Embed Size (px)

Citation preview

Introduction

• This is the Gera Pune Residential Realty Report for January ’15 to June ‘15. The last report was released in January ‘15.

• A total of 3,067 live projects were tracked after a comprehensive listing exercise covering a radius of 30 km from the Pune City Center ( Shivaji nagar)

• The methodology for collecting information is based on proprietary interviewing techniques developed in-house

© Gera Developments Pvt. Ltd. 2

Key Metrics Tracked

• Price per sqft. – This is the quoted price per sqft.

• Total Units Launched - This is the Total Number of Units that have

been Launched ( Sold + Unsold )

• Supply – Unsold units

• Newly Launched – These are Projects that are Newly Launched

• % Units Sold Since Launched - This is the sellout ratio

• Offtake – The number of units sold between two tracks

• Stage of Construction – Early, Mid, End & Ready

• Location – Micromarket the project is situated in (roughly 140 micro

markets )

* All data is collected building wise . If the project has 5 buildings then data is collected for each building and then aggregated. © Gera Developments Pvt. Ltd. 3

Executive Summary

• Residential market under stress

• Regulatory changes will add to the challenges

• Challenging & competitive times lead to the emergence of a better product, more customer centricity, greater customer focus on delivery track records

• Slow down in price appreciation from 12.47% for June ’12 – June ’13 to 10.03% from June ’13 – June ’14 and now down to 3.33% for June ’14 – June ’15

• The half yearly growth rate has also slowed down from 3.04% during the period June ’14 – Dec ’14 down to 0.27% for the period January ’15 - June ’15

© Gera Developments Pvt. Ltd. 4

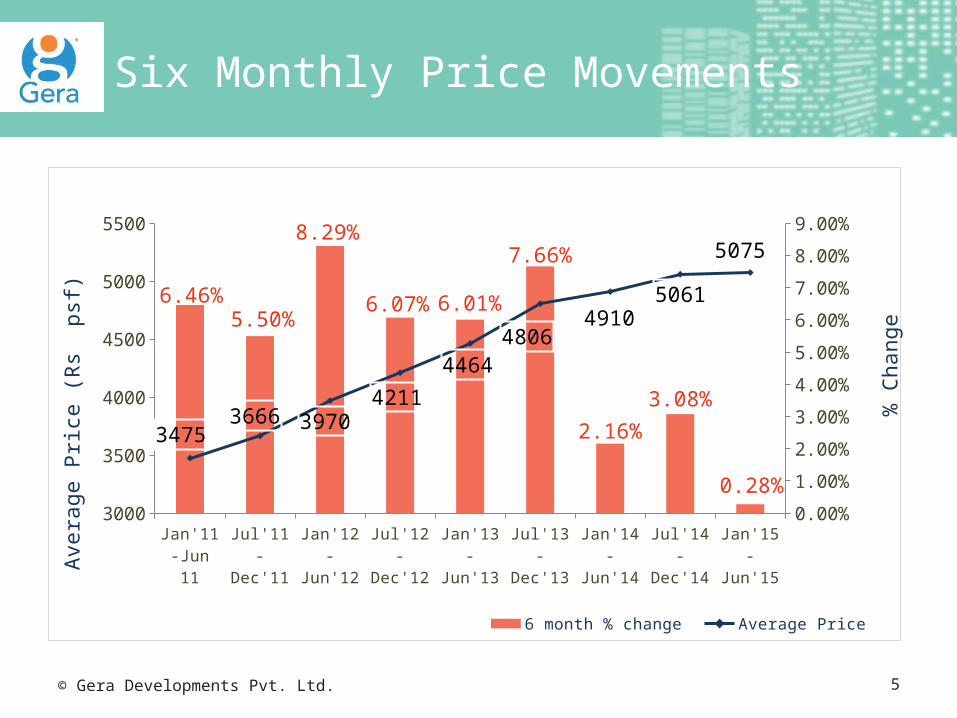

Six Monthly Price Movements

Jan'11 -Jun 11

Jul'11 -Dec'11

Jan'12 -Jun'12

Jul'12 -Dec'12

Jan'13 -Jun'13

Jul'13 -Dec'13

Jan'14 -Jun'14

Jul'14 -Dec'14

Jan'15 -Jun'15

3000

3500

4000

4500

5000

5500

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

6.46%5.50%

8.29%

6.07% 6.01%

7.66%

2.16%

3.08%

0.28%

34753666 3970

4211

44644806

49105061

5075

6 month % change Average Price

Ave

rage P

rice

(R

s p

sf)

% C

hange

© Gera Developments Pvt. Ltd. 5

Overall Supply

• The past12 months has seen a significant increase of 14.36% in the gross inventory from 245,639 (June ’14) to 280,913 (June ’15) units

• The unsold stock (inventory with developers for sale) has shown a steep jump of 36.85% in the same period from 66,350 (June ’14) to 90,799 (June ’15) units

© Gera Developments Pvt. Ltd. 6

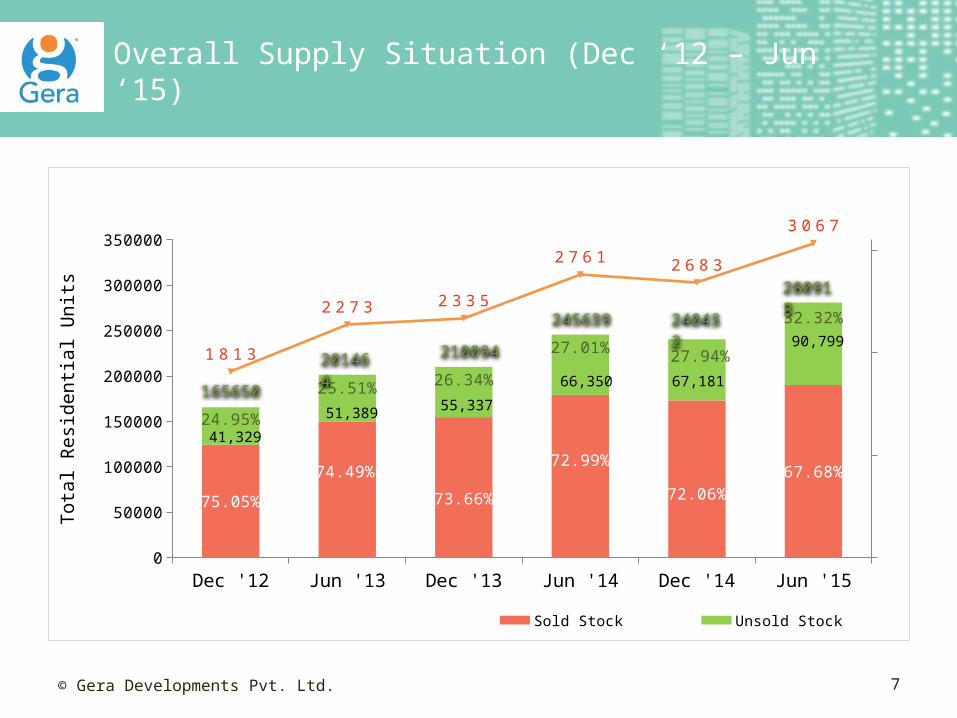

Overall Supply Situation (Dec ‘12 – Jun ‘15)

Dec '12 Jun '13 Dec '13 Jun '14 Dec '14 Jun '150

50000

100000

150000

200000

250000

300000

350000

75.05%

74.49%

73.66%

72.99%

72.06%67.68%

24.95%

25.51% 26.34%

27.01% 27.94%

32.32%

1 8 1 3

2 2 7 3 2 3 3 5

2 7 6 1 2 6 8 3

3 0 6 7

Sold Stock Unsold Stock No of Projects

To

tal R

esi

de

nti

al U

nit

s

165650

201464

210094

245639

280913

240432

© Gera Developments Pvt. Ltd. 7

90,799

67,18166,350

55,33751,389

41,329

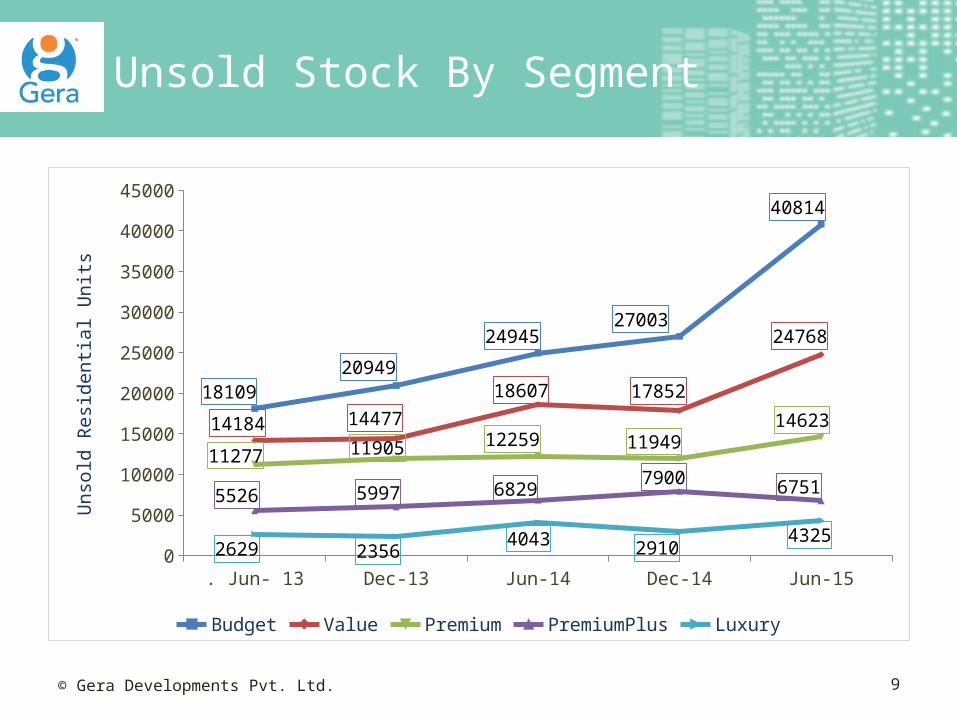

Unsold Stock By Segment

• The Budget Category (where prices presently are below Rs.4,247 psf) has seen an increase of 125% from 18,019 unsold units to 40,814 unsold units.

• The next highest increase is the Value Category (current prices between Rs.4,248 & Rs.5,309 psf) with an increase of 75% from 14,184 units to 24,768 units.

• The Luxury Segment has the next highest increase in unsold inventory at 65% from 2,629 units unsold rising to 4,325 units.

• The Premium and Premium Plus category have relatively low increases at 30% & 22% respectively.

© Gera Developments Pvt. Ltd. 8

Unsold Stock By Segment

. Jun- 13 Dec-13 Jun-14 Dec-14 Jun-150

5000

10000

15000

20000

25000

30000

35000

40000

45000

1810920949

2494527003

40814

14184 1447718607 17852

24768

11277 11905 12259 1194914623

5526 5997 68297900 6751

2629 23564043 2910

4325

Budget Value PremiumPremiumPlus Luxury

Un

sold

Re

sid

en

tia

l U

nit

s

© Gera Developments Pvt. Ltd. 9

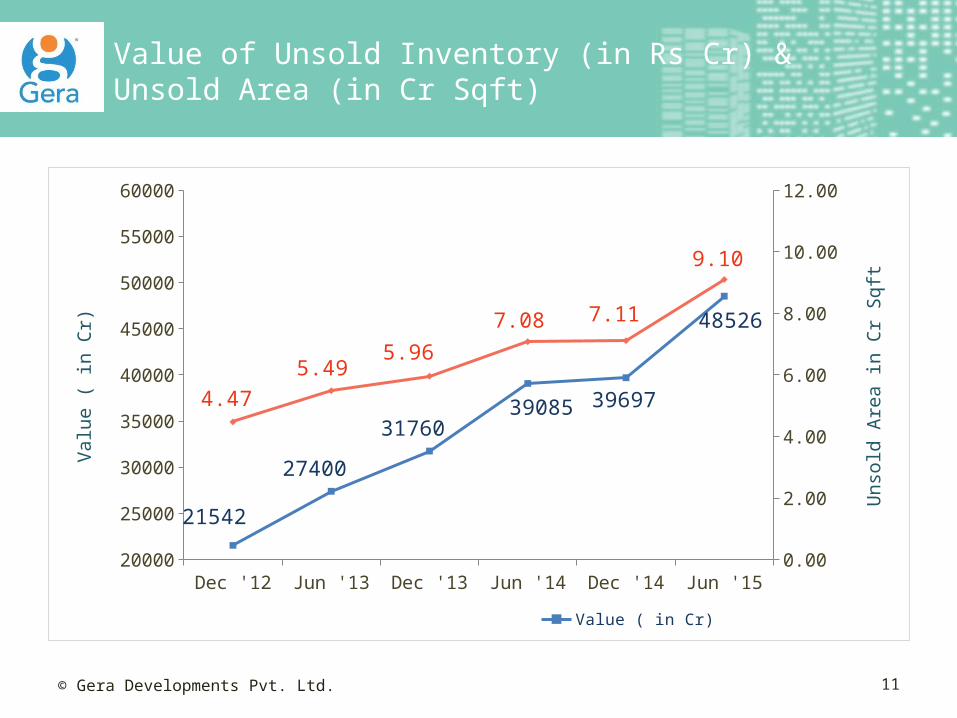

Value of Unsold Inventory (in Rs Cr) & Unsold Area (in Cr Sqft)

• The gross value of the unsold inventory stands at Rs.48,526 crores.

• Opportunity for the state government to garner nearly Rs.3000 crores by way of stamp duty, LBT & VAT.

© Gera Developments Pvt. Ltd. 10

Value of Unsold Inventory (in Rs Cr) & Unsold Area (in Cr Sqft)

Dec '12 Jun '13 Dec '13 Jun '14 Dec '14 Jun '1520000

25000

30000

35000

40000

45000

50000

55000

60000

0.00

2.00

4.00

6.00

8.00

10.00

12.00

21542

27400

3176039085 39697

48526

4.47

5.495.96

7.08 7.11

9.10

Value ( in Cr) Unsold area (in Cr Sqft)

Va

lue

( in

Cr)

Un

sold

Are

a in

Cr

Sq

ft

© Gera Developments Pvt. Ltd. 11

Fresh Supply Launched (PMC vs Non PMC)

• Only 24.55% of the stock added between January ’15 to June ’15 is within PMC limits indicating that most of the incremental stock is added outside the Pune Municipal Corporation limits.

• Indicates the growth of the city outward.

• Will lead to declining revenues by way of development charges and premiums for the PMC.

© Gera Developments Pvt. Ltd. 12

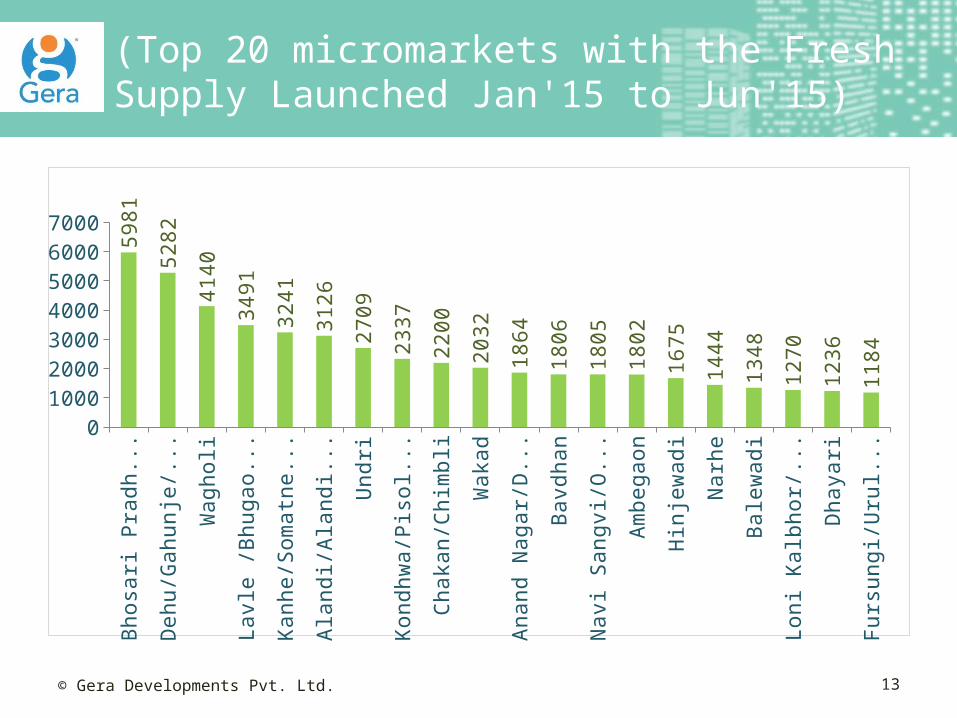

(Top 20 micromarkets with the Fresh Supply Launched Jan'15 to Jun'15)

Bhosa

ri P

radhik

a..

.

Dehu/G

ahunje

/K..

.

Wagholi

Lavl

e /

Bhugaon..

.

Kanhe/S

om

atn

e .

..

Ala

ndi/A

landi R

o..

.

Undri

Kondhw

a/P

isoli/

...

Chaka

n/C

him

bli

Waka

d

Anand N

agar/

Da..

.

Bavd

han

Navi

Sangvi

/Old

...

Am

begaon

Hin

jew

adi

Narh

e

Bale

wadi

Loni K

alb

hor/

Uru

...

Dhaya

ri

Furs

ungi/U

ruli

D..

.01000200030004000500060007000

5981

5282

4140

3491

3241

3126

2709

2337

2200

2032

1864

1806

1805

1802

1675

1444

1348

1270

1236

1184

© Gera Developments Pvt. Ltd. 13

Fresh supply launched (PMC vs Non PMC)

Dec '12 Jun '13 Dec '13 Jun '14 Dec '14 Jun '150

10000

20000

30000

40000

50000

60000

70000

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

43457

51746

40935

60066

46826

63998

13934 15222 16703 1803613483 15709

32.06%

29.42%

40.80%

30.03%28.79%

24.55%

Pune ( PMC + Non PMC) PMC % PMC to Pune

© Gera Developments Pvt. Ltd. 14

Top 10 Micromarkets with the Highest Price Gains in the last 2 years

All

Ma

rke

ts

Ara

nye

shw

ar.

..

Aku

rdi/N

igd

i...

Era

nd

wa

ne

/...

Ma

nja

ri

Fu

rsu

ng

i/U

ru..

.

Bo

at

Clu

b R

...

Ma

rke

t Y

ard

...

Wa

rje

Ka

tra

j/K

he

d..

.

Ch

inch

wa

d..

.0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

13.6

7%

39.9

1%

29.8

1%

25.9

0%

22.6

8%

20.5

9%

18.5

7%

18.2

7%

17.9

2%

17.5

1%

17.1

4%

© Gera Developments Pvt. Ltd. 15

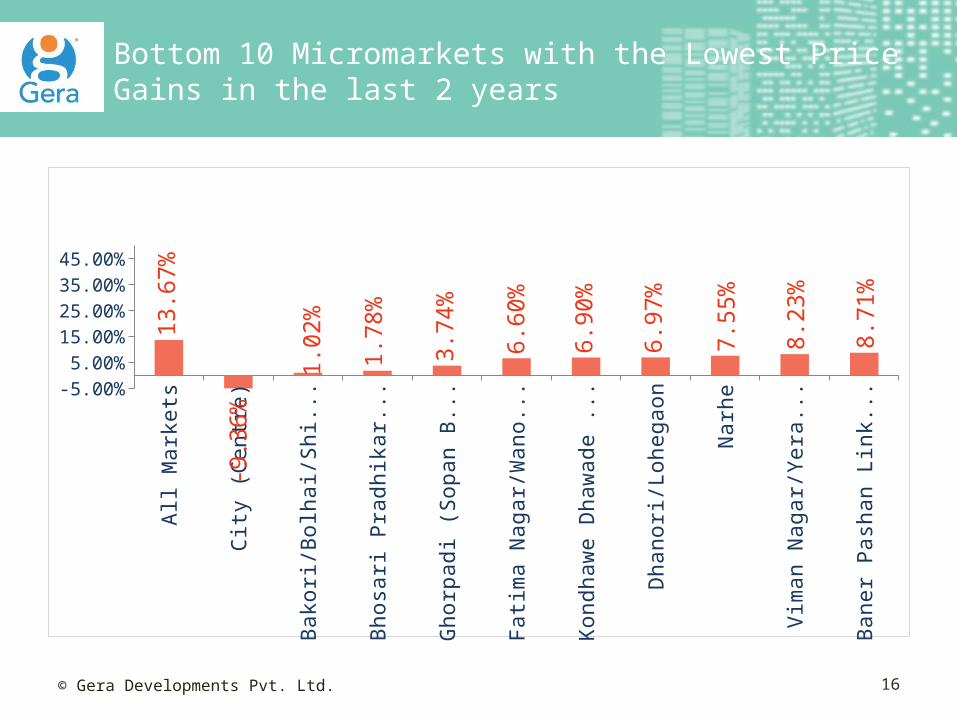

Bottom 10 Micromarkets with the Lowest Price Gains in the last 2 years

All

Mark

ets

Cit

y (C

entr

e)

Bako

ri/B

olh

ai/Shir

sat.

..

Bhosa

ri P

radhik

ara

n/C

...

Ghorp

adi (S

opan B

aug)

Fati

ma N

agar/

Wanow

r...

Kondhaw

e D

haw

ade /

...

Dhanori

/Lohegaon

Narh

e

Vim

an N

agar/

Yera

wada

Baner

Pash

an L

ink

R..

.-5.00%5.00%

15.00%25.00%35.00%45.00%

13.6

7%

-9.3

6%

1.0

2%

1.7

8%

3.7

4%

6.6

0%

6.9

0%

6.9

7%

7.5

5%

8.2

3%

8.7

1%

© Gera Developments Pvt. Ltd. 16

Conclusion

• Big picture shows a challenging scenario

• The market has expanded in terms of supply and at the same

time, while sales numbers have dropped, they continue to happen

• Prices will not see any significant correction unless something

drastic happens

• Regulatory impact will further push prices up when the time is

right (ReRA, MHA)

• Time is right to buy a home

• Govt. should focus on generating revenue by lowering tax rates

for faster sales, increased momentum & higher GDP

© Gera Developments Pvt. Ltd. 17