Embed Size (px)

Citation preview

A Revolution to the Way We Live – The Role of M2M Communications in Smart Cities

Yiru Zhong, Research Analyst

Information & Communication Technologies Information & Communication Technologies

15th June 2011

Focus Points

� Setting the Scene

� An Unmistakable Trend

2

� Opportunities for ICT Industry

� Key Takeaways

Setting the Scene

3

Frost & Sullivan ICT M2M Research Is Supported by Our Other Research Areas

2010/11 Research Coverage to date

• M2M Market Sizing in Europe 2010

• M2M – The role of Telecom Service Providers

• Smart cards in M2M

• A Revolution in the Way We Live – M2M in Smart

Cities

• Ericsson floats the M2M boat with acquisition

Frost & Sullivan’s 9 Research Practices

4

2011 Research Delivery Schedule

• Connected Home Initiatives in Europe

• M2M in Utilities

• M2M in Government – Driving the Smart Cities

Concept

• M2M: Where are we today?

• M2M Market Sizing in Europe 2011

Source: Frost & Sullivan

Looking For The Next Layer of M2M Opportunity

Telecoms M2M Market: M2M Demand in Industries (Europe), 2008-2020

Co

mp

lexit

y o

f M

2M

Dem

an

d Hig

h

• Logistics• Transportation

Not all industries offer equal M2M opportunities forall types of telecom M2M providers.

It is necessary to determine:• Current and future absolute size over a short,

medium and long-term horizon• Current and 3-year/5-year/10-year growth

prospects

5

<2008 2008-2010 2010-2015 2016-2020Timeline

Co

mp

lexit

y o

f M

2M

Dem

an

d

Lo

w

• Logistics• Transportation• Retail

• Logistics• Transportation• Retail• Utilities• Manufacturing• Security

• Logistics• Transportation• Retail• Utilities• Manufacturing• Security• Government

• Transportation• Retail• Utilities• Manufacturing• Security• Government• Healthcare• Emergency Services

Source: Frost & Sullivan

“M2M - The Role of Telecoms Service Providers”

It is a Natural Extension of a Digital Society into One That is Interconnected and Intelligent

COMMUNICATING SOCIALISING

Interacting Watching TV

Playing games

Socialising (virtually)

Internet surfingGambling

Keeping informed

Reading

Blogging/Video blogging

Communicating

Transacting with counterparties

6

WORKING

Home working

Off site workingRemote accessing

Educating

Shopping

Conducting business activities

Reading

Accessing government services

Source: Frost & Sullivan

Ubiquitous communication networks enable the user to conduct its everyday activities

Source: Frost & Sullivan

Branding of Cities Associated with Ubiquity and Intelligent Use of Bits of Data

Smart Economy

Smart Mobility

7

Source: www.smart-cities.eu

Smart Environment

Smart PeopleSmart Living

Smart Governance

An Unmistakable Trend

Rapid urbanisation triggers rethink in urban

8

Rapid urbanisation triggers rethink in urban policies

UN Predicts Further Urbanisation; Formation of Mega-Regions by 2023

JapanNagoya – Osaka –

Kyoto - KobeBeijing - Pyongyang -Seoul - Tokyo

9

Source: UN-Habitat 2010

BrazilRio de Janeiro-São Paulo

Mega RegionsUrban Corridors

ChinaHong Kong – Shenzhen –

Guangzhou

Ghana - Togo - Benin - Nigeria

Mumbai -Delhi

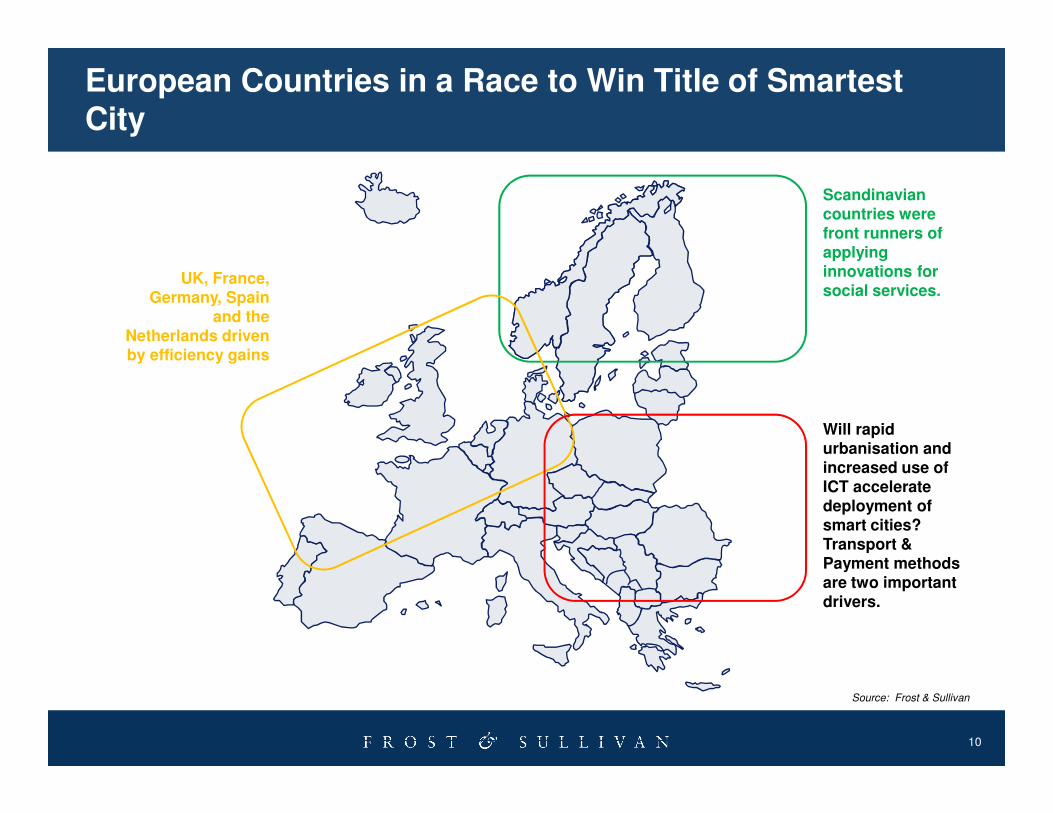

European Countries in a Race to Win Title of Smartest City

Scandinavian countries were front runners of applying innovations for social services.

UK, France, Germany, Spain

and the Netherlands driven by efficiency gains

10

Source: Frost & Sullivan

Will rapid urbanisation and increased use of ICT accelerate deployment of smart cities?Transport & Payment methods are two important drivers.

Drivers and Desired Outcomes of Smart Cities Deployment

Desired OutcomesDesired Outcomes

• Increased citizens’ expectations of a modern city living environment

• Availability of technology at mass market prices for intelligent use of such scarce resources as energy and landmass

Reduce overall government cost burden in

the long run

Drivers for Smart Cities Deployment

Drivers for Smart Cities Deployment

Prestige outcomes aside, governments aim to

achieve three main outcomes

1

11

• National energy targets trigger local government rethink in holistic urbanisation policies

• Public transport policies coincide with local government services initiatives

Improve local government services in an

urban setting2

Achieve any national government’s energy

targets3

• Consumption of local government services

• Local business economy

• Public transportation policies

The Role of M2M Communications in a Smart City Scenario

Smart Economy Smart MobilitySmart

Governance

12

• Citizen’s digital lifestyle• Connected

citizens

• Intelligent Environmental Management

Source: Frost & Sullivan

www.smart-cities.eu

Smart Environment

Smart PeopleSmart Living

Opportunities for ICT Industry

For Whom, How and When

13

For Whom, How and When

Energy & Environment• Utilities

• Environmental Management

For Whom: Is there A Mega-Ecosystem for Smart Cities?

Public Transportation• Rail• Metro-rail• Buses• Air• Traffic Management

Telecoms Industry

Service Providers

Vendors

Systems &

IT IndustrySystem Integrators

Systems &

SoftwareM2M Sector

14

Automotive & Logistics• Traffic Management• Environmentally friendly fleet

Civil & Emergency Services• Security, Access & Public

safety surveillance

• Automated Response Services

SoftwareM2M Sector

Modules

Service Providers

Technology

Providers

Platform Providers

Middle & Software

Providers

Source: Frost & Sullivan

How: What is The Route to Market?

ITS

ecto

rTele

co

ms

Ind

ustr

y

Telecoms M2M Market: Opportunities in the Eco-System (Europe), 2010

Partnerships with either ITor M2M players addressTelcos’ challenges ofindustry credibility, achievingspeed to market, andaccelerating internalexperience enhancement .

Partnerships withTelcos increase ITcompanies’ scope ofcustomers for ITcompanies’ M2M verticalexpertise, integrationservices, systems andsoftware applications.

15

M2MIndustry

Secto

rTele

co

ms

Ind

ustr

ysoftware applications.

Partnerships with Telcos increaseM2M sector’s scope of customersfor M2M modules, technology andsoftware and applications.

Source: Frost & Sullivan

“M2M - The Role of Telecoms Service Providers”

When: Incremental Increase in Intelligence

Telecoms M2M Market: Estimation of M2M Demand on a Product Life Cycle Curve (Europe), 2010

• Utilities - Smart Meters• Transportation -

Connected Cars, E-toll, Advanced Telematics for Insurance Purposes

• Security - Remote Geo-fencing

• Retail - Intelligent Warehousing, Consumer

• Utilities - Automatic Reading in Scandinavia

• Transportation -Telematics, Logistics Track and Trace

• Security - Track and trace • Retail - Warehousing

Volu

me o

f D

em

and

16

Introduction Growth Maturity Decline

Product Life Cycle Phase

Warehousing, Consumer Electronics

• Utilities - Smart Grids, Smart Energy

• Transportation -Connected Cars,

• Retail - Interactive Marketing

• Healthcare• Smart Cities

Volu

me o

f D

em

and

Source: Frost & Sullivan

“M2M - The Role of Telecoms Service Providers”

Stumbling Blocks in Capturing M2M Opportunities in Smart Cities

Imp

act

Low

17

Imp

act

Lack of relevant sector experience to deploy relevant M2M applications

Lack of visibility in decision makers and stakeholders to provide a true end to end solutions

High

Lack of interoperability issues, of networks, protocols, and end points (including sensors and terminals)

Practical partnership tensions in revenue sharing agreements

Key Takeaways

18

Conclusion/Key Take-Aways

• Traditional M2M services become low hanging fruits - M2M offers in readily

used functions such as track and trace expanded within such traditional sectors

as transportation and logistics.

• Telecoms’ M2M offers are relatively similar at this early stage – Telcos are

exploiting their existing enterprise relationships to establish first mover

advantages in such readily functions as telematics, smart metering and even

M2M communications in consumer electronics.

19

M2M communications in consumer electronics.

• Partnerships could yet tilt the dynamics within ICT sector – Some telcos

are aggressively driving cross industry collaborations with industrial equipment

vendors and specialist application providers to be relevant in a world of

interconnected machines and objects.

Next Steps

� Request a proposal for Growth Partnership Services or Growth Consulting Services to support you and your team to accelerate the growth of your company. ([email protected])

� Join us at our annual Growth, Innovation, and Leadership 2012: A Frost & Sullivan Global Congress on Corporate Growthoccurring 15 – 16 May, 2012 (www.gil-global.com)

20

� Register for Frost & Sullivan’s Growth Opportunity Newsletter and keep abreast of innovative growth opportunities (www.frost.com/news)

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

What would you like to see from Frost & Sullivan?

21

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by rating this presentation

Frost & Sullivan’s Growth Consulting can assist with your growth strategies

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

http://www.linkedin.com/companies/4506

22

http://twitter.com/frost_sullivan

http://www.linkedin.com/companies/4506

http://www.slideshare.net/FrostandSullivan

For Additional Information

Joanna Lewandowska

Corporate Communications

ICT

+48 22 390 41 46

Gustavo Cury

Sales Manager

ICT

+44 207 343 8310

23

Yiru Zhong

Researach Analyst

ICT

+48 22 390 41 28

Adrian Drozd

Research Manager

ICT

+44 1865 398 699