Embed Size (px)

Citation preview

HBR AT LARGE

Doesn'tMatter

by Nicholas C.Carr

As information technology's power and ubiquity have

grown, its strategic importance has diminished. The

way you approach IT investment and management will

need to change dramatically

I N 1968, ayoung Intel engineernamedTed Hoff found a way to put the cir-cuits necessary for computer process-

ing onto a tiny piece of silicon. His in-vention of the microprocessor spurred aseries of technological breakthroughs-desktop computers, local and wide areanetworks, enterprise software, and theInternet-that have transformed thebusiness world. Today, no one would dis-pute that information technology hasbecome the backbone of commerce. Itunderpins the operations of individualcompanies, ties together far-flung sup-ply chains, and, increasingly, links busi-nesses to the customers they serve.Hardly a dollar or a euro changes handsanymore without the aid of computersystems.

As IT'S power and presence have ex-panded, companies have come to view itas a resource ever more critical to their

success, a fact clearly reflected in theirspending habits. In 1965, according to astudy by the U.S. Department of Com-merce's Bureau of Economic Analysis,less than 5% of the capital expendituresof American companies went to infor-mation technology. After the introduc-tion of the persona] computer in theearly 1980s, that percentage rose to 15%.By the early 1990s, it had reached morethan 30%, and by the end of the decadeit had hit nearly 50%. Even with the re-cent sluggishness in technology spend-ing, businesses around the world con-tinue to spend well over $2 trillion ayear on IT.

But the veneration of IT goes muchdeeper than dollars. It is evident as wellin the shifting attitudes of top manag-ers. TXventy years ago, most executiveslooked down on computers as prole-tarian tools - glorified typewriters and

MAY 2003 41

HBR AT LARGE • IT Doesn't Matter

calculators-best relegated to low levelemployees like secretaries, analysts, andtechnicians. It was the rare executivewho would let his fingers touch a key-board, much less incorporate informa-tion technology into his strategic think-ing. Today, that has changed completely.Chief executives now routinely talkaboutthe strategic value of informationtechnology, about how they can use ITto gain a competitive edge, about the"digitization" of their business models.Most have appointed chief informationofficers to their senior managementteams, and many bave hired strategyconsulting firms to provide fresh ideason how to leverage their IT investmentsfor differentiation and advantage.

Behind the change in thinking lies asimple assumption: that as lT's potencyand ubiquity have increased, so too hasits strategic value. It's a reasonable as-sumption, even an intuitive one. But it'smistaken. What makes a resource trulystrategic - what gives it the capacity tobe the basis for a sustained competitiveadvantage-is not ubiquity but scarcity.You only gain an edge over rivals byhaving or doing something that theycan't bave or do. By now, tbe core func-tions of IT - data storage, data process-ing, and data transport - have becomeavailable and affordable to all.̂ Tbeirvery power and presence have begun totransform them from potentially strate-gic resources into commodity factors ofproduction. They are becoming costsof doing business that must be paid byall but provide distinction to none.

IT is best seen as the latest in a seriesof broadly adopted technologies thathave reshaped industry over the pasttwo centuries - from the steam engineand the railroad to the telegraph andthe telephone to the electric generatorand the internal combustion engine.Eor a brief period, as they were beingbuilt into the infrastructure of com-merce, all tbese technologies openedopportunities for forward-looking com-

panies to gain real advantages. But astbeir availability increased and theircost decreased-as they became ubiqui-tous-they became commodity inputs.From a strategic standpoint, they be-came invisible; they no longer mattered.Tbat is exactly what is happening to in-formation technology today, and theimplications for corporate IT manage-ment are profound.

Vanishing AdvantageMany commentators have drawn paral-lels between the expansion of IT, par-ticularly the Internet, and the rolloutsof earlier technologies. Most of thecomparisons, though, have focused oneither the investment pattern associ-ated with the technologies-the boom-to-bust cycle-or tbe tecbnologies' rolesin resbaping the operations of entire in-dustries or even economies. Little has

rights to a new packaging material thatgives its product a longer shelf life thancompeting brands. As long as they re-main protected, proprietary technolo-gies can be the foundations for long-term strategic advantages, enablingcompanies to reap higher profits thantbeir rivals.

InfrastiTJctural technologies, in con-trast, offer far more value when sharedthan when used in isolation. Imagineyourself in the early nineteenth century,and suppose that one manufacturingcompany held the rights to all the tech-nology required to create a railroad. If itwanted to, that company could justbuild proprietary lines between its sup-pliers, its factories, and its distributorsand run its own locomotives and railcarson tbe tracks. And it might well operatemore efficientiy as a result. But, for tbebroader economy, the value produced

When a resource becomes essential to competition but

inconsequential to strategy, the risks it creates become

more important than the advantages it provides.

been said about the way the technolo-gies influence, or fail to influence, com-petition at the firm level. Yet it is herethat history offers some of its most im-portant lessons to managers.

A distinction needs to be made be-tween proprietary technologies andwhat might be called infrastructuraltechnologies. Proprietary technologiescan be owned, actually or effectively,by a single company. A pbarmaceuticalfirm, for example, may hold a patent ona particular compound that serves asthe basis for a family of drugs. An in-dustrial manufacturer may discover aninnovative way to employ a processtechnology that competitors find hardto replicate. A company tbat producesconsumer goods may acquire exclusive

Nicholas G. Carr is HBR's editor-at-large. He edited The Digital Enterprise, a collec-tion of HBR articles published by Harvard Business School Press in 2001, and haswritten for the Einancial Times, Business 2.0, and the Industry Standard in additionto HBR. He can be reached at [email protected].

by such an arrangement would be triv-ial compared with the value that wouldhe produced by building an open railnetwork connecting many companiesand many buyers. The characteristicsand economics of infrastructural tech-nologies, whether railroads or telegraphlines or power generators, make it inev-itable tbat they will be broadly shared-that they will become part of the gen-eral business infrastructure.

In the earliest phases of its buildout,however, an infrastructural technologycan take the form of a proprietary tech-nology. As long as access to the technol-ogy is restricted-through physical lim-itations, intellectual property rights,high costs,or a lack of standards-a com-pany can use it to gain advantages overrivals. Consider the period between theconstruction of the first electric powerstations, around 1880, and the wiring ofthe electric grid early in the twentiethcentury. Electricity remained a scarce

42 HARVARD BUSINESS REVIEW

IT Doesn't Matter • HBR AT LARGE

resource during this time, and thosemanufacturers able to tap into it - by,for example, building their plants neargenerating stations - often gained animportant edge. It was no coincidencethat the largest U.S. manufacturer ofnuts and bolts at tbe turn of the century.Plumb, Burdict, and Barnard, located itsfactory near Niagara Falls in New York,the site of one of the earliest large-scalebydroelectiic power plants.

Companies can also steal a march ontheir competitors by baving superior in-sight into the use of a new technology.The introduction of electric power againprovides a good example. Until the endof the nineteenth century, most man-ufacturers relied on water pressure orsteam to operate their machinery. Powerin those days came from a single, fixedsource - a waterwheel at the side of amill, for instance-and required an elab-orate system of pulleys and gears todistribute it to individual workstationsthroughout the plant. When electricgenerators first became available, manymanufacturers simply adopted them asa replacement single-point source, usingthem to power the existing system ofpulleys and gears. Smart manufacturers,however, saw that one of the great ad-vantages of electiic power is that it is eas-ily distributable-tbat it can be broughtdirectly to workstations. By wiring tbeirplants and installing electric motors intiieir machines, they were able to dis-pense with tbe cumbersome, inflexible,and costly gearing systems, gaining animportant efficiency advantage overtheir slower-moving competitors.

In addition to enabling new, more ef-ficient operating metbods, infrastruc-tural technologies often lead to broadermarket changes. Here, too, a companythat sees what's coming can gain a stepon myopic rivals. In the mid-i8oos, wbenAmerica started to lay down rail lines inearnest, it was already possible to trans-port goods over long distances - bun-dreds of steamships plied the country'srivers. Businessmen probably assumedthat rail transport would essentially fol-low the steamship model, with some in-cremental enhancements. In fact, thegreater speed, capacity, and reach of

the railroads fundamentally changed thestructure of American industry. It sud-denly became economical to ship fin-ished products, rather than just rawmaterials and industrial components,over great distances, and the mass con-sumer market came into being. Compa-nies that were quick to recognize thebroader opportunity rushed to buildlarge-scale, mass-production factories.Tbe resulting economies of scale al-lowed them to crush the small, localplants that until tben had dominatedmanufacturing.

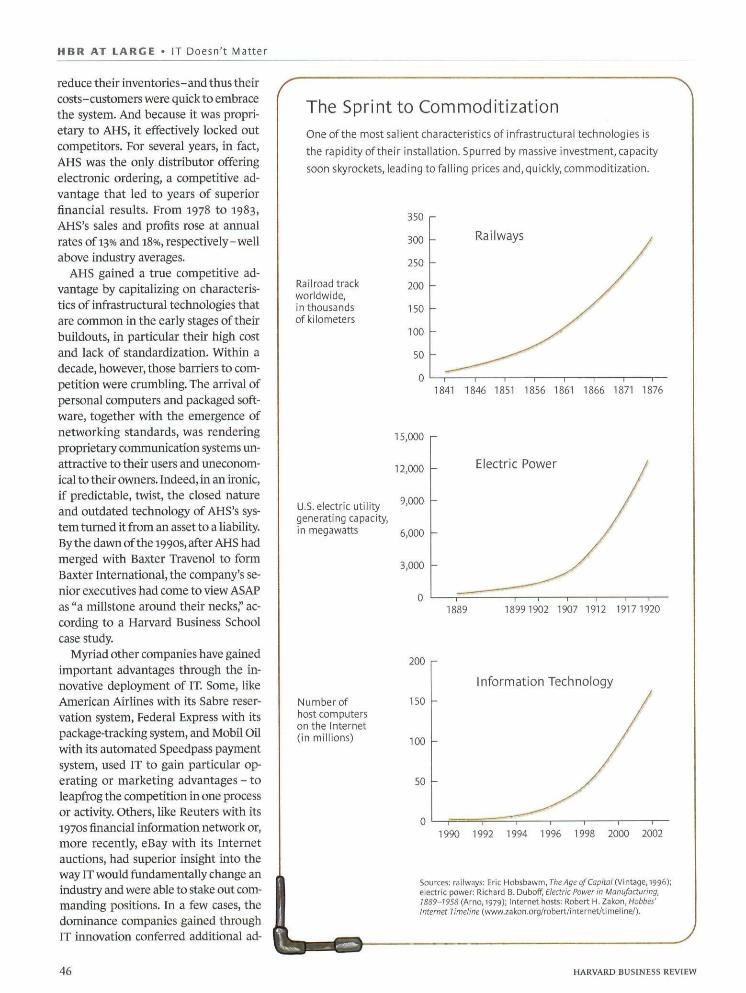

The trap tbat executives often fallinto, however, is assuming that oppor-tunities for advantage will be availableindefinitely. In actuality, the window forgaining advantage from an infrastruc-tural technology is open only briefly.Wben the technology's commercial po-tential begins to be broadly appreciated,huge amounts of cash are inevitably in-vested in it, and its buildout proceedswitb extreme speed. Railroad tracks,telegraph wires, power lines - all werelaid or strung in a frenzy of activity (afrenzy so intense in the case of rail linestbat it cost hundreds of laborers tbeirlives). In the 30 years between 1846 and1876, reports Eric Hobsbawm in TheAge of Capital, the world's total railtrackage increased from 17,424 kilome-ters to 309,641 kilometers. During tbissame period, total steamship tonnagealso exploded, from 139,973 to 3,293,072tons. The telegraph system spread evenmore swiftly. In Continental Europe,there were just 2,000 nules of telegraphwires in 1849; 20 years later, there were110,000, The pattern continued witbelectrical power. The number of centralstations operated by utilities grew from468 in 1889 to 4,364 in 1917, and the av-erage capacity of eacb increased morethan tenfold. (Eor a discussion of thedangers of overinvestment, see the side-bar "Too Mucb of a Good Thing.")

By tbe end of the buildout phase, tbeopportunities for individual advantageare largely gone. The rush to invest leadsto more competition, greater capacity,and falling prices, making the technol-ogy broadly accessible and affordable.At the same time, the buildout forces

MAY 2003

HBR AT LARGE • IT Doesn't Matter

users to adopt universal technical stan-dards, rendering proprietary systemsobsolete. Even the way tbe tecbnologyis used begins to become standardized,as best practices come to be widely un-derstood and emulated. Often, in fact,tbe best practices end up being builtinto the infrastructure itself; afrer elec-trification, for example, all new facto-ries were constructed witb many well-distributed power outlets. Both tbetechnology and its modes of use he-come, in effect, commoditized. The onlymeaningful advantage most companiescan hope to gain from an infrastructuraltecbnology after its buildout is a costadvantage - and even that tends to bevery hard to sustain.

That's not to say that infrastructuraltecbnologies don't continue to influ-ence competition. They do, but theirinfluence is felt at the macroeconomiclevel, not at the level of the individualccjmpany. If a particular country, for in-stance, lags in installing the technol-ogy - whether it's a national rail net-work, a power grid, or a communicationinfrastructure - its domestic industrieswill suffer heavily. Similarly, if an in-dustry lags in harnessing the power ofthe tecbnology, it will be vulnerable todisplacement. As always, a company'sfate is tied to broader forces affectingits region and its industry. The point is,however, that the technology's poten-tial for differentiating one companyfrom the pack-its strategic potential -inexorably declines as it becomes acces-sible and affordable to all.

The Commoditization of ITAlthough more complex and malleablethan its predecessors, IT has all the hall-marks of an infrastructural technology.In fact, its mix of characteristics guar-antees particularly rapid commoditi-zation . IT is, first of all, a transport mech-anism-it carries digital information justas railroads carry goods and power gridscarry electricity. And like any transportmechanism, it is far more valuable whenshared than when used in isolation. Thehistory of IT in business has been a his-tory of increased interconnectivity andinteroperability, from mainframe time-

Too Much of a Good ThingAs many experts have pointed out, the overinvestment in information

technology in the 1990s echoes the overinvestment in railroads in the

i86os. In both cases, companies and individuals, dazzled by the seem-

ingly unlimited commercial possibilities ofthe technologies, threw large

quantities of money away on half-baked businesses and products. Even

worse, the flood of capital led to enormous overcapacity, devastating

entire industries.

We can only hope that the analogy ends there. The mid-nineteenth-

century boom in railroads (and the closely related technologies ofthe

steam engine and the telegraph) helped produce notonly widespread

industrial overcapacity but a surge in productivity. The combination set

the stage for two solid decades of deflation. Although worldwide economic

production continued to grow strongly between the mid-i87osandthe

mid-i89os, prices collapsed - in England, tbe dominant economic power

oftbe time, price levels dropped 40%. In turn, business profits evaporated.

Companies watched the value of tbeir products erode while tbey were in

the very process of making them. As the first worldwide depression took

hold, economic malaise covered much ofthe globe. "Optimism about a

future of indefinite progress gave way to uncertainty and a sense of agony,"

wrote historian D.S. Landes.

It's a very different world today, of course, and it would be dangerous

to assume that history will repeat itself But with companies struggling to

boost profits and the entire world economy flirting with deflation, it would

also be dangerous to assume it can't.

sharing to minicomputer-based localarea networks to broader Ethernet net-works and on to the Internet. Each stagein that progression has involved greaterstandardization of the technology and,at least recently, greater homogeniza-tion of its functionality. Eor most busi-ness applications today, the benefits ofcustomization would be overwhelmedby tbe costs of isolation.

IT is also highly replicable. Indeed, itis hard to imagine a more perfect com-modity than a byte of data - endlesslyand perfectly reproducible at virtuallyno cost. The near-infinite scalability ofmany IT functions, when combinedwith technical standardization, doomsmO5t proprietary applications to eco-nomic obsolescence. Wby write yourown application for word processingor e-mail or, for that matter, supply-chain management when you can buya ready-made, state-of-the-art applica-

tion for a fraction of the cost? But it'snot just the software tbat is replicable.Because most business activities andprocesses have come to he embeddedin software, they become replicable, too.When companies buy a generic appli-cation, they buy a generic process aswell. Both the cost savings and the in-teroperability benefits make the sacri-fice of distinctiveness unavoidable.

The arrival of the Internet has accel-erated the commoditization of IT byproviding a perfect delivery channel forgeneric applications. More and more,companies will fulfill their IT require-ments simply by purchasing fee-based"Web services" from third parties -similar to the way they currently buyelectric power or telecommunicationsservices. Most of the major business-technology vendors, from Microsoft toIBM, are trying to position themselvesas IT utilities, companies that will con-

44 HARVARD BUSINESS REVIEW

IT Doesn't Matter • HBR AT LARGE

trol the provision of a diverse range ofbusiness applications over what is nowcalled, tellingly, "the grid." Again, theupshot is ever greater homogenizationof IT capabilities, as more companiesreplace customized applications withgeneric ones. (Eor more on the chal-lenges facing IT companies, see the side-bar "What About the Vendors?")

Finally, and for all tbe reasons alreadydiscussed, IT is subject to rapid price de-flation. Wben Gordon Moore made hisfamously prescient assertion that thedensity of circuits on a computer chipwould double every two years, he wasmailing a prediction about the comingexplosion in processing power. But hewas also making a prediction about thecoming free fall in the price of computerfunctionality. The cost of processingpower has dropped relentlessly, from$480 per million instructions per sec-ond (MIPS) in 1978 to $50 per MIPS in1985 to $4 per MIPS in 1995, a trend tbatcontinues unabated. Similar declineshave occurred in the cost of data storageand transmission. The rapidly increas-ing affordability of IT functionality hasnot only democratized the computerrevolution, it has destroyed one of themost important potential barriers tocompetitors. Even the most cutting-edge IT capabilities quickly becomeavailable to all.

It's no surprise, given these charac-teristics, that IT'S evolution has closelymirrored that of earlier infrastructuraltecbnologies. Its buildout has been everybit as breathtaking as tbat of the rail-roads (albeit with considerably fewerfatalities). Consider some statistics. Dur-ing the last quarter of the twentiethcentury, the computational power ofa microprocessor increased by a factorof 66,000. In the dozen years from 1989to 2001, the number of host computersconnected to the Internet grew from80,000 to more than 125 million. Overthe last ten years, the number of siteson the World Wide Web bas grownfrom zero to nearly 40 million. Andsince the 1980s, more than 280 millionmiles of fiber-optic cable bave been in-stalled - enough, as BusinessWeek re-cently noted, to "circle the earth 11,320

times." (See the exhibit "The Sprint toCommoditization.")

As with earlier infrastructural tecb-nologies, IT provided forward-lookingcompanies many opportunities for com-petitive advantage early in its buildout,when it could still be "owned"like a pro-prietary technology. A classic exampleis American Hospital Supply. A leadingdistributor of medical supplies, AHS

introduced in 1976 an innovative systemcalled Analytic Systems AutomatedPurcbasing, or ASAP, that enabled hos-pitals to order goods electronically. De-veloped in-house, the innovative systemused proprietary software running ona mainframe computer, and hospitalpurchasing agents accessed it throughterminals at their sites. Because moreefficient ordering enabled hospitals to

What About the Vendors?Just a few months ago, at the 2003 World Economic Forum in Davos,

Swiuerland, Bill Joy, the chief scientist and cofounder of Sun Micro-

systems, posed what for him must have been a painful question: "What

if the reality is that people have already bought most ofthe stuff they want

to own?" The people he was talking about are, of course, businesspeople,

and the stuffis information technology. With the end ofthe great buildout

ofthe commercial IT infrastructure apparently at hand Joy's question is

one that all IT vendors should be asking themselves. There is good reason

to believe that companies'existing IT capabilities are largely sufficient for

their needs and, hence, that the recent and widespread sluggishness in

IT demand is as much a structural as a cyclical phenomenon.

Even if that's true, the picture may not be as bleak as it seems for ven-

dors, at least those with the foresight and skill to adapt to the new environ-

ment. The importanceof infrastructural technologies to the day-to-day

operations of business means that they continue to absorb large amounts

of corporate cash long after they have become commodities-indefinitely,

in many cases. Virtually all companies today continue to spend heavily

on electricity and phone service, for example, and many manufacturers

continue to spend a lot on rail transport. Moreover, the standardized

natureof infrastructural technologies often leads to the establishment

of lucrative monopolies and oligopolies.

Many technology vendors are already repositioning themselves and

their products in response to the changes in the market. Microsoft's

push to turn its Office software suite from a packaged good into an annual

subscription service is a tacit acknowledgment that companies are losing

their need-and their appeti te-for constant upgrades. Dell has succeeded

by exploiting the commoditization ofthe PC market and is now extending

that strategy to servers, storage, and even services. (Michael Dell's essen-

tial genius has always been his unsentimental trust in the commoditiza-

tion of information technology.) And many ofthe major suppliers of

corporate IT, including Microsoft, IBM, Sun, and Oracle, are battling to

position themselves as dominant suppliers of "Web services" - to turn

themselves, in effect, into utilities. This war for scale, combined with the

continuing transformation of IT into a commodity, will lead to the further

consolidation of many sectors ofthe IT industry. The winners will do very

well; the losers will be gone.

MAY 2003 45

HBR AT LARGE • IT Doesn't Matter

reduce tbeir inventories-and thus theircosts-customers were quick to embracethe system. And because it was propri-etary to AHS, it effectively locked outcompetitors. Eor several years, in fact,AHS was tbe only distributor offeringelectronic ordering, a competitive ad-vantage that led to years of superiorfinancial results. Erom 1978 to 1983,AHS's sales and profits rose at annualrates of 13% and 18%, respectively-wellabove industry averages.

AHS gained a true competitive ad-vantage by capitalizing on cbaracteris-tics of infrastructural tecbnologies thatare common in tbe early stages of theirbuildouts, in particular their high costand lack of standardization. Within adecade, however, those barriers to com-petition were crumbling. The arrival ofpersonal computers and packaged soft-ware, together with the emergence ofnetworking standards, was renderingproprietary communication systems un-attractive to tbeir users and uneconom-ical to their owners. Indeed, in an ironic,if predictable, twist, tbe closed natureand outdated technology of AHS's sys-tem tumed it from an asset to a liabiiity.By the dawn oftbe 1990s, after AHS hadmerged with Baxter Travenol to formBaxter International, the company's se-nior executives had come to view ASAPas "a millstone around their necks," ac-cording to a Harvard Business Schoolcase study.

Myriad other companies bave gainedimportant advantages through the in-novative deployment of IT. Some, likeAmerican Airlines with its Sabre reser-vation system, Eederal Express with itspackage-tracking system, and Mobil Oilwith its automated Speedpass paymentsystem, used IT to gain particular op-erating or marketing advantages - toleapfrog the competition in one processor activity. Others, like Reuters with its1970S financial information network or,more recently, eBay with its Internetauctions, had superior insight into theway IT would fundamentally change anindustry and were able to stake out com-manding positions. In a few cases, thedominance companies gained throughIT innovation conferred additional ad-

The Sprint to CommoditizationOne ofthe most saiient characteristics of infrastructural technologies is

the rapidity of their installation. Spurred by massive investment, capacity

soon skyrockets, leading to falling prices and, quickly, commoditization.

Railv^ays

Railroad trackworldwide.in thousandsof kilometers

350

300

250

200

150

100

50

0

15,000

12,000

1841 1846 1851 1856 1861 1866 1871 1876

Electric Power

U.S. electric utilitygenerating capacity,in megawatts 6 000

3,000

0

200

1889 18991902 1907 1912 1917 1920

Number ofhost computerson the Internet(in millions)

150

100

Infornnation Technology

1990 1992 1994 1996 1998 2000 2002

Sources: railway;: Eric Hobsbawm, Tfte^lgeo/Copto/(Vintage, 1996);electric power; Richard B. Dubofij Electric Power in Manufacturing,1889-1958 {Amo,^97g); Internet hosts: Robert H.Zakon.Hodbei'Internet Timeline {www.zakon.org/robert/internet/timeline/).

HARVARD BUSINESS REVIEW

vantages, such as scale economies andbrand recognition, that have provedmore durable than tbe original techno-logical edge. Wal-Mart and E)ell Com-puter are renowned examples of firmsthat have been able to turn temporarytechnological advantages into enduringpositioning advantages.

But the opportunities for gaining IT-based advantages are already dwin-dling. Best practices are now quicklybuilt into software or otherwise repli-cated. And as for IT-spurred industrytransformations, most of the ones thatare going to happen have likely alreadyhappened or are in the process of hap-pening. Industries and markets will con-tinue to evolve, of course, and some willundergo fundamental changes-the fu-ture ofthe music business, for example,conrinues to be In doubt. But bistoryshows that tbe power of an infrastruc-tural technology to transform industriesalways diminishes as its buildout nearscompletion.

While no one can say precisely wbenthe buildout of an infrastructural tech-nology has concluded, there are manysigns that the IT buiidout is much closerto its end than its beginning. Eirst, IT'spower is outstripping most of tbe busi-ness needs it fulfills. Second, the price ofessential IT functionality has droppedto the point where it is more or lessaffordable to all. Third, the capacity ofthe universal distribution network (theInternet) has caught up with demand-indeed, we already have considerablymore fiber-optic capacity than we need.Fourth, IT vendors are rushing to posi-tion themselves as commodity suppli-ers or even as utilities. Finally, and mostdefinitively, the investment bubble basburst, wbicb historically bas been a clearindication tbat an infrastructural tech-nology is reacbing the end of its build-out. A few companies may still be ableto wrest advantages from bighly spe-cialized applications that don't offerstrong economic incentives for repli-cation, but those firms will be the ex-ceptions that prove the rule.

At the close oftbe 1990s, when Inter-net hype was at full boil, technologistsoffered grand visions of an emerging

What Every BoarcMember Should Know

From the # 1 ranked business school in the worldThe Econojnist Intelligence Unit 2002 $ttrvey

Today — more than ever — it is essential for boardmembers to perform skillfully and ethically. |Join the Kellogg School's world-class faculty Iand seasoned board members for executiveeducation that provides the best thought

leadership available.

Discover which governance program

I is right for you.

Strategies for ImprovingDirectors' Effectiveness

Jun 17-20 ,

Women's DirectorDevelopment Program

Nov 12-14

Minority DirectorDevelopment ProgramJun29-Jul2 • Dec 1-4

Governing theFamily Business

Oct 8-11

Phone: 847.467.7000 • Fax: 847.491.4323Exec:[email protected] • www.keHogg.northwestern.edu/execed

HBR AT LARGE - IT Doesn't Matter

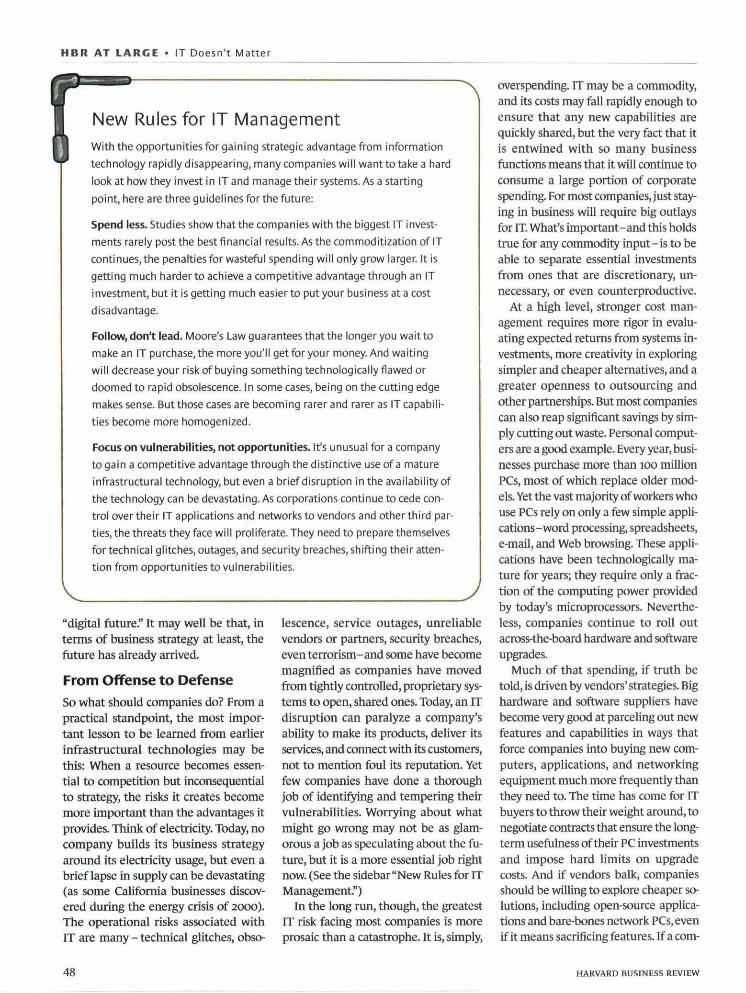

New Rules for IT ManagementWith the opportunities for gaining strategic advantage from information

technology rapidlydisappearing.nnany companies will want to take a hard

look at how they invest in IT and manage their systems. Asa starting

point, here are three guidelines for the future:

Spend Ie5s. Studies show that the companies with the biggest IT invest-

ments rarely post the best financial results. As the commoditization of IT

continues, the penalties for wasteful spending will only grow larger. It is

getting much harder to achieve a competitive advantage through an IT

investment, but it is getting much easierto put your business at a cost

disadvantage.

Follow, don't lead. Moore's Law guarantees that the longer you wait to

make an IT purchase, the more you'll get for your money. And waiting

will decrease your risk of buying something technologically fiawed or

doomed to rapid obsolescence. In some cases, being on the cutting edge

makes sense. But those cases are becoming rarer and rarer as IT capabili-

ties become more homogenized.

Focus on vulnerabilities, not opportunities. It's unusual for a company

to gain a competitive advantage through the distinctive use of a mature

infrastructural technology, but even a brief disruption in the availability of

the technology can be devastating. As corporations continue to cede con-

trol over their IT applications and networks to vendors and other third par-

ties, the threats they face will proliferate. They need to prepare themselves

for technical glitches, outages, and security breaches, shifting their atten-

tion from opportunities to vulnerabilities.

"digital ftiture." It may well be that, interms of business strategy at least, thefuture has already arrived.

From Offense to DefenseSo what sbould companies do? From apractical standpoint, the most impor-tant lesson to be leamed from earlierinfrastructural technologies may bethis: When a resource becomes essen-tial to competition but inconsequentialto strategy, tbe risks it creates becomemore important than the advantages itprovides. Think of electricity. Today, nocompany builds its business strategyaround its electricity usage, but even abrief lapse in supply can be devastating(as some Califomia businesses discov-ered during the energy crisis of 2000).The operational risks associated withn are many - technical glitches, obso-

lescence, service outages, unreliablevendors or partners, security breacbes,even terrorism-and some have becomemagnified as companies bave movedfrom tightly controlled, proprietary sys-tems to open, shared ones. Today, an ITdisruption can paralyze a company'sability to make its products, deliver itsservices, and connect with its customers,not to mention foul its reputation. Yetfew companies have done a thoroughjob of identifying and tempering theirvulnerabilities. Worrying about whatmight go wrong may not be as glam-orous a job as speculating about the fu-ture, but it is a more essential job rightnow. (See the sidebar "New Rules for ITManagement")

In tbe long run, tbough, the greatestIT risk facing most companies is moreprosaic than a catastrophe. It is, simply,

overspending. IT may be a commodity,and its costs may fall rapidly enough toensure that any new capabilities arequickly shared, but the very fact that itis entwined with so many businessfunctions means that it will continue toconsume a large portion of corporatespending. For most companies, just stay-ing in business will require big outlaysfor IT. Wbat's important-and this holdstme for any commodity input-is to beable to separate essential investmentsfrom ones tbat are discretionary, un-necessary, or even counterproductive.

At a high level, stronger cost man-agement requires more rigor in evalu-ating expected returns from systems in-vestments, more creativity in exploringsimpler and cheaper altematives, and agreater openness to outsourcing andother partnerships. But most companiescan also reap significant savings by sim-ply cutting out waste. Personal comput-ers are a good example. Every year, busi-nesses purchase more than lOO millionPCs, most of which replace older mod-els. Yet tbe vast majority of workers whouse PCs rely on only a few simple appli-cations-word processing, spreadsheets,e-mail, and Web browsing. These appli-cations have been technologically ma-ture for years; they require only a frac-tion of the computing power providedby today's microprocessors. Neverthe-less, companies continue to roll outacross-the-board hardware and softwareupgrades.

Much of tbat spending, if truth betold, is driven by vendors' strategies. Bighardware and software suppliers havebecome very good at parceling out newfeatures and capabilities in ways thatforce companies into buying new com-puters, applications, and networkingequipment much more frequently thanthey need to. The time has come for ITbuyers to throw their weight around, tonegotiate contracts that ensure tbe long-term usefulness of their PC investmentsand impose hard limits on upgradecosts. And if vendors balk, companiesshould be willing to explore cheaper so-lutions, including open-source applica-tions and bare-bones network PCs, evenif it means sacrificing features. If a com-

HARVARD BUSINESS REVIEW

pany needs evidence of the kind ofmoney that might be saved, it need onlylook at Microsoft's profit margin.

In addition to being passive in tbeirpurcbasing, companies bave been sloppyin their use of IT. Tbat's particularly tmewitb data storage, which has come toaccount for more than half of manycompanies' IT expenditures. The bulk ofwbat's being stored on corporate net-works has little to do witb making prod-ucts or serving customers ~ it consistsof employees' saved e-mails and files.

Some managers may worry that be-ing stingy witb IT dollars will damagetbeir competitive positions. But studiesof corporate IT spending consistentlyshow that greater expenditures rarelytranslate into superior financial results.In fact, tbe opposite is usually tme. In2002, tbe consulting firm Alinean com-pared the IT expenditures and the fi-nancial results of 7,500 large U.S. com-panies and discovered that the topperformers tended to be among tbemost tightfisted. The 25 companies that

Studies of corporate IT spending consistently show

that greater expenditures rarely translate into superior

financial results. In fact, the opposite is usually true.

including terabytes of spam, MP3s, andvideo clips. Computerworld estimatesthat as mucb as 70% of tbe storage ca-pacity of a typical Windows network iswasted - an enormous unnecessary ex-pense. Restricting employees' ability tosave files indiscriminately and indefi-nitely may seem distasteful to manymanagers, but it can bave a real impacton tbe bottom Une. Now tbat IT basbecome the dominant capital expensefor most businesses, there's no excusefor waste and sloppiness.

Given the rapid pace of technology'sadvance, delaying IT investments can beanother powerful way to cut costs -while also reducing a firm's chance ofbeing saddled witb buggy or soon-to-be-obsolete tecbnology. Many compa-nies, particularly during tbe 1990s,mshed their IT investments either be-cause tbey hoped to capture a first-mover advantage or because tbey fearedbeing left bebind. Except in very rarecases, both the hope and the fear wereunwarranted. The smartest users oftechnology - here again. Dell and Wal-Mart stand out-stay well back from tbecutting edge, waiting to make purchasesuntil standards and best practices solid-ify. Tbey let their impatient competitorsshoulder the bigh costs of experimenta-tion, and then tbey sweep past them,spending less and getting more.

delivered the highest economic retums,for example, spent on average just 0.8%of their revenues on IT, while the typicalcompany spent 3.7%. A recent study byForrester Researcb showed, similarly,tbat the most lavish spenders on ITrarely post the best results. Even Oracle'sLarry Ellison, one of tbe great technol-ogy salesmen, admitted in a recent in-terview that "most companies spend toomuch [on IT] and get very little in re-tum." As the opportunities for IT-basedadvantage continue to narrow, the pen-alties for overspending will only grow.

IT management sbould, frankly, be-come boring. Tbe key to success, for thevast majority of companies, is no longerto seek advantage aggressively but tomanage costs and risks meticulously. If,like many executives, you've begun totake a more defensive posture toward ITin the last two years, spending more fru-gally and thinking more pragmatically,you're already on the right course. Thechallenge will be to maintain that disci-pline when the business cycle strength-ens and the choms of hype about IT'sstrategic value rises anew. ^

1."Information technology" is a fuzzy term. In thisarticle, it is used in its common current sense, as de-noting the technologies used for processing, storing,and transporting information in digital form.

Reprint R0305B; HBR OnPoint 3566To order, see page 131.

A T B O O K S T O R E S E V E R Y W H E R E

IDEAS IN ACTIONW H A T ' S

CREATING AND CAPITALIZINGON THE BEST

MANAGEMENT THINKING !

rHOMAS H. DAVENPORrLAURENCE PRUSAK

WITH H JAMtS WILSON

The secrets of successfulidea practitioners.

B N A S H I I C H U R A V G R T I

Bringing InnouatidritnrtptinarotdWld

An innovator'splaybook for shapingthe market endgame.

HENRY CHE5BR0UGH

OPENThe New Imperative

For Creating and ProFitingFrom Technology

How to ieverage ideasfrom inside and out.

H A R V A R D B U S I N E S S

S C H O O L P R E S S

MAY 2003 w w w . H B S P r e ' s s . o r

Harvard Business Review Notice of Use Restrictions, May 2009

Harvard Business Review and Harvard Business Publishing Newsletter content on EBSCOhost is licensed for

the private individual use of authorized EBSCOhost users. It is not intended for use as assigned course material

in academic institutions nor as corporate learning or training materials in businesses. Academic licensees may

not use this content in electronic reserves, electronic course packs, persistent linking from syllabi or by any

other means of incorporating the content into course resources. Business licensees may not host this content on

learning management systems or use persistent linking or other means to incorporate the content into learning

management systems. Harvard Business Publishing will be pleased to grant permission to make this content

available through such means. For rates and permission, contact [email protected].