Embed Size (px)

Citation preview

Base Erosion and Profit Shifting (‘BEPS’) –Conceptual Analysis and CbyC reporting

ICAI International Tax Convention

Western India Regional Council

Baroda and Anand Branches

C.A. Hitesh D. Gajaria

9 August 2015

•

Areas of discussion

OECD BEPS Action Plan 1

Action 13 – Transfer Pricing Documentation and Country-by-Country reporting9

Action 8 – Transfer Pricing aspects of intangibles7

Action 1 – Address the tax challenges of digital economy2

Action 2 – Neutralise the effect of hybrid mismatch arrangements

Action 5 – Counter harmful tax practices more effectively, taking into account transparency and substance

Action 6 – Prevent treaty abuse

Action 15 – Develop multilateral instrument

3

4

5

6

Action 10 – Transfer Pricing aspects of intragroup services – Discussion draft8

Organization for Economic Co-operation and Development (OECD)

BEPS Action Plan

Organization for Economic Co-operation and Development (OECD)

BEPS Action Plan

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

3

OECD – BEPS 2014/15OECD BEPS Action Plan – In a nutshell

19 July 2013 - OECD Action Plan on Base Erosion and Profit Shifting (BEPS) - 15 focus areas for potential change in international tax rules and treaties, presented to G20 Finance Ministers

Purpose - Ensure profits are taxed where economic activities generating them are performed and where value is created

15 Specific Actions – to be achieved before 31 Dec, 2015

On 16 September 2014, OECD released its first set of recommendations for 7 out of 15 Action Points.

India is not a member of OECD, but has an observer status and is serving on the OECD governing body for the BEPS project

Coherence of corporate

tax at the international

level

Transparency, coupledwith certainty and

predictability

Realignment of taxation

and substance

15 Actions organized around three main pillars

“BEPS arises because under the existing rules MNEs are often able to artificially separate the allocation of their taxable profits from the jurisdictions in which these profits arise

This can result in income going untaxed anywhere, and significantly reduces the corporate income tax paid by MNEs in the jurisdictions where they operate, thus affecting competition, distorting investment decisions and reducing overall trust in the tax system.“

– OECD Webinar

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

4

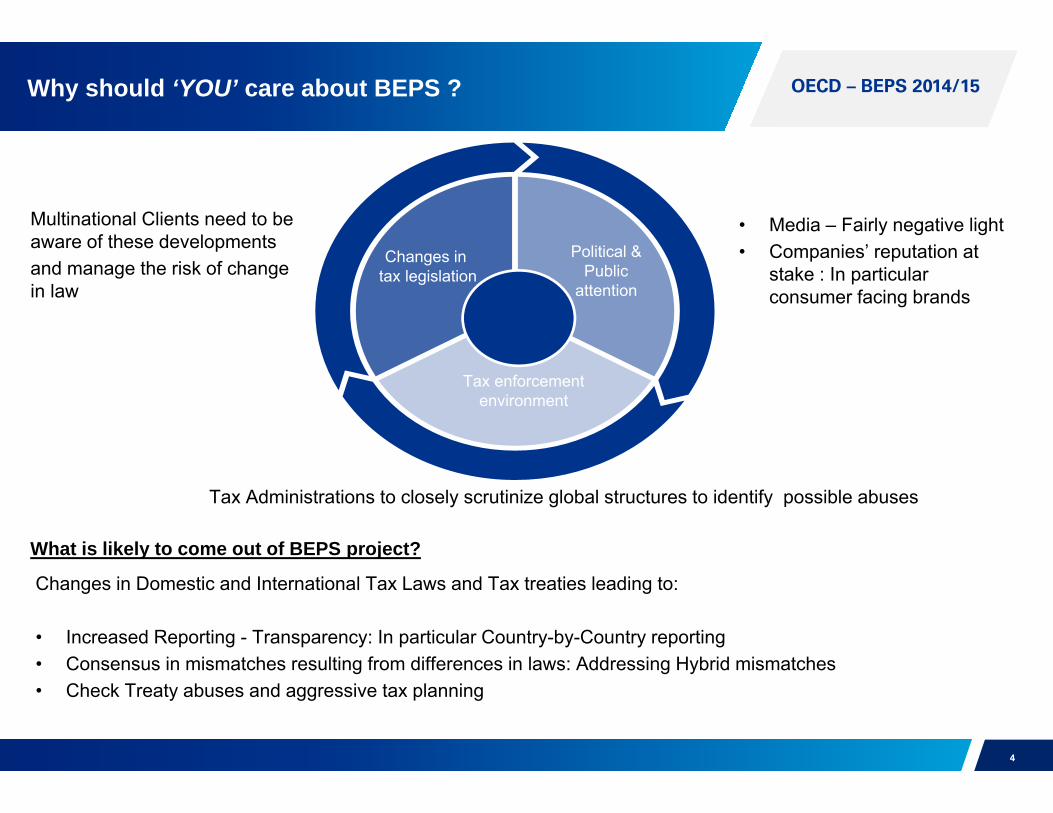

OECD – BEPS 2014/15Why should ‘YOU’ care about BEPS ?

Political & Public

attention

Changes in tax legislation

Tax enforcement environment

• Media – Fairly negative light• Companies’ reputation at

stake : In particular consumer facing brands

Tax Administrations to closely scrutinize global structures to identify possible abuses

Multinational Clients need to be aware of these developments and manage the risk of change in law

What is likely to come out of BEPS project?

Changes in Domestic and International Tax Laws and Tax treaties leading to:

• Increased Reporting - Transparency: In particular Country-by-Country reporting• Consensus in mismatches resulting from differences in laws: Addressing Hybrid mismatches• Check Treaty abuses and aggressive tax planning

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

5

OECD – BEPS 2014/15India's Consent - Important factor for consensus on BEPS

Three-Tier TP Documentation including Country by Country (‘CbyC’) reporting

• Companies should provide information relating to CbyC reporting starting FY 2016-2017

• Indian TP regulations on CbyC reporting would be made public (for comments) prior to implementation in 2016

Changes in Domestic laws and DTAAs as a result of BEPS recommendations

• Indian Government expects Indian Corporates to be aware of BEPS and proposed changes that may happen

• Indian Government would follow BEPS recommendations while drafting domestic laws which will be firmed up in 2016 after all BEPS recommendations are released.

• Development of a Multi-Lateral Instrument (MLI) is key to amend several DTAAs and India is supporting the same

• Grand fathering of previous tax structures - May not happen – but no decision has been taken as of now

Source:1. Minutes of Tax officers offsite organized by Ministry of Finance and CII’s presentation at the meeting on 25 November 20142. www.taxsutra.com

Indian Competent Authority Mr Akhilesh Ranjan has stated that ‘the Indian Government expects Corporations to start providing information relating to CbyC reporting from 2016-17, it was indicated that corporations should be aware of BEPS and proposed changes that may happen and ignorance may not be a valid excuse’

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

6

OECD – BEPS 2014/15India's Consent - Important factor for consensus on BEPS

Automatic Exchange of Information (AEOI):

• On 4 June 2015 India along with Australia, Canada, Chile, Costa Rica, Indonesia and New Zealand joined the Multilateral Competent Authority Agreement (MCAA), bringing up the total number of jurisdictions to have signed the MCAA to 61

• The MCAA implements the Standard for Automatic Exchange of Financial Information in Tax Matters, developed by the OECD and G20 countries and presented in 2014. Till date, 94 jurisdictions have committed to implement the above standard, agreeing to launch the first Automatic Information Exchanges in 2017 or 2018.

Source:1. Minutes of Tax officers offsite organized by Ministry of Finance and CII’s presentation at the meeting on 25 November 20142. www.taxsutra.com

Automatic Exchange of Information (AEOI) by means of a Multilateral Competent Authority Agreement (MCAA), to be used for CbyC Reports

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

7

OECD – BEPS 2014/15

Action 1:

Address the tax challenges of the digital economy

Action 1:

Address the tax challenges of the digital economy

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

8

OECD – BEPS 2014/15Action plan 1 - Background

Digital Economy• Unparalleled reliance on intangible assets,• Massive use of data (notably personal data),• Widespread adoption of multi-sided business models capturing value from externalities generated by

free products,• Difficulty of determining the jurisdiction in which value creation occurs.This raises fundamental question as to how enterprises in the digital economy add value and make theirprofits, and how the digital economy relates to the concepts of source and residence or thecharacterization of income for tax purposes.New ways of doing business may result in a relocation of core business functions and, consequently, adifferent distribution of taxing rights which may lead to low taxation is not per se an indicator of defects inthe existing system.It is important to examine closely how enterprises of the digital economy add value and make their profitsin order to determine whether and to what extent it may be necessary to adapt the current rules in order totake into account the specific features of that industry and to prevent BEPS

MNEs use of gaps in the interaction of different tax systems to artificially reduce taxable income or shift profits to low tax jurisdictions in which little or no economic activity is performed

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

9

OECD – BEPS 2014/15Action 1 – Address the tax challenges of the digital economy

Identify the main difficulties that the digital economy poses for the application of existinginternational tax rules:

• Develop detailed options to address these difficulties, taking a holistic approach and considering bothdirect and indirect taxation.

• Issues to be examined include, ability of a company to have a significant digital presence in theeconomy of another country without being liable to taxation due to the lack of nexus under currentinternational rules.

• Attribution of value created from the generation of marketable location relevant data through the use ofdigital products and services

• Characterisation of income derived from new business models• Application of related source rules• How to ensure the effective collection of VAT / GST with respect to the cross-border supply of digital

goods and services.

Such work will require a thorough analysis of the various business models in this sector.

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

10

OECD – BEPS 2014/15Digital Economy – Key features

Mobility of (i) intangibles on which the digital economy relies heavily, (ii) users, and (iii) business functions as a consequence of the decreased need for local personnel to perform certain functions and (iv) flexibility in many cases to choose the location of servers

Reliance on Data

Network effects, understood with reference to user participation, integration and synergies

Use of multi-sided business models – Markets in Different jurisdictions

Monopoly / Oligopoly in certain business models relying heavily on network effects

Volatility due to low barriers to entry and rapidly evolving technology

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

11

OECD – BEPS 2014/15Digital Economy - Challenges

Ring-fencing of the digital economy from the rest of the economy

Fragmentation of operations among multiple group entities and thereby qualify for PE exceptions

Minimising the income allocable to functions, assets and risks

Using a subsidiary or PE to perform marketing or technical support

Maintaining mirrored servers to enable faster customer access to the digital products sold by the group with a principal company contractually bearing the risks and claiming the ownership of intangible generated by these activities

Maximise the use of deduction for payments made to other group companies in the form of interest, royalties, fees etc.

Avoiding withholding tax

Absence of CFC regulations or CFC regime failing to apply certain categories of income that are highly mobile or CFC regime that can be avoided by using hybrid mismatches

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

12

OECD – BEPS 2014/15Tax Challenges raised by Digital Economy

Identification of sellers / services providers

Determining the extent of activities

Identification of customers

Information collection and verification

Administrative challenges

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

13

OECD – BEPS 2014/15

Action 2:

Neutralising Hybrid Mismatches

Action 2:

Neutralising Hybrid Mismatches

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

14

OECD – BEPS 2014/15Hybrid Mismatches – Background

Hybrid arrangements – Involve use of cross-border differences in characterisation of entities and instruments to produce mismatched tax outcomes

Objective of the BEPS Action Plan is to develop model treaty provisions and design domestic rules to neutralize the effect of hybrid instruments / entities by not permitting:

• Multiple deductions for a single expense

• Deduction in one country without corresponding taxation in another

• Generation of multiple foreign tax credits for one amount of foreign tax paid

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

15

OECD – BEPS 2014/15Hybrid Mismatch – Domestic Rule Recommendations

A Co.

B Co.

Country A

Country BHybrid Financial

instrument

DEDUCTION IN ONE COUNTRY WITHOUT TAXATION IN ANOTHER:

B Co issues a hybrid financial instrument to A Co.

Instrument is characterized as debt in Country B and as equity in Country A

Country B allows deduction to B Co. for interest payments made on the instrument

Country A treats the payment as ‘dividend’, which is entitled to participation exemption

BEPS Recommendations:

Country B to deny deduction to Payer (B Co.)

Defensive rule: Country A to treat receipt as ordinary income of A Co.

Interest

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

16

OECD – BEPS 2014/15Hybrid Mismatch – Domestic Rule Recommendations

A Co.

Country A

Country B

B Co.B Co.

B Sub 1(Operating Sub)

Bank

Interest

Loan

DOUBLE DEDUCTION ON PAYMENTS BY HYBRIDS:

B Co. is a 100% subsidiary of A Co.

B Co. is disregarded for Country A tax purposes

B Co. borrows money and pays interest in Country B (B Co. derives no other income)

Interest payment are deductible in the hands of A Co. in Country A, since B Co. is disregarded

B Co. is consolidated with B Sub 1 for tax purposes in Country B – Interest paid by B Co. claimed as deduction against operating income of B Sub 1

BEPS Recommendations:

Country A (Parent Jurisdiction) to deny deduction

Defensive rule: Country B (Payer Jurisdiction) to deny deduction

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

17

OECD – BEPS 2014/15Hybrid Mismatch – Treaty Recommendations

Dual resident entities: Residential status to be determined by competent authorities on a case to case

basis rather than based on POEM

Transparent entities: Transparent entities to be entitled to treaty benefits to the extent income is treated for

tax purposes as income of a resident

UKPartnership

Income from India

US Partners UK Partners

Outside India

India

60%40%

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

18

OECD – BEPS 2014/15Hybrid Mismatch – Impact of BEPS recommendations in India

BEPS recommendations (once implemented) are likely to impact cross-borderarrangements / instruments where tax characterisations vary in both countries

In an Indian context, such risks may typically revolve around situations where :

• Debt Instruments issued by Indian Cos (e.g. CCDs) may be considered as equityin the debenture holders’ jurisdictions

• Indian Partnerships / LLPs may be considered pass-through in overseasjurisdictions

• Dual-resident companies

There is a need to identify arrangements like the above which could be hit under BEPSand to take remedial measures

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

19

OECD – BEPS 2014/15

Action 5: Countering Harmful Tax Practices by Transparency and Substance

Action 5: Countering Harmful Tax Practices by Transparency and Substance

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

20

OECD – BEPS 2014/15Countering Harmful Tax Practices by Transparency and Substance

Forum on Harmful Tax Practices (‘FHTP’) to take necessary action to:

• Review of member country preferential regimes;

• Strategy to expand participation to non-OECD member countries; and

• Consideration of revisions or additions to the existing framework

In Review of the existing preferential regimes, emphasis put on:

• Devising methodology to define the substantial activity requirement in the context of IP regimes;

• Improving transparency through compulsory spontaneous exchange on rulings related to preferential regimes

Progress report provided on the review of regimes of OECD member and associate countries in the OECD / G20 Project on BEPS

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

21

OECD – BEPS 2014/15Factors

Four Key factors Eight other factors

• No or low effective rates on income from geographically mobile financial and other service activities

• Ring fenced from the domestic economy

• Lacking Transparency

• No effective exchange of information with respect to the regime

• Artificial definition of the tax base

• Failure to adhere to international transfer pricing principles

• Foreign source income exempt from residence country taxation

• Negotiable tax rate or tax base

• Existence of secrecy provisions

• Access to a wide network of tax treaties

• Regime promoted as a tax minimization vehicle

• Encourages purely tax-driven Operations and Arrangements that involve no substantial activities

Where a preferential regime has been found to be actually harmful, the relevant country is given the opportunity to abolish the regime or remove the features that create the harmful effect. Other counties may take defensive measures to counter the effects of the harmful regime, while at the same time continuing to encourage the country applying the regime to modify or remove it.

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

22

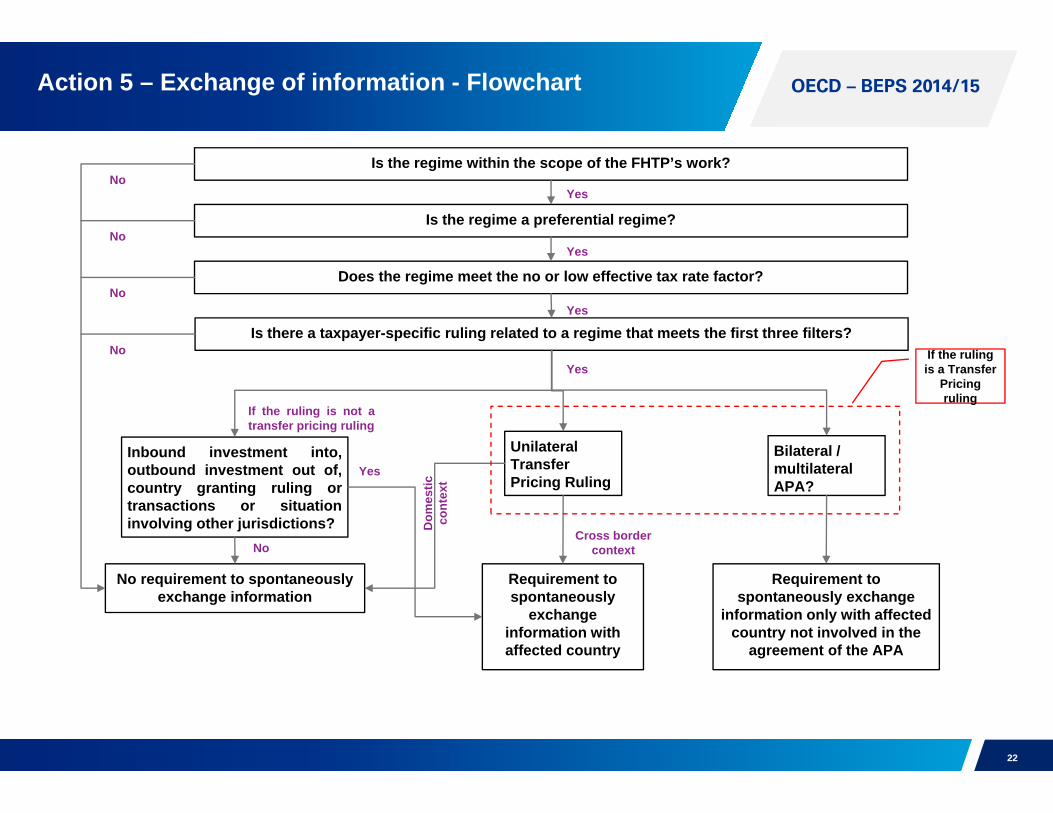

OECD – BEPS 2014/15Action 5 – Exchange of information - Flowchart

Is the regime within the scope of the FHTP’s work?

Is the regime a preferential regime?

Does the regime meet the no or low effective tax rate factor?

Is there a taxpayer-specific ruling related to a regime that meets the first three filters?

Inbound investment into,outbound investment out of,country granting ruling ortransactions or situationinvolving other jurisdictions?

UnilateralTransferPricing Ruling

Bilateral / multilateral APA?

No requirement to spontaneously exchange information

Requirement to spontaneously

exchange information with affected country

Requirement to spontaneously exchange

information only with affected country not involved in the

agreement of the APA

No

No

No

No

No

Yes

Yes

Yes

Yes

Yes

If the ruling is not atransfer pricing ruling

If the ruling is a Transfer

Pricing ruling

Dom

estic

co

ntex

t

Cross border context

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

23

OECD – BEPS 2014/15

Action 6:

Preventing Grant of Tax Treaty Benefits in inappropriate circumstances

Action 6:

Preventing Grant of Tax Treaty Benefits in inappropriate circumstances

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

24

OECD – BEPS 2014/15What is “Tax Treaty Abuse”?

• Term “abuse” in the context of tax treaty has not been defined in the Model Tax Conventions (OECD or UN)

• Paragraph 9.5 of the Commentary on Article 1 (OECD Model Convention 2010 update) :

• main purpose of entering into the transaction was to secure a more favorable tax position; and

• obtaining that more favorable treatment in given facts would be contrary to the object and purpose of

the relevant provisions of the tax treaty

• Instances of tax treaty abuse:

• Treaty shopping

• Conduit arrangements

• Acquiring residency of a specific country

• Attributing profits or income to a specific entity

• Changing the character of an income; etc.

• Treaty abuse, and in particular treaty shopping, identified as one of the most important sources of

BEPS concerns

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

25

OECD – BEPS 2014/15Action 6 – BEPS Action Plan

Objective – To modify rules to more closely align the allocation of income with the economic activity that

generates the income

Draft Report Published – Final Version Expected in September 2015

Section A Section B Section C

• Develop model treaty

provisions

• Recommend design of

domestic rules

• Clarify that tax treaties are not

intended to generate double

non-taxation

• Identify Policy Considerations

for Countries to consider while

entering into tax treaties

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

26

OECD – BEPS 2014/15

Action 15:

Develop Multilateral Instrument to modify Bilateral Tax Treaties

Action 15:

Develop Multilateral Instrument to modify Bilateral Tax Treaties

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

27

OECD – BEPS 2014/15Multilateral instrument to modify Bilateral Tax Treaties

Need to address current bilateral tax treaty system which facilitates BEPS

• Updation of the current tax treaty network highly burdensome due to multiple number of bilateral treaties

Focus on feasibility of use of a multilateral instrument to implement BEPS measures and modify bilateral tax treaties

• Multilateral instrument feasible and desirable based on precedents from various areas other than tax

Convening an International Conference to develop the multilateral instrument by OECD and G20 countries

BEPS – Action plans –Transfer Pricing

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

29

OECD – BEPS 2014/15

Action 8

Transfer Pricing Aspects of Intangibles

Action 8

Transfer Pricing Aspects of Intangibles

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

30

OECD – BEPS 2014/15Transfer Pricing aspects of Intangibles

• Objective • Prevent BEPS that may result from abuse of

TP rules related to cross-border relocation of intangibles and other transactions involving use of intangibles

• Assure that transfer pricing outcomes are in line with 'Value Creation”

To be finalised in 2015 along with other BEPS action points that are closely related (risks and capital, high-risk transactions and hard to value

intangibles)

Key areas covered in the Guidance

• Detailed guidance on location savings, assembled workforce and MNE group synergies as part of Chapter I of OECD guidelines

• Broader definition of intangible property (six specific categories of intangibles discussed)

• Ownership of intangibles and entitlement to returns –who is entitled to returns from intangibles

• Relevant considerations for various transactions involving intangibles

• Supplementary guidance around determining arm’s length conditions involving intangibles – considers unique features of intangible transactions

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

31

OECD – BEPS 2014/15

Extent of Intangible Related Returns to be attributed

Purchasing Function

Controlling Function

Funding Function

Performing Function

Transfer Pricing aspects of Intangibles…cont’d.

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

32

OECD – BEPS 2014/15

Who is entitled to return from intangibles?

• Legal ownership and Contractual Arrangements to be only the starting point for analysis

• Next steps, more importantly focus on thorough analysis of FAR and actual conduct of the various entities

- Who are the parties performing and controlling the functions related to the development, enhancement, maintenance, protection and exploitation of intangibles?

- Who is contributing the assets, including intangibles, physical assets and funding? Only funding without assumption of other risks entitles to only return on funding, not the entire intangible related returns

- Confirm the consistency between conduct of the parties and the legal arrangements

- Recharacterise the transactions as necessary to reflect each party’s contributions towards the intangibles

Legal ownership by itself is not sufficient to decide the allocation of returns

Supplementary guidance on arm’s length price

• Options realistically available to each of the parties to the transactions

• Consideration of the unique features of intangibles (viz. exclusivity, extent and duration of legal protection, useful life, stage of development etc.)

• Comparable Uncontrolled Price (CUP) and the Profit Split Method are likely to be most useful

• Other Valuation techniques may also be useful (like income and discounted cash flow techniques)

• Rule of thumb should not be used

• Guidance does not provide a comprehensive summary of valuation techniques available nor does it endorse or reject any valuation standards utilized by valuation professionals

Transfer Pricing aspects of intangibles…cont’d.

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

33

OECD – BEPS 2014/15India Perspective

• Location savings – Even where local comparables are available, specific adjustment on account of location savings are required – view of Indian Revenue Authorities (IRA)

• Marketing intangibles – Marketer / distributor should be compensated for enhancing the value of trademarks and other marketing intangibles

• R&D arrangements – appropriate compensation for research services will depend on all the facts and circumstances (whether research team possesses unique skills and experience, bears risks, uses its own intangibles etc.)

What needs to be done : Companies operating in India need to analyze:-

• Legal ownership and contractual arrangements vis-à-vis intangibles to begin with

• As next steps more importantly focus has to be on thorough analysis of FAR and actual conduct of the various entities

Various issues included in the Guidance are contemporary, highly debated, and frequently litigated TP issues in India - Indian tax authorities are likely to draw inference and support from OECD guidelines in determining the return from intangibles

Even before the introduction of the BEPS action plan the IRA authorities issued Circular no. 6 which discusses circumstances in which PSM will apply for determination of compensation in case of R&D centers developing intangibles. India also adopts the ‘Significant Peoples Function’ as a criteria in allocation of profits relating to intangibles which is in line with OECDs guidance

Supreme Court to now decide on AMP expense – whether an international transaction. But AMP activity being closely linked to overall marketing and distribution, can be benchmarked on an aggregate basis.

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

34

OECD – BEPS 2014/15

Action 10

Intra-group services –Discussion Draft

Action 10

Intra-group services –Discussion Draft

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

35

OECD – BEPS 2014/15Intra-group services – Discussion Draft

Key Areas Covered

• Determine whether intra-group services have been actually rendered. Focus areas –Benefits Test, Shareholder activities, Duplicative services and Agency services

• Determination of arm’s length price – Direct charge methods vs. Indirect charge methods

• What constitute LVIGS?

• Clarifying the meaning of shareholder activities and duplicative costs

• Guidance on mark-ups, appropriate cost allocation methodologies, benefits test and required documentation

Objective

• Focus on developing rules to prevent BEPS through the use of transactions (management fees, head office expenses etc) which would not, or would only very rarely, occur between independent parties

• Revision of Chapter VII of the OECD guidelines related to Intra-Group Services (IGS)

• Simplified approach suggested to deal with “Low Value-adding Intra-Group Services (LVIGS)” – New section D proposed to be added to Chapter VII

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

36

OECD – BEPS 2014/15Low Value-adding Intra-Group Services – LVIGS

Definition

• Services of supportive nature and not a part of core business of the Group

• Do not require the use of or lead to the creation of valuable and unique intangibles

• No assumption, control or creation of substantial or significant risk

• Understand the nature of the services in order to classify them as LVIGS. LVIGS - Supportive in nature andnot forming part of the core business of the MNE group.

Following activities - likely to meet the definition of LVIGS Following activities - not LVIGS

Accounting and auditing Services relating to the core business of the Group

Processing and management of account receivable and account payable

R & D , manufacturing and production services

Human resource related activities Sales, marketing and distribution activities

Monitoring and compilation of data relating to – health, safety, environment etc

Financial transactions

Information technology services Insurance and reinsurance

Internal and external communication and public support services

Extraction, exploration or processing of natural resources

Legal services / activities relating to tax obligations / generalservices of administrative or clerical nature

Services of corporate senior management

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

37

OECD – BEPS 2014/15Intra-group services – LVIGS

37

Satisfaction of a simplified benefits tests :

Onerous requirements of the “benefits tests” for LVIGS dispensed with. Simplified documentationand reporting requirements should satisfy the conditions of “benefits tests” for LVIGS

Only one member of the MNE group electing for application of simplified method required tomaintain simplified documentation

All tax administrations should generally accept the charges on account of such LVIGS, withoutrequiring each entity taxpayers to bear the onerous burden of justifying the “benefits tests” for suchservices through extensive documentation.

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

38

OECD – BEPS 2014/15India Perspective

38

• Draft guidelines will enable the taxpayers and tax administrations to focus their resources onhigh risk transactions while they can adopt a standard norm for routine LVIGS

• For a Captive Shared Service center, certain points such as nature of services outlined as ‘low value-adding’, manner of classifying core and non-core business activities, and proposed mark-up in the range in 2 per cent to 5 per cent etc. may be challenged by IRA

• MNCs need to take cognizance while planning the cross charge for services which might be routine i.e. low-value adding or high end.

• Adoption of simplified approach for LVIGS may be advantageous for both the taxpayers and tax administrations, as it not only reduces the compliance burden of the taxpayers but also reduces disputes between taxpayers and tax administration.

For Outbound IGS, it remains to be seen how India will adopt the above Guidance, once implemented given the fact that IRA has been claiming much higher markups compared to the recommended range of 2 to 5 percent for certain low end services

For Inbound IGS, it would be interesting to see how India adopts above Guidance, in light of the fact that IRA has been adopting aggressive approach in proposing adjustments and seeking voluminous documentation for such services

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

39

OECD – BEPS 2014/15

Action 13

Transfer Pricing Documentation and Country-by-Country (CbyC) reporting

Action 13

Transfer Pricing Documentation and Country-by-Country (CbyC) reporting

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

40

OECD – BEPS 2014/15Guidance on TP Documentation and CbyC ReportingBackground

● Objective: Risk Assessment● Approach: Provides an overview of the multinational group

and businessMaster file

● Objective: Appropriate considerations in setting transfer prices

● Approach: Provides additional detail on the operations and transactions relevant to that jurisdiction

Local file

● Objective: Prioritize Audit Issues● Approach: Provides summary data by jurisdiction including

revenue, income, taxes, and indicators of economic activityCbyC reporting

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

41

OECD – BEPS 2014/15

• To provide the MNE’s blueprint– The group’s organisational structure – Description of Group's business, intangibles, intercompany financial activities, financial and tax positions

Master file

• To provide jurisdiction-wise information on global allocation of income, taxes paid / accrued, the stated capital, accumulated earnings, number of employees and tangible assets

• Entity-wise details of main business activities which will portray the value chain of inter-company transactions.

Country by Country (‘CbyC’) Report

Local file

• To provide material transfer pricing positions of the local entity / taxpayer with its foreign affiliates – Demonstrates arm’s length nature of transactions– Contains the comparable analysis.

Three-tier documentation structure proposed for all countries

TP documentation and CbyC reporting

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

42

OECD – BEPS 2014/15

CbyC Template –Page 1*

Country

Revenue

Profit(loss) before income

tax

Income tax paid

(on a cash basis)

Income tax

accrued –current

year

Stated capital

and accumulat

ed earnings

Number of employee

s

Tangible assets

other tan cash and

cash equivalent

sRelated

partyUnrelated

party Total

Country A X X X X X X X X X

Country B X X X X X X X X X

CbyC Template –Page 2* (onwards)Activities

Country

Constituent entities resident in

country

Country of organisation or incorporation

in different from country of

residence R&

D

Pur

chas

ing

&

proc

urem

ent

Man

ufac

turin

g &

pro

duct

ion

Sal

es,

mar

ketin

g &

di

strib

utio

nA

dmin

istra

tive,

m

anag

emen

t &

supp

ort

serv

ices

Ext

erna

l se

rvic

e bu

sine

ssR

egul

ated

fin

anci

al

serv

ices

Insu

ranc

e

Hol

ding

co

mpa

ny

Dor

man

t

Oth

er

Country A Entity A Country B

Entity B

*Information obtained from annexure III to chapter V of OECD/G20 base erosion and profit shiftingProject: Guidance on transfer pricing documentation and Country-by-Country reporting

Country-by-Country Reporting Template

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

43

OECD – BEPS 2014/15Implementation Guidelines on CbyC Template

February 6, 2015 – Key Elements - OECD published Guidance on the implementation of CbyC:

● Consolidated group revenue in the preceding fiscal year of 750 million Euros (INR 5,250 crore) or moreWhich MNEs covered?

● For the fiscal years beginning on or after January 1, 2016 ● MNEs allowed 1 year from the fiscal year end to file the CbyC report

Timing

● File CbyC report in the country of the ultimate parent of the MNE ● That country will exchange this information on an automatic basis with

jurisdictions in which the MNE operates and that meet the necessary conditions described in guidance.

Where filed and mechanisms for exchange

● Confidentiality, Consistency and Appropriate Use Necessary Conditions for Obtaining and Using CbyC Reports

● Key elements of statutory legislation ● Agreements based on existing international agreements for the

automatic exchange of the CbyC reports between jurisdictions (both bilateral and multilateral)

Implementation Package

● Primary mechanism – Automatic Exchange from MNE parent country● Secondary mechanism – MNE file the CbyC report locally or with next

tier parent country that would automatically exchange

Government-to-Government Mechanisms for Exchange of CbyCReports

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

44

OECD – BEPS 2014/15India Perspective

Necessary to highlight / action to be taken by the Company management / Audit Committee -implications and meeting the objective of Transparency of BEPS Project very important

* Minutes of Tax officers offsite organized by Ministry of Finance and CII’s presentation at the meeting on 25 November 2014

Key Considerations:• Mechanism for sharing information with tax administrations through Automatic Exchange of Information

under tax treaties• Taxpayers concerns about sharing business sensitive data and increasing compliance cost and burden• CbyC report ought not be used by tax administrations to propose TP adjustments based on a global

formulary apportionment of income• However CbyC report would entitle the tax authorities to make further inquiries into the MNEs cross-border

transactions

What needs to be done

• Companies operating in India especially Indian headquartered companies need to tie up the functional analysis of Indian operations vis-à-vis global operations

• Have Management discussions to re-align functions and pricing to ensure that profits/income are allocated in accordance with value creation in each jurisdiction

• Should analyse their internal accounting systems and MIS data, and upgrade the same to enable gathering of information required in Master File and CbyC report

Indian Competent Authority commented* – Indian Government expects that companies should provide information relating to CbyC reporting starting from FY 2016-2017

© 2012 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

45

OECD – BEPS 2014/15Key Don’ts-- 2 of 2

ADI India

• Avoid using ‘Sales Manager’ or ‘Sales’ in the designation of ADI India employees, instead evaluateusing the term ‘Marketing Support Head / Manager’ in their designations.

• Emails, website, marketing brochure, advertisements, events, related documents etc. toappropriately reflect the above aspects and India arrangements.

• There should not be any reporting by the Indian employees to any other personnel of ADI Australia.

• Commercial invoice / debit notes etc. should not be signed by the same personnel who are on theBOD of ADI India.

Thank you

Hitesh D. GajariaChartered AccountantMobile: +91 9892333375