Embed Size (px)

Citation preview

Getting to VCs’ Love Getting to Love your VC

a.k.a.

Venture financing for startuppers

30-Jul-13

Niccolò Sanarico [email protected] il_nico

Agenda

Introductions

What is Venture Capital?

Getting there

Deal Structuring

Conclusions

Introducing Myself

MSc in ICT Engineering PoliMi

MSc in Computer Science UIC@Chicago

MBA Oxford University

Associate & dealflow manager dPixel

ICT Consulting/Corporate finance experience

Geek & Tech Passionate

Introducing dPixel

x x

Se

lect

ed

Inve

stm

en

ts

Ex

its

Advisor to: - Digital Investments SCA SICAR – Seed compartment - Working Capital Accelerator

Promoter of the Barcamper Acceleration Program

Promoter of TechGarage – Grassroot Innovation

Agenda

Introductions

What is Venture Capital?

Getting there

Deal Structuring

Conclusions

Setting the Perspective

VCs manage Someone Else’s money, in order to make more money for him and for themselves

True story

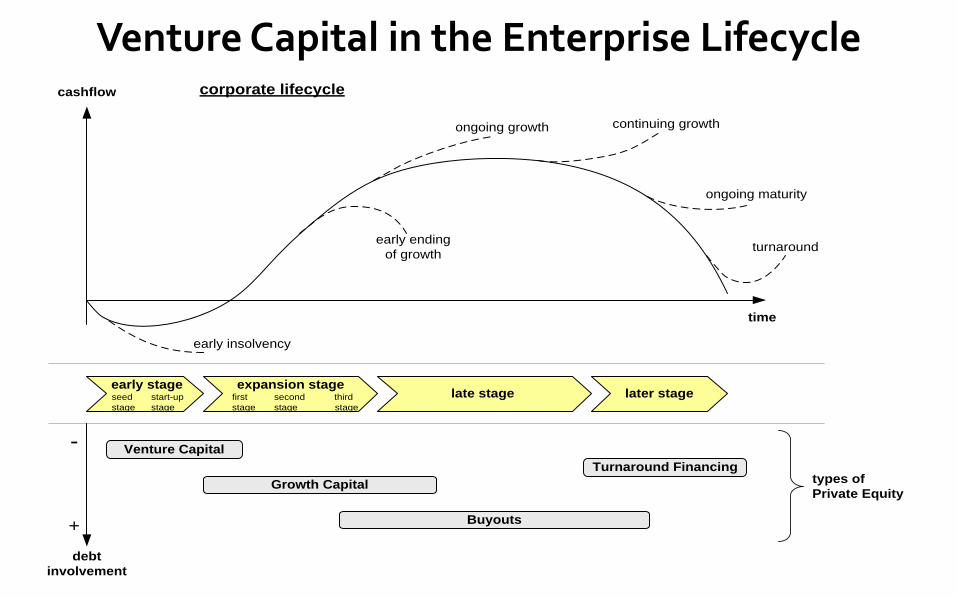

Venture Capital in the Enterprise Lifecycle cashflow

time

early stage expansion stagelate stage later stageseed start-up

stage stage

first second third

stage stage stage

Venture Capital

Buyouts

Growth Capital

Turnaround Financing

debt

involvement

early insolvency

early ending

of growth

ongoing growth continuing growth

ongoing maturity

turnaround

corporate lifecycle

types of

Private Equity

+

-

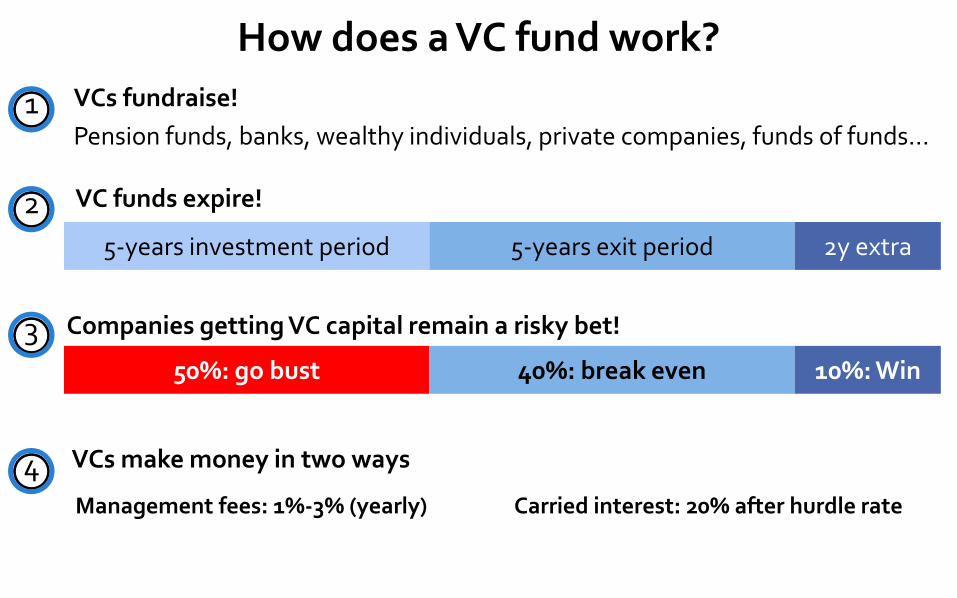

How does a VC fund work?

5-years investment period 5-years exit period 2y extra

VCs fundraise!

Pension funds, banks, wealthy individuals, private companies, funds of funds…

50%: go bust 40%: break even 10%: Win

1

2

3

VC funds expire!

Companies getting VC capital remain a risky bet!

4 VCs make money in two ways

Management fees: 1%-3% (yearly) Carried interest: 20% after hurdle rate

Why VCs, Anyhow?

Active Investor - Leverage the VC partner’s experience - Strong focus on product, customer and go-to-market - Help in planning&recruiting (CxO, bizdev, etc..)

Collaboration - Support & coaching to the management team - High standards for performance, management & integrity - Great attention to execution

Relationships - Access to strong network when required - Access to international markets - Co-investments with other VC funds, support in fundraising & exit

Efficiency - Efficient use of cash - Holistic approach to resources - Create value for all stakeholders

When NOT to look for VCs

VCs are not there to fund any idea. Do not look for VC if: 1. Your market is extremely niche.

2. You want to create a lifestyle business.

3. You are not ready to commit 3+ years in an enterprise.

4. You are not ready to view your company overgrow you as a founder.

5. You are extremely scared of failure.

Agenda

Introductions

What is Venture Capital?

Getting there

Deal Structuring

Conclusions

What VCs look for

Team Market

Opportunity

Technology Traction

Team

1. Founding team of 2/3 people

2. With complementary skills

3. Previous experience working together? Chemistry?

4. Track record counts Anyone investing in these guys?

Market

1. Size DOES count

2. Barriers to entry?

3. Complexity / fragmentation?

4. Do you have previous experience in this market?

TAM: Total Available Market The total reference market

e.g. Accounting Software

SAM: Served/ Serviceable Available Market

Focus on your technology e.g. Saas-based accounting sw for SMB

SOM: Serviceable Obtainable Market

Realistic expectation of what market share you target to obtain

e.g. 5% of Italian market in 5years

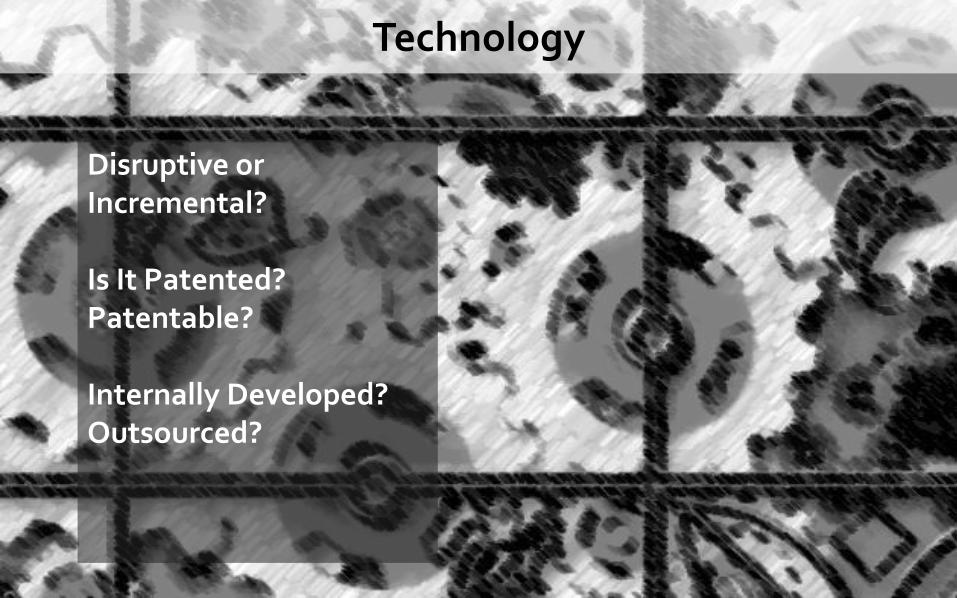

Technology

Disruptive or Incremental? Is It Patented? Patentable? Internally Developed? Outsourced?

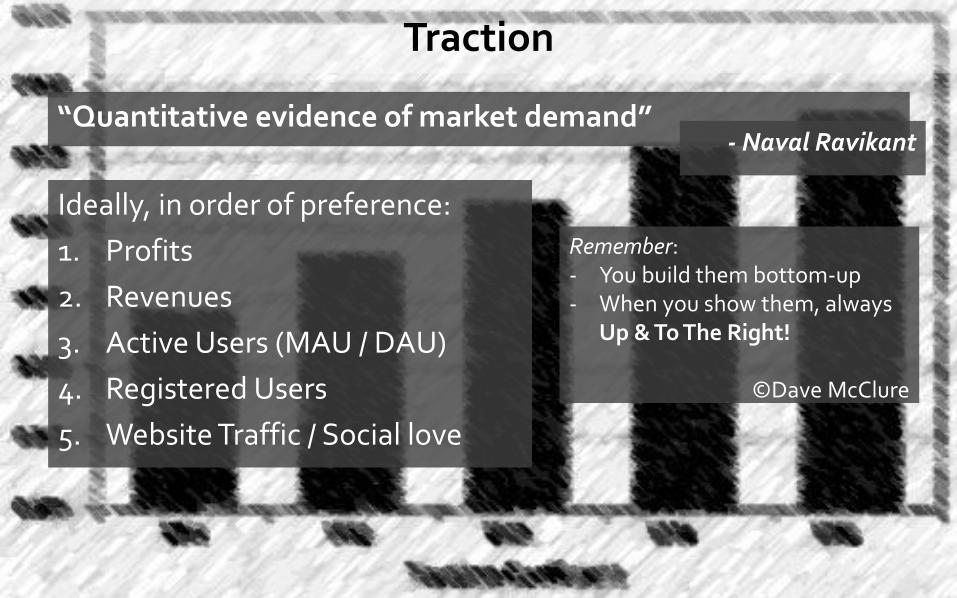

Traction

“Quantitative evidence of market demand” - Naval Ravikant

Ideally, in order of preference:

1. Profits

2. Revenues

3. Active Users (MAU / DAU)

4. Registered Users

5. Website Traffic / Social love

Remember: - You build them bottom-up - When you show them, always

Up & To The Right!

©Dave McClure

Tricks for Telling your Traction Story

http://www.quora.com/Brendan-Baker/Posts/Startups-How-to-Communicate-Traction-to-Investors

Yeah, I know, lazy, but that post is powerful.

Do your own due diligence

When looking for a VC, do your homework!

Active Fund?

Aligned to investment

strategy?

No competitors in

portfolio?

Track Record?

Size / stage / geography?

• Take a deep look at portfolio companies and try to meet the CEOs

• Participate to events / meetups. Be visible

• Find great advisors

Hints:

• Do NOT send unsolicited e-mails to [email protected]

• Find good referral channels

The anatomy of a seed

Brendan Baker, Anatomy of a seed, http://www.slideshare.net/brendanbaker/anatomy-of-seed-7753824

Key Takeaways on Fundraising

• It will take longer than you expect

• Investors are not always active (i.e. summer, winter holidays)

• Too many introductions will take you nowhere (beware of time wasters)

• Investors include leaders and followers – you’ll be much more interesting with a committed investor or two

• Follow Techcrunch, AngeList, Venture Hacks, HackerNews, CheFuturo!, etc…

• Fundraising. Is. Hard.

Agenda

Introductions

What is Venture Capital?

Getting there

Deal Structuring

Conclusions

Process Deal Flow Management Investment process

Pipeline management

Learn & Adapt

- Find new prospects

- Analyze progress, actions and opportunities

- Metrics & KPI from prospects

- Forensic analysis from lost deals

New prospects

Internal Staff Meeting Market & company potential, equity story, team & documentation

Investment Memo

Due Diligence

Term Sheet

Investment Agreement

Due diligence of: - Management

team - Technology - Market - Product - Strategy - Legal/compan

y

Final document Co-investment? Well-known protection clauses for VC: - Drag Along - Tag Along - Liquidation

Preference

Investment contract Final Closing Investment!

weekly

quarterly

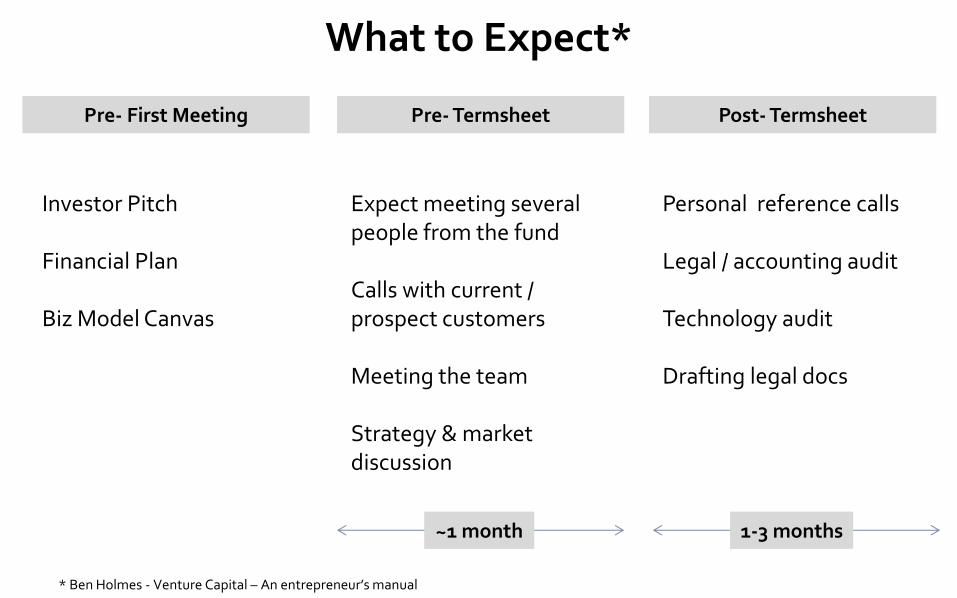

What to Expect*

* Ben Holmes - Venture Capital – An entrepreneur’s manual

Pre- First Meeting Pre- Termsheet Post- Termsheet

Investor Pitch Financial Plan Biz Model Canvas

Expect meeting several people from the fund Calls with current / prospect customers Meeting the team Strategy & market discussion

Personal reference calls Legal / accounting audit Technology audit Drafting legal docs

~1 month 1-3 months

Termsheet clauses / 1

Tag Along - If the founders receive a proposal to purchase their quotas, they must tell the Investor about the proposal, and the investor has the right to participate in the sale

Liquidation

Preference

- In case of liquidation, the fund will get 100% or more of its investment before the other shareholders. The remaining will be distributed following one of many possible rules

Anti-Dilution - In case of down-round, the investors in the previous round do not get diluted in the new one

Drag Along - If the fund receives a proposal for acquiring at least 50.01% of the company, and it wants to sell, can force other shareholders to sell their quotas

Inve

stm

en

t / E

xit

Pro

tect

ion

Termsheet clauses / 2

Key Men Clause - Founders are forced to remain with the company for at least 24 / 36 months.

This is regulated with an option on their quotas, held by the fund. - Non-compete

Veto Rights

- Board of Directors rights: - Selection and dismissal of CEO - Control of extraordinary expenses & remunation of key people - …

Favourable Votes - Favourable votes in Shareholders’ Assembly

- New capital increases - Liquidation / Sale decisions - …

Go

vern

an

ce

Fo

un

de

rs’

Un

de

rta

kin

g

No - Shop - After signing the termsheet, the company cannot enter any negotiations with

other investors for an agreed period of time (usually enough to perform proper due diligence) N

o-S

ho

p

BIN

DIN

G

Valuation

Pre-Money

valuation

- Value of the company before the investment - To be estimated following objective and subjective parameters - Several valuations methods exist (please check a finance book!)

Money

(Investment)

- Total investment - Usually through a Capital Increase (no share purchase!) - Equity or Convertible Loan

Post-Money

Valuation

- Post-Money = Pre-Money + Investment - > Pre-Money - Founders are diluted, but the value of the company may increase significantly - Usually the lowest pre-money valuation for the next round - Beware the down-round!

Post-Money = Pre-Money + Investment

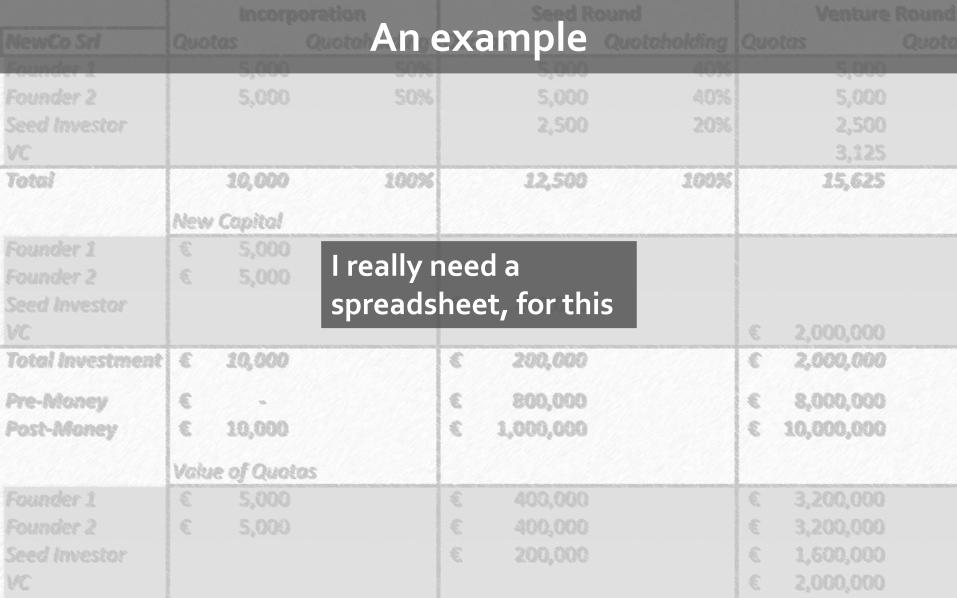

An example

I really need a spreadsheet, for this

Agenda

Introductions

What is Venture Capital?

Getting there

Deal Structuring

Conclusions

Final remarks

1. VCs are not your friends.

2. Nor your enemies.

3. Fundraising is a long and painful job. Prepare yourself.

4. Get acquainted with the vocabulary.

5. Execute

![[Ldb] -lei_nº_9.394_de_20_de_dezembro_de_1996](https://img.pdfslide.net/doc/110x75/557ccdf0d8b42a43438b505f/ldb-leino9394de20dedezembrode1996.jpg)