Embed Size (px)

Citation preview

CUSTOMER SATISFACTION

The Industrial Credit and Investment Corporation of India, ICICI

was formed on January 5, 1955 at the initiative of the World Bank, the

Govt. of India and representatives of Indian industry. The principal

objective was to create a development financial institution for providing

medium-term and long term project financing to Indian business. The

funds were obtained through a variety of Govt. sponsored and Govt.

assisted programmes until the late 1980’s. With the liberalization of the

financial sector in 1990’s ICCI transferred business from a development

financial institution to a diversified services group offering a wide variety

of products and services to broader spectrum of clients.

About ICICI

ICICI is one of the leading financial institution of the country. Its

main business is to lend money to corporates and project finance. Now

ICICI has moved on to become a universal bank. ICICI is the first Indian

company to get listed on New York Stock Exchange (NYSE).

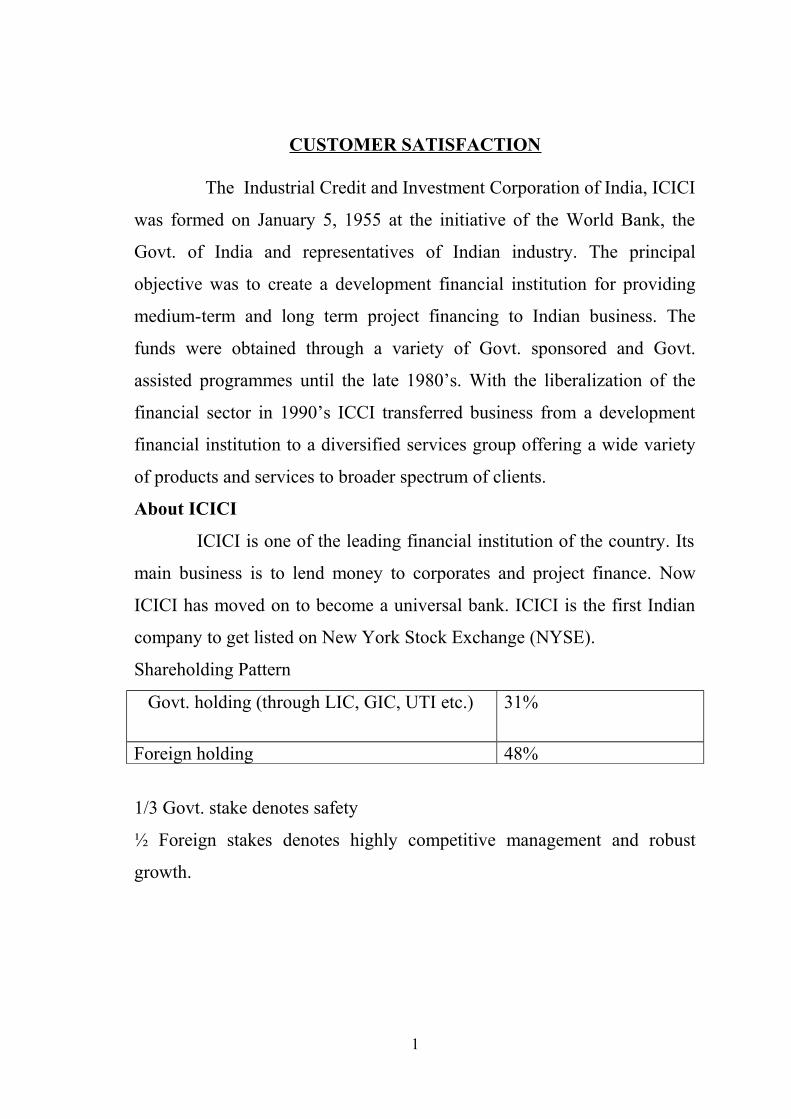

Shareholding Pattern

Govt. holding (through LIC, GIC, UTI etc.) 31%

Foreign holding 48%

1/3 Govt. stake denotes safety

½ Foreign stakes denotes highly competitive management and robust

growth.

1

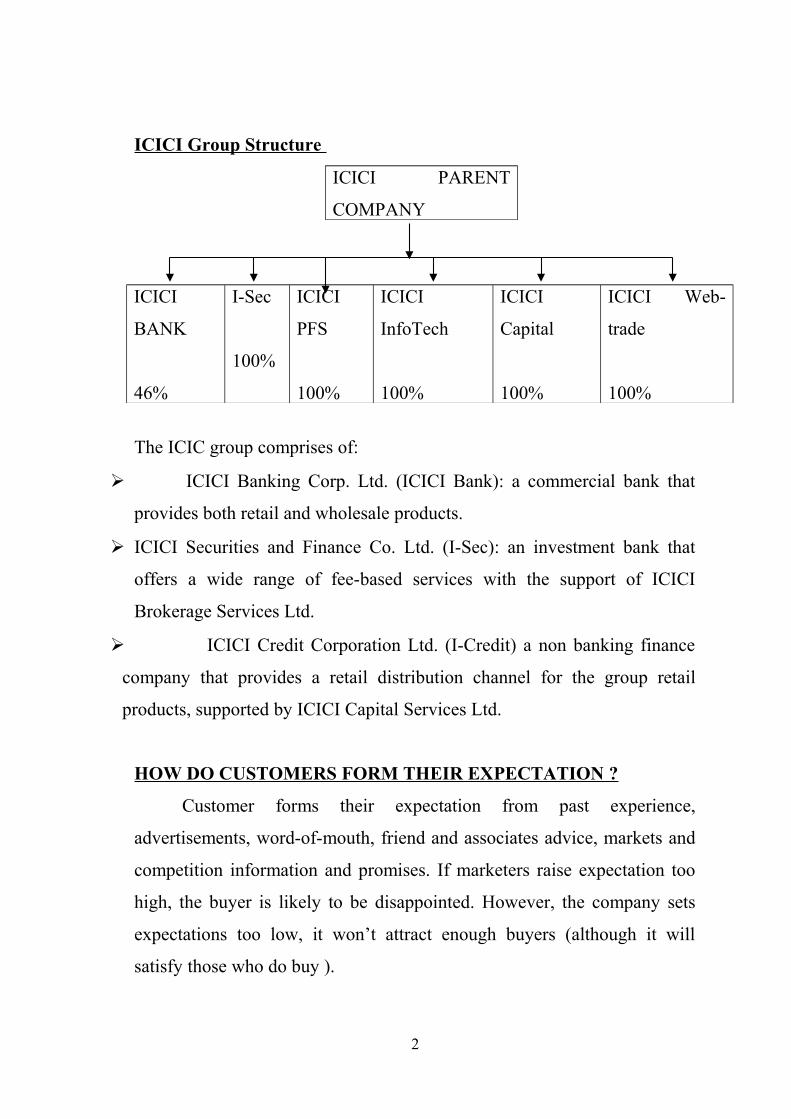

ICICI Group Structure

ICICI PARENT

COMPANY

ICICI

BANK

46%

I-Sec

100%

ICICI

PFS

100%

ICICI

InfoTech

100%

ICICI

Capital

100%

ICICI Web-

trade

100%

The ICIC group comprises of:

ICICI Banking Corp. Ltd. (ICICI Bank): a commercial bank that

provides both retail and wholesale products.

ICICI Securities and Finance Co. Ltd. (I-Sec): an investment bank that

offers a wide range of fee-based services with the support of ICICI

Brokerage Services Ltd.

ICICI Credit Corporation Ltd. (I-Credit) a non banking finance

company that provides a retail distribution channel for the group retail

products, supported by ICICI Capital Services Ltd.

HOW DO CUSTOMERS FORM THEIR EXPECTATION ?

Customer forms their expectation from past experience,

advertisements, word-of-mouth, friend and associates advice, markets and

competition information and promises. If marketers raise expectation too

high, the buyer is likely to be disappointed. However, the company sets

expectations too low, it won’t attract enough buyers (although it will

satisfy those who do buy ).

2

TOTAL CUSTOMER SATISFACTION

Some of today’s most successful companies are expectation and

delivering performance to match. These companies are arriving for TCS-

total customer satisfaction.

A customer decision to be loyal or to defect is the sum of many

small encounters with the company.

For customer’s orientated companies, customer satisfaction is both a

goal and a marketing tool.

TOOLS FOR TRACKING & MEASURING CUSTOMER

SATISFACTION

1) Complaints and Suggestion Systems

A customer-centered organization makes it easy for its customers to

deliver suggestion and complaints. Some customer-centered

companies establish hot lines with toll-free telephone numbers.

Companies are also adding Web pages and e-mail to facilitate two-

way communications. These information flow provide companies

with many good ideas and enable them to act quickly to resolve

problems.

2) Customer Satisfaction Surveys

Studies show that although customers are dissatisfied with one out

of every 4 purchases, less than 5% of dissatisfied customers will

complain. Most customers will buy less or switch supplies.

Complaint levels are thus not a good measure of customer

satisfaction. Responsive companies measure customer’s satisfaction

directly by conducting periodic surveys. They send questionnaires or

3

make telephone calls to a random sample of recent customers. They

also solicit buyer’s views on their competitors’ performances.

In this project questionnaire has been used as a tool for

tracking and measuring satisfaction.

3) Ghost Shopping

Companies can hire persons to pose as potential customers to report

on strong and weak points experienced in buying the company’s and

competitors products. These mystery shoppers can even test whether

the company’s sales personal handle various situations well. Not

only should companies hire mystery shoppers, but managers

themselves should leave their offices from time, enter company and

competitor sale situations where they are unknown, and experience

first-hand the treatment they receive as “customers”.

4) Lost Customer Analysis

Companies should contact customers who have stopped buying or

who have switch to another suppliers to learn why this happened.

Not only is it important to conduct exit interviews when customers

first stop buying, but it is also necessary to monitor the customer

loss rate. If it is increasing, this clearly indicates that the company is

failing to satisfy customers.

ATTRACTING CUSTOMERS

In the past, many companies took granted. Their customers may not

have many alternative source of supply, or all suppliers were equally

deficient in service, or the market was growing so fast that the company

did not worry about satisfying its customers. Clearly things have changed.

Today’s customers are harder to please. They are smarter, more

price conscious, more demanding, less forgiving and approached by

4

competitors with equal or better offers. The challenge according to Jeffery

Gitomer is not to produce satisfied customers but to produce loyal

customers.

Companies seeking to grow their profits and sales have to spend

considerable time and resources searching for new customers. Customers

acquisition requires substantial skills in :

Lead generation

Lead qualification

Account conversion

To generate leads, the company develops ads and place them in media that

will reach new prospects; it sends direct mail and makes phone calls to

possible new prospects; its sales person participate in trade shows where

they might find new leads; and so on. All this activity produces a list of

suspects. The next task is to qualify on their financial standing and so on.

The prospect and work be graded as hot, warm and cool. The sales people

first contract the hot, warm and cool. The sales people first contact the hot

prospects and work on account conversion, which involves making

presentations, objections and negotiating final terms.

COMPUTING THE COST OF LOST CUSTOMERS

It is not enough to be skillful in attracting new customers, the

company must keep them. Too many companies suffer from high customer

churn- namely, they gain new customers only to lose many of them. It is

like constantly adding water to a leaking pot. Today’s companies must pay

closer attention to their customer defection rate ( the rate at which they

lose customers ).

5

STEP TO REDUCE CUSTOMER DEFECTION RATE

There are four step in trying to reduce the defection rate. They are as

follows.

1) First the company must define and measure its retention.

2) Then the company must distinguish the cause of customer attrition

and identify those than can be managed better. Not much can be

done about customers who leave the region or go out of business,

but much can be done about customers who have because of poor

service, shoddy products or high prices. The company needs to

examine the percentage of customers who defect for these or

different reasons.

3) Next, the company needs to estimate how much profit it loses when

it loses customers. In the case of an individual customer, the lost

profit is equal to the customer’s lifetime value- that is, the present

value of the profit stream that the company would have realized if

the customer had not defected prematurely

4) Lastly the company needs to figure out how much it would cost to

reduce the defection rate. As long as the cost is less than the cost is

less than the profit, the company would spend that amount to reduce

the defection rate. Finally, nothing beats plain old listening. to

customers.

NEED FOR CUSTOMER RETENTION

Unfortunately, most marketing theory and practice center on the art

of attracting new customers rather than on retaining existing ones. The

emphasis traditionally has been building relationships on preserving and

selling rather than caring for the customer.

6

The key to customer retention is customer satisfaction. A highly satisfied

customer:

♦ Stays loyal longer

♦ Buys more as the company introduce new product and upgrade

existing products.

♦ Talks favorably about to company and its products.

♦ Pays less attention to competing brands and advertising and is less

sensitive to price

♦ Offer product or serve ideas to the company.

♦ Costs less to serve than new customers because transactions are

reutilized.

Thus a company would be wise to m4easure customer satisfaction

regularly. The company could phone recent customers and enquire how

many are very satisfied, satisfied indifferent and very dissatisfied. If might

lose as much as 80% of the very dissatisfied customers, maybe about 40%

of the very dissatisfied customers, about 20% of the indifferent customers

and maybe 10% of the satisfied customers. But it may lose only 1 or 2% of

its very satisfied customers. The moral: Try to exceed customer

expectations, not merely meet them.

Some companies think they are getting a sense of customer satisfaction by

tallying customer complaints. But, 95% of the dissatisfied customers don’t

complain; many just sop buying. The best thing a company can do is to

make it easy for the customer to complain. Suggestion forms, company

toll-free numbers and e-mail address serve this purpose. Listening is not

enough, however. The company must respond quickly and constructively

7

to the complaints. Because loyal customers account for a substantial

amount of company’s profits, a company should not risk losing a customer

by ignorance a grievance or quarreling over a small amount. Winning back

lost customers is an important marketing, activity and often cost less than

attracting first-time customers.

Today, more and more companies are recognizing the importance of

satisfying and retaining current customers. Following are some interesting

facts bearing on customer retention:

Acquiring new customer can cost five times more than the cost

involved in satisfying and retaining current customers.

The average company loses 10% of its customers each year.

The customer project rate trends to increase over the life of the of

the retained customer

A 5 % reduction in the customer defection rate can increase profits

by 25% to 85% depending on the industry.

WAYS TO STRENGTHEN CUSTOMER RETENTION

There are two ways to strengthen customer retention. One is to erect

high switching barriers. Customers are less inclined to switch to another

company when this would involve high capital costs, high search costs, or

the loss of loyal-customer discounts. The better approach is to deliver high

customer satisfaction. This makes it harder for competitors to overcome

switching barriers by simply offering lower prices or switching

inducements.

8

Suspect

Prospect Disqualified Prospect

First-time Customers

Repeat Customers

Inactive Ex-Customer

Clients

Members

Advocates

Partners

9

CUSTOMER DEVELOPMENT PROCESS

To understand customer relationship marketing, the involved in

attracting and keeping customers must be considered. The main step in the

customer-development process can be explained as:

The starting point is suspects, everyone who might conceivable buy

the product or services. The company looks hard at the suspects to

determine who are the most likely prospects-the people who have a strong

potential interest in the product and the ability to pay for it. Disqualified

prospect are those the company rejects because they have poor credit or

would be unprofitable. The company hopes to convert many of its

qualified prospects into first-time customers. Both first-time and repeat

customers may continue to buy from competitors as well. The company

treats very specially and knowledgeably. The next challenge is to turn

clients into members, by starting a membership program that offers a

whole set of benefits to customers who enthusiastically recommend the

company and its products and service to others. The ultimate challenge is

to turn advocates into partners where the customer and the company work

together actively.

Some customers will inevitable become inactive or drop out for

reasons of bankruptcy, moves to other locations, dissatisfaction and so on.

Here the company’s challenge is to reactive dissatisfied customers through

customer win-back strategies. It is often easier to retract ex-customers,

because company knows company knows their names and histories than to

find new ones.

10

CUSTOMER LOYALTY

The task of creating loyalty is called relationship marketing.

Relationship

marketing embraces all those steps that companies undertake to know and

serve their

value customers better. Development more loyal customers increases

revenue. However, the company has to spend more to build greater

customer loyalty. How much should a company invest in relationship

building so that the costs do not exceed the gains? For this there is need to

distinguish five different levels of investment in customer-relationship

building:

1) Basic Marketing

The salesperson simply sells the product.

2) Reactive Marketing

The salesperson sells the product and encourages the customers to

call if he or she has questions, comments or complaints.

3) Accountable Marketing

The salesperson phones the customer a short time after the sale to

check whether the product is meeting expectations. The salespersons

also ask the customers for any product or service-improvement

suggestion and any specific disappointments.

4) Proactive Marketing

The company salespersons contact the customers from time to time

with suggestion about improved product uses or helpful new

products.

11

5) Partnership Marketing

The company works continuously with the customer to discover ways to

perform better.

Most companies practice only basic marketing when their market

contain many customer and their unit profit margin are small. At the other

extreme, in the market with few customers and high profit margin most

companies will move towards partnership marketing.

The best relationship marketing going on today is driven by

technology. Companies are using e-mail, web sites, call centers, database

software to foster continuous contact between company and customers.

Integrate the telephone along with Web technology and an extremely

powerful mean of attracting and retaining customers is obtained.

TOOLS FOR CONVERTING NEUTRAL AND SATISFIED

CUSTOMERS INTO HIGHLY SATISFIED/LOYAL CUSTOMERS

There are some specific marketing tools that a company can use to

develop stronger customer bonding and satisfaction. Berry and

Parasuraman have distinguished there value-building approaches:

1) Adding Financial Benefits

Two financial benefits that companies can offer are frequency

marketing programs and club marketing programs. Frequency marketing

programs (FMPs) are designed to provide rewards to customers who buy

frequently and/or in substantial amounts. Frequency marketing is an

acknowledge of the fact that 20% of a company’s customers might

account for 80% of its business. Typically, the first company to introduce

12

an FMP gains the most benefit, especially if competitors are slow to

respond. After competitions respond, FMPs can become a financial

burden to all the offering companies.

Many companies have created club membership programs to bound

customers closer to the company. Club membership can be open to

everyone who purchases a product or service, or it can limited to an

affinity group or to those willing to pay a small fee. Although open clubs

are good for building a database or snagging customers from competitors,

limited membership clubs are more powerful long-term loyalty builders.

Fees and membership conditions prevent those with only a fleeting

interest in a company’s product joining. Limited customers clubs attract

and keep those customers who are responsible for the larger portions of

business.

2) Adding Social Benefits

Here company personnel work on increasing their social bonds with

customers by individual and personalize customer relationships. In

essence, thoughtful companies turn their customers into clients.

Donnelly, Berry and Thompson draw this distinction.

Customers may be nameless to the institution; clients cannot be

nameless. Customers are served as part of the mass or as part of larger

segment; clients are served on an individual basis… Customers are

served by anyone who happens to be available; clients are served by the

professional assigned to them.

Some companies take steps to bring their customers together to meet

and enjoy each other.

13

3) Adding Structure Ties

The company may supply customers with special equipment or

computer linkages that help customer’s mange their orders, payroll,

inventory and so on. For example Milliken & Company, provides sale

leads, sales training etc to its loyal customers

TOTAL QUALITY MANAGEMENT

One of the major value customers expect from organizations is high

product and services quality. Today’s originations view the task of

improving product and services quality as their top priority. If companies

want to stay in the race, let alone be profitable, they have no choice but to

adopt quality management (TOM)

“Total quality management (TQM) is an organization wide

approach to continually improving the quality of all the organization of all

the origination’s process products and services.”

There is an intimate connection among product and service quality,

customer satisfaction and company profitability. Higher levels of quality in

higher levels of customer satisfaction while supporting higher prices and

(often) lower costs. Therefore quality improvement programs (QIPs)

normally increase profitability. The well-known PIMS studies show high

correlation between relative product quality and company profitability. A

customer that satisfies most of its customer’s need most of the time is

called a quality company.

Quality has been defined differently by different authors. Various

expect have defined it as “fitness for use”, “conformance to requirements”,

“freedom from variations” and so on. The American Society for Quality

Control’s definition, which has been adopted world wide.

14

“Quality is the totality of feature and characteristics of a product or

services that bear on its ability to satisfy sated or implied needs”

Total quality is the key value creation and customer’s satisfaction.

Total quality is everyone’s job, just as marketing is everyone’s job

15

COMPANY PROFILE

ICICI Bank is India’s second largest bank with total assets of about

Rs. 2,513.89 bn at March 31.2006 and profit after tax of Rs.25.40 bn for

the year ended March 31,2006 (Rs. 25.04 bn in fiscal 2005). ICICI Bank

has a network of about 950 branches and extension counters and over 3300

ATMs. ICICI Bank offers a wide range of banking products and financial

services to corporate and retail customers through a variety of delivery

channels and through its specialized subsidiaries and affiliates in the areas

of investment banking, life and non-life insurance to offer products

internationally. ICICI currently has subsidiaries in the United Kingdom,

Canada and Russia, branches in Singapore and Bahrain and representative

offices in the United States, China, United Arab Emirates, Bangladesh and

South Africa.

ICICI Bank’s equity shares are listed in India on the stock Exchange,

Mumbai and the National Stock Exchange of India Limited and its

American Depositary Receipts (ADRs) are listed on the New York Stock

Exchange (NYSE).

As required by the Stock Exchanges, ICICI Bank has formulated a Code

of Business Conduct and Ethics for its directors and employees.

ICICI Bank was originally promoted in 1994 by ICICI Limited, an

Indian financial institution, and was its wholly-owned subsidiary. ICICI’s

share holding in ICICI Bank was reduced to 6% through a public offering

of shares in India in fiscal 1998, an equity offering in the form of ADRs

Listed on the NYSE in fiscal 2000, ICICI Bank’s acquisition of Bank of

16

Madura Limited in an all-stock amalgamation in fiscal 2001, and

secondary market sales by ICICI to institutional investors in fiscal 2001

and fiscal 2002. ICICI was formed in 1955 at the initiative of the World

Bank, the Government of India and representatives of Indian industry. The

principal objective was to create a development of India and

representatives of Indian industry. The principal objective was to create a

development financial institution for providing medium-term and long-

term project financing to Indian businesses. In 1990, ICICI transformed its

business from a development financial institution offering only project

finance to a diversified financial services group offering a wide variety of

products and services, both directly and through a number of subsidiaries

and affiliates like ICICI Bank. In 1999, ICICI become the first Indian

company and the first bank or financial institution from non-Japan Asia to

be listed on the NYSE.

After consideration of various corporate structuring alternatives in the

context of the emerging competitive scenario in the Indian banking

industry, and the move towards universal banking, the managements of

ICICI and ICICI Bank formed the view that the merger of ICICI with

ICICI Bank would be the optimal strategic alternative for both entities,

and would create the optimal legal structure for the ICICI group’s

universal banking strategy. The merger would enhance value for ICICI

shareholders through the merged entity’s access to low-cost deposits,

greater opportunities for earning fee-based income and the ability to

participate in the payments system and provide transaction-banking

services.

The merger would enhance value for ICICI Bank shareholders through a

large capital base and scale of operations, seamless access to ICICI’s

17

strong corporate relationships built up over five decades, entry into new

business segments, higher market share in various business segments,

particularly fee-based services, and access to the vast talent pool of ICICI

and its subsidiaries. In October 2001, the boards of Directors of ICICI and

ICICI Bank approved the merger of ICICI and two of its wholly owned

retail financial subsidiaries, ICICI Personal Financial Services Limited

and ICICI Capital Services Limited, with ICICI Bank. The merger was

approved by shareholders of ICICI and ICICI Bank in January 2002, by

the High Court of Gujarat at Ahmadabad in March 2002, and by the High

Court of Judicature at Mumbai and the Reserve Bank of India in April

2002, Consequent to the merger, the ICICI group’s financing and banking

operations, both wholesale and retail, have been integrated in a single

entity.

AN OVERVIEW OF BANKING INDUSTRY

The Indian banking history can be broadly categorized into nationalized

(Government owned) private banks and specialized banking institution.

The reserve bank of India acts as a centralized monitoring any

discrepancies and shortcoming in the system. Since the nationalization of

banks in 1969, the public sector or the nationalized banks have required a

place of prominence and has since then seen tremendous progress. The

need to become highly customer focused has forced the slow moving

public sector banks to adopt a fast track approach. The unleashing of

products and services through the net has galvanized the players at all level

of banking and financial institutions market grid to look a new at their

existing port folio offering.

18

The liberalize policy of government of India permitted entry to private

sector in the banking; the industry has witnessed the entry of new

generation private banks. The major differentiating parameter that

distinguishes these banks from all the other banks in the Indian banking is

the level of service that is offered to the customer. Verify the focus has

always been centered on the customer. Understanding his needs.

Preempting him and consequently delighting him with various

configurations of benefits and a wide portfolio of products and services.

These banks have generally been established by promoters of repute or by

high value of domestic financial institutions. The popularity or these banks

can be gauged by the fact that in a short span of time. These banks have

gained considerable customer confidence and consequently have shown

impressive growth rates. Today, the private banks corner almost 4% share

of the total share of deposit. Most of the banks in this category are

concentrated in the high growth urban areas of metros (that account for

approximately 70% of the total banking businesses. With efficiency being

the major focus, these banks leveraged on their strength and competencies

viz. management, operation efficiency and flexibility, superior product

positioning a higher employee productivity skill.

The private banks with their focused business and services portfolio have

an reputation of being niche player in the industry, A strategy that has

allowed these banks to concentrate on few reliable high net worth

companies and individuals rather than career to the mass market. These

well chalked out integrates strategy plans have allowed most of these

banks to deliver superlative level at personalized service. With the re serve

bank of India allowing these banks to operate 70% of their business to

19

urban areas, this statuary requirement has translated into lower deposit

mobilization costs and higher margins relative to public sector banks.

Existing products and services are changing way for value added ones

thanks to the one gunmanship game among competing banks, sparked off

soaring consumer demand. For example, cash management products may

soon morph from its current form into products that use payment gateways

and alternate settlement mechanism for quicker movement of money

across manufacturers, suppliers, distributors and customers.

Banks are increasingly finding that most viable way of differentiating

themselves will be successfully manage customer relationship and enhance

the overall customer experience. In future, the market space will see banks

and non-banks striving to seek opportunities for profit, in the wake of

products communization.

The high interest rate spread is often sought to be justified due to the high

level of non-performing asset (NPAs). But it is the bureaucracy and the

high level of expenses that are the underlying region, the cycle in which

public sector banks are caught in vicious. Excess bureaucracy leads to

inefficiency. Inefficiency leads to higher costs. Higher costs to leads to

higher lending rates. Higher lending rates increase the risk for borrowers.

Increased risk translates into higher NPAs. NPAs add to transaction costs,

etc!

Having provided for NPAs in their lending rates, banks should act quickly

to liquidate NPA at whatever valuation they can get and book the profit on

NPAs. The legislative framework has traditionally prevented banks form

liquidation on NPAs aggressively to facilitate a quick recovery. Successive

governments have undertaken considerable legislative reform to expedite

20

this process. The setting up of debt recovery tribunals to deal with NPAs

has helped the process considerable. The recent passage of the

Securitization Act, which enables banks to seize and liquidate the assets of

defaulting borrowers, has also resulted in favorable recovery climate for

banks.

The global experience of securitization is that between 20 to 30% of the

principles out standing in an account is recovered. There is no reason to

expect the Indian experience to be any better. The ideal solution to an

BPAs is a negotiated settlement, backed up by the threat of the

securitization Act.

Public sector banks are reluctant to negotiate a settlement. As they fear this

could lead to an allegation of corruption and to investigation by the CBI,

CAG or CVC. A proposal for negotiated settlements must pass though the

bank’s bureaucracy, which can take months, even years, by which time the

vrale of security often, deteriorates to zero. Private Banks follow flexible

recovery policies. Their objective is to quickly settle NPA s so that those

funds can be deployed profitable elsewhere. To achieve this corrective,

they pursue4 settlements aggressively and make it worthwhile for the

borrower to settle. Public sector banks should be encouraged to enter into

negotiated settlement. If the value of the security held by the bank is less

than the principle outstanding in an account, the bank should encourage

negotiating a settlement based on the value of security.

To induce dynamism and vibrancy to the banking sector, the government

must strive to introduce competition India’s experience with competition

has been that it has resulted in lowering cost, improving service, expansion

of the sector etc. the experience of the telecommunication sector is a prime

21

example. A policy to increase competition by issuing banking licenses to

new entrants should be put in place. Once an organization revives a

banking license, it should be put in place. Once an organization receives a

banking license, it should be free to set up as many branches as it deems

necessary, without having to approach the Reserve Bank of India (RBI) for

individual branch licenses.

To unlock the true potential of public sector banks, talent and resources

from private sector should be drawn by diluting government equity share

holding is necessary if India hopes to build a first world banking industry.

This will unlock great shareholder value for the government, whose fund

can be utilized to retire public dept or to invest in social infrastructure.

Banks are making huge profit and reforming of the financial sector is in

full steam. We should seize this opportunity to modernize and globalize

the banks to give the best deal to the common man.

RETAIL BANKING

Retail banking group (RBG) has emerged as the fastest growing segment

within ICICI BANK LIMITED. Within RBG, retail channel and liability

group mobilize the much needed resources at highly competitive rates

through Deposits and Bonds and retail assets and products group deploys

the available resources through various channels like home Loans,

Personnel Loans, Consumer Durables Loans, Commercial vehicle Loans

etc. in the retail assts.

Across the world retail banking has been the high volume low value

business proposition. Enormous amount of resources are required to

acquire and service customer in terms of infrastructure and operation.

22

Given the current stage of evolution of the Indian market. We have

adopted an organization model that continuous to focus on product and on

achieving market leadership in various product segments. In order to

enable closer attention and dedicated service, and tat the same time

facilitate the widening and deepening of customer relationships two

customer centric groups private banking and salary accounts group and

trusts, Association, Society and Club (TASC) and household group has

been created.

Small enterprises group which includes all clients with net worth up to Rs.

250.00 million and cumulative credit exposure up to 100.00 million has

been categorized into geographical and industry- based cluster groups,

corporate linked small enterprises, standalone small enterprises and

emerging corporate the SEG segment has strong synergies with the retail

business in terms of customer profile and servicing is done through

technology platform and retail branches.

LEARNING AREAS

ACCOUNT OPENING

Processing of form

Footfall entry Survey

Five “S”

Collecting form of HSBC IPOs

Issuing of MAT form

Customer queries regarding (PIN, ATM. ADDRESS CHANGE)

23

Providing information such as

Balance inquiry in FINANCE

Dispatch of PIN, ATM CARD, CHEQUE BOOK in E-

SEARCH

24

PRODUCTS OF ICICI BANK

“7 Ps” of Banking Product

Successful marketing strategy for any banking would depend on the skill with

which it weaves all these ‘7Ps’ in marketing effort. Simply put, it is not

enough for a bank to have a ‘right product’. It also need s ‘right pricing’ for

the product made available at ‘right place and delivered by ‘right people’

using ‘right process’ and packaged in ‘right way’.

PODUCT: Marketer believes that people do not buy products but solutions.

The implication for the marketers is to crate products that meet expectation of

the customers. New product development should involve conducting

marketing research on consumer’s expectation and buying behavior. So in

banking sector, bank product also need to carry value addition to attract

buyers, as well as require customization to suit different target audience.

PRICE: driven competition is one of the significant emerging trends in bank

marketing. Product pricing depends on the factor such as cost of deposit , cost

of intermediation, cost of capital, cost of default and margin. To effectively

compete on price, bank should launch a massive drive to mobilize low cost

deposit. It is also important to understand that not in all cases customer buy

product based on pricing. So marketers need to understand that customer’s

price sensitivity is not same across product category. Customer are also not

well informed about traditional charges such as charges for stop payment,

cheque return, non maintenance if minimum balance etc, bank marketer

should use this information to distinguish their product form competitors and

while pricing their service charges.

25

PLACE: convenience is an important criterion for a customer to choose his

bank. Banks have to critically examine as to what extend their delivery

channels provide convenience for customer. Place would comprise location of

the branches, parking space, customer space, customer support, structure

inside the bank, sign board for easy identification of counter, product specific

counter. Today banks have created alternate delivery channels for providing

services. New technology tools have redefined and expanded the scope of

place in marketing. Customers access their account through ATMs, internet

banking tele-banking, mobile technology etc, the design layout and marketing

orientation of these delivery channels are critical for effective marketing.

PROMOTION: Promotion helps in communicating products and services of

banks to customers. To put simply, the first step on buying process is the

awareness of the product/services, followed by the interest and the desire to

avail them resulting in actual purchase of product/services. Most banks limit

themselves to creating products without much focus on reaching the product

to the customer.

PEOPLE: Customer not only want product but also better buying experience.

Banking is not mechanical processing but creating pleasant experience for

clients, Customer desire employee to be courteous friendly knowledgeable

willing to provide information and guidance, accept mistakes and provide

services with smile. People should be equipped with knowledge on 4Cs

namely Know your customer, Commodity, Company and Competitors.

PROCESS: The process of delivering services is another important aspects in

marketing. Is the process hassle free or cumbersome? Should the customer

visit the branches several times or the sales executive would visit him for

documentation at his doorstep. Is the process simple, easy to understand or

26

lengthy and complicated? Thus banks need to design their processes in order

to make buying experience pleasurable for the client.

PHYSICAL EVIDENCE: The ambience, décor air-conditioning, dress code

of the staff, cleanness of the office, arrangement and color scheme of the

furniture appearances and condition of product broacher etc. constitute

physical evidence. These things communicate positive or negative feelings to

the customer. So physical evidence must be taken seriously in banking

services.

PRODUCTS OF ICICI BANK

ICICI Bank offers wide variety of Deposit products to suit requirements.

Coupled with convenience of networked branches / over 1800 ATMs and

facility of E-channel like Internet and Mobile Banking, ICICI Bank brings

banking at your doorstep. Select any of our deposit products and provide

your details online and our representative will contact you for Account

Opening.

SAVING ACCOUNT

When liquidity is concern, the most common and basic option offered by a

bank is a saving bank account. ICICI Bank offers you a power packed

Savings Account with a host of convenient features and banking channels

to transact through, So now you can bank at your convenience, without the

stress of waiting in queues

FEATURES

DEBIT CUM ATM CARD

27

AUTO INVEST ACCOUNT

INTERNET BANKING

PHONE BANKING

ANYWHERE BANKING

CHEQUE BOOK

NIMINATION FACILITY

DOORSTEP SERVICE

Money Multiplier Account

DEBIT CUM ATM CARD

You can access your money via a Debit Card. When you make a payment

on your debit card, it immediately gets deducted from your bank account.

You can freely access your bank account and check your balance too. You

can deposit cash, cheque also through ATM, request for changing Pin No.,

request for issuing a cheque book etc.

AUTO INVEST ACCOUNT

By opening a value added saving account, if the balance in the saving

account goes above Rs. 10000.00, the additional amount in multiple of

Rs.5000.00 is moved into a fixed deposit automatically. This helps

accountholder earn a better return on their idle money. Moreover, they can

access the amount in fixed deposit just like they access their saving

account either through a cheque or through ATM card. To facilitate this

28

fixed deposit is broken in multiple of Rs. 1000.00, for that no charges are

levied.

INTERNET BANKING

The internet banking facility provides you easy and secure access to your

account. Accountholder can pay their utility bills like telephone, mobile,

electricity bill online or through phone banking.

ANYWHERE BANKING

The anywhere baking facility entitles you to withdraw or deposit cash up

to a pre-specified limit (depending on your bank) across all the bank’s 560

branches and 1900 ATMs across the country.

STANDING INSTRUCTIONS

Customers can give various type of instruction the bank, like automatically

deduct their credit card and other payment from their account. They can

give other various standing instructions too, like transferring a specified

sum to fixed deposit account at regular intervals.

CHEQUE BOOK

The chequebook facility permits you to access your fund or transfer them.

Accountholder get a personalize chequebook free of cost.

NOMINATION FACILITY

Accountholders at a liberty to specify any nominee as well as change the

nominee for their account during the course of their relationship with the

bank.

29

MINIMUM BALANCE

Accountholder must maintain a minimum balance in his account. All the

above facility can be availed of for maintaining quarterly average balance

(QAB of Rs.5000). It can even go to zero. But in quarter, the average

balance has to be Rs. 5000. If it is not so there is a service charge of Rs.

750 per quarter and 10% tax per quarter is charged if the average balance

is not maintained.

ROAMING CURRENT ACCOUNT

Only Roaming Current Account from ICICI Bank travels the distance with

your business. With advanced technological features, your banking needs

are well taken care of. You can access your accounts at over 500-

networked branches across the country. So while you take care of your

business, let ICICI Bank’s Roaming Current Account simplify banking for

you. Besides there is round – the – clock phone banking. Of course, you

can also log in to www.icicibank.com or even get mobile banking.

PRODUCT FEATURES

Choose your account

Multi city cheque facility

Anywhere Banking Facility

Upcountry Cheque Collection

Pay Order and Demand Draft

Phone Banking Facility

30

Doorstep Banking Facility

Internet Banking Facility

Debit / ATM Card

Mobile Banking

More Useful Facilities

CHOOSE YOUR ACCOUNT

ICICI Bank offers a site of current account product that meets all banking

requirement of the customer.

There is a current account that fits their budget for quarterly average

balance (QAB).

31

ACCOUNT TYPE QAB (Rs.)

STANDARD 10000

CLASSIC 25000

PREMIUM 50000

GOLD 100000

PLATINUM 500000

MULTICITY CHEQUE FACILITY

Within this facility all cheque issued by customer will be payable at par at

various ICICI Bank branches across the country. This is a unique facility,

which gives the power to customer to issue cheque that is treated as local

cheque at all centre across India.

ANYWHERE BANKING

With unparalleled set of networked branches across India, ICICI offers

“anywhere banking” in the true set of the term to its customer. ICICI

Bank’s roaming current account is one centre can be operated from any

other designated branch across any other center. So a cheque deposited in

customer account in any other center will be credited to their account much

faster, likewise accountholder can deposit or withdraw cash from

designated ICICI Bank branches up to a prescribed limit. Customer can

also transfer funds across accounts in ICICI Bank.

32

UPCOUNTRY CHEQUE COLLECTION

If somebody sends a cheque payable at a remote location to the customer

account in that situation ICICI Bank’s reach coupled with its

correspondence bank networked will ensure that cheque is credited to their

account extra fast.

PAY ORDER AND DEMAND DRAFTS

With this facility customer can carry out their baking transaction over

phone. Customers can make balance enquiry, request for a cheque book,

and request for a stop payments, make an FD, request for DD etc.

INTERNET BANKING

ICICI Bank’s internet facility allows the customer to access their account

from anywhere, anytime. Accountholder can :

Check Account Balance

Transfer Funds

Request for Chequebooks and DDs

Pay Utility Bills Online

DEBIT ATM CARD

This facility is available for sole proprietorships and partnership concerns.

Accountholder can use the Debit / ATM Card for the following

transactions:

Cash Withdrawal

33

Cash Deposit

Balance Enquiry

Cheque Book Request

Mini Account Request

Transaction at Various Merchants

Establishment Across the Country

MOBILE BANKING

Customer account balance will be communicated to the customer via SMS

everyday. What’s more, in case customer’s account has insufficient

balance when a cheque hits, bank will send an SMS alert to customer

immediately.

MORE USEFUL FACILITY

Free Monthly Account Statement

Free Standing Instruction

Customer Can Also Option For Power Pay To Make Their Salary

Payments To Employee Absolutely Hassles Free.

Free Daily Statements On E-Mail.

FIXED DEPOSIT

Wide Range Of Tenures

Choice Of Investment Plans

34

Partial Withdrawal Permitted

Safe Custody Of Fixed Deposit Receipts

Auto Renewal Possible

Loan Facility Available

Wouldn’t you like a Fixed Deposit that allows you to deposit your money

for just as long as you wish? ICICI Bank’s Fixed Deposit allows you just

that – deposits can opened for periods ranging from 15 days to 10 years

Other features include:

Choice of Two Investment Plans:

TRADITIONAL

Interest payable monthly, quarterly or half – yearly as per your

convenience

Maturity period ranges from 15 days to 10 years.

35

REINVESTMENT

Interest is compounded quarterly and reinvested with principle

amount

Maturity period ranges from 6 months to 10 years.

MINIMUM BALANCE

You can avail of ICICI Bank Fixed Deposits for a minimum deposit

of Rs. 10,000 and thereafter in multiples of just Rs. 1,000.

NOMINATION

Nomination facility is available for relationships in the names of

individuals. Unless otherwise specifically, given in writing by

depositors, nomination in deposit accounts will be at Customer ID

level.

Depositor(s) however has/have the right to specify different

nomination at account level by completing appropriate forms.

Further, the applicant(s) us/are at liberty to change the nominee, through

declaration in the appropriate form to revise the nomination during the

currency of the relationship accounts with the Bank

PARTIAL WITHDRAWAL

Pre – mature withdrawal in units of Rs. 1000. The balance amount earns

the original rate of interest. No penalty is levied on pre – mature

withdrawal from a single deposit of less than Rs. 15 LAKH. The

36

withdrawn amount will earn the interest for the period for which it is held

with the bank.

SAFE CUSTODY OF FIXED DEPOSIT RECEIPTS

Customer can leave their fixed deposit receipts with the bank in safe

custody and on maturity customer just have to inform to the bank of their

choices and bank will have them executed.

AUTO RENEWAL POSSIBLE

Bank also offers the customer the option of automatic renewal of their

fixed deposit on maturity for a same period as was originally specified the

customer.

LOAN FACILITY AVAILABLE

Customer can take a loan against fixed deposit. The loan will be available

for 85% of the fixed deposit value, at a nominal rate above the fixed

deposit rate.

EASY DEPOSIT

Free Debit / ATM Card.

No Need To Open A Saving Account.

Options Of Easy Withdrawal And Easy Loan.

Wide Range Of Tenures

Auto Renewal Possible

Loan Facility Available

37

ICICI Bank Salary Account

ICICI Bank Salary Account is a benefit – rich payroll account for

Employers and Employees

As an organization, you can opt for our Salary Accounts to enable easy

disbursements of salaries and enjoy numerous other benefits too

With ICICI Bank Salary Accounts your employees will enjoy the

convenience of :

Having the largest network of ATMs at their command.

Free 24 hour Phone Banking

Free Internet Banking

All you would require to do is to send ICICI Bank an advice (in form of a

cheque / debit instruction, ecs, etc) for the total salary amount along with

the salary details of the designated employees in a soft and hard copy

format and will credit the respective employee’s Accounts as per your

statement of advice.

38

REVIEW OF LITERATURE AND PROBLEM STATEMENT

Retail banking group (RBG) has emerged as the fastest growing segment

within ICICI BANK LIMITED. Within RBG, retail channel and liability

group mobilize the much needed resources at highly competitive rates

through Deposits and Bonds and retail assets and products group deploys

the available resources through various channels like home Loans,

Personnel Loans, Consumer Durables Loans, Commercial vehicle Loans

etc. in the retail assts.

Across the world retail banking has been the high volume low value

business proposition. Enormous amount of resources are required to

acquire and service customer in terms of infrastructure and operation.

Given the current stage of evolution of the Indian market. We have

adopted an organization model that continuous to focus on product and on

achieving market leadership in various product segments. In order to

enable closer attention and dedicated service, and tat the same time

facilitate the widening and deepening of customer relationships two

customer centric groups private banking and salary accounts group and

trusts, Association, Society and Club (TASC) and household group has

been created.

PRODUCTS OF ICICI BANK

“7 Ps” of Banking Product

Successful marketing strategy for any banking would depend on the skill with

which it weaves all these ‘7Ps’ in marketing effort. Simply put, it is not

enough for a bank to have a ‘right product’. It also need s ‘right pricing’ for

39

the product made available at ‘right place and delivered by ‘right people’

using ‘right process’ and packaged in ‘right way’.

Literature Review It is relevant to refer briefly to the previous studies and

research in the related areas of the subject to find out and to fill up the

research gaps, if any. Literature on financial services can generally be found;

a number of books are available on banking related aspects as merchant

banking, loan syndication, securitization, profitability and productivity etc.

but, few studies are undertaken on the role of technology in the banking

services. Uppal R.K. (2010) studies the extent of mobile banking in Indian

banking industry during 2000-2007. The study concludes that among all e-

channels, ATM is the most effective while mobile banking does not hold a

strong position in public and old private sector but in new private sector banks

and foreign banks m-banking is good enough with nearly 50 pc average

branches providing m-banking services. M-banking customers are also the

highest in ebanks which have positive impact on net profits and business per

employee of these banks. Among all, foreign banks are on the top position

followed by new private sector banks in providing m-banking services and

their efficiency is also much higher as compared to other groups. The study

also suggests some strategies to improve m-banking services. Abdullah

D.N.M.A. and Rozario F. (2009) study the influence of service and product

quality towards customer satisfaction. 149 respondents from one of the well

known hotel in Kuala Lumpur, Malaysia are selected as a sample.

Psychometric testing is conducted to determine the reliability and validity of

the questionnaire. The study finds positive significant relationship between

place/ambience and service quality with customer satisfaction. Although,

relationship between food quality and customer satisfaction is significant, it is

in the negative direction. Future researchers can concentrate on determining

40

attributes that influence customer satisfaction when cost/price is not a factor

and reasons for place/ambience is currently becoming the leading factor in

determining customer satisfaction.

Aktan B., Teker E. and Erosy P. (2009) examines the usage of internet in

Turkey to make a basic due-diligence investigation for the financial

institutions, including banking, stock trading, insurance and provision of

financial information over the period 2005 and 2008. The findings show that

internet usage in Turkey with its young population has continued to grow

dramatically in financial services in terms of customers and financial

transactions of various natures. Azouzi Dhekra (2009) aims to check if the

current and prompt technological revolution altering the whole world has

crucial impacts on the Tunisian banking sector. On the basis of empirical

analysis, the study concludes that panoply of factors is affecting the

customersattitude toward e-banking. For instance; age, gender and educational

qualifications seem to be important and they split up the group into electronic

banking adopters and traditional banking defenders and so, they have

significant influence on the customers’ adoption of e-banking. It also shows

that despite the presidential incentives and in spite of being fully aware of the

ebanking benefits, numerous respondents are still using the conventional

banking. Fear of loss because of transactions errors or hackers plays a

significant role in alienating Tunisian customers from online banking. Finally,

the study highlights the limitations and suggests some research perspectives.

Ganesan R. and Vivekanandan K. (2009) describe a secured hybrid

architecture model for the internet banking using Hyperelliptic curve

cryptosystem and MD5. This hybrid model is implemented with the

Hyperelliptic curve cryptosystem (HECC) and it performs the encryption and

decryption processes in an efficient way merely with an 80-bit key size. The

41

various screen shots given in this contribution shows that the hybrid model

which encompasses HECC can be considered in the internet banking

environment to enrich the privacy and integrity of the sensitive data

transmitted between the clients and the application server. Hua G. (2009)

investigates the online banking acceptance in China by conducting an

experiment to investigate how users’ perception about online banking is

affected by the perceived ease of use of website and the privacy policy

provided by the online banking website. The 110 undergraduate students in

Chinese University are involved in the investigation. The study finds that both

perceived ease of use and privacy policy have a significant impact on user’s

adoption of online banking. The study also investigates relative importance of

perceived ease of use, privacy, and security. Perceived ease of use is of less

importance than privacy and security. Security is the most important factor

influencing user’s adoption. The study also discusses the implications of these

results and limitations.

identified and the extent to which current online retailers provide online

service attributes are analyzed to be low or moderate on most of the

dimensions for both the e-travel and e-mart service providers. The model

tested for the relationship between the service quality dimensions and

customer satisfaction is also found to be correlated at a low level.

Oghenerukeybe E. A. (2009) describes a user study performed to

investigate user’s perception of factors influencing the effective

implementation of existing SI objectives and to evaluate the effectiveness

of SI in banking web browsers using the Communication-Human

Information Processing Model (C-HIP) model, a model proposed by

Wogalter in 2006 in the field of warning sciences. Findings reveal that SI

is not very effective at alerting and shielding users from revealing sensitive

42

information to spoofed sites. 27 pc participants do not understand the full

meaning of the SI noticed in the banking sites while the attention of some

users is not captured enough, for they ignore the warnings completely.

Even with the presence of SI, 18.3 pc participants still go ahead to submit

sensitive information. These outcomes may help the management of banks

develop effective security strategies for the future of electronic banking in

Nigeria. Rao N. and Tiwari S. (2009) study the efficiency of 5 public

sector banks selected on the basis of deposits size in 2005. The study

concludes that all employee efficiency factors have insignificant influence

on deposits, assets and advances, from branch efficiency, only operating

profits per branch and from operating efficiency, cost of deposits have

significant and positive impact. Liquidity influencing factors and ultimate

profit factors do not influence deposits, assets and advances significantly

although all profit factors have negative effect. The study also suggests

some measures to improve efficiency. Riquelme H.E., Mekkaoui K.A. and

Rios R.E. (2009) identify which customer service and online attributes

predict overall satisfaction, determine that if satisfied customers use more

online banking features than less satisfied customers and the characteristics

of less satisfied customers. The sample of 185 customers is drawn from

one of the main banks in Kuwait, the Middle East and multiple regression

and discriminant analysis are used to analyze the data. The findings

suggest that satisfaction can be generated through improving courtesy,

content, timeliness and product and services offered and the majority of the

customers in the sample are satisfied or very satisfied with the service and

online systems attributes. The study explores that companies that offer a

wide product portfolio and relevant website content accompanied by

prompt and courteous response create satisfaction online. Thulani D.,

Tofara C. and Langton R. (2009) explore the extent of adoption and usage

43

of internet banking by commercial banks in Zimbabwe. The study

concludes that while the majority of the banks in Zimbabwe have adopted

internet banking, usage levels have remained relatively low, as not many

customers are using this innovation in Zimbabwe. Compatibility with

existing legacy systems, cost of implementation and security concerns are

the challenges faced by banks in the adoption of IB. The implications of

the study are that banks in Zimbabwe should vigorously promote the usage

of IB among customers while Government and the Reserve Bank of

Zimbabwe should increase investments targeted at infrastructure

development so as to encourage banks and individuals alike to adopt the

innovation. Hugar S.S. and Vaz N.H. (2008) evaluate the customer

orientation in public sector banks for 5 public sector, 3 new private sector

and 3 foreign banks are selected. The study concludes that new private

sector banks have more ATMs at the end of March 2006 followed by SBI

group where 77.5 pc branches are fully computerized and 18.2 pc are

partially computerized. Business per employee and profits per employee

are higher in foreign banks where SBI has received more number of

complaints followed by ICICI. The study also suggests adopting CRM by

public sector banks to stand strong in competitive environment. Kaleem A.

and Ahmad S. (2008) aims to collect bank employees’ perceptions of the

potential benefits and risks associated with electronic banking in Pakistan.

The study shows that public bank employees who have professional

degrees consider ‘minimizing transaction costs’ and ‘reduction in HR

requirements’ as the most and the least important benefits of electronic

banking respectively. Private bank employees having masters or bachelor

degrees, and less than 10 years experience, perceive ‘time saving and

minimizing inconvenience’ as the major benefits of electronic banking.

Branch managers viewed ‘facilitates quick response’ as the most important

44

benefit of electronic banking. Bankers in all segments consider

‘government access to data’ as the biggest risk associated to electronic

banking. The empirical analysis suggests that bankers in Pakistan perceive

electronic banking as tool for minimizing inconvenience, reducing

transaction costs and saving time. Migdadi Y.K.A. (2008) aims to identify

the quality of internet banking service encounter of the retail banks in

Jordan, and to identify the quality dimensions that should be improved or

sustained. The study evaluates the banks' web sites by using the web site

quantitative evaluation method (QEM) in March 2008 for sixteen retail

banks in Jordan. The results indicate that the banks in Jordan have

significant positive quality of the internet banking service encounter,

further the banks' web sites are rich in their content and significant in the

navigation, but the speed of home page down load and web site

accessibility should be developed in the future. Munusamy J. and Fong V.

O. (2008) examine the level of customer satisfaction with regard to

IBBM’s training services. The study investigates the dimensions of service

quality that have significant effect on customer satisfaction in IBBM’s

training services. The study finds that the dimensions of service quality

and customer knowledge are positively correlated to customer satisfaction

among IBBM’s corporate clients. However, only four factors, namely,

competence, credibility, accessibility, and tangibles have significant effect

on customer satisfaction. Therefore, the management of IBBM should

focus efforts on upgrading areas of competence, credibility, accessibility

and tangibles in order to continually increase customer satisfaction for

continued profitability and success in training business. Murali R., Richard

S., Nafis A. and Mudiarasan K. (2008) evaluate consumer perceptions on

quality of e-services and Internet banking adoption in Malaysia. The data

is collected from 150 retail banking customers of the Klang Valley area.

45

Results show that Internet banking users and non-users have different

expectations towards e-service quality preferences. Not all of the

dimensions are preferable by the respondents. The study also discusses

implications and recommendations to improve Internet banking service

quality in Malaysia. Qureshi T.M., Zafar M.K. and Khan M.B. (2008)

evaluate the customer acceptance of online banking. Study concludes that

majority of customers are accepting online banking culture because of

many favorable factors, usefulness, security and privacy are the main

perusing

Statement of the problem

The problem is how feasible is Kaizen techniques in India and what is

customer conception as to use kaizen techniques as a marketing tool it is

important to know what the people think about new techniques and what

erectly want to gather information.

46

OBJECTIVES OF STUDY

To study the financial product of ICICI BANK LIMITED.

To study the customer behavior about the financial product of the

bank.

To study the software uses at ICICI bank

To stduy the uses of Kaizen techniques at ICICI Bank

To suggest some ideas to the bank that will give an edge over the

competitors.

47

RESEARCH METHODOLOGY

Statement of the problem

The problem is how feasible is Kaizen techniques in India and what is

customer conception as to use kaizen techniques as a marketing tool it is

important to know what the people think about new techniques and what

erectly want to gather information.

METHODOLOGY OF RESEARCH

In common parlance, research is a search for facts. The search for facts

many be made through either.

a) Arbitrary method.

b) Scientific method.

• Arbitrary method:- Arbitrary method of seeking answers to

question consists of imagination, opinion, blind belief or

impression.

• Scientific method:- This is a systematic method approach of

seeking facts. It climates the drawback of arbitrary method. It is

objective, precise and Ames at conclusion on the basis of the

variable evidence.

Therefore, Scientific method rather than arbitrary method should make

research for facts. Then only we may get verifiable and accurate facts.

Hence, research is a systematic and logical study of an issue or problem or

phenoucra through scientific method.

48

TYPES OF RESEARCH

(1) Descriptive Research

(2) Analytical Research.

(3) Applied Research.

(4) Fundamental Research.

(5) Concept ional Research.

(6) Imperial Research.

DESCRIPTIVE RESEARCH

This includes surveys and fact-finding inquiries of different kinds. The

major purpose of descriptive research is description of the state of affairs

as it exist at present. The main characteristic of this method is the

researcher does not have any controlled our the variable. Most of these

researchers seek to major much items as, for example frequency of

shopping, preference of people or similar data. These studies also include

attempts by researcher to discover causes even when they can not control

the variables.

EMPIRICAL RESEARCH

It is a Data Based Research, Coming up with result, which are capable of

being verified by ostentation or experiments. In such type of research, it is

necessary to get at facts first hand, at thin source and actively to go about

curtain things to stimulate the production of designed information. In

search a result the researcher must provide himself with working

hypothesis guess as to probable recounts.

49

This profit work has been done using the method “Secretive Research” and

Analytical Research”. The researcher is making use of the facts and

information already available its to make a critical evaluation of the

materials and also include survey and fact finding inquiries of different

kinds.

LIMITATION OF THE STUDY

Answer given by the customers and the bank personal can be biased,

which may have affected my project.

As my project was for Patna region only, it may not provide an overall

view of the market of financial product.

As for the figures for the various financial products were not available

to me, I couldn’t include any portion from viewpoint of finance. It is

totally a topic of marketing.

As the topic of my project was completely research – oriented, I didn’t

get any suitable book for my project.

Due to shortage of time I was not able to take more sample size than

150, which could also be a hurdle in my suggestion.

50

DATA ANALYSIS & INTERPRETATION

AGE GROUP

AGE GROUP

A, 47%

B, 25%

C, 19%D, 9% A

B

C

D

IMPLICATION: If we closely look at the pie-chart, we can say that the

people between the age group of 25 to 55 are the main customer of the

bank, which contributes almost 75% of the bank’s customers. But the old

age and the young people have been less attractive on this leading product

of ICICI Bank, which is a matter of concern. So more focus should be

given to them as they have the huge potential.

51

OCCUPATION

OCCUPATION

SERVICE51%BUSINES

S32%

STUDENT7%

OTHERS10%

SERVICE

BUSINESS

STUDENT

OTHERS

IMPLICATIONS: This pie chart clearly shows that service holder and the

business people are the main customer of the bank. Reason for this could

be as per interviewed was working hour and anywhere banking which suits

them. 8 to 8 banking give them the freedom to do banking work after the

office. Student’s contribution is less as student account is not available in

Patna and 5000 as minimum balance is not possible for them. Other

section should be increased by creating awareness about the banking

products.

52

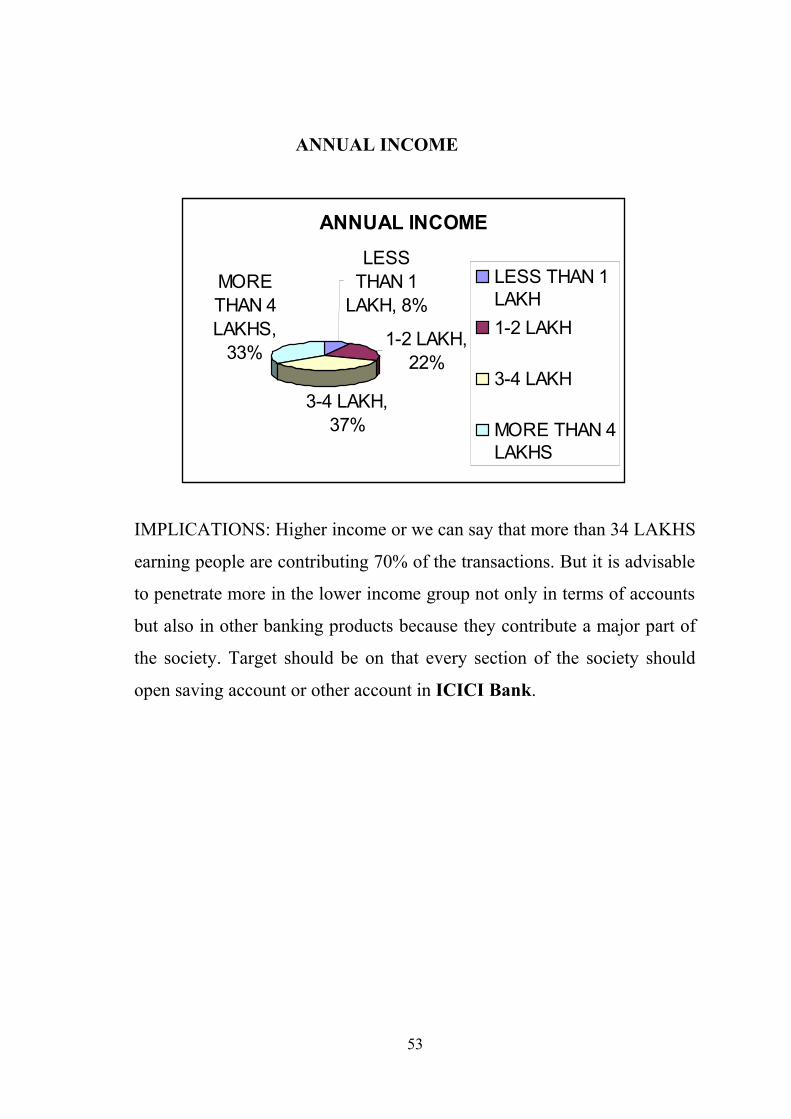

ANNUAL INCOME

LESS THAN 1

LAKH, 8%

1-2 LAKH, 22%

3-4 LAKH, 37%

MORE THAN 4 LAKHS,

33%

LESS THAN 1LAKH

1-2 LAKH

3-4 LAKH

MORE THAN 4LAKHS

ANNUAL INCOME

IMPLICATIONS: Higher income or we can say that more than 34 LAKHS

earning people are contributing 70% of the transactions. But it is advisable

to penetrate more in the lower income group not only in terms of accounts

but also in other banking products because they contribute a major part of

the society. Target should be on that every section of the society should

open saving account or other account in ICICI Bank.

53

WHAT FEATURES ATTRIBUTES DO YOU EXPECT FROM A

BANK WHILE OPENING AN ACCOUNT

FEATURES / ATTRIBUTES

QUICK SERVICE ,

44%

PROPER INFO, 14%

WORKING HOUR, 28%

LESS FORMALITIE

S, 8%

VARIETY OF PRODUCTS,

6% QUICK SERVICE

PROPER INFO

WORKING HOUR

LESSFORMALITIES

VARIETY OFPRODUCTS

IMPLICATIONS: When a customer visits a bank the first and foremost

thing he looks, that how quickly he is served, how his problem is

entertained by the bank employee and what is the working hour of the

bank. That’s why these three things contribute the maximum of this pie –

chart. Less formalities and variety of products although contributes less but

it has a major impact on the customer. So bank should follow on these

things also. Service sector like banking, preference should be given to

make.

54

WHICH OF THE FOLLOWING ATTRIBUTES COMPELLED YOU

MOST TO OPEN SAVING ACCOUNT IN ICICI BANK

SAVINGS A/C ATTRIBUTES

ATM CUM DEBIT

CARD, 26%

VALUE ADDED S. A/C, 48%

CHEQUE BOOK, 16%

PHONE / INTERNET BANKING,

10%

ATM CUM DEBITCARD

VALUE ADDED S.A/C

CHEQUE BOOK

PHONE /INTERNETBANKING

IMPLICATIONS: As we found in our finding that majority of the people

like the saving account, this chart reveals that what are the factor and their

contribution making their product really leading product of ICICI Bank.

VALUE ADDED SAVING ACCOUNT is undoable a unique sub product

of ICICI Bank. Since it has the appeal catch maximum customer as it

provides the facility of FIXED deposit in saving account ATM cum debit

card is also a major attributes as it made the banking easy. Personalized

chequebook is also a major attraction in this section. As far as other factors

are concern they are showing less appearance in this chart.

55

ACCOUNT TYPE

SAVING54%CURRENT

18%

FIXED15%

NRI8%

OTHER5%

SAVING

CURRENT

FIXED

NRI

OTHER

WHAT TYPE OF ACCOUNT DO YOU HAVE IN ICICI BANK?

IMPLICATIONS: Saving account is the leading and attractive product for

the ICICI Bank as it has occupied a major chunk in this chart. This number

and percentage clearly shows that this product has all the quality to give

the customer best services and ability to satisfy them. On the second and

third position current and fixed deposit has also been helpful to increase

the customer base but still their performance needs to be improved. As far

as NRI and other accounts are concerned they have less appearance. So

majority of the business is moving around few leading products. Reason

could be either people are not aware about the various products of the bank

or bank has limited range of products. So bank must ascertain that where

things are going wrong and for that what sort of necessary step could be

taken.

56

WHICH FACTOR AMONG THE FOLLOWING INFLUENCED

YOU MOST TO OPEN AN ACCOUNT IN ICICI BANK?

INFLUENCED FACTOR

FRIENDS / RELATIVE

44%

ADVERTISE MENT 33%

BANK EMPLOYEE

12%

PROSPECT US

11% FRIENDS / RELATIVE

ADVERTISEMENT

BANK EMPLOYEE

PROSPECTUS

IMPLICATIONS: It has been said a satisfied customer is the best medium

for an advertisement since in this chart friend / relative have played a key

role in opening the accounts of others. Which implies that bank’s real

customers are satisfied enough with facilities available on the products and

services enjoyed by them. On the other hand advertisement also plays a

vital role in influencing the customer. As their behavior not only please the

customer but also attract the customer. Well maintained prospectus is also

a major attributes of attracting the customer. Main focus of the bank

should be no satisfaction of customer.

57

YOUR REMARKS ON SAVING ACCOUNT?

REMARKS

EXCELLEN T

34%

GOOD 45%

AVERAGE 18%

POOR 3%

EXCELLENT

GOOD

AVERAGE

POOR

IMPLICATIONS: As this chart is showing at what level people are

satisfied with saving account. With its unique facility, features and ability

to serve all the needs of customers because by and large it can be said 79%

people of this chart are saying good and excellent saving account. Reason

for this could be different type of facility associated with this product,

either are rendering true value to the customer. Effort may be given to

know why there are people who are still saying average and poor along

saving account and what are the factor that are going wrong with the

people.

58

IN COMPARISION TO OTHER BANKS HOW WOULD YOU

RATE ICICI BANK?

COMPARISON

EXCELLENT

27%

GOOD47%

AVERAGE14%

POOR5%

CAN'T SAY7%

EXCELLENT

GOOD

AVERAGE

POOR

CAN'T SAY

IMPLICATIONS: Comparison with other banks depends on its overall

performance in the eyes of the people. In this chart it is clearly showing

that 74% of the people are satisfied with ICICI Bank. In a short span of

time of its existence in this city with strong competition from major public

sector bank like SBI and other private players bank has done well it has

occupied a different position in the people’s mind.

59

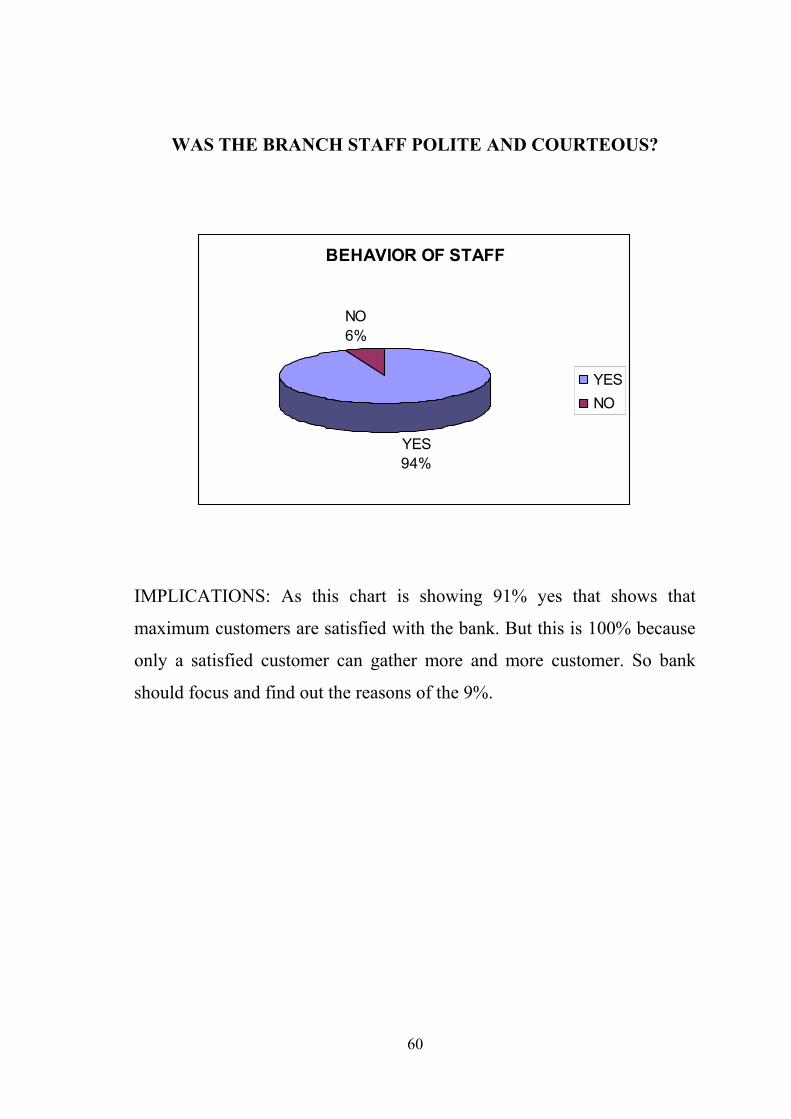

WAS THE BRANCH STAFF POLITE AND COURTEOUS?

BEHAVIOR OF STAFF

YES94%

NO6%

YES

NO

IMPLICATIONS: As this chart is showing 91% yes that shows that

maximum customers are satisfied with the bank. But this is 100% because

only a satisfied customer can gather more and more customer. So bank

should focus and find out the reasons of the 9%.

60

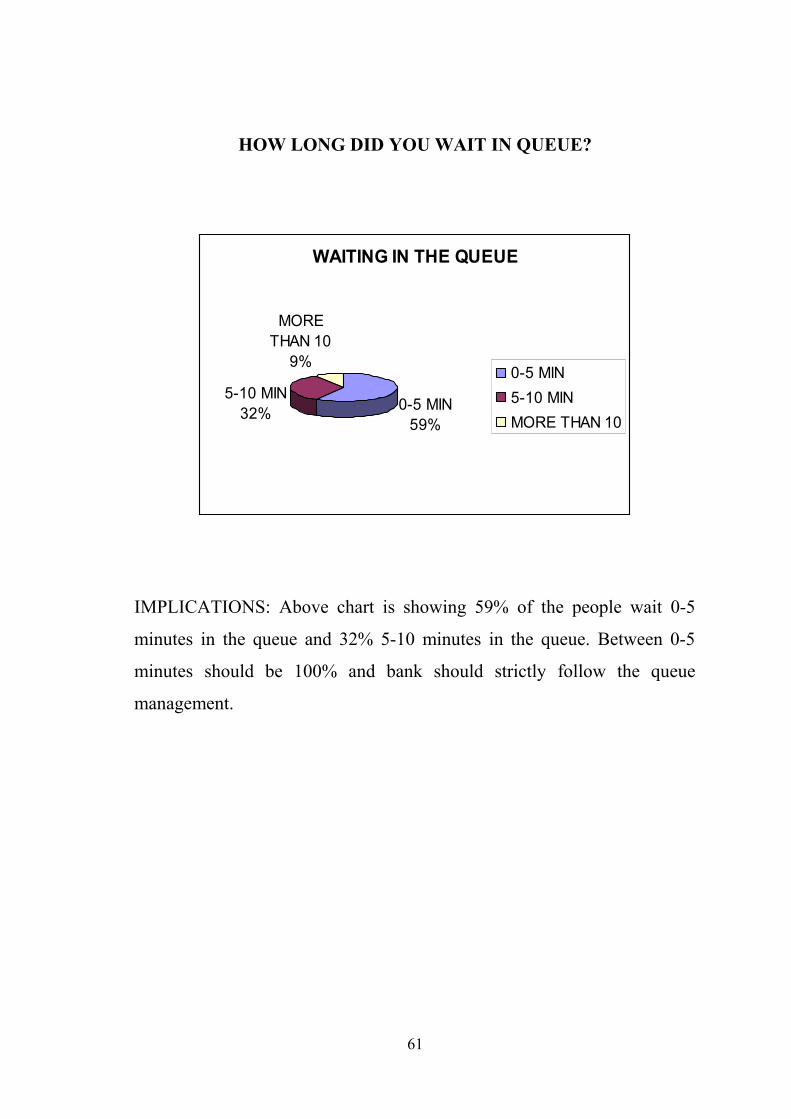

HOW LONG DID YOU WAIT IN QUEUE?

WAITING IN THE QUEUE

0-5 MIN59%

5-10 MIN32%

MORE THAN 10

9%0-5 MIN

5-10 MIN

MORE THAN 10

IMPLICATIONS: Above chart is showing 59% of the people wait 0-5

minutes in the queue and 32% 5-10 minutes in the queue. Between 0-5

minutes should be 100% and bank should strictly follow the queue

management.

61

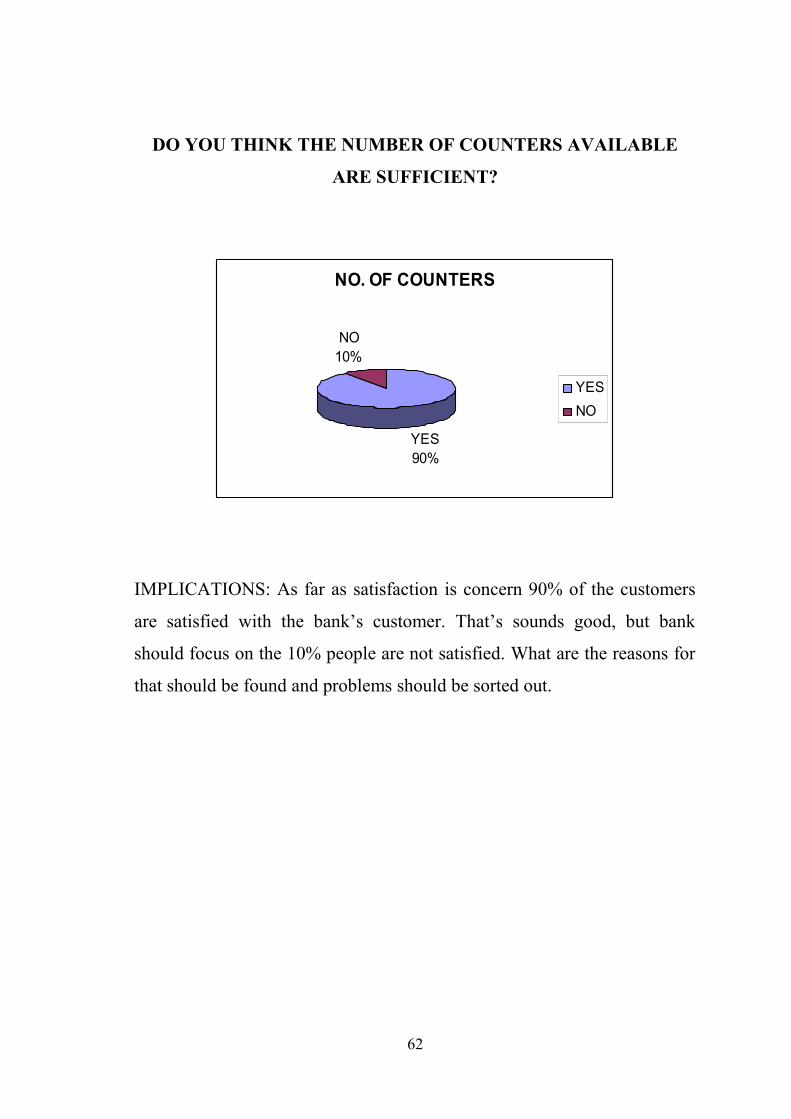

DO YOU THINK THE NUMBER OF COUNTERS AVAILABLE

ARE SUFFICIENT?

NO. OF COUNTERS

YES90%

NO10%

YES

NO

IMPLICATIONS: As far as satisfaction is concern 90% of the customers

are satisfied with the bank’s customer. That’s sounds good, but bank

should focus on the 10% people are not satisfied. What are the reasons for

that should be found and problems should be sorted out.

62

WOULD YOU RECOMMEND ICICI BANK TO OTHERS?

RECOMMANDATION

YES95%

NO5%

YES

NO

IMPLICATIONS: As per the chart we show that 5% of the people don’t

want to recommend ICICI Bank to others. Bank must find the reason of

their dissatisfaction because in this competitive world we have to achieve

this target.

63

FINDINGS & CONCLUSIONS

The liberalize policy of government of India permitted entry to private

sector in the banking, the industry has witnessed the entry of new