Embed Size (px)

Citation preview

CRM & customer singularity horizon

Marek Rucinski – Managing Director Accenture Interactive

May 2015

Consumers vs. Brands – power reversal is complete and irreversible

Information-rich & Innovation-drivers…the consumers have rightly taken the marketing mantle

~4M searches on Google

~38K photos shared

~347K tweets

~100 hours of video uploaded

1 DIGITAL MINUTE…

Copyright © 2015 Accenture All rights reserved. 2

Information landscape enriched… …Impacting the buying process… …and marketing realities

~3.1M likes on Facebook

~277K snapchats received

~3.5K pins

~$275K (USD) transactions

TRADITIONAL FUNNEL IS OUT-DATED…

Use

Discover

Expectation

Promise

Reality

Delivery Evaluate

Consider

Evaluate

Purchase

Open content & channels

Branded content & channels

Insights & Profiling

Analytics & data collection

Vision & Strategies

Omni-channel interactions

Product & service for customers

HIGH IMPACT

MEDIUM IMPACT

3

Consumer Clarity vs. Cloudiness – start point for relevant interactions

Mastery of the customer data… internal/ external… and real-time… is foundational

“BELOW AVERAGE” DATA-LANDSCAPE

Have and leveraging as needed

Have some and more needed

Don’t’ have it but may need it

Structured Unstructured

External

Internal

Batch

Copyright © 2015 Accenture All rights reserved.

Structured Unstructured

External

Internal

Batch

Call Center

Stores

Websites

Mobile App/ SMS

Social media/ blogs

Locations/ Geo-tagging

Direct Mail/ emails

Offer and Promotion preferences

Demographics

Survey data

Psychographics/ Lifestyle

Household/ Occupation/ Income & assets

Spending Patterns & product/ service propensities

Communication & Interaction/ touch points preferences

Customer Profile

“ABOVE AVERAGE” DATA-LANDSCAPE

4

Knowing vs Understanding – real personalisation a new baseline

Linking detailed customer profiles to relevant actions a new baseline for personalised engagement

Copyright © 2015 Accenture All rights reserved.

PE

RS

ON

ALIS

AT

ION

Customer Profile

Recognise

Remember

Relate

Recommend

4 Rs OF PERSONALISATION: One size fits all… Segmented… Detailed

5

Wanting vs getting – customers desire personalisation and seamlessness

Being time-poor and information-rich has made consumers mode demanding and less patient

Copyright © 2015 Accenture All rights reserved.

Leading retailers are responding by integrating processes into seamless workflows

SEAMLESS RETAIL BY DIMENSION

Consistent Experience 1

Connected Shopping 2

Integrated Merchandizing 3

Flexible Fulfilment/ Returns 4

Personalized Interaction 5

Better, Faster, & Memorable

Absent Under- developed

Developed Advanced Highly Advanced

6

Source: Accenture Retail Practice

6

Predicting vs. Self-learning – the singularity is coming

Predictive modelling for decision support is about to move to AI driven self learning mode

Copyright © 2015 Accenture All rights reserved.

From discrete

to real-time

…across relevant touch points & locations

…with personalised offers to:

Attract & Drive traffic Convert to Customers

Engage and Retain

Propensities, Rules, offers &

Recommendations

Machine Learning

& AI

Data Integration Analytics & Insights Business Execution

Customers’ Profiles & segments

Network Profiles & clusters

Business Performance

…and closed loop learnings

& model refinements

7

Cool vs Creepy – the uncanny valley of CRM

Insights from a recent Accenture survey of retail customers in North America

Copyright © 2015 Accenture All rights reserved.

Good knowledge and strong recommendations from staff were appreciated…

Customers were happy to receive discounts and complementary item suggestions when shopping…

82% of respondents were happy to receive coupons and loyalty points, the preferred method of personalisation

Amazon was the most trusted of all retailers represented in the survey, with 69% of surveyed trusted them

…but intervention in purchases of food or clothes were criticised by 46% of those surveyed

…but found seeing recommendations from their friends while online shopping was delving too far into ‘creepy’

…but 52% were uncomfortable with being tracked by a retailer in store at all

…only a third of respondents felt confident that the information they supplied to online retailers was being correctly safeguarded

Vs.

COOL… CREEPY…

8

Good vs Great – what does it look like ?

AstraZeneca orchestrates insights, marketing collateral as well as offer ideation on global basis to

shorten the time & cost to market while driving the relevance to the customers up

Copyright © 2015 Accenture All rights reserved.

• Pharma player … 90 countries

• End to end MRM and CM capabilities

• Global DAM for marketing artefacts

• Insights lead targeting and closed loop ideation

• In-house marketing with global marketing services

WHAT?

• Workflow / back-end industralisation @ global scale

• Customer centric at heart – localised insights driven

• Streamlined workflows to minimise time to market

• Global orchestration and support to drive adoption

• Through the channel approach

• Data driven insights balanced with creative ideation

• Top line and cost out benefits

WHY?

9

Good vs Great – what does it look like ?

Procter & Gamble has scaled the marketing service in partnership with global partners to deliver

scaled and timely execution, that is tied to customer insights for each brand and market

Copyright © 2015 Accenture All rights reserved.

• Global FMCG player

• Focus on scaled digital innovation to drive brands’ health

• CRM visualisation, automation and optimisation focus

• Content management and scaled usage globally

• Service provision of marketing services by partner

WHAT?

• Global orchestration of CRM / MRM workflows & content

• Initiated unprecedented wave of digital innovation

• 90% of global marketing initiatives coverage

• 1500+ Customer centric and personalised websites

• Closed loop analysis and refinement process

• Reduction of time to market for initiatives by a half

• Reduction in production costs by a third

WHY?

10

Good vs Great – what does it look like ?

European telco successfully orchestrated real time customer and website data and behaviour to

drive real time personalised interactions leading to breakthrough conversion results

Copyright © 2015 Accenture All rights reserved.

• Digital sales acquisition and growth focus

• Growing importance of digital customer – 60% of decisions

• SEO SEM lead generation and sales cycle optimisation

• Value based commercial model

• Insights, analytics and content for personalised interactions

WHAT?

• Base-lined performance and closed up uplift measures

• Personalisation and Engagement in Real-Time

• Sales up 2.5x

• Conversion up 2x

• Sustainable knowledge transfer – process, org & digital

WHY?

Personalised

version

+79% click-through to Check outs

+ 31% click-through to order

Original

version

11

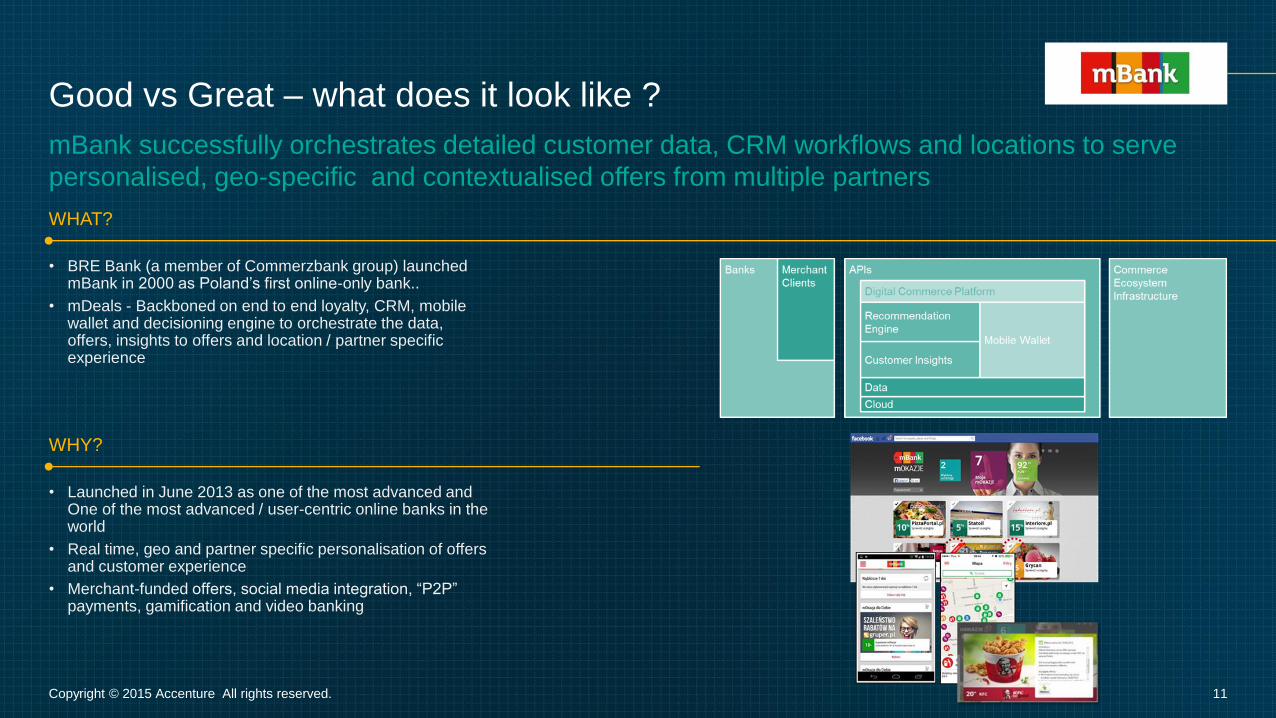

Good vs Great – what does it look like ?

mBank successfully orchestrates detailed customer data, CRM workflows and locations to serve

personalised, geo-specific and contextualised offers from multiple partners

Copyright © 2015 Accenture All rights reserved.

• BRE Bank (a member of Commerzbank group) launched mBank in 2000 as Poland’s first online-only bank..

• mDeals - Backboned on end to end loyalty, CRM, mobile wallet and decisioning engine to orchestrate the data, offers, insights to offers and location / partner specific experience

WHAT?

• Launched in June 2013 as one of the most advanced and One of the most advanced / user-centric online banks in the world

• Real time, geo and partner specific personalisation of offers and customer experience

• Merchant-funded offers, social media integration, “P2P” payments, gamification and video banking

WHY?

12

Reality vs Theory – where are the break points and how to forge ahead ?

Progressive capability building across DELTA … to deliver real applications for customer engagement

Copyright © 2015 Accenture All rights reserved.

12

Progressive

Balanced

Power the business and customer experiences by

optimizing the marketing, content, and commerce

technology and operations scaled as needed to perform

Robust, Scalable, Deployed Fast

Transform the business and operating models towards

customer-centricity and agility while infusing innovation

and analytics into the core culture

Effective, Agile, Delivers ROI

DELIGHT YOUR CUSTOMER

FLEX YOUR PLATFORM

RE-ORIENT YOUR BUSINESS

Understand your customer to design delightful omni-

channel experiences and services

Relevant, Elegant, Simple

Talking vs doing – how to make this real ? …we can help

For further information, please contact

Marek Rucinski

Managing Director – Accenture Interactive

![Singularity - easybuilders.github.ioeasybuilders.github.io/easybuild/files/EUM17/20170208-1_Singularity… · Singularity Workflow 1. Create image file $ sudo singularity create [image]](https://img.pdfslide.net/doc/110x75/5f0991027e708231d4277151/singularity-singularity-workflow-1-create-image-file-sudo-singularity-create.jpg)