Embed Size (px)

Citation preview

Pay for performance plans signal a movement away from entitlements, sometimes a very slow movement toward pay that varies with some measure of individual or organizational performance.

Pay will vary with some measure of individual, team, or organizational performance.

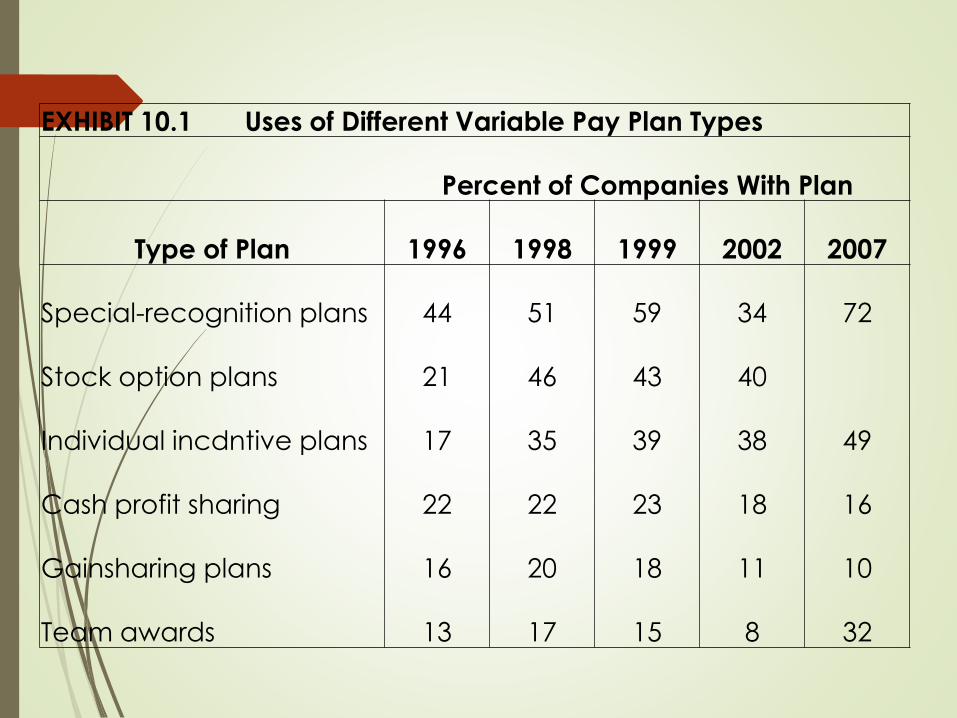

EXHIBIT 10.1 Uses of Different Variable Pay Plan Types

Percent of Companies With Plan

Type of Plan 1996 1998 1999 2002 2007

Special-recognition plans 44 51 59 34 72

Stock option plans 21 46 43 40

Individual incdntive plans 17 35 39 38 49

Cash profit sharing 22 22 23 18 16

Gainsharing plans 16 20 18 11 10

Team awards 13 17 15 8 32

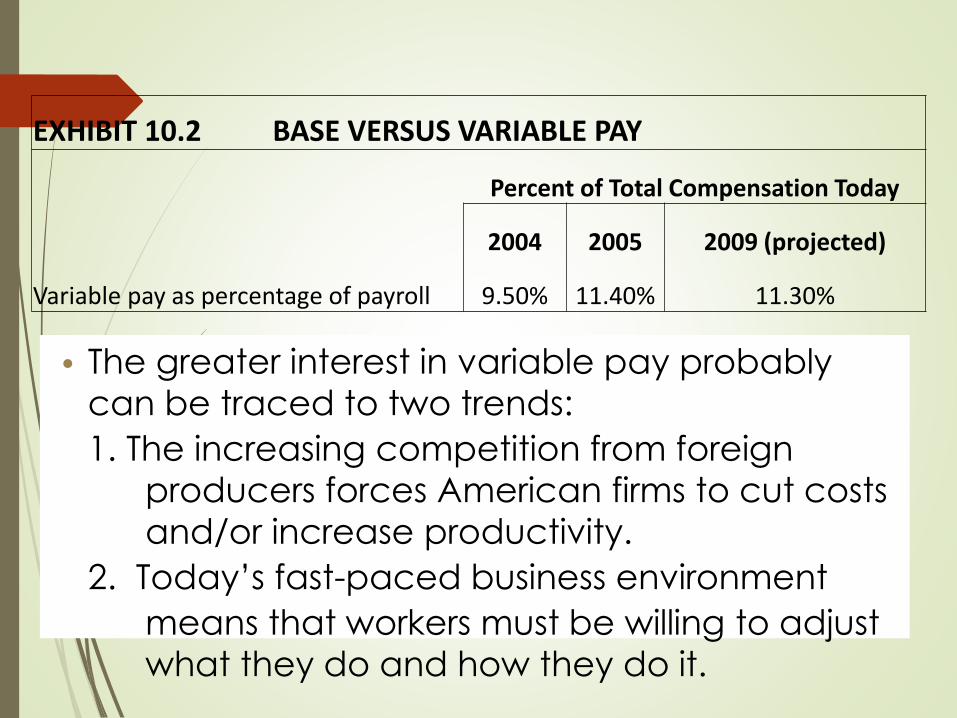

EXHIBIT 10.2 BASE VERSUS VARIABLE PAY

Percent of Total Compensation Today

2004 2005 2009 (projected)

Variable pay as percentage of payroll 9.50% 11.40% 11.30%

• The greater interest in variable pay probably

can be traced to two trends:

1. The increasing competition from foreign

producers forces American firms to cut costs

and/or increase productivity.

2. Today’s fast-paced business environment

means that workers must be willing to adjust

what they do and how they do it.

Pay-for-performance, those that introduce variability into the level of

pay you receive, seem to have a positive impact on performance if

designed well. Notice that we have qualified out statement that

variable-pay plans can be effective if they are designed well.

Merit Pay

Lump-Sum Bonuses

Individual Spot Awards

Individual Incentive Plans

Individual Incentive Plans:

Advantages and Disadvantages

Individual Incentive Plans: Examples

Merit Pay

a system links

increases in base pay

to how highly

employees are rated

on an performance

evaluation. Well Above Above Below Well Below

Average Average Average Average Average

Performance rating 1 2 3 4 5

Merit pay increase 5% 4% 3% 1% 0%

Lump-Sum Bonuses

are thought to be a

substitute for merit pay.

are earned at the end

of a specified time

period, such as

monthly, quarterly, or

annually, when an

employee achieves a

specific level of his

work or quota.

Individual Spot Awards/Spot

Awards

An immediate recognition to

reward an employee for

exceptional performance

beyond the prescribed

expectation of the

employee’s job. Spot awards

are given after the event has

been completed, usually without pre‐determined goals

or set performance levels and paid as a one‐time bonus.

Individual Incentive Plans

Incentive plans are part of an employee's compensation or

pay. The incentive plan gives an employee the opportunity

to increase his annual pay

based upon either company

performance or individual

performance. Incentive plans

are a way for companies to keep employees motivated to

perform to the best of their

abilities, thus increasing company profit.

There are four general categories of

plan:1. Cell 1

The most frequently implemented incentive system is a straight

piecework system.

Rate determination is based on units of production per time period, and

wages vary directly as a function of production level.

The major advantages of this type of system are that it is easily

understood by workers and, perhaps consequently, is more readily

accepted than some of the other incentive systems.

There are four general categories of

plan:2. Cell 2

Two relatively common plans set standards

based on time per unit and tie incentives

directly to level of output:

a. Standard hour plan is a generic term for plans setting the incentive rate based on completion of a task in some expected time period.

b. Bedeaux plan provides a variation on straight piecework and standard hour plans. It requires division of a task into simple actions and determination of the time required by an average skilled worker to complete each action.

There are four general categories of

plan:3. Cell 3

The two plans included in cell 3 provide for variable

incentives as a function of units of production per time

period:

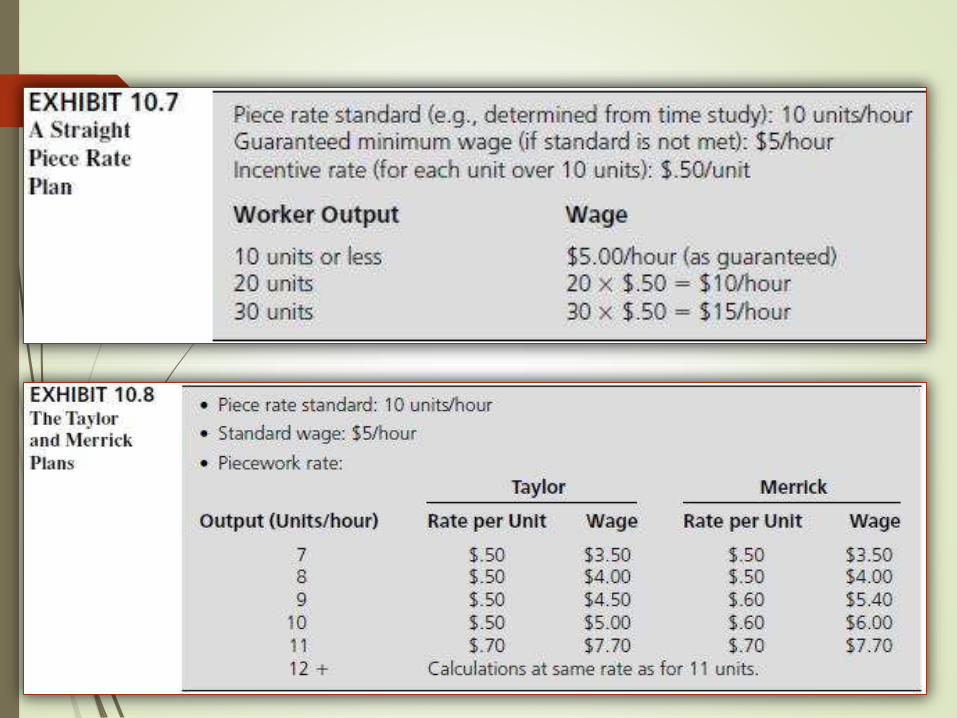

a. Taylor Plan – establishes two piecework rates:

1) Goes into effect when a worker exceeds the

published standard for a given time period.

2) Established for production below standard, and

this rate is lower than the regular wage.

b. Merrick Plan – operates in the same way, except

that three piecework rates are set:

1) High for production exceeding 100% of standard

2) Medium for production between 83 and 100% of

standard

3) Low for production less than 83% of standard

There are four general categories of

plan:4. Cell 4

The three plans included in cell 4 provide for variable

incentives linked to a standard expressed as a time

period per unit of production:

a. Halsey 50-50 method – derives its name from the

shared split between worker and employer of any

savings in direct cost.

b. Rowan Plan – similar to the Halsey plan in that an

employer and employee both share in savings

resulting from work completed in less than standard

time.

c. Gantt Plan – differs from both the Halsey and the

Rowan plans in that the standard time for a task is

purposely set at a level requiring high effort to

Individual Incentive Plans: Advantages

Substantial impact that raises productivity, lowers

production costs, and increases earnings of

workers.

Less direct supervision is required to maintain

reasonable levels of output than under payment

by time.

In most cases, systems of payments by results, if

accompanied by improved organizational and

work measurement, enable labor costs to be

estimated more accurately than under payment

by time. This helps costing and budgetary control.

Individual Incentive Plans: Disadvantages

Greater conflict may emerge between employees seeking to maximize output and managers concerned about deteriorating quality levels.

Attempts to introduce new technology may be resisted by employees concerned about the impact on production standards.

Reduced willingness of employees to suggest new production methods for fear of subsequent increases in production standards.

Increased complaints that equipment is poorly maintained, hindering employee efforts to earn larger incentives.

Increased turnover among new employees discouraged by the unwillingness of experienced workers to cooperate in on-

Individual Incentive Plans: Examples

Comparing Group and Individual Incentive

Plans

Large Group Incentive Plans

Gain-Sharing Incentive Plans

Profit-Sharing Incentive Plans

Earnings-at-Risk Plans

Group Incentive Plans: Advantages and

Disadvantages

Group Incentive Plans: Examples

Failures of team incentives schemes can

be attributed to at least 5 causes:

1) Teams come in many varieties

2) Level problem

3) Complexity

4) Control

5) Communication

3 C’s

Comparing Group and Individual Incentive Plans

Large Group

Incentive Plans

Two Types of Plans

1) Gain-Sharing

Plans – use

operating

measures

2) Profit-Sharing Plans – use

financial

measures

Gain-Sharing Plans

looks at cost components of the

income ledger and identifies savings

over which employees have more

impact.

Key elements in designing a gain-

sharing plan:

1) Strength of reinforcement

2) Productivity standards

3) Sharing the gains split between

management and workers

4) Scope of the formula

5) Great care must be exercised with

such alternative measures

6) Perceived fairness of the formula

Gain-Sharing Plans

Three Gain-Sharing Formulas

1) Scanlon Plan – are designed

to lower labor costs without

lowering the level of a firm’s activity.

2) Rucker Plan – involves more

complex formula than a

Scanlon plan for

determining worker

incentive bonuses.

3) Improshare (Improved

Productivity through

Sharing) – is gain-sharing plan that has proved easy

to administer and to

Implementation of the Scanlon/Rucker Plans

Two major components are vital to the implementation and

success of a Rucker/Scanlon Plan:

1) a productivity norm

2) effective worker committees

Similarities and Contrasts Between Scanlon and Rucker Plans

They differ from individual incentive plans which focus on

using wage incentives to motivate higher.

There are two important differences between the two plans:

1) Rucker plans tie incentives to a wide variety of savings not

just the labor savings focused on Scanlon plans.

2) This greater flexibility may help explain why Rucker plans

are more amenable to linkages with individual incentive

Profit-Sharing Plans

Profit sharing

continues to be

popular because

the focus is on the

measure that

matters most to be

people, a

predetermined

index of

profitability.

Earnings-at-Risk Plans

Two categories:

1) Success sharing plans

- employee base wages

are constant and

variable pay adds on

during successful years.

2) Risk sharing plans

- base pay is reduced by

some amount relative to

the level that would be

offered in a success-

sharing plan.

Group Incentive Plans: Advantages

1) Positive impact on organization and individual performance of about 5 to 10 percent per year.

2) Easier to develop performance measure than it is for individual plans.

3) Signals that cooperation, both within and across groups, is a desires behavior.

4) Teamwork meets with enthusiastic support from most employees.

5) May increase participation of employees in decision-making process.

Group Incentive Plans: Disadvantages

1) Line-of-sight may be lessened, that

is employees may find it more

difficult to see how their individual

performance affects their

incentive payouts.

2) May lead to increased turnover

among top individual performers

who are discouraged because

they must share with lesser

contribution.

3) Increases compensation risk to

employees because of lower

income stability. May influence

some applicants to apply for jobs

in firms where base pay is a larger

compensation component.

Group Incentive Plans:

Examples

Can be described by

common features:

1) the size of the group that participates in the plan

2) the standard against which performance is compared

3) the payout schedule

Employee Stock Ownership Plans

(ESOPs)

Performance Plans (Performance Share

and Performance Unit)

Broad-Based Option Plans (BBOPs)

Combination Plans: Mixing Individual

and Group

Employee Stock Ownership Plans

(ESOPs)

It is a benefit or retirement-

type plan for employees of a

company. In an ESOP,

employees receive regular

shares of the company’s stock

as a benefit for working at the

company. All employees are

eligible to participate in the

ESOP after a certain period of

time employed, usually one to

two years depending on the

Plan.

Performance Plans

(Performance Share and

Performance Unit)

Performance plans

typically features

corporate performance

objectives for a time three

years in the future. They

are driven by financial

earnings or return

measures, and they pay

out for meeting or

exceeding specific goals.

Broad-Based Option Plans (BBOPs)

BBOPs are stock grants. The company gives employees

shares of stock over a

designated time period. The

strength of BBOPs id their

versatility. Depending on the

way they are distributed to

employees, they can either

reinforce a strong emphasis on performance (performance

culture) or inspire greater

commitment and retention (ownership culture) of

employees.

Combination Plans: Mixing Individual and Group

It’s not uncommon for companies to use both

individual and group incentives. The goal is to

both motivate individual behavior and to insure

that employees work together, where needed,

to promote team and corporate goals. These

combination programs start with standard

individual (e.g., performance appraisal,

quantity of output) and group measures (e.g.,

profit, operating income).