Embed Size (px)

Citation preview

Accenture Life SciencesRethink Reshape Restructure…for better patient outcomes

Affordability and Value—The Economics of Pharma’sNew ScienceAccenture High Performance Business Research

Investors continue to reward new science.

Copyright © 2016 Accenture All Rights Reserved. 2

Key Findings Summary: New Science – New ChallengesHigh Performers in pharma today are all about new science, but achieving high performance will also require adapting operating models to better deliver patient and economic value.

Affordability and market access will challenge new science as a growth driver.

High Performers will increasingly combine breakthrough medical science with clearly demonstrated outcomes for patients and healthcare systems.

Growth has returned and is forecast to accelerate while margins have improved—but growth continues to be polarized at a company level.

Copyright © 2016 Accenture All Rights Reserved. 3

The Pipeline Replacement Revenue Ratio has shifted markedly—back to levels not seen since before the patent cliff of 2012.

Enterprise Value (EV) rose six percent in 2015.

There were 45 NMEs approved in 2015, the highest number since 1996.

In 2015, the industry saw mixed performance at a company level as well as declines since Q4-15, but overall performed five percent above the S&P500 across the year.

Investors continue to reward new science.

Enterprise Value ($ Billion) for “Pure Plays” 2008-15

Key Finding #1: Key Finding #1:

Enterprise Value grows for the 5th year in a row.

$1,140 $1,372$1,263

$1,501$1,703

$1,632$1,714

$2,155

-$207 -$190-$323 -$405 -$347

1178.226328800041298.43548474998

1712.602417425721808.30533410821

$69.1

$85.4$76.8

$85.1$80.2 $79.9 $76.3

-$95

2010

+12%

Nov-152008

$1,046

2012

-$2

$1,538

20142013

+6%

2011

$1,073

2009

$1,165

-$94

FVNOPLAT CVEV

Note: 16 pure play biopharma companies only. Japanese companies have March year end (YE14 = Mar-15). Constant USD FOREX used from Oct 2015. Nov 19 th 2015 share price used in latest EV and Q3-15 NOPLAT.Source: Accenture Research, Dec 2015.

-9% -18% -18.0% -27% -31% -6% 0% -19%FV/EV =

Copyright © 2016 Accenture All Rights Reserved. 4

Patent expiries rose markedly in 2015 as did new drug approvals and pipeline replacement ratio.

$8.5

$15.6 $13.4$11.7

$18.8$22.7

$27.8$31.6

$16.8 $24.9

$28.4

$19.4

$22.6

$16.3

$21.9

$16.1

$12.1

$5.7

$19.0$16.0

$3.9

$17.0

$23.7

$8.9

4.6

5.5

3.6

2.72.3

1.0 1.1

1.9

2.52.8

3.2

4.0

5.2

4.4

5.7

$8.9

$0.5

$45.6

2018

$33.3

2017

$26.5

2016

$35.5

2015

$47.4

2020

$25.0

20192014

$30.6

2013

$28.9

2012

$31.6

$0.0

2011

$29.0

$1.2

2010

$24.1

$1.5

2009

$18.8

$0.0

2008

$12.6

$0.9

2007

$14.8

$1.4

2.7

2006

$15.7

$0.1

2005

Sales Losing Exclusivity (Biotech Rx)Sales Losing Exclusivity (Conventional Rx)Pipeline Replacement Ratio

LantusNeulastaGleevecAbilifyNexiumEpogen

HumiraAdvairCrestorZetia

ZytigaCialis

RituxanRemicadeLyricaSpiriva

RevlimidAvastinHerceptinGilenyaLevimirInvega Sus

BotoxTysabri

Source: Accenture Research Nov-15, based on Evaluate Pharma and FDA CDER Statistics.

Key Patent Upcoming Expiries:

5 year Average FDA NME Approvals2006-10

22.4

5 year Average FDA NME Approvals2011-15

36.4

Patent Exposure & Pipeline ReplacementPharma Industry 2005-20E

Copyright © 2016 Accenture All Rights Reserved. 5

Copyright © 2016 Accenture All Rights Reserved. 6

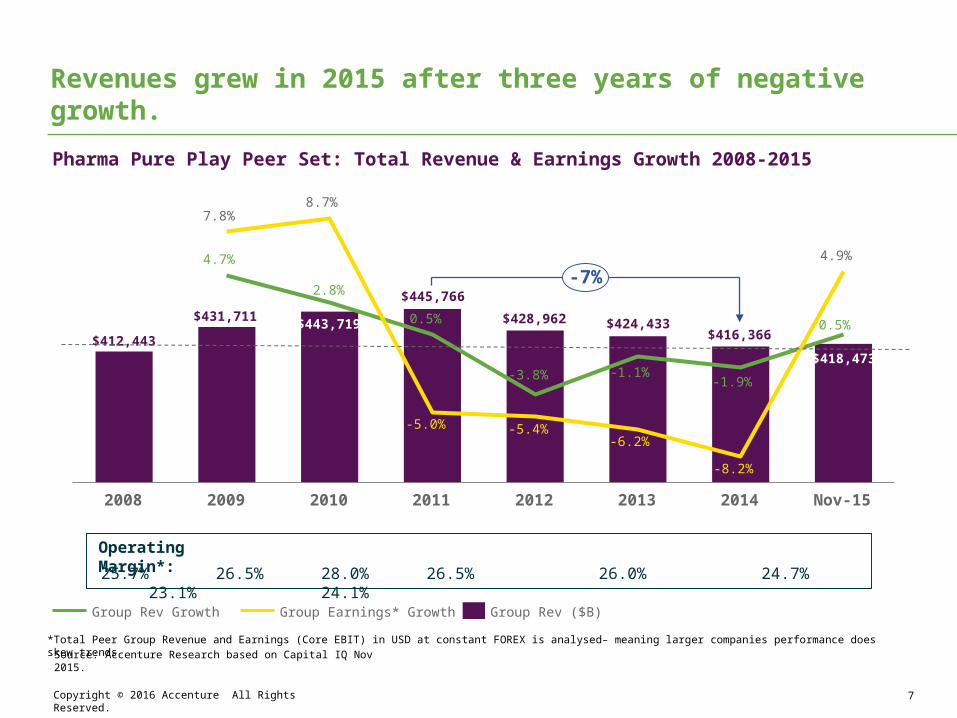

Growth has returned and is forecast to accelerate while margins have improved—but growth continues to be polarized at a company level.

After three years of negative revenue growth, the peer set overall has returned to positive growth and is forecasted to accelerate.

Six companies are outperforming their peers, with Eli Lilly joining the High Performers for the first time.

These High Performers are also growing faster than the rest of their peers.

After four years of falling Core Operating Margins, the peer set saw a one percentage point improvement in 2015.

Revenues grew in 2015 after three years of negative growth.Pharma Pure Play Peer Set: Total Revenue & Earnings Growth 2008-2015

$412,443

$431,711$445,766

$428,962 $424,433$416,366

4.7%

0.5%

-3.8% -1.1%-1.9%

0.5%

7.8%8.7%

-5.0% -5.4%-6.2%

-8.2%

4.9%

$443,719

2008 Nov-15

-7%

20142009 20132012

2.8%

2010 2011

$418,473

Group Rev Growth Group Earnings* Growth Group Rev ($B)

25.7% 26.5% 28.0% 26.5% 26.0% 24.7% 23.1% 24.1%

Source: Accenture Research based on Capital IQ Nov 2015.

Operating Margin*:

*Total Peer Group Revenue and Earnings (Core EBIT) in USD at constant FOREX is analysed– meaning larger companies performance does skew trends

Copyright © 2016 Accenture All Rights Reserved. 7

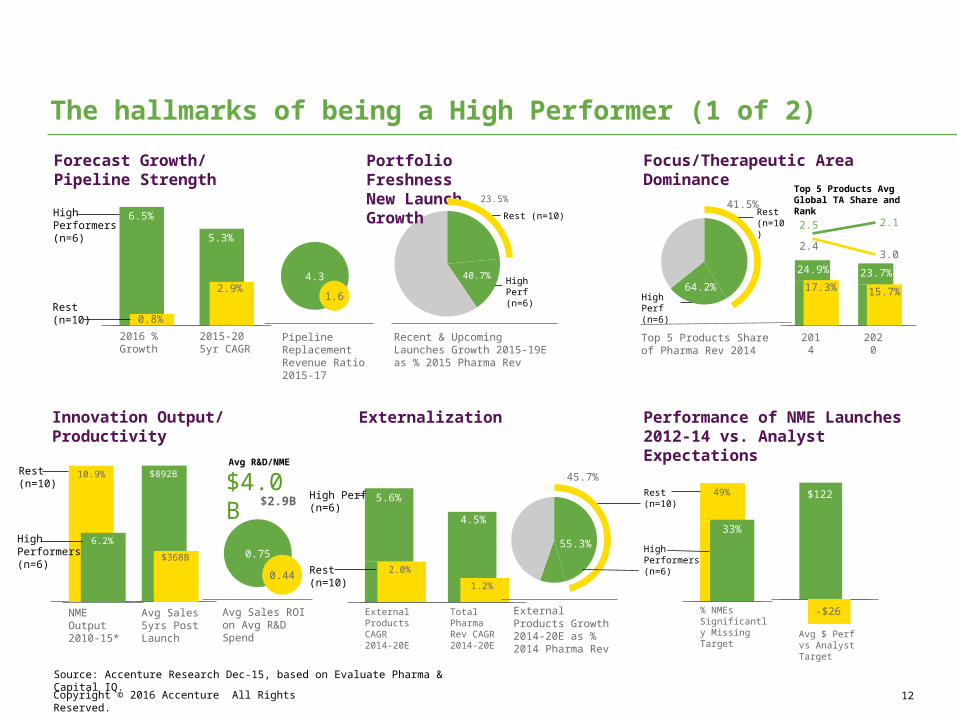

High Performers have stronger forecast growth and pipeline replacement revenue ratio as well as higher operating margins.

1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0

12%

10%

8%

6%

4%

2%

0%

-2%

Novo Nordisk

Astellas

Amgen

BMS

Pipeline Replacement Ratio 2015-20

CA

GR

201

5-18

Roche

EliLilly

Avg 3.4%

Avg 2.8x

RestHigh

-15.0% -10.0% -5.0% 0.0% 5.0% 10.0%5%

10%

15%

20%

25%

30%

35%

40%

45%

∆ 2013-15*

2015

* Cor

e EB

IT /

Rev

Astellas

Novo Nordisk

BMS

Eli Lilly

Roche

Amgen

Avg 22.2%

Avg -0.1%

Revenue Growth Forecast vs. Pipeline Replacement Revenue Ratio

Core Operating Margin vs. Change in last 2 years

Source: Accenture Research Nov-15, based on Evaluate Pharma & Capital IQ.

*Core EBIT Margin is based on Trailing 12 months to Q3-2015. Pipeline Replacement Revenue Ratio reflects Revenue growth from patented products divided by Revenue lost to unpatented products (and those with undefined patent status).

Copyright © 2016 Accenture All Rights Reserved. 8

Copyright © 2016 Accenture All Rights Reserved. 9

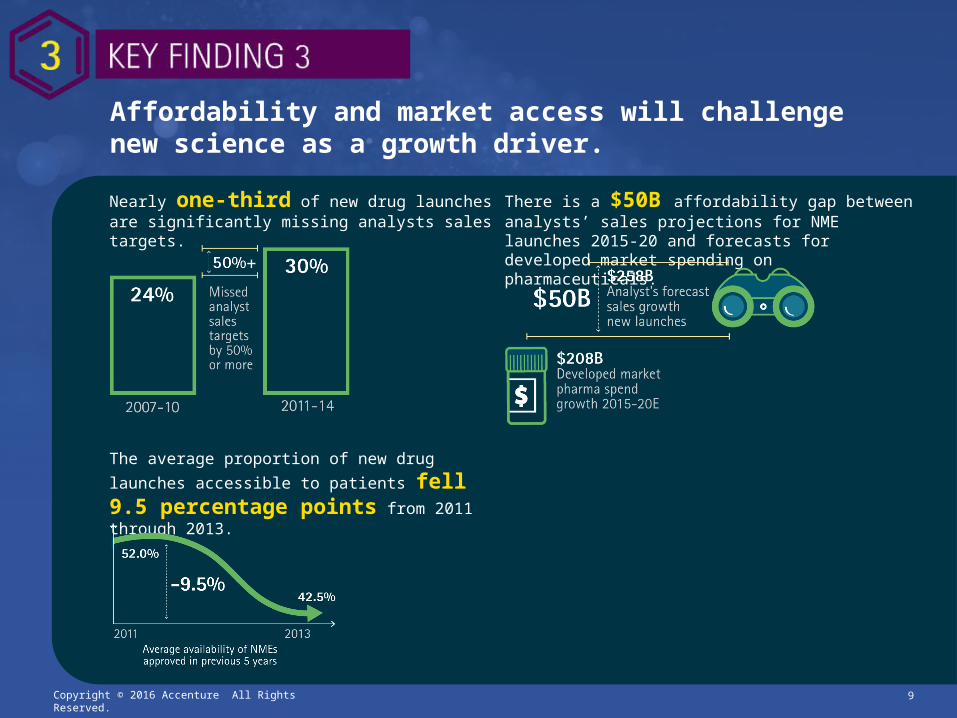

Affordability and market access will challenge new science as a growth driver.

Nearly one-third of new drug launches are significantly missing analysts sales targets.

There is a $50B affordability gap between analysts’ sales projections for NME launches 2015-20 and forecasts for developed market spending on pharmaceuticals.

The average proportion of new drug launches accessible to patients fell 9.5 percentage points from 2011 through 2013.

Accessibility and affordability are under pressure.

2011 2012 201325%

30%

35%

40%

45%

50%

55%

60%

65%

70%

-18.3%

FR

Average

SK

SP

CA

UK

US

JP

52.0%

GY

IT

Availability of NMEs Approved in Previous 5 Years - Selected Developed Markets 2011-13

Source: Accenture Research based on Evaluate Pharma Dec-15 and IMS Health Global Outlook for Medicines publications 2012-14.

87.0000000000099

121.000000000014

$136

$122

Net GenericsSavings

Pharma Net Spending Growth ($B)

Recent & Upcoming Launches - Growth

2015-20E

+$50

$258

Dev Markets Forecast growth

2015-20E

$208

Recent Launches 2011-15

Upcoming Launches 2016-20

Affordability of Recent and Upcoming NME approvals 2015-20E ($ Billion)

Copyright © 2016 Accenture All Rights Reserved. 10

“TheAffordabilityGap”

Copyright © 2016 Accenture All Rights Reserved. 11

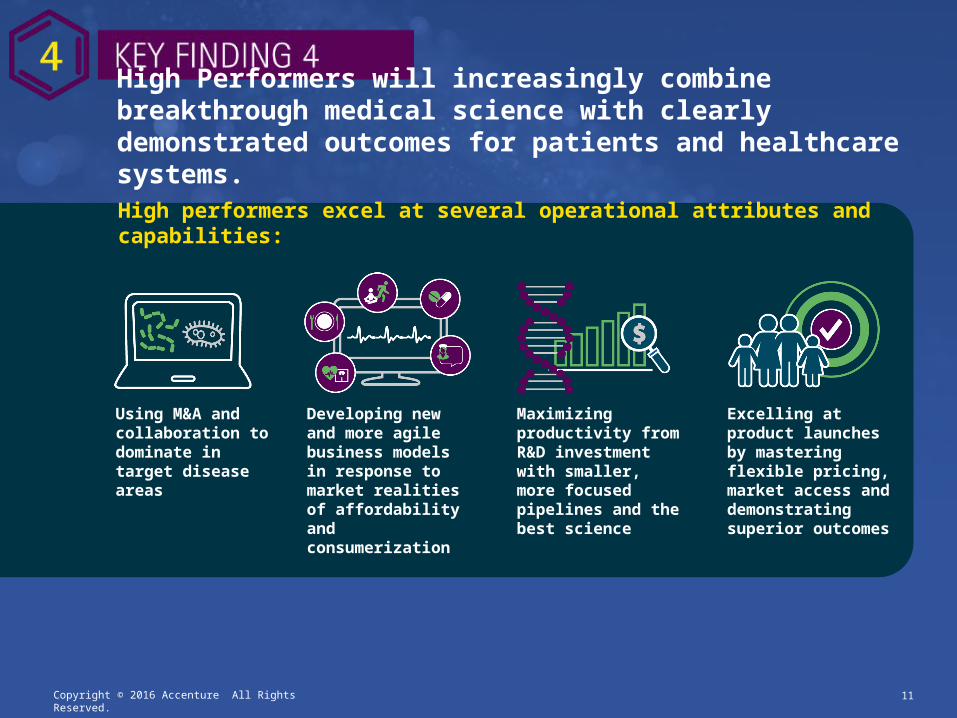

High Performers will increasingly combine breakthrough medical science with clearly demonstrated outcomes for patients and healthcare systems.

Using M&A and collaboration to dominate in target disease areas

Developing new and more agile business models in response to market realities of affordability and consumerization

Maximizing productivity from R&D investment with smaller, more focused pipelines and the best science

Excelling at product launches by mastering flexible pricing, market access and demonstrating superior outcomes

High performers excel at several operational attributes and capabilities:

NME Output 2010-15*

Rest (n=10)

10.9%

The hallmarks of being a High Performer (1 of 2)Forecast Growth/Pipeline Strength

Portfolio FreshnessNew Launch Growth

High Performers(n=6)

2015-20 5yr CAGR

5.3%

2016 % Growth

6.5%

4.3

1.6

Pipeline Replacement Revenue Ratio 2015-17

High Perf (n=6)

40.7%

Rest (n=10)

23.5%

Recent & Upcoming Launches Growth 2015-19E as % 2015 Pharma Rev

Focus/Therapeutic Area Dominance

64.2%

41.5%

Top 5 Products Share of Pharma Rev 2014

2020

15.7%

23.7%

3.0

2.1

2014

17.3%

24.9%

2.5

2.4

Top 5 Products Avg Global TA Share and Rank

Innovation Output/Productivity

Externalization Performance of NME Launches2012-14 vs. Analyst Expectations

High Performers(n=6)

6.2%0.75

0.44

Avg Sales ROI on Avg R&D Spend

$4.0B$2.9B

Avg R&D/NME

55.3%

45.7%

External Products Growth 2014-20E as % 2014 Pharma Rev

5.6%

2.0%

4.5%

1.2%

Rest (n=10)

High Perf (n=6)

Total Pharma Rev CAGR 2014-20E

External Products CAGR 2014-20E

% NMEs Significantly Missing Target

49%Rest (n=10)

High Performers(n=6)

Source: Accenture Research Dec-15, based on Evaluate Pharma & Capital IQ.

Avg $ Perf vs Analyst Target

$122

33%

2.9%

Rest (n=10) 0.8%

$892B

Avg Sales 5yrs Post Launch

$368B

Copyright © 2016 Accenture All Rights Reserved. 12

High Perf (n=6)

Rest (n=10)

-$26

The hallmarks of being a High Performer (2 of 2)

Source: Accenture Research Dec-15, based on Evaluate Pharma & Capital IQ.

Core Operating Margin

Pipeline Replacement Rev Ratio 2015-20

28.9%High Performers(n=6)

15%

20%

25%

30%

20102008 2012 Nov-15

18.1%Rest (n=10)

High Performers – Key Attributes:1) Faster Growth, Higher Pipeline Replacement Ratio

• Already back to growth & faster growth forecast• Stronger Pipeline covering IP Exposure

2) Fresher Portfolio driving Growth• Stronger $ Growth potential from Recent & Upcoming

Launches

3) Focus and Therapy Area Dominance• Top 5 products larger share of Group Rev• Higher Avg Global Rank/Mkt Share of Top 5 Products

4) Innovation Output & Productivity• Fewer NME launches, and higher R&D spend on each• But Higher Sales at 5 years, and Sales ROI on R&D

5) Greater and more effective Externalisation• Higher $ Forecast from externally originated products• Externally derived products growth faster for company

6) New Launch - Commercial Traction years 1 & 2• Fewer NME launches significantly missing Analyst

Targets• Average $ performance beating analyst expectations

7) More Profitable• Higher Core Operating Margin, holding up better in

recent years

Copyright © 2016 Accenture All Rights Reserved. 13

Our HPB study ranks the long term performance of a peer set of 16 of the largest pure-play biopharma companies* over an eight-year period based on year-end trailing 12 month Q4-2014 financials. These results have been compared with our previous 2014 and 2013 studies, to identify relative movements in the performance rankings. A detailed analysis over one, three, five and seven years is combined with equity analyst consensus forecasts to gain a view of forecast revenue growth from portfolio and new product launches, as well as the potential impact of patent expiries and mature products.

About Accenture’s High Performance Business Study:Methodology

*Pure Biopharma defined as companies having more than 75% of revenue coming from pharmaceutical products

14

HPB Metrics • Longevity• Profitability• Historical Growth• Future Value Component of

Enterprise Value• Consistency• Pipeline Growth/IP Risk

Contact UsAnne O’RiordanSenior Managing DirectorAccenture Life Sciences, [email protected]

Tom SchwengerSenior Managing DirectorAccenture Life Sciences, North [email protected]

Andrea BruecknerManaging DirectorAccenture Life Sciences, [email protected]

Copyright © 2016 Accenture All Rights Reserved.

Copyright © 2016 Accenture All Rights Reserved. 15

To learn more, visit:accenture.com/PharmaHPB

AuthorPhilip J. DavisHead of Life Sciences & Healthcare ResearchAccenture [email protected]

Stay Connectedlinkedin.com/company/accenture_life_sciences

twitter.com/AccentureLifSci

accenture.com/lifesciencesblog