Embed Size (px)

Citation preview

TV advertising’s killer chartsWhat every marketer should know

46 nickable chartsWith notes

Full Deck

Published: June 2015

Thinkbox is supported by 99% of UK broadcasting

Main shareholders

Associates & supporters

TV Killer Facts

03

01 TV is the best profit generator

02 TV is the lead effectiveness medium

TV has unbeatable scale and reach

05 TV is the most talked about media

06 Multi-screening brings viewers closer to content and brands

We spend more time with TV than any other media04

07 All TV ads can be response ads

08

TV is everywhere09TV is the emotional medium and builds brand fame 10

TV is the catalyst for other media

11 Handy slides

1. TV is the best profit generator

TV is the best profit generator

TV Radio Press Online Display Out of Home£0.00

£0.20

£0.40

£0.60

£0.80

£1.00

£1.20

£1.40

£1.60

£1.80

£2.00

£1.79 £1.52 £1.48

£0.91

£0.37

2008-2011

Pro

fit R

OI

Source: Payback 4, 2008-2011 & 2011-2014, Ebiquity

Payback 4 (2011-2014)

TV is vital for long term profit

TV Other brand Activation-20%

0%

20%

40%

60%

80%

100%

120%

140%

3+ year campaigns onlyA

vera

ge

up

lift i

n p

rofit

effe

cts

Source: ‘Advertising Effectiveness: the long and short of it’, 2013, IPA

We are starting to uncover the payback of TV sponsorship

…a word from our sponsor

Source: Payback 4, 2008-2014, Ebiquity. Retail & FMCG categories only

Ave

rage

Pro

fit R

OI

TV Spot TV Spon Press Radio OOH£0.00

£0.20

£0.40

£0.60

£0.80

£1.00

£1.20

£1.40

£1.60

£1.51

£0.87£0.70 £0.65

£0.50

Based on limited retail and FMCG only

2. TV is the lead effectiveness medium

TV is the lead effectiveness medium

TV Press Radio Online Display Out of Home0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%100%

52%

27%

13% 11%

Twice as effective ‘per impact’ as any other medium

Source: Payback 4, 2008-2011 & 2011-2014, Ebiquity

Effe

ctiv

ene

ss I

ndex

TV

Ind

ex =

100

Largest effects accumulate over time

Number of very large business effects

% Very large profit gains0

10

20

30

40

50

60

70

80

90

100

1 year2 year3+ yearsIn

de

x

Source: ‘Advertising Effectiveness: the long and short of it’, 2013, IPA

Nearly half of TV’s sales effects are delivered after the first year of investment

Year 1 Year 2 Year 3 Year 4 Year 50%

20%

40%

60%

80%

100%

Rev

enue

effe

ct a

s %

of

year

1

effe

ct

TV

The effects of TV are long lasting

Source: Payback 1, 2008, PriceWaterhouseCoopers

TV gives the best business results

TVRadio

Press

Posters

Internet

Sponsorship PR0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Incr

ea

se in

no

. of b

usi

ne

ss e

ffect

s

Source: ‘Advertising Effectiveness: the long and short of it’, 2013, IPA

TV is by far the most trusted form of advertising

37%

TV Set

12%

Newspapers

7%

7%

Radio

7%

Magazines

3% 3% 3%

Websites Search Social media Outdoor

Source: TV Nation, 2014, Ipsos Media CT/Thinkbox. Base: all adults 15+. Question: ‘in which, if any, of the following places are you most likely to find advertising that you trust?’

Media where you’re most likely to find advertising that you trust

3. TV has unbeatable scale and reach

TV has extremely high daily, weekly and monthly reach

Source: BARB, 2014, individuals, reach 1min+

Commercial TV reaches

71.4% of the population in a day

92.8% of the population in a week

98.2% of the population in a month

Commercial reach has remained stable over 5 years

Source: BARB, 2014, reach 1min+

Weekly reach %2010 2011 2012 2014

92.8

93.3

92.3

88.6

92.4

90

Individuals

Adults

ABC1 adults

16-34

Men

Kids

2013

Women 94.2

92.6 93.7 93.5 93.4

93.1 94 93.8 93.8

92.1 93.2 92.8 92.6

88.2 90.1 89.6 89.5

92.3 93 92.9 92.7

89.8 91.6 91.6 91.4

93.9 95 94.7 94.8

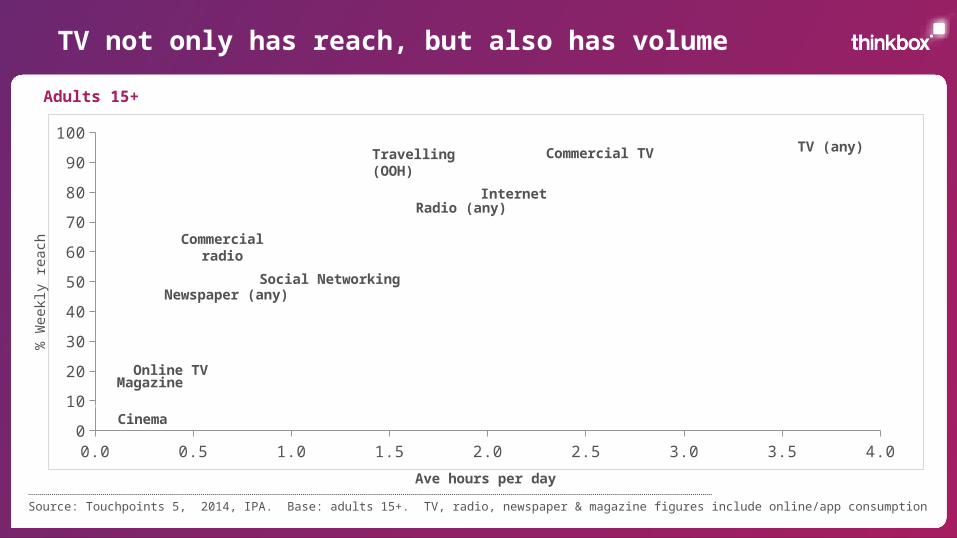

TV not only has reach, but also has volume

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.00

10

20

30

40

50

60

70

80

90

100TV (any)

Commercial radio

Travelling (OOH)

Social NetworkingNewspaper (any)

Magazine

Cinema

Ave hours per day

% W

eekl

y re

ach

Source: Touchpoints 5, 2014, IPA. Base: adults 15+. TV, radio, newspaper & magazine figures include online/app consumption

Online TV

Commercial TV

InternetRadio (any)

Adults 15+

4. We spend more time with TV than any other media

TV accounts for nearly half of people’s chosen media day

TV 48.0%

Radio 21.2%

Video clips/movies/music online 1.9%

Adults 15+

Includes only media which people choose to consume (i.e. excludes out of home)Source: Touchpoints 5, 2014, IPA. Base: adults 15+. TV, radio, newspaper & magazine figures include online/app consumption

Newspapers 3.9%

Magazines 0.6%Cinema 0.4%

• TV, radio, newspaper & magazine figures include online/app consumption

Other online activity 1.3%

Online games 1.1%

Online buying/product info/banking 1.6%

Online browsing/info seeking 4.6%

Internet for work 3.7%

Email 5.6%

Social networking/messaging 6.2%

TV accounts for over 40% of 15-24s chosen media day

TV 41.3%

Radio 13.1%

Adults 15-24

Newspapers 1.4%Magazines 0.4%

Cinema 1.0%

• TV, radio, newspaper & magazine figures include consumption via internet/appsOther online activity 1.5%

Online games 1.8%

Online buying/product info/banking 1.8%

Online browsing/info seeking 7.4%

Internet for work 3.2%

Email 5.4%

Social networking/messaging 15.7%

Video clips/movies/music online 6.3%

Includes only media which people choose to consume (i.e. excludes out of home)Source: Touchpoints 5, 2014, IPA. Base: adults 15-24. TV, radio, newspaper & magazine figures include online/app consumption

Total UK video consumption – all platforms & devices

Source: 2014, BARB / comScore / Broadcaster stream data / OFCOM Digital Day / IPA Touchpoints 5 / Rentrak

7.5%

6.9%

6.6%

3.7%

9.1%

6.9%

9.5%

48.8%

3.5%4.5%

4.6%

2.2%

3.8%

3.0%

10.9%

67.1%

YouTube

Other online video

Online 'adult' video

Cinema

Subscription VOD

DVD

Broadcaster VOD

Playback TV

Live TV

All Individuals: 4hrs, 20 mins

16-24s: 3hrs, 30 mins

All Individuals

16-24s

Average video time per day

0.4%

1.0%

Commercial TV Online (exc TV, radio, press)

Commercial Radio Newspapers Magazines Cinema

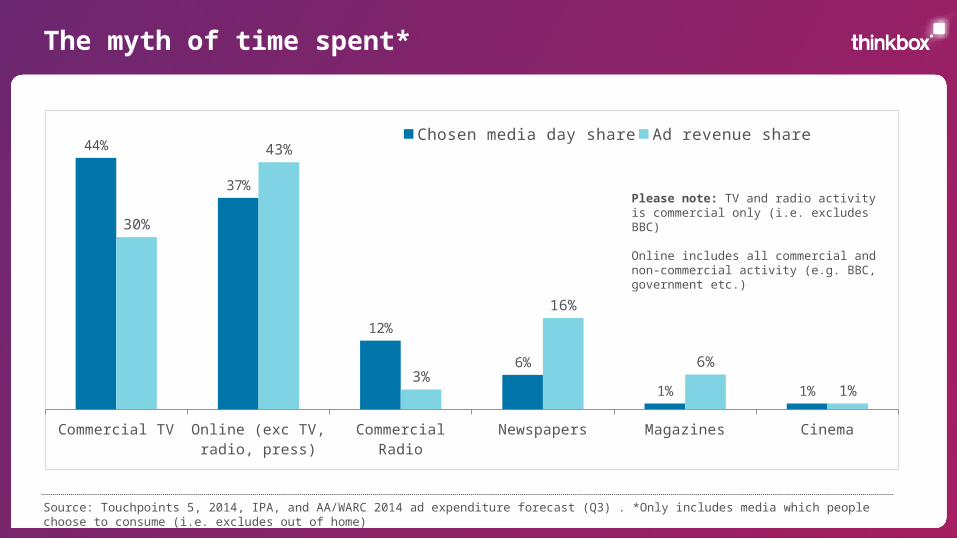

44%

37%

12%

6%

1% 1%

30%

43%

3%

16%

6%

1%

Chosen media day share Ad revenue share

The myth of time spent*

Source: Touchpoints 5, 2014, IPA, and AA/WARC 2014 ad expenditure forecast (Q3) . *Only includes media which people choose to consume (i.e. excludes out of home)

Please note: TV and radio activity is commercial only (i.e. excludes BBC)

Online includes all commercial and non-commercial activity (e.g. BBC, government etc.)

Average daily reach by half hour

6:0

0

6:3

0

7:0

0

7:3

0

8:0

0

8:3

0

9:0

0

9:3

0

10

:00

10

:30

11

:00

11

:30

12

:00

12

:30

13

:00

13

:30

14

:00

14

:30

15

:00

15

:30

16

:00

16

:30

17

:00

17

:30

18

:00

18

:30

19

:00

19

:30

20

:00

20

:30

21

:00

21

:30

22

:00

22

:30

23

:00

23

:30

0

5

10

15

20

25

30

35

40

45

50 TV Radio Newspaper Magazine Internet

Time of day

Source: Touchpoints 5, 2014, IPA. Base: adults 15+. TV, radio, newspaper & magazine figures include online/app consumption

% R

each

We watch 2 hours and 25 mins of commercial TV a day

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 20140.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

Non-commercial viewing Commercial viewing

No

. of h

ou

rs o

f TV

vie

we

d p

er

da

y

2 hrs 25 m

2 hrs 33 m

2 hrs 34 m

2 hrs 36 m

2 hrs 33 m

1 hr16 m

1 hr19 m

1 hr27 m

1 hr26 m

1 hr29 m

Source: BARB, 2004-2014. Base: individuals

4 hrs 2 m

4 hrs 2 m

4 hrs 1 m

3 hrs 52 m 3 hrs

41 m3 hrs 45 m

3 hrs 44 m

3 hrs 38 m

3 hrs 36 m

3 hrs 39m

3 hrs 42 m

2 hrs 16 m

1 hr26 m

2 hrs 16 m

1 hr23 m

2 hrs 15 m

1 hr21 m

2 hrs 16 m

1 hr22 m

2 hrs 22 m

1 hr22 m

2 hrs 24 m

1 hr21 m

Average person in the UK sees 45 TV ads a day

Source: BARB, 2004 – 2014. Base: individuals*digital switchover complete

Only includes ads viewed at normal speedDaily UK totals are now 2.65 billion TV ads seen every day

2004 2005 2006 2007 2008 2009 2010 2011 2012* 2013 2014

38 39 39 40 42 43 46 47 47 47 45

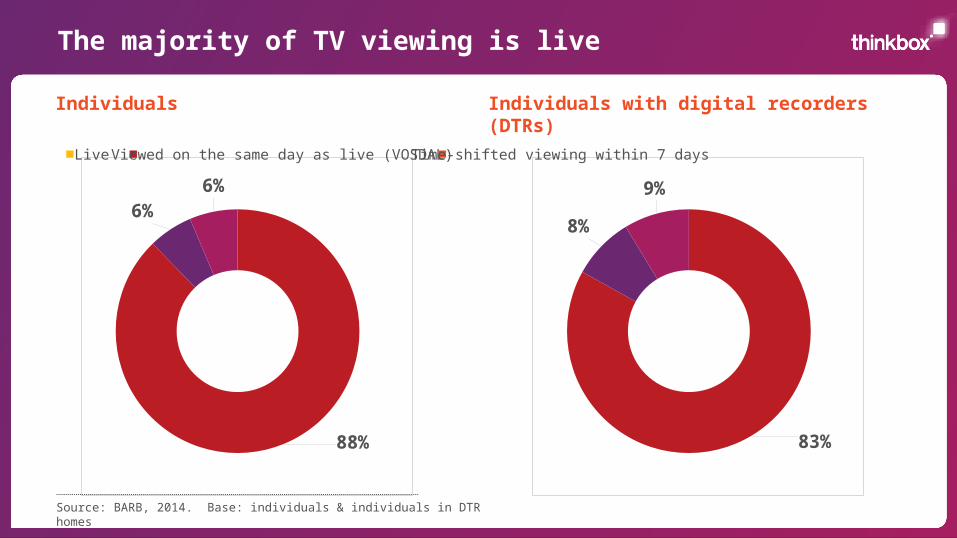

The majority of TV viewing is live

Source: BARB, 2014. Base: individuals & individuals in DTR homes

Individuals Individuals with DTRs

88%

6%6%

Individuals Individuals with digital recorders (DTRs)

83%

8%

9%

Live Viewed on the same day as live (VOSDAL) Time-shifted viewing within 7 days

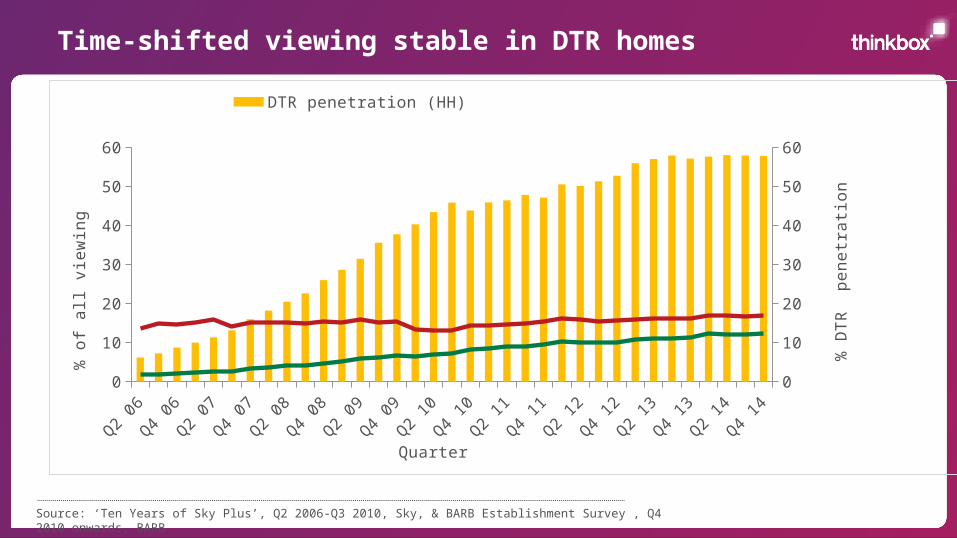

Time-shifted viewing stable in DTR homes

Source: ‘Ten Years of Sky Plus’, Q2 2006-Q3 2010, Sky, & BARB Establishment Survey , Q4 2010 onwards, BARB

Q2 06

Q4 06

Q2 07

Q4 07

Q2 08

Q4 08

Q2 09

Q4 09

Q2 10

Q4 10

Q2 11

Q4 11

Q2 12

Q4 12

Q2 13

Q4 13

Q2 14

Q4 14

0

10

20

30

40

50

60

0

10

20

30

40

50

60

DTR penetration (HH) % time-shifted viewing in DTR homes (inds)

% o

f all

vie

win

g

% D

TR

pe

ne

tra

tion

Quarter

Time-shifting is driven by programme genre not ad avoidance

Comm

ercia

l Dra

ma

inc.s

oaps

BBC Dra

ma

inc.s

oaps

Comm

ercia

l Doc

umen

tarie

s

BBC Doc

umen

tarie

s

Comm

ercia

l Film

s

BBC Film

s

Comm

ercia

l Ent

erta

inm

ent

BBC Ent

erta

inm

ent

Comm

ercia

l Kid

s

BBC Kid

s

Comm

ercia

l Spo

rt

BBC Spo

rt

Comm

ercia

l New

s

BBC New

s0%

10%20%30%40%50%60%70%80%90%

100%

65% 64%78% 80% 79% 82% 80% 81%

88% 89% 90% 91% 97% 97%

35% 36%22% 20% 21% 18% 20% 19%

12% 11% 10% 9% 3% 3%

Time-shifted Live

Source: BARB, 2014. Base: individuals in DTR homes, commercial TV vs. BBC

5. TV is the most talked about medium both on and offline

TV ads are the most talked about

Source: TV Nation, 2014, Ipsos Media CT/Thinkbox. Base: all adults 15+. Question: ‘On which medium are you likely to find advertising that you talk about either face to face or over the phone / online?’

On which medium are you likely to find advertising that you talk about…

TV Social networks

Newspapers Websites Online search

Radio Magazines Out of home0%

10%

20%

30%

40%

50%

60%

70%

58%

10% 9% 8% 8%5% 4% 3%

28%

11%

4%8%

5% 3% 3% 2%

Face to face / on the phoneOnline

TV advertising drives 51% of all marketing-generated conversations

Series10%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

9%

19%

51%

21%

Paid media TV Brand news, PR & events Product/serviceBase/market/seasonality

Influenced variables

Source: POETIC, 2013, Data2Decisions/Keller Fay/Thinkbox

6. Multi-screening brings viewers closer to content and brands

Multi-screening is a common activity

Source: TouchPoints 5, 2014, IPA. Base: adults 15+

25 mins Using internet while watching TV per day

6:0

06

:30

7:0

07

:30

8:0

08

:30

9:0

09

:30

10

:00

10

:30

11

:00

11

:30

12

:00

12

:30

13

:00

13

:30

14

:00

14

:30

15

:00

15

:30

16

:00

16

:30

17

:00

17

:30

18

:00

18

:30

19

:00

19

:30

20

:00

20

:30

21

:00

21

:30

22

:00

22

:30

23

:00

23

:30

0

5

10

15

20

25

30

35

40

45

50

Watching TV Watching TV and internet use Watching TV and social networking

Time

Ave

. da

ily %

of a

du

ltsMulti-screening usage patterns follow TV

Source: Touchpoints 5, 2014, IPA. Base: adults 15+ who have home internet access

Ad break multi-screeners are more likely to stay in front of ads

% agreeing with each statement

I just stayed where I was and waited for the programme to restart

I left the room during the ad breaks

I found myself watching the adverts almost by accident

57%

36%

35%

49%

41%

28%

Everyone elseMulti-screeners

Source: Screen Life: TV advertising everywhere, 2014, Craft/Thinkbox. Mobile diary 7pm-11pm.

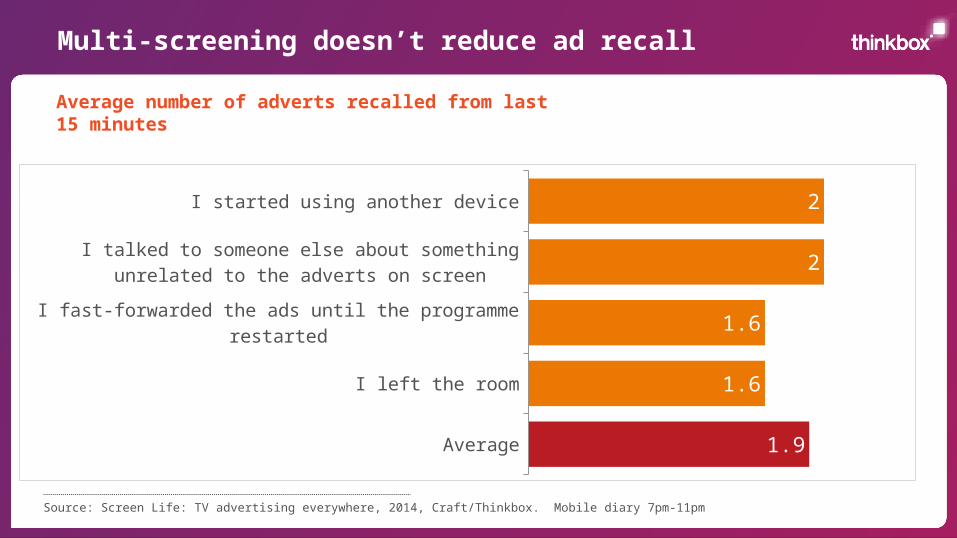

Multi-screening doesn’t reduce ad recall

Average number of adverts recalled from last 15 minutes

Average

I left the room

I fast-forwarded the ads until the programme restarted

I talked to someone else about something unrelated to the adverts on screen

I started using another device

1.9

1.6

1.6

2

2

Source: Screen Life: TV advertising everywhere, 2014, Craft/Thinkbox. Mobile diary 7pm-11pm

7. All TV ads can be response ads

TV is a catalyst for direct response

Source: POETIC, 2013, Data2Decisions/Keller Fay/Thinkbox. % of variables which can be influenced to drive website visits

69%of website visits are

generated by paid media

47%Of these 69% website visits

were generated by paid TV media

People welcome social elements within TV ad campaigns

52% welcome TV campaigns which carry a social media call to action

Source: Screen Life: TV advertising everywhere, 2014, Craft/Thinkbox. Base: individuals 16+

With Facebook and Twitter being the most desired platforms to be directed to

8. TV is the catalyst for other media

TV boosts other advertising channels

Reactive Interactive Active

TV is a multiplier of other awareness building channels

TV to radio is strongest and can be >100%

TV to press and OOH can be up to 50%

Branded search is 33% more responsive to TV in 2011-2014

TV to generic search on average +5% shift in conversion per 100 TVRs

TV helps drive significantly greater promotional effectiveness

Observed multiplier effects up to 100%

Source: Payback 4, 2011-2014, Ebiquity

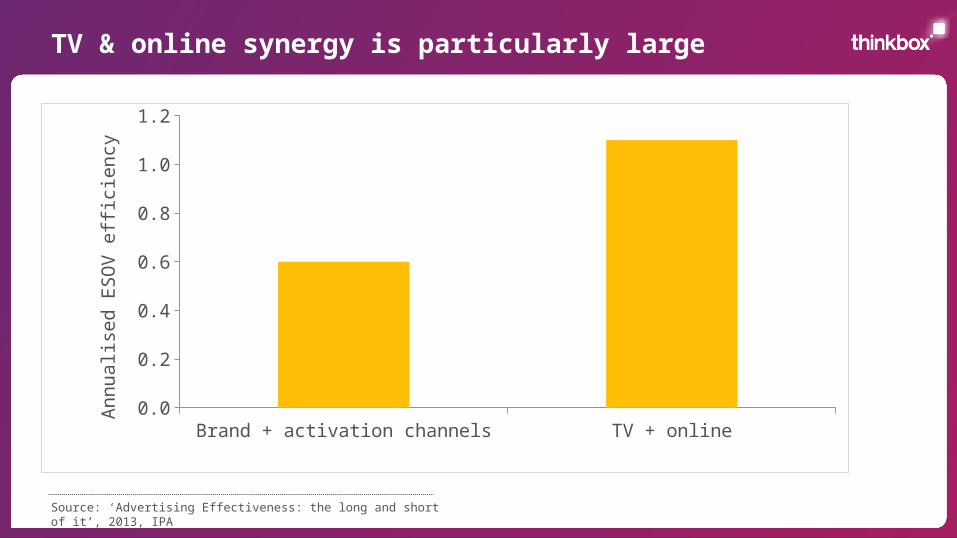

TV & online synergy is particularly large

Brand + activation channels TV + online0.0

0.2

0.4

0.6

0.8

1.0

1.2A

nn

ua

lise

d E

SO

V e

ffici

en

cy

Source: ‘Advertising Effectiveness: the long and short of it’, 2013, IPA

TV & online are great together…

Brand + activation channels

TV + online0.0

0.2

0.4

0.6

0.8

1.0

1.2

An

nu

alis

ed

ES

OV

effi

cie

ncy

Source: ‘Advertising Effectiveness: the long and short of it’, 2013, IPA

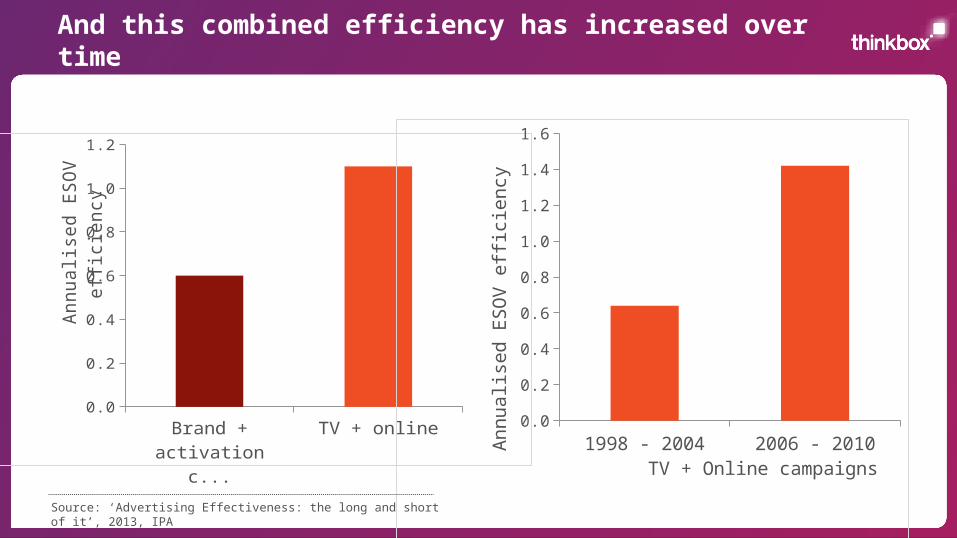

And this combined efficiency has increased over time

Brand + activation channels

TV + online0.0

0.2

0.4

0.6

0.8

1.0

1.2

An

nu

alis

ed

ES

OV

effi

cie

ncy

1998 - 2004 2006 - 20100.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

TV + Online campaigns

An

nu

alis

ed

ES

OV

effi

cie

ncy

Source: ‘Advertising Effectiveness: the long and short of it’, 2013, IPA

9. TV is everywhere

New devices enhance viewing and interaction

Source: Ipsos Tech Tracker, Q4 2014, adults 15+. Penetration figures (Laptop and Personal Computer, Any Tablet, Any Smartphone)

35% 63%65%

UK device penetration

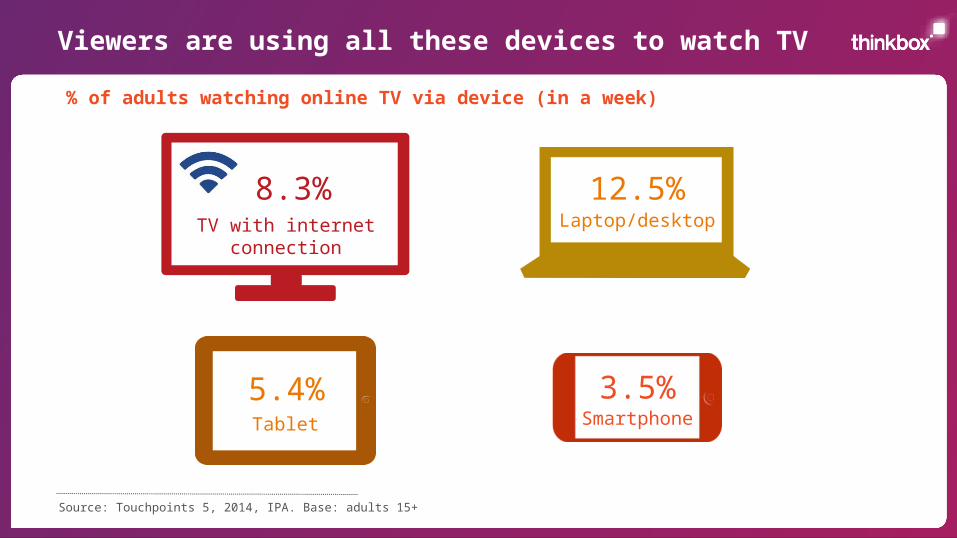

Viewers are using all these devices to watch TV

TV with internet connection

Laptop/desktop

Tablet Smartphone

8.3% 12.5%

5.4% 3.5%

Source: Touchpoints 5, 2014, IPA. Base: adults 15+

% of adults watching online TV via device (in a week)

TV viewing is expanding beyond the living room

Bathroom 9% Bedroom 46%

Kitchen 19% Living room 56% Study 24%

Garden 12%

Where people watch television via tablets, laptops and/or smartphones

Source: Screen Life: TV advertising everywhere, 2014, Craft/Thinkbox

TV is viewed in many places outside of the home

Usage of devices to watch TV out of home – location

Someone else's house

Public transport At work Public building In a car Travelling on business

0%

2%

4%

6%

8%

10%

12%

14%

5%

2%

4%3%

1%3%

8%7%

5% 5% 6%5%

11%

13%

9% 10%9%

7%

PC/Laptop Tablet Smartphone

Source: Screen Life: TV advertising everywhere, 2014, Craft/Thinkbox

Net: 17% Net: 13% Net: 12% Net: 10%Net: 13%Net: 16%

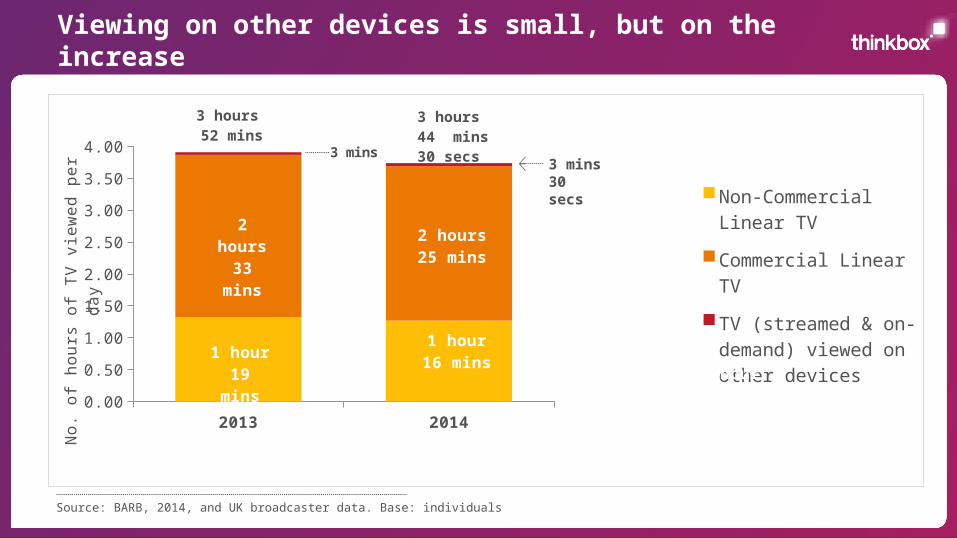

Viewing on other devices is small, but on the increase

Source: BARB, 2014, and UK broadcaster data. Base: individuals

2013 20140.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Non-Commercial Linear TV

Commercial Linear TV

TV (streamed & on-demand) viewed on other devices

No

. of h

ou

rs o

f TV

vie

we

d p

er

da

y

1 hour18 mins

3 hours 44 mins30 secs

2 hours 25 mins

1 hour16 mins

2 hours 33 mins

1 hour19 mins

3 hours 52 mins

3 mins3 mins 30 secs

10. TV is the emotional medium and builds brand fame

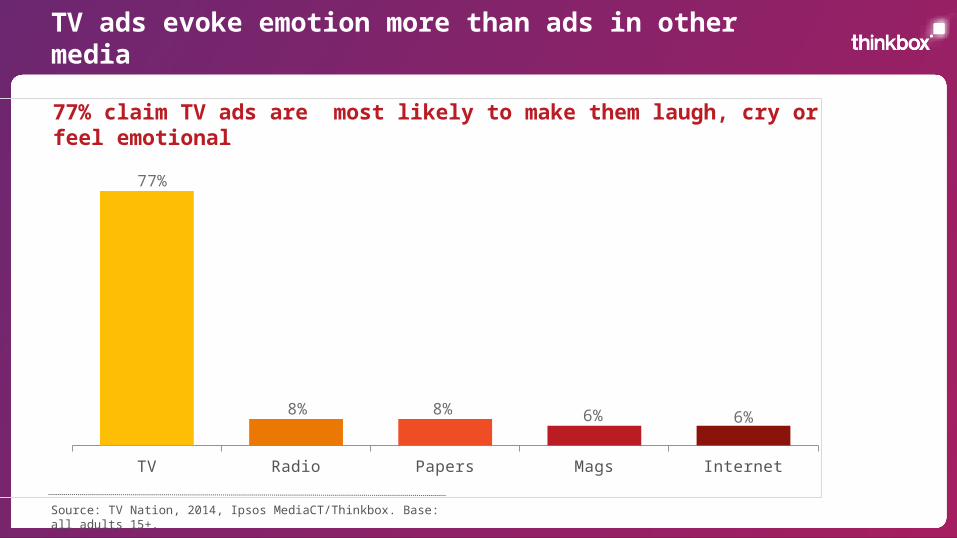

TV ads evoke emotion more than ads in other media

TV Radio Papers Mags Internet

77%

8% 8% 6% 6%

Source: TV Nation, 2014, Ipsos MediaCT/Thinkbox. Base: all adults 15+.

77% claim TV ads are most likely to make them laugh, cry or feel emotional

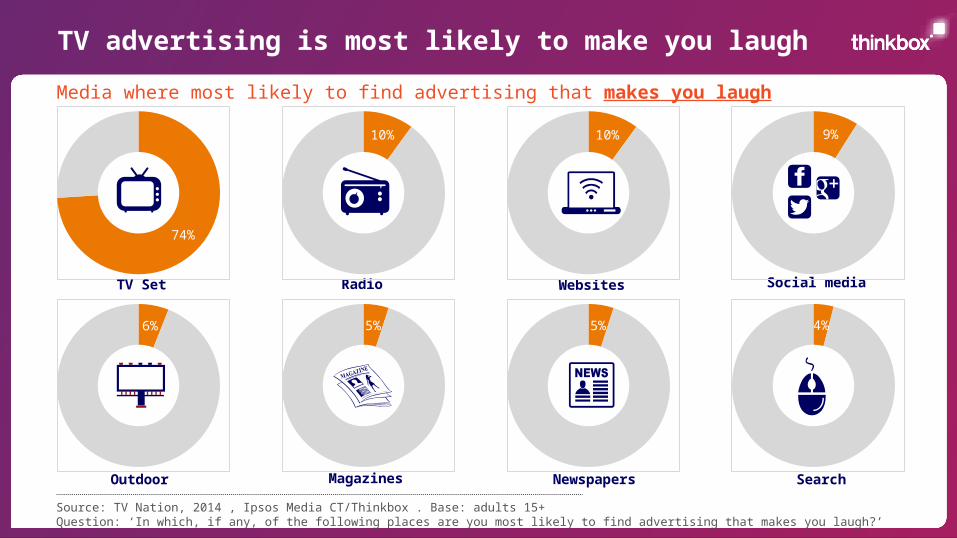

TV advertising is most likely to make you laugh

Source: TV Nation, 2014 , Ipsos Media CT/Thinkbox . Base: adults 15+Question: ‘In which, if any, of the following places are you most likely to find advertising that makes you laugh?’

Media where most likely to find advertising that makes you laugh

74%

TV Set Radio

Newspapers

Websites

Outdoor Magazines

Social media

Search

10% 10% 9%

6% 5% 5% 4%

Fame and emotion generate the most sales and profit

Sales Profit0%

10%

20%

30%

40%

50%

60%

70%

58%

39%

Fame

Emotive

Informative

Persuasive

Source: ‘Marketing in the Era of Accountability’, 2007, IPA

Emotive campaigns or ads which achieved fame 50% more likely to gain large business effects

Handy to know!

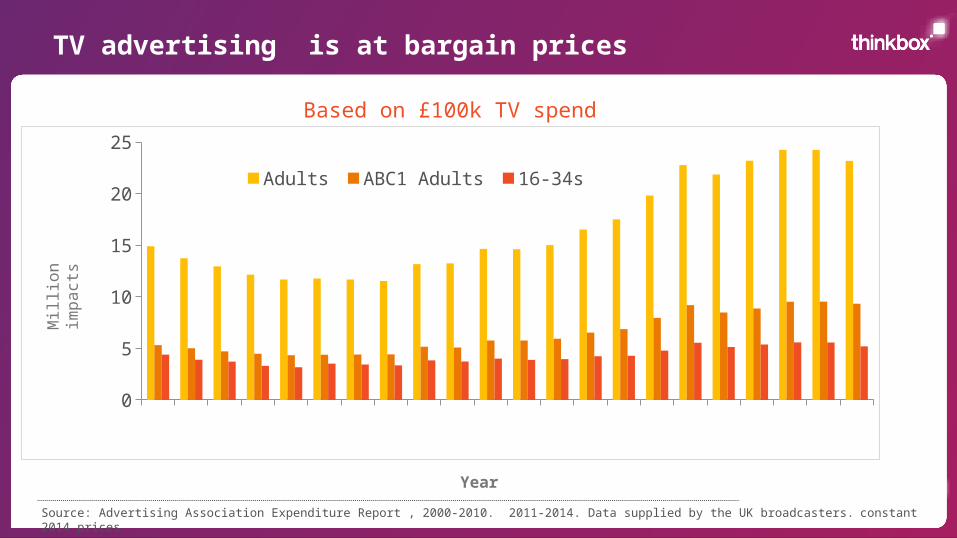

Source: Advertising Association Expenditure Report , 2000-2010. 2011-2014. Data supplied by the UK broadcasters. constant 2014 prices

TV advertising is at bargain prices

Based on £100k TV spend

19931994

19951996

19971998

19992000

20012002

20032004

20052006

20072008

20092010

20112012

20132014

0

5

10

15

20

25

Adults ABC1 Adults 16-34s

Year

Mill

ion

imp

act

s

Average TV view costs £0.05

Source: BARB, 2014, and data supplied by UK Broadcasters. Constant 2014 prices, based on average adults CPT

The average cost of buying the media space to get one person in the UK to see a TV advert only costs half a penny

An average broadcast TV campaign

of 400 TVRs in the UK gets

234 million views

Thank you.

www.thinkbox.tvHelping you get the best out of television