Embed Size (px)

Citation preview

– 1 –We make ICT strategies work

Tim Dörflinger, Detecon International GmbH, South AfricaIAD Summit 2015, Victoria Falls, Zimbabwe

15.04.2015

“Telco and OTT partnerships – the way ahead in a changing industry?”

– 2 –

4/14

/201

5© D

etec

on

Our lives are constantly reshaped by innovation, in the Telco sector the trend

setters are now the OTT players

Introduction: The drivers for fixed and mobile data growth

Innovation in the field of ICT products and services is significantly changing human communication behavior and drives data usage on both fixed and mobile networks.

© D

etec

on

– 3 –

The drivers for fixed and mobile data growth Selected quantified global data drivers

+4%

2019

8.506

1.782

4.383

2.341

2013

6.657

4.531

1.919207

<3G3G4G / LTE

+1.029%

+128%

-69%

Mobile Subscribers (in Million)

97 341

159

2019

365

25

+6%

2013

256

Regular TVsSmart TVs

TV Device Sales (in Million)

+721%

-86%

Source: IC Intelligence Centre (2013) - TV Devices ForecastsSource: Ovum (2014) - Mobile Subscription and Revenue ForecastSource: Ovum (2013) - Global Cellular M2M ConnectionsSource: Strategy Analytics (2013) - VoLTE, OTT Voice & Video Call Forecasts

494

199

2013 2019

+16%

M2M Connections (in Million)

+% Compound Annual Growth Rate (CAGR)

185

2013 2019

1.636

+44%

Active Videocall* Accounts (in Million)

* e.g. Skype and Facetime

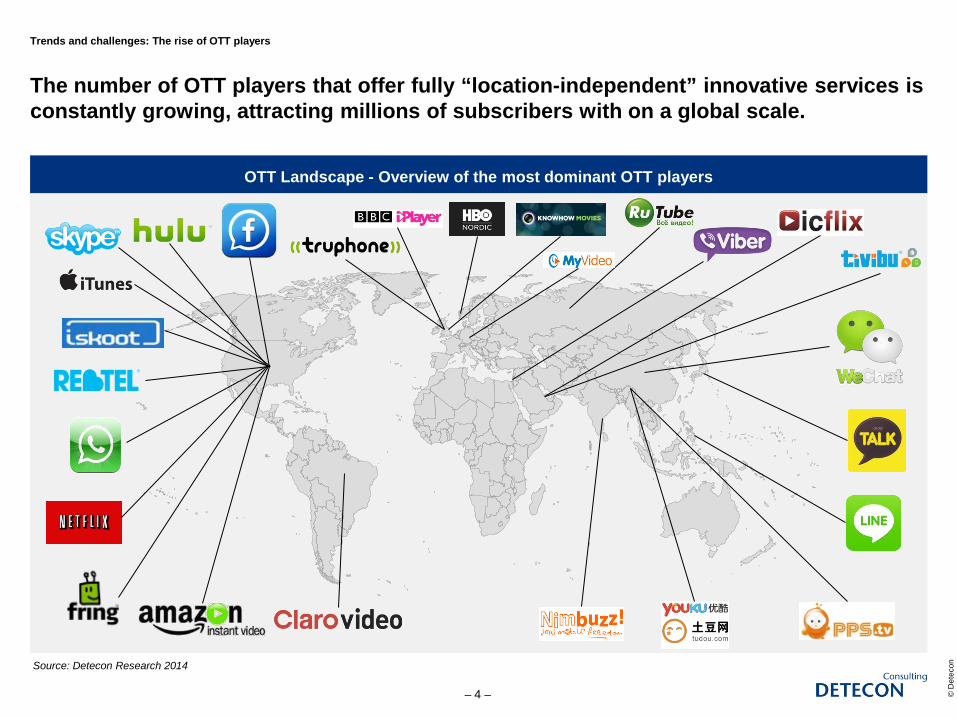

Trends and challenges: The rise of OTT players

The number of OTT players that offer fully “location-independent” innovative services is constantly growing, attracting millions of subscribers with on a global scale.

© D

etec

on

– 4 –

OTT Landscape - Overview of the most dominant OTT players

Source: Detecon Research 2014

Regulatory Challenge: Deregulation of Telcos vs. Regulation of OTTs?

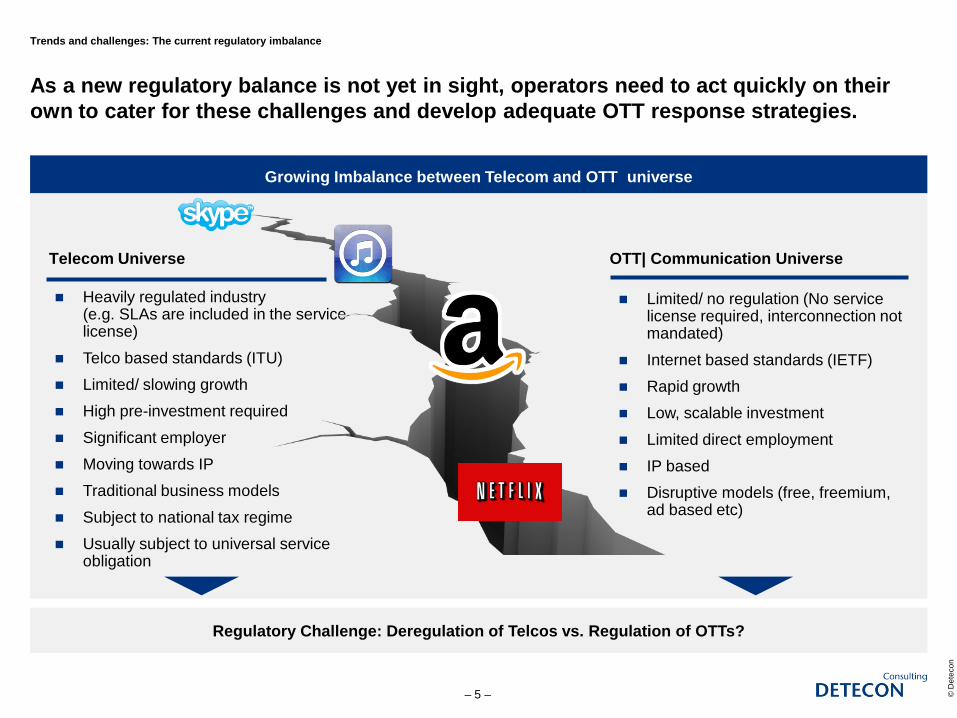

Trends and challenges: The current regulatory imbalance

As a new regulatory balance is not yet in sight, operators need to act quickly on their own to cater for these challenges and develop adequate OTT response strategies.

© D

etec

on

– 5 –

Growing Imbalance between Telecom and OTT universe

Limited/ no regulation (No service license required, interconnection not mandated)

Internet based standards (IETF) Rapid growth Low, scalable investment

Limited direct employment IP based Disruptive models (free, freemium,

ad based etc)

OTT| Communication Universe

Heavily regulated industry (e.g. SLAs are included in the service license)

Telco based standards (ITU) Limited/ slowing growth High pre-investment required

Significant employer Moving towards IP Traditional business models

Subject to national tax regime Usually subject to universal service

obligation

Telecom Universe

– 6 –

4/14

/201

5© D

etec

on

Operators find themselves at a cross roads and need to take a strategic decision…

Trends and challenges: Operators at the crossroads

Operators need to carefully decide how to deal with OTT players as their different types of business models may determine the sustainable future of operators business.

© D

etec

on

– 7 –

OTTs’ business models develop at a fast pace and change the traditional revenue split

Advertisement is the main revenue source of many OTTs.

Paid subscriptions start to work for larger customer base OTTs

Fremium apps have thrived as a innovative monetization strategy

Cloud storage as an add-on service has ramped profitability

Business Intelligence is the most powerful tool of content distributors

Best-effort free services cannibalize traditional revenues

Flexibility and innovation are the only way operators can monetize on future opportunities

Operators face a crossroad regarding OTT impact on their business OTT Business Models

Service deployment over time

Prof

itabi

lity

leve

l ove

r tim

e

OTT Business Model Refinement & Maturity

Strategic decisionneeded

OTT Perspective Operator Perspective

Voice and Messaging

High Bandwidth Video

– 8 –

4/14

/201

5© D

etec

on

What can operators do about it?

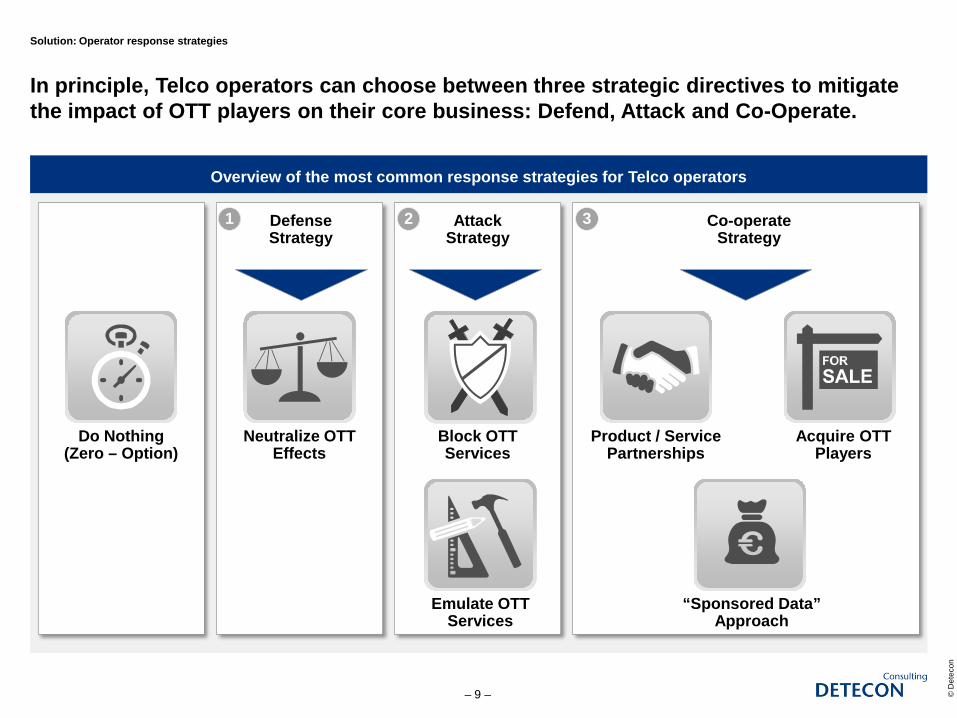

Solution: Operator response strategies

In principle, Telco operators can choose between three strategic directives to mitigate the impact of OTT players on their core business: Defend, Attack and Co-Operate.

© D

etec

on

– 9 –

Overview of the most common response strategies for Telco operators

Product / Service Partnerships

Block OTT Services

Neutralize OTT Effects

Do Nothing (Zero – Option)

1 Defense Strategy

Attack Strategy

Emulate OTT Services

Co-operate Strategy

Acquire OTT Players

“Sponsored Data” Approach

2 3

– 10 –

4/14

/201

5© D

etec

on

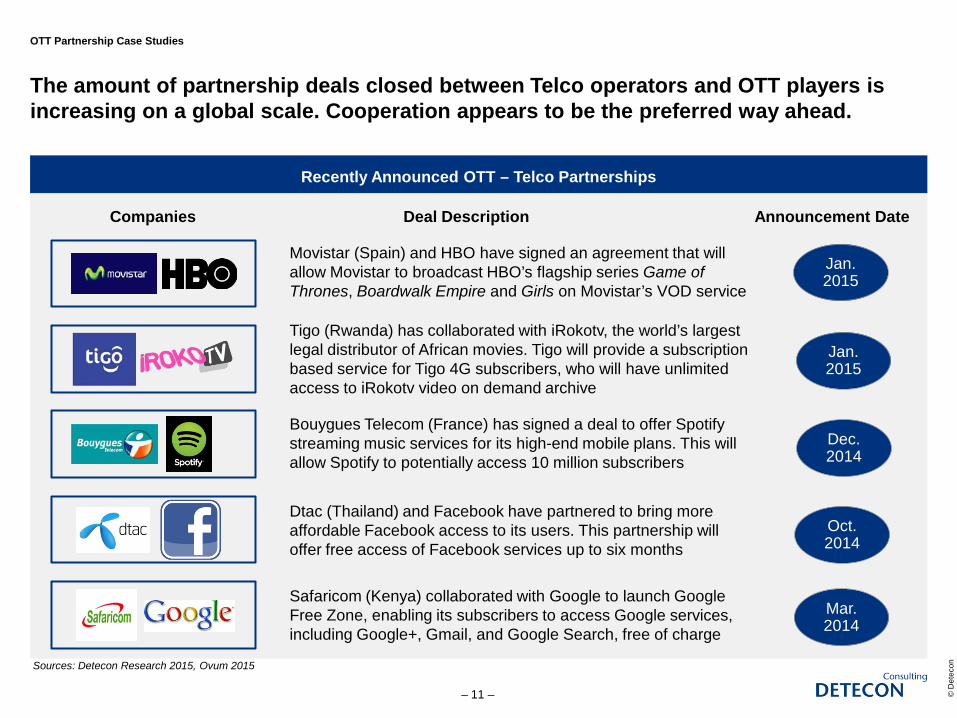

OTT Partnership Case Studies

Recently Announced OTT – Telco Partnerships

The amount of partnership deals closed between Telco operators and OTT players is increasing on a global scale. Cooperation appears to be the preferred way ahead.

© D

etec

on

OTT Partnership Case Studies

– 11 –

Movistar (Spain) and HBO have signed an agreement that will allow Movistar to broadcast HBO’s flagship series Game of Thrones, Boardwalk Empire and Girls on Movistar’s VOD service

Jan.2015

Companies Deal Description Announcement Date

Jan. 2015

Bouygues Telecom (France) has signed a deal to offer Spotifystreaming music services for its high-end mobile plans. This will allow Spotify to potentially access 10 million subscribers

Dec. 2014

Tigo (Rwanda) has collaborated with iRokotv, the world’s largest legal distributor of African movies. Tigo will provide a subscription based service for Tigo 4G subscribers, who will have unlimited access to iRokotv video on demand archive

Dtac (Thailand) and Facebook have partnered to bring more affordable Facebook access to its users. This partnership will offer free access of Facebook services up to six months

Oct. 2014

Safaricom (Kenya) collaborated with Google to launch Google Free Zone, enabling its subscribers to access Google services, including Google+, Gmail, and Google Search, free of charge

Mar. 2014

Sources: Detecon Research 2015, Ovum 2015

Airtel Nigeria and WhatsApp

Partnership between OTT messaging player WhatsApp and Airtel Nigeria

Exclusive WhatsApp-branded mobile data plan from Airtel to compensate SMS revenue loss and increase brand perception

The partnership has been extended regionally to other AirtelMarkets (e.g. India) and to include other OTT platforms such as Twitter and Facebook

OTT Messaging Monetization

Nigeria

Affordable Access through OTTs

Internet.Org & Google “Loon”

OTT players such as Facebook or Google investigate “affordable internet access” solutions

Internet.Org is a partnership between Facebook and mobile operators to deliver access to basic internet services for free

Google is investigating commercially viable ways to provide internet access to remote areas using high-altitude balloons

Google Freezone provides access to Google services free of charge

Selected Case Studies: Overview

The following case studies were chosen to discuss different types of Telco & OTT partnerships, both from a regional as well as an OTT offering perspective.

© D

etec

on

– 12 –

OTT Video, Gaming, Music

MTN creates the content platform MTN Play to reduce usage of OTT content and increase brand perception

Subscribers get mobile access to content such as games, news wallpapers, ringtones, music, and videos

MTN Play is now available to MTN subscribers in 22 Markets in Africa and the Middle East

Integration of Simfy Music Streaming into MTN Play portfolio

Video, Gaming, Music Monetization

South Africa

We make ICT strategies work

Thank you for your attention!

Questions, comments and discussion?

Dr. Christoph SchetelichManaging Partner / VP Southern Africa

Detecon International GmbHBuilding 27, Woodlands Office Park,Woodmead 2191, South AfricaMobile: +27 84 777 9710e-Mail: [email protected]

Your Contact Persons

© D

etec

on

– 14 –

In case you have any questions or would like to initiate further discussions, please contact our topic experts at Detecon’s regional office in Johannesburg, South Africa.

Dr. Steffen OehlerManaging Partner

Detecon International GmbHBuilding 27, Woodlands Office Park,Woodmead 2191, South AfricaMobile: +27 82 654 1751Email: [email protected]

Tim DörflingerManaging ConsultantDetecon International GmbHBuilding 27, Woodlands Office Park,Woodmead 2191, South AfricaMobile: +27 82 321 6730 Email: Tim.Dö[email protected]