Embed Size (px)

Citation preview

TechnologyOfficeOutlook

United States2015

JLL TECHNOLOGY OFFICE OUTLOOK

tech’sfirmly planted roots

as well as opportunities for branching out.In examining

markets across the country for their attractiveness to the technology industry, we hope to showcase…

< 2 0 1 5 >

WHAT WE LEARNED < 2 0 1 5 >

Proximity to a hub is not necessarily enough: Local markets with an existing techcluster that are also more affordable than the Bay Area will likely experience accelerated industry growth as firms explore new marketsfor expansion.

1.Secondary markets are quickly catching up: In 2015, roughly 60% of unicorn companies were located in San Francisco and Silicon Valley, down from almost 76% in 2014.

2.Startup momentum will cost you: Markets with the greatest startup momentum, characterized by access to capital, innovation and top talent (such as New York, San Francisco and Silicon Valley), are also the most expensive.

3.

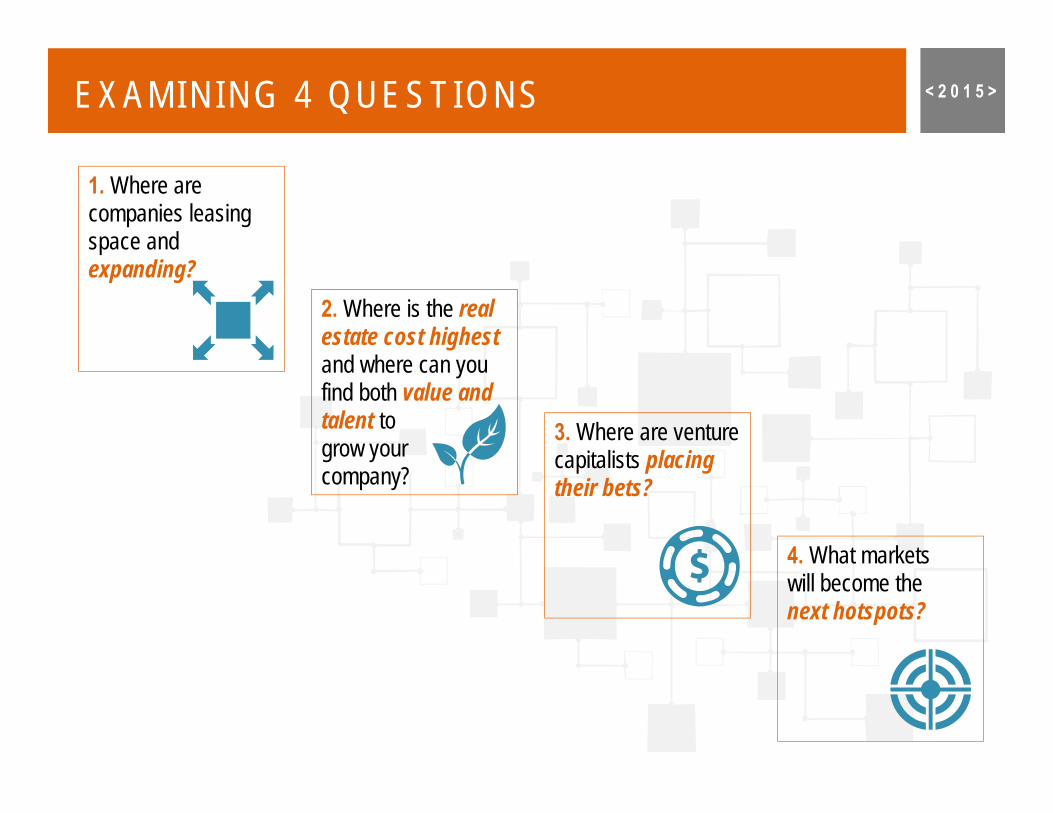

EXAMINING 4 QUESTIONS < 2 0 1 5 >

1. Where are companies leasing space and expanding?

3. Where are venture capitalists placing their bets?

4. What markets will become the next hotspots?

2. Where is the real estate cost highest and where can you find both value and talent to grow your company?

JLL TECHNOLOGY OFFICE OUTLOOK < 2 0 1 5 >

TECHis the elusive linchpin that

separates the growing companies from those that

are shrinking

JLL TECHNOLOGY OFFICE OUTLOOK < 2 0 1 5 >

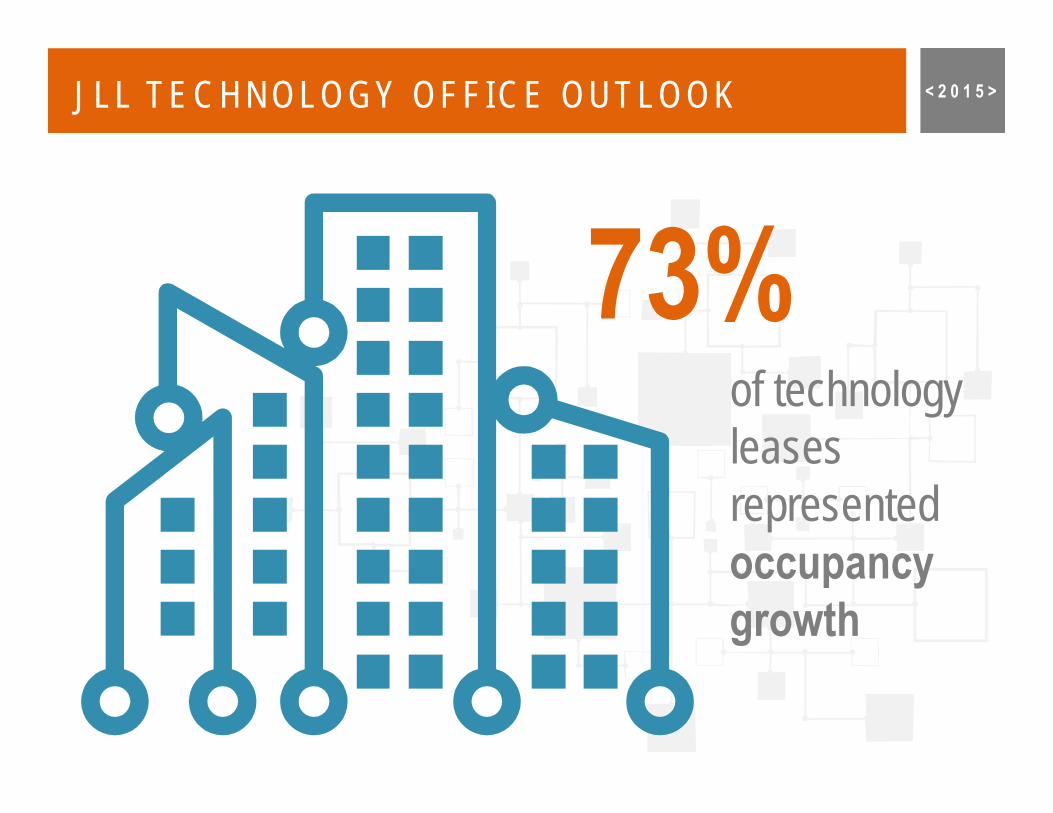

73% of technology leases represented occupancy growth

JLL TECHNOLOGY OFFICE OUTLOOK < 2 0 1 5 >

Secondary and tertiary markets are looking much more attractive to both young and mature companies as industry saturation in the most mature tech hubs has created both competitive and costly leasing environments.

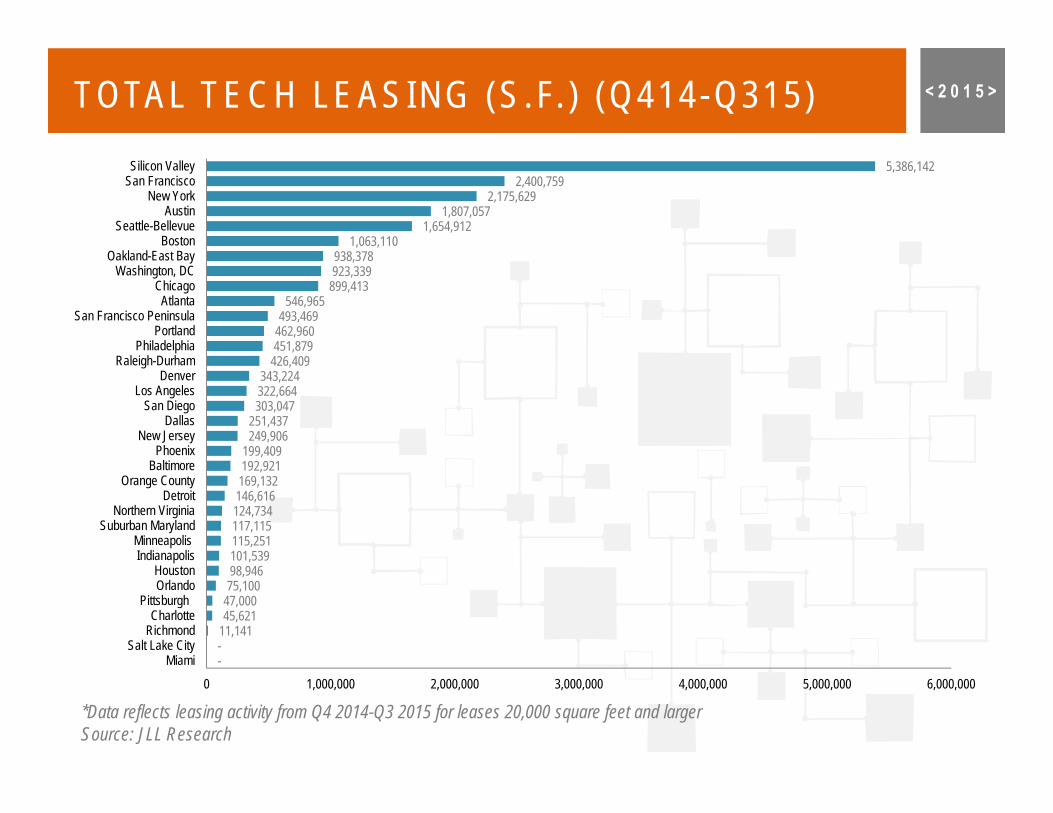

TOTAL TECH LEASING (S .F. ) (Q414-Q315) < 2 0 1 5 >

--11,141 45,621 47,000 75,100 98,946 101,539 115,251 117,115 124,734 146,616 169,132 192,921 199,409

249,906 251,437

303,047 322,664 343,224

426,409 451,879 462,960 493,469

546,965 899,413 923,339 938,378

1,063,110 1,654,912

1,807,057 2,175,629

2,400,759 5,386,142

0 1,000,000 2,000,000 3,000,000 4,000,000 5,000,000 6,000,000

MiamiSalt Lake City

RichmondCharlotte

PittsburghOrlandoHouston

IndianapolisMinneapolis

Suburban MarylandNorthern Virginia

DetroitOrange County

BaltimorePhoenix

New JerseyDallas

San DiegoLos Angeles

DenverRaleigh-Durham

PhiladelphiaPortland

San Francisco PeninsulaAtlanta

ChicagoWashington, DC

Oakland-East BayBoston

Seattle-BellevueAustin

New YorkSan FranciscoSilicon Valley

*Data reflects leasing activity from Q4 2014-Q3 2015 for leases 20,000 square feet and largerSource: JLL Research

JLL TECHNOLOGY OFFICE OUTLOOK < 2 0 1 5 >

Demand toward creative space is intensifying not only among technology companies but throughout the office-using

workforce and will begin to push rents

at a faster rate.

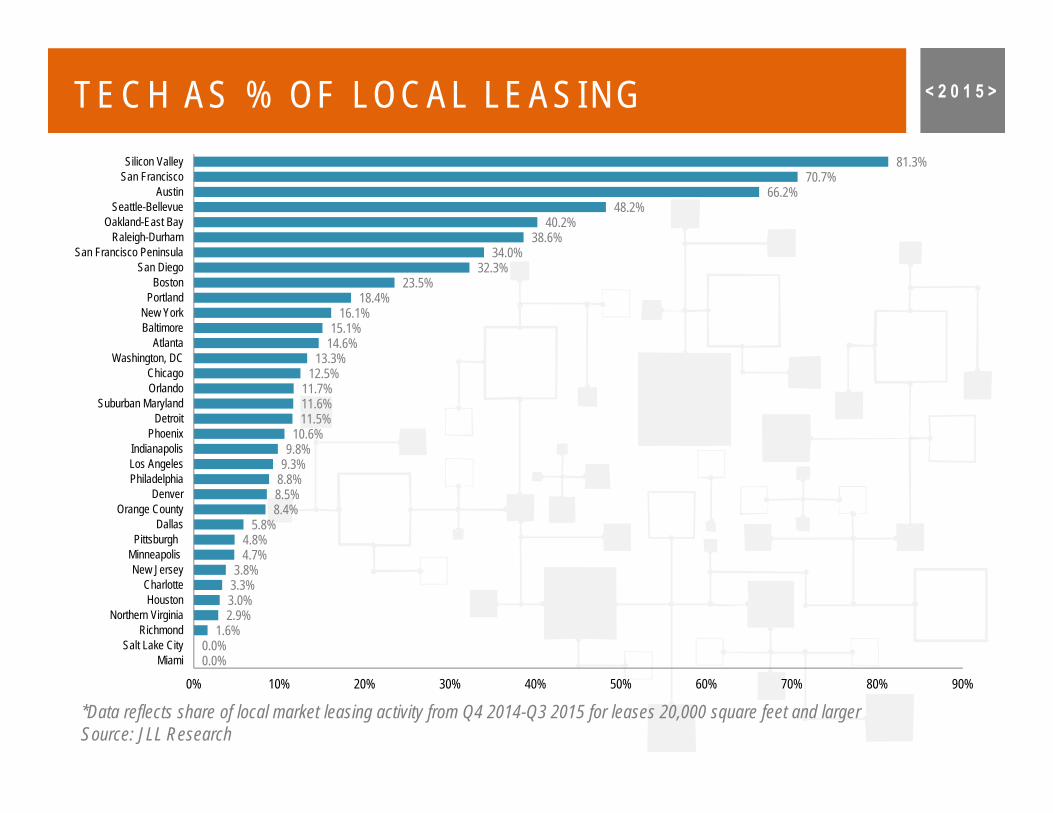

TECH AS % OF LOCAL LEASING < 2 0 1 5 >

*Data reflects share of local market leasing activity from Q4 2014-Q3 2015 for leases 20,000 square feet and largerSource: JLL Research

0.0%0.0%

1.6%2.9%3.0%3.3%3.8%

4.7%4.8%

5.8%8.4%8.5%8.8%9.3%9.8%

10.6%11.5%11.6%11.7%

12.5%13.3%

14.6%15.1%

16.1%18.4%

23.5%32.3%

34.0%38.6%

40.2%48.2%

66.2%70.7%

81.3%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

MiamiSalt Lake City

RichmondNorthern Virginia

HoustonCharlotte

New JerseyMinneapolis

PittsburghDallas

Orange CountyDenver

PhiladelphiaLos AngelesIndianapolis

PhoenixDetroit

Suburban MarylandOrlandoChicago

Washington, DCAtlanta

BaltimoreNew York

PortlandBoston

San DiegoSan Francisco Peninsula

Raleigh-DurhamOakland-East Bay

Seattle-BellevueAustin

San FranciscoSilicon Valley

JLL TECHNOLOGY OFFICE OUTLOOK < 2 0 1 5 >

Within the primary tech hubsthe technology industry’s saturation and fast growth has created highly competitiveleasing conditions.

JLL TECHNOLOGY OFFICE OUTLOOK < 2 0 1 5 >

With an average vacancy rate of 7.6%in the 15 most expensive tech submarkets,

tech companies in need of those locations must be

willing to pay.

MOST EXPENSIVE IN-DEMAND SUBMARKETS < 2 0 1 5 >

Market Submarket Average asking rent (Q3 2015)

1. Silicon Valley Downtown Palo Alto $98.682. Silicon Valley Downtown Mountain View $87.533. San Francisco Mission Bay/China Basin $81.504. New York Hudson Square $81.505. New York SoHo $79.806. New York Gramercy Park $76.587. San Francisco Peninsula Menlo Park* $73.448. San Francisco South Financial District $68.619. San Francisco North Financial District $68.53

10. Boston East Cambridge $67.2111. San Francisco South of Market $66.0712. Silicon Valley Cupertino $65.5213. San Francisco Peninsula Redwood City $63.0614. New York Greenwich Village $61.4915. Los Angeles Santa Monica $59.75

TOP 15

*Excludes Sand Hill Road

JLL TECHNOLOGY OFFICE OUTLOOK < 2 0 1 5 >

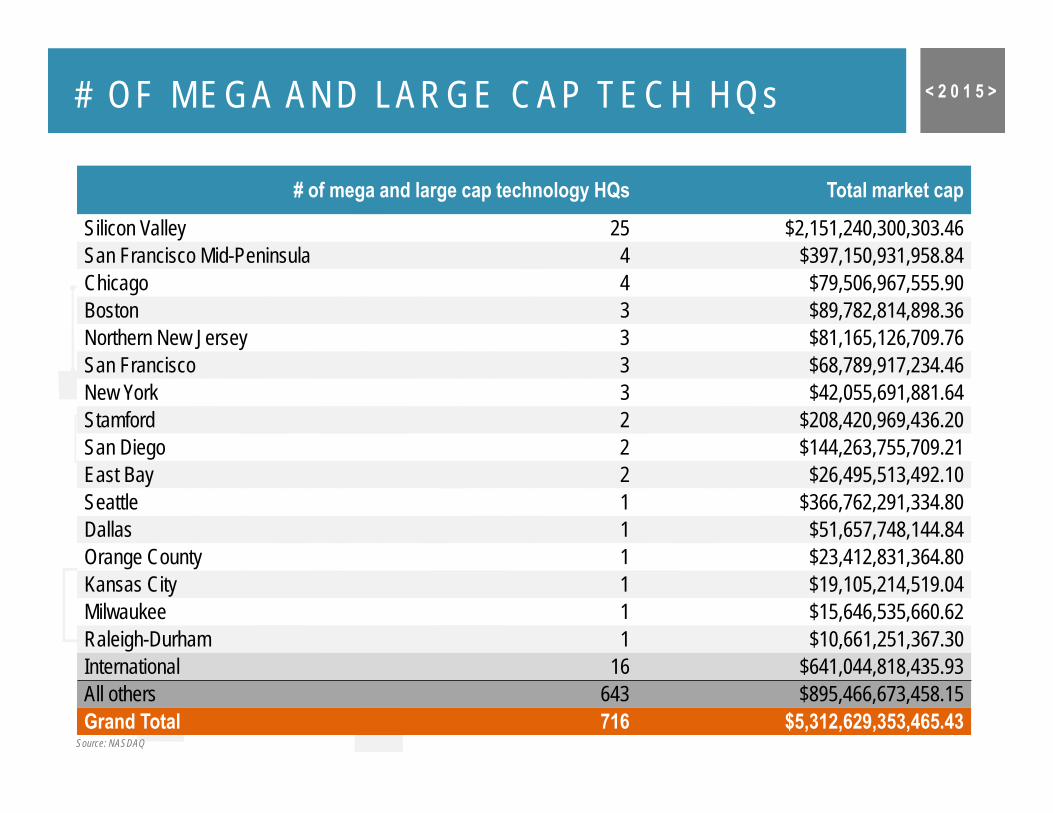

Does concentration of brand-name headquarter location present potential risk to

the market or does it simply affirm its place

as the epicenter of the technology industry?

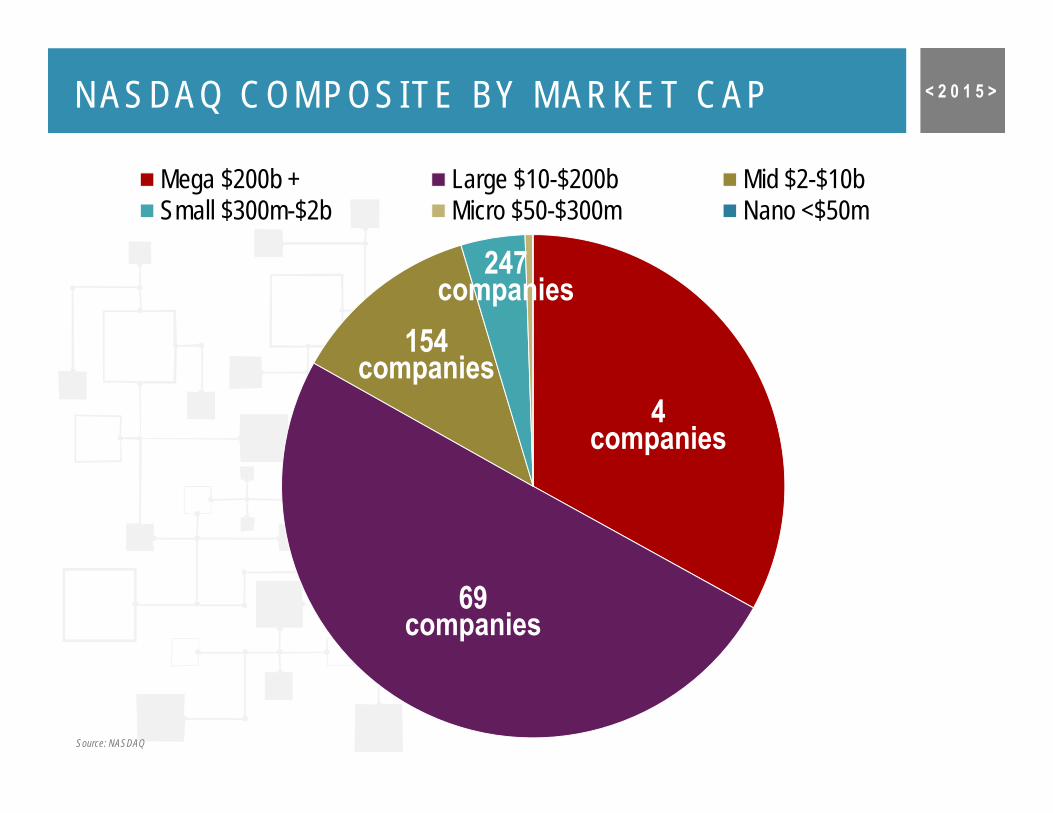

NASDAQ COMPOSITE BY MARKET CAP < 2 0 1 5 >

Mega $200b + Large $10-$200b Mid $2-$10bSmall $300m-$2b Micro $50-$300m Nano <$50m

69 companies

4 companies

154 companies

247 companies

Source: NASDAQ

JLL TECHNOLOGY OFFICE OUTLOOK < 2 0 1 5 >

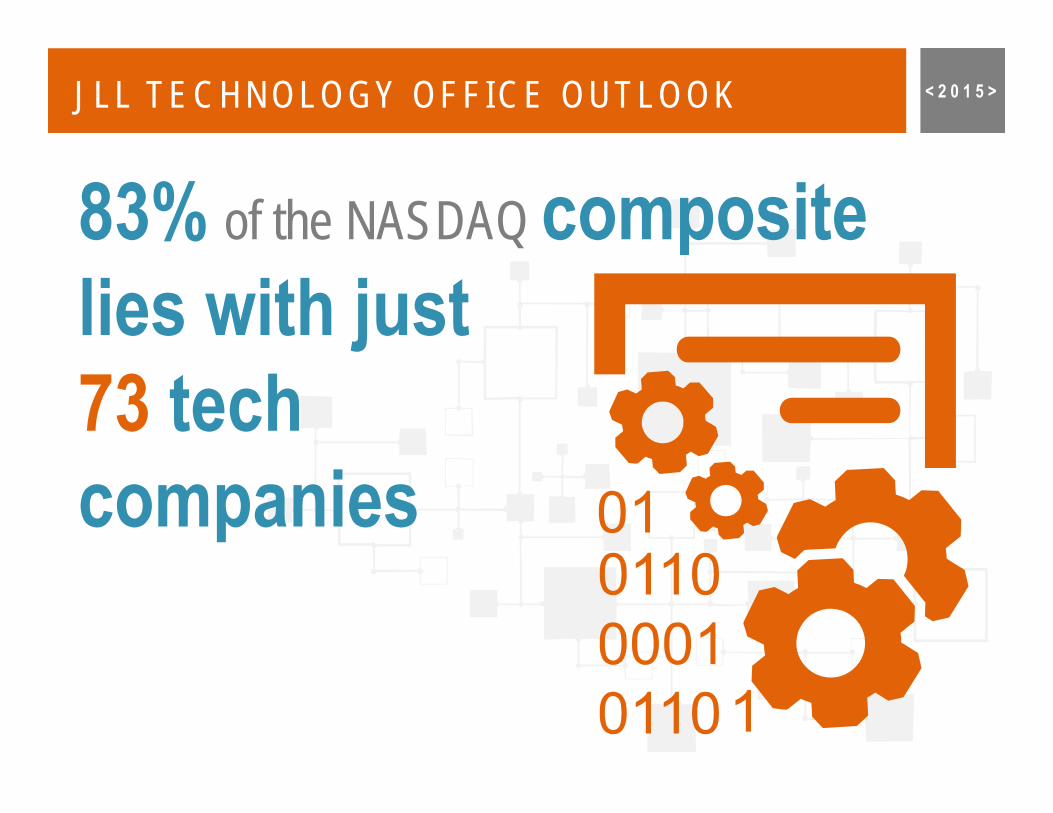

83% of the NASDAQ composite lies with just 73 tech companies

# OF MEGA AND LARGE CAP TECH HQs < 2 0 1 5 >

# of mega and large cap technology HQs Total market cap

Silicon Valley 25 $2,151,240,300,303.46 San Francisco Mid-Peninsula 4 $397,150,931,958.84 Chicago 4 $79,506,967,555.90 Boston 3 $89,782,814,898.36 Northern New Jersey 3 $81,165,126,709.76 San Francisco 3 $68,789,917,234.46 New York 3 $42,055,691,881.64 Stamford 2 $208,420,969,436.20 San Diego 2 $144,263,755,709.21 East Bay 2 $26,495,513,492.10 Seattle 1 $366,762,291,334.80 Dallas 1 $51,657,748,144.84 Orange County 1 $23,412,831,364.80 Kansas City 1 $19,105,214,519.04 Milwaukee 1 $15,646,535,660.62 Raleigh-Durham 1 $10,661,251,367.30 International 16 $641,044,818,435.93 All others 643 $895,466,673,458.15 Grand Total 716 $5,312,629,353,465.43

Source: NASDAQ

JLL TECHNOLOGY OFFICE OUTLOOK < 2 0 1 5 >

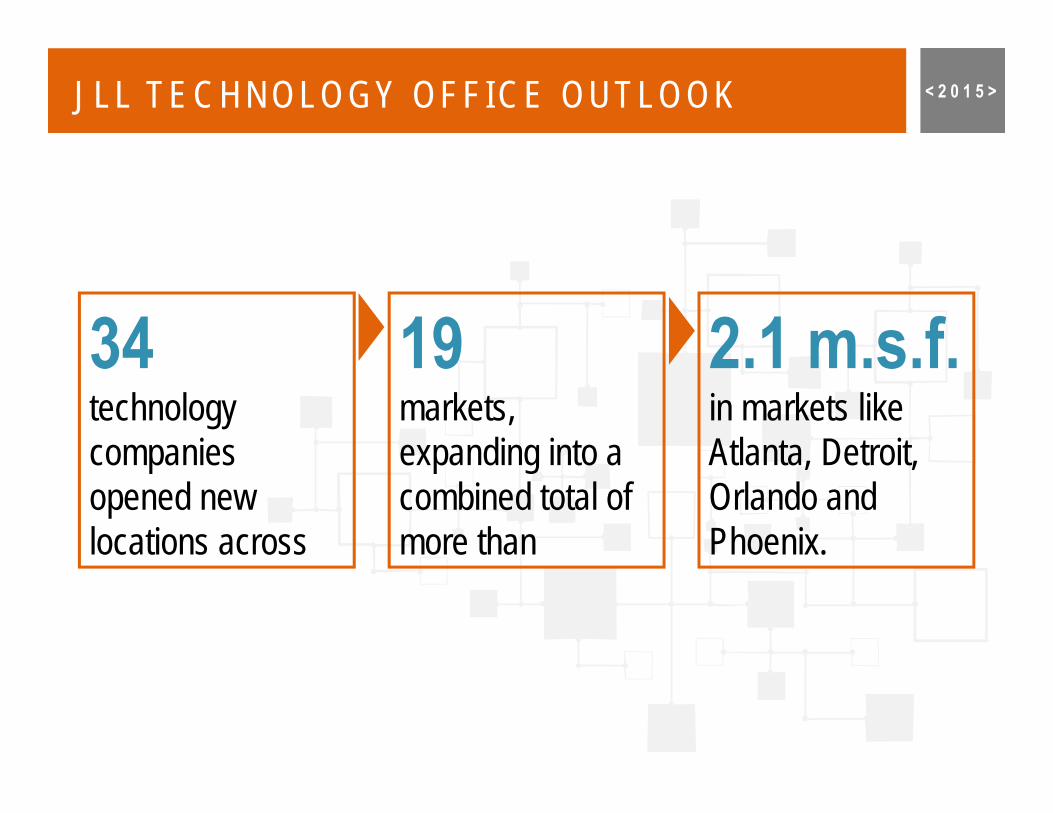

34technology companies opened new locations across

19markets, expanding into a combined total of more than

2.1 m.s.f.in markets like Atlanta, Detroit, Orlando and Phoenix.

JLL TECHNOLOGY OFFICE OUTLOOK < 2 0 1 5 >

The number of unicorns in the industry has nearly tripled.

JLL TECHNOLOGY OFFICE OUTLOOK < 2 0 1 5 >

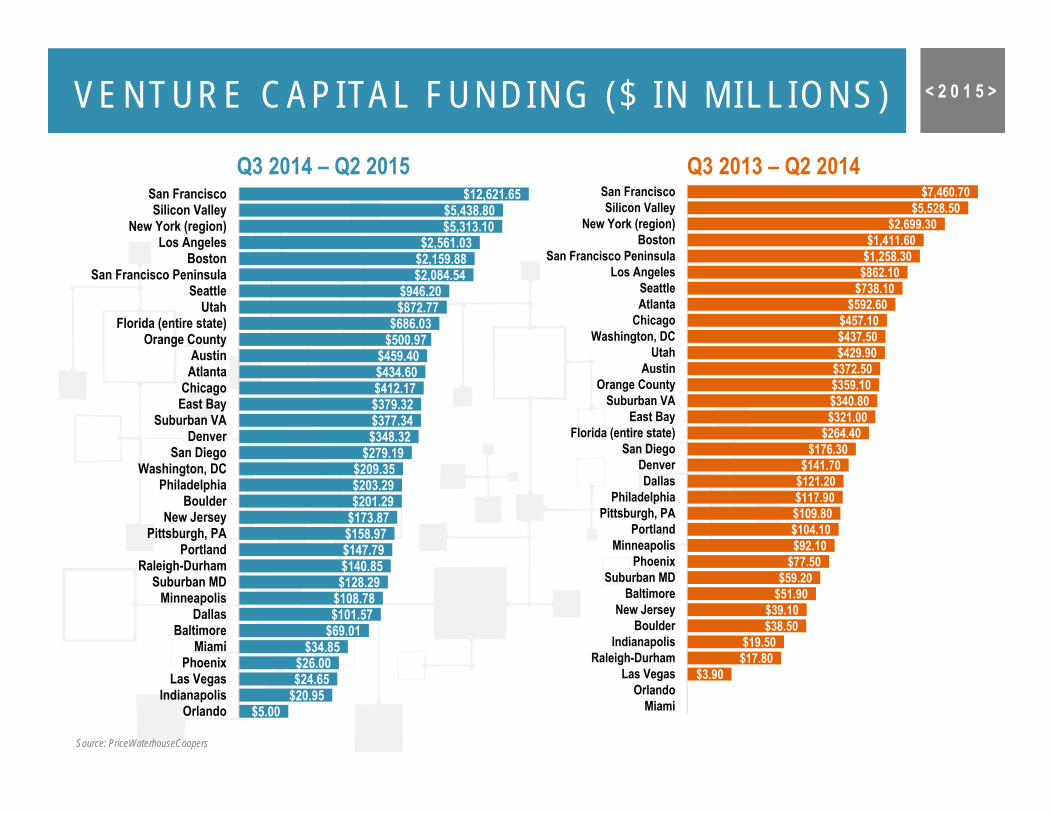

The trend of tech growth in secondary markets is beginning to dispel the traditional mentality that startups need to locate to the Bay Area in order to have access to private capital.

VENTURE CAPITAL FUNDING ($ IN MILL IONS) < 2 0 1 5 >

$5.00$20.95$24.65$26.00

$34.85$69.01$101.57$108.78$128.29$140.85$147.79$158.97$173.87$201.29$203.29$209.35

$279.19$348.32$377.34$379.32$412.17$434.60$459.40

$500.97$686.03

$872.77$946.20

$2,084.54$2,159.88$2,561.03

$5,313.10$5,438.80

$12,621.65

OrlandoIndianapolis

Las VegasPhoenix

MiamiBaltimore

DallasMinneapolis

Suburban MDRaleigh-Durham

PortlandPittsburgh, PA

New JerseyBoulder

PhiladelphiaWashington, DC

San DiegoDenver

Suburban VAEast BayChicago

AtlantaAustin

Orange CountyFlorida (entire state)

UtahSeattle

San Francisco PeninsulaBoston

Los AngelesNew York (region)

Silicon ValleySan Francisco

$3.90$17.80$19.50

$38.50$39.10

$51.90$59.20

$77.50$92.10$104.10$109.80$117.90$121.20$141.70

$176.30$264.40

$321.00$340.80$359.10$372.50$429.90$437.50$457.10

$592.60$738.10$862.10$1,258.30$1,411.60

$2,699.30$5,528.50

$7,460.70

MiamiOrlando

Las VegasRaleigh-Durham

IndianapolisBoulder

New JerseyBaltimore

Suburban MDPhoenix

MinneapolisPortland

Pittsburgh, PAPhiladelphia

DallasDenver

San DiegoFlorida (entire state)

East BaySuburban VA

Orange CountyAustin

UtahWashington, DC

ChicagoAtlantaSeattle

Los AngelesSan Francisco Peninsula

BostonNew York (region)

Silicon ValleySan Francisco

Source: PriceWaterhouseCoopers

Q3 2014 – Q2 2015 Q3 2013 – Q2 2014

JLL TECHNOLOGY OFFICE OUTLOOK < 2 0 1 5 >

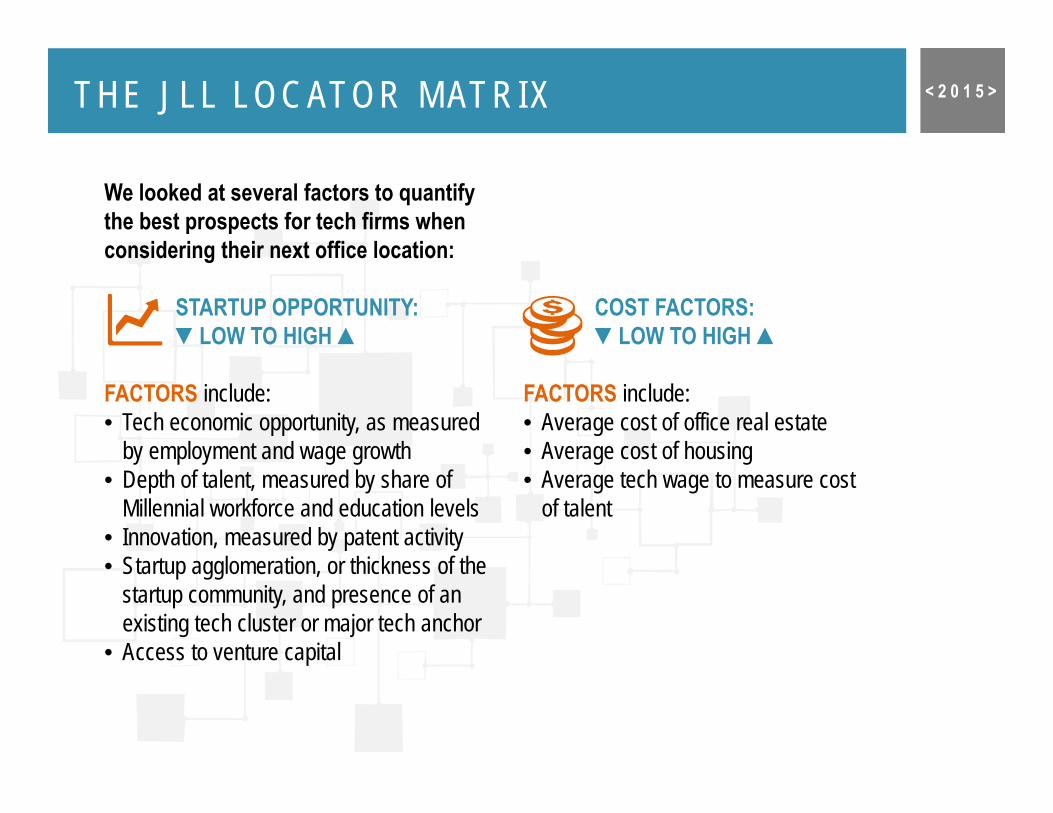

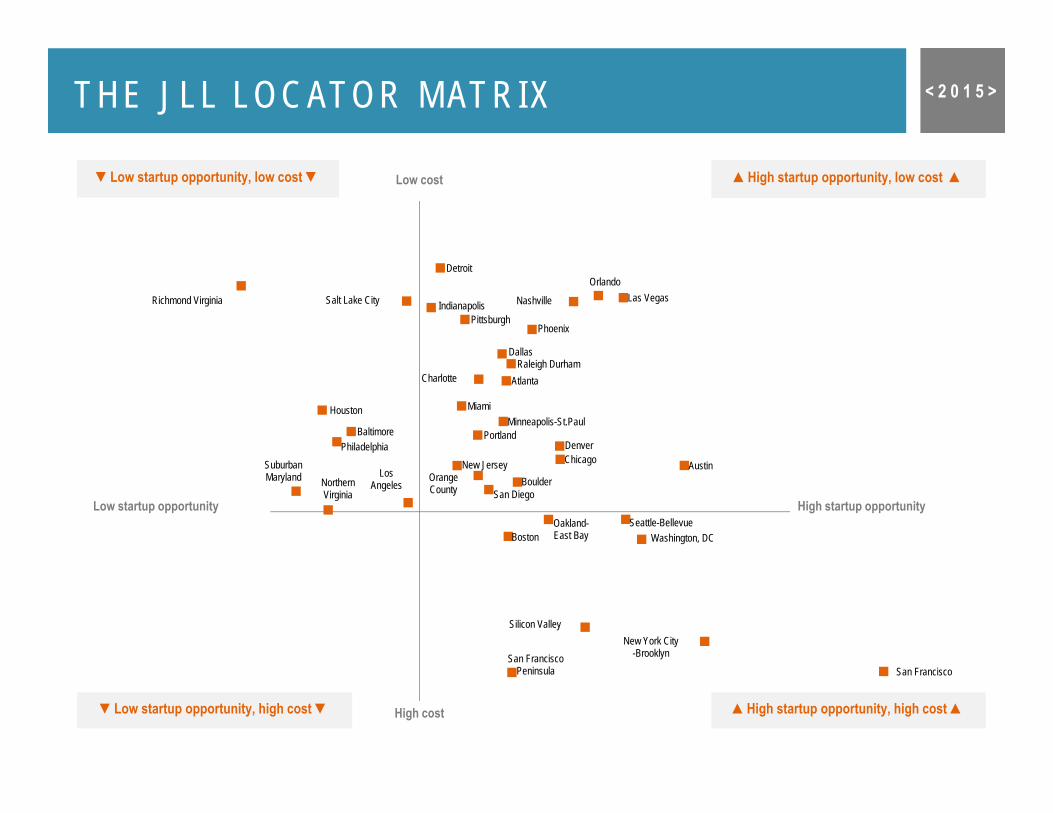

The Locator Matrix is a tool for growing startups and established tech firms to determine the best location for continued company expansion.

THE JLL LOCATOR MATRIX < 2 0 1 5 >

We looked at several factors to quantify the best prospects for tech firms when considering their next office location:

STARTUP OPPORTUNITY:▼LOW TO HIGH ▲

FACTORS include:• Tech economic opportunity, as measured

by employment and wage growth• Depth of talent, measured by share of

Millennial workforce and education levels• Innovation, measured by patent activity• Startup agglomeration, or thickness of the

startup community, and presence of an existing tech cluster or major tech anchor

• Access to venture capital

COST FACTORS:▼LOW TO HIGH ▲

FACTORS include:• Average cost of office real estate• Average cost of housing• Average tech wage to measure cost

of talent

JLL TECHNOLOGY OFFICE OUTLOOK < 2 0 1 5 >

The results of our model divide the markets into four different quadrants, making it clear which markets present the best opportunity for growth based on the cost and startup momentum.

THE JLL LOCATOR MATRIX < 2 0 1 5 >

Atlanta

Austin

Baltimore

Boston

Boulder

Charlotte

Chicago

Dallas

Denver

Detroit

IndianapolisLas Vegas

LosAngeles

MiamiMinneapolis-St.Paul

Nashville

New Jersey

New York City-Brooklyn

Northern Virginia

Oakland-East Bay

Orange County

Orlando

Philadelphia

PhoenixPittsburgh

Portland

Raleigh Durham

Richmond Virginia Salt Lake City

San Diego

San Francisco

Seattle-Bellevue

San Francisco Peninsula

Silicon Valley

Suburban Maryland

Washington, DC

Houston

Low startup opportunity

Low cost

High cost

High startup opportunity

▼Low startup opportunity, high cost ▼

▲High startup opportunity, low cost ▲

▲High startup opportunity, high cost ▲

▼Low startup opportunity, low cost ▼

JLL TECHNOLOGY OFFICE OUTLOOK < 2 0 1 5 >

The Market Score is a tool for real estate investors to determine momentum and potential investment opportunity in a particular market with tech in mind.

T

THE MARKET SCORE

L

JLL TECHNOLOGY OFFICE OUTLOOK < 2 0 1 5 >

Our ranking model revealed that San Francisco provides real estate investors the best mix of favorable attributes for those already invested in a tech market or targeting tech markets for acquisition opportunities.

JLL TECHNOLOGY OFFICE OUTLOOK < 2 0 1 5 >

As the traditional tech markets like San Francisco and New York become increasingly unaffordable for younger firms, markets like Denver, Boulder, Nashville and Salt Lake City are poised to capture the next wave of tech demand.

JLL TECHNOLOGY OFFICE OUTLOOK < 2 0 1 5 >

As for the bottom five markets in this year’s ranking, the biggest surprise may be the San Francisco Peninsula’sposition toward the bottom.

THE JLL MARKET SCORE < 2 0 1 5 >

San Francisco 93.4Washington, DC 89.4New York City 81.9Denver 79.8Chicago 79.2Boulder 79.0Nashville 78.8Seattle-Bellevue 78.3Salt Lake City 77.3Northern Virginia 75.7Oakland-East Bay 75.1Austin 75.0Atlanta 74.6Las Vegas 73.9Raleigh-Durham 73.4Boston 73.1Portland 72.1San Diego 71.9Silicon Valley 71.8

Los Angeles 71.8Orlando 71.3Dallas 71.2Minneapolis 70.5Suburban Maryland 70.3Orange County 68.9Richmond 68.4Pittsburgh 68.2Houston 67.2Philadelphia 66.8Miami 66.5New Jersey 66.0Indianapolis 65.4Phoenix 64.6Charlotte 63.6San Francisco Peninsula 60.6Detroit 60.2Baltimore 60.0

us.jl

l.com

/tech

-out

look

TechnologyOfficeOutlook

United States2015

© Copyright 2015 Jones Lang LaSalle

CONTACTS:

1. Amber SchiadaVice President, Director of ResearchNorthern California & Rocky Mountain Region+1 415 395 [email protected]

2. Julia GeorgulesVice President, Director of U.S. Office ResearchAmericas Research+1 415 354 [email protected]

FOR MORE INFO ON THE:

<TECHNOLOGY OFFICE OUTOOK>

REACH OUT TO:

OR VISIT:us.jll.com/tech-outlook

![[IoT Tech Expo] Smart Cities – Leveraging Messaging from Project to City to Nation](https://img.pdfslide.net/doc/110x75/58a1bafd1a28ab537c8b63e3/iot-tech-expo-smart-cities-leveraging-messaging-from-project-to-city.jpg)