Embed Size (px)

DESCRIPTION

Presentation on the sustainability of the Alaska budget before the Alaska House Task Force on Sustainable Education, 8.28 - 29-.2013.

Citation preview

Sustainability of the Alaska Budget

Brad KeithleyPresident, Keithley Consulting, LLC

August 28-29, 2013

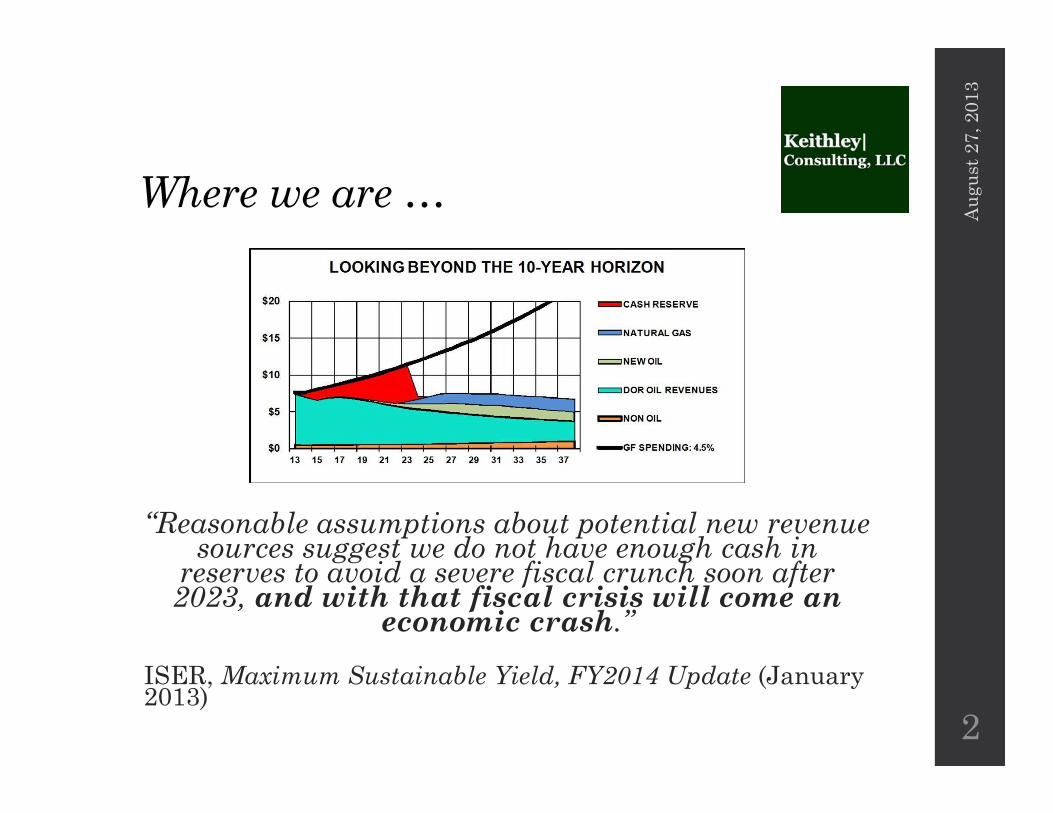

Where we are …

“Reasonable assumptions about potential new revenue sources suggest we do not have enough cash in

reserves to avoid a severe fiscal crunch soon after 2023, and with that fiscal crisis will come an

economic crash.”

ISER, Maximum Sustainable Yield, FY2014 Update (January 2013)

Aug

ust 2

7, 2

013

2

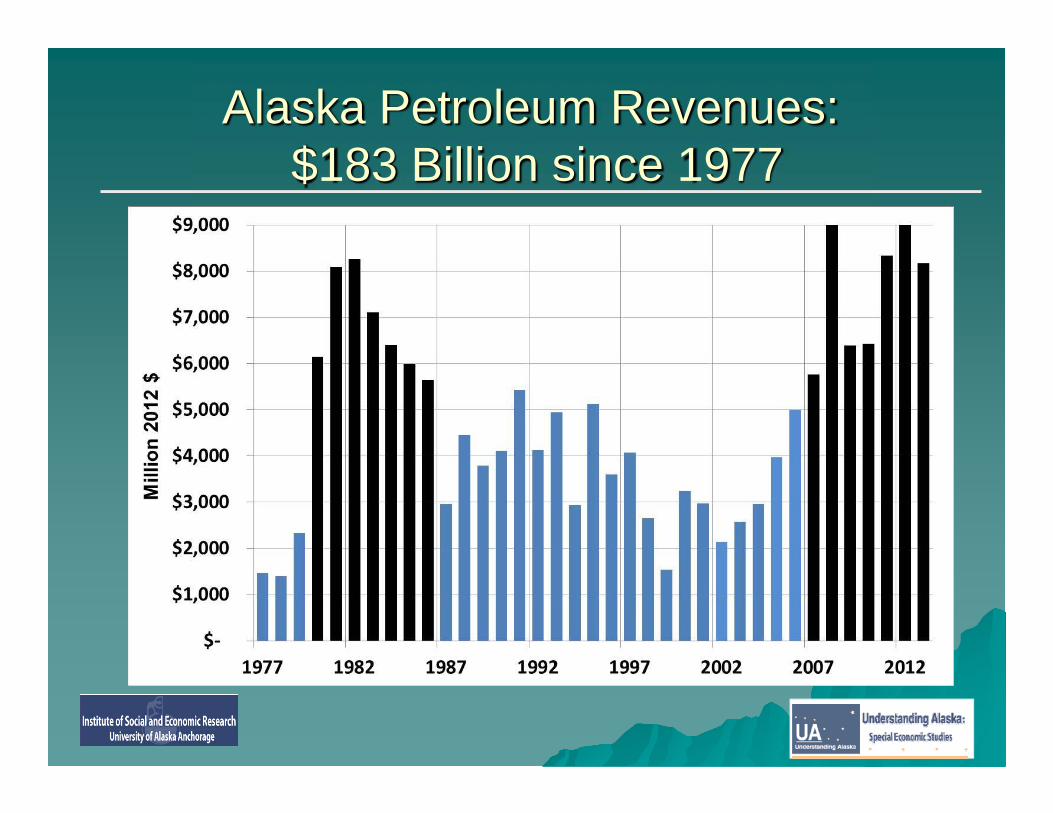

Alaska Petroleum Revenues:$183 Billion since 1977

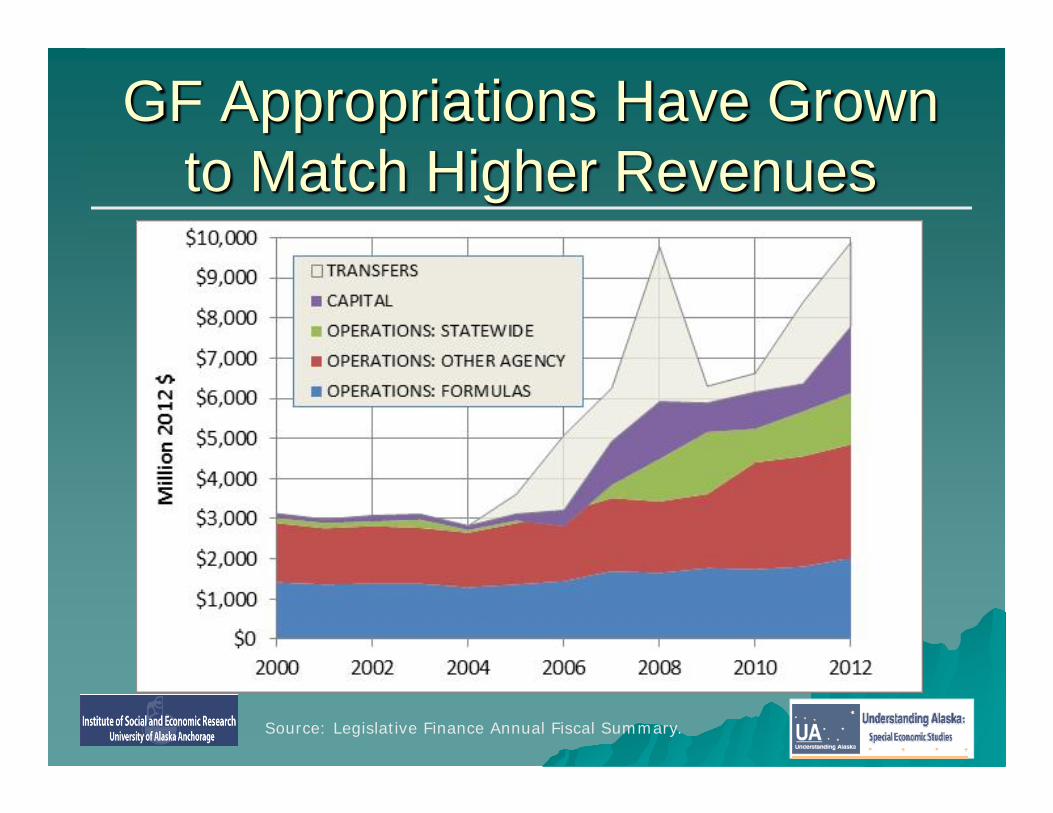

GF Appropriations Have Grown to Match Higher Revenues

Source: Legislative Finance Annual Fiscal Summary.

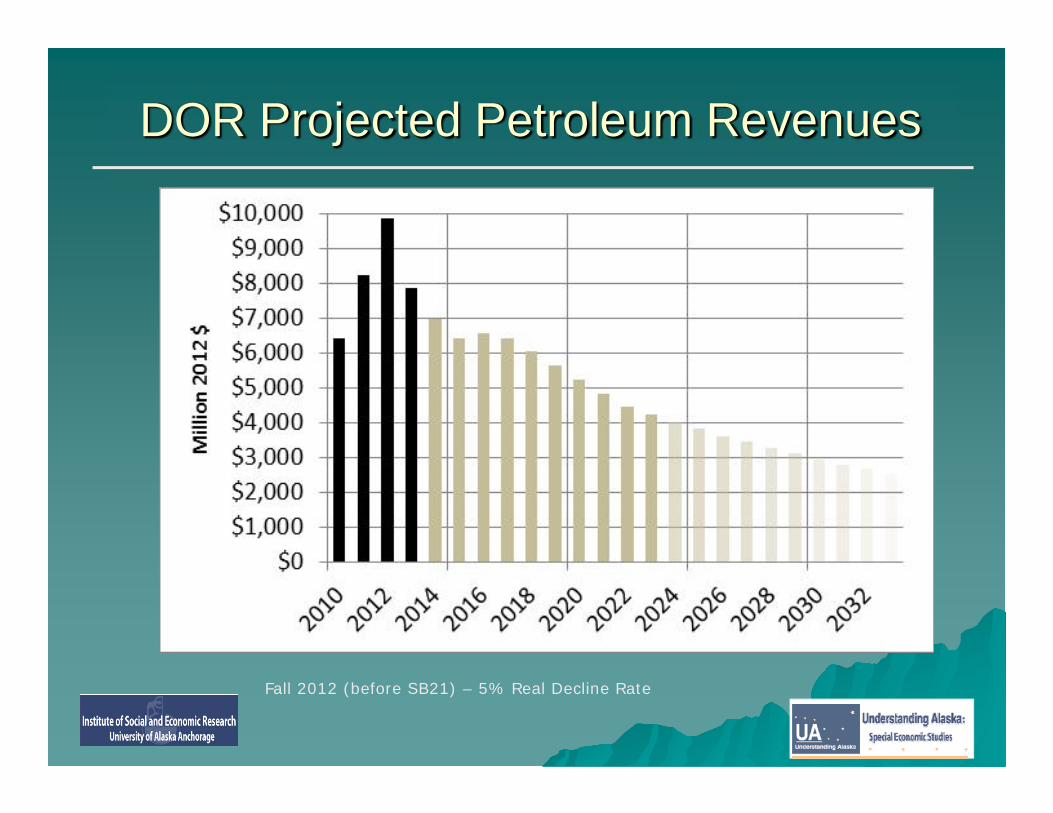

DOR Projected Petroleum Revenues

Fall 2012 (before SB21) – 5% Real Decline Rate

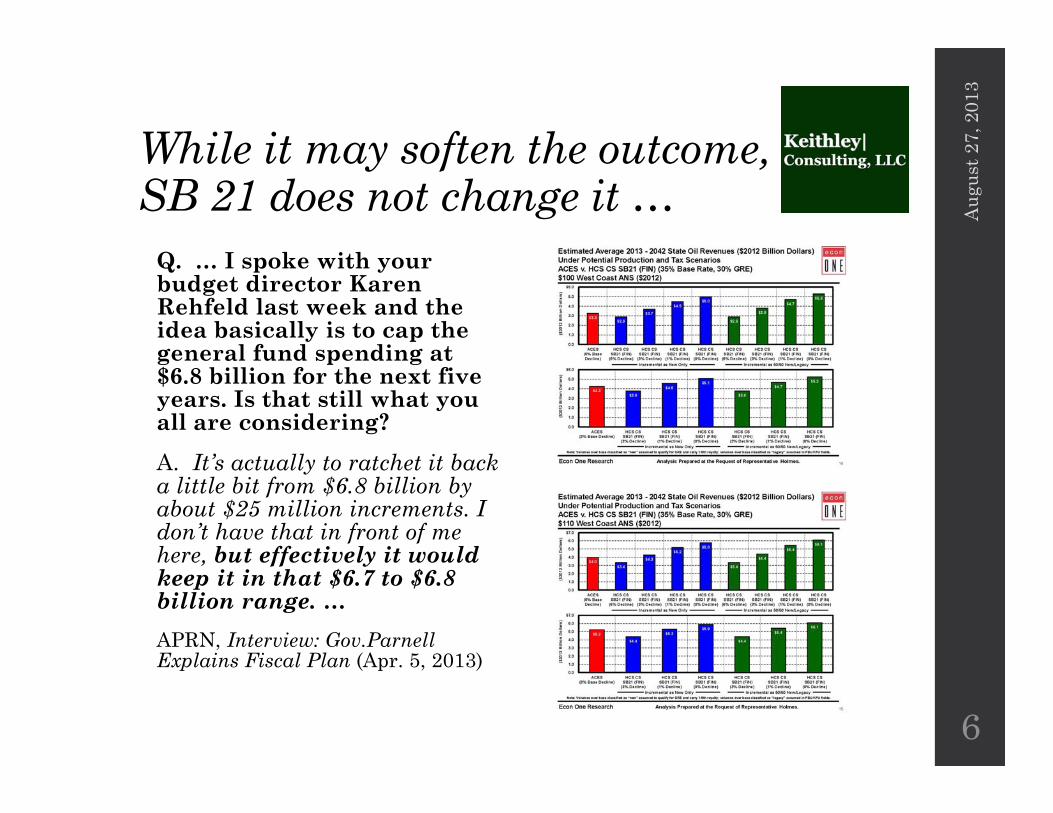

While it may soften the outcome,SB 21 does not change it …

Q. … I spoke with your budget director Karen Rehfeld last week and the idea basically is to cap the general fund spending at $6.8 billion for the next five years. Is that still what you all are considering?A. It’s actually to ratchet it back a little bit from $6.8 billion by about $25 million increments. I don’t have that in front of me here, but effectively it would keep it in that $6.7 to $6.8 billion range. …APRN, Interview: Gov.ParnellExplains Fiscal Plan (Apr. 5, 2013)

Aug

ust 2

7, 2

013

6

There also should be concernabout ongoing development …A concern: Alaska will not attract significant long term investment tied to natural resource development as long as potential investors see the type of fiscal cliff demonstrated in ISER’s analysis and anticipate that, once reached, they will be part of the solution.

Mar

ch 2

9, 2

013

7

Policy Option 1: Business as Usual

“The state does not currently have either a general sales tax or a personal income tax. However, the non-OCS projection of future state population and public sector demands compared to revenues suggests that a number of adjustments to the state’s fiscal structure will be necessary in future years to maintain adequate public services. Two options available to the state, in addition to reducing expenditures, are institution of a broad-based tax, and use of a portion of the earnings of the Permanent Fund. … It is anticipated that both options will be required in the non-OCS case. The value shown above assumes a personal income tax, similar to the tax that was eliminated in 1980, will be phased in between 2022 and 2026.”Northern Economics and ISER, Potential National-Level Benefits of Alaska OCS Development (Feb. 2011)

Aug

ust 2

7, 2

013

8

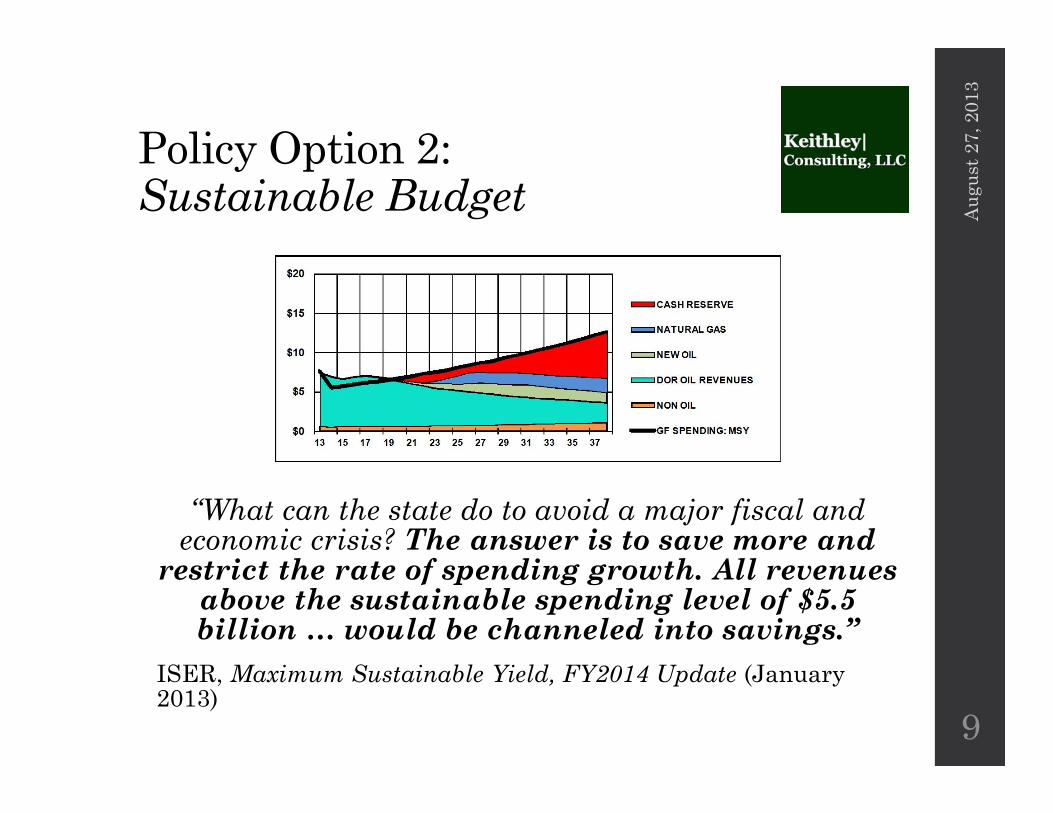

Policy Option 2:Sustainable Budget

“What can the state do to avoid a major fiscal and economic crisis? The answer is to save more and

restrict the rate of spending growth. All revenues above the sustainable spending level of $5.5 billion … would be channeled into savings.”

ISER, Maximum Sustainable Yield, FY2014 Update (January 2013)

Aug

ust 2

7, 2

013

9

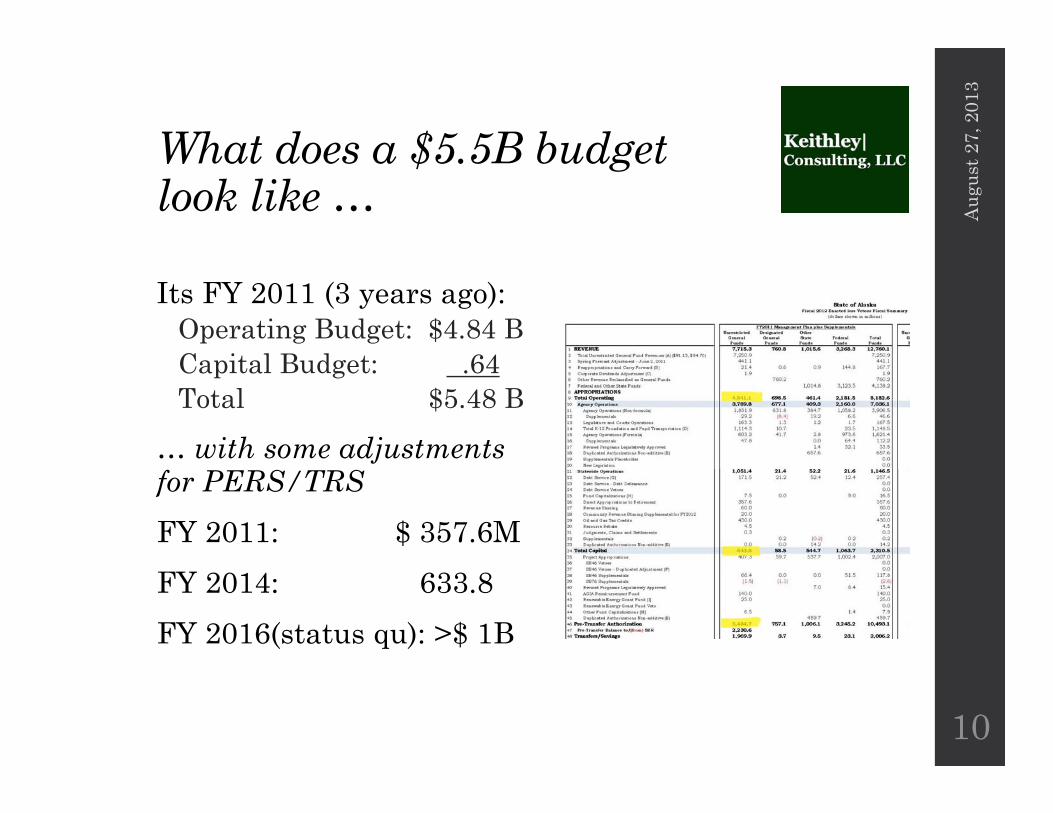

What does a $5.5B budget look like …

Its FY 2011 (3 years ago):Operating Budget: $4.84 BCapital Budget: .64Total $5.48 B

… with some adjustments for PERS/TRSFY 2011: $ 357.6MFY 2014: 633.8FY 2016(status qu): >$ 1B

Aug

ust 2

7, 2

013

10

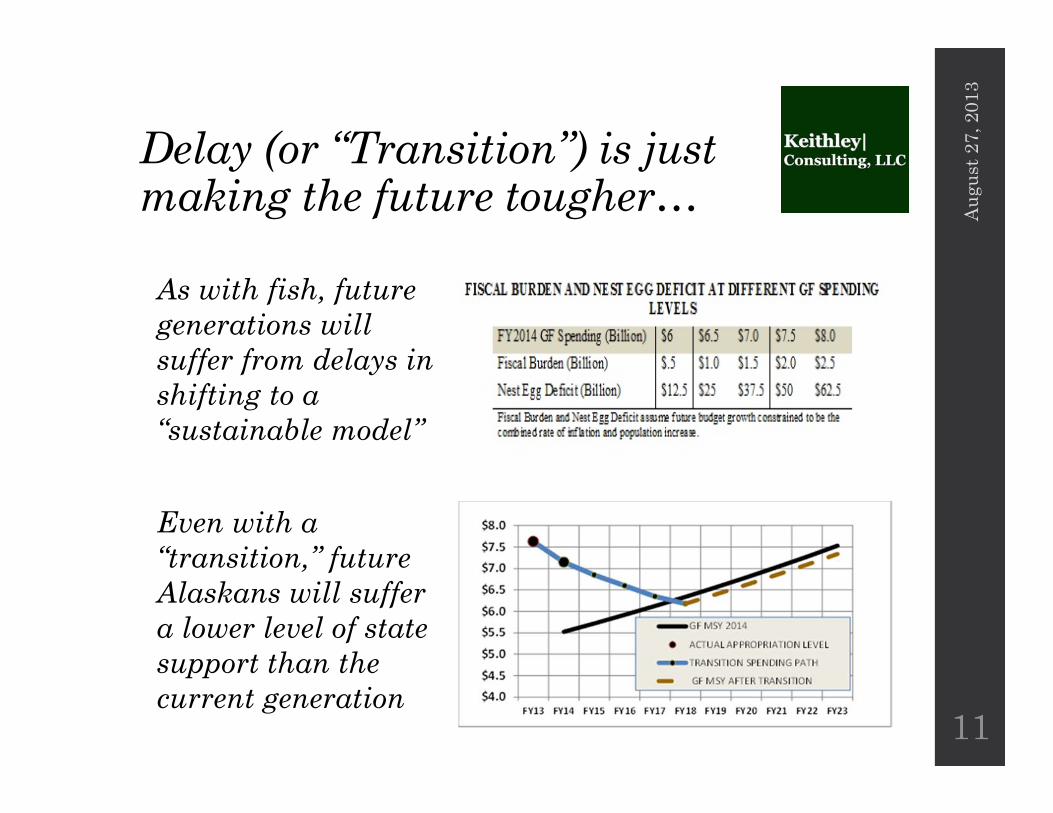

Delay (or “Transition”) is just making the future tougher…

As with fish, future generations will suffer from delays in shifting to a “sustainable model”

Even with a “transition,” future Alaskans will suffer a lower level of state support than the current generation

Aug

ust 2

7, 2

013

11

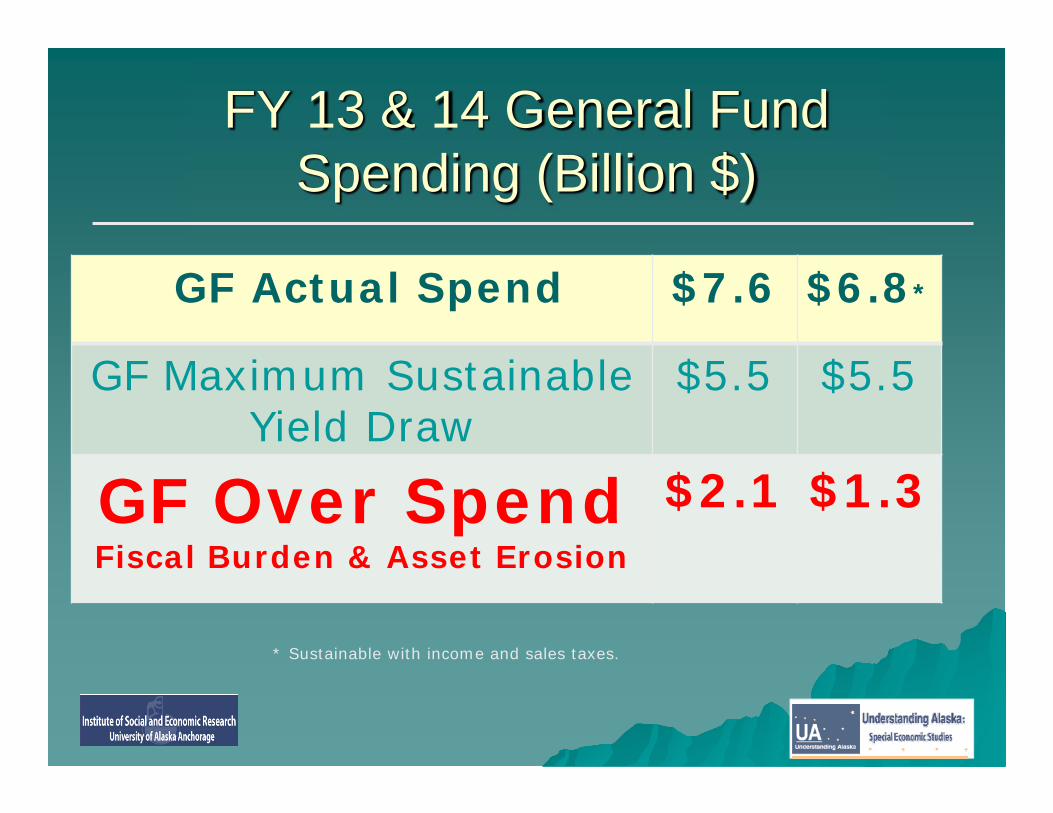

FY 13 & 14 General Fund Spending (Billion $)

GF Actual Spend $7.6 $6.8*

GF Maximum Sustainable Yield Draw

$5.5 $5.5

GF Over Spend Fiscal Burden & Asset Erosion

$2.1 $1.3

* Sustainable with income and sales taxes.

Stopping short …

Two simple steps:• Cap annual spending* at the annually calculated “sustainable” level

• Commit all other annual revenues, as well as financial reserves (SBR and CBR), to a long term, growth oriented investment pool (“Permanent Fund II”)

Aug

ust 2

7, 2

013

13*In this context, spending and revenues both refer to Unrestricted General Fund (UGF) moneys.

Continuing on the current course… A

ugus

t 27,

201

3

14

Bradford G. KeithleyPresident & Principal, Keithley Consulting, LLC

Publisher, Thoughts on Alaska Oil & Gaskeithleyconsulting.com

email: [email protected]

Aug

ust 2

7, 2

013

15

For more information, contact …