Embed Size (px)

DESCRIPTION

Mobile Forum Mexico. Nov 2014

Citation preview

#AdReaction

Connecting with

Mexican

Consumers in 2014James Galpin,

Head of Media & Digital, LATAM

AdReaction 2014

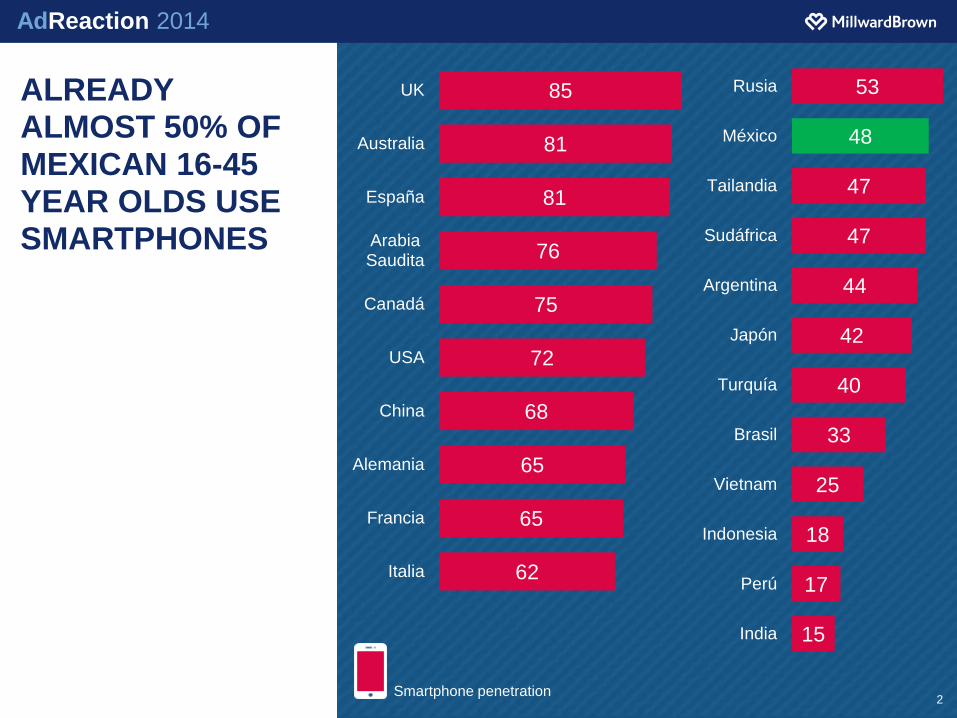

ALREADY ALMOST 50% OF MEXICAN 16-45 YEAR OLDS USE SMARTPHONES

2

62

65

65

68

72

75

76

81

81

85

Italia

Francia

Alemania

China

USA

Canadá

ArabiaSaudita

España

Australia

UK

15

17

18

25

33

40

42

44

47

47

48

53

India

Perú

Indonesia

Vietnam

Brasil

Turquía

Japón

Argentina

Sudáfrica

Tailandia

México

Rusia

Smartphone penetration

MORE PEOPLE ARE NOW GOING ONLINE FOR FIRST TIME ON MOBILE, THAN ARE ON PC

The Mexican consumer is

moving to smartphone

connectivity very fast

Marketing in the multiscreen world

AdReaction 2014

MEXICO

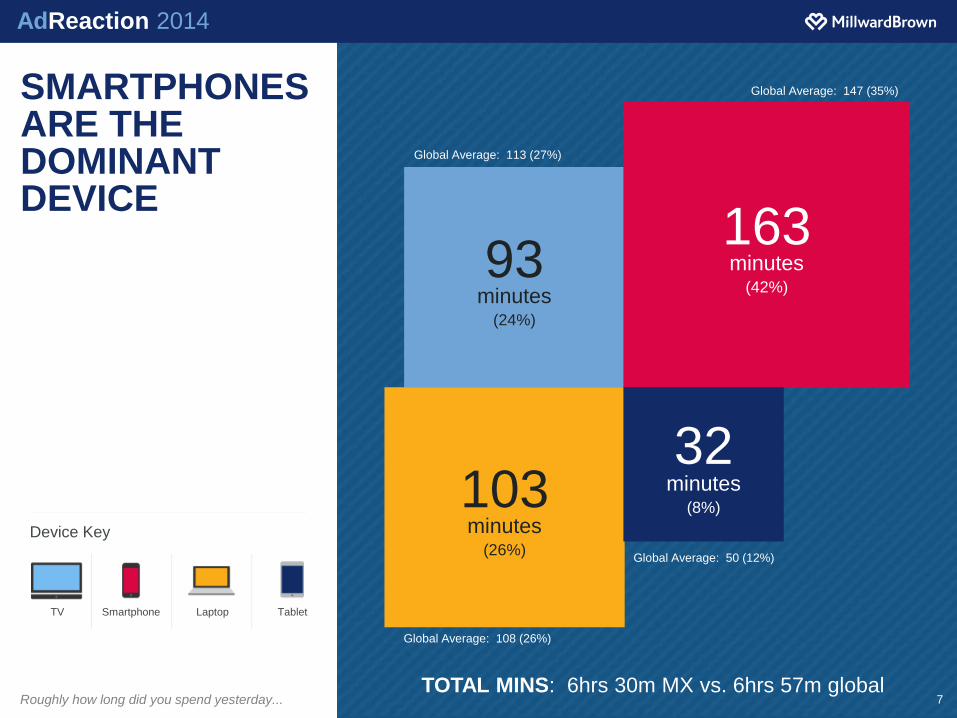

HOW MUCH & WHEN ARE SCREENS USED IN MEXICO?

AdReaction 2014

SMARTPHONES ARE THE DOMINANT DEVICE

Roughly how long did you spend yesterday... 7

TV Smartphone Laptop Tablet

Device Key

93minutes

(24%)

163minutes

(42%)

103minutes

(26%)

32minutes

(8%)

Global Average: 113 (27%)

Global Average: 108 (26%)

Global Average: 50 (12%)

Global Average: 147 (35%)

TOTAL MINS: 6hrs 30m MX vs. 6hrs 57m global

AdReaction 2014

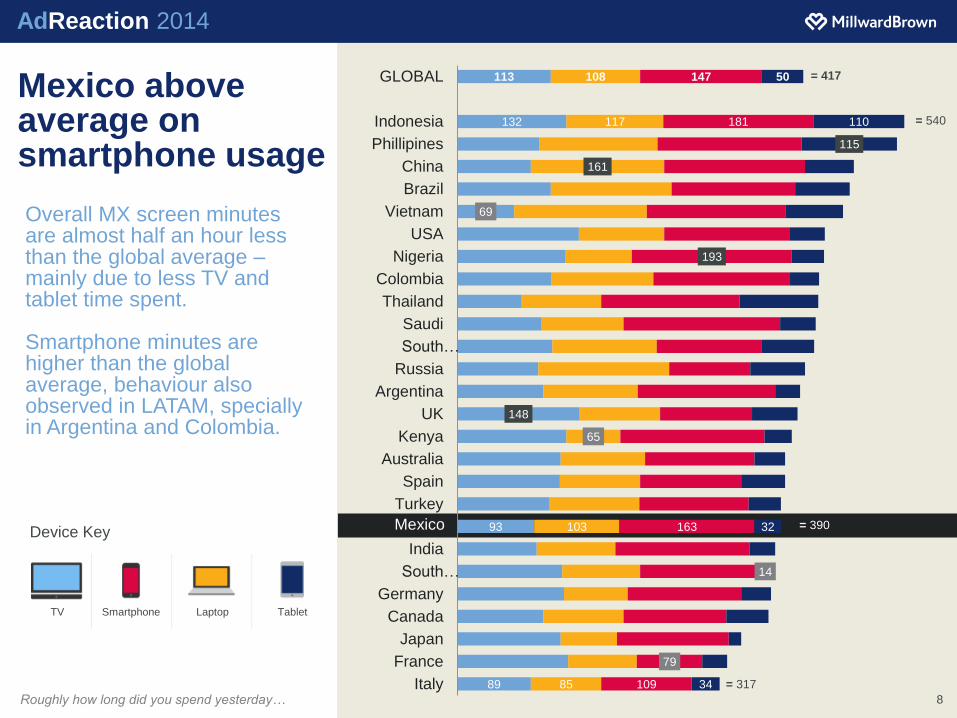

Mexico above average on smartphone usage

Overall MX screen minutes are almost half an hour less than the global average –mainly due to less TV and tablet time spent.

Smartphone minutes are higher than the global average, behaviour also observed in LATAM, specially in Argentina and Colombia.

Roughly how long did you spend yesterday… 8

TV Smartphone Laptop Tablet

Device Key

= 417

= 390

= 540

= 31789

93

148

69

132

113

85

103

65

161

117

108

109

79

163

193

181

147

34

14

32

115

110

50

Italy

France

Japan

Canada

Germany

South…

India

Mexico

Turkey

Spain

Australia

Kenya

UK

Argentina

Russia

South…

Saudi

Thailand

Colombia

Nigeria

USA

Vietnam

Brazil

China

Phillipines

Indonesia

GLOBAL

Mexico

AdReaction 2014

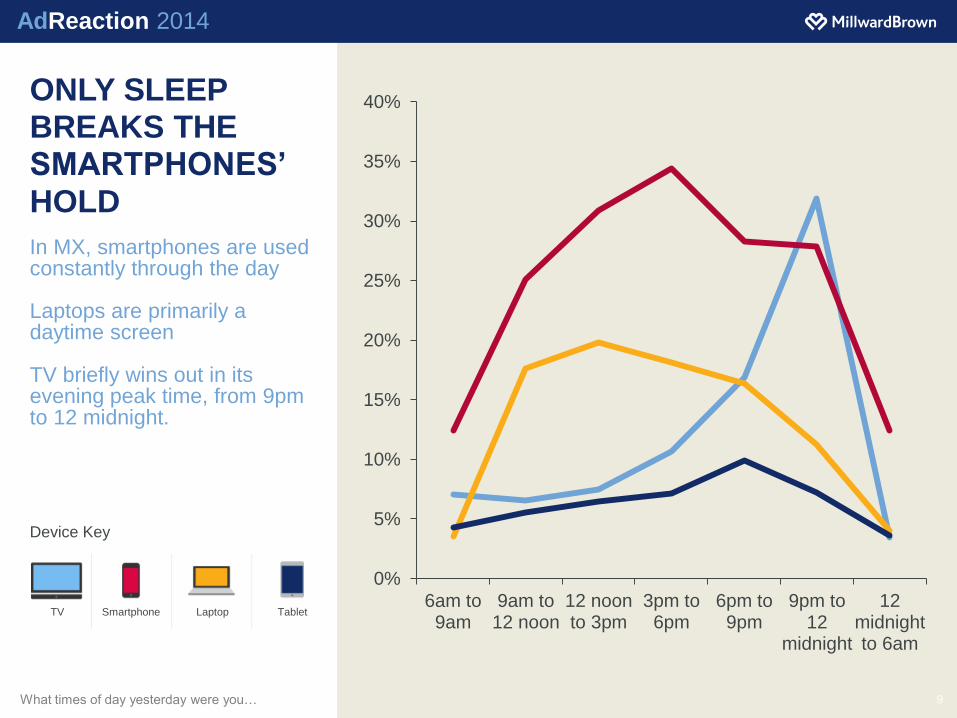

In MX, smartphones are used constantly through the day

Laptops are primarily a daytime screen

TV briefly wins out in its evening peak time, from 9pm to 12 midnight.

What times of day yesterday were you… 9

0%

5%

10%

15%

20%

25%

30%

35%

40%

6am to9am

9am to12 noon

12 noonto 3pm

3pm to6pm

6pm to9pm

9pm to12

midnight

12midnightto 6am

TV Smartphone Laptop Tablet

Device Key

ONLY SLEEP BREAKS THE SMARTPHONES’ HOLD

AdReaction 2014

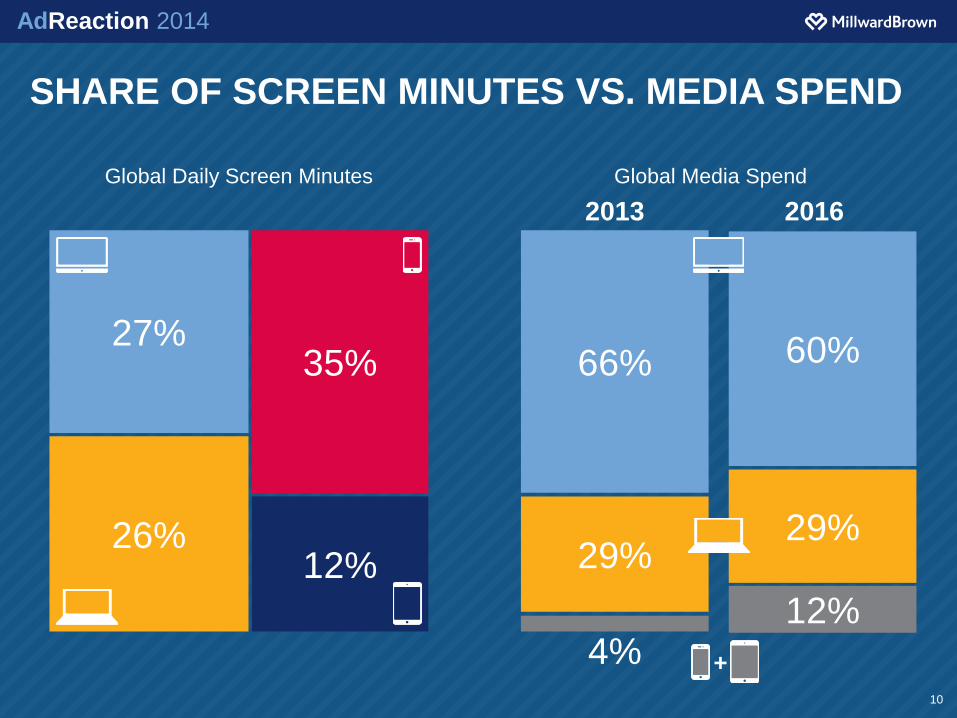

SHARE OF SCREEN MINUTES VS. MEDIA SPEND

10

Global Daily Screen Minutes

27%

12%26%

35%

12%

29%

60%

2016

66%

29%

4%

Global Media Spend

2013

+

When are the peak times for digital /

online marketing communications?

Which connected device is used most

then?

So which device gives brands the best

chance to reach consumers at the right

moment?

HOW ARE SCREENS USED?

AdReaction 2014

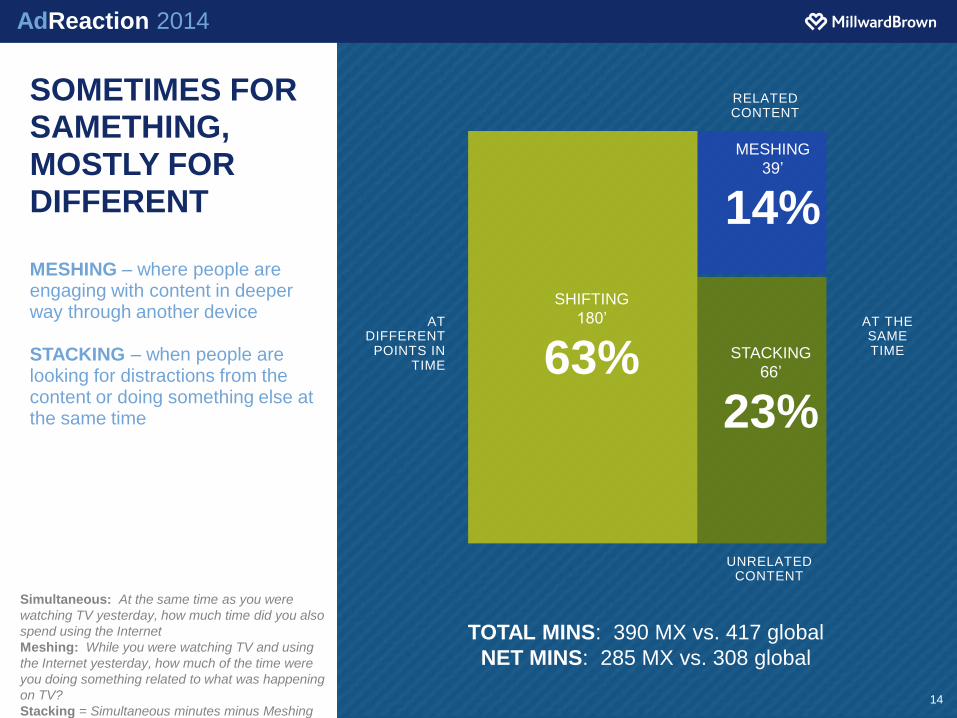

AT THE SAME TIME

AT DIFFERENT

POINTS IN TIME

PEOPLE NOW ROUTINELY USE CONNECTED DEVICES WHILE WATCHING TV

Of their 6.5 hours screen consumption, 105 minutes is simultaneous consumption of another digital screen while watching TV.

Simultaneous: At the same time as you were

watching TV yesterday, how much time did you also

spend using the Internet

13

SHIFTING

180’

63%

SIMULTANEOUS

105’

37%

TOTAL MINS: 390 MX vs. 417 global

NET MINS: 285 MX vs. 308 global

AdReaction 2014

RELATED CONTENT

UNRELATED CONTENT

AT THE SAME TIME

AT DIFFERENT

POINTS IN TIME

Simultaneous: At the same time as you were

watching TV yesterday, how much time did you also

spend using the Internet

Meshing: While you were watching TV and using

the Internet yesterday, how much of the time were

you doing something related to what was happening

on TV?

Stacking = Simultaneous minutes minus Meshing

minutes

14

SHIFTING

180’

63% STACKING

66’

23%

TOTAL MINS: 390 MX vs. 417 global

NET MINS: 285 MX vs. 308 global

MESHING

39’

14%

SOMETIMES FOR SAMETHING, MOSTLY FOR DIFFERENT

MESHING – where people are engaging with content in deeper way through another device

STACKING – when people are looking for distractions from the content or doing something else at the same time

AdReaction 2014

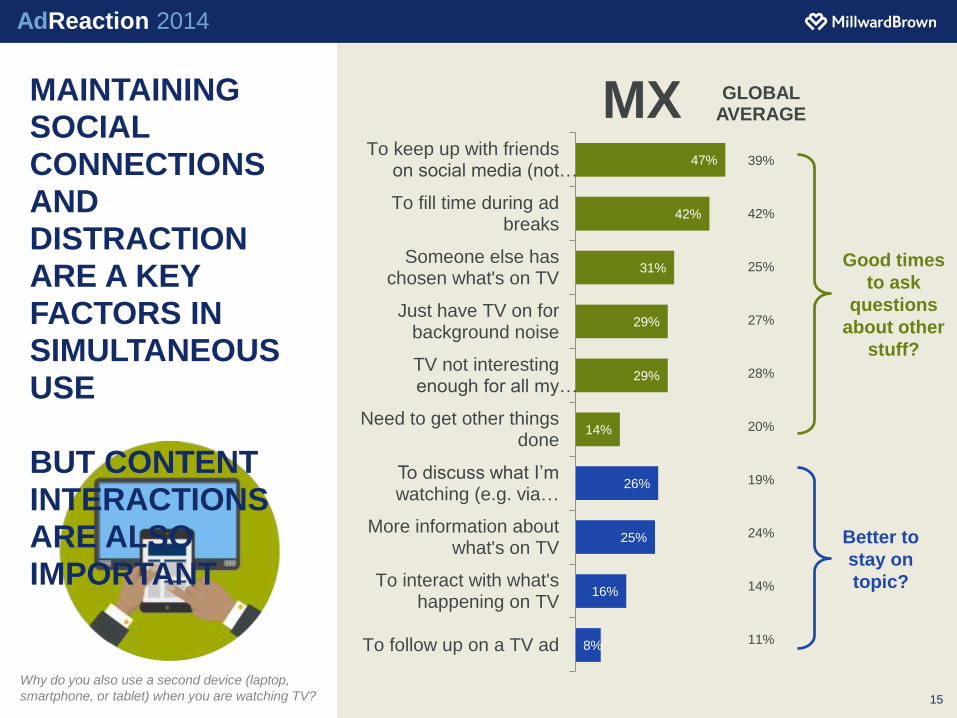

8%

16%

25%

26%

14%

29%

29%

31%

42%

47%

To follow up on a TV ad

To interact with what'shappening on TV

More information aboutwhat's on TV

To discuss what I’m watching (e.g. via …

Need to get other thingsdone

TV not interestingenough for all my…

Just have TV on forbackground noise

Someone else haschosen what's on TV

To fill time during adbreaks

To keep up with friendson social media (not…

MAINTAINING SOCIAL CONNECTIONS AND DISTRACTION ARE A KEY FACTORS IN SIMULTANEOUS USE

BUT CONTENT INTERACTIONS ARE ALSO IMPORTANT

Why do you also use a second device (laptop,

smartphone, or tablet) when you are watching TV? 15

MX GLOBAL AVERAGE

39%

42%

25%

27%

28%

20%

19%

24%

14%

11%

Good times

to ask

questions

about other

stuff?

Better to

stay on

topic?

AdReaction 2014

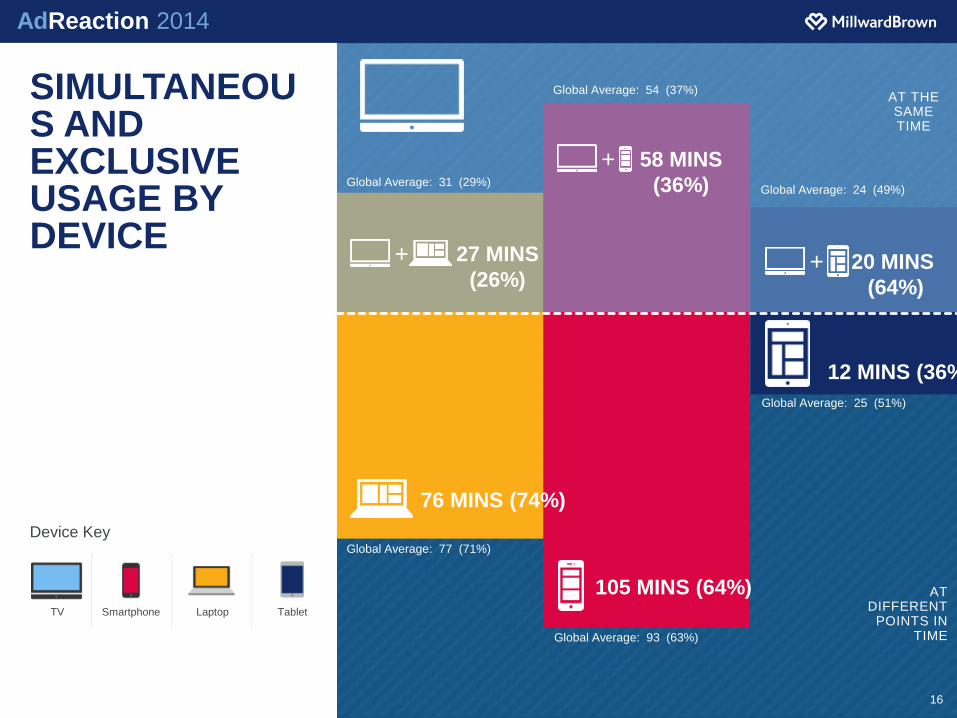

SIMULTANEOUS AND EXCLUSIVE USAGE BY DEVICE

16

TV Smartphone Laptop Tablet

Device Key

+ 27 MINS

(26%)

+ 58 MINS

(36%)

+ 20 MINS

(64%)

76 MINS (74%)

105 MINS (64%)

12 MINS (36%)

Global Average: 77 (71%)

Global Average: 31 (29%)

Global Average: 93 (63%)

Global Average: 25 (51%)

Global Average: 24 (49%)

Global Average: 54 (37%)AT THE SAME TIME

AT DIFFERENT

POINTS IN TIME

AdReaction 2014

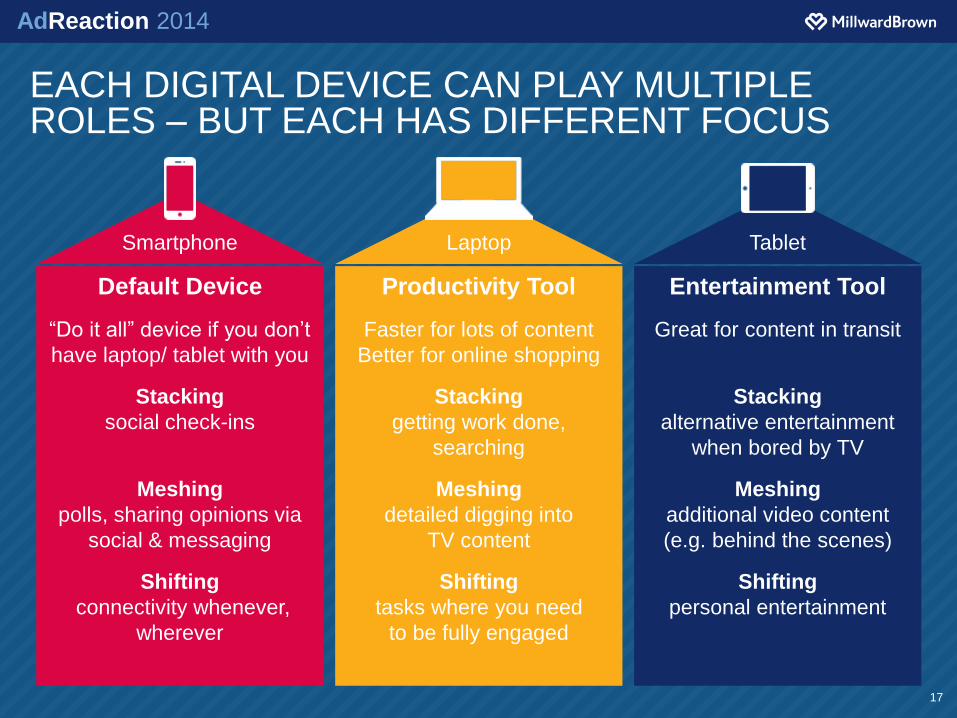

EACH DIGITAL DEVICE CAN PLAY MULTIPLE ROLES – BUT EACH HAS DIFFERENT FOCUS

17

Entertainment Tool

Great for content in transit

Stacking

alternative entertainment

when bored by TV

Meshing

additional video content

(e.g. behind the scenes)

Shifting

personal entertainment

Productivity Tool

Faster for lots of content

Better for online shopping

Stacking

getting work done,

searching

Meshing

detailed digging into

TV content

Shifting

tasks where you need

to be fully engaged

Default Device

“Do it all” device if you don’t

have laptop/ tablet with you

Stacking

social check-ins

Meshing

polls, sharing opinions via

social & messaging

Shifting

connectivity whenever,

wherever

Smartphone Laptop Tablet

AdReaction 2014

Smartphones do not just connect across screens

Festival of Media LATAM 2014 – Winner, Best use of Digital

AdReaction 2014

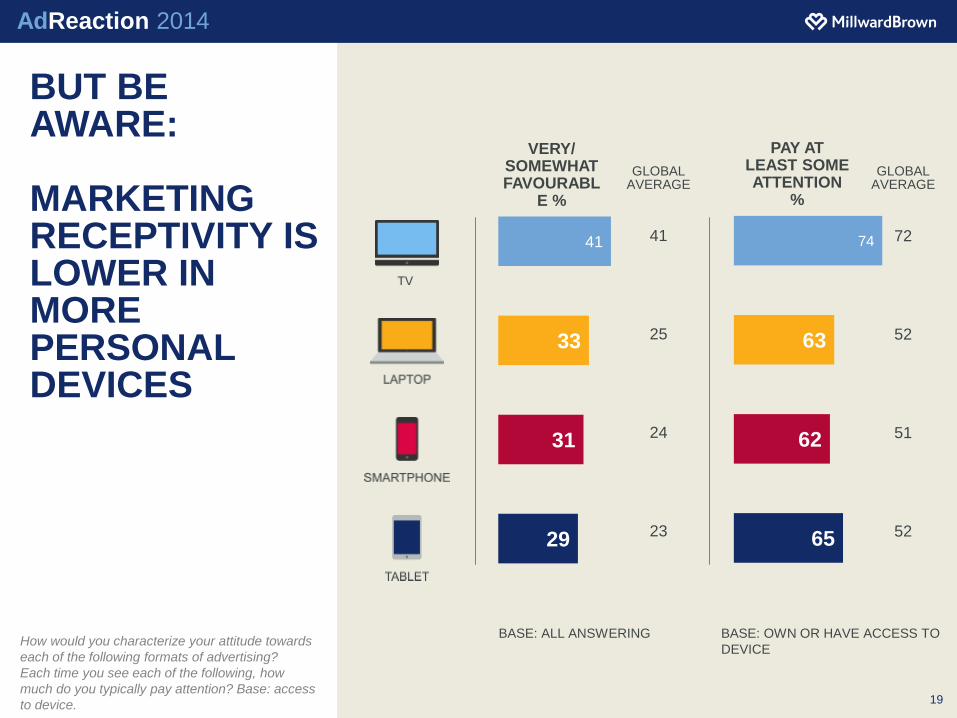

BUT BE AWARE:

MARKETING RECEPTIVITY IS LOWER IN MORE PERSONAL DEVICES

How would you characterize your attitude towards

each of the following formats of advertising?

Each time you see each of the following, how

much do you typically pay attention? Base: access

to device. 19

29

31

33

41

VERY/ SOMEWHAT FAVOURABL

E %

65

62

63

74

PAY AT LEAST SOME ATTENTION

%

41

25

24

23

GLOBAL AVERAGE

72

52

51

52

GLOBAL AVERAGE

BASE: ALL ANSWERING BASE: OWN OR HAVE ACCESS TO

DEVICE

Smartphones are becoming the

connective tissue between all consumer

touchpoints

They are allowing the analog to become

digital

Mobile connectivity offers Brands many

new opportunities to engage with and

build relationships with people

But personal devices are just that.

Personal. Marketers must not be too

intrusive or invasive.

HOW TO MEASURE MOBILE CAMPAIGN EFFECTIVENESS?

# BrandBrand Value

(USD MM)Country

1 Corona 8,025 México

2 Skol 7,055 Brasil

3 Falabella 6,084 Chile

4 Telcel 5,308 México

5 Bradesco 4,177 Brasil

6 Sodimac 4,107 Chile

7 Televisa 3,625 México

8 Brahma 3,585 Brasil

9 Aguila 3,565 Colombia

10 Modelo 3,477 México

* Concentra valores de Modelo Especial, Negra Modelo y Modelo Light. 23

Consumer decision-making

Source: The Consumer Decision Journey,

McKinsey Quarterly Review

24

BRAND

CONSIDERATION:

brands in the initial-

consideration set can be

up to three times more

likely to be purchased

eventually than brands

that aren’t in it.”

O c t o b e r 5 , 2 0 1 4 8 : 1 4 p m

G o o g l e u p b e a t o v e r b r a n d a d v e r t i s i n g t o o l s

G o o g l e h a s c l a i m e d p r o m i s i n g e a r l y r e s u l t s f r o m i t s l a t e s t a t t e m p t t o d r a w b r a n d a d v e r t i s e r s , f o l l o w i n g y e a r s o f d i s a p p o i n t m e n t o v e r t h e s l o w g r o w t h o f b r a n d e d d i s p l a y a n d v i d e o a d s t o m a t c h i t s s e a r c h b u s i n e s s .

25

Brand Impact of Mobile - AdIndex for Mobile

26

W E H A V E C O M P L E T E D 4 0 0 + M O B I L E A D V E R T I S I N G E F F E C T I V E N E S S S T U D I E S A C R O S S A B R O A D R A N G E O F I N D U S T R Y V E R T I C A L S

Tablets

Location

Multi-

Screen

Display &

Rich

Media

Ads

SMS

Apps

Mobile

Video

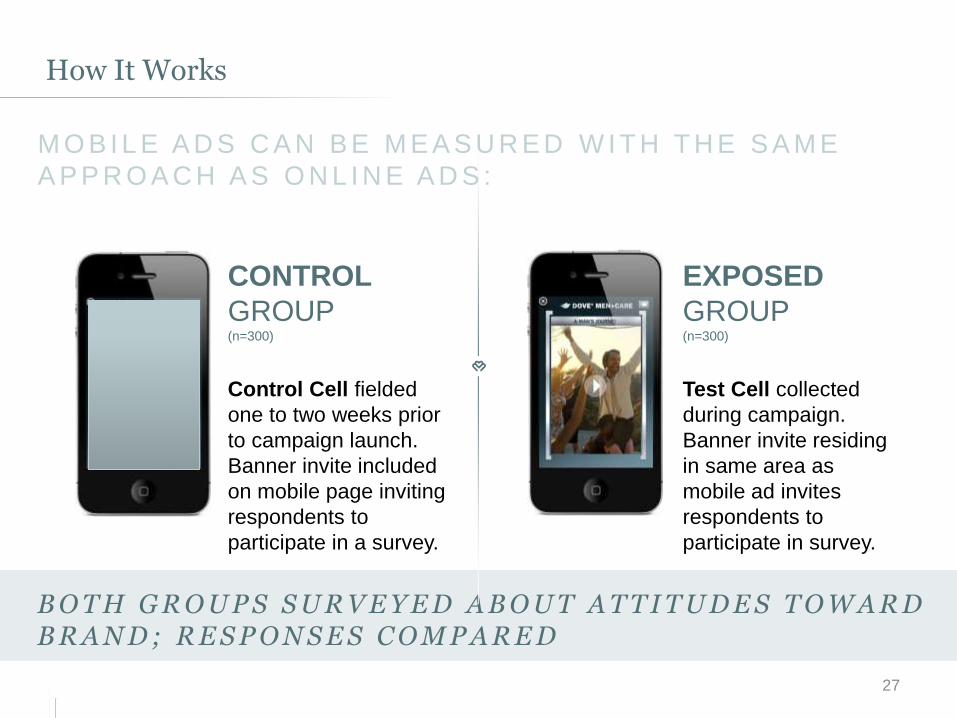

How It Works

27

B O T H G R O U P S S U R V E Y E D A B O U T A T T I T U D E S T O W A R D B R A N D ; R E S P O N S E S C O M P A R E D

M O B I L E A D S C A N B E M E A S U R E D W I T H T H E S A M E

A P P R O A C H A S O N L I N E A D S :

CONTROL

GROUP(n=300)

Control Cell fielded

one to two weeks prior

to campaign launch.

Banner invite included

on mobile page inviting

respondents to

participate in a survey.

EXPOSED

GROUP(n=300)

Test Cell collected

during campaign.

Banner invite residing

in same area as

mobile ad invites

respondents to

participate in survey.

MOBILE EFFECTIVENESS Vs. OTHER CHANNELSCrossMedia Research

28

How can I optimise moving forward?

What was their cost efficiency?

What role did each channel play?

How did my campaign perform?

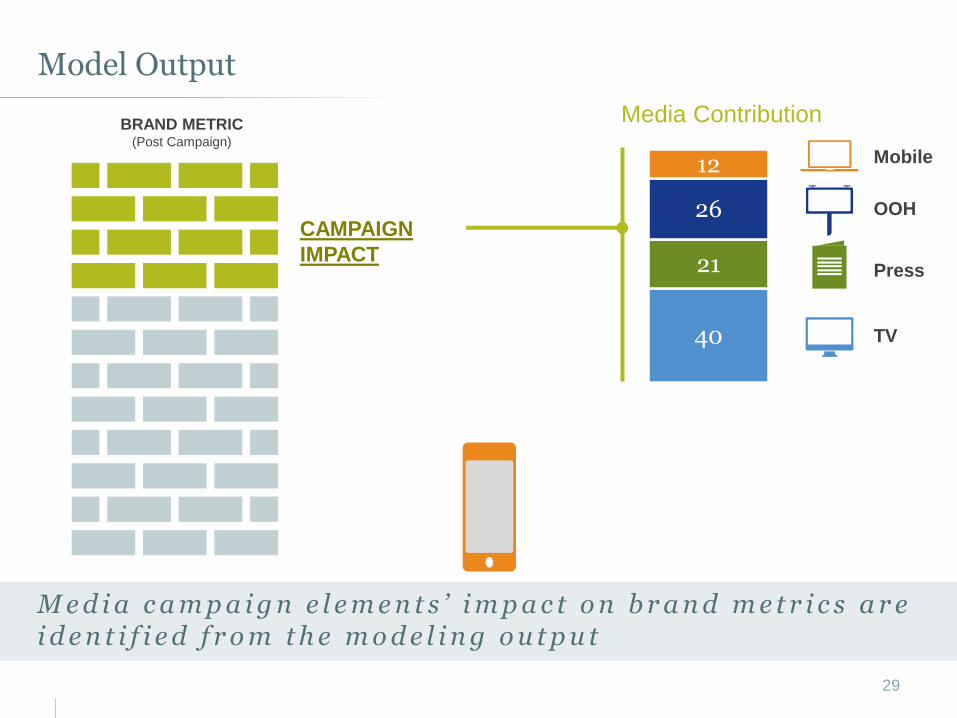

40

21

26

12

Model Output

29

M e d i a c a m p a i g n e l e m e n t s ’ i m p a c t o n b r a n d m e t r i c s a r e i d e n t i f i e d f r o m t h e m o d e l i n g o u t p u t

Media Contribution

Mobile

OOH

Press

TV

CAMPAIGN

IMPACT

BRAND METRIC(Post Campaign)

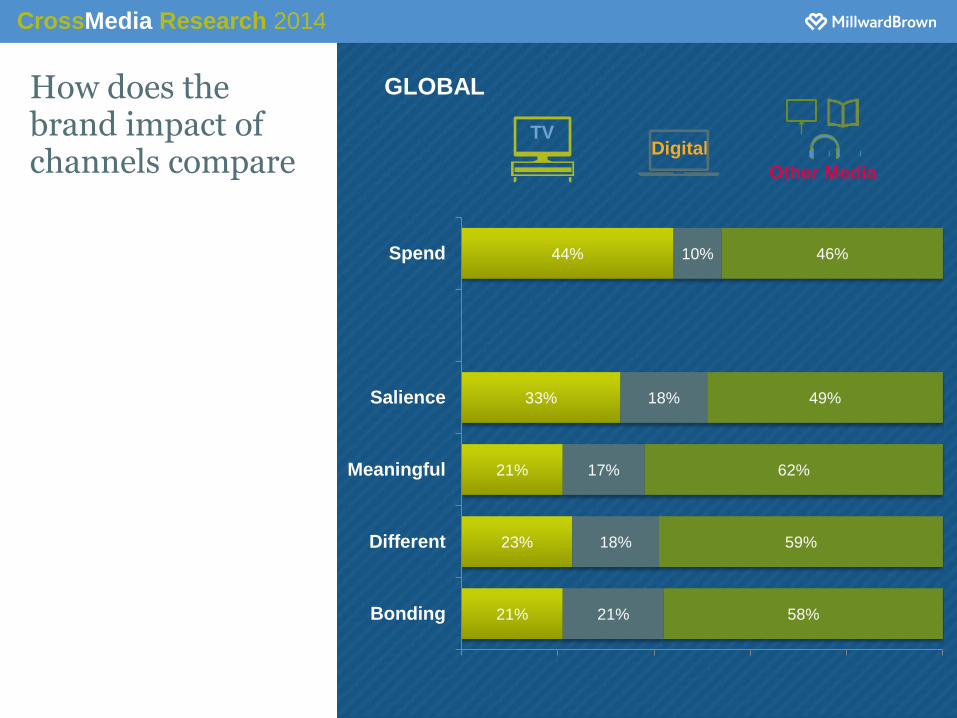

How does the brand impact of channels compare

DigitalTV

GLOBAL

21%

23%

21%

33%

44%

21%

18%

17%

18%

10%

58%

59%

62%

49%

46%

Bonding

Different

Meaningful

Salience

Spend

Other Media

CrossMedia Research 2014

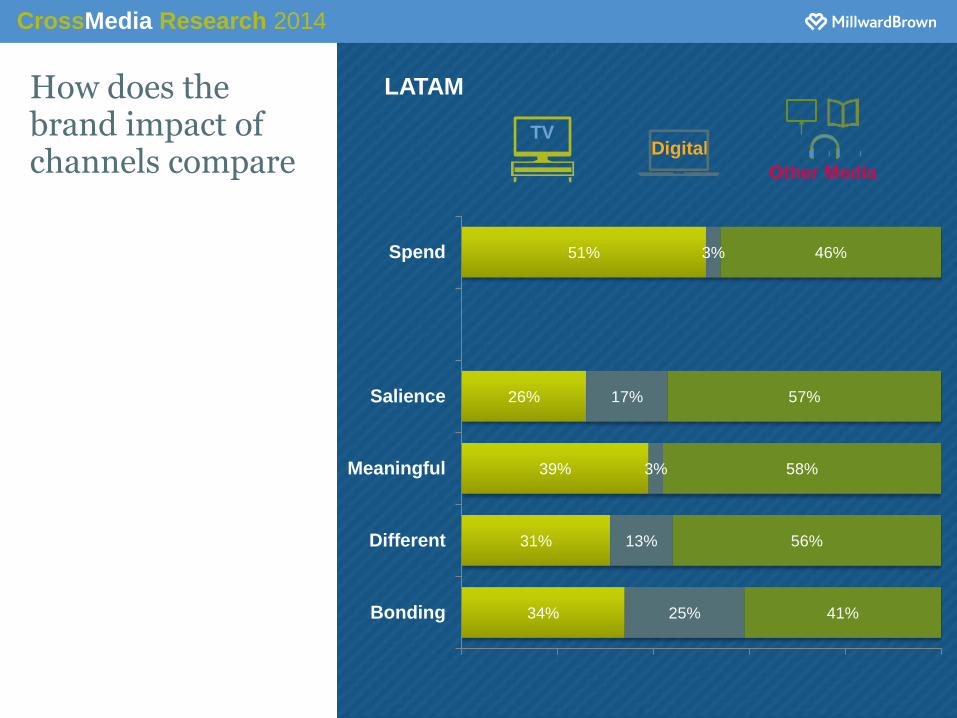

How does the brand impact of channels compare

DigitalTV

LATAM

34%

31%

39%

26%

51%

25%

13%

3%

17%

3%

41%

56%

58%

57%

46%

Bonding

Different

Meaningful

Salience

Spend

Other Media

CrossMedia Research 2014

WHAT SHOULD BRANDS DO?

AdReaction 2014

• The key to consumer interaction and

information exchange is now personal

mobile devices,

• Core consumer segments are going

mobile fast

• Brand Marketers need to follow them if

they wish to effectively grow their

brands in future

• But must test and learn more to

maximize impact and ROI of mobile

investments

#AdReaction

Thank you

James Galpin,

Head of Media & Digital, LATAM

www.millwardbrown.com/AdReaction

www.millwardbrown.com/BrandZ