Embed Size (px)

Citation preview

P O D C A S T I N GSounding out the opportunity

2

Gautham Iyer@iyer_gautham/in/GauthamVIyer

With input fromGimlet Media

3

Executive Summary

• Digitization of media continues; news and talk radio beginning to bedisrupted by emergence of podcasting

• Podcasting market is estimated at ~$90M in 2014, and is expected togrow at ~24% annual growth through 2020

• Individual podcasts can succeed through a combination of factorswhich have been leveraged by popular podcasts

• Podcasting economics potentially appealing

• Competitive landscape shows that content producers likely to see thehighest margins while aggregators and distributors see highest volume

Investment opportunitiesContent: Invest in producers w/ top talent

Aggreg/Distributors: Invest in Distribution networks

4

Digitization is causing significant changes across medialandscape

Traditional Digital

Shift from in-storepickup to on-

demand mail-in andstreaming modelV

ideo

Shift from real-timeTV viewing to on-demand TV, and

streamedproductionsTe

levi

sion

Shift from real-timeradio and physical

CDs to digitaldownloads and

streaming

Mu

sic

5

Disruption now impacting talk/news/public radio, wherepodcasts emerging as a new format

Traditional Digital

Shift from real-timetalk radio to on-

demand downloadand streaming model

New

s/Ta

lkR

adio

6

Podcast searches have increased over time, with topplayers like Serial fueling recent spikes

0

20

40

60

80

100

Indexed google searches within "Radio" category

Radiolab

Podcast

Serial

2010

-01

2010

-07

2011

-01

2011

-07

2012

-01

2012

-07

2013

-01

2013

-07

2014

-01

2014

-07

2015

-01

Invisibilia

Planet Money

Source: Google Analytics

7

Agenda

•Market overview

•Audience acquisition

•Economics

•Competitive Landscape

8

Podcasting has grown by ~25% over the last 5 years;growth expected to stay fairly consistent into 2020

0

100

200

300

400

0.0

0.1

0.2

0.3

0.4%

Estimated podcasting market spend ($M)

2010

43

2011

53

2012

58

2013

75

2014

90

2015

133

2016

167

2017

207

2018

256

2019

318

2020

395

25%

10-15ECAGR

24%

15E-20ECAGR

24 2422 11 29 19 48 25 24 24Y/y % marketgrowth

11 25 2713 13 15 18 20 21 22 24Average CPM ($)

26 91 10232 37 43 51 59 66 74 82Digital mediaspend ($B)

Share of digital media spend

Podcasting spend

Share of digitalmedia spend

Note: CPM price change estimated by applying change in Cost per Loyal User Index (measures cost of acquiring a loyal user for brands whoactively market their apps) to 2015 CPM costSources: CPM: Multiple press sources; Pricing change: Fiksu and Interactive Advertising Bureau

PRELIMINARY

9

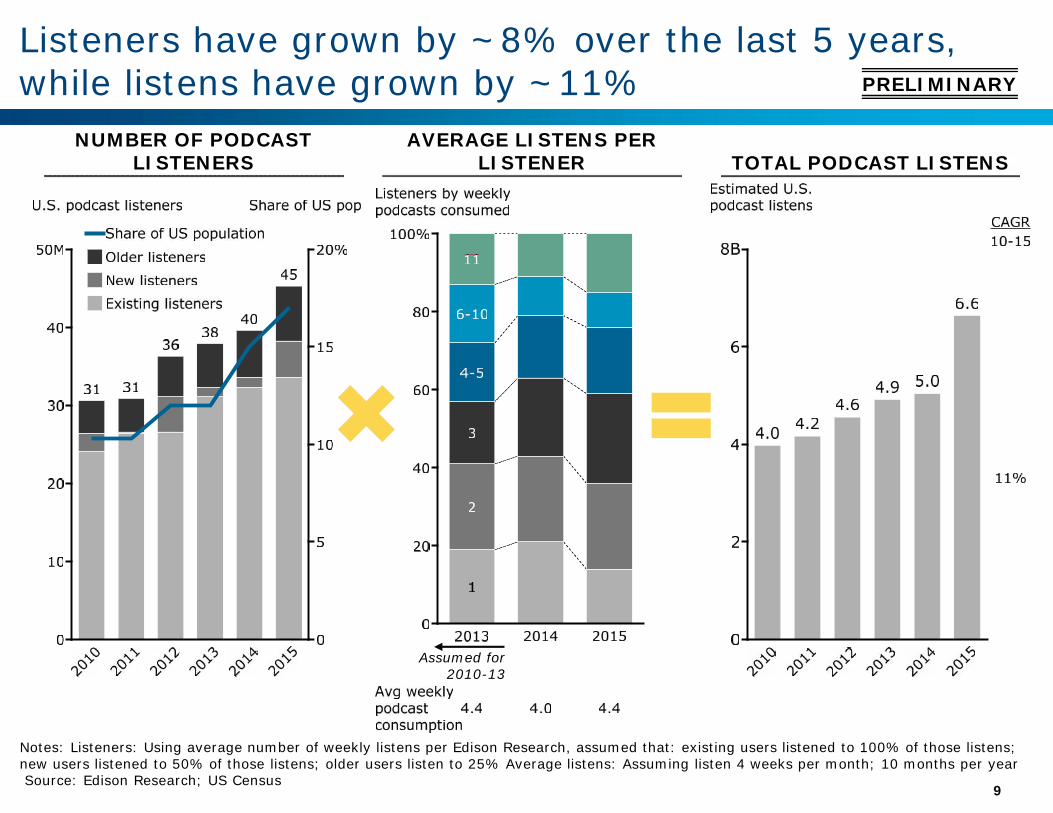

Listeners have grown by ~8% over the last 5 years,while listens have grown by ~11%

Notes: Listeners: Using average number of weekly listens per Edison Research, assumed that: existing users listened to 100% of those listens;new users listened to 50% of those listens; older users listen to 25% Average listens: Assuming listen 4 weeks per month; 10 months per yearSource: Edison Research; US Census

NUMBER OF PODCASTLISTENERS

AVERAGE LISTENS PERLISTENER TOTAL PODCAST LISTENS

Assumed for2010-13

PRELIMINARY

10

Under select scenarios, podcasting space could stayrelatively flat, or hit over 40% US penetration

0

200

400

600

800

1,000

Estimated podcasting market spend ($M)

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

25%

10-15ECAGR

48%

24%

2%

15-20ECAGR

24 2422 11 29 19 48 25 24 24Y/y % marketgrowth

11 25 2713 13 15 18 20 21 22 24Average CPM ($)

0.17 0.35 0.390.17 0.16 0.17 0.18 0.23 0.25 0.28 0.31Share of digitalmedia spend

Base

High

Low

Note: CPM price change estimated by applying change in Cost per Loyal User Index (measures cost of acquiring a loyal user for brands whoactively market their apps) to 2015 CPM costSources: CPM: Multiple press sources; Pricing change: Fiksu and Interactive Advertising Bureau

Base

11

Agenda

•Market overview

•Audience acquisition

•Economics

•Competitive Landscape

12

Podcasts have acquired listeners through several routes

Personality • Podcasts can grab initial share of viewers with well-knownradio personalities or celebrity hosts

Cross-promotion

• Featured segment of newer podcasts on popular podcastshas helped drive listeners to the new podcast

SocialMedia /Buzz

• Social media and buzz playing a more significant role indriving podcast growth

TraditionalMedia

• Discussion of podcasts in more mainstream media outletsdraws in newer listeners who may not have listened topodcasts before

Listpositioning

• Presence in the iTunes top 10 list has been significant factorin building listener base

13

Acquisition routes of recently successful podcasts

Fastestpodcast

in iTuneshistory toreach 5M

listens

Launchedin Top 5

of iTunes,remainsin top 40

Launched in fallof ‘14, about aa journalisticinvestigationinto a Baltimoremurder

Launched inSummer ‘14,the story oflaunching apodcastingcompany

Note: Article mentions determine through Factiva searches on: “Serial & podcast & Koenig” and “Startup & podcast & Blumberg”Source: Factiva

PERSONALITYCROSS-

PROMOTIONSOCIAL

MEDIA / BUZZTRADITIONAL

MEDIALIST

POSITIONING

• Hostedby SarahKoenig,produceron ThisAmericanLife (TAL)

• At least5 Serialoffshootpodcasts

• 185Ktwitterfollowers

• 387articlesfinal 3 mosof 2014

• Parody ofSerial onSNL

• 24 articlementionsin final 3months of2014

• Hostedby AlexBlumberg,15-yearpublicradioveteran

• Debuted10/3/14on TAL, apopularpodcast

• #2 iniTunesTop 10in May

• HoversaroundiTunesTop 20

• 21.3Kfollowerson twitter

• Featuredon TALsegmenton9/5/14

= Major contributor

Impact on audience acquisition= Moderate contributor = Minor contributor

14

Over time, public radio affiliated podcasts have retaineda strong presence in iTunes Top 10

1 SPONTANEANATIONwith Paul F. Tompkins This American Life This American Life This American Life This American Life This American Life

2 ESPN: Bill Don't Lie Radiolab from WNYCNPR Programs: WaitWait... Don't Tell Me!

Podcast

David Guetta -Nothing But The Beat,

The Movie

Stuff You ShouldKnow

Alvin And TheChipmunks: The

Squeakquel "Making aScene" Featurette

3 This American Life NPR: TED Radio HourPodcast WNYC's Radiolab

NPR Programs: WaitWait... Don't Tell Me!

PodcastFreakonomics Radio Freakonomics Radio

4 SerialNPR Programs: WaitWait... Don't Tell Me!

Podcast

NPR: TED Radio HourPodcast WNYC's Radiolab The Moth Podcast Stuff You Should

Know

5 Radiolab from WNYC The Moth Podcast Stuff You ShouldKnow Freakonomics Radio The Adam Carolla

ShowNPR: Wait Wait...

Don't Tell Me! Podcast

6 TED Radio Hour Welcome to NightVale The Moth Podcast NPR Programs: Fresh

Air Podcast WNYC's Radiolab NPR: Fresh AirPodcast

7Psychobabble with

Tyler Oakley & KoreyKuhl

Freakonomics RadioStarTalk Radio Show

by Neil deGrasseTyson » Shows

Stuff You ShouldKnow

NPR: Wait Wait...Don't Tell Me! Podcast

The Ricky GervaisPodcast

8 Invisibilia Stuff You ShouldKnow Norm Macdonald Live

Alvin and theChipmunks:

Chipwrecked: Behind-the-Scenes

NPR: Fresh AirPodcast

Real Time with BillMaher

9 Fresh Air NPR Programs: FreshAir Podcast Here's The Thing NPR: Car Talk Podcast ESPN: 1st and 10 WNYC's Radiolab

10 Wait Wait... Don't TellMe! The Nerdist The Joe Rogan

ExperienceThe Adam Carolla

Show Happy Tree Friends MacBreak WeeklyVideo (large)

RANK APRIL 2015 APRIL 2014 APRIL 2013 APRIL 2012 APRIL 2011 APRIL 2010

= Public radio/ affiliated = Entertainment = EducationalNote: Top 10 for the first of April, each yearSource: http://www.itunescharts.net/us/charts/podcasts/

15

Agenda

•Market overview

•Audience acquisition

•Economics

•Competitive Landscape

16

0

20

40

60

80

$100

Cost per thousand

Gener

al

displa

y

2

Mobile

3

Prem

ium

displa

y

10

YouT

ube

15

Video

25

Podc

ast

(Avg

)

30

Seria

l

40

Gimlet

100

0

5

10

15

$20

Estimated podcast CPM*

2010

11

2011

13

2012

13

2013

15

2014

18

2015

20

13%

10-15CAGR

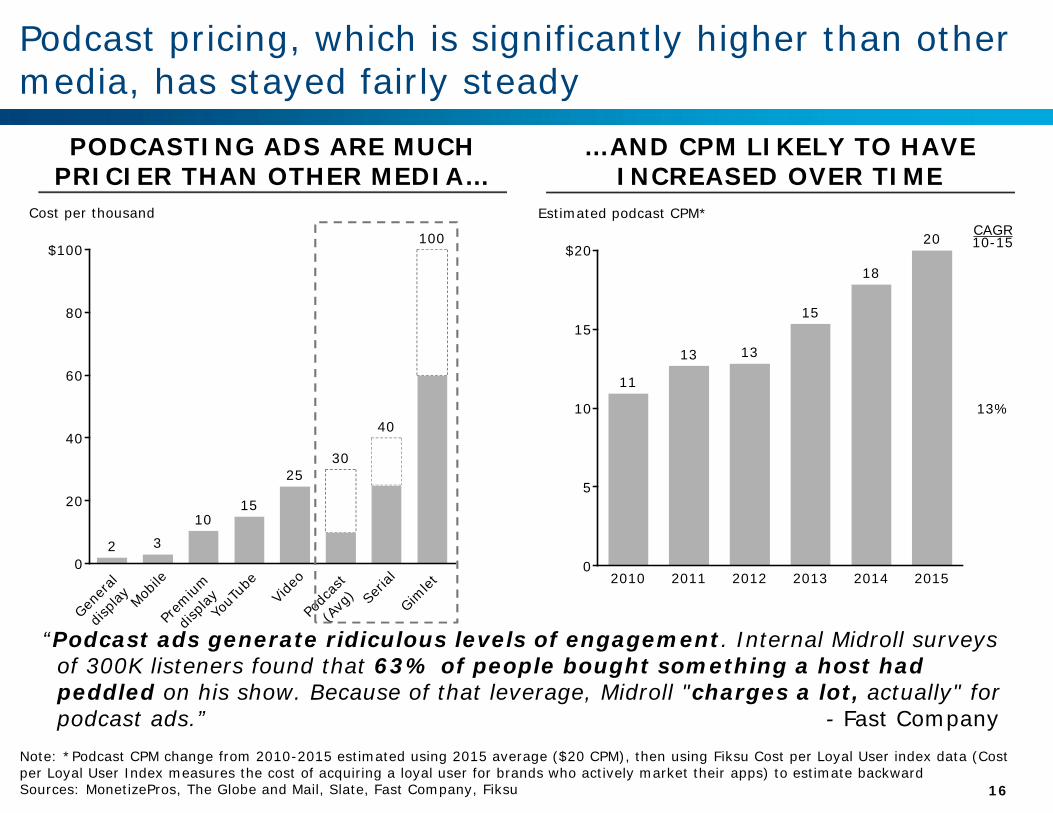

Podcast pricing, which is significantly higher than othermedia, has stayed fairly steady

PODCASTING ADS ARE MUCHPRICIER THAN OTHER MEDIA…

…AND CPM LIKELY TO HAVEINCREASED OVER TIME

“Podcast ads generate ridiculous levels of engagement. Internal Midroll surveysof 300K listeners found that 63% of people bought something a host hadpeddled on his show. Because of that leverage, Midroll "charges a lot, actually" forpodcast ads.” - Fast Company

Note: *Podcast CPM change from 2010-2015 estimated using 2015 average ($20 CPM), then using Fiksu Cost per Loyal User index data (Costper Loyal User Index measures the cost of acquiring a loyal user for brands who actively market their apps) to estimate backwardSources: MonetizePros, The Globe and Mail, Slate, Fast Company, Fiksu

17

Estimation of performance for “Serial” podcast showspotentially attractive margin opportunity

0

200

400

$600K

Serial podcast economics

Revenue

585

Ad salescomission

-176

RadioPersonality

Salaries

-150

Radio StaffSalaries

-75

Cost of datahosting/transfer

-48

OtherExpenses

-50

Margin

87

Note: Revenue: assumes 12 podcasts at 1.5M downloads at $33 CPM per listen; Ad sales commission: assumes 30% of gross revenues;Salaries: assumes 2 radio personalities and 3 radio staffers worked 50% of the year on ‘Serial’ podcast at $150K and $50K salaries,respectively; Cost of data hosting: assumes $4K monthly cost of data transferSources: http://www.business2community.com/content-marketing/serial-effect-podcasting-business-profitable-strategy-01124873;http://glog.glennf.com/blog/2014/11/23/show-me-the-numbers-serials-data-transfer-costs

ILLUSTRATIVE

~15%estimatedmargin for

Serial

Does not includeadditional

donations solicitedduring Season 1

18

Agenda

•Market overview

•Audience acquisition

•Economics

•Competitive Landscape

19

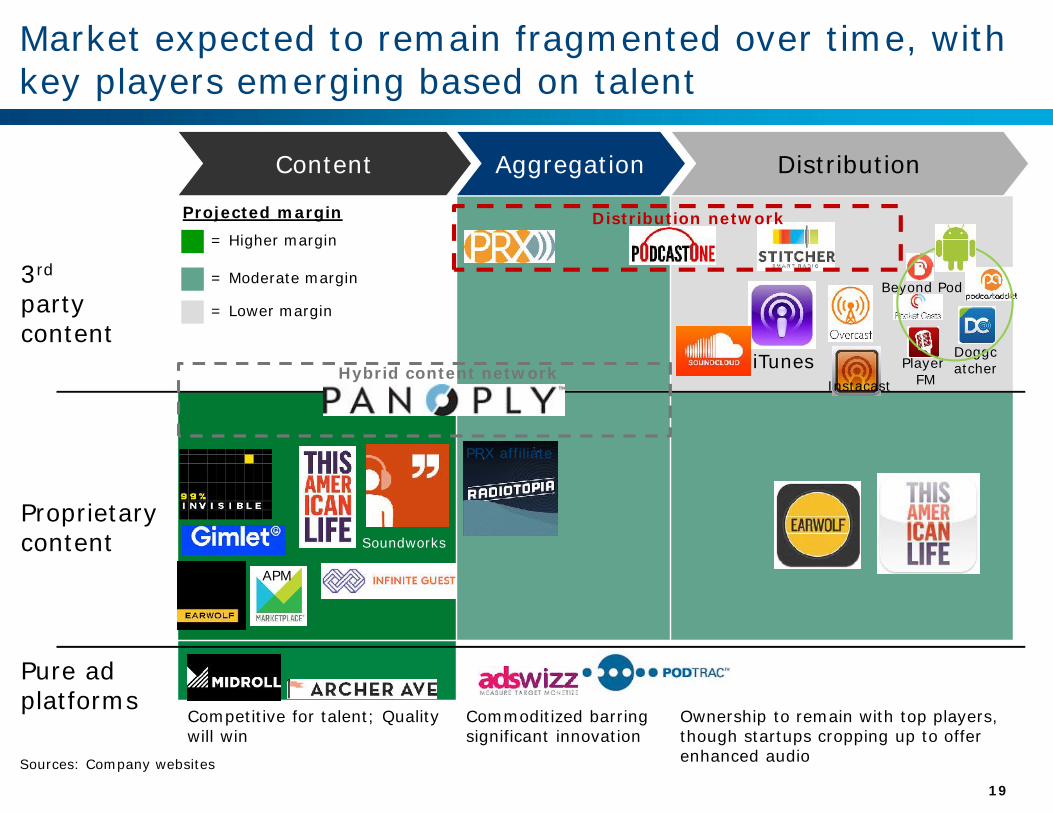

Competitive for talent; Qualitywill win

Commoditized barringsignificant innovation

Ownership to remain with top players,though startups cropping up to offerenhanced audio

Market expected to remain fragmented over time, withkey players emerging based on talent

Content Aggregation Distribution

iTunes

Beyond Pod

DoggcatcherPlayer

FM

PRX affiliate

Soundworks

APM

Proprietarycontent

3rd

partycontent

Pure adplatforms

InstacastHybrid content network

Distribution network= Higher margin

= Moderate margin

= Lower margin

Projected margin

Sources: Company websites

20

Backup

21

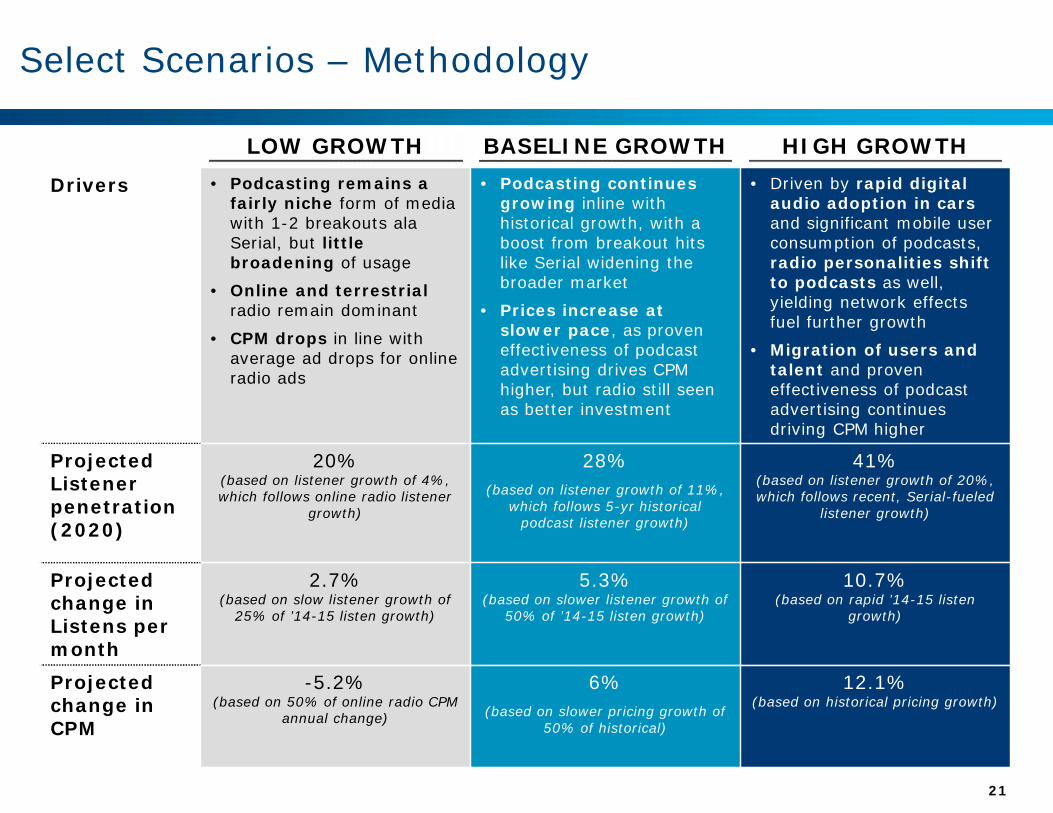

Select Scenarios – Methodology

Drivers • Podcasting remains afairly niche form of mediawith 1-2 breakouts alaSerial, but littlebroadening of usage

• Online and terrestrialradio remain dominant

• CPM drops in line withaverage ad drops for onlineradio ads

• Podcasting continuesgrowing inline withhistorical growth, with aboost from breakout hitslike Serial widening thebroader market

• Prices increase atslower pace, as proveneffectiveness of podcastadvertising drives CPMhigher, but radio still seenas better investment

• Driven by rapid digitalaudio adoption in carsand significant mobile userconsumption of podcasts,radio personalities shiftto podcasts as well,yielding network effectsfuel further growth

• Migration of users andtalent and proveneffectiveness of podcastadvertising continuesdriving CPM higher

ProjectedListenerpenetration(2020)

20%(based on listener growth of 4%,which follows online radio listener

growth)

28%(based on listener growth of 11%,

which follows 5-yr historicalpodcast listener growth)

41%(based on listener growth of 20%,which follows recent, Serial-fueled

listener growth)

Projectedchange inListens permonth

2.7%(based on slow listener growth of

25% of ’14-15 listen growth)

5.3%(based on slower listener growth of

50% of ’14-15 listen growth)

10.7%(based on rapid ’14-15 listen

growth)

Projectedchange inCPM

-5.2%(based on 50% of online radio CPM

annual change)

6%(based on slower pricing growth of

50% of historical)

12.1%(based on historical pricing growth)

LOW GROWTH BASELINE GROWTH HIGH GROWTH