Embed Size (px)

Citation preview

Attention to Retail

June 23rd, 2015

E-Commerce, M-Commerce And AdaptingTo Consumer Behaviour Anne-Marie Schwab, General Manager and VPRetailMeNot France

A bit about us…

The world’s largest marketplace for digital offers

CONSUMERS RETAILERS & BRANDS

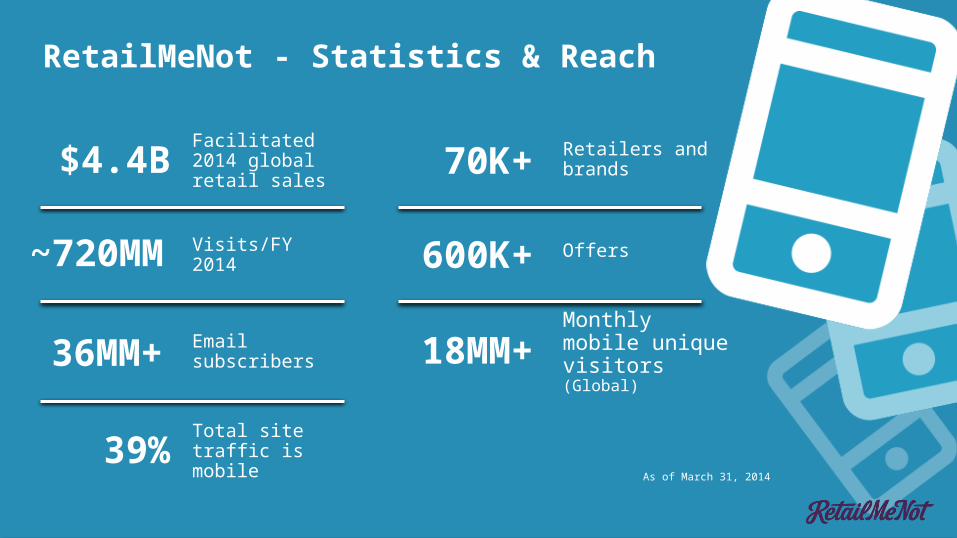

70K+$4.4B Facilitated 2014 global retail sales

RetailMeNot - Statistics & Reach

36MM+ Email subscribers 18MM+Monthly mobile unique visitors (Global)

39% Total site traffic is mobile

~720MM Visits/FY 2014 600K+

As of March 31, 2014

Retailers and brands

Offers

We’re working with over 70,000 leading retailers

WHAT WE’LL TALK ABOUT TODAY

• Objectives of retail remain the same but the rules are changing

• Consumers have changed their mindset

• How retailers can respond

A brave new world of retail

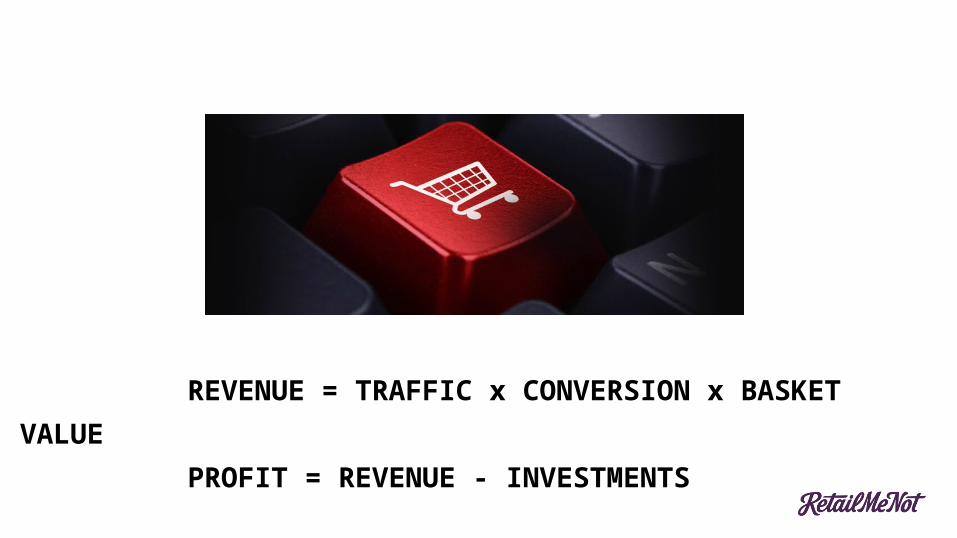

REVENUE = TRAFFIC x CONVERSION x BASKET VALUE

PROFIT = REVENUE - INVESTMENTS

2011 2012 2013 2014

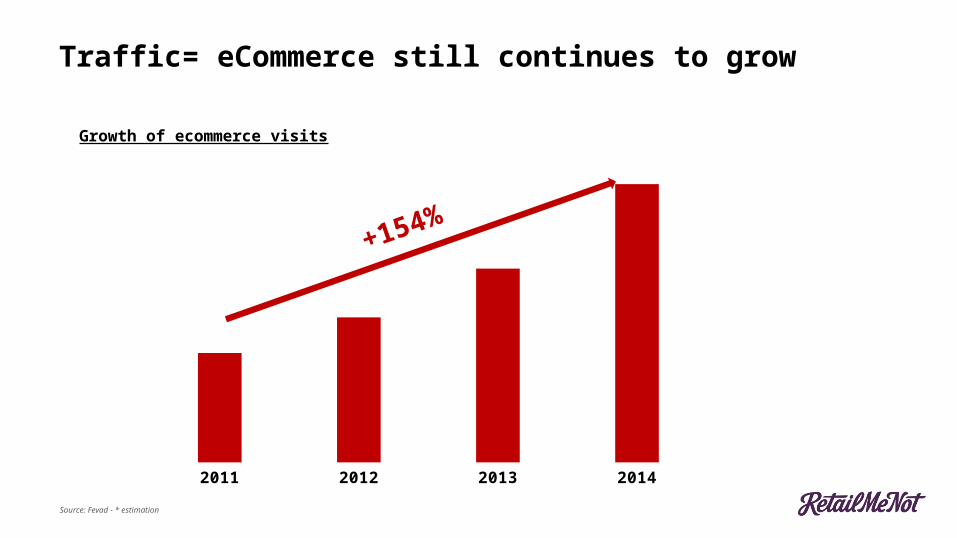

Traffic= eCommerce still continues to grow

Growth of ecommerce visits

Source: Fevad - * estimation

+154%

2011 2012 2013 2014€76

€78

€80

€82

€84

€86

€88

€90

€92

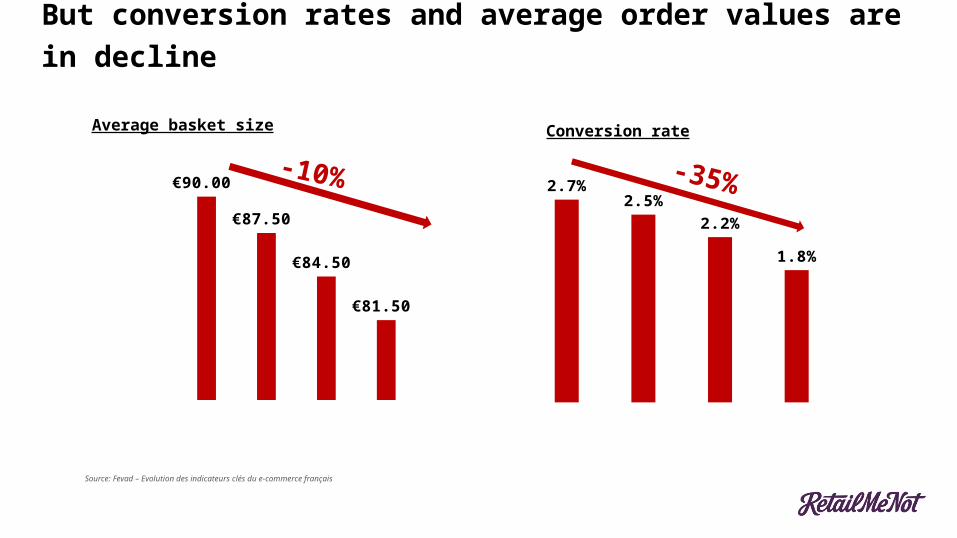

€90.00

€87.50

€84.50

€81.50

-10%

2011 2012 2013 20140.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%2.7%

2.5%

2.2%

1.8%

But conversion rates and average order values are in decline

Source: Fevad – Evolution des indicateurs clés du e-commerce français

Average basket size Conversion rate

-35%

Mobile is disrupting the industry

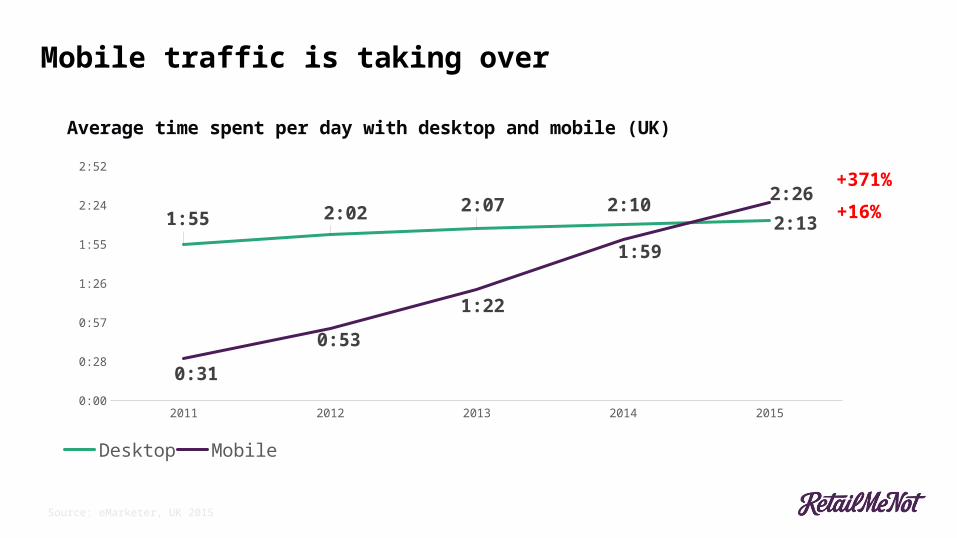

Mobile traffic is taking over

2011 2012 2013 2014 20150:00

0:28

0:57

1:26

1:55

2:24

2:52

1:55 2:02 2:07 2:102:13

0:31

0:53

1:22

1:59

2:26

Average time spent per day with desktop and mobile (UK)

Desktop Mobile

+16%

+371%

Source: eMarketer, UK 2015

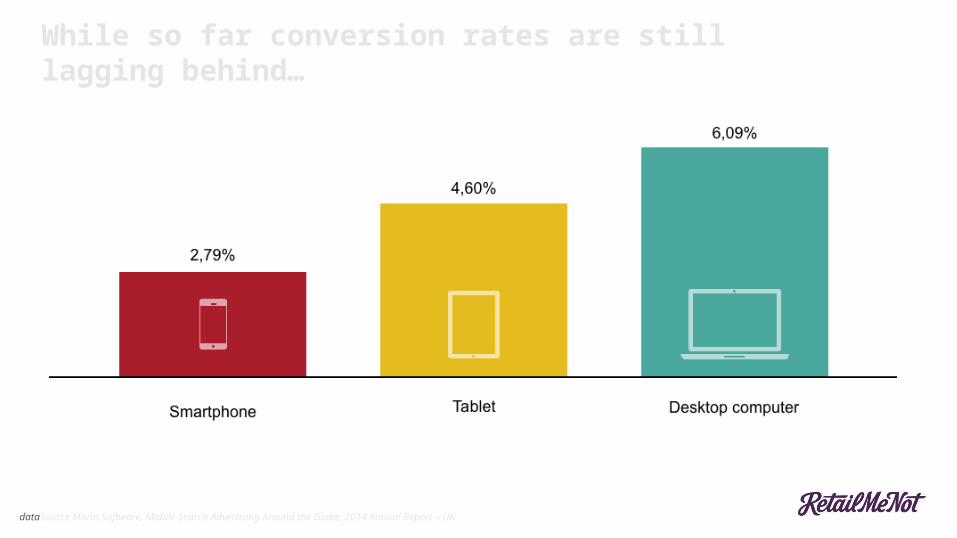

dataSource Marin Software, Mobile Search Advertising Around the Globe, 2014 Annual Report – UK

Conversion rates by channel

While so far conversion rates are still lagging behind…

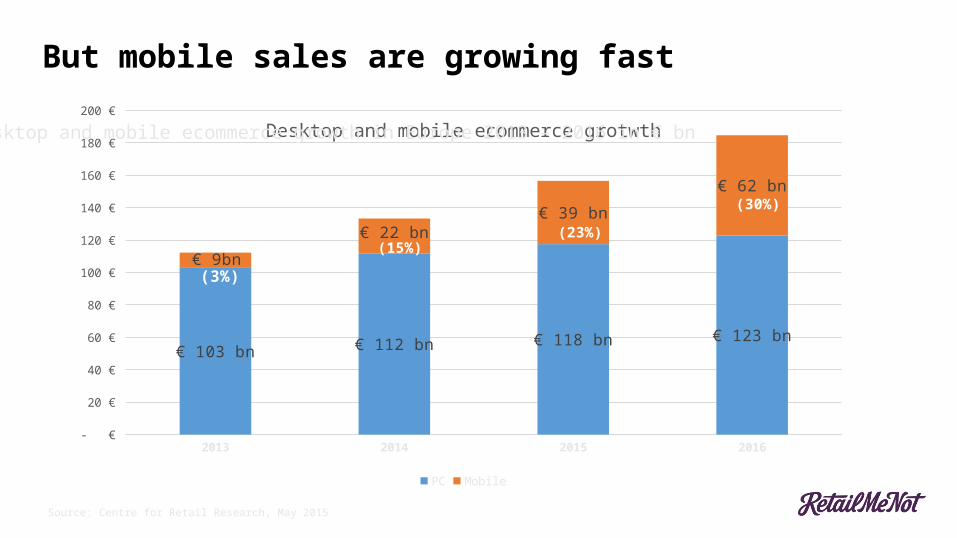

But mobile sales are growing fast

2013 2014 2015 2016 - €

20 €

40 €

60 €

80 €

100 €

120 €

140 €

160 €

180 €

200 €

€ 103 bn € 112 bn € 118 bn € 123 bn

€ 9bn

€ 22 bn€ 39 bn

€ 62 bn

Desktop and mobile ecommerce grotwth

PC Mobile

(3%)

(15%)(23%)

(30%)

Desktop and mobile ecommerce growth in Europe 2013 – 2016 in € bn

Source: Centre for Retail Research, May 2015

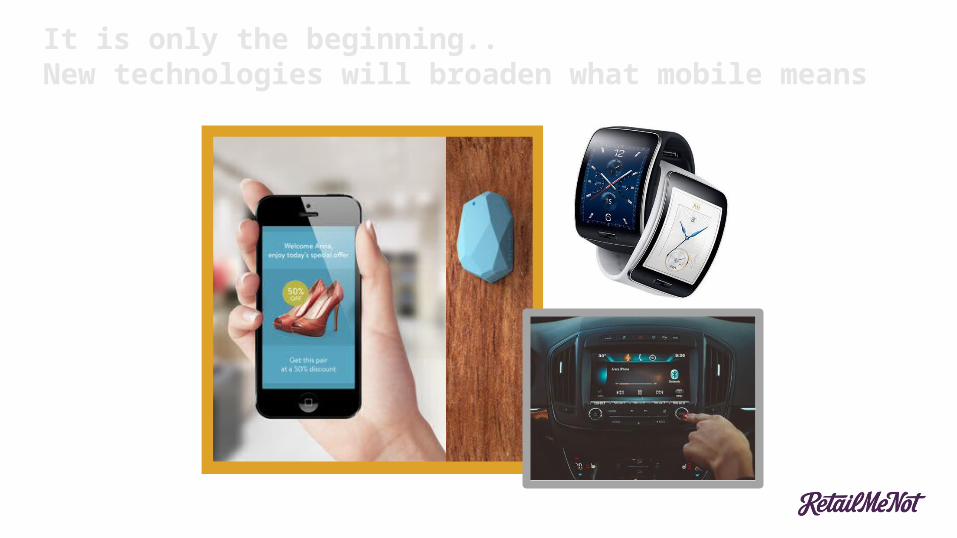

It is only the beginning..New technologies will broaden what mobile means

REVENUE = TRAFFIC x CONVERSION x BASKET VALUE

PROFIT = REVENUE - INVESTMENTS

Consumer have changed their

mindset…

The perception of the right price is shifting

Leaving 4 out of 5 consumers think that a product sold without any discount is overpriced

Source: CCM Benchmark, 2013

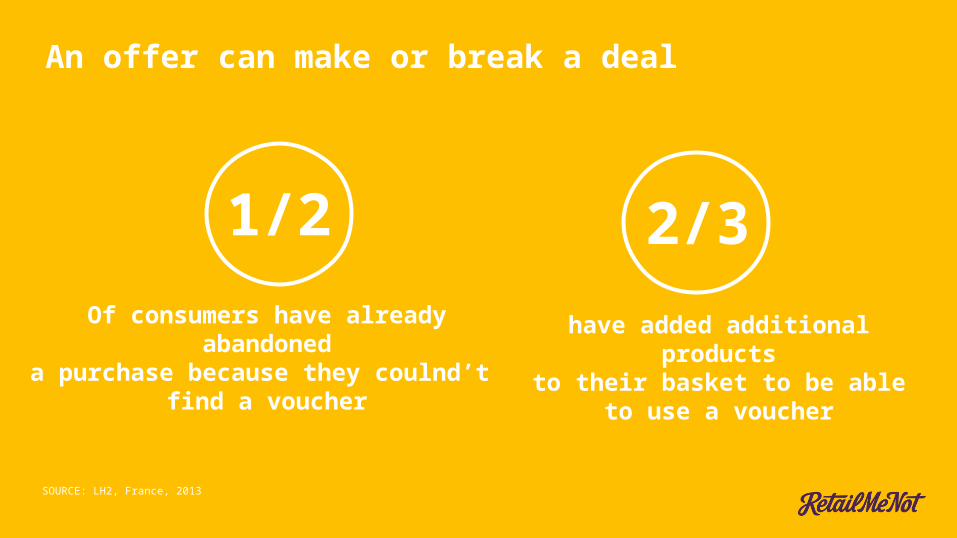

SOURCE: LH2, France, 2013

1/2 2/3Of consumers have already

abandoned a purchase because they coulnd’t

find a voucher

have added additional productsto their basket to be able to use

a voucher

An offer can make or break a deal

Category 1 Category 2 Category 3 Category 40

2

4

6

8

10

12

14 Series 3

Series 2

Series 1

Sources: Deloitte Digital, Forrester Research (2014), RetailMeNot and The Omnibus Company (April 2013).

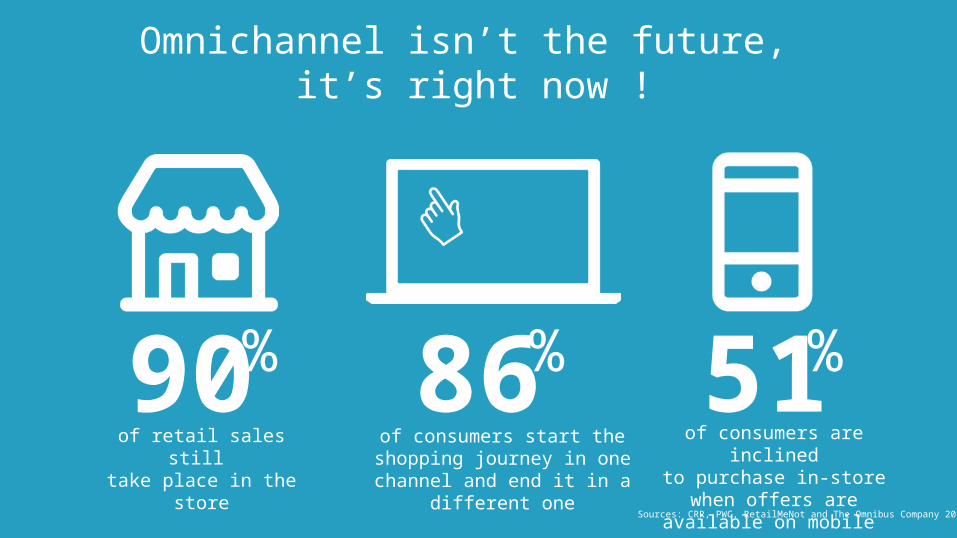

Omnichannel isn’t the future, it’s right now !

86 51of retail sales still

take place in the storeof consumers are inclinedto purchase in-store when

offers are available on mobile

% % %

Sources: CRR, PWC, RetailMeNot and The Omnibus Company 2013

90of consumers start the shopping journey in one channel and end it

in a different one

Consumers think about products & brands,

not channels!

Consumer seek « the right price »

What does this mean to brands and retailers?

Rule #1 – Listen to your customers

Source Deloitte, the Omnichannel Opportunity, 2014 amount spent on the most recent purchase

A clear mismatch between consumers’ expectations and what retailers offer

Explore& find Buy

Of consumers expect to find the same

promotions online as instore

Of retailers offer the same price online

and instore

Of consumersexpect to buy online and pick-up in store

Of retailersoffer this service

73%

Only

16% 30%

50%

Source Deloitte, the Omnichannel Opportunity, 2014 amount spent on the most recent purchase

And multi-channel shoppers spend more!

offline online

Boughtoffline

Bought offline, online research

prior to purchase

Boughtonline

Bought online, additional store research prior to purchase

€101

€158 €148

€106

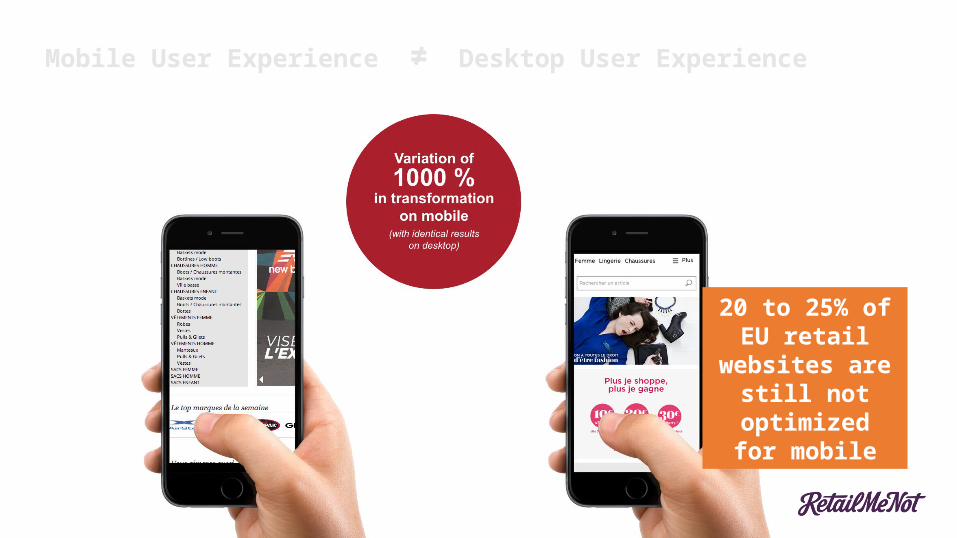

Rule #2 – Mobile ≠ Desktop

Mobile User Experience ≠ Desktop User Experience

20 to 25% of EU retail websites

are still not optimized for

mobile

Rule #3 – Location matters

(go where the consumer is)

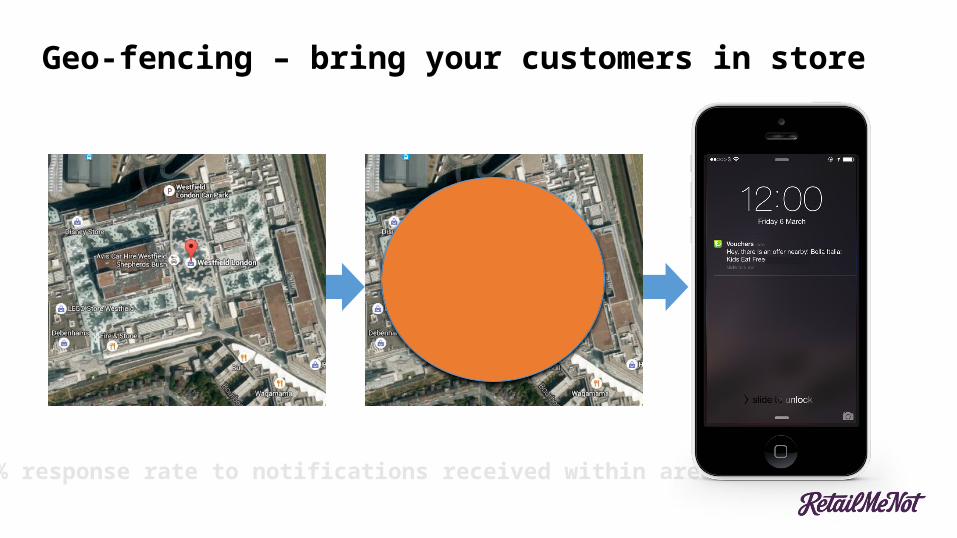

Geo-fencing – bring your customers in store

51% response rate to notifications received within area

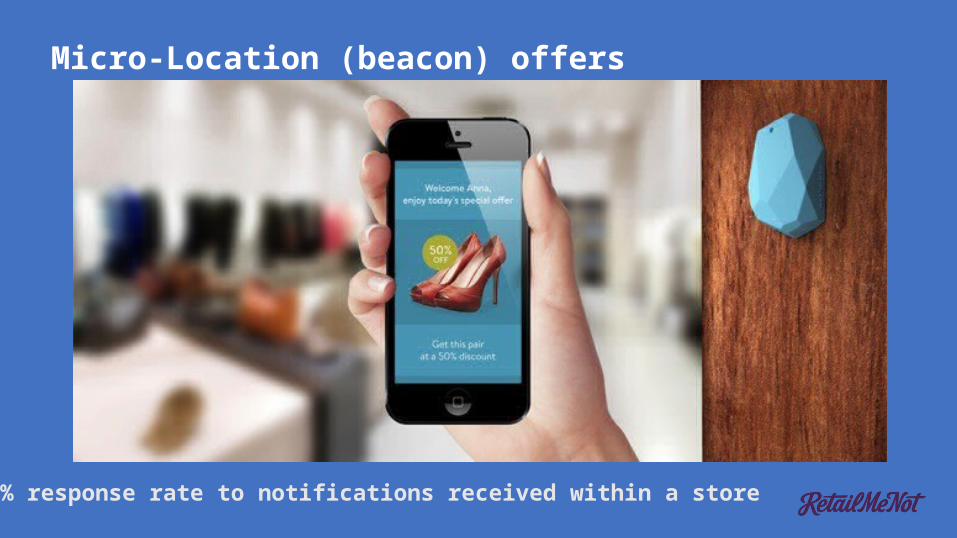

Micro-Location (beacon) offers

63% response rate to notifications received within a store

Rule #4 – Make it personal (but make it right)

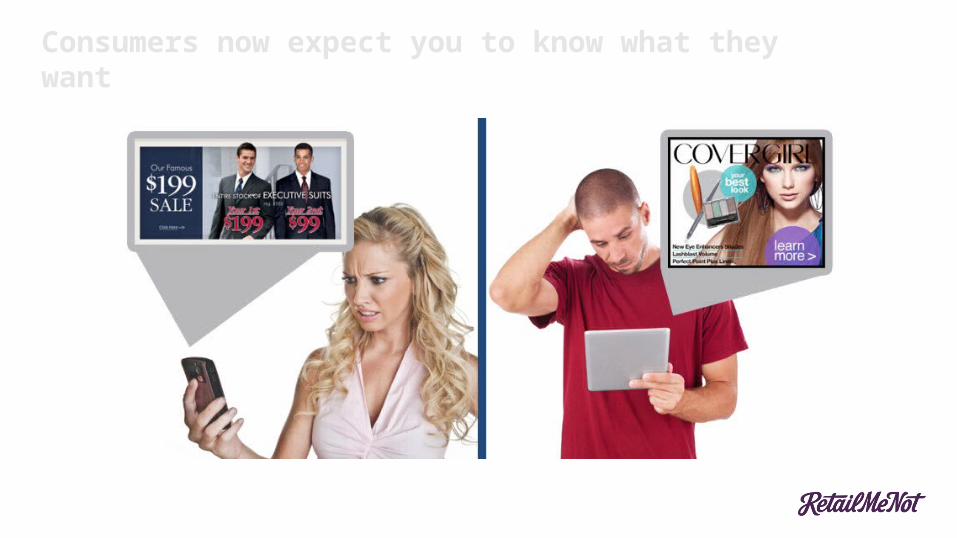

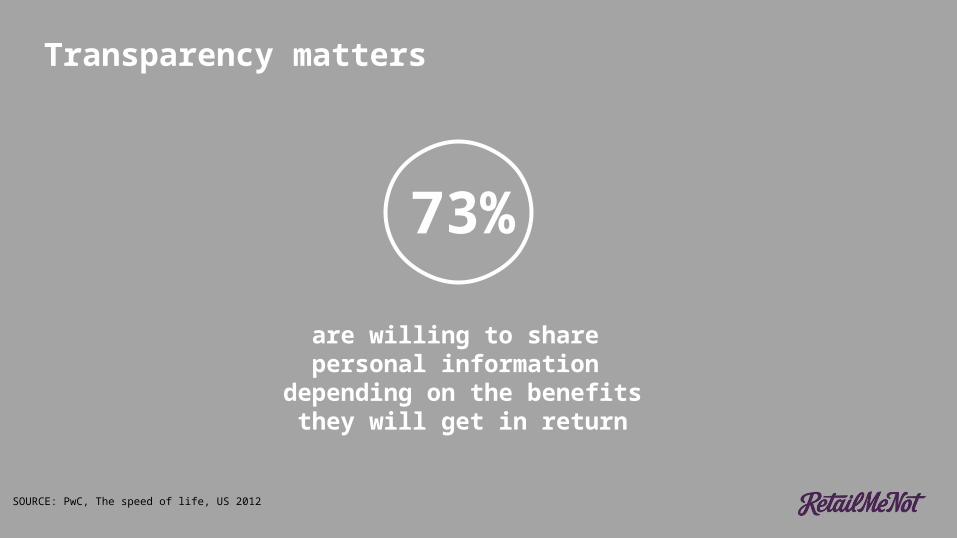

Consumers now expect you to know what they want

SOURCE: PwC, The speed of life, US 2012

73%

are willing to share personal information

depending on the benefitsthey will get in return

Transparency matters

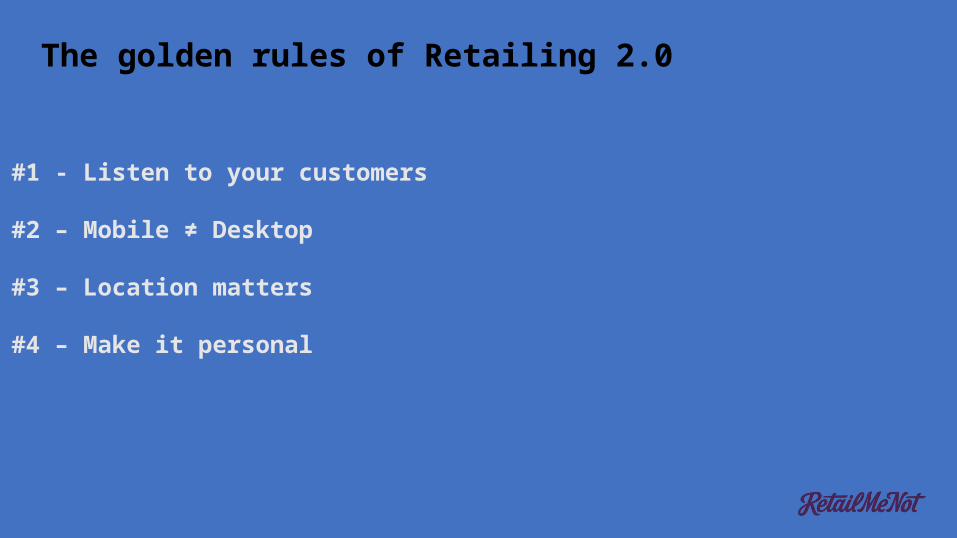

The golden rules of Retailing 2.0

#1 - Listen to your customers

#2 – Mobile ≠ Desktop

#3 – Location matters

#4 – Make it personal

REVENUE = TRAFFIC x CONVERSION x BASKET VALUE

PROFIT = REVENUE - INVESTMENS

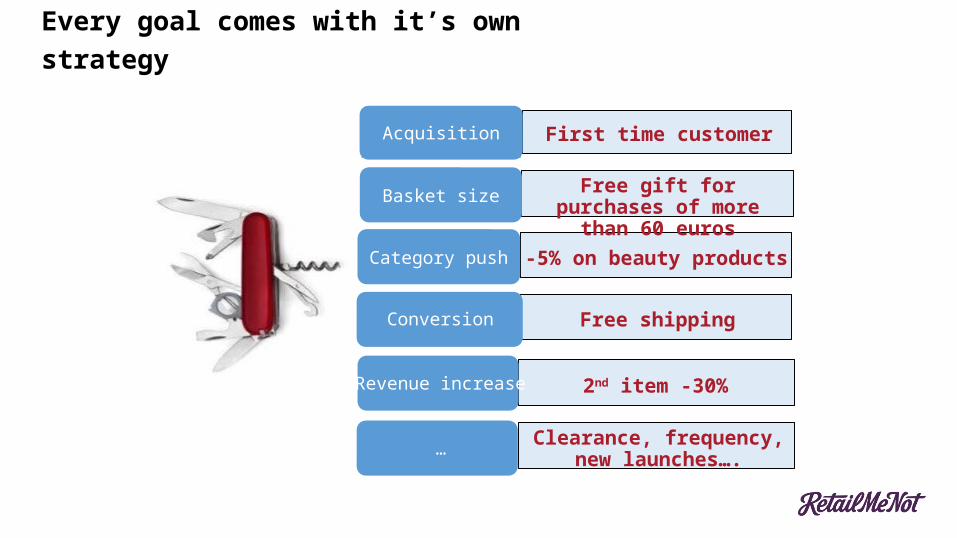

Every goal comes with it’s own strategy

Acquisition

Basket size

Category push

Conversion

Revenue increase

… Clearance, frequency, new launches….

2nd item -30%

First time customer

Free gift for purchases of more than 60 euros

Free shipping

-5% on beauty products

Case Study InStoreThe Body Shop (UK)

Objective: Drive footfall and storeand generate new sign-ups

Incentive: Free lip balm (value £3; exclusive for our members)

What we’ve done: - Push notifications sent to 1.2 million users- Dedicated code alert email, sent to 6.9 million members- Prominent listing on the app (2.9 million downloads)- Vouchercodes.co.uk homepage (5.7 million visits/month)- Editorial and social media coverage, including blog, Twitter and Facebook

Results

• +50k customers driven in store in 11 days

• 41k new customers recruited

• £93k of additional sales

Retail Challenges, Solved.

DRIVE online and in-store sales

INCREASE average order value

ACCELERATE new customer acquisitionBOOST customers revenue

RE-ENGAGE lapsed consumers

Let’s prepare tomorrow

As she walks past a Douglas partner store, she receives an offer of a discount of 3,50 € on Nivea lotions, only available todayShe lives in

Berlin, and it’s one of the first sunny days of the year

Julia is 30 years old and has sensitive skin.

Sending the right offers to the right person at the right moment incites spontaneous purchases