Embed Size (px)

Citation preview

1

9th Australian Wind Energy

Conference

Craig Oakeshott

Director – Wholesale Markets Branch

Australian Energy Regulator

18 November 2013

Outlook for the National

Electricity Market

2

Outline - Outlook for the NEM

• Very Brief Background

• Factors impacting on wholesale market prices – Changes in electricity consumption patterns

• impact of high delivered electricity costs;

• efficiency improvements;

• solar; and

• economic growth.

• Intermittent nature of wind generation – Impacts on spot price volatility and existing thermal

generators

• Industry at a Crossroads

• NOTE these are my interpretations and not necessarily the official position of the AER

3

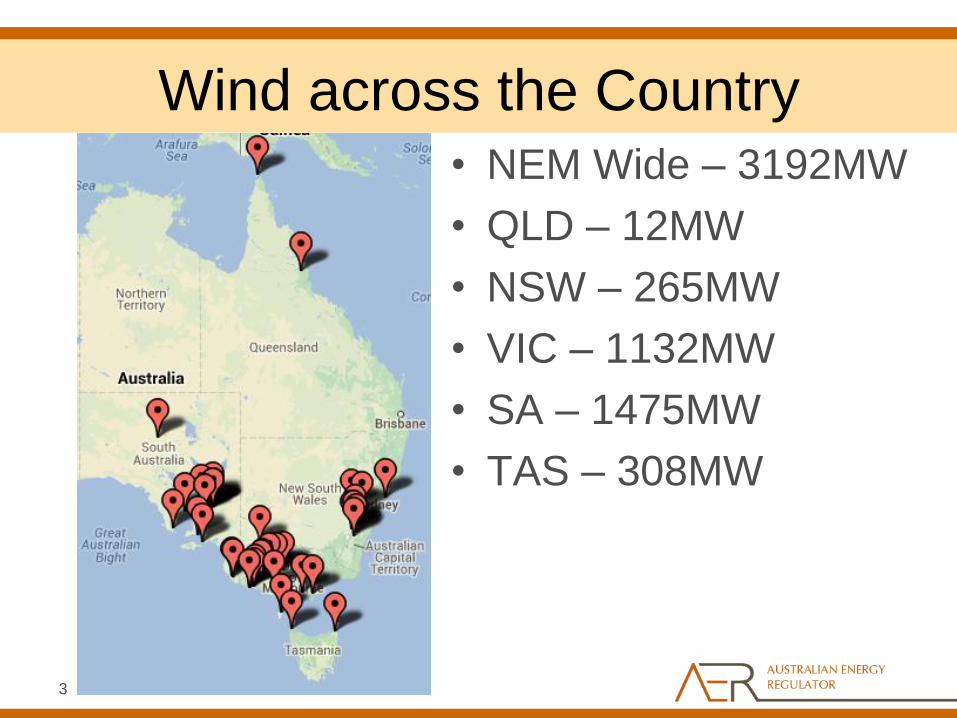

Wind across the Country • NEM Wide – 3192MW

• QLD – 12MW

• NSW – 265MW

• VIC – 1132MW

• SA – 1475MW

• TAS – 308MW

4

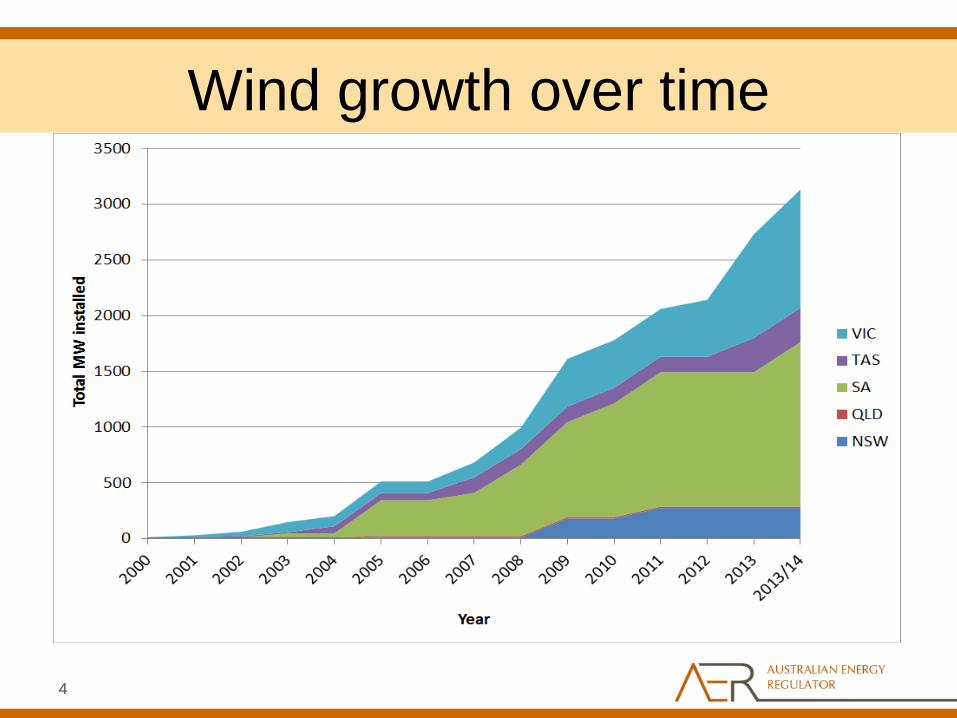

Wind growth over time

5

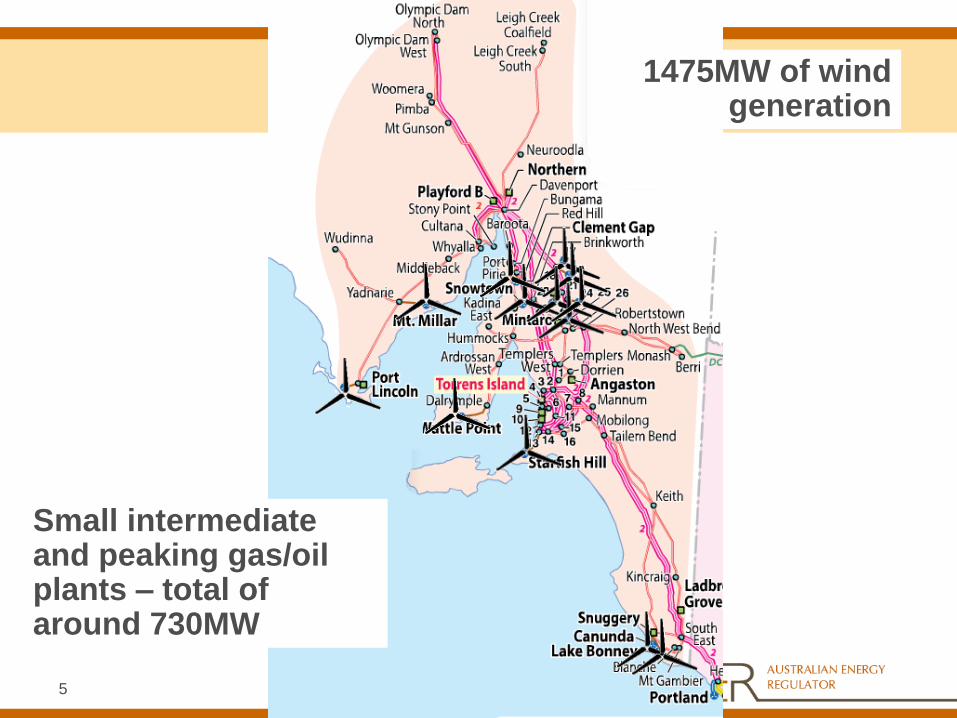

1475MW of wind generation

Small intermediate and peaking gas/oil plants – total of around 730MW

6

Factors impacting on

wholesale market prices

7

Demand

• Customer demand forecasts are flat in all states

– many other places in the world

• Delivered electricity prices have risen noticeably

• Causes are not actually black and white

– Economic conditions – some big customer failures

– High prices have encouraged domestic conservation

– Rooftop PV with FiTs • Eaten into the load profile

• But intermittent not firm

• But what about at a wholesale market level?

8

Market Prices

0

20

40

60

80

100

120

140

160

180

2003–04 2004–05 2005–06 2006–07 2007–08 2008-09 2009–10 2010-11 2011-12 2012-13

Co

un

t o

f n

eg

ativ

e p

ric

es

Qld NSW Vic SA

0

20

40

60

80

100

120

140

160

180

0-100 100-200 200-300 300-400 400-500 500-600 600-700 700-800 >800

Av

era

ge

Sp

ot

Pri

ce (

$M

Wh

)

Wind ouput (MW)

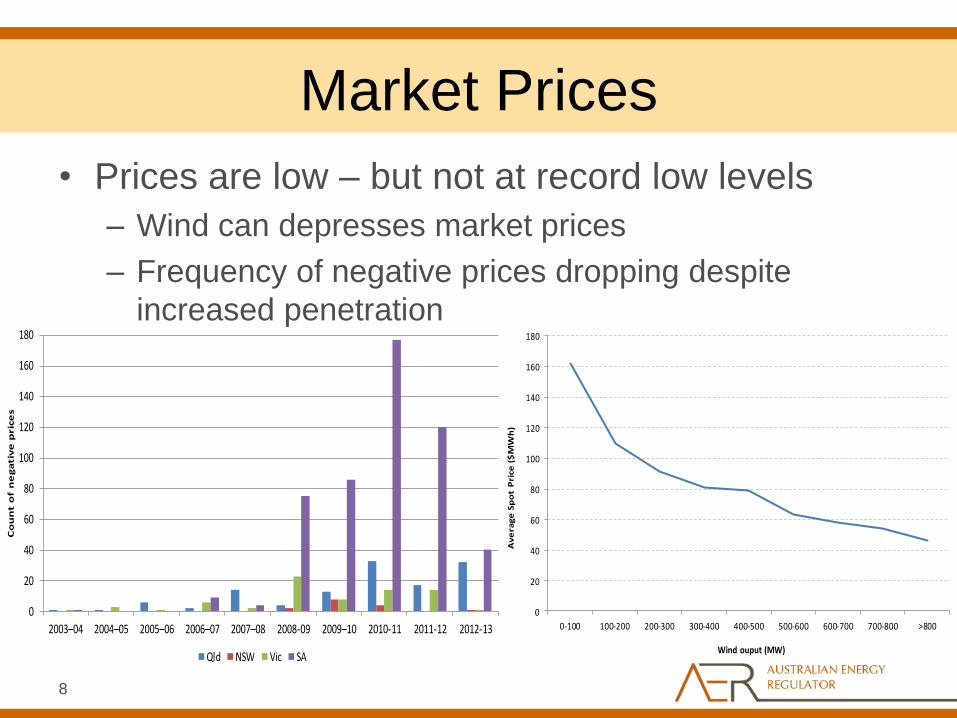

• Prices are low – but not at record low levels

– Wind can depresses market prices

– Frequency of negative prices dropping despite

increased penetration

9

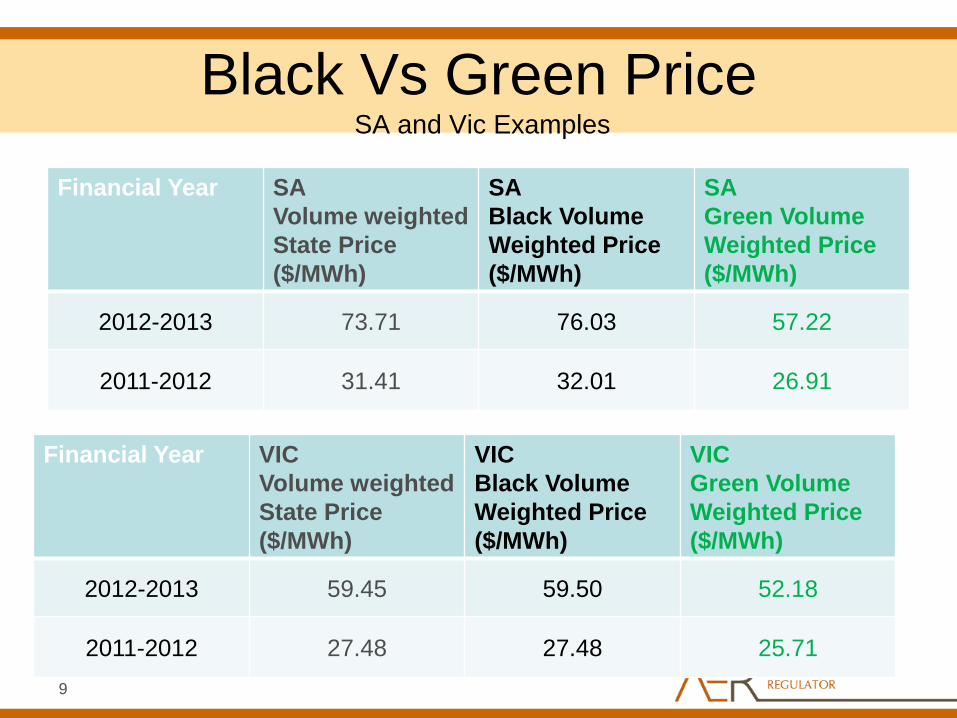

Black Vs Green Price SA and Vic Examples

Financial Year SA

Volume weighted

State Price

($/MWh)

SA

Black Volume

Weighted Price

($/MWh)

SA

Green Volume

Weighted Price

($/MWh)

2012-2013 73.71 76.03 57.22

2011-2012 31.41 32.01 26.91

Financial Year VIC

Volume weighted

State Price

($/MWh)

VIC

Black Volume

Weighted Price

($/MWh)

VIC

Green Volume

Weighted Price

($/MWh)

2012-2013 59.45 59.50 52.18

2011-2012 27.48 27.48 25.71

10

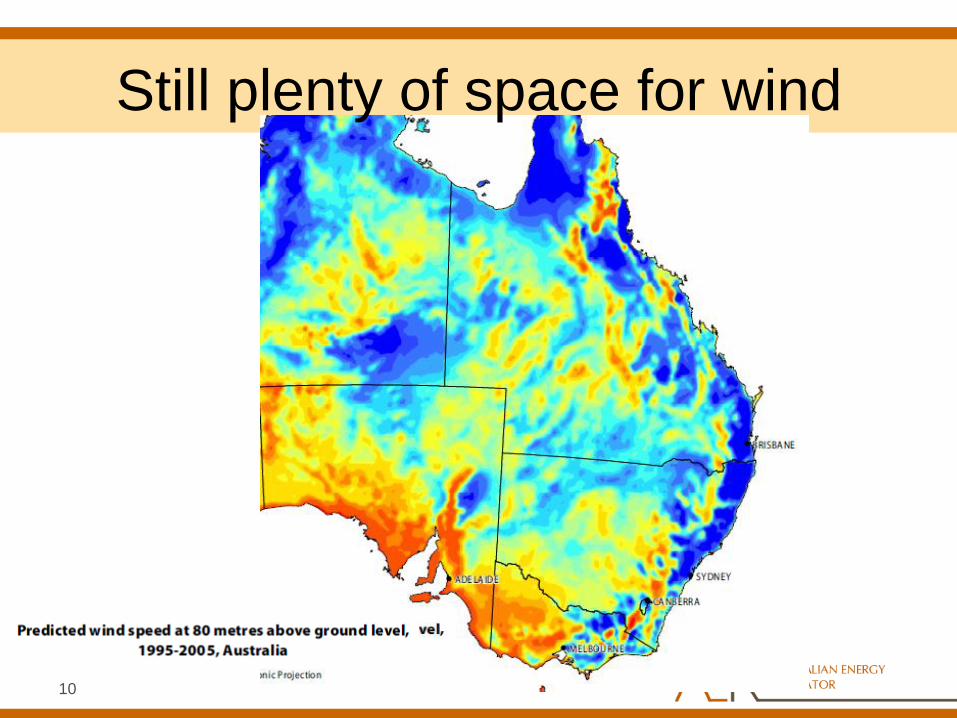

Still plenty of space for wind

11

Other factors affecting spot

prices • Transmission pricing and congestion

– ElectraNet outcome

– Connection and congestion is still an issue

– Market design is to deliver power to customers

– Affects all generators equally

• Uncertainty about 2014 RET review

• Short and long term future of Carbon

• New technologies advancing

• Potential future Gas price hikes

12

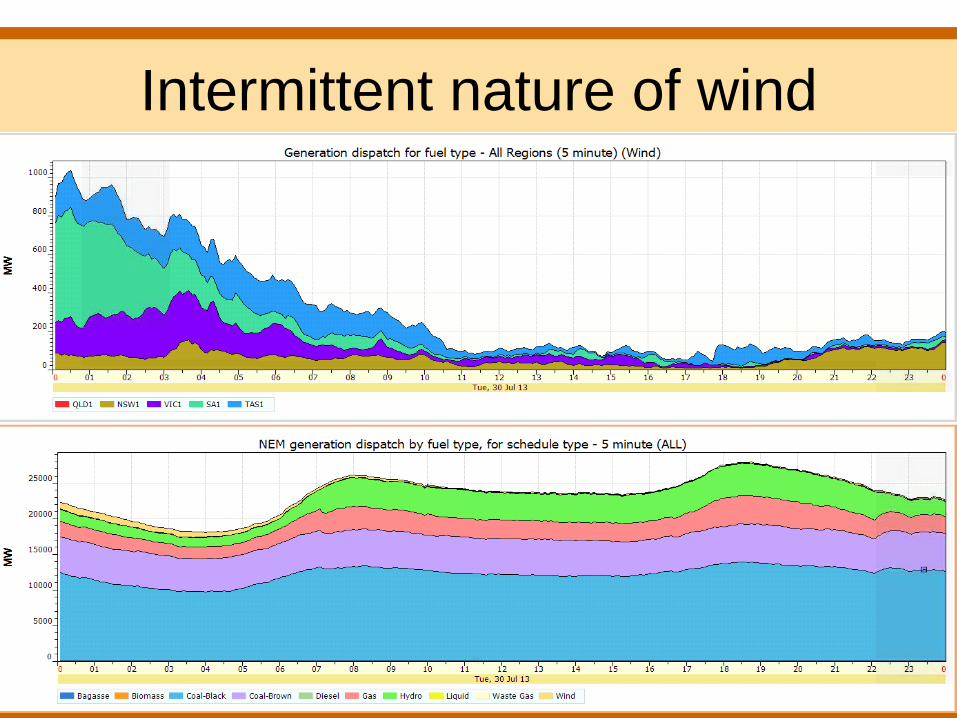

Intermittent nature of wind

13

Intermittent nature of wind

• Despite distribution of farms, output can be correlated.

• Worst case if wind drops as demand is increasing

• Output variability over short term and long term

• Longer term problem is– AEMO’s

• Shorter term may be Wind farms – causer pays FCAS

• Low and negative prices

14

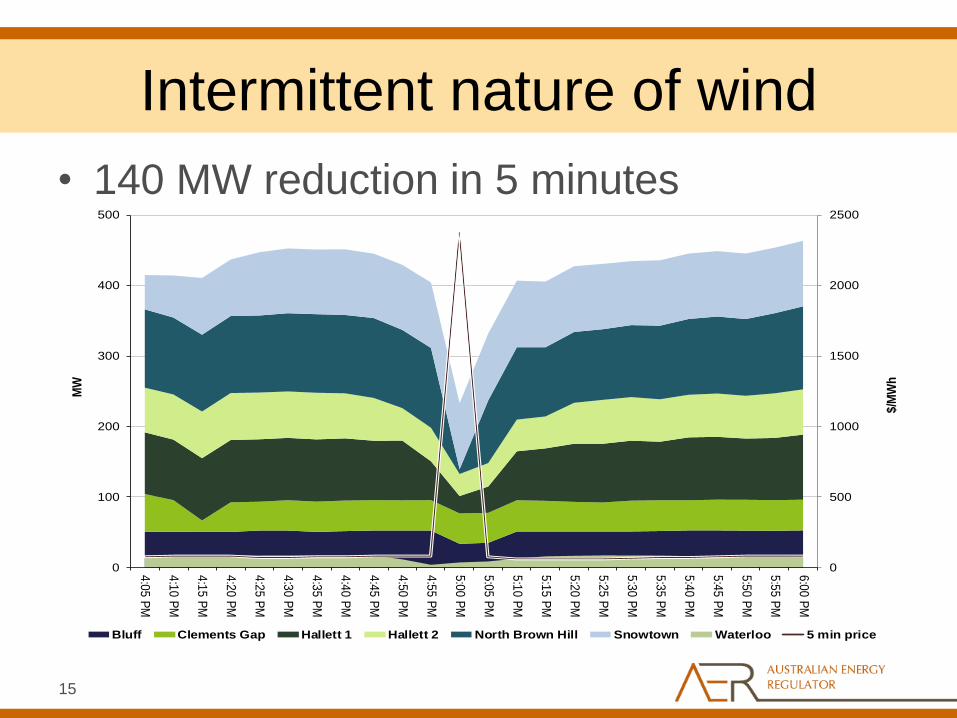

Intermittent nature of wind

15

0

500

1000

1500

2000

2500

0

100

200

300

400

500

4:0

5 P

M

4:1

0 P

M

4:1

5 P

M

4:2

0 P

M

4:2

5 P

M

4:3

0 P

M

4:3

5 P

M

4:4

0 P

M

4:4

5 P

M

4:5

0 P

M

4:5

5 P

M

5:0

0 P

M

5:0

5 P

M

5:1

0 P

M

5:1

5 P

M

5:2

0 P

M

5:2

5 P

M

5:3

0 P

M

5:3

5 P

M

5:4

0 P

M

5:4

5 P

M

5:5

0 P

M

5:5

5 P

M

6:0

0 P

M

$/M

Wh

MW

Bluff Clements Gap Hallett 1 Hallett 2 North Brown Hill Snowtown Waterloo 5 min price

Intermittent nature of wind

• 140 MW reduction in 5 minutes

16

With whom is wind competing

• Wind offers at the bottom of the bid stack

– Normally a price taker not a price setter

– Amongst the other “determined to stay on”

generators

• So as wind increase what changed ?

17

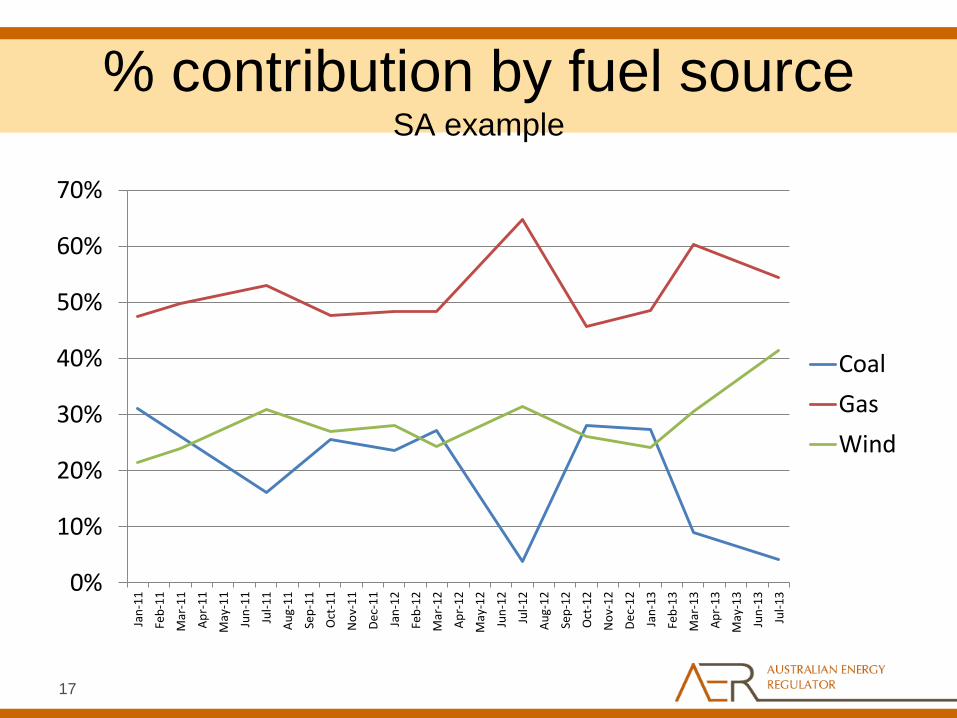

% contribution by fuel source SA example

0%

10%

20%

30%

40%

50%

60%

70%

Jan

-11

Feb

-11

Mar

-11

Ap

r-1

1

May

-11

Jun

-11

Jul-

11

Au

g-1

1

Sep

-11

Oct

-11

No

v-1

1

De

c-1

1

Jan

-12

Feb

-12

Mar

-12

Ap

r-1

2

May

-12

Jun

-12

Jul-

12

Au

g-1

2

Sep

-12

Oct

-12

No

v-1

2

De

c-1

2

Jan

-13

Feb

-13

Mar

-13

Ap

r-1

3

May

-13

Jun

-13

Jul-

13

Coal

Gas

Wind

18

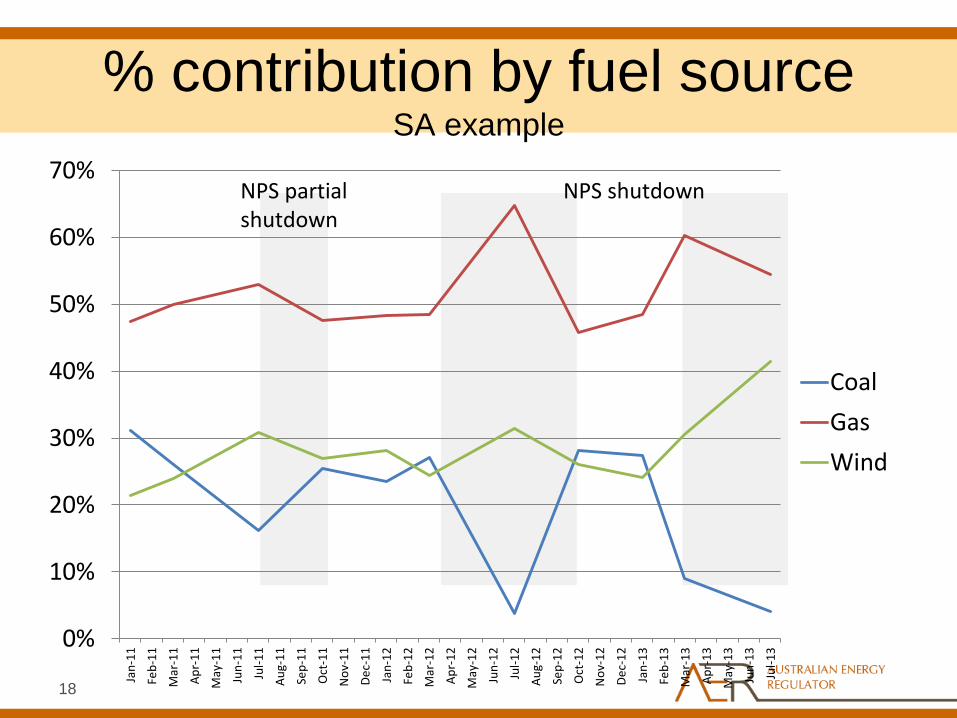

% contribution by fuel source SA example

0%

10%

20%

30%

40%

50%

60%

70%

Jan

-11

Feb

-11

Mar

-11

Ap

r-1

1

May

-11

Jun

-11

Jul-

11

Au

g-1

1

Sep

-11

Oct

-11

No

v-1

1

De

c-1

1

Jan

-12

Feb

-12

Mar

-12

Ap

r-1

2

May

-12

Jun

-12

Jul-

12

Au

g-1

2

Sep

-12

Oct

-12

No

v-1

2

De

c-1

2

Jan

-13

Feb

-13

Mar

-13

Ap

r-1

3

May

-13

Jun

-13

Jul-

13

Coal

Gas

Wind

NPS shutdown NPS partial shutdown

19

Industry at a Cross Roads

• SO Where to from here?

20

Industry at a Cross Roads

• Lean.….

21

Industry at a Cross Roads

• Lean.….Green

22

Industry at a Cross Roads

• Lean.….Green…..Gas Dream

23

Industry at a Cross Roads

• Lean.….Green…..Gas Dream…..Storage

24

So many factors to consider

• Challenges OR Opportunities – Changes to consumption patterns

• Greater Energy efficiency and Home automation

• Electric vehicles

– Technology • When is the technology available and where will it be built

• Energy transport - pipelines v transmission lines

• Higher efficiency fossil fuels

• Renewable intermittent generation – Wind in a different market role

– More rooftop solar PV eroding demand

– Solar thermal

– Fuel switching and international pricing

– Energy Storage • Distributed and/or Central

25

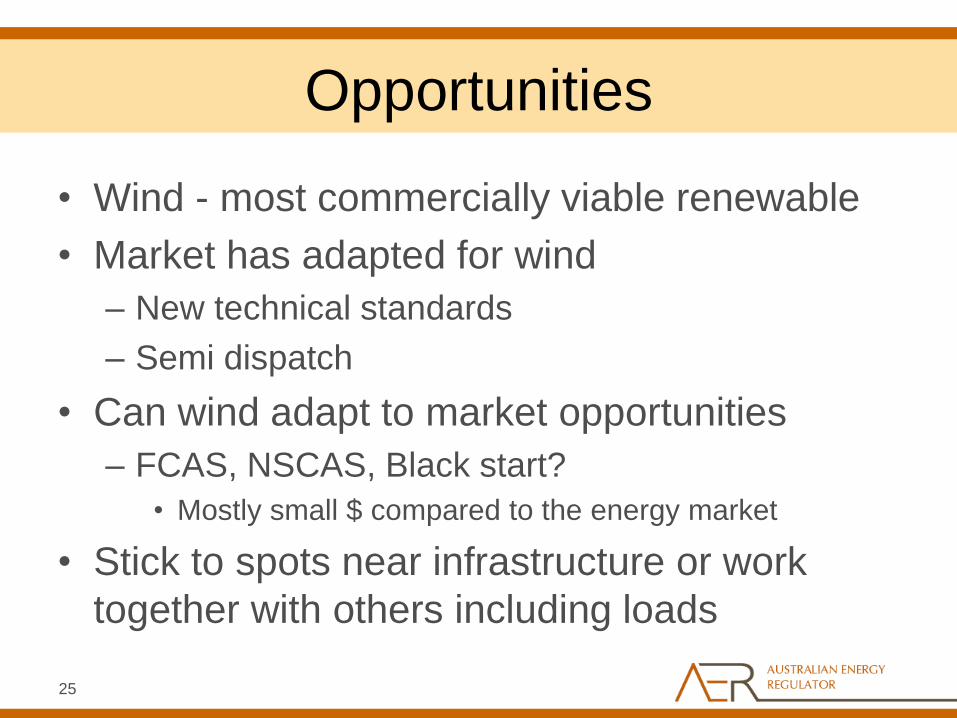

Opportunities

• Wind - most commercially viable renewable

• Market has adapted for wind

– New technical standards

– Semi dispatch

• Can wind adapt to market opportunities

– FCAS, NSCAS, Black start?

• Mostly small $ compared to the energy market

• Stick to spots near infrastructure or work

together with others including loads

26

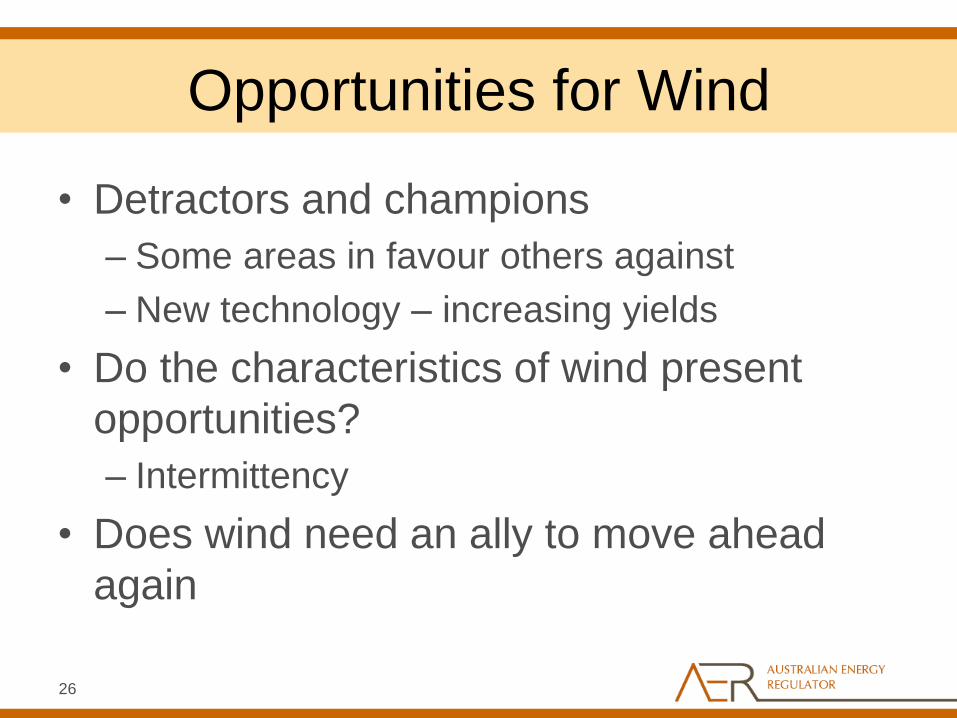

Opportunities for Wind

• Detractors and champions

– Some areas in favour others against

– New technology – increasing yields

• Do the characteristics of wind present

opportunities?

– Intermittency

• Does wind need an ally to move ahead

again

27

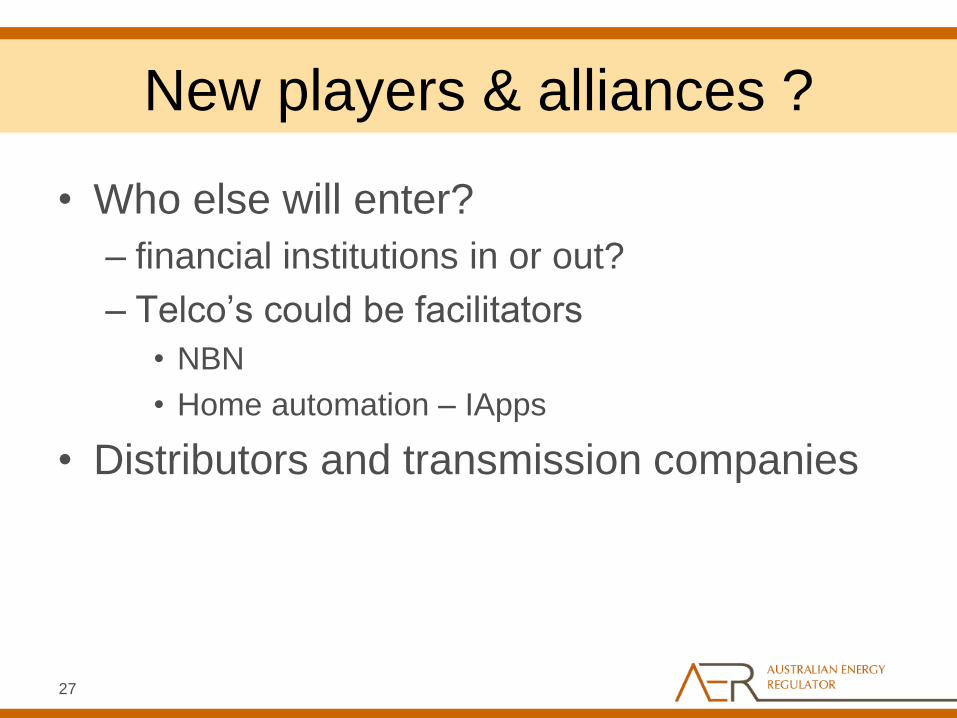

New players & alliances ?

• Who else will enter?

– financial institutions in or out?

– Telco’s could be facilitators

• NBN

• Home automation – IApps

• Distributors and transmission companies

28

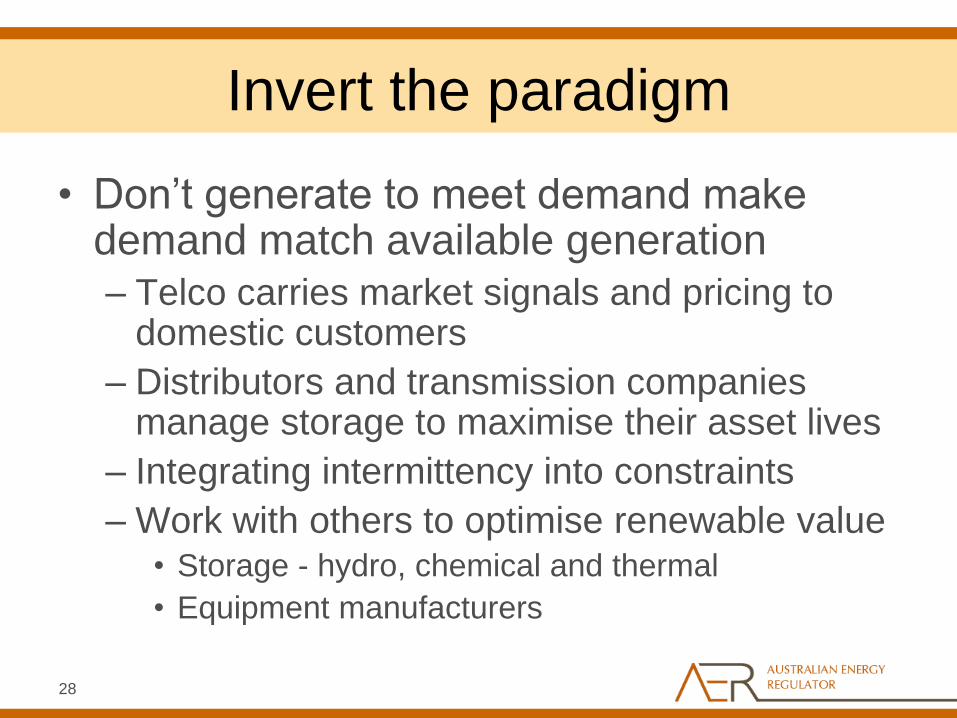

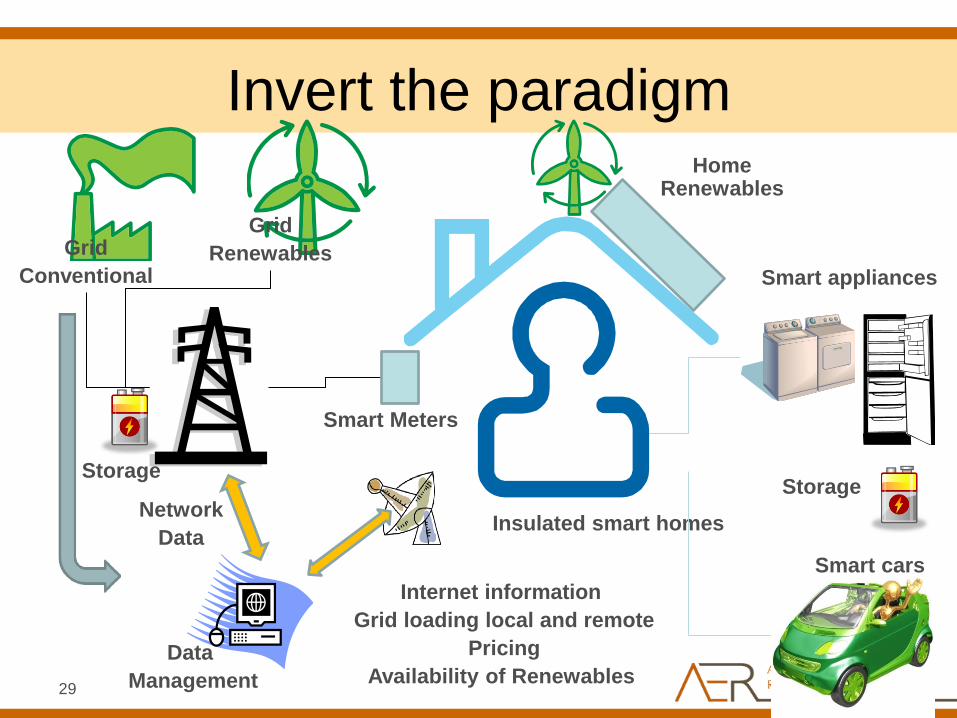

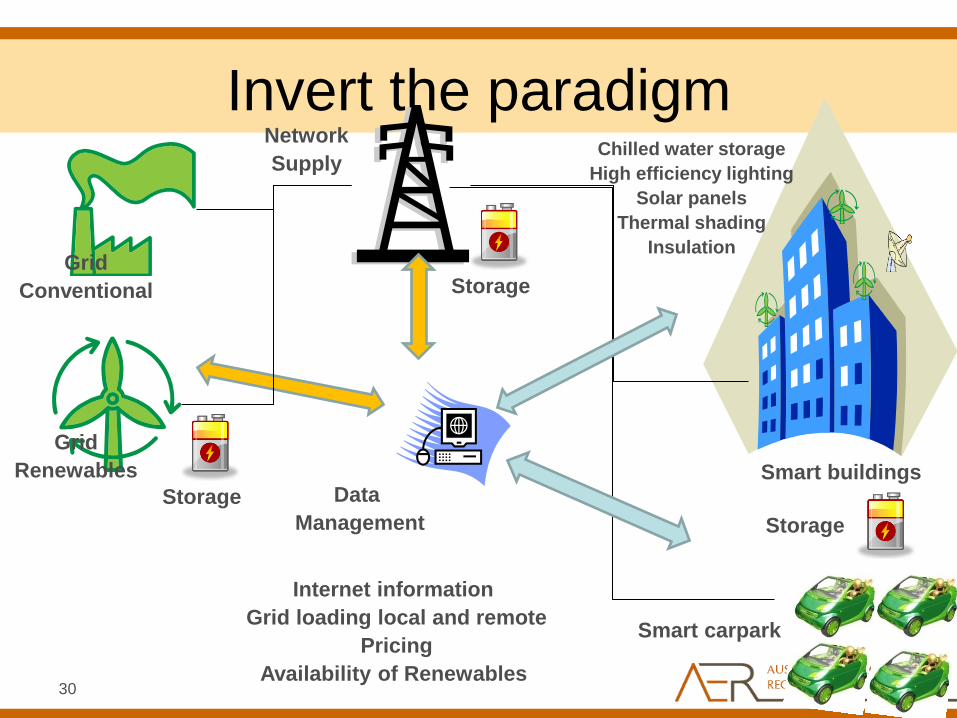

Invert the paradigm

• Don’t generate to meet demand make demand match available generation

– Telco carries market signals and pricing to domestic customers

– Distributors and transmission companies manage storage to maximise their asset lives

– Integrating intermittency into constraints

– Work with others to optimise renewable value • Storage - hydro, chemical and thermal

• Equipment manufacturers

29

Invert the paradigm

Smart appliances

Smart cars

Network

Data

Home Renewables

Insulated smart homes

Smart Meters

Data

Management

Grid

Renewables Grid

Conventional

Internet information

Grid loading local and remote

Pricing

Availability of Renewables

Storage Storage

30

Invert the paradigm

Smart carpark

Network

Supply

Data

Management

Grid

Renewables

Grid

Conventional

Internet information

Grid loading local and remote

Pricing

Availability of Renewables

Smart buildings

Chilled water storage

High efficiency lighting

Solar panels

Thermal shading

Insulation

Storage

Storage

Storage

31

Thank You

![[Terry Nardin] the Philosophy of Michael Oakeshott(Bookos.org)](https://img.pdfslide.net/doc/110x75/5460c5f8b1af9f04598b55d2/terry-nardin-the-philosophy-of-michael-oakeshottbookosorg.jpg)

![[Scherma] - Ewart Oakeshott - Sword in the Age of Chivalry](https://img.pdfslide.net/doc/110x75/55cf9bf4550346d033a800d4/scherma-ewart-oakeshott-sword-in-the-age-of-chivalry.jpg)

![Ser Conservador [Michael Oakeshott]](https://img.pdfslide.net/doc/110x75/568bd9701a28ab2034a711aa/ser-conservador-michael-oakeshott.jpg)

![INGLES- OAKESHOTT Hobbes on Civil Association [1975].pdf](https://img.pdfslide.net/doc/110x75/577cdadc1a28ab9e78a6ba63/ingles-oakeshott-hobbes-on-civil-association-1975pdf.jpg)