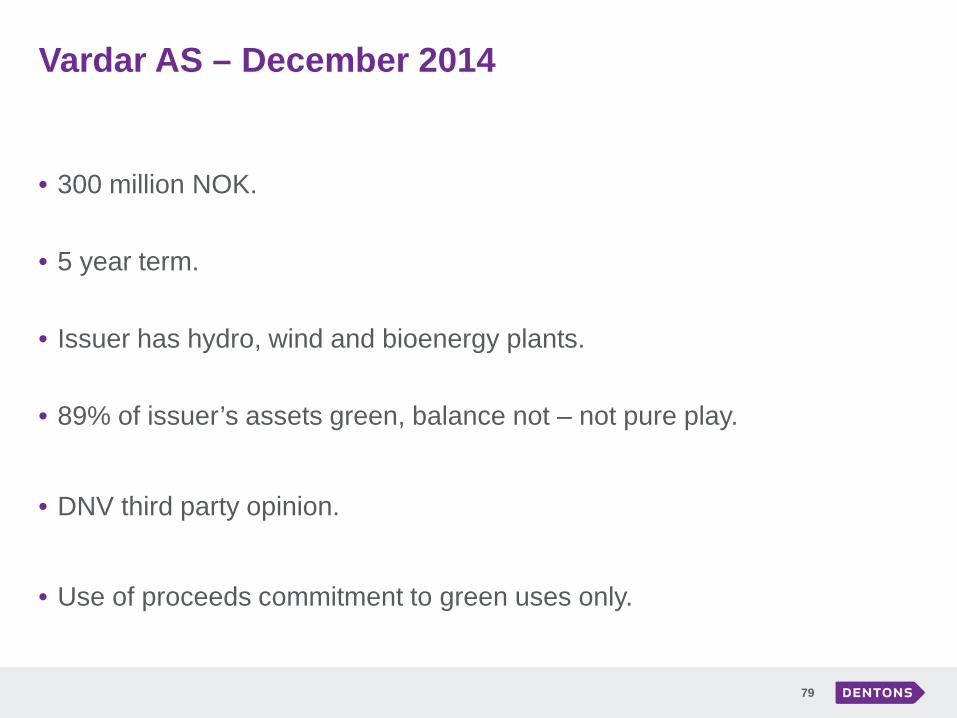

Vardar AS – December 2014

79

• 300 million NOK.

• 5 year term.

• Issuer has hydro, wind and bioenergy plants.

• 89% of issuer’s assets green, balance not – not pure play.

• DNV third party opinion.

• Use of proceeds commitment to green uses only.

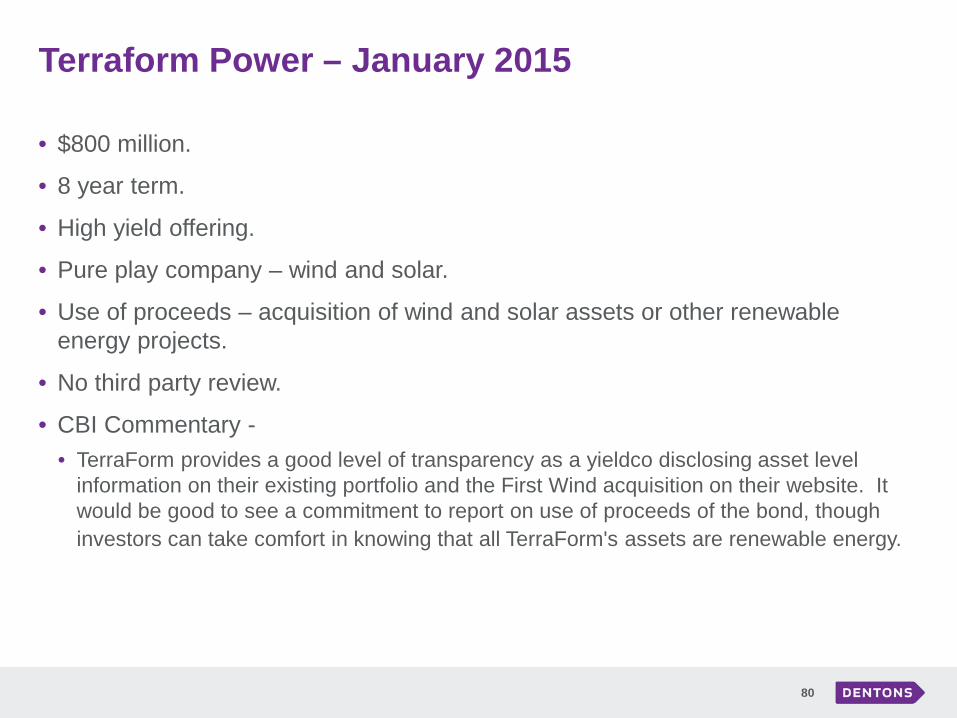

Terraform Power – January 2015

80

• $800 million.

• 8 year term.

• High yield offering.

• Pure play company – wind and solar.

• Use of proceeds – acquisition of wind and solar assets or other renewable energy projects.

• No third party review.

• CBI Commentary - • TerraForm provides a good level of transparency as a yieldco disclosing asset level

information on their existing portfolio and the First Wind acquisition on their website. It would be good to see a commitment to report on use of proceeds of the bond, though investors can take comfort in knowing that all TerraForm's assets are renewable energy.

Terraform Power – January 2015

81

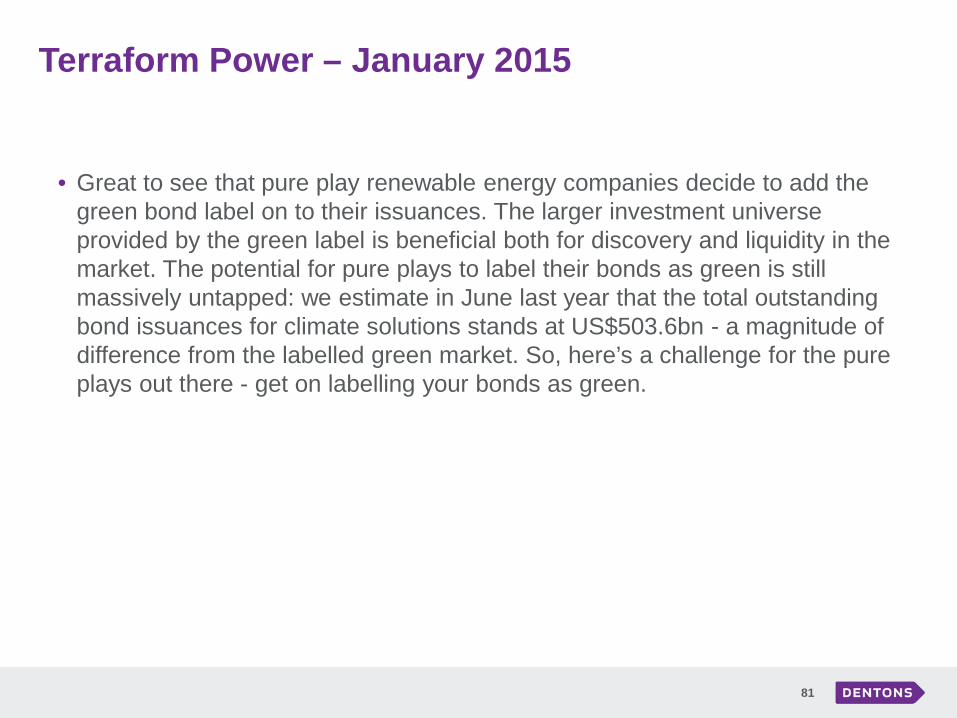

• Great to see that pure play renewable energy companies decide to add the green bond label on to their issuances. The larger investment universe provided by the green label is beneficial both for discovery and liquidity in the market. The potential for pure plays to label their bonds as green is still massively untapped: we estimate in June last year that the total outstanding bond issuances for climate solutions stands at US$503.6bn - a magnitude of difference from the labelled green market. So, here’s a challenge for the pure plays out there - get on labelling your bonds as green.

Northland Power – November 2014

82

• Project bond for solar power project.

• CBI Commentary – • If Northland had decided to monitor and report on proceeds (and ideally gained

a second opinion on green) we could easily have welcomed it to the green labelled universe.

• Overall, exciting issuance structure – we hope to see it replicated by other utilities and renewable energy developers. Great work, Northland!

Nord-Trondelag Elektrisitetsverk – November 2014

83

• 650 million NOK.

• 3 – 5 year term.

• Refinancing debt used to acquire 4 hydro projects in Norway.

• Second opinion – compliance with Green Bond Principles.

• CBI – not all hydro is green and so need analysis of environmental benefits on project basis.

Jefferson County NY – November 2014

84

• Biomass power plant.

• CBI Commentary - • sustainability of sourcing of biomass? Air pollution? – need a report on on

sustainability and reporting of air emissions.

Utah Associated Municipal Power System – December 2014

85

• $21 million.

• 20 year term.

• Recycling waste heat to generate power and potential to remove 737,000 tonnes of CO2 over 30 years.

• CBI Commentary – • When taken in isolation (from the gas turbine) it can be described as a “green” project –

but its entire process is dependent on gas, where the jury is still well and truly out about what you could call “green”. The project could be compared to a refurbishment or energy efficiency project in a gas power plant which would elongate the life of the gas generator. Hmm… not quite convinced on the green credentials of this one yet, although we do appreciate there’s a complex argument about gas as a transition investment in some countries – but that needs careful analysis as it doesn’t always stack up.

Green Bonds - Appendix Other Projects

Unilever – March 2014

87

• £250 million (pounds).

• 5 year term.

• Use of Proceeds - to fund a number of new factories.

• DNV GL, an environmental consultancy, developed green bond sustainability framework based on Green Bond Principles.

• Capital expenditures to cut in half the amount of waste, water usage and greenhouse gas emissions of existing factories.

• DNV GL is to vet the projects annually against the pledged criteria.

• Reportedly 3 times over-subscribed.

Toyota - March, 2014

88

• $1.75 billion.

• 1 – 6 year term.

• Prospectus supplement to base prospectus.

• Toyota used securitizations of car leases to finance new Toyota and Lexus gas, electric, hybrid or alternative fuel power train vehicles (low emission vehicles).

Innovatec – October 2014

89

• 10 million Euros.

• 6 year term.

• Pure play company – energy efficiency/services company.

• But use of proceeds – "energy efficiency projects".

• CBI – need a second opinion.

• CBI - However, Innovatec has not provided a second party opinion on the green criteria of the bond, or details around disclosure and reporting. This isn't just us pushing for that, it's also in the Green Bond Principles. While less crucial for pure play companies than non-pure play corporations, it really would help to have this to provide further transparency for investors.

![Green Bonds - - EESL PPT Gaurav.pdf · 4 Leading Green Bonds in Asia [1/2] Thought Leadership in Green bonds in Asia India Green Bonds Market Development Council: In recognition of](https://img.pdfslide.net/doc/110x75/5b93665609d3f2d9098d351d/green-bonds-eesl-ppt-gauravpdf-4-leading-green-bonds-in-asia-12-thought.jpg)

![Green bonds - OECD.org bonds PP [f3] [lr].pdf · Debt currently finances the majority of LCR Annual issuance of labelled green bonds ... of green bonds. l The speed at which green](https://img.pdfslide.net/doc/110x75/5ae1edf67f8b9a7b218b5d7e/green-bonds-oecd-bonds-pp-f3-lrpdfdebt-currently-finances-the-majority-of.jpg)