Embed Size (px)

Citation preview

‘How to prevent bad debt and maximise profit’

Colin Sanders

Welcome to the webinar

We will start at 02:00 p.m.

Philip King

Introduction

• About CICM & Graydon

• Presentation

• Discussion

• Q&A

Philip King & Colin Sanders

About CICM

www.cicm.com

• Europe’s largest professional association for the credit community. • Expertise for all credit and collections matters, it represents the

profession across trade, consumer and international credit, and all credit-related services.

• We help organisations manage credit and maximise cash collection efficiently.

• Highest standards in range of training and regulated qualifications that have become the recognised standard in the credit profession.

About Graydon

www.graydon.co.uk

• Graydon believes that transparency boosts trust between businesses. • Convert data from diverse data sources into information. Based on this

information, we generate invaluable economic, financial and commercial insights that help our customers make better business decisions and ultimately gain competitive advantage.

• Leading provider of credit information to the business community, a trusted supplier and recognised as one of the leading CRA’s in the UK by our clients and the credit insurance sector for providing information.

Before we move on….

What is bad debt prevention and what do we mean by profit?

What does it take to be a Savvy Credit Manager? The agenda:

Understanding Credit Risk

1. How to analyse your (potential) customer throughout the life cycle

2. How to use (credit) information that will grow your business

3. How to handle sales pressure and stick to the facts

4. How to spot and prevent fraud

5. How to think outside of the box

1. Analyse the (potential) customer throughout the life cycle

“It’s not just about the maths and assessment never ends.”

Check the customer during the life cycle

Credit Marketing

Acquisition

Account management

Collections

• Pre checks with reliable data sources to acquire profitable customers

• Continually assess your customer through analytics

• Keep the dialogue alive with your customer and sales

• Stick to simple guidelines to always Know Your Customer (KYC)

“The key is to really know your customer.”

1. Be aware, that you can never know enough

2. Take emotion out of the system by following simple guidelines

3. Analyse new and existing customers

4. There is no such thing as a brand new business

5. Ask questions about the history

6. Use both internal and external data sources to investigate

Key pointers to KYC

1. Check the company when you want to do business

2. Set up a policy for monitoring your customers

3. Use different internal and external sources

4. Align and combine different sources to get a 360 degree view

5. Communicate your credit policy internally

Checklist KYC Guide Lines

“There is no such thing as a brand new business.”

2. How to use (credit) information to grow your business?

Poll

I share credit information across different departments, like marketing and sales:

Always

Sometimes

Never

“Knowing all about your customer and market is not a one stop shop.”

Use internal data sources

CRM

Marketing database

ERP

Sales dialogue

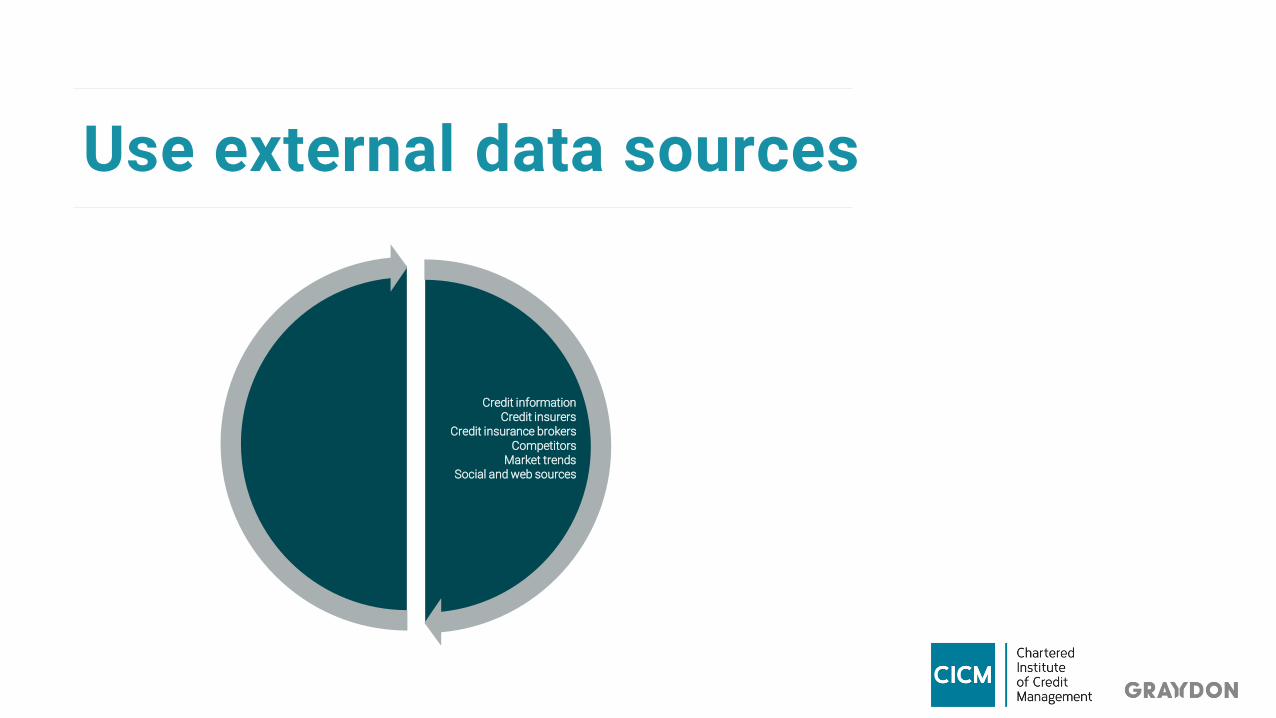

Use external data sources

Credit information Credit insurers

Credit insurance brokers Competitors

Market trends Social and web sources

What's your risk appetite?

Credit insurers Credit insurance brokers

Competitors Social and web sources

Credit Risk

Policy

Company Vision Long term goals

Executive input

Risk appetite Growth targets

ROI targets

Credit Underwriting standards Regulatory requirements

Collateral requirements

Operational standards Process description

Accountability

3. How to handle sales pressure and stick to the facts?

Poll

How would you describe your alignment with sales to improve your insights on markets and customers?

Very good

Good

Average

Bad

Very bad

“Sales are the life blood of any organisation. You don't sell, you don't make profit, it’s as simple as that.”

1. Sales and credit professional need to understand each other’s role within your organisation

2. Don’t just say no to a deal, but look for solutions (like pro forma/cash basis deals)

3. Make sure they understand why a no is a no

4. Communicate your credit policy with sales

5. Make sure sales uses financial insights to know what the profitable markets and customers are

How to handle sales pressure and improve business?

4. How to spot and prevent fraud?

Poll

How often do you check your procedures to ensure you avoid fraud?

Quarterly

Half yearly

Yearly

Biyearly

Hardly ever

“The job of credit managers and controllers has changed due to the risk of fraud.”

Situation:

• Application received by our timber client requesting 40K and XXXXX company for 100K. Also, XXXXX company for 15K. Signature on 31 May 15 accounts is not the same as signature on all apps.

• Trading allegedly changed from meat transporters to building houses. They also have an outstanding debt with a major sugar supplier who are owed £150K. They have approached several timber customers.

Prevention:

• Research by Graydon on facts.

• Could not find old website, date of establishment does not correspondent with Graydon database.

Result:

• Prevented a fraud deal of 155K.

Case study (1): James H. Yates

Case study (1): James H. Yates

• And these were the supposed trading premises.

• Note the “To Let” sign

Yes, this really was a company that was set up.

Note the trading address. Isn’t this near to where “Del Boy” and “Rodney” lived?

Case study (2): Deltacap

There are many tips to avoid fraud, many more in the book but here are just a few:

A. Scrutinise the application form. Has it been completed in full? Do take up

references. Fraudsters expect you not to. B. Check signatures from the application form against Companies House

documentation. C. Validate VAT numbers. D. Check supposed trading premises via “Google Earth”. You can spot virtual offices

quite easily from this as well as spotting empty premises which are allegedly being used.

E. What type of telephone number is being used? A mobile number? Non-geographical, i.e., 0345, 0845 etc.

How to prevent fraud?

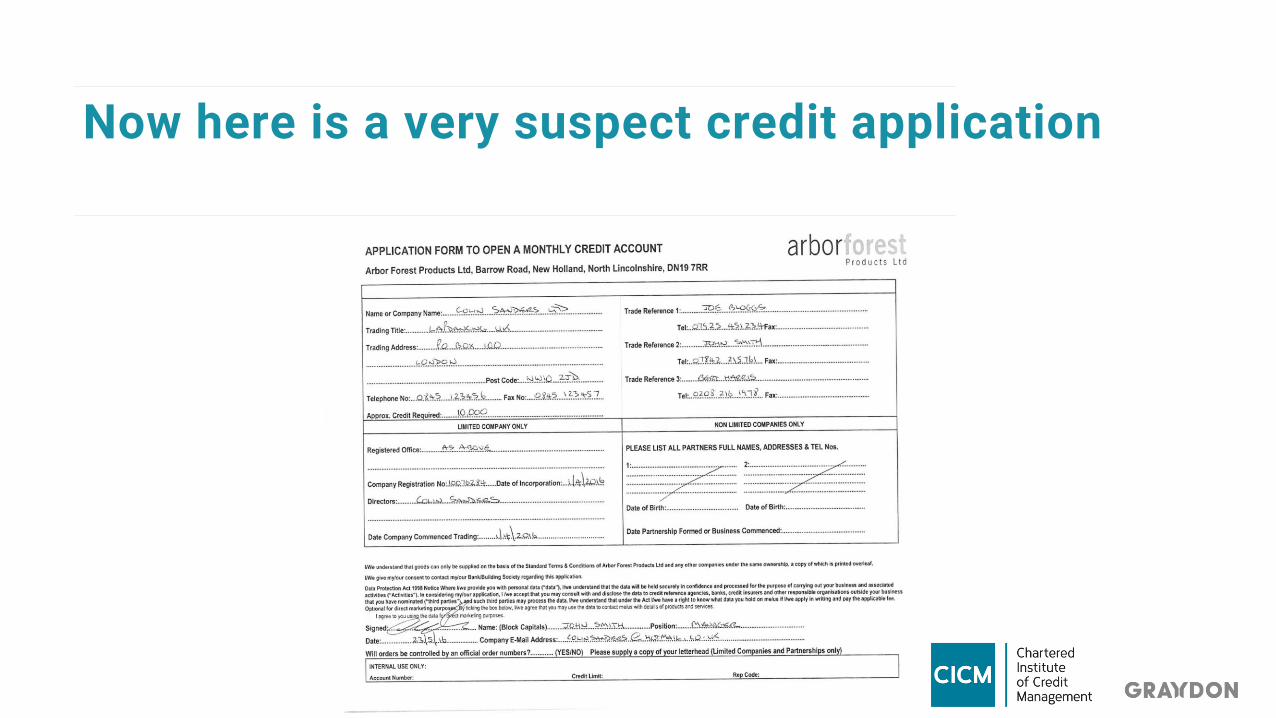

Now here is a very suspect credit application

5. How to think outside of the box?

“The key is to have your policy and sources in place, but never forget to use your common sense.”

• Research, research and research some more

• Know both your customer and their industry sector

• It’s not always about the maths

• If it looks too good to be true, it probably is

• Get the “now” situation on your customer /prospect

Key pointers

• Work with sales, not against them but....

• If that sales application is not 100% complete, reject it!

• Take up trade refs but remember, an independent one is pure Gold

• Training is available, use it to stay up to date on procedures

• Complacency is the mother of bad debts

Any questions? Please contact us or download the guide:

www.graydon.co.uk/downloads [email protected]

www.graydon.co.uk

www.cicm.com