Embed Size (px)

Citation preview

Management Accounting

Variance Analysis ExcerptManagement and Cost Accounting

Douglas A. Sledge, CPA, CGMA, CMA, MBA, Certified QuickBooks ProAdvisorManagement AccountantDba: Douglas A. Sledge. CGMA Consultant

www.dougsledgecma.com

Exhibits and information presented in this seminar text are general in nature and the author does not represent that the use of such will be correct in any specific application.

Copyright 2008Douglas A. Sledge

This document, or any portions thereof, may not be reproduced

© Douglas A. Sledge Page 1

without the express written consent of the author

© Douglas A. Sledge Page 2

Basics of Operations CostingManufacturing Cost Accounting

A Brief Series PublicationDouglas A. Sledge, CMA, CPA, MBA, Certified QuickBooks® ProAdvisor

The Brief Series of handbooks is designed as a quick read review of today’s hot business topics. Each handbook in the series is a short, easy to understand reading, ideal for the business executive wishing to understand and review essential, sometimes make or break, operational measures of small business. The Brief Series concept concentrates on management understanding rather than on technical detail.

In the Brief Series, we will confine our discussion to the small for-profit business operation. Small business is generally defined as less than fifty million dollars in annual sales. This business group has generally not been provided analytical and control support commensurate with medium and large scale operations in the area of cost accounting. In this text we will explore cost accounting for the small manufacturer.

The operations costing concept to be discussed develops the cost of the product at any stage of production from Raw Material (RM), to work-in-process (WIP), through Finished Goods (FG). Costs and inputs are developed for each product through the identification and accumulation of materials, labor and overhead expenses incurred in processing the product to each sequential step being reviewed. In addition, the identification and analysis of material, labor and overhead variances provides support for decision making and resolution of efficiency and spending issues in the operation.

For small & medium business (SMB), this methodology is generally designated as Manufacturing Resource Planning (MRPII), an extension of earlier Materials Resource Planning (MRP) methodologies. MRPII is the counterpart to Enterprise Resource Planning (ERP) for larger operations… The main difference in the two concepts is that ERP addresses cost impact through external support and interactive operations, whereas MRPII typically addresses cost influences at one location. The basic cost and analysis concepts are the same for either level of operation. The three terms, MRP, MRPII and ERP, are often used interchangeably in production environment discussions.

Disclaimer: The training, information and materials used and offered in this course of training are presented with no specific guarantee or warranty as to use, knowledge or application of such information, and/or training. While due diligence and significant review have been taken by the program developer and sponsors, neither the presenter(s), author, compiler, editor, sponsoring organizations (including, without limitation, its officers and directors) shall have any liability to any person or entity with respect to any losses, misapplication of programs, or damage caused or alleged to have been caused directly or indirectly by the use, instructions or information contained and/or presented in this program.

© Douglas A. Sledge Page 3

Your Seminar Leader: Douglas A. Sledge, CPA, CGMA, CMA, MBA, Certified Intuit (QuickBooks®) ProAdvisor

Resume Brief 2015 Douglas A. Sledge is a Certified Public Accountant (CPA) (Alabama & Texas), a Chartered Global Management Accountant (CGMA), a Certified Management Accountant (CMA), a Certified Intuit (QuickBooks®) ProAdvisor (Premier, On-Line & Enterprise Solutions), and holds a Master of Business Administration (MBA) from the University of North Alabama (UNA). He has been employed professionally in support of startup, turnaround and continuing operations for a diverse mix of employers and clients ranging from local shops to a major school system to national corporations. He provides Management Consulting Services (Executive Advisor/CFO/Controller/Cost Controller/Management Accountant)… he does not provide CPA attest functions.

He completed coursework for a major in Accounting at the University of North Alabama (UNA) in 1973, as a Bachelor of Science post-graduate, following a three-year enlistment as a German language qualified Intelligence Agent with the US Army. Previously, he graduated with undergraduate double majors (B.S.) from UNA in Physics and Chemistry in 1968. He accomplished his MBA in 1977.

He instructed with UNA in an adjunct capacity for several years, and conducted a variety of seminars with subjects related to strategic business planning, budgeting, inventory control, cost accounting, presentation techniques, and general accounting; for UNA, Brookhaven Community College (DCCCD . Dallas), Northeast Community College (TCCD . Fort Worth), UT Arlington-SBDC, and the GulfSouth Council of the Institute of Management Accountants (IMA). He is an approved provider for continuing education with the Alabama Board of Heating and Air Conditioning Contractors (HVAC).

He is a Certified Journeyman Gas Fitter and a Certified HVAC Contractor (#83142) in the State of Alabama (both inactive, but current status). Early in his career, he held supervisory positions in production manufacturing & maintenance, HVAC and gas fitting. While employed as a Cost Accountant/Analyst with Ford Motor Company, he completed a two year management development program, supervising production operations and industrial plant maintenance. Recently, he provided Management Accounting Consultant services in the aerospace distribution industry in Texas.

He is a former Regional Council President and National Vice President with the Institute of Management Accountants (IMA). He currently is a member of the IMA, the American Institute of Certified Public Accountants (AICPA), and the Alabama Society of Public Accountants (ASCPA). He serves on the School of Accountancy Advisory Committee with UNA (SME Management Accountant). He is an honorary member of Delta Mu Delta Business Honor Society (2000). He was a member of the national Member Services Committee of the IMA in 2003, and completed requirements for certification as an Alabama Certified School Financial Officer in 2004 (AASBO). He has been certified as a Intuit (QuickBooks®) ProAdvisor since 2008, and is a gold member of the QuickBooks National Advisors Network (NAN).

© Douglas A. Sledge Page 4

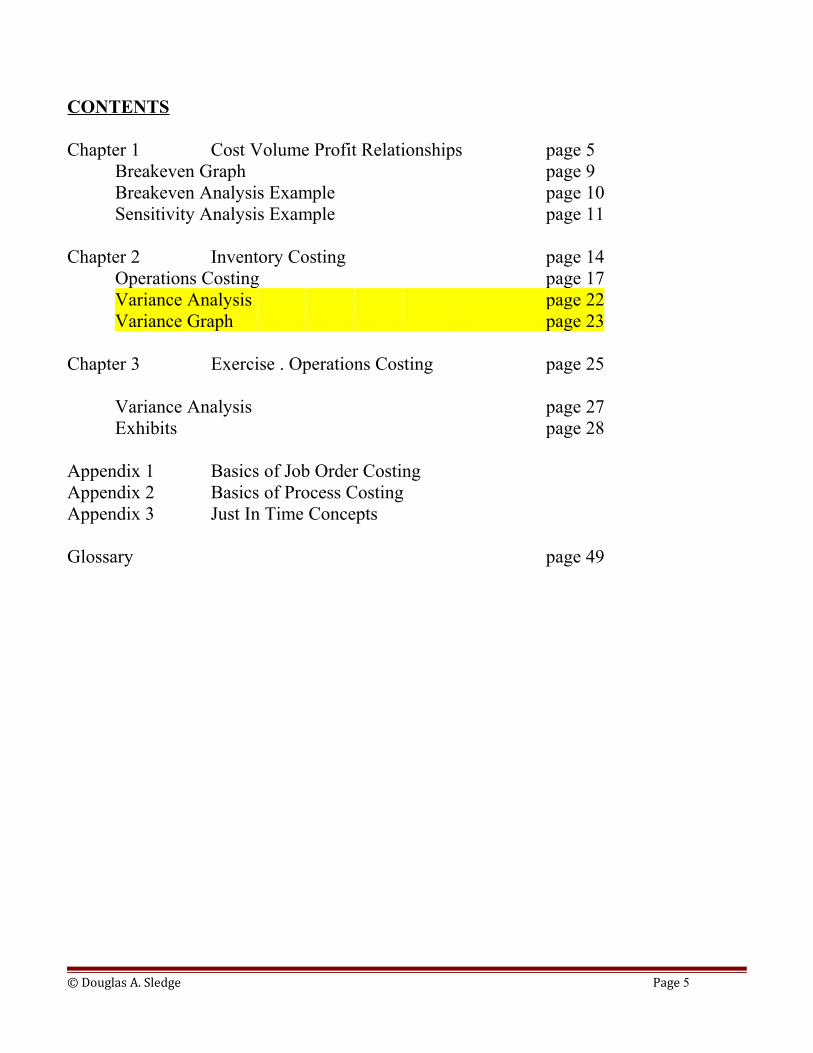

CONTENTS

Chapter 1 Cost Volume Profit Relationships page 5Breakeven Graph page 9Breakeven Analysis Example page 10Sensitivity Analysis Example page 11

Chapter 2 Inventory Costing page 14Operations Costing page 17Variance Analysis page 22Variance Graph page 23

Chapter 3 Exercise . Operations Costing page 25

Variance Analysis page 27Exhibits page 28

Appendix 1 Basics of Job Order CostingAppendix 2 Basics of Process CostingAppendix 3 Just In Time Concepts

Glossary page 49

© Douglas A. Sledge Page 5

Variance Analysis:

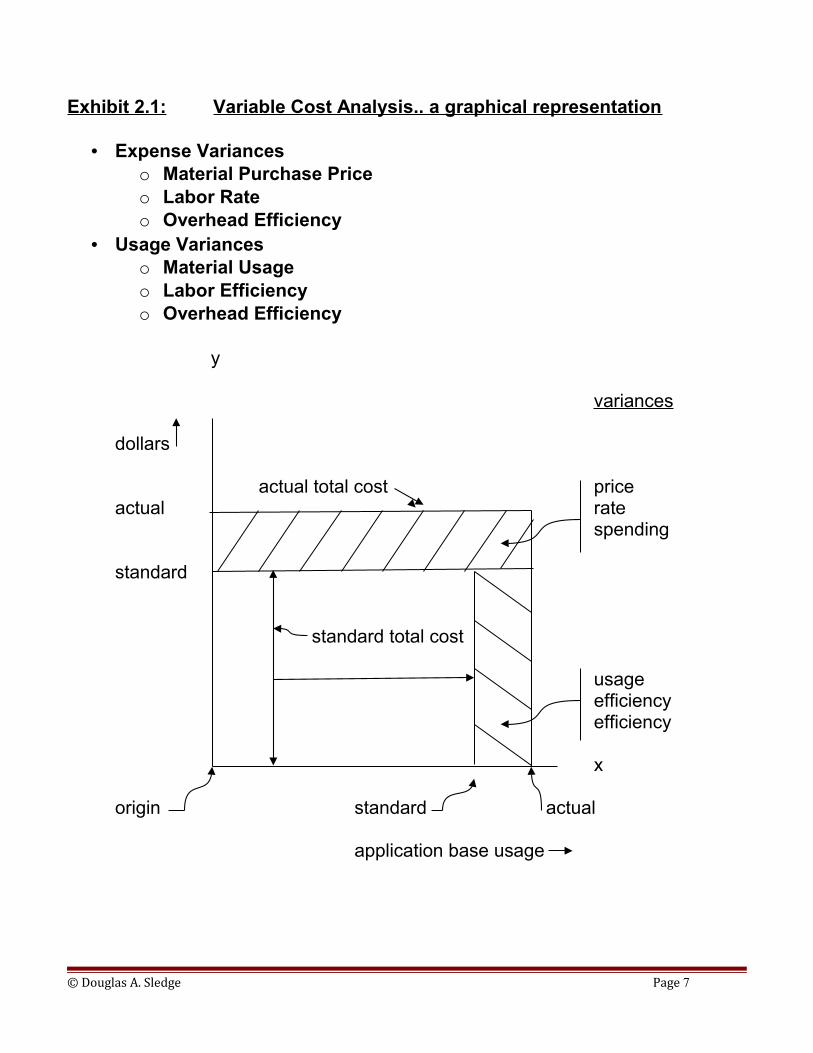

Variance analysis is a important element of management’s production control and operations improvement. Following are definitions of generally recognized production variances and methods of calculation. Variable cost variances are defined with differing terms, but generally they are either price or usage variances… Exhibit 2.1 illustrates the concept of price and usage variances to the three variable costs of manufacturing.

Price variance: material price, labor rate, overhead spending.Usage variances: material usage, labor efficiency, overhead efficiency

Fixed overhead variance analysis seeks to identify variances of application… the reporting is for spending (expense) and applied volume. The variances indicate if we paid more than production activity provided for as applied. Keep in mind that for the small manufacturer... the overall miss to budget expenditures for fixed cost is the expense to be analyzed, recalling that fixed costs, by definition, do not change as a result of production activity. The important analysis for fixed cost variance is to identify which costs have increased or decreased… such as rent, management salary, etc…..

Definitions of production cost variances:

1. Material usage variance: (standard quantity less actual quantity) extended at standard unit cost.

2. Material purchase price variance: (standard unit price less actual unit price) extended at actual units.

3. Labor efficiency variance: (standard labor hours less actual hours) extended at standard labor hourly rate.

4. Labor rate variance: (standard labor hourly rate less actual hourly rate) extended at actual hours.

5. VOH efficiency variance: (standard base less actual base) extended at the standard rate.6. VOH spending variance: (actual base extended at the standard rate) less the actual

expense.7. FOH Spending variance… Actual total FOH expended less the (actual unit quantity

application base produced multiplied by the budgeted FOH application rate)8. FOH Volume variance: Budgeted application rate multiplied by (the actual application

base produced less the standard application base)

© Douglas A. Sledge Page 6

Exhibit 2.1: Variable Cost Analysis.. a graphical representation

• Expense Varianceso Material Purchase Priceo Labor Rateo Overhead Efficiency

• Usage Varianceso Material Usageo Labor Efficiencyo Overhead Efficiency

y

variances

dollars

actual total cost priceactual rate

spending

standard

standard total cost

usageefficiencyefficiency

x

origin standard actual

application base usage

© Douglas A. Sledge Page 7

GLOSSARY:

TERM: Assembly – A combination of any raw material (RM) or subassemblies through the application of conversion activity. The assembly may be constructed by any means which facilitates the combination or differentiation from the prior item. The assembly can be accomplishment by any means, to include…. welding, cooking, extrusion, chemical process, mixing, molding, injection molding, fastening, strapping… and so on…

TERM: Finished Goods (FG) are products completed and available for sale and shipment to customers.

TERM: Fixed Costs are those costs which do not change as a direct result of cost object activity.

TERM: Fixed Overhead (FOH) is made up of those production support costs which are not included in VOH as defined above. Federal regulations require that some administrative costs be included in FOH.

TERM: Job Order Costing refers to a system of cost development in which cost components are accumulated by job. Examples are repair shops, professional services, medical services, construction and so on… Costs are developed for each job, be it vehicle repair or surgery. This system remains in use in various forms in the service industry. See Appendix 1 for further discussion.

TERM: JUST IN TIME INVENTORY CONTROL SYSTEM: Early on, the Institute of Management Accountants (IMA) defined a just-in-time (JIT) inventory system as something like: “ A system whose purpose is to produce or procure the right parts at the right time, as they are needed rather than when they can be made. It is a “pull” manufacturing system that moves goods through a shop based on end-unit demand. Just-in-time focuses on maintaining a constant flow of components and products rather than batches of work-in-process inventory.”

TERM: Materials {Raw Materials (RM)} are those inventory items purchased for inclusion in the product to be manufactured.

© Douglas A. Sledge Page 8

TERM: Process Costing refers to a system of cost development for products which are homogeneous in development (each unit is similar to any other unit of the same product). Examples are milk processors, paint manufacturers, water treatment plants, and so on. This system has been virtually obsoleted by MRPII and ERP systems. Process costing is discussed further in Appendix 2.

TERM: Relevant Range of Activity… That operational range of cost activity, within which the company should expect to operate, and within which, variable cost relationships and fixed costs remain reasonably stable (constant).

TERM: Routing.. The production path followed for development of a finished assembly (finished product)… i.e…. A sequential delineation of workcenter activity (operation) and costing for production of each subassembly and the final finished product.

TERM: Subassembly… Any assembly which is a component of another assembly.

TERM: Unit Variable Contribution is the unit sales price less the unit variable cost.

TERM: Variable Contribution is the excess of revenue over variable costs.

TERM: Variable Contribution Ratio: The ratio of variable contribution to sales price, expressed as a decimal.

TERM: Variable Costs are those costs which change in direct relation to, and as a result of, changes in cost object activity, within the relevant range of activity. This cost object activity is different for different businesses… Examples include:

• Production cost for manufacturing• Installation and service cost for HVAC and other construction and service

operations.• Material cost for merchandising• Percentage based sales commissions

TERM: Variable Cost Ratio: The ratio of variable costs to sales price, expressed as a decimal.

TERM: Variable Overhead (VOH) is made up of those production/service support costs which are incurred as a direct result of production/service activity and fluctuate linearly with such activity.

© Douglas A. Sledge Page 9

TERM: Work-In-Process (WIP) are those partially completed inventory items at various stages of completion.

© Douglas A. Sledge Page 10