Embed Size (px)

Citation preview

Research & Forecast Report

GREATER TORONTO AREAOFFICE Q2 2015

2 Research & Forecast Report | Q2 2015 | Greater Toronto Area / Office | Colliers International

Market Summaries

GTA Market Overview ....................................................................................................3 Downtown ............................................................................................................... 4 Midtown .................................................................................................................. 5 Central North .......................................................................................................... 6 Central East ............................................................................................................ 7 GTA East ................................................................................................................. 8 GTA North ............................................................................................................... 9 GTA West .............................................................................................................. 10

Glossary .............................................................................................................................. 11

Table of Contents

3Research & Forecast Report | Q2 2015 | Greater Toronto Area / Office | Colliers International

GTA Market Overview

Market OverviewToronto’s Downtown office market continues to experience high demand, where vacancy rates declined once again and now sit at 2.6 percent. As displayed in previous quarters, much of demand within the Downtown market continues to be for newly-built or renovated space. Numerous companies have vacated and continue to leave older buildings within the Downtown for newer ones. Currently, of the big block spaces (100,000 square feet and up) available within the Downtown, much is within older Class AAA and Class A buildings. On the other hand, many of the newly-constructed buildings have no available space, and of the almost four million square feet of office space that is currently under construction, much of this is fully pre-leased or more than 50 percent pre-leased. This is a trend that is not exclusive to Downtown as large tenants are favouring newer space within certain suburban markets. An example of the shift towards new office space is Marsh & Mclennan Companies and TJX Companies occupying space within newly- built 120 Bremner (Downtown) and 60 Standish Court (GTA Suburban West) this quarter, both leaving big block space that is still available in the older buildings that they vacated. Building amenities, collaborative workspaces and environmental efficiencies show the differences between newly-built buildings and older office stock and why these new spaces are successfully attracting tenants across various industries.

Investment MarketThe Toronto investment market saw a gradual increase in activity over Q1, 2015 but has continued to remain relatively slow in transaction activity in contrast to recent years. Despite the slowdown within the central markets, buyers continue to purchase space throughout the Greater Toronto Area, beyond the traditional Downtown and Midtown markets. According to RealNet data, during Q2, 2015, sales outside of the Downtown and Midtown markets (+$2MM CND) attributed to 64% of all deal volume. Sales within the City of Markham alone contributed to 31% of the total deal volume, with the GTA’s largest sale in Q2, 2015 taking place in Markham at 675 Cochrane Drive, a 365,000 office asset sold by BCIMC Realty Corporation to Crown Realty Partners for $97,470,000.

Market IndicatorsRelative to prior period

Market Q1 2015

Market Q2 2015

Market Q3 2015* Trend

VACANCY RATE 5.3% 5.5%

NET ABSORPTION 432,300 391,852

AVAILABILITY RATE 11.4% 10.7%

NET RENTAL RATE** $17.77 $18.65 *Projected **Rental rates for current quarter are for CBD. Rent forecast is for metro-wide rents.

Tenant DemandThe financial services sector is leading demand for office space throughout the GTA, but primarily in the Downtown and GTA West this quarter. There is also an increased demand from engineering and communications companies looking for space within the GTA. The engineering companies are almost exclusively looking for space within the GTA West, while Communications companies are seeking space throughout the city.

Q2 2015 – 1,678,600 Square Feet Financial Services

Engineering

Communications

Technology/Software

Architectural, Engineering and Related Services

Government Services

* Other (Entertainment, Interior Design, Law, Transportation and Retail Trade.

30%

15%

15%

10%

5%

5%

4%

3%

3%2%

8%Financial Services

Engineering

Communications

Technology/Software

Architectural, Engineering, and Related Services

Government Services

Real Estate

Wholesale trade

Security Services

Banking

Other (Entertainement, Interior Design, Law, Transportation andRetail Trade)

Real Estate

Wholesale Trade

Security Services

Banking

Other*

Historical Performance and Forecast

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

-1,000,000

-500,000

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

1Q

2015

2Q

2015

3Q

2015

4Q

2016

1Q

(600,000)

(400,000)

(200,000)

-

200,000

400,000

600,000

800,000

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

2009

Q2

2009

Q3

2009

Q4

2010

Q1

2010

Q2

2010

Q3

2010

Q4

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

Net Absorption (SF) New Supply (SF) Vacancy Rate (%)

4 Research & Forecast Report | Q2 2015 | Greater Toronto Area / Office | Colliers International

DowntownWhile overall vacancy rates continue to be low within the Downtown market, there is a large amount of big block space available in some of the market’s bigger Class AAA and A buildings. 181 Bay Street, First Canadian Place, Bay Adelaide Centre and 161 Bay Street are some examples of high-quality buildings with an inventory of available big block space. This is partially due to increased competition stemming from the success of new or under construction buildings in attracting a diverse set of tenants. Not only are large tenants such as RBC and Marsh & Mclennan Companies moving into new buildings, but smaller companies across numerous industries are favoring newly-built office space. For example, 134 Peter (currently under construction) has been fully pre-leased with a mix of small- and medium-sized tenants across numerous industries such as investment, consumer goods, technology/software and others.

Trends > Vacancy rates remain low within the Downtown submarkets, primarily the Downtown West, South and East.

Notable Lease TransactionsTENANT NAME - ADDRESS TYPE APPROXIMATE

SIZE (SF)

1. Blaney McMurty LLP - 2 Queen St East Renewal 80,000

2. Torkin Manes LLP - 151 Yonge St Renewal 50,000

3. D+H - 120 Bremner Blvd Headlease 31,000

Summary Statistics Q2 2015 Regional Office Market Q1 2015 Q2 2015 Trend

Office Inventory 75,928,990 75,928,990

Net Absorption 602,230 236,367

Vacancy Rate 2.7% 2.6%

Availability Rate 9.2% 7.7%

Average Asking Net Rent $28.55 $29.18

Notable Lease Notable Sale New Supply

Upcoming New SupplyADDRESS CLASS FLOORS SIZE (SF) DEVELOPER COMPLETION STATUS

6. 134 Peter Street A 17 299,178 Allied Properties REIT Q2 2015 Under Construction

7. 22 Adelaide Street West AAA 44 1,020,000 Brookfield Financial Real Estate Group Q1 2016 Under Construction

8. 351 King Street East A 17 500,000 First Gulf Q2 2016 Under Construction

9. 43A Parliament St 5 71,000 Bresler, Urbacon Q2 2016 Under Construction

10. 1 York Street A 35 800,000 HOOPP / Menkes Q3 2016 Under Construction

11. 100 Adelaide Street W AAA 40 905,722 Oxford Properties Group Inc. Q2 2017 Under Construction

12. 130 Queens Quay East 178,300 Daniels Corporation Q2 2019 Under Construction

Notable Sale TransactionsPURCHASER - ADDRESS PRICE APPROXIMATE

SIZE (SF)

4. Hullmark - 230 & 240 Richmond Street West $17,500,000 119,442

5. Allied Properties REIT - 176 - 180 John Street $8,290,000 62,469

TORONTO

Union

Dundas

Bloor / YongeBay Castlefrank

Wellesley

Queen’s ParkCarlton StCollege St

Dundas St

Queen St

King St

Spad

ina

Ave

Univ

ersi

ty A

ve

Yong

e St

Parli

amen

t St

Bloor St

Gardiner Expwy

15

94

3

6 827

10

11

12

Lake Ontario

Historical Performance and Forecast

(600,000)

(400,000)

(200,000)

-

200,000

400,000

600,000

800,000

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

2009

Q2

2009

Q3

2009

Q4

2010

Q1

2010

Q2

2010

Q3

2010

Q4

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

Net Absorption (SF) New Supply (SF) Vacancy Rate (%)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

-200,0000

200,000400,000600,000800,000

1,000,0001,200,0001,400,0001,600,0001,800,000

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

1Q

2015

2Q

2015

3Q

2015

4Q

2016

1Q

5Research & Forecast Report | Q2 2015 | Greater Toronto Area / Office | Colliers International

MidtownThe overall vacancy rate in the Midtown market once again decreased this quarter from the previous one from 3.0 percent to 2.4 percent. The Yonge-Bloor and Yonge-Eglinton submarkets continue to have very low vacancy and availability rates as space demand increases within these transit accessible markets. With no new supply or office space under construction within the Midtown market, vacancy rates are likely to remain the same for the foreseeable future. This could lead to an increase in average rental rates.

Trends > The total number of under construction and planned residential condominiums within the Yonge-Bloor and Yonge-Eglinton submarkets continues to increase.

> The condominiums that are currently under construction within the Yonge-Bloor and Yonge-Eglinton submarkets could lead to increased demand for live-work office space within the area.

Summary Statistics Q2 2015 Regional Office Market Q1 2015 Q2 2015 Trend

Office Inventory 19,387,861 19,387,861

Net Absorption -18,575 65,388

Vacancy Rate 3.0% 2.4%

Availability Rate 8.6% 6.8%

Average Asking Net Rent $19.19 $18.48

Notable Lease Notable Sale New Supply

Upcoming New SupplyADDRESS CLASS FLOORS SIZE (SF) DEVELOPER COMPLETION STATUS

4. 135 Yorkville Avenue A 11 50,000 Camrost Felcorp Q3 2016 Planned

Notable Sale TransactionsPURCHASER - ADDRESS PRICE APPROXIMATE

SIZE (SF)

1. Clifton Blake - 1133 Yonge Street $21,500,000 63,237

2. 2462790 Ontario Inc. - 17 Prince Arthur Avenue $16,200,000 20,000

3. Manulife Financial - 1300 Yonge Street $9,310,000 99,875

Bloor St

Dundas St

Queen St

Eglinton Ave

Lans

dow

ne A

ve

Yong

e St

Bayv

iew

Ave

Duffe

rin S

t

Lawrence Ave

Gardiner Expwy

TORONTO

314

2

Historical Performance and Forecast

(600,000)

(400,000)

(200,000)

-

200,000

400,000

600,000

800,000

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

2009

Q2

2009

Q3

2009

Q4

2010

Q1

2010

Q2

2010

Q3

2010

Q4

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

Net Absorption (SF) New Supply (SF) Vacancy Rate (%)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

-100,000

-50,000

0

50,000

100,000

150,000

200,000

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

1Q

2015

2Q

2015

3Q

2015

4Q

2016

1Q

6 Research & Forecast Report | Q2 2015 | Greater Toronto Area / Office | Colliers International

Central NorthThe Central North experienced negative absorption this quarter as space previously held by Proctor and Gamble within 4711 Yonge has become available. With this large block of space coming to market, it could test the demand for space within area. Little space was previously available throughout the Central North, especially in the North-Yonge Corridor.

Trends > With great public transit and highway accessibility, the North-Yonge Corridor continues to be an attractive submarket for companies.

Summary Statistics Q2 2015 Regional Office Market Q1 2015 Q2 2015 Trend

Office Inventory 12,026,988 12,026,988

Net Absorption -1,456 -183,571

Vacancy Rate 1.7% 3.2%

Availability Rate 6.8% 6.1%

Average Asking Net Rent $17.27 $17.08

Notable Lease Notable Sale New Supply

Upcoming New SupplyADDRESS CLASS FLOORS SIZE (SF) DEVELOPER COMPLETION STATUS

2. 4800 Yonge Street A 25 393,000 Oxford Properties Group Q4 2016 Planned

3. 4050 Yonge Street A 7 367,000 Build Toronto Inc. Q4 2016 Planned

Notable Sale TransactionsPURCHASER - ADDRESS PRICE APPROXIMATE

SIZE (SF)

1. Manulife Financial - 100 Sheppard Avenue East $33,329,000 273,850

Sheppard Ave

Highway 401

Lawrence Ave

Finch Ave

Yong

e St

Bayv

iew

Ave

Keel

e St

Steeles Ave

Eglinton Ave

Bath

urst

St

York University

3

2

TORONTO

VAUGHAN

1

Lawrence

Sheppard

Finch

Downsview

Lawrence West

Eglinton West Eglinton

Historical Performance and Forecast

(600,000)

(400,000)

(200,000)

-

200,000

400,000

600,000

800,000

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

2009

Q2

2009

Q3

2009

Q4

2010

Q1

2010

Q2

2010

Q3

2010

Q4

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

Net Absorption (SF) New Supply (SF) Vacancy Rate (%)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

-100,000

-50,000

0

50,000

100,000

150,000

200,000

250,000

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

1Q

2015

2Q

2015

3Q

2015

4Q

2016

1Q

7Research & Forecast Report | Q2 2015 | Greater Toronto Area / Office | Colliers International

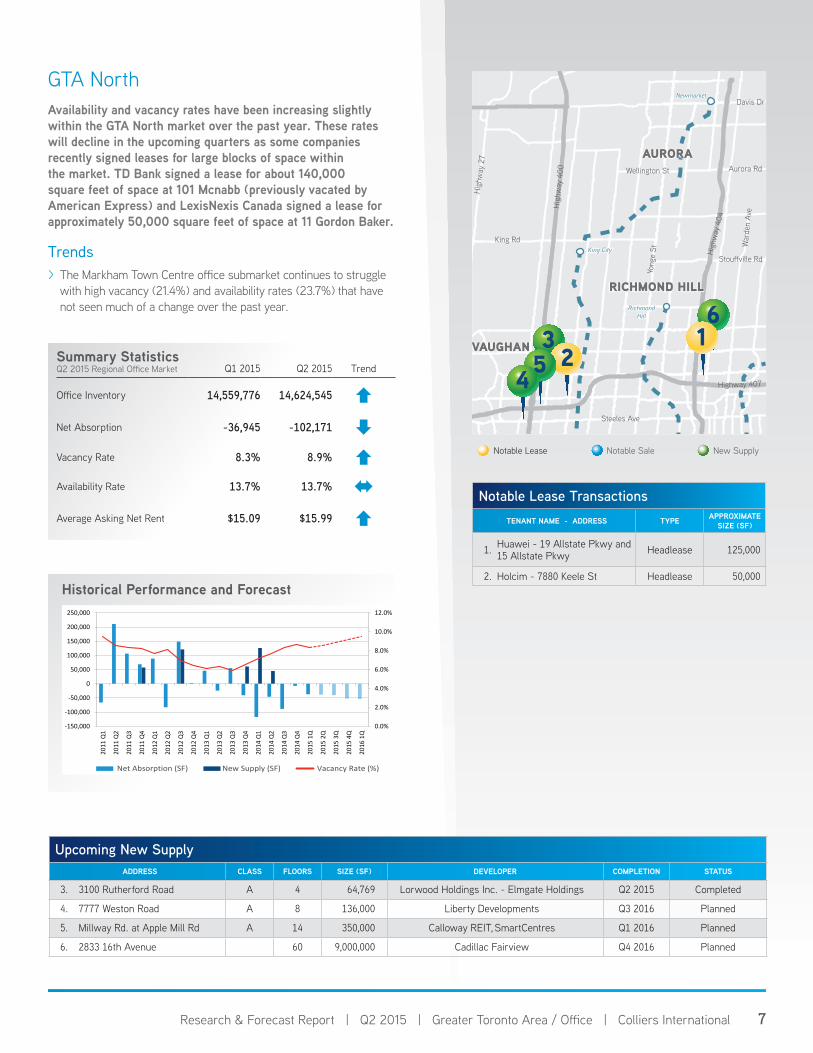

GTA NorthAvailability and vacancy rates have been increasing slightly within the GTA North market over the past year. These rates will decline in the upcoming quarters as some companies recently signed leases for large blocks of space within the market. TD Bank signed a lease for about 140,000 square feet of space at 101 Mcnabb (previously vacated by American Express) and LexisNexis Canada signed a lease for approximately 50,000 square feet of space at 11 Gordon Baker.

Trends > The Markham Town Centre office submarket continues to struggle with high vacancy (21.4%) and availability rates (23.7%) that have not seen much of a change over the past year.

Notable Lease TransactionsTENANT NAME - ADDRESS TYPE APPROXIMATE

SIZE (SF)

1. Huawei - 19 Allstate Pkwy and 15 Allstate Pkwy Headlease 125,000

2. Holcim - 7880 Keele St Headlease 50,000

Summary Statistics Q2 2015 Regional Office Market Q1 2015 Q2 2015 Trend

Office Inventory 14,559,776 14,624,545

Net Absorption -36,945 -102,171

Vacancy Rate 8.3% 8.9%

Availability Rate 13.7% 13.7%

Average Asking Net Rent $15.09 $15.99

Notable Lease Notable Sale New Supply

Upcoming New SupplyADDRESS CLASS FLOORS SIZE (SF) DEVELOPER COMPLETION STATUS

3. 3100 Rutherford Road A 4 64,769 Lorwood Holdings Inc. - Elmgate Holdings Q2 2015 Completed

4. 7777 Weston Road A 8 136,000 Liberty Developments Q3 2016 Planned

5. Millway Rd. at Apple Mill Rd A 14 350,000 Calloway REIT, SmartCentres Q1 2016 Planned

6. 2833 16th Avenue 60 9,000,000 Cadillac Fairview Q4 2016 Planned

Newmarket

RichmondHill

King City

Highway 407

Aurora RdWellington St

High

way

404

Yong

e St

Stouffville Rd

War

den

AveH

ighw

ay 4

00

Steeles Ave

King Rd

Hig

hway

27

Davis Dr

36

VAUGHAN

RICHMOND HILL

AURORA

1254

Historical Performance and Forecast

(600,000)

(400,000)

(200,000)

-

200,000

400,000

600,000

800,000

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

2009

Q2

2009

Q3

2009

Q4

2010

Q1

2010

Q2

2010

Q3

2010

Q4

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

Net Absorption (SF) New Supply (SF) Vacancy Rate (%)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

-150,000

-100,000

-50,000

0

50,000

100,000

150,000

200,000

250,000

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

1Q

2015

2Q

2015

3Q

2015

4Q

2016

1Q

8 Research & Forecast Report | Q2 2015 | Greater Toronto Area / Office | Colliers International

Central EastThe overall vacancy rate within the Central East market was left unchanged from the previous quarter, remaining at 5.5 percent. While vacancy rates have stayed relatively the same within this market, opportunity could exist for growth as the Eglinton LRT gets closer to completion. The availability of transit (LRT), coupled with great highway access and very competitive net and gross rents, could increase office leasing activity within this market, primarily the Don Mills/Eglinton Submarket.

Trends > No new office buildings are currently under construction within this market, as supply seems to be currently meeting market demand. not seen much of a change over the past year.

Notable Lease TransactionsTENANT NAME - ADDRESS TYPE APPROXIMATE

SIZE (SF)

1. TD Bank - 101 McNabb St Headlease 140,000

Summary Statistics Q2 2015 Regional Office Market Q1 2015 Q2 2015 Trend

Office Inventory 18,259,041 18,259,041

Net Absorption -23,719 -17,548

Vacancy Rate 5.5% 5.5%

Availability Rate 10.6% 12.0%

Average Asking Net Rent $12.96 $13.38

Notable Lease Notable Sale New Supply

Upcoming New SupplyADDRESS CLASS FLOORS SIZE (SF) DEVELOPER COMPLETION STATUS

4. 3377 Steeles Avenue East A 6 280,000 Bentall Real Estate Services Planned

5. 101 Gordon Baker Road A 12 250,000 Osmington Inc. Planned

Notable Sale TransactionsPURCHASER - ADDRESS PRICE APPROXIMATE

SIZE (SF)

2. The Bank of Nova Scotia - 90 Wynford Drive $16,600,000 172,113

3. Integrated Condominium Management - 18 Wynford Drive $12,311,830 97,615

Highway 407

Eglinton Ave

Finch Ave

Hig

hway

404

Yong

e St

Vict

oria

Par

k Av

e

Kenn

edy

Ave

Sheppard Ave

Steeles Ave

Highway 401

Mar

kham

Rd

Keel

e St

4

SCARBOROUGH

TORONTO

5Finch

Kennedy

Union

Lake Ontario

1

3 2

Historical Performance and Forecast

(600,000)

(400,000)

(200,000)

-

200,000

400,000

600,000

800,000

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

2009

Q2

2009

Q3

2009

Q4

2010

Q1

2010

Q2

2010

Q3

2010

Q4

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

Net Absorption (SF) New Supply (SF) Vacancy Rate (%)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

-300,000

-200,000

-100,000

0

100,000

200,000

300,000

400,000

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

1Q

2015

2Q

2015

3Q

2015

4Q

2016

1Q

9Research & Forecast Report | Q2 2015 | Greater Toronto Area / Office | Colliers International

GTA EastLittle has changed within this market over the past year with a slowing in leasing activity. Vacancy and availability rates remain relatively high in the Pickering/Oshawa submarket at 7.4 percent and 15.6 percent respectively. Leasing activity within the Scarborough Town Centre submarket will be enhanced by the Consilium Place renovations which will be completed this fall. With businesses throughout the city displaying an appetite for new built-out office space, Consilium Place should be competitive in attracting companies. The location of the STC subway stop is under review.

Trends > Average Net and Gross Rents in the GTA East market are very cost competitive as they remain the lowest in the GTA.

Summary Statistics Q2 2015 Regional Office Market Q1 2015 Q2 2015 Trend

Office Inventory 7,406,240 7,406,240

Net Absorption -52,552 -12,531

Vacancy Rate 6.9% 7.1%

Availability Rate 7.7% 9.9%

Average Asking Net Rent $11.51 $11.53

Notable Lease Notable Sale New Supply

Upcoming New SupplyADDRESS CLASS FLOORS SIZE (SF) DEVELOPER COMPLETION STATUS

1. 65 Bayly Street West 2 31500 Medallion Corporation 2016 Under Construction

2. 400 Consilium Place 15 375,000 (up to 900,000 available in 3 towers) Kevric Corporation Planned

Taunton Rd

Kingston Rd

Highway 407

Broc

k Rd

Harm

ony Rd

Sheppard Ave

Steeles Ave

Highway 401

York

& D

urha

m L

ine

ScarboroughTown Centre

Stouffville

Pickering Oshawa

Markham

21

TORONTO

OSHAWA

PICKERING

Lake Ontario

Historical Performance and Forecast

(600,000)

(400,000)

(200,000)

-

200,000

400,000

600,000

800,000

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

2009

Q2

2009

Q3

2009

Q4

2010

Q1

2010

Q2

2010

Q3

2010

Q4

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

Net Absorption (SF) New Supply (SF) Vacancy Rate (%)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

-150,000

-100,000

-50,000

0

50,000

100,000

150,000

200,000

250,000

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

1Q

2015

2Q

2015

3Q

2015

4Q

2016

1Q

10 Research & Forecast Report | Q2 2015 | Greater Toronto Area / Office | Colliers International

GTA WestAlthough the GTA West vacancy and availability rates continue to trail the performances of other suburban centers and the downtown node, there was just under 800,000 square feet of new office inventory added to the market and another 1.3 million square feet that is currently under construction. Sobeys Inc. completed their office expansion and consolidation into 237,000 square feet in Q2, 2015 as did TJX Group of Companies with their new facility at 60 Standish Court. This continuing trend of movement to newer office facilities has developers announcing further speculative office projects with the most recent being Carterra Private Equities who will break ground on just over 100,000 square feet within their Oakwoods Business Park Development in Oakville in late summer.

Trends > Recent announcements have several of the large block vacancies being leased up. These include PointClickCare and the Bank of Nova Scotia.

Notable Lease TransactionsTENANT NAME - ADDRESS TYPE APPROXIMATE

SIZE (SF)

1. Desjardins - 3 Robert Speck pkwy & 1 Robert Speck pkwy

Renewal and Expansion

190,000 & 60,000

2. PointClickCare - 5550 Explorer Dr Headlease 185,000

3. Maple Leaf Foods - 6985 Financial Dr Renewal 104,731

4. Investment Planning Council - Spectrum Square Headlease 50,000

Summary Statistics Q2 2015 Regional Office Market Q1 2015 Q2 2015 Trend

Office Inventory 49,617,239 50,402,705

Net Absorption -36,683 405,918

Vacancy Rate 10.0% 10.4%

Availability Rate 16.9% 16.6%

Average Asking Net Rent $15.13 $14.63

Notable Lease Notable Sale New Supply

Upcoming New SupplyADDRESS CLASS FLOORS SIZE (SF) DEVELOPER COMPLETION STATUS

8. 60 Standish Court (West Tower) A 7 179,000 Orlando Corporation Q2 2015 Completed

9. 60 Standish Court (East Tower) A 6 156,000 Orlando Corporation Q2 2015 Completed

10. 1 Prologis Boulevard A 5 146,863 HOOPP - Healthcare of Ontario Pension Plan Q2 2015 Completed

11. 5015 Spectrum Way A 5 134,000 HOOPP - Healthcare of Ontario Pension Plan Q2 2015 Completed

12. 1100 Walker’s Line A 6 60,000 Kamisa Corp Q2 2015 Completed

13. 85 Prologis Boulevard B 1 44,751 HOOPP - Healthcare of Ontario Pension Plan Q2 2015 Completed

14. 1006 Skyview Drive A 2 36,339 Q2 2015 Completed

15. 1375 North Service Road East A 1 28,513 Carttera Private Equities Inc. Q2 2015 Completed

Notable Sale TransactionsPURCHASER - ADDRESS PRICE APPROXIMATE

SIZE (SF)

5. Manulife Financial - 5090 Explorer Drive $22,540,000 169,050

6. The Regional Municipality of Peel - 7150 Mississauga Road $21,950,000 79,406

7. Manulife Financial - 25 Watline Avenue $8,428,000 88,550

Kipling

Georgetown

Milton

Lake OntarioQEW

Highway

407

Highway

403

hwy 427

Highway 10

Highway 4016

15

13

14

TORONTO

BRAMPTON

OAKVILLE

MISSISSAUGA

12

38 59

1011 247 1

Historical Performance and Forecast

(600,000)

(400,000)

(200,000)

-

200,000

400,000

600,000

800,000

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

2009

Q2

2009

Q3

2009

Q4

2010

Q1

2010

Q2

2010

Q3

2010

Q4

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

Net Absorption (SF) New Supply (SF) Vacancy Rate (%)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

-600,000

-400,000

-200,000

0

200,000

400,000

600,000

800,000

1,000,000

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

1Q

2015

2Q

2015

3Q

2015

4Q

2016

1Q

11Research & Forecast Report | Q2 2015 | Greater Toronto Area / Office | Colliers International

Glossary

Weighted Average Asking Net Rent: The dollar amount requested by landlords for an available space, expressed as an average based on the weight of available space.

Availability: The total amount of space that is currently being marketed as available for lease or sublease at the end of the quarter. It includes space that is available, regardless of whether the space is vacant or occupied.

Net Absorption: The net absorption in available space in a given market between the current quarter and the previous quarter.

Direct Availability: Space that is being offered for lease directly from the landlord or owner of a building, not space by another tenant in the building trying to sublet a space that has already been leased.

Sublease Availability: Sublet space that is available for sublease by a tenant to another lessee for a term equal to or shorter than that held by the tenant under its original lease with the landlord.

Under Construction: Buildings where actual ground breaking has occurred (site excavation or foundation poured) and construction is ongoing (not abandoned or discontinued) but for which a certificate of occupancy has not yet been issued.

New Supply: Total square footage with completed construction, where all that remains is the installation of tenant finishes.

Days on the Market (DOM): How many days an available industrial property has been on the market for.

GTA Central: Includes East York, Etobicoke, North York, Scarborough, Toronto and York.

GTA East: Includes Ajax, Oshawa, Pickering, and Whitby.

GTA North: Includes Aurora, Markham, Newmarket, Richmond Hill, Vaughan and Whitchurch-Stouffville.

GTA West: Includes Brampton, Burlington, Caledon, Milton, Mississauga and Oakville.

GTA Southwest: Includes Hamilton and Stoney Creek.

Forecast Assumptions & TerminologyAbsorption was calculated using moving averages of historical absorption data and supplemented with incoming new speculative and build-to-suit developments.Colliers International has adopted NAIOP’s terms and definitions which is reflected in this glossary and report.

Copyright © 2015 Colliers International.

The information contained herein has been obtained from sources deemed reliable. While every reasonable effort has been made to ensure its accuracy, we cannot guarantee it. No responsibility is assumed for any inaccuracies. Readers are encouraged to consult their professional advisors prior to acting on any of the material contained in this report.

About Colliers International Group Inc.Colliers International Group Inc. is a global leader in commercial real estate services, with more than 16,300 professionals operating out of 502 offices in 67 countries. Colliers International delivers a full range of services to real estate occupiers, owners and investors worldwide, including global corporate solutions, brokerage, property and asset management, hotel investment sales and consulting, valuation, consulting and appraisal services, mortgage banking and insightful research. In 2014 the firm handled $97 billion in total transaction value for 84,600 leases and sales. Colliers manages more than 1.7 billion square feet of commercial properties.

Colliers International Group Inc. generates more than US$2.3 billion in annual revenues. With significant insider ownership and an experienced management team, Colliers International has a long-term track record of creating value and superior returns for shareholders – previously under the ownership of FirstService, and as of June 2015, continuously as an independently owned company. The common shares of Colliers International Group Inc. trade on the NASDAQ under the symbol “CIGI” and on the Toronto Stock Exchange under the symbol “CIG”.

collierscanada.com

502 offices in 67 countries on 6 continentsUnited States: 140 Canada: 31 Latin America: 24 Asia Pacific: 199 EMEA: 108

$2.3billion in annual revenue

1.7billion square feet under management

16,300professionals and staff

MARKET CONTACT:John ArnoldiExecutive Managing Director | Toronto BrokerageDIRECT: +1 416 643 3733 [email protected]

REGIONAL AUTHORS:Kimberlee WestMarket Intelligence Team Leader | Toronto +1 416 643 [email protected]

Shawn GilliganMarket Intelligence Coordinator | Toronto DIRECT: +1 (416) 607 [email protected]

Colliers International | TorontoOne Queen Street East, Suite 2200Toronto, ON | Canada

+1 416 777 2200