Embed Size (px)

Citation preview

Mobile Network Infrastructure Sharing

Industry overview and Coleago’s approach

Chris Buist, Director

May 2016

© copyright Coleago 2016

Data traffic and global initiatives to provide rural broadband coverage will be the future drivers

JVs between MNOs and tower sale-and-leaseback deals have taken

off since 2009. In the last few years some multinational MNOs have

started to establish captive tower companies. Sharing has also led

some shareholders to consider consolidation.

Looking forwards, new trends are likely to be rural/remote

infrastructure sharing and increased spectrum sharing. Technologies

such as NFV and SDN may open up new sharing opportunities.

To identify potential sharing options, operators need to consider five

dimensions: technology scope, geographical scope, architectural

scope, potential partners and sourcing.

Ultimately network sharing is driven by the need to maximise

Enterprise Value. The major benefit from network sharing is a net

reduction in network CapEx and OpEx, usually in the range from 10-

40% of the in-scope costs dependent on the sharing option. As with

any major programme, there are numerous risks that need to be

analysed and, where possible, mitigated.

1

Mobile Network Infrastructure Sharing

Network sharing has grown rapidly since 2009

There is no time to lose because there is clear evidence of a first-

mover advantage, or at least a last-mover disadvantage. For

passive/active sharing JVs, it is better to choose your preferred

partner than be handed a partner by default or, in the case of a three-

player market, left with no partner. Similarly, information from

completed tower sales shows that the first to market will command a

higher price than the followers.

Coleago’s approach is applicable regardless of the sharing option

selected. It is designed to work as well for a tower deal with a

TowerCo as it does for an active RAN share with another MNO.

Typically, it takes between 9 and 15 months for the first three phases

depending on the sharing option, regulatory approval(s), the need to

transfer assets and the willingness/ambition of the partners. The

Transformation phase may take several years to deliver all the

savings.

During the last decade our consultants have built up experience

across every type of sharing deal and all phases. We provide a

complete range of services to support or lead your project team

throughout the process.

First-mover advantage – operators need to act

Executive Summary

Mobile data traffic is

doubling every two

years. Revenues are

growing much more

slowly or even

falling. Financial

performance will

suffer unless

operators take action

to share infra-

structure or enter

into M&A.

In many emerging

markets, sharing is

also being driven by

limited spectrum

availability or

government ambition

to improve rural

broadband services

– the latter driven by

a plethora of global

initiatives led by the

UN, NGOs and

commercial entities

such as the GSMA.

• Internal & external analysis

• Business case

• Approach partner(s)

• Negotiate Heads of Agreement

Strategy

• Regulatory approval

• Design “To-Be”

• NegotiateAgreement(s)

• Conduct due diligence

Negotiation• Plan

• Establish JV

• Transfer staff, assets

• Implement processes, systems

Transition

• Depends on sharing scope

Transformation

© copyright Coleago 2016 2

Section: Page

1 Industry Status, Trends and Drivers 2

2 Potential Solutions, Benefits and Risks 7

3 Coleago’s Approach 14

4 Coleago’s Experience and Services 21

5 Why Coleago?

Appendix:

A Connecting the Unconnected: Rural/Remote Broadband Initiatives

B Network Sharing Database and Regional Indexes

C Tower Companies

D About Coleago

E Contacts

Co

nte

nts

Mobile Network Infrastructure Sharing

© copyright Coleago 2016

Global situation. Current and future trends. Key drivers.

Industry status, trends and drivers

3

1Mobile Network Infrastructure Sharing

© copyright Coleago 2016

Network sharing has grown rapidly since 2009

4

Mobile Network Infrastructure Sharing

1. Industry status, trends and drivers

Countries shaded

according to deal

with “deepest” extent

of sharing.

Status is based on

public

announcements to

end-2015.

Excludes national

roaming, MVNOs,

transmission-only,

captive tower

companies and

informal or

unannounced site

sharing deals.

© copyright Coleago 2016

Current and future trends in mobile network sharing

Current trends

Mobile network sharing is not new. It has been around for decades in one form or another, starting with national roaming and site sharing –usually encouraged or mandated by regulators to help new entrants.

Four trends have emerged since the millennium:

Network sharing Joint Ventures (JVs) between MNOs

Whereas site sharing started off in many markets as a mutual exchange involving a small percentage of sites, a JV can go much further to maximise the number of shared sites and cost savings, typically 25-40% of the in-scope costs. Furthermore the scope of radio access network (RAN) sharing has been extending from passive to active (MORAN) and, in some cases, to spectrum pooling/sharing (MOCN).

Tower sale-and-lease-back deals

By the end of 2015, some 45 operators had sold their towers to third parties (or formed joint ventures) and leased them back. The majority of these transactions have been in Africa but similar deals are now taking place in all other regions. Given their long-term secure cash flows and growth prospects, tower companies are attracting considerable Private Equity (PE) investment thereby facilitating further deals.

Captive tower companies

Separating passive infrastructure into a subsidiary may be beneficial from an operational efficiency perspective. It may also open up a range of alternative financing options including joint ventures, stock exchange flotation or eventually a sale. Recent examples include Airtel Africa, América Móvil (Telesites), Axiata (edotco), Telefónica (Telxius) and Telecom Italia (INWIT). It may explain some of the recent drop-off in sale-and-lease-back deals.

In-market consolidation

Undoubtedly discussions about sharing are leading some shareholders to be more radical and consider consolidation; Coleago believes that most markets will end up within the next five years with only three mobile operators and two (shared) RANs.

Future trends

Three further trends are expected to emerge over the next five years:

Rural/remote infrastructure sharing

Most MNOs have finished rolling out 2G, and in some cases 3G, coverage as far as is financially feasible. Any further roll-out will be slow and depend on GDP growth and unit cost reductions. Most governments have now developed national broadband plans, encouraged by the ITU and the Broadband Commission, that include objectives to provide broadband access to rural areas (see next page). Usually the only cost-effective solution to achieve such an objective is 3G or 4G infrastructure shared between two or more MNOs using active sharing or roaming.

Network Functions Virtualisation (NFV) and Software-Defined Networking (SDN)

NFV and SDN are emerging complementary technology developments that might enable and encourage further types of network sharing in the future, depending on how standards and OEM products/services evolve. In particular they may enable much greater core network sharing.

Spectrum sharing

There are currently 14 spectrum pooling/sharing (MOCN) joint ventures between MNOs. With mobile data traffic doubling every two years, MOCN deals are likely to increase but NRAs will still be under considerable pressure to release more spectrum. Some NRAs such as the FCC in the USA and Ofcom in the UK are evaluating advanced spectrum sharing using “lightly licensed” or unlicensed spectrum.

5

Mobile Network Infrastructure Sharing

1. Industry status, trends and drivers

More than 60% of

the deals to date are

RAN-sharing joint

ventures that

maximise savings.

Tower companies

are expanding

rapidly with the

backing of PE funds

but in the last few

years MNOs have

also started to

establish captive

tower companies.

Of the future trends,

rural/remote sharing

is probably the most

significant given the

sums involved and

the plethora of global

initiatives led by UN

bodies such as the

ITU, UNESCO and

the World Bank.

© copyright Coleago 2016

Drivers: EBITDA pressure, spectrum scarcity and government policy

What is driving the huge increase in sharing, tower sales and

consolidation? The uptick in sharing deals since 2009 has been due

almost exclusively to EBITDA pressure but this is set to change with

the global initiatives to provide rural/remote broadband coverage.

EBITDA pressure from competition and the data tsunami

EBITDA pressure has been and will continue to be the predominant

driver, be it as a result of revenue competition (new entrants, MVNOs

or OTT players), regulators reducing termination rates or international

roaming fees (Europe and Africa), or the rapid increase in mobile

data traffic. The latter is possibly the most significant, with data traffic

forecast to double every two years.

LTE roll-out has been the “burning platform” for numerous network

sharing deals. LTE creates two major cost pressures for an operator.

Initially it requires a major capital investment in licence/spectrum

fees, network elements and transmission, with a commensurate

increase in operating costs. Later, as take-up increases, LTE users

consume two to three times the amount of data compared to 3G

users, incurring further capital and operating expenditure but with

limited revenue upside.

Spectrum scarcity will be a driver in some markets

In many emerging markets with more than four mobile and fixed-

wireless operators, limited spectrum availability is causing operators

to evaluate MOCN sharing versus consolidation. Which direction they

choose to go will depend on government competition policy,

shareholder objectives and the business case.

Connecting the unconnected: rural/remote broadband initiatives

At the last count there were more than ten global initiatives with a

similar objective: to “connect the unconnected” or in other words to

provide broadband services in rural/remote areas to those who

currently don’t have access to the Internet. Putting aside the question

of how effective they are, there has undoubtedly been some progress

at the national level as most countries now have a national

broadband plan, although the quality of the plans and the

implementation progress to date are mixed to say the least. Similarly,

many government departments and regulators have realised that

mobile is the most cost-effective technology for such areas and that

infrastructure sharing is a key enabler. Consequently some

governments have become much more proactive about sharing and

have started to change their regulatory frameworks accordingly.

Yet the industry has not appreciated two of the key ingredients to

finding a solution for such remote areas:

All operators will need to actively share a single network

The government will also need to provide fiscal measures (e.g.,

tax changes, licence/spectrum fee reductions, USF funding, etc.)

Without this common understanding, progress will continue to be

slow and patchy.

6

Mobile Network Infrastructure Sharing

1. Industry status, trends and drivers

EBITDA pressure

has been and will

continue to be the

predominant driver.

Government policy

related to broadband

objectives for

rural/remote areas

will become

increasingly more

important over the

next five years.

Connecting the unconnected: making sense of the initiatives

See Appendix A

for further details

EBITDA: Earnings Before

Interest, Tax, Depreciation

and Amortisation

© copyright Coleago 2016

Five dimensions of network sharing. Maximising Enterprise Value. Common risks.

Potential solutions, benefits and risks

7

2Mobile Network Infrastructure Sharing

© copyright Coleago 2016

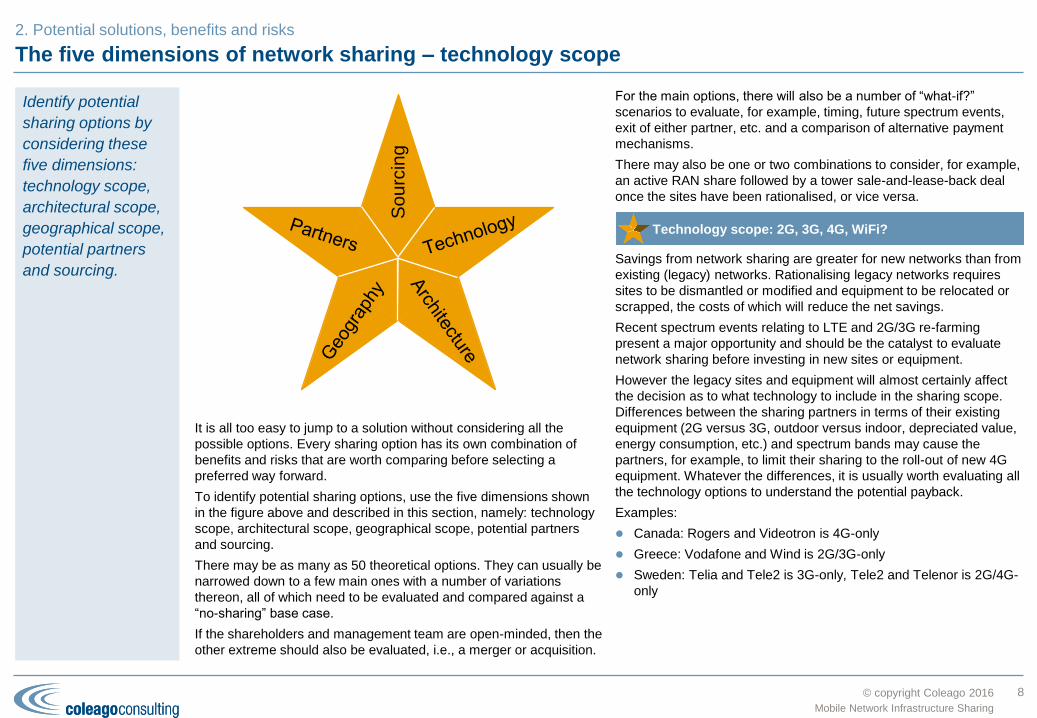

The five dimensions of network sharing – technology scope

It is all too easy to jump to a solution without considering all the

possible options. Every sharing option has its own combination of

benefits and risks that are worth comparing before selecting a

preferred way forward.

To identify potential sharing options, use the five dimensions shown

in the figure above and described in this section, namely: technology

scope, architectural scope, geographical scope, potential partners

and sourcing.

There may be as many as 50 theoretical options. They can usually be

narrowed down to a few main ones with a number of variations

thereon, all of which need to be evaluated and compared against a

“no-sharing” base case.

If the shareholders and management team are open-minded, then the

other extreme should also be evaluated, i.e., a merger or acquisition.

For the main options, there will also be a number of “what-if?”

scenarios to evaluate, for example, timing, future spectrum events,

exit of either partner, etc. and a comparison of alternative payment

mechanisms.

There may also be one or two combinations to consider, for example,

an active RAN share followed by a tower sale-and-lease-back deal

once the sites have been rationalised, or vice versa.

Savings from network sharing are greater for new networks than from

existing (legacy) networks. Rationalising legacy networks requires

sites to be dismantled or modified and equipment to be relocated or

scrapped, the costs of which will reduce the net savings.

Recent spectrum events relating to LTE and 2G/3G re-farming

present a major opportunity and should be the catalyst to evaluate

network sharing before investing in new sites or equipment.

However the legacy sites and equipment will almost certainly affect

the decision as to what technology to include in the sharing scope.

Differences between the sharing partners in terms of their existing

equipment (2G versus 3G, outdoor versus indoor, depreciated value,

energy consumption, etc.) and spectrum bands may cause the

partners, for example, to limit their sharing to the roll-out of new 4G

equipment. Whatever the differences, it is usually worth evaluating all

the technology options to understand the potential payback.

Examples:

Canada: Rogers and Videotron is 4G-only

Greece: Vodafone and Wind is 2G/3G-only

Sweden: Telia and Tele2 is 3G-only, Tele2 and Telenor is 2G/4G-

only

8

Mobile Network Infrastructure Sharing

Identify potential

sharing options by

considering these

five dimensions:

technology scope,

architectural scope,

geographical scope,

potential partners

and sourcing.

2. Potential solutions, benefits and risks

Technology scope: 2G, 3G, 4G, WiFi?

So

urc

ing

© copyright Coleago 2016

The five dimensions of network sharing – architectural scope

9

Mobile Network Infrastructure Sharing

2. Potential solutions, benefits and risks

The table at right shows the main architectural models for network

sharing.

Undoubtedly active sharing provides the greatest total savings.

However it is important to understand the incremental benefit over

the other models particularly given variations in some of the other

network sharing dimensions, e.g., potential partners and sourcing.

If the two potential partners are about to invest in new RAN

equipment to introduce new technology (3G or 4G), then an active

share becomes much more attractive.

Less than 10% of network sharing deals involve spectrum sharing or

pooling (MOCN) for a variety of reasons, such as:

Both partners have sufficient spectrum for their needs (capacity

and broadband speed) taking into account features such as

carrier aggregation

One partner has a spectrum advantage and is unwilling to share it

for competitive reasons

The regulator is unwilling to sanction spectrum trading or sharing.

As mobile data traffic continues to grow, regulators will be pressured

to release more spectrum. In some markets, spectrum pooling may

be one of the solutions to this demand.

To date there are no Core Network (GWCN) sharing deals because

regulators have strongly opposed such arrangements for reasons of

competition. However, developments in NFV and SDN may change

this situation and therefore sharing agreements should recognise this

potential future change in scope.

Examples:

Bangladesh: Airtel and Telenor (Grameenphone) is passive

Denmark: Telenor and Telia is active (MOCN)

UK: EE and Hutchison is active (MORAN)

MORAN: Multi-Operator Radio Access Network

MOCN: Multi-Operator Core Network

GWCN: Gateway Core Network

MVNO: Mobile Virtual Network Operator

Architectural scope

Architectural

Model

Sit

e

An

ten

nas &

feed

ers

RA

N e

lem

en

ts

Tra

nsm

issio

n

(backh

au

l)

Sp

ectr

um

Co

re n

etw

ork

ele

men

ts

Tra

nsm

issio

n

(backb

on

e)

Passive

Active RAN

Transmission

Core Network

(GWCN)

National

Roaming

Full MVNO

Thin MVNO

MORAN

MOCN

© copyright Coleago 2016

The five dimensions of network sharing – geographical scope and potential partners

Urban areas usually present more valuable opportunities than rural

areas for competitive differentiation in terms of network quality, in-

building coverage, service features, etc. and so it often makes

strategic sense not to share in such areas – but where to draw the

line?

For the same reason, regulatory or competition authorities may

impose a limit on the geographical extent of network sharing; in

Sweden, Telenor and Hutchison were only allowed to share their 3G

RANs up to a maximum 70% population coverage (since relaxed).

CapEx and OpEx differ between rural (typically towers) and urban

(typically rooftop) sites resulting in different payback periods and

NPV. Urban sites may also present difficulties in terms of space

availability, radiation limits, planning restrictions, etc.

Given the emerging trend to extend broadband coverage to

rural/remote areas (see page 6), it may be necessary to consider

different sharing arrangements for urban, rural and remote areas.

Taking a theoretical example of a country with four MNOs, it might

end up with two MNOs sharing in the urban and rural areas, the other

two MNOs only sharing in rural areas and all four MNOs sharing in

the remote areas.

Geography is also an important aspect when considering the

sourcing dimension (next page). An approach used in some sharing

deals is to partition the country between the parties for design, build

and O&M, for example, Vodafone and O2 in the UK.

Other examples:

Finland: Telia and DNA is rural-only, equating to 50% land area

and 15% of the population

France: SFR and Bouygues is rural-only, equating to 57% of the

population

Greece: Vodafone and Wind is rural and limited selected urban

areas, equating to 70% of rural and 40% of urban population

10

Mobile Network Infrastructure Sharing

Geographical scope

There may only be a few potential MNO partners or tower companies

from which to choose but you still need to evaluate their fit against a

number of criteria (see chart above). High-level examples of the

evaluation criteria include:

Commercial fit: for example, market share, competitive

differentiation (including brand)

Technical fit: in terms of spectrum (and therefore site grid),

technologies, vendors and MS providers

Cultural fit: experience from any existing relationship,

management styles, corporate values, etc.

Ownership: international versus local, public versus private,

shareholder ambitions, etc.

Note that the evaluation score of a potential partner may differ

according to the sharing option being evaluated.

Potential partners

2. Potential solutions, benefits and risks

© copyright Coleago 2016

The five dimensions of network sharing – sourcing

11

Mobile Network Infrastructure Sharing

2. Potential solutions, benefits and risks

Joint Venture (JV) JV outsources to MSP

JV outsources geographically to Partners Unilateral or Bilateral

For active sharing and some passive sharing deals, a 50:50 JV is the norm. It will be the overall authority for designing, building and operating the shared network. However responsibility for any of these activities may be undertaken by the JV itself or outsourced, possibly on a geographical basis, to:

The JV partners: one or both of the partners may be the best solution for delivering some of the scope, for example, each partner could take responsibility for designing and building the shared network in different geographical areas with the JV

responsible for overall design authority, programme management and O&M

Managed Service (MS) provider(s): one or more MS providers may be part of the solution; their contract(s) could also be extended to include the (unshared) legacy networks, thereby providing benefits beyond the network sharing itself.

By its nature, roaming is a unilateral or bilateral arrangement.

© copyright Coleago 2016

Ultimately network sharing is driven by the need to maximise Enterprise Value

12

Mobile Network Infrastructure Sharing

2. Potential solutions, benefits and risks

Network sharing’s

impact on Enterprise

Value (EV) is

primarily through a

net reduction in

network CapEx and

OpEx, which in turn

improves EBITDA,

ROCE and the EV.

EBITDA: Earnings Before

Interest, Tax, Depreciation and

Amortisation

ROCE: Return on Capital

Employed

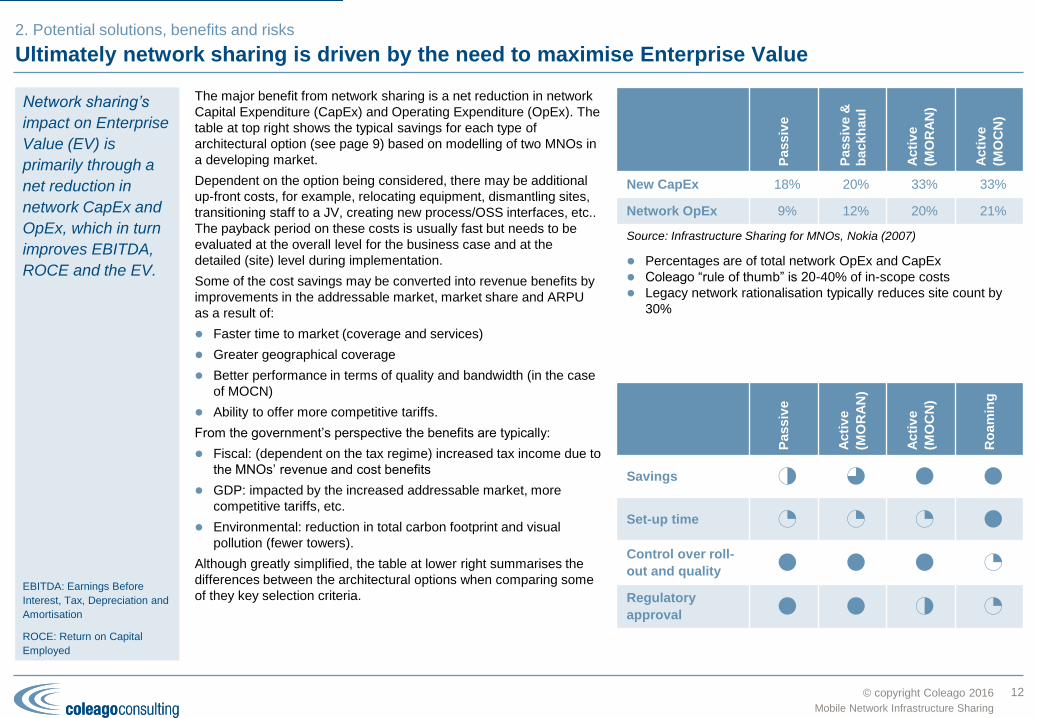

The major benefit from network sharing is a net reduction in network

Capital Expenditure (CapEx) and Operating Expenditure (OpEx). The

table at top right shows the typical savings for each type of

architectural option (see page 9) based on modelling of two MNOs in

a developing market.

Dependent on the option being considered, there may be additional

up-front costs, for example, relocating equipment, dismantling sites,

transitioning staff to a JV, creating new process/OSS interfaces, etc..

The payback period on these costs is usually fast but needs to be

evaluated at the overall level for the business case and at the

detailed (site) level during implementation.

Some of the cost savings may be converted into revenue benefits by

improvements in the addressable market, market share and ARPU

as a result of:

Faster time to market (coverage and services)

Greater geographical coverage

Better performance in terms of quality and bandwidth (in the case

of MOCN)

Ability to offer more competitive tariffs.

From the government’s perspective the benefits are typically:

Fiscal: (dependent on the tax regime) increased tax income due to

the MNOs’ revenue and cost benefits

GDP: impacted by the increased addressable market, more

competitive tariffs, etc.

Environmental: reduction in total carbon footprint and visual

pollution (fewer towers).

Although greatly simplified, the table at lower right summarises the

differences between the architectural options when comparing some

of they key selection criteria.

Passiv

e

Acti

ve

(MO

RA

N)

Acti

ve

(MO

CN

)

Ro

am

ing

Savings 2 3 4 4

Set-up time 1 1 1 4

Control over roll-

out and quality4 4 4 1

Regulatory

approval4 4 2 1

Passiv

e

Passiv

e &

backh

au

l

Acti

ve

(MO

RA

N)

Acti

ve

(MO

CN

)

New CapEx 18% 20% 33% 33%

Network OpEx 9% 12% 20% 21%

Percentages are of total network OpEx and CapEx

Coleago “rule of thumb” is 20-40% of in-scope costs

Legacy network rationalisation typically reduces site count by

30%

Source: Infrastructure Sharing for MNOs, Nokia (2007)

© copyright Coleago 2016

Maximising the savings by combining tower sales, active sharing and outsourcing deals

13

Mobile Network Infrastructure Sharing

2. Potential solutions, benefits and risks

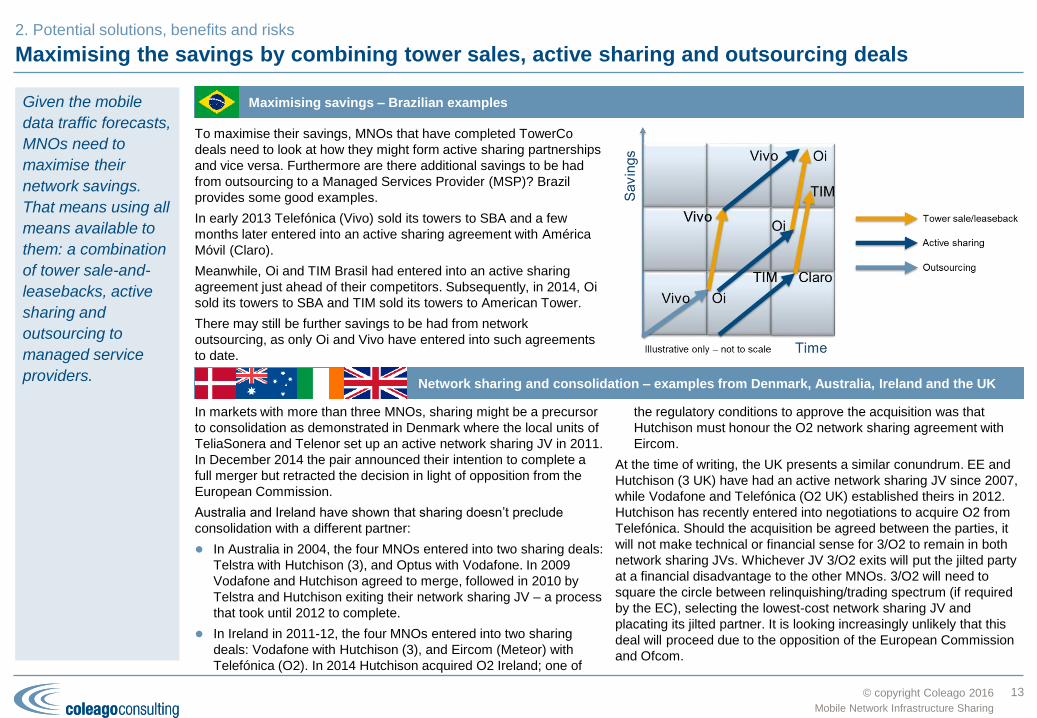

To maximise their savings, MNOs that have completed TowerCo

deals need to look at how they might form active sharing partnerships

and vice versa. Furthermore are there additional savings to be had

from outsourcing to a Managed Services Provider (MSP)? Brazil

provides some good examples.

In early 2013 Telefónica (Vivo) sold its towers to SBA and a few

months later entered into an active sharing agreement with América

Móvil (Claro).

Meanwhile, Oi and TIM Brasil had entered into an active sharing

agreement just ahead of their competitors. Subsequently, in 2014, Oi

sold its towers to SBA and TIM sold its towers to American Tower.

There may still be further savings to be had from network

outsourcing, as only Oi and Vivo have entered into such agreements

to date.

Maximising savings – Brazilian examples

In markets with more than three MNOs, sharing might be a precursor

to consolidation as demonstrated in Denmark where the local units of

TeliaSonera and Telenor set up an active network sharing JV in 2011.

In December 2014 the pair announced their intention to complete a

full merger but retracted the decision in light of opposition from the

European Commission.

Australia and Ireland have shown that sharing doesn’t preclude

consolidation with a different partner:

In Australia in 2004, the four MNOs entered into two sharing deals:

Telstra with Hutchison (3), and Optus with Vodafone. In 2009

Vodafone and Hutchison agreed to merge, followed in 2010 by

Telstra and Hutchison exiting their network sharing JV – a process

that took until 2012 to complete.

In Ireland in 2011-12, the four MNOs entered into two sharing

deals: Vodafone with Hutchison (3), and Eircom (Meteor) with

Telefónica (O2). In 2014 Hutchison acquired O2 Ireland; one of

the regulatory conditions to approve the acquisition was that

Hutchison must honour the O2 network sharing agreement with

Eircom.

At the time of writing, the UK presents a similar conundrum. EE and

Hutchison (3 UK) have had an active network sharing JV since 2007,

while Vodafone and Telefónica (O2 UK) established theirs in 2012.

Hutchison has recently entered into negotiations to acquire O2 from

Telefónica. Should the acquisition be agreed between the parties, it

will not make technical or financial sense for 3/O2 to remain in both

network sharing JVs. Whichever JV 3/O2 exits will put the jilted party

at a financial disadvantage to the other MNOs. 3/O2 will need to

square the circle between relinquishing/trading spectrum (if required

by the EC), selecting the lowest-cost network sharing JV and

placating its jilted partner. It is looking increasingly unlikely that this

deal will proceed due to the opposition of the European Commission

and Ofcom.

Network sharing and consolidation – examples from Denmark, Australia, Ireland and the UK

Given the mobile

data traffic forecasts,

MNOs need to

maximise their

network savings.

That means using all

means available to

them: a combination

of tower sale-and-

leasebacks, active

sharing and

outsourcing to

managed service

providers.

© copyright Coleago 2016

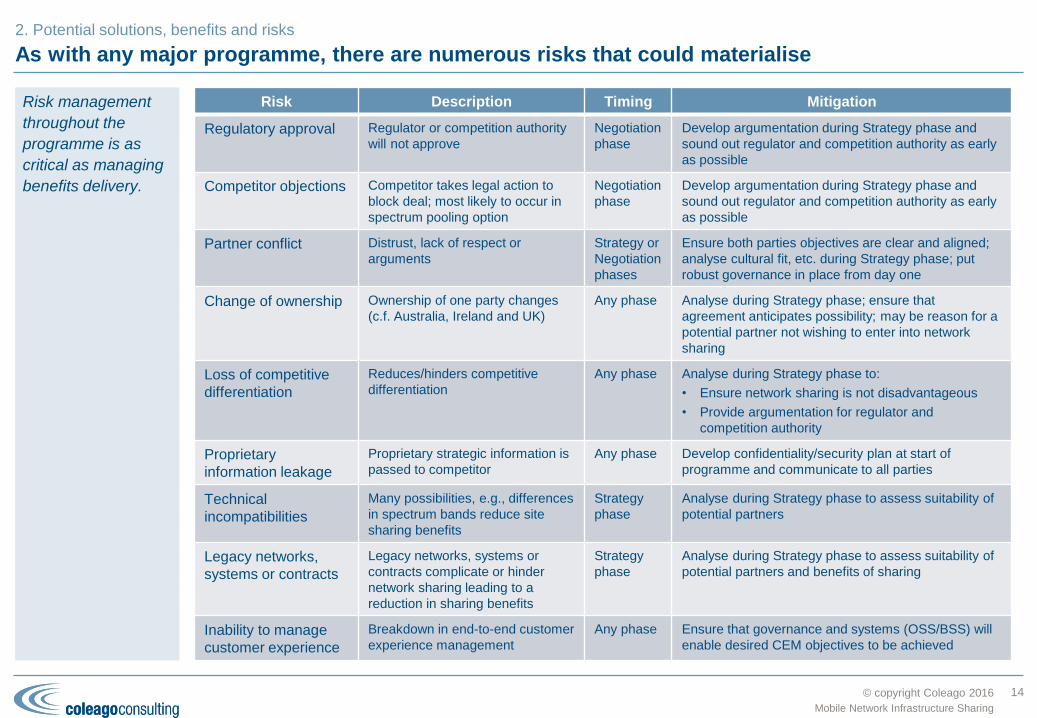

As with any major programme, there are numerous risks that could materialise

14

Mobile Network Infrastructure Sharing

Risk management

throughout the

programme is as

critical as managing

benefits delivery.

2. Potential solutions, benefits and risks

Risk Description Timing Mitigation

Regulatory approval Regulator or competition authority

will not approve

Negotiation

phase

Develop argumentation during Strategy phase and

sound out regulator and competition authority as early

as possible

Competitor objections Competitor takes legal action to

block deal; most likely to occur in

spectrum pooling option

Negotiation

phase

Develop argumentation during Strategy phase and

sound out regulator and competition authority as early

as possible

Partner conflict Distrust, lack of respect or

arguments

Strategy or

Negotiation

phases

Ensure both parties objectives are clear and aligned;

analyse cultural fit, etc. during Strategy phase; put

robust governance in place from day one

Change of ownership Ownership of one party changes

(c.f. Australia, Ireland and UK)

Any phase Analyse during Strategy phase; ensure that

agreement anticipates possibility; may be reason for a

potential partner not wishing to enter into network

sharing

Loss of competitive

differentiation

Reduces/hinders competitive

differentiation

Any phase Analyse during Strategy phase to:

• Ensure network sharing is not disadvantageous

• Provide argumentation for regulator and

competition authority

Proprietary

information leakage

Proprietary strategic information is

passed to competitor

Any phase Develop confidentiality/security plan at start of

programme and communicate to all parties

Technical

incompatibilities

Many possibilities, e.g., differences

in spectrum bands reduce site

sharing benefits

Strategy

phase

Analyse during Strategy phase to assess suitability of

potential partners

Legacy networks,

systems or contracts

Legacy networks, systems or

contracts complicate or hinder

network sharing leading to a

reduction in sharing benefits

Strategy

phase

Analyse during Strategy phase to assess suitability of

potential partners and benefits of sharing

Inability to manage

customer experience

Breakdown in end-to-end customer

experience management

Any phase Ensure that governance and systems (OSS/BSS) will

enable desired CEM objectives to be achieved

© copyright Coleago 2016

Overview of our approach, methodology, deliverables and indicative timescales.

Coleago’s approach

15

3Mobile Network Infrastructure Sharing

© copyright Coleago 2016

Overview of Coleago’s approach to network sharing

16

Mobile Network Infrastructure Sharing

3. Coleago’s Approach

Phases Strategy Negotiation Transition Transformation

Responsibility Prospective Partners Prospective Partners Partners and JV JV

Steps Internal & external analysis

Business case

Partner engagement

Obtain regulatory approval

Design “To-Be”

Negotiate Agreement(s)

Conduct due diligence

Plan

Transition

Depends on scope

Project management

Internal and external communications

Deliverables Business Case

Data Room

Information Memorandum

(TowerCo only)

Heads of Agreement

Regulatory approval(s)

“Target Operating Model

(TOM)” design

Agreement(s)

Legal entity and financing

Staff, assets, contracts,

etc. transferred from

parents

Transformation (within

parents)

JV operational

OpEx and CapEx savings

from, e.g.:

Site dismantling

Equipment relocation or

replacement

Subcontract

renegotiation

Duration 4-5 months 2-5 months but may be

longer dependent on the

regulatory approval

4-6 months Months to years

Variants on the approach

This approach is applicable regardless of the sharing option. It is

designed to work as well for a tower deal with a TowerCo as it does

for an active RAN share with another MNO.

Examples of how the approach varies:

For sharing with another MNO, the Information Memorandum is

not required as the partner selection is not conducted through a

formal, competitive process

The form of the Agreements referred to in the Negotiation phase

will depend on the sharing option, for example, for a tower deal a

Sale/Purchase Agreement and Master Lease Agreement will be

needed

For some sharing options, the entity referred to in the Transition

and Transformation phases may not be a joint venture; for

example, it may be a subsidiary of a tower company or one of the

MNOs.

This approach is

applicable

regardless of the

sharing option. It is

designed to work as

well for a tower deal

with a TowerCo as it

does for an active

RAN share with

another MNO.

Milestone

© copyright Coleago 2016

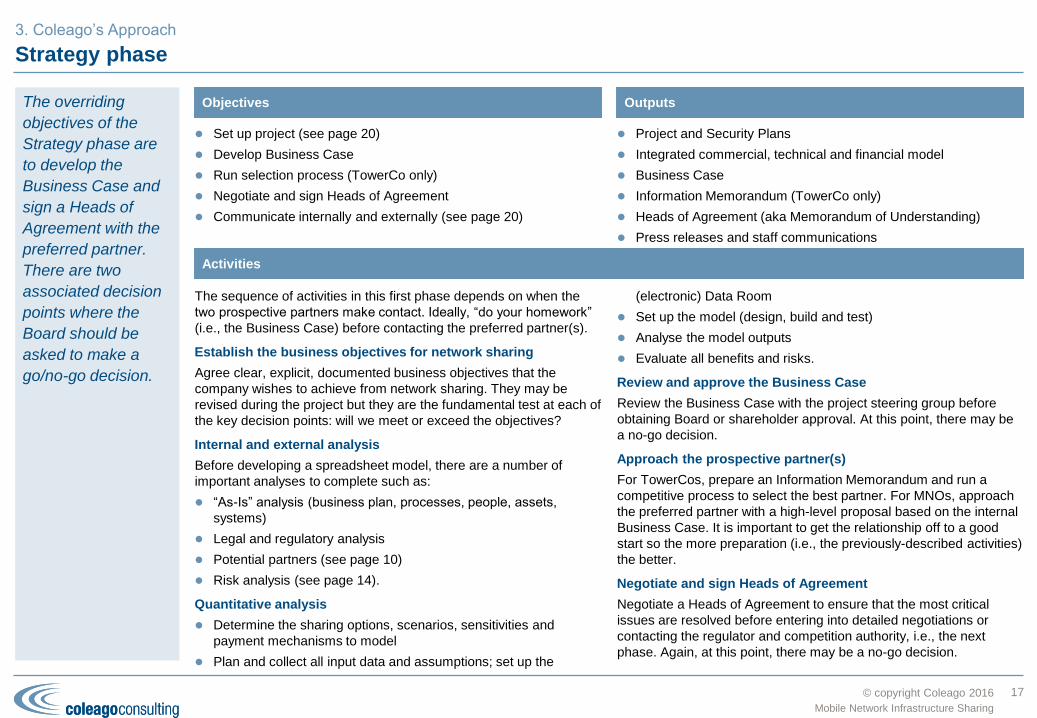

Strategy phase

17

Mobile Network Infrastructure Sharing

3. Coleago’s Approach

The sequence of activities in this first phase depends on when the

two prospective partners make contact. Ideally, “do your homework”

(i.e., the Business Case) before contacting the preferred partner(s).

Establish the business objectives for network sharing

Agree clear, explicit, documented business objectives that the

company wishes to achieve from network sharing. They may be

revised during the project but they are the fundamental test at each of

the key decision points: will we meet or exceed the objectives?

Internal and external analysis

Before developing a spreadsheet model, there are a number of

important analyses to complete such as:

“As-Is” analysis (business plan, processes, people, assets,

systems)

Legal and regulatory analysis

Potential partners (see page 10)

Risk analysis (see page 14).

Quantitative analysis

Determine the sharing options, scenarios, sensitivities and

payment mechanisms to model

Plan and collect all input data and assumptions; set up the

(electronic) Data Room

Set up the model (design, build and test)

Analyse the model outputs

Evaluate all benefits and risks.

Review and approve the Business Case

Review the Business Case with the project steering group before

obtaining Board or shareholder approval. At this point, there may be

a no-go decision.

Approach the prospective partner(s)

For TowerCos, prepare an Information Memorandum and run a

competitive process to select the best partner. For MNOs, approach

the preferred partner with a high-level proposal based on the internal

Business Case. It is important to get the relationship off to a good

start so the more preparation (i.e., the previously-described activities)

the better.

Negotiate and sign Heads of Agreement

Negotiate a Heads of Agreement to ensure that the most critical

issues are resolved before entering into detailed negotiations or

contacting the regulator and competition authority, i.e., the next

phase. Again, at this point, there may be a no-go decision.

Activities

Set up project (see page 20)

Develop Business Case

Run selection process (TowerCo only)

Negotiate and sign Heads of Agreement

Communicate internally and externally (see page 20)

Objectives

Project and Security Plans

Integrated commercial, technical and financial model

Business Case

Information Memorandum (TowerCo only)

Heads of Agreement (aka Memorandum of Understanding)

Press releases and staff communications

OutputsThe overriding

objectives of the

Strategy phase are

to develop the

Business Case and

sign a Heads of

Agreement with the

preferred partner.

There are two

associated decision

points where the

Board should be

asked to make a

go/no-go decision.

© copyright Coleago 2016

Negotiation phase

18

Mobile Network Infrastructure Sharing

3. Coleago’s Approach

Obtain regulatory approval(s)

The process and timing to obtain the necessary regulatory approvals

depends on the sharing option and the applicable local legal and

regulatory framework. In general, it is better to consult the

telecommunications and competition authorities as early as possible

to ensure that the sharing option and agreements take into account

their policies, requirements, etc.

Design “To-Be” entities

A lot of preparatory work is required to develop the details needed for

the Agreement(s). Having agreed on the sharing option in the

Strategy phase, the teams now need to develop the governance

structure, process maps, RACI tables, organisation structures, high-

level job descriptions, KPIs and network/OSS architectures for the JV

and parent companies. This will enable the teams to define interfaces

between the entities, identify the resources (assets, contracts,

people, etc.) to be transferred or procured and prepare the

Implementation Plan.

Prepare JV Business Plan and update Business Cases

Whereas during the Strategy phase the savings estimates are only

accurate to a high order of magnitude, the project teams now need to

develop a more accurate picture. The accuracy will depend on the

resources and time available: if limited, one approach is to analyse a

number of sample/pilot areas in detail in order to adjust the key

assumptions for the whole in-scope network. Outputs from this

activity include the commercial terms, JV Business Plan and updated

Business Cases.

Negotiate and sign Agreement(s)

All the previous activities will enable the appropriate agreements to

be drafted and negotiated, all of which usually takes place in parallel

(see schedule on page 21). Signature will depend on the partners’

governance processes; completion will usually be subject to

obtaining final regulatory approval and, if appropriate, completing due

diligence. Again, at this point, there may be a no-go decision.

Undertake appropriate Due Diligence (DD)

The need for a DD and its scope/duration will depend on the sharing

option and what, if anything, is being transferred to the JV.

Activities

Obtain regulatory approval

Design “To-Be” entities and prepare Implementation Plan

Prepare JV Business Plan and update Business Cases

Negotiate and sign Agreement(s)

Undertake appropriate due diligence

Communicate internally and externally (see page 20)

Objectives

“To-Be” design

High-level Implementation Plan

JV Business Plan

Updated Business Cases

Regulatory approval(s)

Agreement(s)

Press releases and staff communications

Due diligence reports, if required

OutputsKey objectives for

the Negotiation

phase are to

negotiate the JV

agreement and gain

the appropriate

regulatory approval.

© copyright Coleago 2016

Transition phase

19

Mobile Network Infrastructure Sharing

3. Coleago’s Approach

Develop detailed Implementation Plan

The Implementation Plan prepared during the previous phase is high

level: sufficient to agree milestones and develop a budget for the JV

Business Plan. Start work on the detailed Implementation Plan as

soon as the partners are confident that they will proceed; at latest

when the JV Agreement is ready for signature.

For a smooth operational handover from the parents to the JV, it is

important to define how all in-scope assets and activities will be

transferred and at what point the JV takes over responsibility for

meeting KPIs.

Establish legal entity and initial financing

Go through the necessary steps to establish the new legal entity

including providing the initial financing.

Lease and fit out office(s)

Find suitable offices and fit out ready for staff move.

Transfer or recruit/procure staff, assets and contracts

In accordance with the “To-Be” design and the JV Agreement,

transfer/recruit staff, transfer/procure all assets and novate/procure

all third-party contracts.

Implement processes and systems

In accordance with the “To-Be” design and the JV Agreement,

implement all processes and systems.

Transform parent organisations

Implement the changes to the parent organisations in accordance

with the “To-Be” design and the JV Agreement. These activities will

take place before or in parallel with the JV set-up activities.

Start JV operation

At this point the JV takes over responsibility for delivering services in

accordance with the SLAs and KPIs set out in the JV Agreement.

Note that there may still be transfer, recruitment, procurement and

implementation activities in progress.

Activities

Set up JV governance and project team (see page 20)

Develop detailed Implementation Plan

Establish legal entity and initial financing

Transfer staff, assets, contracts, etc. from parents

Transform parent organisations to work with the JV

Communicate internally and externally (see page 20)

Start JV operation

Objectives

Detailed Implementation Plan

Legal entity established

Staff, assets, contracts, etc. transferred from parents

Operational JV

Post-implementation review(s)

OutputsThe overall objective

of this phase is to

get the shared entity

operational. The full

benefits may take

several years to

deliver, which will be

managed against the

JV’s Business Plan.

© copyright Coleago 2016

Use best-practice project management and communications management throughout

Benefits of sound project management

The benefits of using best-practice project management are generally

understood. In the case of network sharing it is particularly important

in order to:

Co-ordinate the activities of numerous parties and resources

across three organisations, especially during the Transition phase

Make the most effective use of the CxO team during the Strategy

and Negotiation phases

Manage post-Transition benefits delivery.

Having decided that network sharing is worth investigating, set it up

as a formal project with a steering group, sponsor, manager, Project

Plan, regular (weekly) reporting cycle, etc.

Given the strategic nature of the project, it is extremely important to

prepare a Security Plan and ensure that anyone joining the project

understands it.

Co-ordinated Transition management

Only a few activities need to be co-ordinated between the prospective

partners during the Strategy and Negotiation phases, namely

negotiations, communications (see text at right), internal approvals

and regulatory approvals. However, during the Transition phase

almost all activities must be co-ordinated between the prospective

partners and the JV to ensure it proceeds smoothly. The

Implementation Plan (pages 18 and 19) must clearly define the split

of responsibilities, handover points, etc.

20

Mobile Network Infrastructure Sharing

Project management

Communication is critical

Network sharing may have a material impact on the Enterprise Value

and therefore all external communications must be managed very

carefully. Similarly internal communications are also highly sensitive

because jobs may be transferred or closed.

For these reasons, involve senior representatives from Human

Resources (HR) and Investor Relations (IR) from the start of the

project. Legal advice will probably also be required with respect to

applicable employment, telecommunications and financial law.

Co-ordinated communications

It is important to co-ordinate communications at a fine level of detail:

the wording and timing of communications must be

exchanged/agreed (subject to legal constraints) between the two

partners and, once it is established, the JV.

Prepare and maintain a Joint Communications Plan

Prepare a Communications Plan at the start of the project and

maintain it through all the phases. It should cover all stakeholders

and all proactive/reactive, internal/external communications activities.

Prior to signing the Heads of Agreement, work with the prospective

partner to extend the Communications Plan to include their

stakeholders and communications activities, i.e., a Joint Plan.

Key milestones for internal and external communications are:

Heads of Agreement signature

JV Agreement signature

JV Agreement completion following regulatory approval and DD

JV operational – usually an internal communication only.

Communications management

3. Coleago’s Approach

Be clear about the

split of

responsibilities

between the

partners and the JV.

Ensure all activities

are well co-

ordinated,

particularly during

Transition.

© copyright Coleago 2016

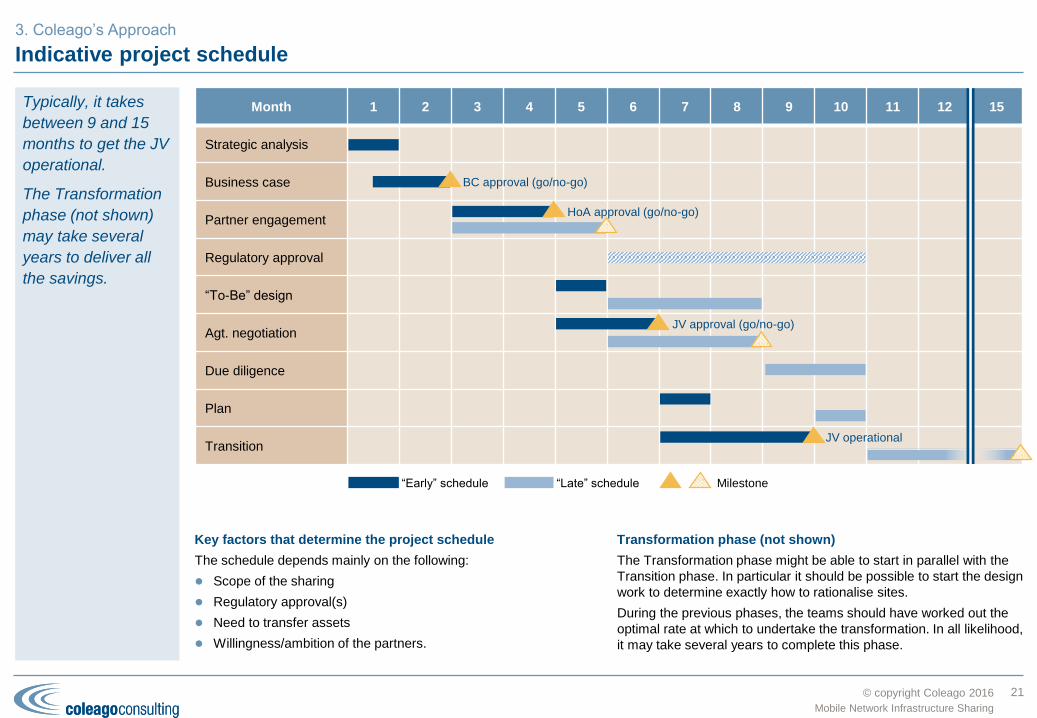

Indicative project schedule

21

Mobile Network Infrastructure Sharing

3. Coleago’s Approach

Month 1 2 3 4 5 6 7 8 9 10 11 12 15

Strategic analysis

Business case

Partner engagement

Regulatory approval

“To-Be” design

Agt. negotiation

Due diligence

Plan

Transition

Typically, it takes

between 9 and 15

months to get the JV

operational.

The Transformation

phase (not shown)

may take several

years to deliver all

the savings.

Key factors that determine the project schedule

The schedule depends mainly on the following:

Scope of the sharing

Regulatory approval(s)

Need to transfer assets

Willingness/ambition of the partners.

Transformation phase (not shown)

The Transformation phase might be able to start in parallel with the

Transition phase. In particular it should be possible to start the design

work to determine exactly how to rationalise sites.

During the previous phases, the teams should have worked out the

optimal rate at which to undertake the transformation. In all likelihood,

it may take several years to complete this phase.

BC approval (go/no-go)

HoA approval (go/no-go)

JV approval (go/no-go)

JV operational

“Early” schedule “Late” schedule Milestone

© copyright Coleago 2016

During the last decade our consultants have built up experience across most types of

sharing deals and phases. We provide a complete range of services to support or lead

your project team.

Coleago’s experience and services

22

4Mobile Network Infrastructure Sharing

© copyright Coleago 2016

Our consultants have built up experience across most types of sharing deals and project phases

Region Sharing

Option

Description

Global All On behalf of the Communications Regulators’ Association of Southern Africa (CRASA) and the International

Telecommunications Union (ITU) developed the ICT and Broadcasting Infrastructure Sharing Guidelines for

the Southern African Development Community (SADC) countries (though applicable anywhere in the world).

Europe All Developed this operator’s 2G, 3G and 4G technology strategy including network sharing, equipment

sourcing and managed services. The project evaluated all possible sharing options and identified the two

most attractive dependent on subsequent expected regulatory events.

Europe Active Modelling of the active network sharing options including alternative commercial terms to help this client

decide its network sharing strategy before entering into negotiations.

Europe Passive

(TowerCo)

Carried out a market and technical analysis for the potential creation of a mobile network towers and

infrastructure sharing business in a major European market.

Asia Active As part of several spectrum valuation projects, evaluated the impact on Enterprise Value of different network

sharing options.

Africa & Asia Active For the GSMA’s Connected Society programme, developed the Infrastructure Economics Toolkit to help

governments and MNOs understand the infrastructure sharing options and fiscal measures needed to

provide rural/remote broadband access to 100% of the population.

Europe Passive Appointed to act as the independent mediator for a passive, antennae and transmission sharing deal. Work

included preparation of the joint business case and a draft heads of agreement.

Middle East

& Africa

Active (MOCN

and roaming)

Provided expert support for the Business Case development and JV Agreement negotiation for a 3G and 4G

MOCN network share and 2G roaming.

Europe Passive

(TowerCo)

Analysed the passive network sharing options for this mobile operator. Working with the client’s legal and

financial advisers, developed the Information Memorandum and drafted the services schedule for the Master

Agreement.

Europe Active Led the technical and commercial activities to develop the relevant JV Agreement schedules for a 3G active

network share in a major European market.

Middle East

& Africa

Passive

(TowerCo)

Technical and commercial due diligence of tower portfolios in Tanzania, Ghana, South Africa and Uganda.

Reviewed the purchaser’s business plans and carried out detailed review of the site portfolio to assess

attractiveness to local market demand.

23

Mobile Network Infrastructure Sharing

In addition to

working on every

type of sharing deal

for MNOs, Coleago’s

consultants have

also worked for

regulators and the

ITU to bring

regulatory

frameworks up to

best practice.

4. Coleago’s Experience and Services

© copyright Coleago 2016

We provide a complete range of services to support or lead your project team

Phase Service Description

Strategy Business Case Internal and external analysis including “As-Is” (business plan, processes, people, assets,

systems), legal and regulatory, potential partners and risks. Quantitative analysis including

commercial, technical and financial modelling. Business Case and Board presentation

preparation.

Info. Memorandum

(TowerCos)

Information Memorandum preparation (with your legal or financial advisors). Evaluation process

design and execution. Board presentation preparation.

HoA negotiation Negotiation team training. Draft HoA (with your legal or financial advisors). Establish internal

position on key terms. Lead or support negotiations. Board presentation preparation.

Negotiation Regulatory support Internal briefing document preparation. Presentations/papers preparation for submission to the

regulatory authorities in support of requests for approvals.

“To-Be” design Design of the governance structure, process maps, RACI tables, organisation structures, high-

level job descriptions, KPIs and network/OSS architectures for the JV and parent companies.

Implementation

Planning

High-level and detailed Implementation Plans (WBS, schedule, resources and costs).

JV Business Plan Commercial terms analysis (in support of negotiation). Business Case update. JV Business

Plan preparation.

Agreement

negotiation

Negotiation team training. Draft Agreement(s) (with your legal or financial advisors). Lead or

support negotiations. Board presentation preparation.

Due diligence Commercial and technical due diligence.

Transform-

ation

RAN rationalisation Lead or support the site or RAN rationalisation.

Any Phase Project

management

Project set-up: governance, Project Plan and reporting cycle. Project management of any phase

including Transition.

Communications

support

Communications planning support to your HR and IR managers. Assistance with drafting Press

Releases and internal communications.

Expert advice Expert advice to the Board and CxO team. Knowledge transfer to the project team.

24

Mobile Network Infrastructure Sharing

Coleago can help

throughout the

project at all levels.

Our consultants

become part of your

project team.

Our methodology

includes templates

and tools based on

our experience

which increase the

team’s efficiency and

reduce risk.

4. Coleago’s Experience and Services

© copyright Coleago 2016

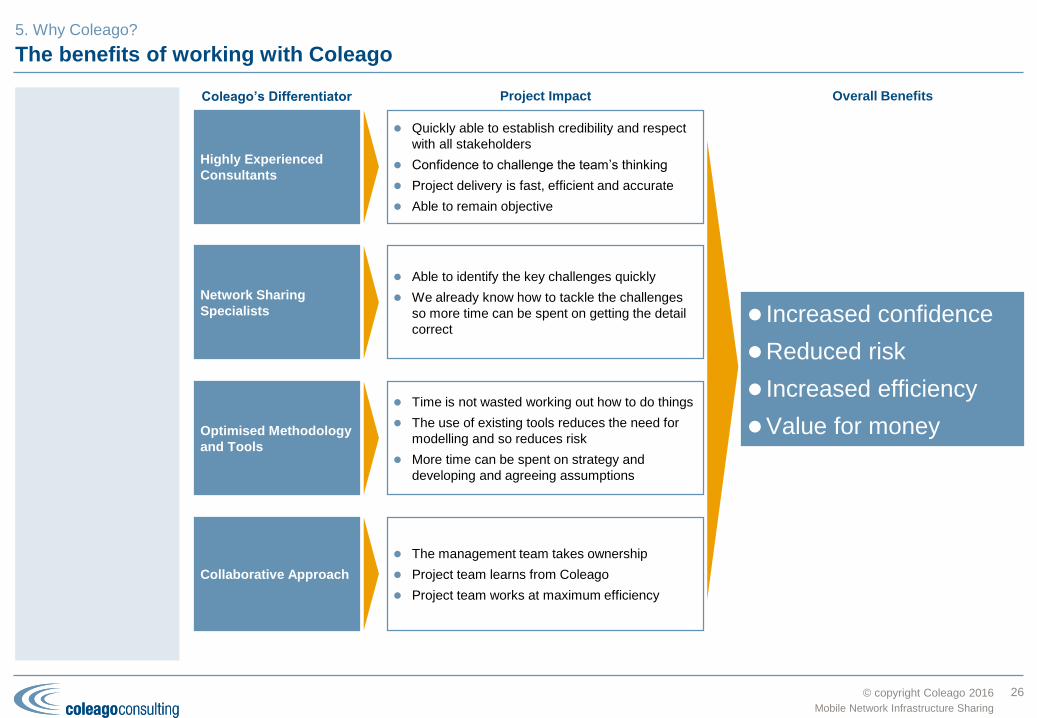

The key benefits of working with Coleago.

Why Coleago?

25

Mobile Network Infrastructure Sharing

5

© copyright Coleago 2016

The benefits of working with Coleago

Coleago’s Differentiator Overall Benefits

Mobile Network Infrastructure Sharing

5. Why Coleago?

Quickly able to establish credibility and respect

with all stakeholders

Confidence to challenge the team’s thinking

Project delivery is fast, efficient and accurate

Able to remain objective

Able to identify the key challenges quickly

We already know how to tackle the challenges

so more time can be spent on getting the detail

correct

Time is not wasted working out how to do things

The use of existing tools reduces the need for

modelling and so reduces risk

More time can be spent on strategy and

developing and agreeing assumptions

The management team takes ownership

Project team learns from Coleago

Project team works at maximum efficiency

Network Sharing

Specialists

Optimised Methodology

and Tools

Highly Experienced

Consultants

Collaborative Approach

Increased confidence

Reduced risk

Increased efficiency

Value for money

Project Impact

26

© copyright Coleago 2016

Connecting the Unconnected: Rural/Remote Broadband Initiatives

Appendix A

27

Mobile Network Infrastructure Sharing

A

© copyright Coleago 2016

Making sense of the plethora of global initiatives – public bodies

UN:

2030 Sustainable Development Goals (SDGs):

– Goal 9: build resilient infrastructure, promote sustainable

industrialization and foster innovation

– Target: Significantly increase access to information and

communications technology and strive to provide universal and

affordable access to the Internet in least developed countries

by 2020

World Summit on the Information Society (WSIS)

– Organised annually by ITU, UNESCO, UNDP and UNCTAD

– Plan of Action: 12 Action Lines; C2 is Infrastructure

ITU:

Connect the World: conference series focused on the

implementation of the connectivity targets from the UN's World

Summit on the Information Society (WSIS) and the Regional

Initiatives adopted by Member States at the ITU's World

Telecommunication Development Conference (WTDC) (every 4

years, last one in 2014)

Connect 2020 Agenda has four goals:

– Growth

– Inclusiveness: bridge the digital divide and provide broadband

for all

– Sustainability

– Innovation

ITU & UNESCO: Broadband Commission for Sustainable

Development

Following adoption of the UN's SDGs in Sep 2015, the

Commission was re-launched as the Broadband Commission for

Sustainable Development to showcase and document the power

of ICT and broadband-based technologies for sustainable

development

Six focus areas:

– Economy and finance

– Social development

– Post 2015 development agenda

– Environment and climate change

– Education and science

– Broadband advocacy

World Bank Group: Broadband Access for All

Two goals by 2030:

– End extreme poverty by decreasing the percentage of people

living on less than $1.90 a day to no more than 3%

– Promote shared prosperity by fostering the income growth of

the bottom 40% for every country

ICT sector strategy has three action areas:

– Transformation

– Connectivity: scaling up affordable access to broadband

for all

– Innovation

28

Mobile Network Infrastructure Sharing

There are more than

ten global initiatives

with a similar

objective: to

“connect the

unconnected” or in

other words to

provide broadband

services in

rural/remote areas to

those who currently

don’t have access to

the Internet.

Appendix A

Public Bodies

© copyright Coleago 2016

Making sense of the plethora of global initiatives – NGOs

World Economic Forum (WEF): Internet for All

WEF:

– Established in 1971 as a not-for-profit foundation

– Headquartered in Geneva

– independent, impartial and not tied to any special interests

10 Global Challenge Initiatives, one of which is "Future of the

Internet".

Consists of four projects, one of which is "Internet for All"

Objective: develop a scalable, replicable new model of public-

private collaboration that accelerate internet access and adoption

for the 4 billion people currently not on the internet

Two phases:

– Internet for All report (2015)

– Country programmes (2016 onwards)

– Rwanda, Kenya, Uganda and South Sudan

– Additional country programmes (up to three in total) in other

regions of the world (Asia, Latin America)

Alliance for Affordable Internet (A4AI)

Global coalition working to make broadband affordable for all

Currently working in six countries — Nigeria, Ghana,

Mozambique, Liberia, Myanmar and the Dominican Republic — to

make Internet more affordable and accessible for nearly 300

million people. In each of these countries, we’ve signed formal

memoranda of understanding with the government, and have

worked with a wide range of in-country stakeholders to build

strong national multi-stakeholder coalitions. These national

coalitions work to develop solutions tailored to local realities, and

lead efforts in their country to realise more affordable access.

Research and international advocacy

ONE:

International campaigning and advocacy organisation of more than

7 million people

Focused on the UN SDGs

Digital Impact Alliance (DIAL):

Includes the UN Foundation, Bill & Melinda Gates Foundation,

USAID, etc.

DIAL’s mission is to accelerate the collective efforts of

government, industry and development organizations to realize the

vision of a more inclusive digital economy for the underserved in

emerging markets

29

Mobile Network Infrastructure Sharing

Appendix A

Non-Governmental Organisations (NGOs)

© copyright Coleago 2016

Making sense of the plethora of global initiatives – commercial entities

GSMA:

Mobile for Development - Connected Society programme has

four work streams:

– Affordability

– Infrastructure economics

– Digital literacy

– Locally-relevant content

Facebook: Internet.org

Free Basics offers access to basic websites for local audiences

Connectivity Lab developing ways to make affordable internet

access possible in communities around the world

– Aquila unmanned aircraft

Express Wi-Fi working with carriers, ISPs and local entrepreneurs

to help expand connectivity to underserved locations

Innovation Lab, an Ericsson-Facebook collaboration, helps

developers understand how their apps work in different parts of

the world

Alphabet: Project Loon

Network of balloons traveling on the edge of space, designed to

connect people in rural and remote areas, help fill coverage gaps,

and bring people back online after disasters

30

Mobile Network Infrastructure Sharing

Appendix A

Commercial Entities

© copyright Coleago 2016

Network Sharing Database and Regional Indexes

Appendix B

31

Mobile Network Infrastructure Sharing

B

© copyright Coleago 2016

Network Sharing Database and Regional Indexes

32

Mobile Network Infrastructure Sharing

Appendix B

MNO Network Sharing Deals by Region (2001-15) Network Sharing Experience by Group (end-2015)

Coleago’s Sharing Indexes by Region (end-2015)Database (charts above and tables on following pages)

Coleago’s database is based on public announcements by MNOs. It

includes passive and active sharing deals between MNOs and tower

JVs with, or sales to, TowerCos. It excludes M&A, national roaming,

transmission-only and informal or unannounced site sharing deals.

Note that the “Date” column in the following tables is the date that the

deal was announced. The completion date may be different.

Regional Indexes (see chart at right)

As the number of countries and MNOs differ considerably between

regions, Coleago has developed two indexes in order to compare the

status of network sharing. The “TowerCo Index” is calculated by

dividing the number of sale-and-leaseback deals by the total number

of MNOs in the region. The “MNO Sharing Index” is calculated by

dividing the number of passive/active sharing deals by the number of

MNOs and multiplying by two. In both cases, the index may exceed

100 depending on the industry structure within a country.

© copyright Coleago 2016

Americas (1 of 2)

Country MNO1 MNO2 TowerCo or MNO3 Deal Type Date

Canada Bell Mobility Telus Active (MORAN) Oct-08

Jamaica LIME América Móvil (Claro) Passive Jul-09

Canada Rogers Videotron Active (MORAN) Jul-09

Canada Rogers Manitoba Telecom Active (MORAN) Jul-09

Canada Bell Mobility SaskTel Active (MORAN) Oct-09

Chile Telefónica (Movistar) ATC TowerCo Jul-10

Colombia MIC (Tigo) ATC TowerCo Jul-11

Mexico Telefónica (Movistar) ATC TowerCo Dec-11

Chile Telefónica (Movistar) ATC TowerCo Jan-12

Brazil Telefónica (Vivo) SBA TowerCo Jan-13

Brazil Oi TIM Brasil Active (MORAN) Mar-13

Brazil Telefónica (Vivo) América Móvil (Claro) Active (MORAN) Mar-13

Colombia Telefónica (Movistar) MIC (Tigo) Active (MORAN) Aug-13

Brazil NII ATC TowerCo Aug-13

Mexico AT&T [formerly Nextel] ATC TowerCo Aug-13

USA AT&T Crown Castle TowerCo Oct-13

Brazil Oi SBA TowerCo Dec-13

Brazil Oi SBA TowerCo Jun-14

Venezuela Movilnet Telefónica (Movistar) Digitel Passive Oct-14

Brazil TIM Brasil ATC TowerCo Nov-14

33

Mobile Network Infrastructure Sharing

The network sharing

picture in the

Americas has been

dominated by

TowerCo deals (over

70%) to the extent

that the region is on

a par with the MEA

region on the

TowerCo Index.

However it is still

early days as these

deals have only

taken place in five

countries (Brazil,

Chile, Colombia,

Mexico and USA).

An even greater

opportunity is active

sharing between

MNOs where the

only deals to date

have been in

Canada, Colombia

and Brazil.

Appendix B

© copyright Coleago 2016

Americas (2 of 2)

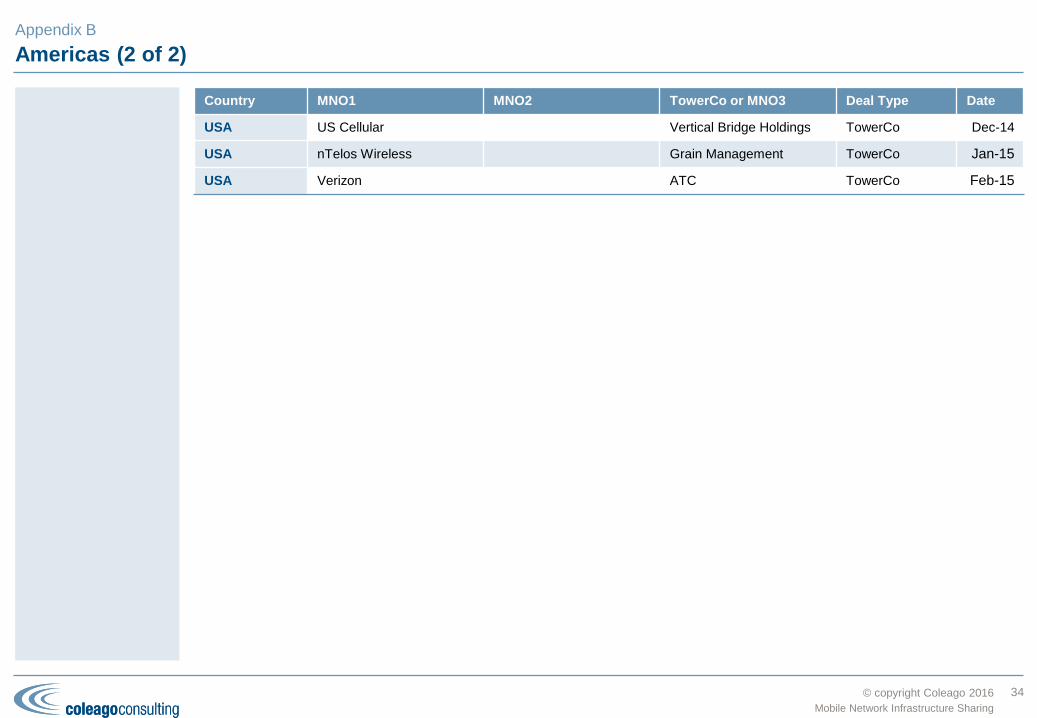

Country MNO1 MNO2 TowerCo or MNO3 Deal Type Date

USA US Cellular Vertical Bridge Holdings TowerCo Dec-14

USA nTelos Wireless Grain Management TowerCo Jan-15

USA Verizon ATC TowerCo Feb-15

34

Mobile Network Infrastructure Sharing

Appendix B

© copyright Coleago 2016

Europe (1 of 2)

Country MNO1 MNO2 TowerCo or MNO3 Deal Type Date

Sweden TeliaSonera Tele2 Active (MOCN) Jan-01

Sweden Telenor Sweden Hutchison (3) Active (MOCN) Apr-01

Spain Vodafone Spain Orange Spain Active (MORAN) Nov-06

Italy Vodafone Italia TIM Passive Nov-07

United

Kingdom

T-Mobile UK [now EE] Hutchison (3) Active (MORAN) Dec-07

Germany Vodafone Germany Telefónica (O2 Germany) Passive Mar-09

Spain Vodafone Spain Telefónica (Movistar) Passive Mar-09

Ireland Vodafone Ireland Telefónica O2 Ireland

[now Hutchison (3)]

Passive Mar-09

Sweden Tele2 Telenor Sweden Active (MOCN) Apr-09

Italy TIM Hutchison (3) Passive Jul-09

Belgium Orange (Mobistar) KPN (BASE) Passive Oct-09

Czech

Republic

Telefónica O2 [now O2

Czech Republic]

T-Mobile CR Active (MORAN) Feb-11

Ireland Hutchison (3) [formerly

Telefónica O2 Ireland]

Eircom (Meteor) Passive Apr-11

Denmark TeliaSonera Denmark Telenor Denmark Active (MOCN) Jun-11

Poland T-Mobile (PTC) PTK Centertel [now

Orange Polska]

Active (MORAN) Jul-11

Russia Rostelecom MTS Passive Feb-12

United

Kingdom

Vodafone UK Telefónica (O2 UK) Active (MORAN) Jun-12

35

Mobile Network Infrastructure Sharing

Europe has gone the

furthest in terms of

“depth of sharing”

with 17 active

(MORAN and

MOCN) sharing

deals to date but has

been the laggard

when it comes to

TowerCo deals. With

no sharing of any

form in half of

Europe, there is still

some way to go.

Appendix B

© copyright Coleago 2016

Europe (2 of 2)

Country MNO1 MNO2 TowerCo or MNO3 Deal Type Date

Ireland Vodafone Ireland Hutchison (3) Passive Jul-12

France Bouygues Antin IP TowerCo Nov-12

Netherlands KPN Protelindo TowerCo Nov-12

Greece Vodafone Greece Wind Hellas Active (MORAN) Jun-13

Romania Vodafone Orange Active (MORAN) Aug-13

Spain Telefónica (Movistar) TeliaSonera (Yoigo) Abertis TowerCo Aug-13

Netherlands T-Mobile Tele2 Passive Sep-13

Iceland Fjarskipti (Vodafone) Nova Active (MOCN) Nov-13

France SFR Bouygues Active (MORAN) Jan-14

Finland TeliaSonera Finland DNA Active (MOCN) Aug-14

Russia Vimpelcom MTS Active (MORAN) Dec-14

Hungary T-Mobile (Magyar

Telekom)

Telenor Active (MORAN) Feb-15

Italy Vimplecom (Wind) Abertis TowerCo Mar-15

Finland Ukko Mobile Digita Passive Dec-15

36

Mobile Network Infrastructure Sharing

Appendix B

© copyright Coleago 2016

Middle East & Africa (1 of 2)

Country MNO1 MNO2 TowerCo or MNO3 Deal Type Date

Iran MCCI Irancell Taliya Passive Jan-07

Qatar Qtel [now Ooredoo] Vodafone Qatar Passive Mar-09

Ghana MIC (Tigo) Helios TowerCo Jan-10

South Africa Cell C ATC TowerCo Nov-10

Ghana MTN ATC TowerCo Dec-10

Nigeria Starcomms SPAN TowerCo Dec-10

Tanzania MIC (Tigo) Helios TowerCo Dec-10

DRC MIC (Tigo) Helios TowerCo Dec-10

Uganda MTN Uganda ATC TowerCo Dec-11

Uganda Orange Eaton TowerCo Mar-12

Uganda Warid [now Airtel] Eaton TowerCo Mar-12

Côte d'Ivoire MTN IHS Holding TowerCo Oct-12

Cameroon MTN IHS Holding TowerCo Oct-12

Rwanda Rwanda Development

Board

KT Corp Open Access Mar-13

Tanzania MIC (Tigo) Vodafone (Vodacom) Helios TowerCo Jul-13

Israel Partner (Orange) Golan Passive Oct-13

Israel Partner (Orange) HOT Mobile Active (MOCN) Nov-13

Rwanda MTN IHS Holding TowerCo Dec-13

Zambia MTN IHS Holding TowerCo Dec-13

37

Mobile Network Infrastructure Sharing

Africa leads the

world in TowerCo

deals; the regional

Index being pulled

down from 17 to 13

because of the lack

of deals in the

Middle East. Three

multinational

operators, Millicom

(Tigo), MTN, and

Airtel, account for

more than 80% of

the deals.

Appendix B

© copyright Coleago 2016

Middle East & Africa (2 of 2)

Country MNO1 MNO2 TowerCo or MNO3 Deal Type Date

DRC Airtel Helios TowerCo Jul-14

Republic of

Congo

Airtel Helios TowerCo Jul-14

Nigeria Etisalat Nigeria IHS Holding TowerCo Aug-14

Nigeria MTN Nigeria IHS Holding TowerCo Sep-14

Israel Cellcom Golan Active (MOCN) Sep-14

Israel Cellcom Pelephone Passive Sep-14

Egypt Orange (MobiNil) Eaton TowerCo Nov-14

Nigeria Airtel ATC TowerCo Nov-14

Rwanda Airtel IHS Holding TowerCo Dec-14

Zambia Airtel IHS Holding TowerCo Dec-14

Tunisia Ooredoo Tunisia Tunisie Telecom Active (MORAN) Oct-15

Burkina Faso Airtel Eaton TowerCo Oct-15

38

Mobile Network Infrastructure Sharing

Similar to the

Americas, there are

still more than 30

African countries

without TowerCos

and an even bigger

opportunity for active

sharing between

MNOs.

With the exception of

Israel, Middle

Eastern operators

have yet to embark

on the TowerCo or

network sharing

journey.

Appendix B

© copyright Coleago 2016

Asia Pacific (1 of 2)

Country MNO1 MNO2 TowerCo or MNO3 Deal Type Date

Australia Vodafone Hutchison

Australia

Optus Active (MORAN) Aug-04

Pakistan PTCL (Ufone) Telenor Pakistan Passive Jul-07

India Airtel (Bharti Infratel) Essar [now Vodafone] Idea Cellular Passive Dec-07

Indonesia Axiata (XL) Hutchison (3) Passive Dec-07

New Zealand Vodafone NZ NZ Communications Passive Oct-08

Vietnam Viettel [formerly EVN

Telecom]

Hanoi Telecom

(Vietnamobile)

Active (MOCN) Apr-09

India Aircel Datacom Solutions [now

Videocon]

Passive Sep-09

India BSNL Tata Teleservices Passive Oct-09

India BSNL Aircel Passive Oct-09

Bangladesh Axiata (Robi) Warid [now Airtel] Passive Oct-09

India BSNL Datacom Solutions [now

Videocon]

Passive Oct-09

India BSNL MTS (SSTL) Passive Nov-09

Bangladesh Vimpelcom (banglalink) Telenor (Grameenphone) Passive Feb-10

Bangladesh Axiata (Robi) Telenor (Grameenphone) Passive Feb-10

India Essar [now Vodafone] ATC TowerCo Feb-10

Bangladesh Warid [now Airtel] Citycell Passive Apr-10

Hong Kong PCCW Hutchison (3) Active (MOCN) Oct-10

Bangladesh Warid [now Airtel] Telenor (Grameenphone) Passive Nov-10

39

Mobile Network Infrastructure Sharing

Asia Pacific stands

out for its passive

sharing between

MNOs but the Index

is exaggerated by

the multiplicity of

deals in Bangladesh

and India.

Appendix B

© copyright Coleago 2016

Asia Pacific (2 of 2)

Country MNO1 MNO2 TowerCo or MNO3 Deal Type Date

Malaysia Celcom DiGi Passive Jan-11

Pakistan PTCL (Ufone) Vimpelcom (Mobilink) Passive Apr-11

Pakistan Telenor Pakistan Vimpelcom (Mobilink) Passive May-11

Malaysia Maxis U Mobile Active (MORAN) Oct-11

Thailand AIS TOT Passive Jan-12

Malaysia Maxis REDTone Active (MOCN) Jul-12

Bangladesh Axiata (Robi) Teletalk Passive Jan-13

Azerbaijan Bakcell Azerfon Active (MOCN) May-13

India RCOM Reliance Jio Passive Jun-13

Malaysia Celcom Puncak Semangat (Altel) Active (MOCN) Jul-13

India Airtel Reliance Jio Passive Dec-13

Bangladesh Airtel (formerly Warid) Teletalk Passive Feb-14

China China Mobile China Telecom China Unicom Passive Jul-14

Papua New

Guinea

Telikom PNG bmobile Active (MORAN) Aug-14

India BSNL Reliance Jio Passive Aug-14

Indonesia Axiata (XL) Solusi Tunas Pratama

(STP)

TowerCo Oct-14

Indonesia Telkom Indonesia Tower Bersama

Infrastructure (TBI)

TowerCo Oct-14

Pakistan Warid TowerShare TowerCo Apr-15

Thailand AIS DTAC Passive Aug-15

40

Mobile Network Infrastructure Sharing

Although the

TowerCo Index is as

low as Europe, the

segment is expected

to grow rapidly with

a number of

operators such as

Axiata (Malaysia,

Bangladesh, etc.)

establishing their

own captive tower

businesses and

TowerCos such as

American Tower and

Viom expanding into

India and Myanmar

respectively.

Similar to the

Americas and MEA,

active sharing still

leaves huge

potential.

Appendix B

© copyright Coleago 2016

Tower Companies

Appendix C

41

Mobile Network Infrastructure Sharing

C

© copyright Coleago 2016

Multinational tower companies

42

Mobile Network Infrastructure Sharing

Appendix C

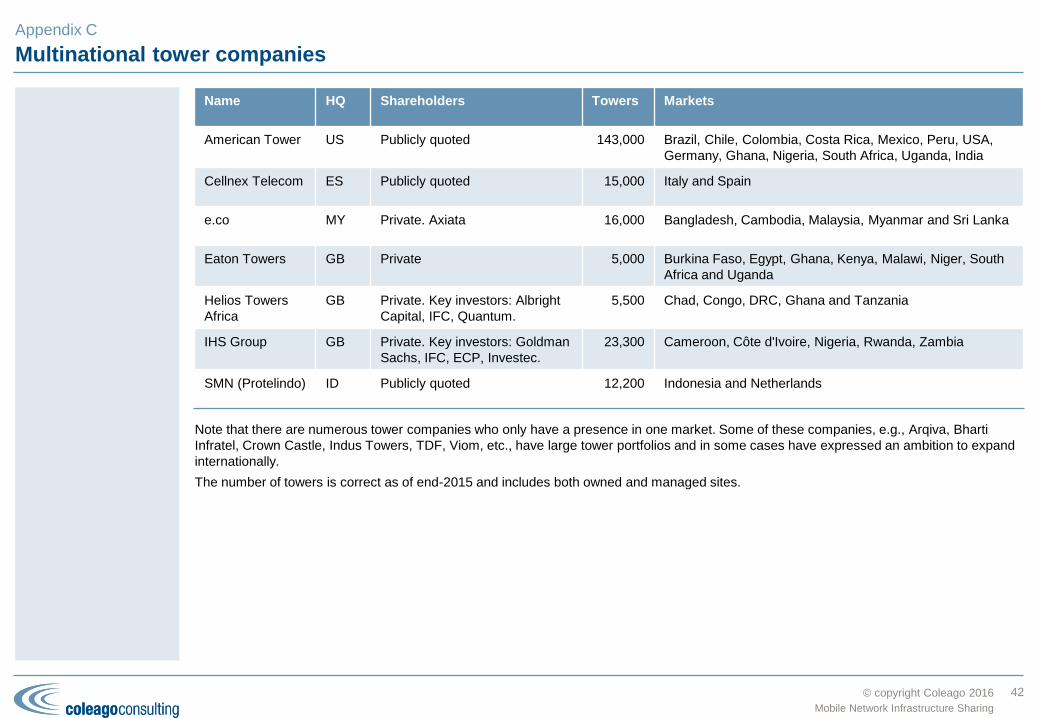

Name HQ Shareholders Towers Markets

American Tower US Publicly quoted 143,000 Brazil, Chile, Colombia, Costa Rica, Mexico, Peru, USA,

Germany, Ghana, Nigeria, South Africa, Uganda, India

Cellnex Telecom ES Publicly quoted 15,000 Italy and Spain

e.co MY Private. Axiata 16,000 Bangladesh, Cambodia, Malaysia, Myanmar and Sri Lanka

Eaton Towers GB Private 5,000 Burkina Faso, Egypt, Ghana, Kenya, Malawi, Niger, South

Africa and Uganda

Helios Towers

Africa

GB Private. Key investors: Albright

Capital, IFC, Quantum.

5,500 Chad, Congo, DRC, Ghana and Tanzania

IHS Group GB Private. Key investors: Goldman

Sachs, IFC, ECP, Investec.

23,300 Cameroon, Côte d'Ivoire, Nigeria, Rwanda, Zambia

SMN (Protelindo) ID Publicly quoted 12,200 Indonesia and Netherlands

Note that there are numerous tower companies who only have a presence in one market. Some of these companies, e.g., Arqiva, Bharti

Infratel, Crown Castle, Indus Towers, TDF, Viom, etc., have large tower portfolios and in some cases have expressed an ambition to expand

internationally.

The number of towers is correct as of end-2015 and includes both owned and managed sites.

© copyright Coleago 2016

Tower/site sharing through third-party tower companies

Business rationale for tower companies

Saddled with the high cost of 3G licences and the cost of 3G build

out, many mobile operators sought to release capital from the sale of

their tower assets. This also had advantages from the stock market

perspectives since the telecoms business and the tower business

were valued on a different basis. Mobile telecoms operators are

deemed to be growth stocks whereas the tower business is based on

predictable, stable cash flow.

The communication tower or mast business is a large business

dominated by infrastructure and or real estate orientated companies

as opposed to technology companies. For example Crown Castle

International Inc. and American Tower Corp. are the dominant

independent tower companies in the USA.

More recently, tower companies also moved into the transmission

space, benefitting from the growth in demand for backhaul as a result

of increase mobile data traffic.

The features that make the tower business attractive to investors are:

Restrictions in granting building permits may create a local

monopoly. It is this which also makes it risky for operators to sell

their tower assets to a dominant supplier.

Long-term contracts are the norm.

High switching costs result in high renewal rates.

Most of the OpEx is fixed.

The combination of predictable revenue and OpEx results in a

steady cash flow.

Tower companies have low borrowing costs because they can

offer towers as collateral.

Renting tower space