Embed Size (px)

Citation preview

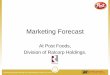

3.8%

8.0%

9.5%

12.9%

W. Continental Europe

APAC, LATAM, Africa, ME, Central…

N. America

UK

4.7%

8.0%

8.8%

10.6%

10.8%

US

APAC

All other markets

UK

LATAM

8.2%

5.7%

2.0%

5.5%

2014 Organic revenue growth

WPP use rate of US$1.6475 to the pound (2013: 1.5646)

Publics use rate of US$1.3267 to the euro (2013: 1.3277)

Organic Growth: the year-on-year increase or decrease in revenue from

the prior period, excluding the FX impact and net acquisition revenue

NB: Source data published by each of the four holding companies

WPP posted record profits for 2014, strengthening its position as the world’s

largest marketing services company. The group experienced organic

revenue growth of 8.2% in 2014, with total revenue of £11.5bn ($19bn).

Omnicom’s organic growth was 5.7%, with revenues of $15.3bn. Publicis

experienced weak organic growth with 2%, and revenue of €7.3bn ($9.6bn).

IPG’s organic growth was 5.5%, with revenue of $7.5bn.

WPP announced a headline profit before tax of £1.5bn ($2.5bn), the highest in

its history. Headline EBITDA was £1.9bn ($3.1bn), with a margin of 16.6%.

Omnicom’s EBITDA increased 6.1% to $2.2bn, with a margin of 14.6%. Publicis’

EBITDA increased 6.5% to €1.2bn ($1.7bn), and is still ahead of its peers with a

strong 18% margin. IPG’s EBITDA was up 25.5% to $1bn, but their margin is still

lagging at 13.3%, despite a strong year for McCann Worldgroup, who

recently published a number of new client wins.

The UK remains a robust market for most of the four largest players, with WPP

reporting £1.6bn ($2.7bn) revenue and 12.9% organic growth in the region,

Publicis being the only one of the four being underweight in the UK. IPG

experienced very strong organic growth in the LATAM region, but

underperformed in the US given its size in the market.

Continental Europe was a drag on all four holding companies in 2014. Most of

the major networks are struggling with the shrinking of some of their

fragmented Continental European markets.

Overall a strong 2014 posted by WPP.

1.0%

4.0%

4.5%

5.2%

7.5%

10.1%

Europe

LATAM

APAC

UK

N. America

Africa/ Middle East

2.3%

3.5%

6.7%

N. America

BRIC + MISSAT

Rest of World

Organic revenue growth by region

2014 revenue & EBITDA (US$bn)

EBITDA Revenue

13.3%14.6% 18.0%

19

15.3

16.6%

9.6

7.5

% shows EBITDA Margin

Strong 2014 performance from WPP, led by UK and US, but Continental Europe remains a struggle for the large holding companies

*Europe excludes Russia and Turkey

BRIC: Brazil, Russia, India & China

ME: Middle East

MISSAT: Mexico, Indonesia, Singapore, South Africa & Turkey

3.1 2.21.7 1.0

Europe -1.3%

Europe* -0.6%

APAC, LATAM, ME, Africa,

Central & E. Europe

Snapshot: Marketing services sectorLarge Holding Companies – 2014 annual results analysis

Snapshot: Marketing services sectorLarge Holding Companies – 2014 annual results analysis

James Whyms

Analyst

T 020 3640 8638

Afsor Miah

Director

T 020 7993 7543

The intellectual property rights to the research and data provided herein is owned by Ciesco Limited (“Ciesco Group” or Ciesco). Any unauthorised use, including but not limited to copying, distributing, transmitting or otherwise of any data appearing is not permitted without Ciesco’s prior consent. Ciesco do not accept or assume any liability or obligation for or relating to the content or information (“data”) contained herein, any errors, inaccuracies, omissions or delays in the data, or for any actions taken or not taken by anyone in reliance on the information in this publication or for any decision based on it.

While this publication has been carefully prepared, it has been written in general terms and should be seen as broad guidance only. The publication cannot be relied upon to cover specific situations and you should not act, or refrain from acting, upon the information contained therein without obtaining specific professional advice. Please contact Ciesco to discuss these matters in the context of your particular circumstances. In no event shall Ciesco, its partners, employees and agents be liable for any special, incidental, or consequential damages or for any loss arising out of the use of the data.

Ciesco Limited is registered in England and Wales under no. 0724319. Our registered office is based at 96 Kensington High Street, London W8 4SG, United Kingdom.

© March 2015 Ciesco Limited. All rights reserved.

Ciesco is a boutique corporate finance advisory firm, specialising in the digital, media,

marketing and technology sectors. We advise our clients on mergers & acquisitions,

business strategy and executive search.

About Ciesco