Embed Size (px)

Citation preview

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Direct TaxUnion Budget 2015-16

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Let us see what Mr. Robinhood has for us........

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Mr. Jaitley is confused as to what should be done ……..Let us help him as his secretary has just left him..

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Lets begin with.........

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Increase in rates of Surcharges

Assessee Existing New

All persons except a Company

@ _____ if Income exceeds Rs. 1 Crore

@ __% if Incomeexceeds Rs. 1 Crore

Domestic Company

Income Rs. 1 Crore-Rs.10 Crores – 5%Income exceeding Rs. 10 Crores – 10%

Income Rs. 1 Crore-Rs.10 Crores – 7%Income exceeding Rs. 10 Crores – 12%

Foreign Companies

Income Rs. 1-Rs.10 Crores –2%Income exceeding Rs. 10 Crores – 5%

________________

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

And the answer is........

Assessee Existing New

All persons except a Company

@ 10% if Income exceeds Rs. 1 Crore

@ 12% if Incomeexceeds Rs. 1 Crore

Domestic Company

Income Rs. 1 Crore-Rs.10 Crores – 5%Income exceeding Rs. 10 Crores – 10%

Income Rs. 1 Crore-Rs.10 Crores – 7%Income exceeding Rs. 10 Crores – 12%

Foreign Companies

Income Rs. 1-Rs.10 Crores –2%Income exceeding Rs. 10 Crores – 5%

No change

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Increase in other Surcharges.......

Increase in surcharge from _______ to 12% tax on distribution of dividends and buyback of shares, or by mutual funds and securitisation trusts on distribution of income.

Education Cess and higher education cess is proposed to be continued for F.Y. 2015-16 for all taxpayers.

Correspondingly the __________ has been abolished

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Its answer time..........

Increase in surcharge from 10 to 12% tax on distribution of dividends and buyback of shares, or by mutual funds and securitisation trusts on distribution of income.

Education Cess and higher education cess is proposed to be continued for F.Y. 2015-16 for all taxpayers.

Correspondingly the wealth tax has been abolished

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Let us talk about the need of Increasing surcharges….

Simplification strategy in place of whole new levy

Tool to curb Inflation

Attempt to improve financial gap between rich and middle sections of society.

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

To reduce the tax rate from ________ over the next ____ years but NOT from budget year

Corporate Tax rates..........

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Corporate Tax rates..........

To reduce the tax rate from 30% to 25% over the next 4 years but NOT from budget year

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Extension of benefits......

Transport allowance increased to Rs. ____ pm

Sukanya Samriddhi Scheme -

Investment eligible for deduction u/s ____

Interest received will be exempt

Withdrawls ______be liable to tax (w.e.f.01/04/2015)

Section 80D deduction limit increased

• From ` 15000 to ______

• From ` 20000 to ` 30000

• Deduction for incurred for treatment of ________________

allowed as deduction upto ` 30000.

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Benefits......

Transport allowance increased to Rs. 1600 pm

Sukanya Samriddhi Scheme -

Investment eligible for deduction u/s 80C

Interest received will be exempt

Withdrawls shall not be liable to tax (w.e.f.01/04/2015)

Section 80D deduction limit increased

• From ` 15000 to 25000

• From ` 20000 to ` 30000

• Deduction for incurred for treatment of very senior citizens

allowed as deduction upto ` 30000.

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Deduction limit u/s 80DDB (Medical expense on treatment of specified decease) -

• Limit for very senior citizens raised from _______ to ________

• Changes in Conditions –

• Prescription to be obtained from specialist doctor instead of certificate from Government Hospital

Deduction limit u/s 80DD – (Medical treatment or payments to LIC / insurer under a scheme for dependent) and 80U (Self deduction for disability) –

• Disability deduction increased – From ` 50,000 to 75,000

• Severe Disability deduction increased – From ` 1,00,000 to _________

Extension of benefits......

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Deduction limit u/s 80DDB (Medical expense on treatment of specified decease) -

• Limit for very senior citizens raised from `60,000 to`80,000

• Changes in Conditions –

• Prescription to be obtained from specialist doctor instead of certificate from Government Hospital

Deduction limit u/s 80DD – (Medical treatment or payments to LIC / insurer under a scheme for dependent) and 80U (Self deduction for disability) –

• Disability deduction increased – From ` 50,000 to 75,000

• Severe Disability deduction increased – From ` 1,00,000 to 1,25,000

Deductions...

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Deduction limit u/s 80CCC (Contribution to Pension Fund for self-employed)-

• Limit raised From _________ to 1,50,000

Deduction u/s 80CCD (Contribution to Pension schemefor employees) –

• New subsection 80CCD(1B) inserted • Additional deduction upto ` 50,000 over and above u/s

80CCD(1) allowed • 80CCD(1A) omitted -Threshold limit of ___________ removed

Furnishing of Form _________ for non deduction of TDS frompayments receivable under Life insurance policies, not covered by Section 10 (10D) (Payments received from any Insurance policies)( w.e.f. 01/06/2015)

Extension of benefits......

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Deduction limit u/s 80CCC (Contribution to Pension Fund for self-employed)-

• Limit raised From ` 1,00,000 to 1,50,000

Deduction u/s 80CCD (Contribution to Pension scheme for employees) –

• New subsection 80CCD(1B) inserted • Additional deduction upto ` 50,000 over and above u/s

80CCD(1) allowed • 80CCD(1A) omitted -Threshold limit of ` 1,00,000 removed

Furnishing of Form 15G / 15H for non deduction of TDS frompayments receivable under Life insurance policies, not covered by Section 10 (10D) (Payments received from any Insurance policies)( w.e.f. 01/06/2015)

Here comes the answer......

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

What could be the logic behind increasing deductions ?

For boosting investment habits

As a tool to curb inflation

Tool to neutralize effect of increasing Medical cost

Motivate people for retirement planning

Lower the tax burden on middle and upper middle sections

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Extension of benefits........

More funds included in 100% bracket for donations u/s _____ –

• National Fund for Control of Drug Abuse

• Swachh Bharat Kosh - w.r.e.f from 01-04-2015

• Clean Ganga Fund - w.r.e.f from 01-04-2015

• Deduction NOT available if Donations to Swachh Bharat

Kosh & Clean Ganga Fund considered as a part of _______ Activities

u/s 135 of Companies Act 2013

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

And the Answer is.............

More funds included in 100% bracket for donations u/s 80G –

• National Fund for Control of Drug Abuse

• Swachh Bharat Kosh - w.r.e.f from 01-04-2015

• Clean Ganga Fund - w.r.e.f from 01-04-2015

• Deduction NOT available if Donations to Swachh Bharat

Kosh & Clean Ganga Fund considered as a part of CSR Activities

u/s 135 of Companies Act 2013

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

To promote ‘Make in India’

Deduction u/s _______ (For employment of new

workmen) –

Benefit to ALL ASSESSEES instead of Corporate Assessee only.

Minimum no. of workmen to be employed reduced to 50

instead of _____.

Extension of benefits........

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

To promote ‘Make in India’

Deduction u/s 80JJAA (For employment of new

workmen) –

Benefit to ALL ASSESSEES instead of Corporate Assessee only.

Minimum no. of workmen to be employed reduced to 50

instead of 100.

Check your answers........

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Section 10 exemptions

(Section 10(23C) – Trust exemption)

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Section 10 exemptions

(Section 10(23C) – Trust exemption)

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

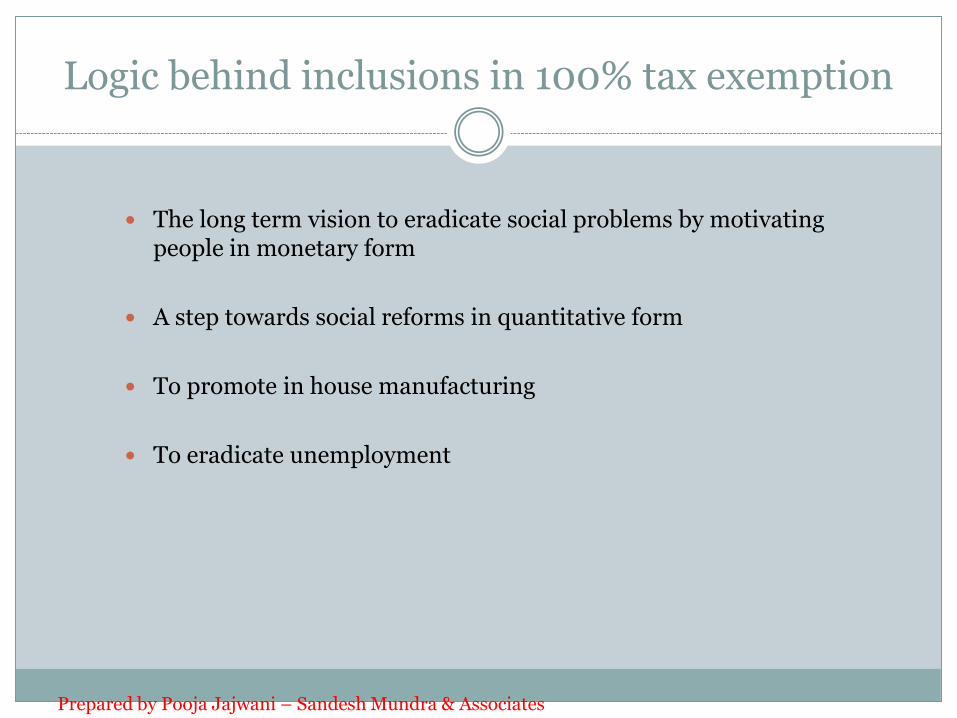

Logic behind inclusions in 100% tax exemption

The long term vision to eradicate social problems by motivating people in monetary form

A step towards social reforms in quantitative form

To promote in house manufacturing

To eradicate unemployment

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Waah waah..........

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Lets talk about.......

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

TDS and TCS provisions.....

Amendment in Section 194A

Expressed that TDS not applicable to interest payment by co-operative society to its members but Applicable to _________ Banks (w.e.f. 1/06/2015).

Interest on Recurring deposit is ___________

Extension of concessional rate of TDS u/s 194LD (Concessional TDS rates to NRI’s on specific bonds) –

Concessional rate of ___, on interest to FIIs / QFIs, ex-tended till 30/06/2017.

( w.e.f. 01/06/2015 )

TDS u/s194I is not liable on rent paid to _________ on asset held by that trust

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Get ready for Answer.....

Amendment in Section 194A

Expressed that TDS not applicable to interest payment by co-operative society to its members but Applicable to cooperative Banks (w.e.f. 1/06/2015)

Interest on Recurring deposit is taxable

Extension of concessional rate of TDS u/s 194LD (Concessional TDS rates to NRI’s on specific bonds) –

Concessional rate of 5%, on interest to FIIs / QFIs, ex-tended till 30/06/2017.

( w.e.f. 01/06/2015 )

TDS u/s194I is not liable on rent paid to business trust on asset held by that trust

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Logic behind the said amendments

Clarification between the intention of TDS levy on co-operative banks and not on co-operative societies

Attracting inflow of funds from foreign investments

Extension of benefits for business trust

Attracting people to go for business trust concept

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

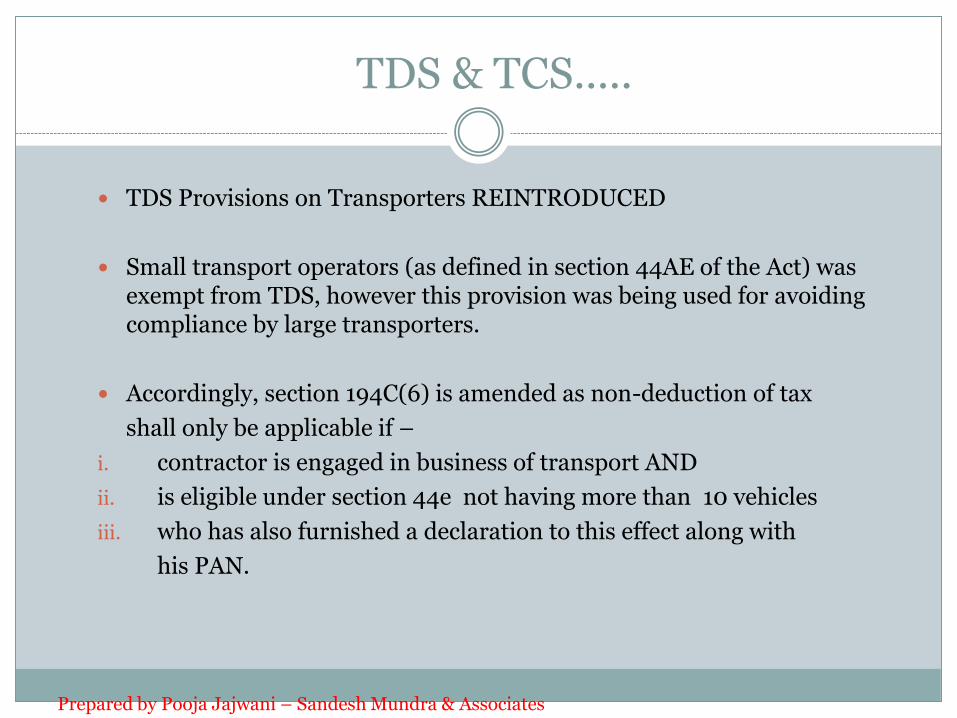

TDS Provisions on Transporters REINTRODUCED

Small transport operators (as defined in section _____ of the Act) was exempt from TDS, however this provision was being used for avoiding compliance by large transporters.

Accordingly, section 194C(6) is amended as non-deduction of tax

shall only be applicable if –

i. contractor is engaged in business of transport AND

ii. is eligible under section _________ not having more than ____ vehicles

iii. who has also furnished a declaration to this effect along with

his PAN.

TDS and TCS provisions.....

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

TDS Provisions on Transporters REINTRODUCED

Small transport operators (as defined in section 44AE of the Act) was exempt from TDS, however this provision was being used for avoiding compliance by large transporters.

Accordingly, section 194C(6) is amended as non-deduction of tax

shall only be applicable if –

i. contractor is engaged in business of transport AND

ii. is eligible under section 44e not having more than 10 vehicles

iii. who has also furnished a declaration to this effect along with

his PAN.

TDS & TCS.....

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Logic behind the above amendment

Large transporters were evading from there responsibilities and to curb this tendency govt. has expressly redefined the intention of provision

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Amendment in TCS Provisions

TCS returns will NOW be processed in the same manner as in case of _________ – Section 206CB Inserted;

Section 234E fee to be levied for delay in filing TCS statement –Section 206CB inserted

(w.e.f. 01/06/2015)

Branch of ____________ is treated as separate entity for TDS provisions.

TDS and TCS provisions.....

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Amendment in TCS Provisions

TCS returns will NOW be processed in the same manner as in case of TDS returns – Section 206CB Inserted;

Section 234E fee to be levied for delay in filing TCS statement –Section 206CB inserted

(w.e.f. 01/06/2015)

Branch of foreign banking company is treated as separate entity for TDS provisions.

Result time..........

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

And The Reason behind the change is…..

To ease compliance process

To curb the tendency of banking companies evading from TDS liability by tax planning

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Amendments in Minimum Alternate Tax Regime

Amendments in Minimum Alternate Tax Regime

Section 115JB (MAT on company) is amended and the share of income of an Assessee on which no tax is payable u/s 86 (Income received from AOP) is exempt.

Capital Gains of FII to be excluded from Book Profit:

Capital Gain on securities, (other than STCL on which STT is not chargeable), to Foreign Institutional Investor is exempt u/s 115JB

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Intention of statue behind this change is…..

Removing cascading effect of taxability of AOP share of profit in the hands of company opting for MAT

Removing double taxation of Capital gain in form of STT and Income tax

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Let us move on to.........

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Amendment in scheme of settlement commission......

Change in definition of ‘Case’ –

• If a notice u/s 148 is issued for any AY assesseee can approach Settlement Commission for other AY even if notice under has not been issued.

However, filing of return of income for such other assessment years is mandatory.

Criteria for commencement of proceedings changed in respect of cases other than 153A, 153C, 148, 254, 263 & 264:-

In existing position of law, the proceedings for any assessment years for a case other than 153A, 153C, 148, 254, 263 & 264 were deemed to be commenced from the 1st day of the AY.

Now the same is changed from the date of furnishing of return

(w.e.f 01/06/2015.)

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Let us talk about the logic behind the change…

Before change, Assessee becomes eligible to approach Settlement Commission only for the AY. for which notice is issued. If similar issue involved in other AY, assessee didn’t had any option. Therefore, the change was required.

To reduce the interest amount levied on people by reducing the time lag

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Seized assets u/s 132B allowed to be appropriated against the liability arising on application to the Settlement Commission u/s 245C (Payment of additional tax by Settlement commission) only.

(w.e.f 01/06/2015.)

To amend section 245K , any person related to the person who has already approached the Settlement Commission once, also cannot approach the Settlement Commission subsequently.

Amendment in scheme of settlement commission......

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Logic behind the change…

To make provision more stringent by not allowing appropriation of sized property to actual tax liability but to additional liability of Settlement Commission

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

• The related person with respect to a person means –

(i) In case of individual - any company, firm or AOP or BOI in which such person has more than 50% interest, or any HUF in which he is a karta;

(ii) In case of a company, any individual who held more than 50% of the shares

(iii) In case of a firm or AOP or BOI, any individual who has more than 50% share

(iv) In case of a HUF, the karta of that HUF.

Extra period of six months provided in case of an application made by department before settlement commission for rectification.

Amendment in scheme of settlement commission......

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Period for charging interest u/s 234B has been increased for Proceedings before settlement commission

( w.e.f. 1st day of June 2015)

Amendment in scheme of settlement commission......

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Let us look at Intention of Statue…..

To make interest provisions more stringent by increasing interest amount by extending interest period

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Let us talk about........

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Penal provisions.........

Non-filling or inadequate filing to have rigorous punishment upto 7 years.

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Let us talk about Logic behind change……

No penalty on adequate and effective disclosure resulting disclosure of inadequate or hiding of information from department hence govt. has introduced penal provisions for the same.

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Quiz Awaited - International Taxation.......

Amendment in criteria of Residential Status for a company -

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Wish u the best for answer......

Amendment in criteria of Residential Status for a company -

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

And the logic behind such change is……

To expand the base of income taxable in India govt. has increased the instance of income being taxed in India

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Moving on to another Quiz - Instance of Taxability clarified...

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

And the answer is......

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Intention of statue is……

To motivate Business Outsource Operations from India Govt. has reduced instances of taxability in India

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Next Quiz is - Clarity in Indirect transfer and International taxes provisions...

Asset or capital asset, being any share or interest in a company or entity registered or incorporated _________ India deemed to be situated in India if share or interest derives, directly or indirectly, its value substantially from the assets located in India.

Empower CBDT to notify rules for giving foreign tax credit

Tax rate on royalty and fees for technical services as per Section 115a (Chart for tax treaties) reduced from ______ to 10%

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Check out the answer.....

Asset or capital asset, being any share or interest in a company or entity registered or incorporated outside India deemed to be situated in India if share or interest derives, directly or indirectly, its value substantially from the assets located in India.

Empower CBDT to notify rules for giving foreign tax credit

Tax rate on royalty and fees for technical services as per Section 115a (Chart for tax treaties) reduced from 25% to 10%

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Intention on Statue……….

From reducing taxes govt. has enhanced benefit to BPO units

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Lets discuss amendments related to....

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Next Quiz is -

‘Holding _________ is mandatory to represent

Now only those chartered accountants ____________

are eligible –

(i) To represent before the Income Tax department,

(ii) To provide certificates and reports where ever required

(iii) Eligible for appointment as an auditor

Person convicted by a court for fraud not eligible to act as authorised representative for a period of 10 years from the date of such conviction

(w.e.f. 01/06/2015)

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Reporting and certifications....

‘Holding COP is mandatory to represent

IF ineligible to carry audit of Company as per provisions of 2013 act -then CA

(i) Can represent before the Income Tax department,

(ii) Can-not provide certificates and reports where ever required

(iii) Can-not be Eligible for appointment as an auditor

Person convicted by a court for fraud not eligible to act as authorised representative for a period of 10 years from the date of such conviction

(w.e.f. 01/06/2015)

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

The logic behind the change…….

To improve the authenticity and reliability of reports and certificates produced to departments by CA

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Ointment to hurted brothers……..

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Another Quiz - Promote investment in AP and Telangana states

Investment allowance u/s 32AD (Manufacturing in backward areas) -

• Additional _____ depreciation on investments for manufacturing activity beginning from April, 2015 to March, 2020

• Over and above allowance u/s 32AC (Invest. In Plant and Machinery by corporate @ 15%)

Additional depreciation @ 35% u/s 32(1)(iia) (Additional 15% allowance in case of new manufacturing entity other than ships and aircraft)

Enhanced rate of additional depreciation @ ____ as against ____

for other states

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

And the answer is.......

Investment allowance u/s 32AD (Manufacturing in backward areas) -

• Additional 15% depreciation on investments for manufacturing activity beginning from April, 2015 to March, 2020

• Over and above allowance u/s 32AC (Invest. In Plant and Machinery by corporate @ 15%)

Additional depreciation @ 35% u/s 32(1)(iia) (Additional 15% allowance in case of new manufacturing entity other than ships and aircraft)

Enhanced rate of additional depreciation @ 35% as against 20% for other states

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Intention of Govt. is…..

Promoting capital expenditure on Plant and Machinery

Supporting Telangna and AP being self-dependent after separation

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Transfer pricing and Additional Depreciation…

Threshold limit for applicability of Domestic Transfer Pricing increased

Threshold limit u/s 92BA increased to ` 20 crores from ` 5 crores

Additional Depreciation in case of Assets used for Less Than 180 days u/s 32(1)(iia) (For Plant and Mach. Except to Aircraft and Ship)

50% of the Additional benefit i.e. 10% in purchase year; and

Remaining in immediate subsequent year

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Intention behind the change……

Increase the exemption limit and reducing the compliance requirements of small companies

To provide clarity in case of availing additional benefit where the asset is used for half-year.

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Charity and Social phases…..

Rationalization of definition of charitable purpose

If the aggregate receipts from activities, during the previous year, exceed 20% of the total receipts, of the trust, then same not considered as ‘charitable purpose’.

Emphasis to promote ‘Yoga’

‘Yoga’ considered as an activity of charitable purpose defined u/s 2(15)

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Assessments and Litigations…….

Single member bench of ITAT authorized to dispose of cases where total income assessed by AO is not more than ` 15 Lakhs (Earlier it was `1 Lakh). [Section 255(3)]

(w.e.f. 01/06/2015)

(w.e.f. 01/06/2015)

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Logic behind change……

To ease appeal disposing mechanism and disposing pending appeals

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Erroneous or prejudicial terms defined….

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

COA in Merger

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Let us move to Black Money conflict…

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

No person shall receive/repay loan, advance or deposit in cash for ______ or more

Penalty upto ____ and 10 years jail for black money evaders

Undisclosed income from foreign asset to be taxable at maximum rate.

PAN mandatory for transactions exceeding Rs. ______

Third party reporting entities required to furnish information of foreign currency sale and cross border transactions

Next Quiz - Provisions to curb Black Money

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

No person shall receive/repay loan, advance or deposit in cash for `20,000 or more

Penalty upto 300% and 10 years jail for black money evaders

Undisclosed income from foreign asset to be taxable at maximum rate.

PAN mandatory for transactions exceeding Rs. 1 lacs

Third party reporting entities required to furnish information of foreign currency sale and cross border transactions

And the answer is......

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

The intention of govt. is…….

To curb the tendency of people keeping undisclosed income by increasing penal provisions

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Awaited dream….GAAR

Deferment of General Anti Avoidance Rule (‘GAAR’)

• Proposed to make GAAR applicable from FY 2017-18

Prepared by Pooja Jajwani – Sandesh Mundra & Associates

Thank u.............