Embed Size (px)

Citation preview

Insights into the Connected Consumer Survey 2015

© Analysys Mason Limited 2015

WHITE PAPER

analysysmason.com

Insights into the Connected Consumer Survey 2015

30/3/15

Martin Scott and Patrick Rusby

Insights into the Connected Consumer Survey 2015

© Analysys Mason Limited 2015

KEY QUESTIONS ANSWERED IN THE CONNECTED

CONSUMER SURVEY 2015 REPORT SERIES

WHO NEEDS TO READ THESE REPORTS

How can mobile operators improve customer retention – what are the

drivers of churn and what attracts customers to a new deal?

How can fixed broadband operators reduce churn and do fixed–mobile

convergent bundles improve customer retention?

How can operators address OTT messaging and voice services – do

unlimited minutes or SMS bundles work?

Does OTT video compete with pay TV, or can both services be

complementary – does the role of pay-TV providers change as OTT

services become more popular?

Which demographic groupings use mobile money services, and are these

services successful?

2

This white paper presents a small amount of

the data from Analysys Mason’s Connected

Consumer Survey, conducted in July and

August 2014 in the USA, Europe, Asia, the

Middle East and Africa. The Asian, Middle

East and African data was collected using

On Device Research’s mobile panel.

Analysys Mason’s Connected Consumer

Survey is a multi-year study that tracks and

measures consumers’ changing telecoms

and media habits, device ownership,

connectivity options and future plans.

Key topics covered include: mobile customer

retention, fixed broadband customer

retention, pay-TV and online video

consumption, OTT communication and the

digital economy.

About the Connected Consumer 2015

The reports derived from the Connected Consumer Survey 2015 cover a

wide array of topics related to the telecoms media and tech (TMT) sector;

the reports are relevant to telecoms operators, as well as network

equipment and consumer electronics vendors, Internet players and

businesses engaging directly or indirectly with consumers in the digital

economy.

The reports will be particularly relevant to executives and managers in

product, strategy, marketing and market intelligence teams of these

types of business.

Insights into the Connected Consumer Survey 2015

© Analysys Mason Limited 2015 3

Geographical coverage of Connected Consumer 2015

Online survey – Survey

Sampling International

Browser based mobile survey

– On Device Research

USA

UK

Spain

France

Germany

Poland

Turkey

Morocco

Saudi

Arabia

UAE

South

Africa

South

Korea

Malaysia

Indonesia

Qatar

Insights into the Connected Consumer Survey 2015

© Analysys Mason Limited 2015

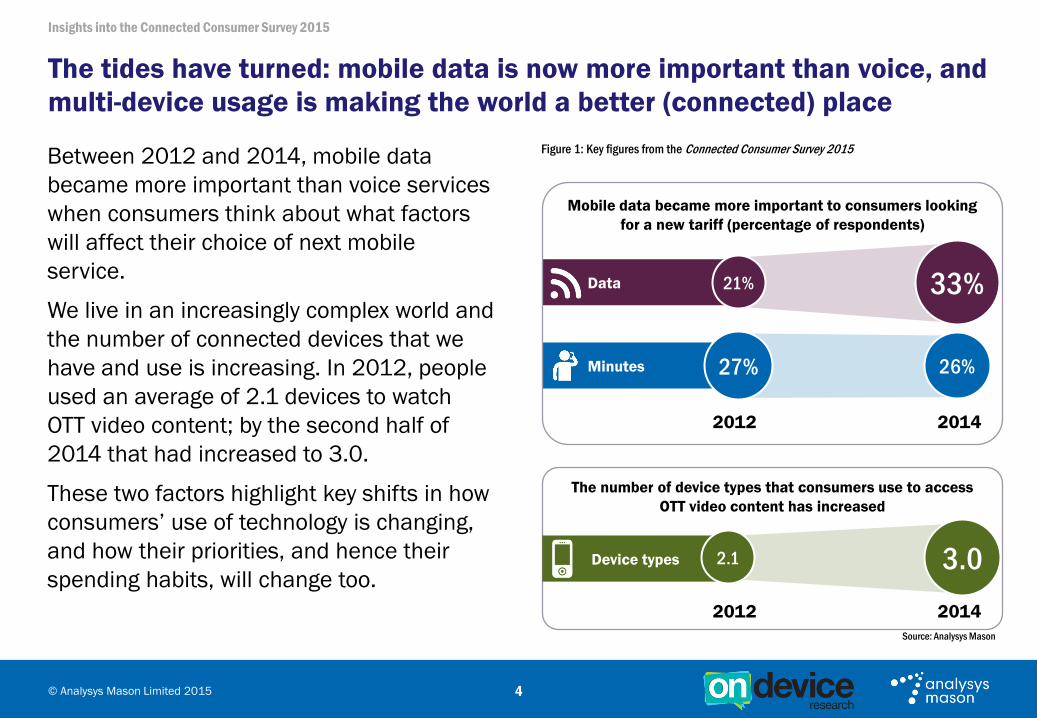

Figure 1: Key figures from the Connected Consumer Survey 2015

4

Between 2012 and 2014, mobile data

became more important than voice services

when consumers think about what factors

will affect their choice of next mobile

service.

We live in an increasingly complex world and

the number of connected devices that we

have and use is increasing. In 2012, people

used an average of 2.1 devices to watch

OTT video content; by the second half of

2014 that had increased to 3.0.

These two factors highlight key shifts in how

consumers’ use of technology is changing,

and how their priorities, and hence their

spending habits, will change too.

The tides have turned: mobile data is now more important than voice, and

multi-device usage is making the world a better (connected) place

Data

Minutes

21%

27%

33%

26%

Mobile data became more important to consumers looking

for a new tariff (percentage of respondents)

2012 2014

The number of device types that consumers use to access

OTT video content has increased

2012 2014

Device types 2.1 3.0

Source: Analysys Mason

Insights into the Connected Consumer Survey 2015

© Analysys Mason Limited 2015 5

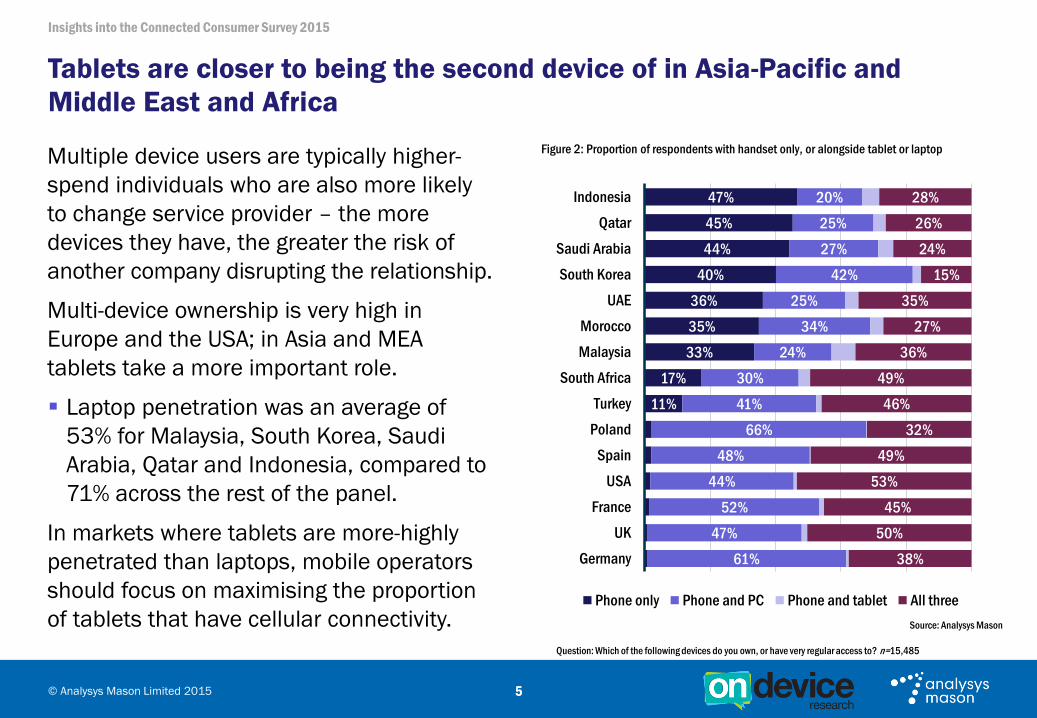

Multiple device users are typically higher-

spend individuals who are also more likely

to change service provider – the more

devices they have, the greater the risk of

another company disrupting the relationship.

Multi-device ownership is very high in

Europe and the USA; in Asia and MEA

tablets take a more important role.

Laptop penetration was an average of

53% for Malaysia, South Korea, Saudi

Arabia, Qatar and Indonesia, compared to

71% across the rest of the panel.

In markets where tablets are more-highly

penetrated than laptops, mobile operators

should focus on maximising the proportion

of tablets that have cellular connectivity.

Tablets are closer to being the second device of in Asia-Pacific and

Middle East and Africa

Figure 2: Proportion of respondents with handset only, or alongside tablet or laptop

Source: Analysys Mason

Question: Which of the following devices do you own, or have very regular access to? n=15,485

11%

17%

33%

35%

36%

40%

44%

45%

47%

61%

47%

52%

44%

48%

66%

41%

30%

24%

34%

25%

42%

27%

25%

20%

38%

50%

45%

53%

49%

32%

46%

49%

36%

27%

35%

15%

24%

26%

28%

Germany

UK

France

USA

Spain

Poland

Turkey

South Africa

Malaysia

Morocco

UAE

South Korea

Saudi Arabia

Qatar

Indonesia

Phone only Phone and PC Phone and tablet All three

Insights into the Connected Consumer Survey 2015

© Analysys Mason Limited 2015

iPhone

users

iPad

users

Laptop

users

Smartphone

users

Tablet

users

Laptop

users

8% of Apple

device owners use

all three devices

from Apple

2% of Samsung

device owners use

all three devices

from Samsung

2.43 hours

per day per Apple

device

2.03 hours

per day per

Samsung device

Source: Analysys Mason

Questions: Which of the following devices do you own, or have very regular access to? n=7,485

What is the manufacturer/brand of your most used phone? n=7,052

You stated earlier that you own or have access to a tablet. What is the brand of the tablet? n=3,344

What is the brand of your most-used laptop? n=5,705

6

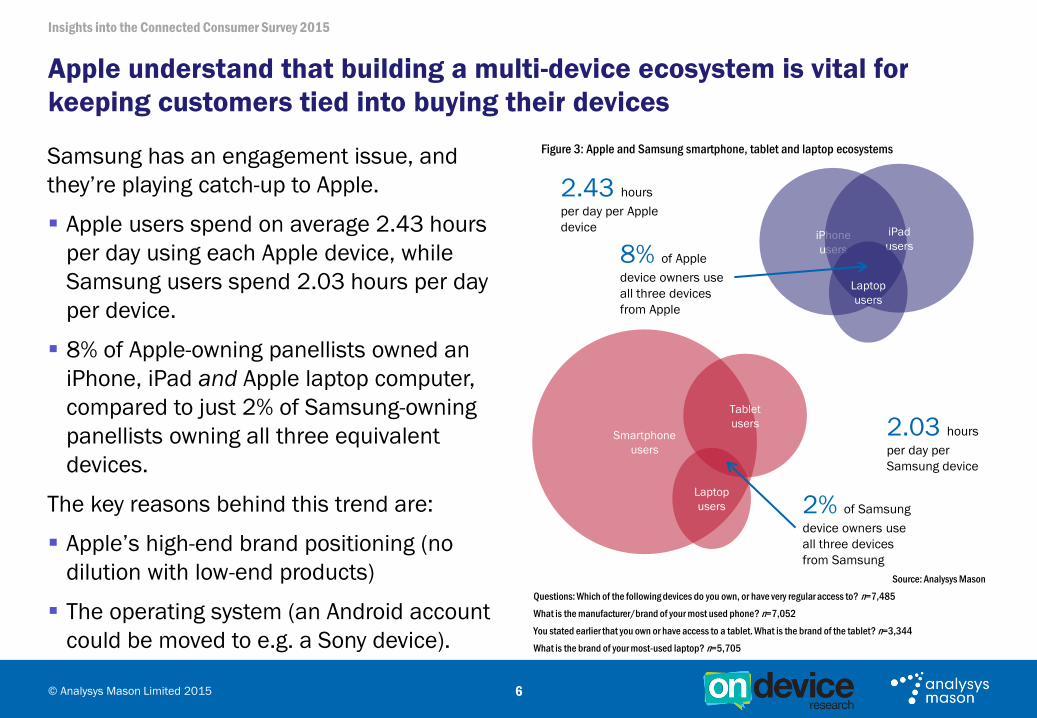

Samsung has an engagement issue, and

they’re playing catch-up to Apple.

Apple users spend on average 2.43 hours

per day using each Apple device, while

Samsung users spend 2.03 hours per day

per device.

8% of Apple-owning panellists owned an

iPhone, iPad and Apple laptop computer,

compared to just 2% of Samsung-owning

panellists owning all three equivalent

devices.

The key reasons behind this trend are:

Apple’s high-end brand positioning (no

dilution with low-end products)

The operating system (an Android account

could be moved to e.g. a Sony device).

Apple understand that building a multi-device ecosystem is vital for

keeping customers tied into buying their devices

Figure 3: Apple and Samsung smartphone, tablet and laptop ecosystems

Insights into the Connected Consumer Survey 2015

© Analysys Mason Limited 2015

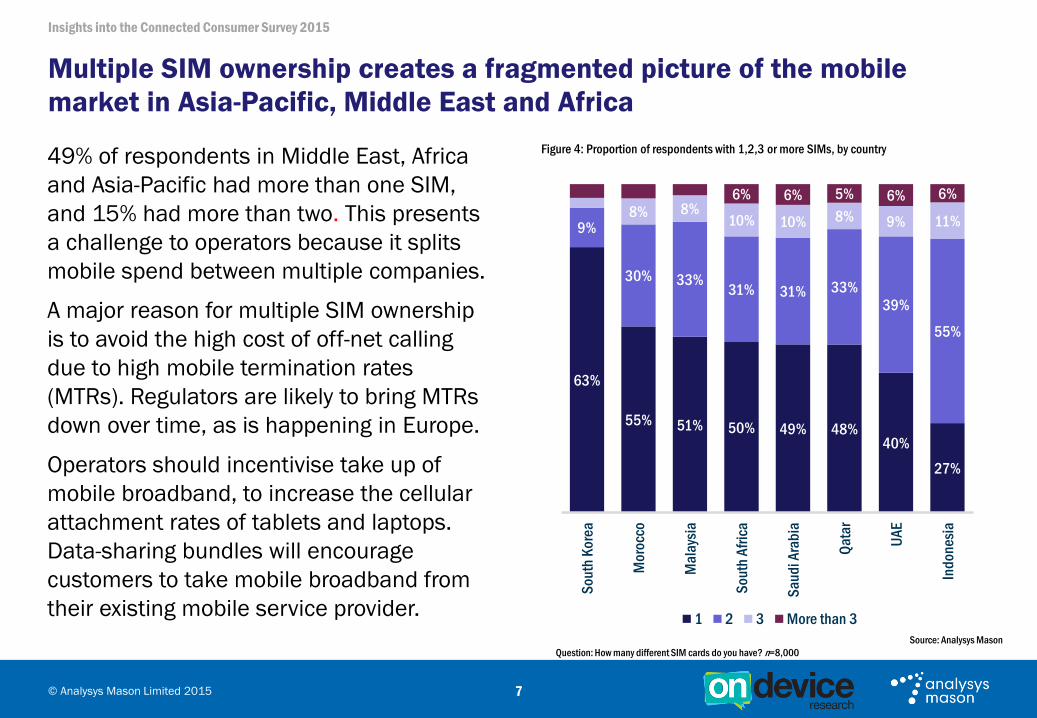

Figure 4: Proportion of respondents with 1,2,3 or more SIMs, by country

7

49% of respondents in Middle East, Africa

and Asia-Pacific had more than one SIM,

and 15% had more than two. This presents

a challenge to operators because it splits

mobile spend between multiple companies.

A major reason for multiple SIM ownership

is to avoid the high cost of off-net calling

due to high mobile termination rates

(MTRs). Regulators are likely to bring MTRs

down over time, as is happening in Europe.

Operators should incentivise take up of

mobile broadband, to increase the cellular

attachment rates of tablets and laptops.

Data-sharing bundles will encourage

customers to take mobile broadband from

their existing mobile service provider.

Multiple SIM ownership creates a fragmented picture of the mobile

market in Asia-Pacific, Middle East and Africa

Source: Analysys Mason

Question: How many different SIM cards do you have? n=8,000

63%

55% 51% 50% 49% 48%40%

27%

9%

30% 33%31% 31% 33%

39%

55%

8% 8%10% 10% 8% 9% 11%

6% 6% 5% 6% 6%

So

uth

Ko

rea

Mo

rocc

o

Ma

lays

ia

So

uth

Afr

ica

Sa

ud

i Ara

bia

Qa

tar

UA

E

Ind

on

esia

1 2 3 More than 3

Insights into the Connected Consumer Survey 2015

© Analysys Mason Limited 2015

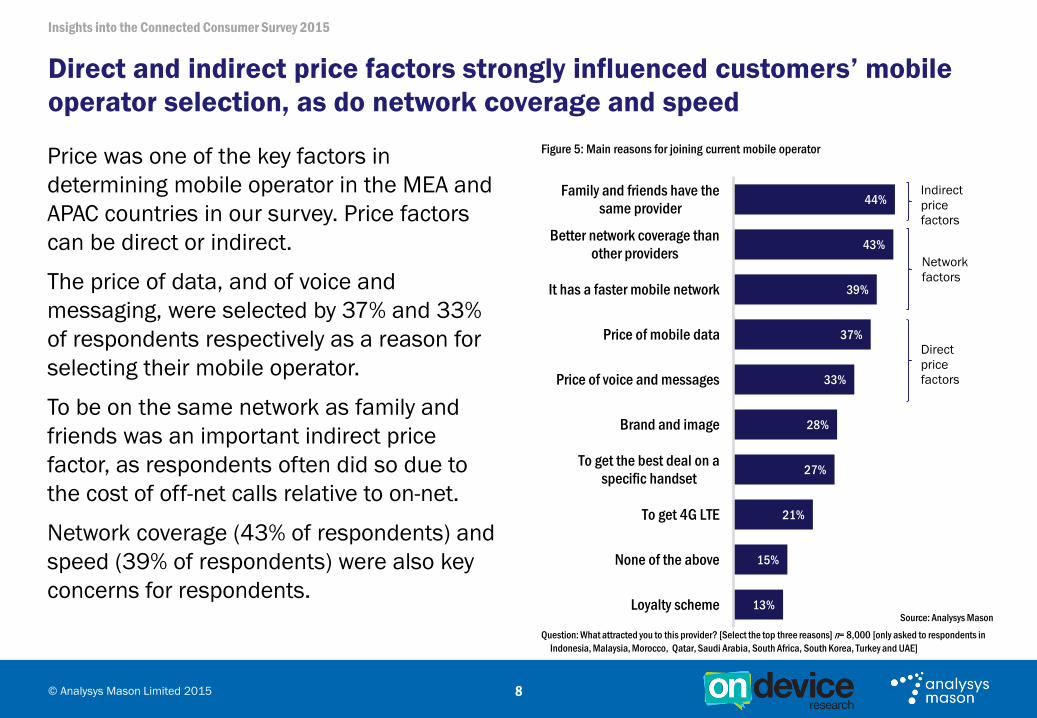

Figure 5: Main reasons for joining current mobile operator

8

Source: Analysys Mason

Question: What attracted you to this provider? [Select the top three reasons] n= 8,000 [only asked to respondents in

Indonesia, Malaysia, Morocco, Qatar, Saudi Arabia, South Africa, South Korea, Turkey and UAE]

Price was one of the key factors in

determining mobile operator in the MEA and

APAC countries in our survey. Price factors

can be direct or indirect.

The price of data, and of voice and

messaging, were selected by 37% and 33%

of respondents respectively as a reason for

selecting their mobile operator.

To be on the same network as family and

friends was an important indirect price

factor, as respondents often did so due to

the cost of off-net calls relative to on-net.

Network coverage (43% of respondents) and

speed (39% of respondents) were also key

concerns for respondents.

Direct and indirect price factors strongly influenced customers’ mobile

operator selection, as do network coverage and speed

13%

15%

21%

27%

28%

33%

37%

39%

43%

44%

Loyalty scheme

None of the above

To get 4G LTE

To get the best deal on a

specific handset

Brand and image

Price of voice and messages

Price of mobile data

It has a faster mobile network

Better network coverage than

other providers

Family and friends have the

same provider

Indirect

price

factors

Network

factors

Direct

price

factors

Insights into the Connected Consumer Survey 2015

© Analysys Mason Limited 2015

8%

9%

9%

10%

10%

11%

12%

13%

15%

15%

16%

17%

19%

20%

21%

Mobile Money SA (MTN)

MéditelCash

M-Pesa (Vodacom)

KT MoCa (KT)

eCash (Bank Mandiri)

M-Pesa (Vodafone)

Dompetku (Indosat)

AirCash (Celcom)

Paypin (SK Telecom)

M-Money (Maxis)

XL Tunai (XL Axiata)

MobiCash (Maroc Telecom)

Etisalat Mobile Commerce

T-Cash (Telkomsel)

Ooredoo Mobile Money

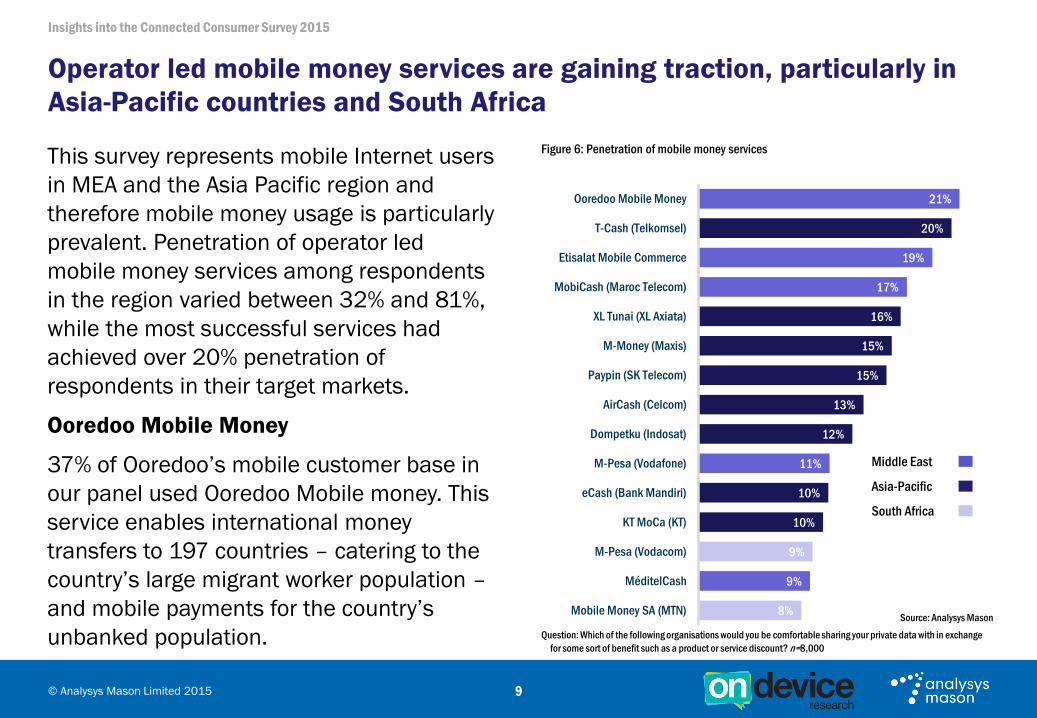

Figure 6: Penetration of mobile money services

9

Source: Analysys Mason

Question: Which of the following organisations would you be comfortable sharing your private data with in exchange

for some sort of benefit such as a product or service discount? n=8,000

This survey represents mobile Internet users

in MEA and the Asia Pacific region and

therefore mobile money usage is particularly

prevalent. Penetration of operator led

mobile money services among respondents

in the region varied between 32% and 81%,

while the most successful services had

achieved over 20% penetration of

respondents in their target markets.

Ooredoo Mobile Money

37% of Ooredoo’s mobile customer base in

our panel used Ooredoo Mobile money. This

service enables international money

transfers to 197 countries – catering to the

country’s large migrant worker population –

and mobile payments for the country’s

unbanked population.

Operator led mobile money services are gaining traction, particularly in

Asia-Pacific countries and South Africa

Middle East

Asia-Pacific

South Africa

Insights into the Connected Consumer Survey 2015

© Analysys Mason Limited 2015

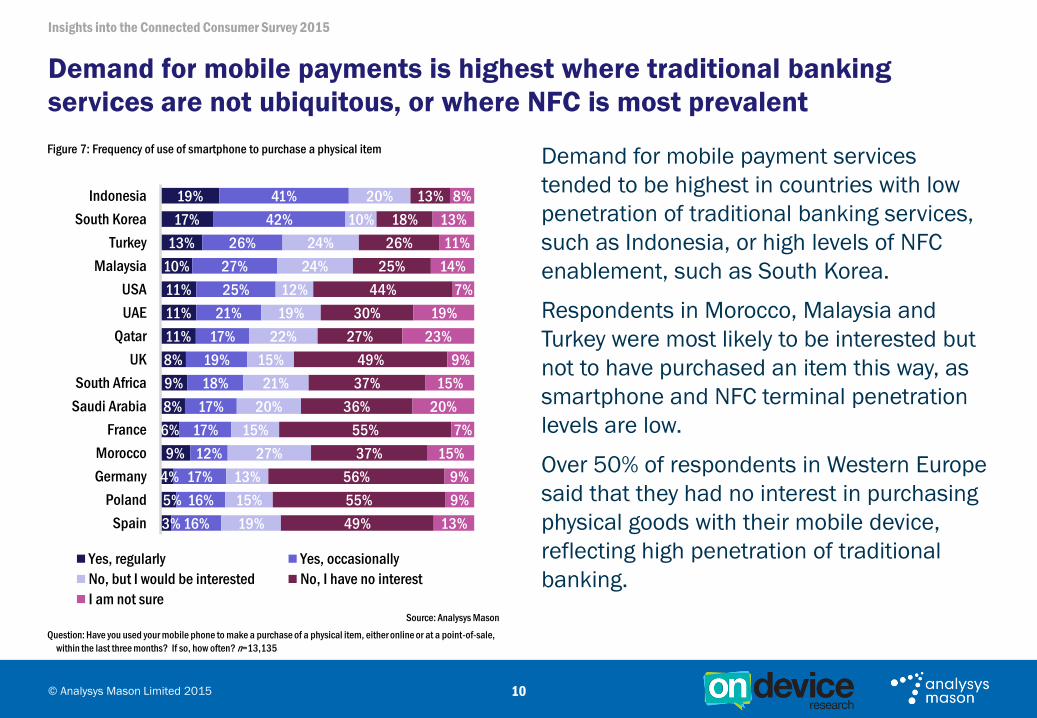

Figure 7: Frequency of use of smartphone to purchase a physical item

10

Source: Analysys Mason

Question: Have you used your mobile phone to make a purchase of a physical item, either online or at a point-of-sale,

within the last three months? If so, how often? n=13,135

Demand for mobile payment services

tended to be highest in countries with low

penetration of traditional banking services,

such as Indonesia, or high levels of NFC

enablement, such as South Korea.

Respondents in Morocco, Malaysia and

Turkey were most likely to be interested but

not to have purchased an item this way, as

smartphone and NFC terminal penetration

levels are low.

Over 50% of respondents in Western Europe

said that they had no interest in purchasing

physical goods with their mobile device,

reflecting high penetration of traditional

banking.

Demand for mobile payments is highest where traditional banking

services are not ubiquitous, or where NFC is most prevalent

3%

5%

4%

9%

6%

8%

9%

8%

11%

11%

11%

10%

13%

17%

19%

16%

16%

17%

12%

17%

17%

18%

19%

17%

21%

25%

27%

26%

42%

41%

19%

15%

13%

27%

15%

20%

21%

15%

22%

19%

12%

24%

24%

10%

20%

49%

55%

56%

37%

55%

36%

37%

49%

27%

30%

44%

25%

26%

18%

13%

13%

9%

9%

15%

7%

20%

15%

9%

23%

19%

7%

14%

11%

13%

8%

Spain

Poland

Germany

Morocco

France

Saudi Arabia

South Africa

UK

Qatar

UAE

USA

Malaysia

Turkey

South Korea

Indonesia

Yes, regularly Yes, occasionally

No, but I would be interested No, I have no interest

I am not sure

Insights into the Connected Consumer Survey 2015

© Analysys Mason Limited 2015

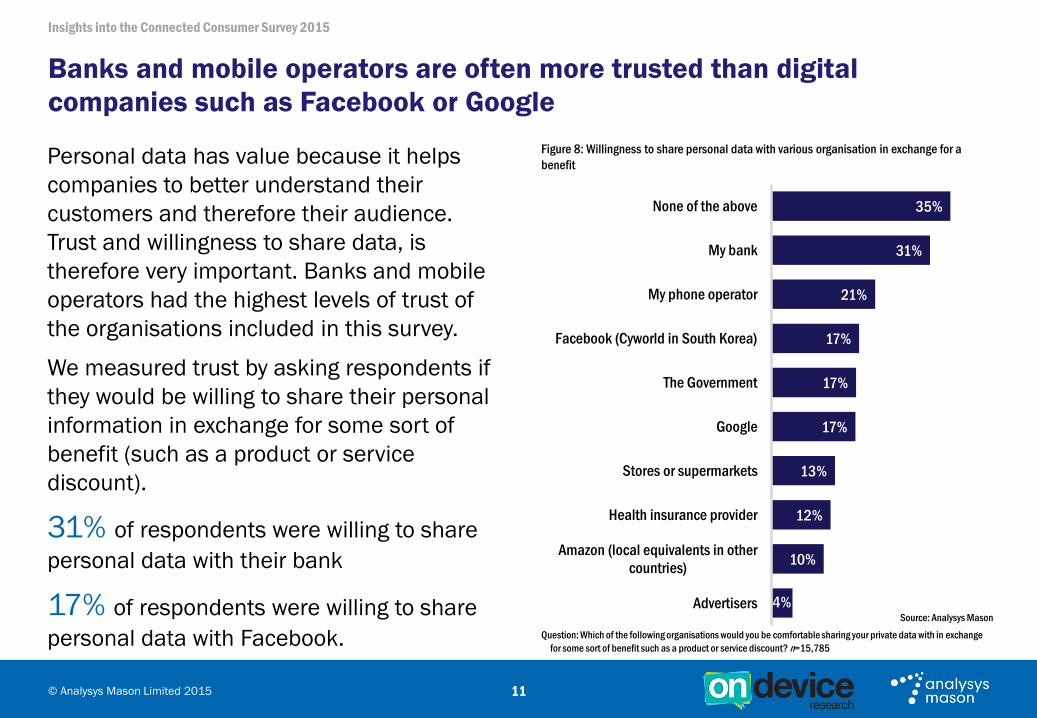

Figure 8: Willingness to share personal data with various organisation in exchange for a

benefit

11

Source: Analysys Mason

Question: Which of the following organisations would you be comfortable sharing your private data with in exchange

for some sort of benefit such as a product or service discount? n=15,785

Personal data has value because it helps

companies to better understand their

customers and therefore their audience.

Trust and willingness to share data, is

therefore very important. Banks and mobile

operators had the highest levels of trust of

the organisations included in this survey.

We measured trust by asking respondents if

they would be willing to share their personal

information in exchange for some sort of

benefit (such as a product or service

discount).

31% of respondents were willing to share

personal data with their bank

17% of respondents were willing to share

personal data with Facebook.

Banks and mobile operators are often more trusted than digital

companies such as Facebook or Google

4%

10%

12%

13%

17%

17%

17%

21%

31%

35%

Advertisers

Amazon (local equivalents in other

countries)

Health insurance provider

Stores or supermarkets

The Government

Facebook (Cyworld in South Korea)

My phone operator

My bank

None of the above

Insights into the Connected Consumer Survey 2015

© Analysys Mason Limited 2015

Published

The Connected Consumer Survey 2015. This report collates the ‘headline’ findings from the Connected Consumer Survey series, including the impact of factors on intention

to churn, customer retention strategies (with a focus on bundling strategies), and the impact of OTT communications and video streaming services on traditional mobile,

fixed-line and pay-TV businesses.

The Connected Consumer Survey 2015: mobile customer retention. This report provides insight into the attitudes and behaviours of mobile customers, including insight into the

drivers of churn, the impact of fixed-mobile convergent bundling, 4G and larger data allowances on customers’ intention to churn. This report also provides net promoter

scores (NPS) for major mobile operators in Europe and the USA.

The Connected Consumer Survey 2015: fixed broadband customer retention. This report addresses fixed broadband customers’ future intentions, and reasons for these, as well as

discussing strategies that AT&T, Iliad, Turkcell Superonline and Virgin Media have put in place to retain customers. We again address the impact of bundling on fixed

broadband customer retention, and analyse NPS for the major fixed broadband operators in each market.

The Connected Consumer Survey 2015: the Middle East and North Africa. In this report, we offer an insight into the of role of LTE to improve data monetisation prospects for

operators in the Middle East and North Africa, as well as OTT service and digital economy usage trends and the most critical levers for customer retention. We also

provide recommendations for operators as to how to address the OTT challenge, reduce churn and exploit opportunities in the digital economy.

Coming soon

The Connected Consumer Survey 2015: Pay-TV and OTT video services. Pay-TV operators have reached much of their addressable market, leaving little room for growth in

subscriber numbers. Meanwhile OTT video services are becoming increasingly popular and viewing habits are changing, as consumers view video content on multiple

devices.

The Connected Consumer Survey 2015: OTT communications services. OTT messaging and voice apps are widely adopted, and are disrupting mobile operators’ businesses.

Among respondents to our survey, OTT messaging apps have had the greatest impact, as they offer a differentiated user experience compared with SMS, while VoIP

apps have a less clear use case in most markets.

The Connected Consumer Survey 2015: Asia-Pacific . This report covers a diverse set of trends within consumer telecoms, focussing specifically on customer retention,

satisfaction, and drivers of churn; use of OTT communication services and consumer attitudes towards digital economy services such as mobile money and healthcare

specifically in the Asia-Pacific region.

The Connected Consumer Survey 2015: Digital economy services. This report will address consumer attitudes and behaviours with regard to digital economy services, specifically

mobile financial services (payments and commerce), mobile health and fitness, and smart homes.

12

Publications in the Connected Consumer Survey Series

Insights into the Connected Consumer Survey 2015

© Analysys Mason Limited 2015

About On Device Research

On Device Research is a global mobile sample and research technology

provider. Headquartered in London, UK, with offices in Dubai and

Singapore, the company pioneered the use of the mobile internet to gain

access to consumer opinion at any time or location.

Mobile research brings fresh, instant responses that accurately capture

consumer's feelings, thoughts and opinions, in a quick and cost effective

way. Working with the world’s largest market research agencies, fast

moving consumer goods companies, handset manufacturers and media

agencies, the company has conducted over 20 million surveys in 79

countries.

More info: www.ondeviceresearch.com

Contact: Ikram Mirza ([email protected])

Insights into the Connected Consumer Survey 2015

© Analysys Mason Limited 2015

Surveys work on

any internet

connected device

Insights into the Connected Consumer Survey 2015

© Analysys Mason Limited 2015 15

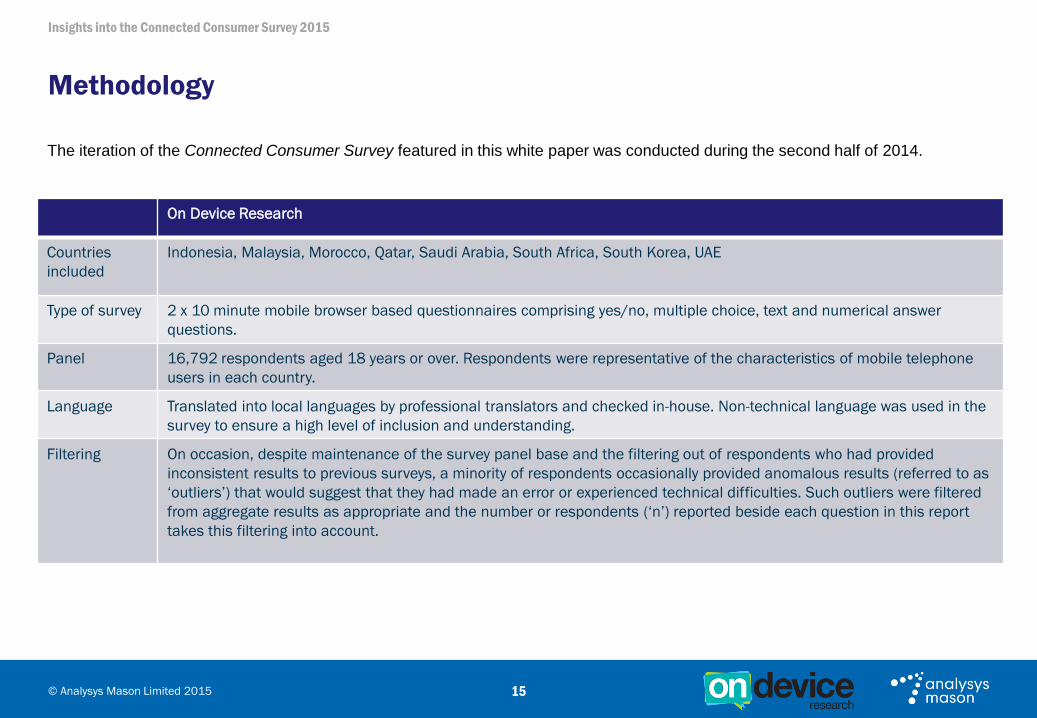

Methodology

The iteration of the Connected Consumer Survey featured in this white paper was conducted during the second half of 2014.

On Device Research

Countries

included

Indonesia, Malaysia, Morocco, Qatar, Saudi Arabia, South Africa, South Korea, UAE

Type of survey 2 x 10 minute mobile browser based questionnaires comprising yes/no, multiple choice, text and numerical answer

questions.

Panel 16,792 respondents aged 18 years or over. Respondents were representative of the characteristics of mobile telephone

users in each country.

Language Translated into local languages by professional translators and checked in-house. Non-technical language was used in the

survey to ensure a high level of inclusion and understanding.

Filtering On occasion, despite maintenance of the survey panel base and the filtering out of respondents who had provided

inconsistent results to previous surveys, a minority of respondents occasionally provided anomalous results (referred to as

‘outliers’) that would suggest that they had made an error or experienced technical difficulties. Such outliers were filtered

from aggregate results as appropriate and the number or respondents (‘n’) reported beside each question in this report

takes this filtering into account.

Insights into the Connected Consumer Survey 2015

© Analysys Mason Limited 2015 16

About the authors

Patrick Rusby (Analyst) is an analyst in Analysys Mason's Consumer Services research practice, focussing on mobile services markets,

MVNOs, LTE pricing, OTT communications services and fixed and mobile customer retention strategies. He contributes to the design, analysis

and write-up of the Analysys Mason's Connected Consumer Survey (a multi-year study of consumer behaviour relating to fixed and mobile

telecoms, TV and online services). He holds a Master’s degree in Contemporary British Politics from Goldsmiths College, University of London

and a Bachelor’s degree in Politics from the University of Southampton.

Martin Scott (Practice Head) leads Analysys Mason’s Consumer Services research practice, which includes the Fixed Broadband and Multi-

Play, Next-Generation Services, Mobile Services, Mobile Devices and Digital Economy research programmes. His primary areas of specialisation

include the bundling and pricing of multi-play services, including quadruple-play bundling, customer satisfaction and consumer-facing marketing

strategy. He also specialises in statistics, surveys and the analysis of primary research; he co-ordinates Analysys Mason's Connected Consumer

Survey and Consumer smartphone usage series of research.

Insights into the Connected Consumer Survey 2015

© Analysys Mason Limited 2015 17

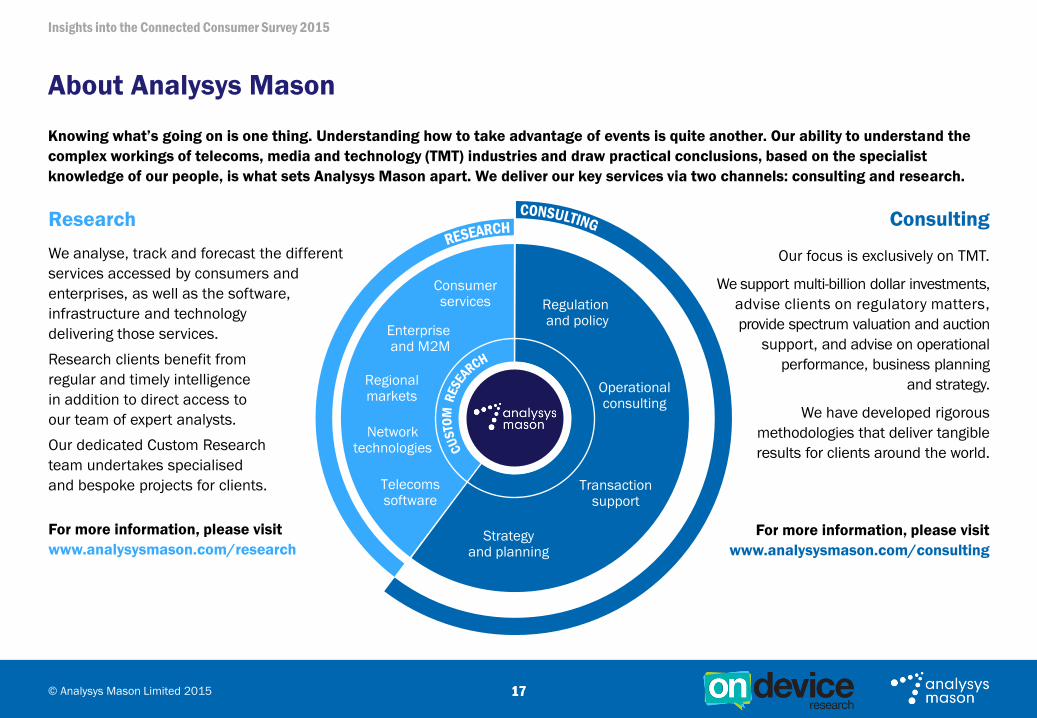

About Analysys Mason

Knowing what’s going on is one thing. Understanding how to take advantage of events is quite another. Our ability to understand the

complex workings of telecoms, media and technology (TMT) industries and draw practical conclusions, based on the specialist

knowledge of our people, is what sets Analysys Mason apart. We deliver our key services via two channels: consulting and research.

Consulting

Our focus is exclusively on TMT.

We support multi-billion dollar investments,

advise clients on regulatory matters,

provide spectrum valuation and auction

support, and advise on operational

performance, business planning

and strategy.

We have developed rigorous

methodologies that deliver tangible

results for clients around the world.

For more information, please visit

www.analysysmason.com/consulting

Research

We analyse, track and forecast the different

services accessed by consumers and

enterprises, as well as the software,

infrastructure and technology

delivering those services.

Research clients benefit from

regular and timely intelligence

in addition to direct access to

our team of expert analysts.

Our dedicated Custom Research

team undertakes specialised

and bespoke projects for clients.

For more information, please visit

www.analysysmason.com/research

17

Consumer services

Enterprise and M2M

Regional markets

Network technologies

Telecoms software

Strategy and planning

Transaction support

Operational consulting

Regulation and policy

Insights into the Connected Consumer Survey 2015

© Analysys Mason Limited 2015 18

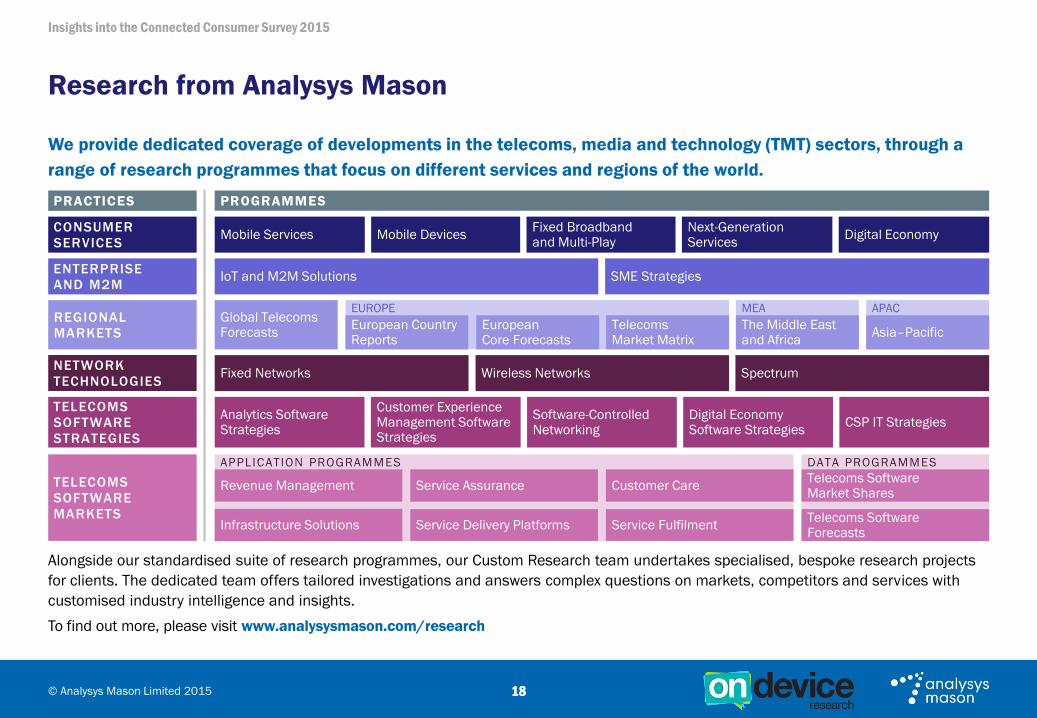

Research from Analysys Mason

We provide dedicated coverage of developments in the telecoms, media and technology (TMT) sectors, through a

range of research programmes that focus on different services and regions of the world.

Alongside our standardised suite of research programmes, our Custom Research team undertakes specialised, bespoke research projects

for clients. The dedicated team offers tailored investigations and answers complex questions on markets, competitors and services with

customised industry intelligence and insights.

To find out more, please visit www.analysysmason.com/research

18

NETWORK

TECHNOLOGIES

Spectrum Fixed Networks Wireless Networks

PRACTICES PROGRAMMES

CONSUMER

SERVICES

ENTERPRISE

AND M2M IoT and M2M Solutions SME Strategies

TELECOMS

SOFTWARE

STRATEGIES

DATA PROGRAMMES APPLICATION PROGRAMMES

Telecoms Software Forecasts

Service Assurance Telecoms Software Market Shares

Revenue Management

Infrastructure Solutions Service Fulfilment Service Delivery Platforms

Customer Care

MEA APAC REGIONAL

MARKETS

EUROPE

European Core Forecasts

Telecoms Market Matrix

European Country Reports

The Middle East and Africa

Asia–Pacific Global Telecoms Forecasts

TELECOMS

SOFTWARE

MARKETS

Customer Experience Management Software Strategies

Digital Economy Software Strategies

Analytics Software Strategies

Software-Controlled Networking

CSP IT Strategies

Mobile Services Mobile Devices Fixed Broadband and Multi-Play

Next-Generation Services

Digital Economy

Insights into the Connected Consumer Survey 2015

© Analysys Mason Limited 2015 19

Consulting from Analysys Mason

For more than 25 years, our consultants

have been bringing the benefits of applied

intelligence to enable clients around the world

to make the most of their opportunities.

Our clients in the telecoms, media and technology (TMT)

sectors operate in dynamic markets where change is

constant. We help shape their understanding of the

future so they can thrive in these demanding conditions.

To do that, we have developed rigorous methodologies

that deliver real results for clients around the world.

Our focus is exclusively on TMT. We advise clients on

regulatory matters, help shape spectrum policy and

develop spectrum strategy, support multi-billion dollar

investments, advise on operational performance and

develop new business strategies. Such projects result in

a depth of knowledge and a range of expertise that sets

us apart.

We help clients solve their most pressing problems,

enabling them to go farther, faster and achieve their

commercial objectives.

To find out more, please visit

www.analysysmason.com/consulting

19

AREA Research programmes

EXPERTISE

T R A N SA C T I O N SUP P O R T

R EG UL A T I O N

SP EC T R U M P O L I C Y A N D A UC T I O N SUP P O R T

O P ER A T I O N A L C O N SUL T I N G

ST R A T EG Y A N D P L A N N I N G

Technical due

diligence

Commercial due

diligence

Regulatory due

diligence

Net cost of universal service

Margin squeeze tests

Regulatory economic costing

Policy development

and response

Expert legal support Postal sector costing,

pricing and regulation Media regulation

Analysing regulatory

accounts

Radio spectrum auction support Radio spectrum management

Corporate value

analysis

Networks, procurement

and IT excellence

Transformation

services

Sales, customer and back-office

excellence

Innovation, product and pricing

portfolio excellence

Market analysis Market research

Market sizing

and forecasting

National and regional broadband strategy and implementation

Benchmarking

and best practice

Business strategy

and planning

Insights into the Connected Consumer Survey 2015

© Analysys Mason Limited 2015

Published by Analysys Mason Limited • Bush House • North West Wing • Aldwych • London • WC2B 4PJ • UK

Tel: +44 (0)20 7395 9000 • Fax: +44 (0)20 7395 9001 • Email: [email protected] • www.analysysmason.com/research • Registered in England No. 5177472

© Analysys Mason Limited 2015. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means – electronic,

mechanical, photocopying, recording or otherwise – without the prior written permission of the publisher.

Figures and projections contained in this report are based on publicly available information only and are produced by the Research Division of Analysys Mason Limited independently of any

client-specific work within Analysys Mason Limited. The opinions expressed are those of the stated authors only.

Analysys Mason Limited recognises that many terms appearing in this report are proprietary; all such trademarks are acknowledged and every effort has been made to indicate them by the

normal UK publishing practice of capitalisation. However, the presence of a term, in whatever form, does not affect its legal status as a trademark.

Analysys Mason Limited maintains that all reasonable care and skill have been used in the compilation of this publication. However, Analysys Mason Limited shall not be under any liability for

loss or damage (including consequential loss) whatsoever or howsoever arising as a result of the use of this publication by the customer, his servants, agents or any third party.

![Mobile and the Digital Economy [Analysys Mason, 2014]](https://img.pdfslide.net/doc/110x75/577cd0611a28ab9e78921a04/mobile-and-the-digital-economy-analysys-mason-2014.jpg)