Embed Size (px)

Citation preview

A CEB Sponsored Webinar by Misys

Digital Corporate Banking for the Connected

Corporate Customer

TODAY’S SPEAKERS

© 2016 CEB. All rights reserved.

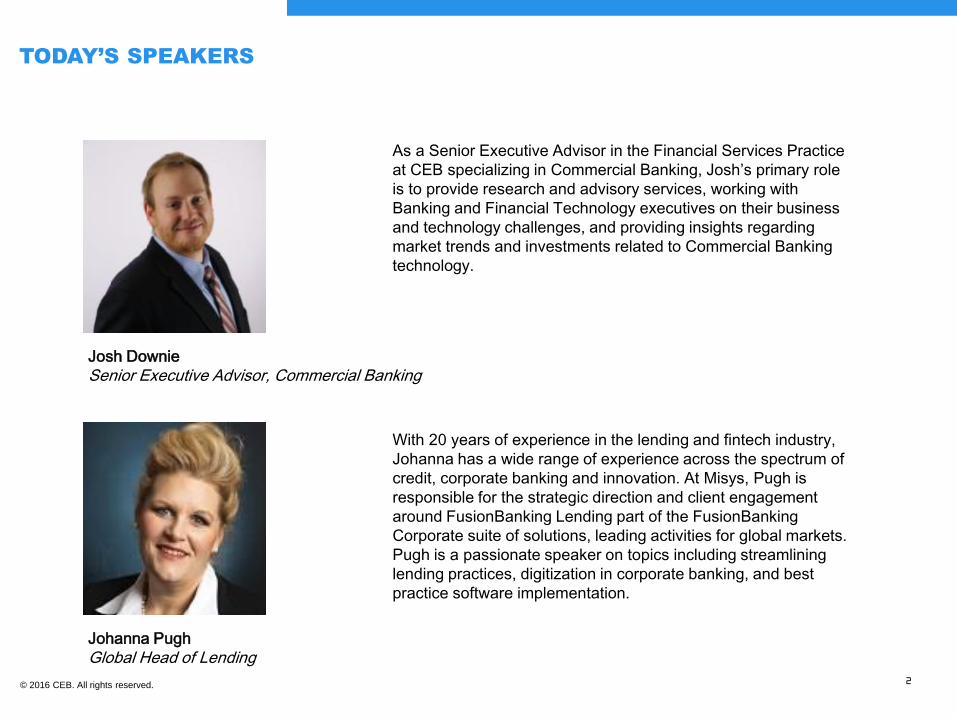

Josh Downie

Senior Executive Advisor, Commercial Banking

As a Senior Executive Advisor in the Financial Services Practice

at CEB specializing in Commercial Banking, Josh’s primary role

is to provide research and advisory services, working with

Banking and Financial Technology executives on their business

and technology challenges, and providing insights regarding

market trends and investments related to Commercial Banking

technology.

2

Johanna Pugh

Global Head of Lending

With 20 years of experience in the lending and fintech industry,

Johanna has a wide range of experience across the spectrum of

credit, corporate banking and innovation. At Misys, Pugh is

responsible for the strategic direction and client engagement

around FusionBanking Lending part of the FusionBanking

Corporate suite of solutions, leading activities for global markets.

Pugh is a passionate speaker on topics including streamlining

lending practices, digitization in corporate banking, and best

practice software implementation.

© 2016 CEB. All rights reserved.

ROADMAP FOR THE PRESENTATION

Commercial Banking

Business

Environment

Improving Customer

Service Through

Digitization

Current State of

Digital Investments

3

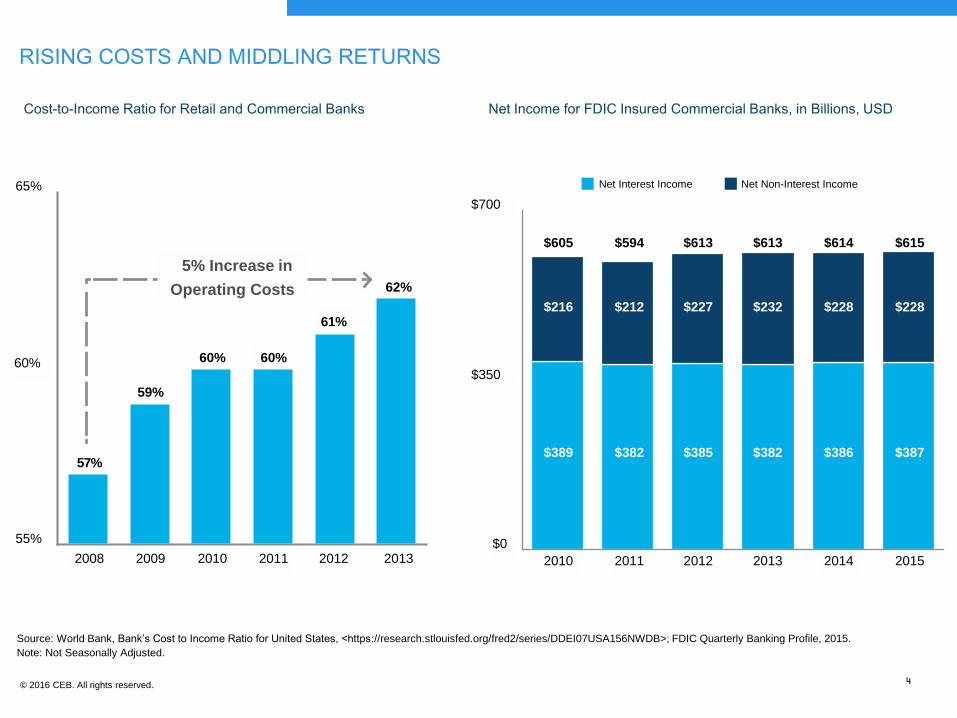

Cost-to-Income Ratio for Retail and Commercial Banks

RISING COSTS AND MIDDLING RETURNS

Net Income for FDIC Insured Commercial Banks, in Billions, USD

Source: World Bank, Bank’s Cost to Income Ratio for United States, <https://research.stlouisfed.org/fred2/series/DDEI07USA156NWDB>; FDIC Quarterly Banking Profile, 2015.

Note: Not Seasonally Adjusted.

2008 2009 2010 2011 2012 2013

55%

60%

65%

57%

59%

60% 60%

61%

62%

5% Increase in

Operating Costs

2010 2011 2012 2013 2014 2015

$0

$350

$700

$389

$216

$382

$212

$385

$227

$382

$232

$386

$228

$387

$228

$605 $594 $613 $613 $614 $615

Net Interest Income Net Non-Interest Income

© 2016 CEB. All rights reserved. 4

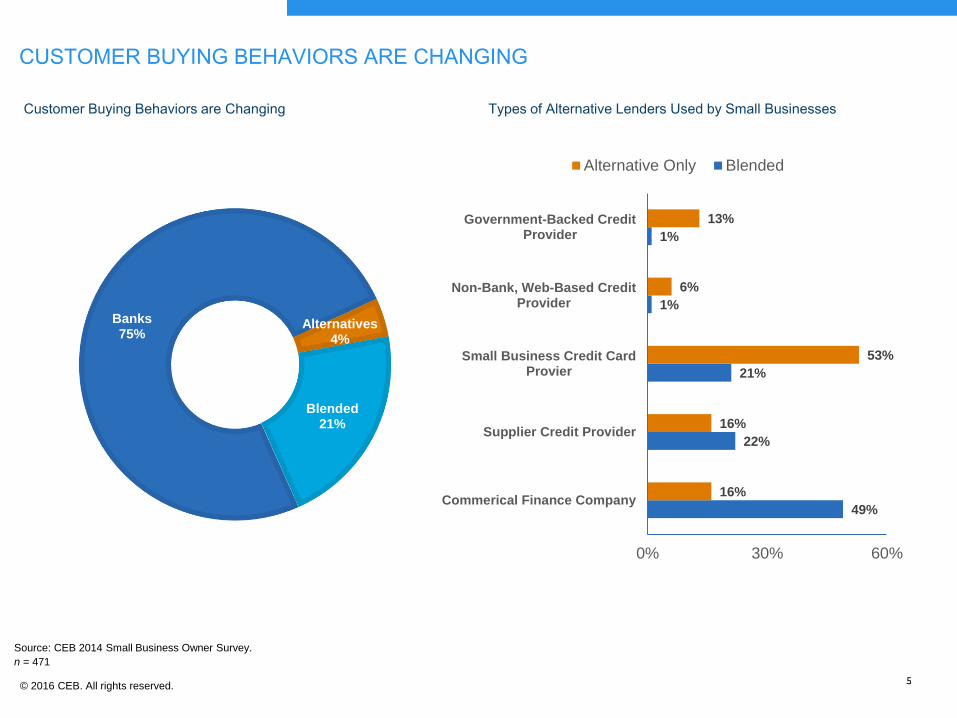

Customer Buying Behaviors are Changing

CUSTOMER BUYING BEHAVIORS ARE CHANGING

Types of Alternative Lenders Used by Small Businesses

Banks75%

Alternatives4%

Blended21%

49%

22%

21%

1%

1%

16%

16%

53%

6%

13%

0% 30% 60%

Commerical Finance Company

Supplier Credit Provider

Small Business Credit CardProvier

Non-Bank, Web-Based CreditProvider

Government-Backed CreditProvider

Alternative Only Blended

Source: CEB 2014 Small Business Owner Survey.

n = 471

© 2016 CEB. All rights reserved.5

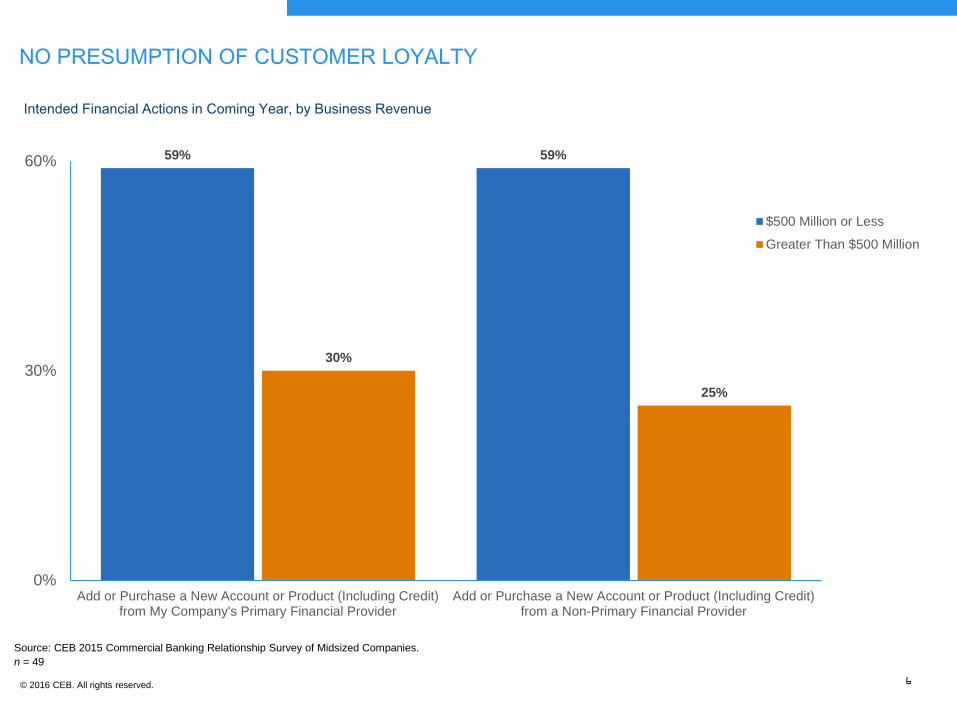

Intended Financial Actions in Coming Year, by Business Revenue

NO PRESUMPTION OF CUSTOMER LOYALTY

59% 59%

30%

25%

0%

30%

60%

Add or Purchase a New Account or Product (Including Credit)from My Company's Primary Financial Provider

Add or Purchase a New Account or Product (Including Credit)from a Non-Primary Financial Provider

$500 Million or Less

Greater Than $500 Million

© 2016 CEB. All rights reserved. 6

Source: CEB 2015 Commercial Banking Relationship Survey of Midsized Companies.

n = 49

© 2016 CEB. All rights reserved.

ROADMAP FOR THE PRESENTATION

Commercial Banking

Business

Environment

Improving Customer

Service Through

Digitization

Current State of

Digital Investments

7

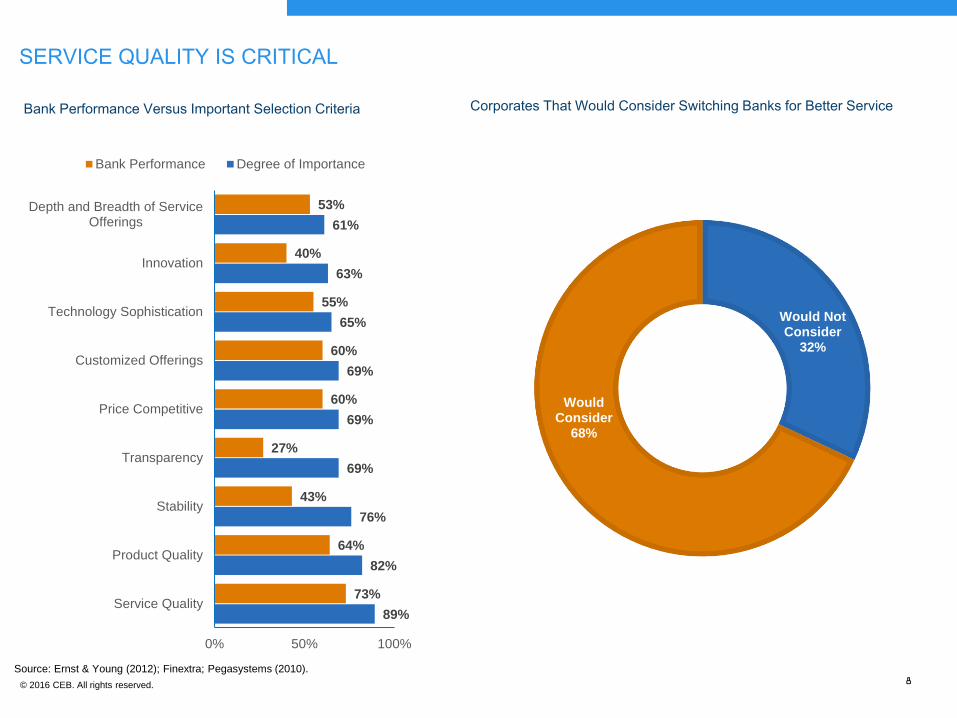

Bank Performance Versus Important Selection Criteria

SERVICE QUALITY IS CRITICAL

Corporates That Would Consider Switching Banks for Better Service

89%

82%

76%

69%

69%

69%

65%

63%

61%

73%

64%

43%

27%

60%

60%

55%

40%

53%

0% 50% 100%

Service Quality

Product Quality

Stability

Transparency

Price Competitive

Customized Offerings

Technology Sophistication

Innovation

Depth and Breadth of ServiceOfferings

Bank Performance Degree of Importance

Would Not Consider

32%

Would Consider

68%

© 2016 CEB. All rights reserved. 8

Source: Ernst & Young (2012); Finextra; Pegasystems (2010).

Correlation Between Online and Mobile Access and Customer Service

DIGITAL CHANNELS INVESTMENT LINKED TO CUSTOMER SERVICE

Payments

Cash ManagementFX

Trade Finance

Liquidity

Pooling / NettingBank-Assisted Open

Account

Forecasting

40%

50%

60%

70%

80%

20% 30% 40% 50% 60% 70% 80% 90% 100%

Custo

mer

Satisfa

ctio

n b

y M

ain

Bankin

g P

art

ner

(Perc

ent of C

orp

ora

te P

ractitio

ners

Ratin

g S

erv

ice "

4"

or

"5"

on a

5-p

oin

t scale

)

Product Areas Covered by Online or Mobile Banking Solutions(Percent of Banking Service Providers)

Source: 2015 AFP Transaction Banking Survey, Association of Financial Professionals.

n = 784

© 2016 CEB. All rights reserved. 9

Percent of Business Leaders in Financial Services

DIGITAL: IMPORTANT, BUT UNCLEAR

35% Agree

65% Disagree

n = 209 FSI Business Leaders.

Source: CEB 2016 Digital Enterprise Survey.

“ I Have a Clear

Understanding of How

Digitization Applies to

My Organization.”

“Our key issue is to get bankers comfortable with digital.”

Australian Commercial Bank Executive “Everything is trending towards

“digital”—customers have expectations that banks will deliver.”

North American Commercial Bank Executive

“There are so many buzz words —data scientist, digital marketing, big data…”

North American Commercial Bank Executive

“Our digital strategy needs improvement."

South African Commercial Bank Executive

“We want to use digitization to improve our core capabilities.”

European Commercial Bank Executive

“What’s the impact of digital on the RM?”

European Commercial Bank Executive

“What does define a digital bank?”

Asian Commercial Bank Executive

“Commercial banking is still a little behind on our use of digital.”

North American Commercial Bank Executive

“How do we invest in new technology?"

North American Commercial Bank Executive

© 2016 CEB. All rights reserved. 10

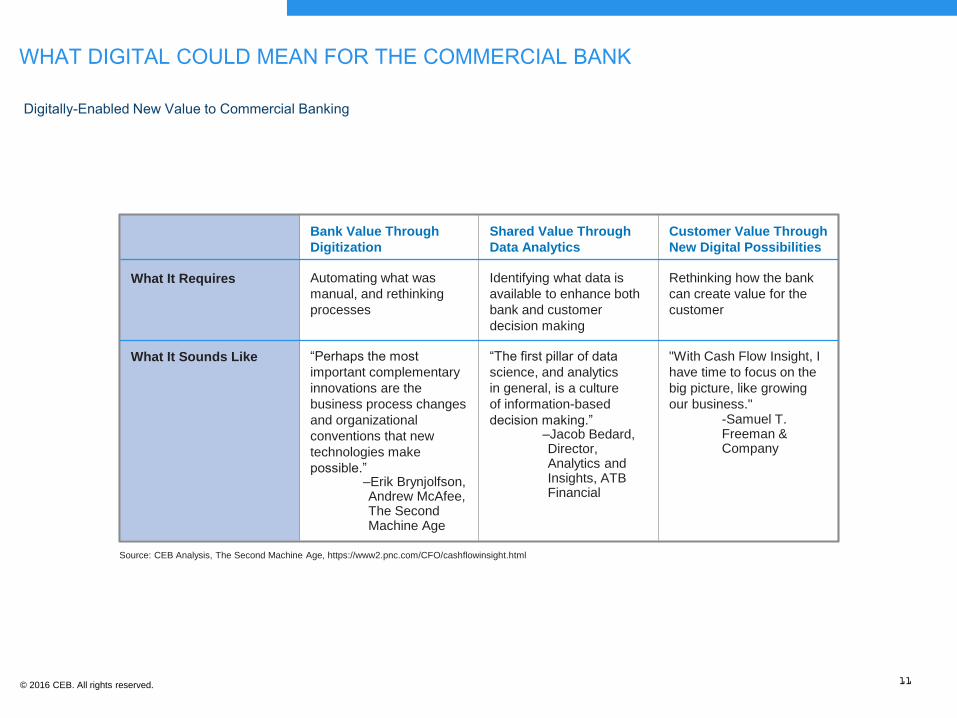

Digitally-Enabled New Value to Commercial Banking

WHAT DIGITAL COULD MEAN FOR THE COMMERCIAL BANK

Bank Value Through

Digitization

Shared Value Through

Data Analytics

Customer Value Through

New Digital Possibilities

What It Requires Automating what was

manual, and rethinking

processes

Identifying what data is

available to enhance both

bank and customer

decision making

Rethinking how the bank

can create value for the

customer

What It Sounds Like “Perhaps the most

important complementary

innovations are the

business process changes

and organizational

conventions that new

technologies make

possible.” –Erik Brynjolfson, Andrew McAfee, The Second Machine Age

“The first pillar of data

science, and analytics

in general, is a culture

of information-based

decision making.” –Jacob Bedard, Director, Analytics and Insights, ATB Financial

"With Cash Flow Insight, I

have time to focus on the

big picture, like growing

our business."-Samuel T. Freeman & Company

Source: CEB Analysis, The Second Machine Age, https://www2.pnc.com/CFO/cashflowinsight.html

© 2016 CEB. All rights reserved. 11

THE DIGITAL EXPERIENCE

Source: Uber, accessed 24 May 2016, https://www.newsroom.uber.com

© 2016 CEB. All rights reserved. 12

© 2016 CEB. All rights reserved.

ROADMAP FOR THE PRESENTATION

Commercial Banking

Business

Environment

Improving Customer

Service Through

Digitization

Current State of

Digital Investments

13

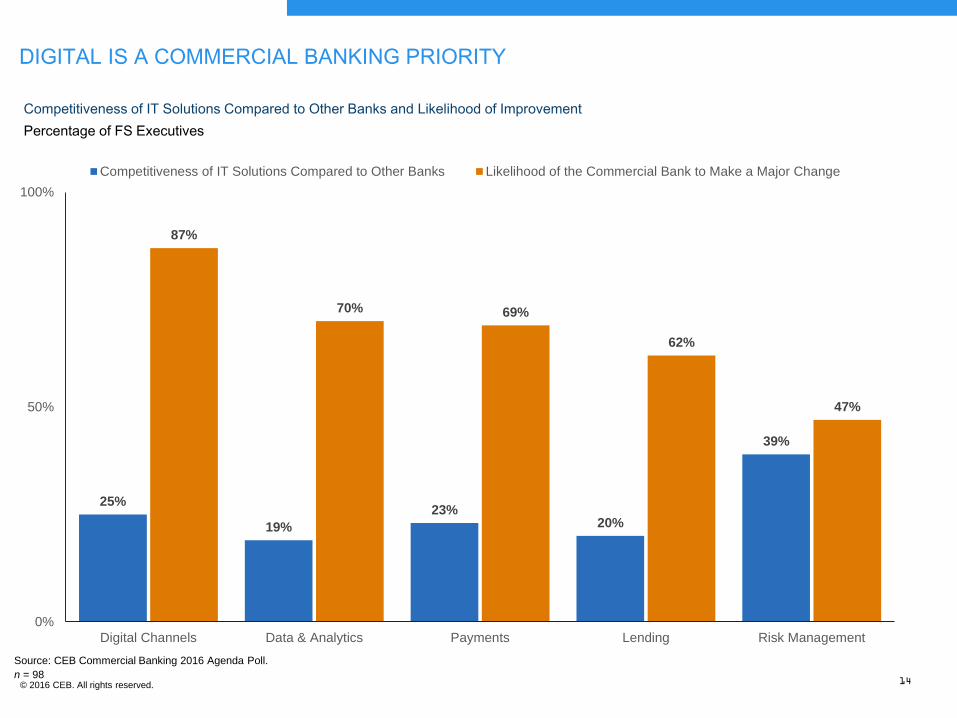

Competitiveness of IT Solutions Compared to Other Banks and Likelihood of Improvement

Percentage of FS Executives

DIGITAL IS A COMMERCIAL BANKING PRIORITY

25%

19%

23%20%

39%

87%

70% 69%

62%

47%

0%

50%

100%

Digital Channels Data & Analytics Payments Lending Risk Management

Competitiveness of IT Solutions Compared to Other Banks Likelihood of the Commercial Bank to Make a Major Change

© 2016 CEB. All rights reserved. 14

Source: CEB Commercial Banking 2016 Agenda Poll.

n = 98

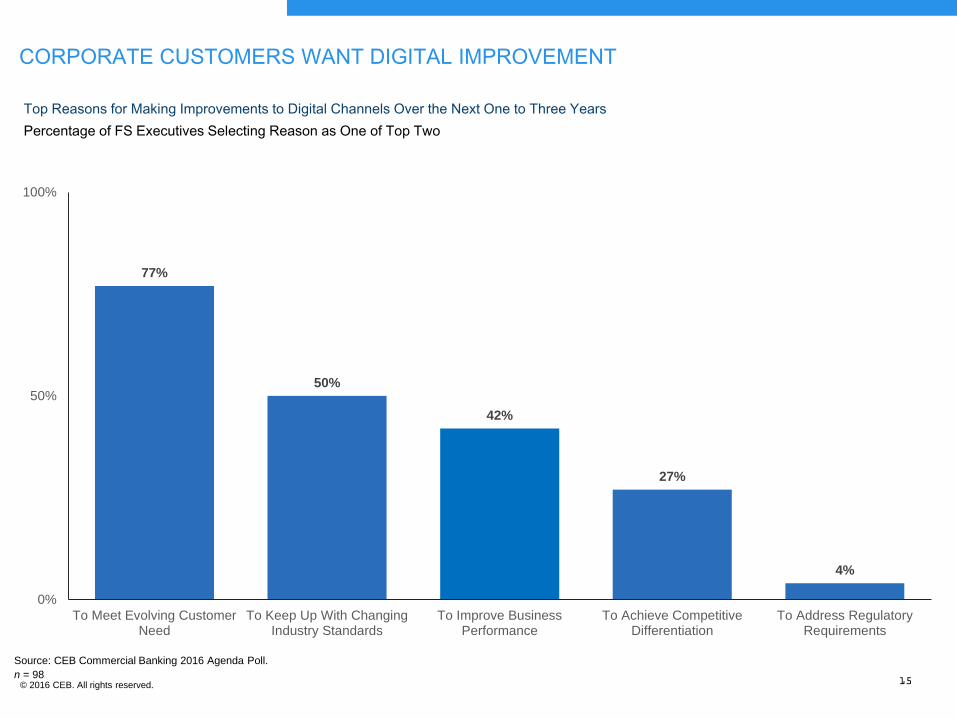

Top Reasons for Making Improvements to Digital Channels Over the Next One to Three Years

Percentage of FS Executives Selecting Reason as One of Top Two

CORPORATE CUSTOMERS WANT DIGITAL IMPROVEMENT

77%

50%

42%

27%

4%

0%

50%

100%

To Meet Evolving CustomerNeed

To Keep Up With ChangingIndustry Standards

To Improve BusinessPerformance

To Achieve CompetitiveDifferentiation

To Address RegulatoryRequirements

© 2016 CEB. All rights reserved. 15

Source: CEB Commercial Banking 2016 Agenda Poll.

n = 98

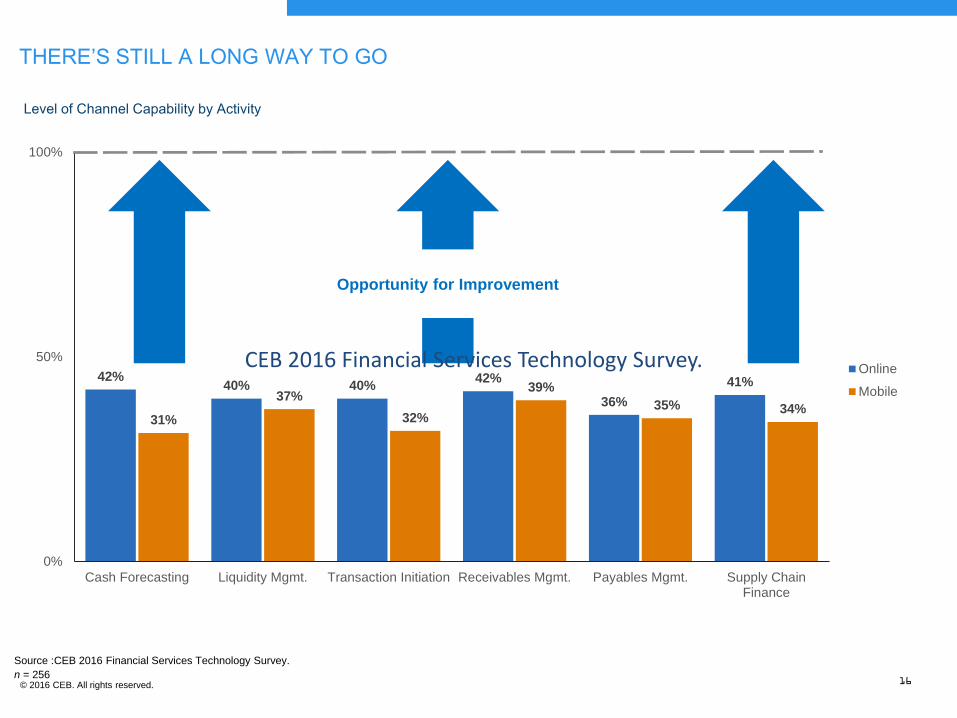

42%40% 40%

42%

36%

41%

31%

37%

32%

39%

35% 34%

0%

50%

100%

Cash Forecasting Liquidity Mgmt. Transaction Initiation Receivables Mgmt. Payables Mgmt. Supply ChainFinance

Online

Mobile

Opportunity for Improvement

Level of Channel Capability by Activity

THERE’S STILL A LONG WAY TO GO

© 2016 CEB. All rights reserved. 16

Source :CEB 2016 Financial Services Technology Survey.

n = 256

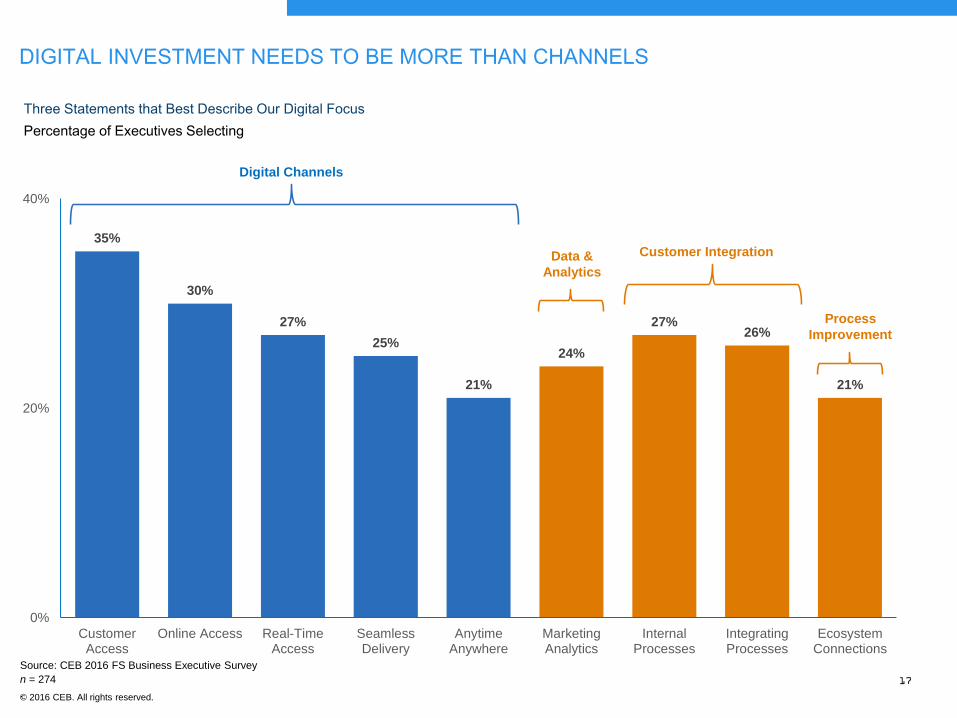

CEB 2016 Financial Services Technology Survey.

Three Statements that Best Describe Our Digital Focus

Percentage of Executives Selecting

DIGITAL INVESTMENT NEEDS TO BE MORE THAN CHANNELS

35%

30%

27%

25%

21%

24%

27%26%

21%

0%

20%

40%

CustomerAccess

Online Access Real-TimeAccess

SeamlessDelivery

AnytimeAnywhere

MarketingAnalytics

InternalProcesses

IntegratingProcesses

EcosystemConnections

Data &

Analytics

Digital Channels

Customer Integration

Process

Improvement

Source: CEB 2016 FS Business Executive Survey

n = 274

.© 2016 CEB. All rights reserved.

17

1

The challenge

© Misys 24 May 2016

Complexity

Disconnected user experience

Onboarding? Follow the customer?

Sales, service and operational

inefficiency

Fragmented digitalisation

No single customer view

Slow technology adoption

Lack of agility for right product,

right time

Data islands

Trapped capital and liquidity

Compliance and reporting burden

Who’s your most

profitable customer?

Spiraling cost Risk hitting profitsLoss of revenue

Case in point: all-in-one corporate banking demands

© Misys 224 May 2016

American Finance Airlines

- Head Office in Sydney

- Subsidiaries / Offices in London, New York, Sao Paulo,

Singapore, Hong Kong, China, Tokyo

• 4 Current Accounts

• 1 Current Account with Overdraft

• 2 Term Deposits

• 3 Loan Accounts

• 3 Letters of Credit

Bank

- Head Office in Sydney

- Regional presence in Singapore, Hong Kong, and China.

• Cash / Transactional Services

• Trade Finance

• Lending

• Treasury

BANK

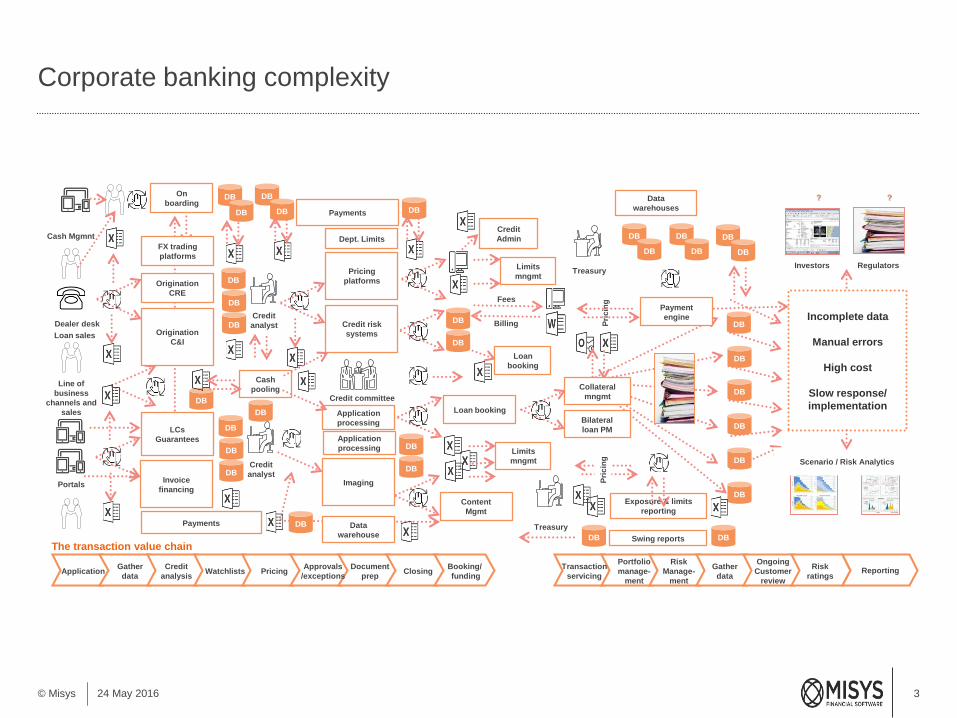

Corporate banking complexity

3© Misys 24 May 2016

Pri

cin

gFees

Credit committee

Credit

analyst

Credit

analyst

Line of

business

channels and

sales

Origination

CRE

LCs

Guarantees

Pricing

platformsDB

DB

DB

DB

DB

DB

Credit risk

systems

Application

processing

Imaging

DB

DB

DB

DB

Content

Mgmt

Loan booking

Loan

booking

Credit

Admin

Limits

mngmt

Billing

Treasury

Treasury

Data

warehouses

Pri

cin

g

Exposure & limits

reporting

DB

DB

DB

DB

DB

DB

Bilateral

loan PM

Payment

engine

Collateral

mngmt

Origination

C&I

Invoice

financing

DB

Investors Regulators

Incomplete data

Manual errors

High cost

Slow response/

implementation

?

? ?

?

Scenario / Risk Analytics

Limits

mngmt

DB

DB

DB

DB

DB

DB

On

boardingDB

DB

DB

DB

Dept. Limits

Cash

pooling

Payments

Payments

Swing reports

DB

DB

Loan sales

Cash Mgmnt

Data

warehouse

Dealer desk

Portals

FX trading

platforms

DB

DB

ApplicationGather

data

Credit

analysisWatchlists Pricing

Approvals

/exceptions

Document

prepClosing

Booking/

funding

Transaction

servicing

Gather

data

Risk

ratings

Portfolio

manage-

ment

Ongoing

Customer

review

Risk

Manage-

ment

The transaction value chain

Application

processing

Reporting

DB

4

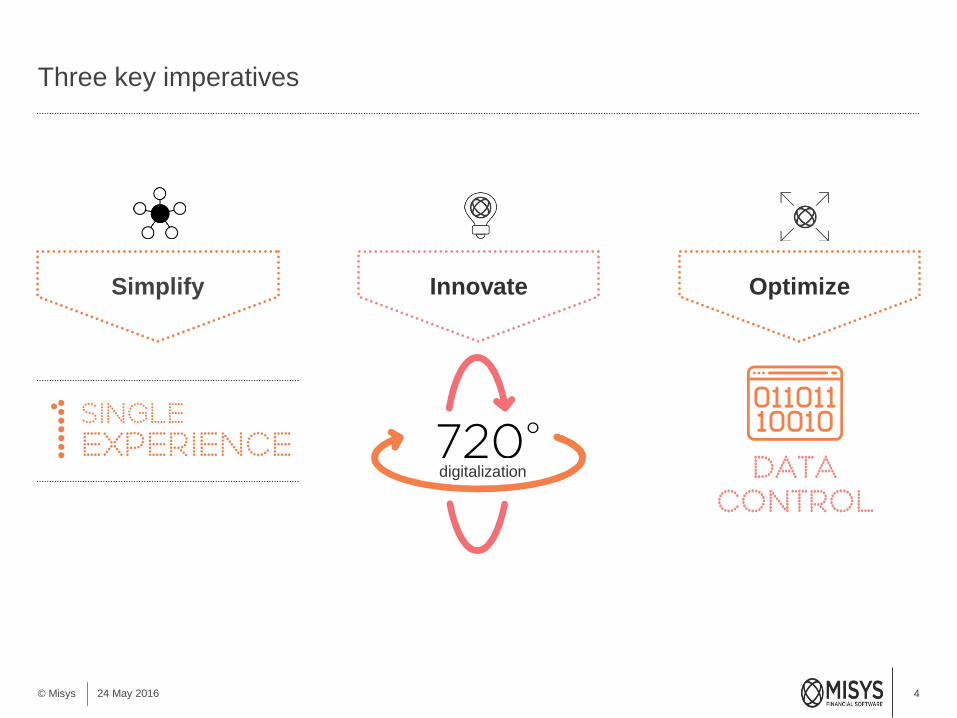

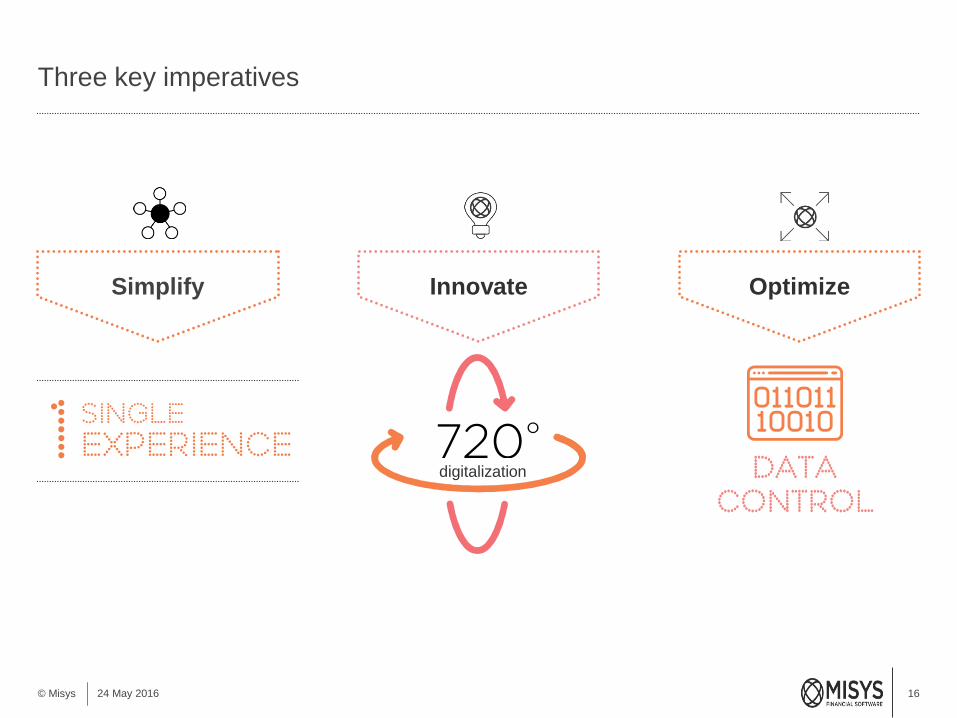

Three key imperatives

© Misys 24 May 2016

Simplify Innovate Optimize

digitalization

© Misys

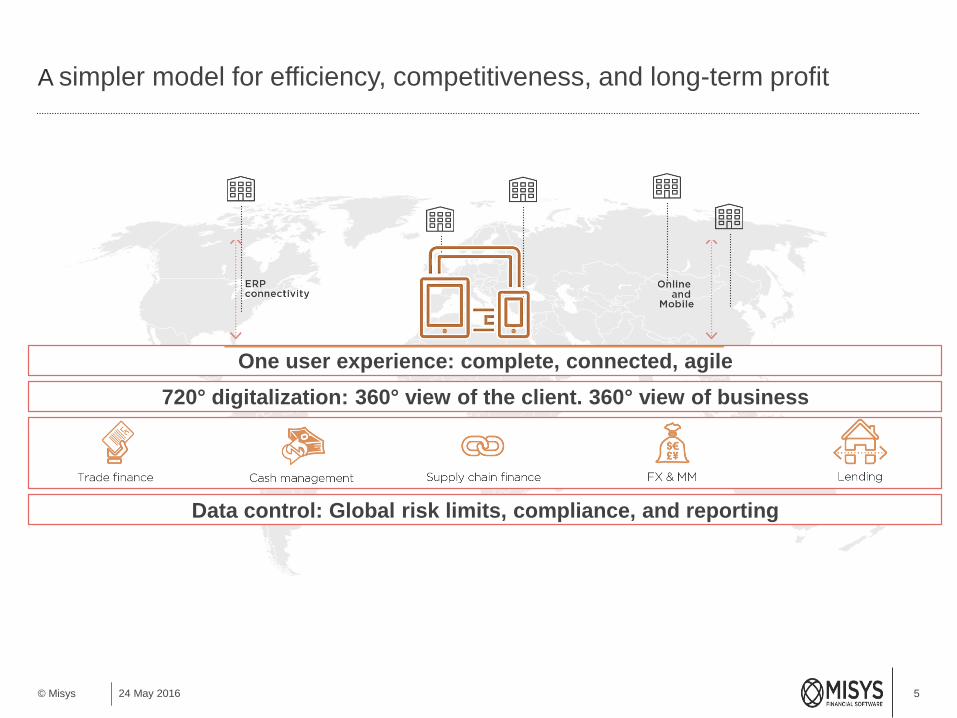

A simpler model for efficiency, competitiveness, and long-term profit

524 May 2016

GlobalisationOne user experience: complete, connected, agile

Data control: Global risk limits, compliance, and reporting

720° digitalization: 360° view of the client. 360° view of business

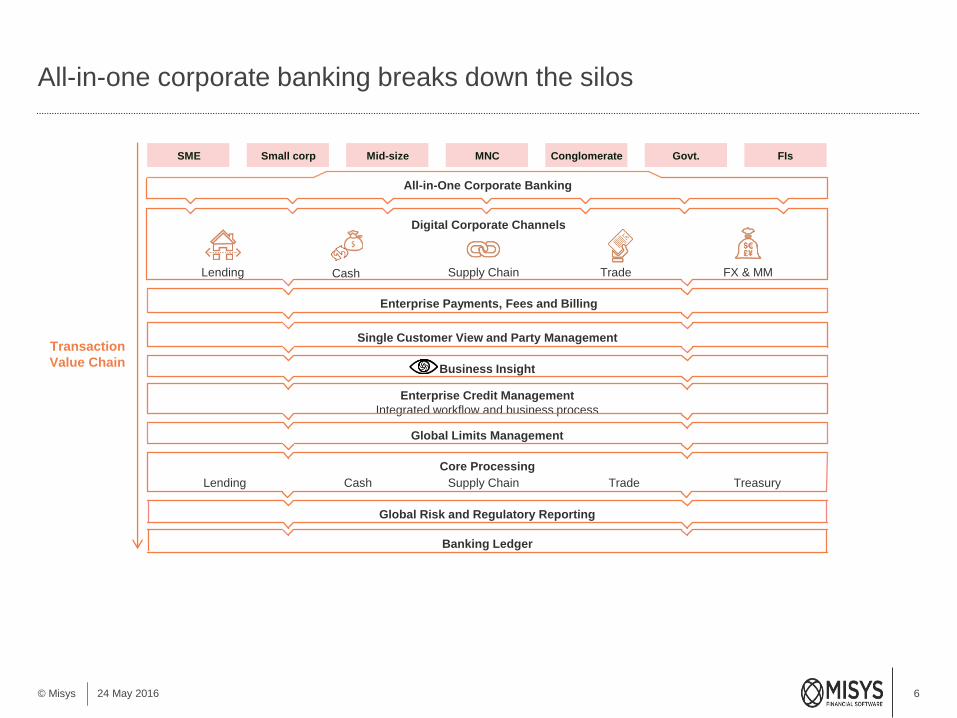

All-in-one corporate banking breaks down the silos

6© Misys 24 May 2016

Small corp Mid-size MNC Conglomerate Govt.SME

Transaction

Value Chain

FIs

All-in-One Corporate Banking

Digital Corporate Channels

Lending FX & MMSupply Chain TradeCash

Enterprise Payments, Fees and Billing

Single Customer View and Party Management

Business Insight

Enterprise Credit Management

Integrated workflow and business process

Global Limits Management

Lending Cash Supply Chain Trade Treasury

Core Processing

Banking Ledger

Global Risk and Regulatory Reporting

Case in point: all-in-one corporate banking demands

© Misys 224 May 2016

American Finance Airlines

- Head Office in Sydney

- Subsidiaries / Offices in London, New York, Sao Paulo,

Singapore, Hong Kong, China, Tokyo

• 4 Current Accounts

• 1 Current Account with Overdraft

• 2 Term Deposits

• 3 Loan Accounts

• 3 Letters of Credit

Bank

- Head Office in Sydney

- Regional presence in Singapore, Hong Kong, and China.

• Cash / Transactional Services

• Trade Finance

• Lending

• Treasury

BANK

8

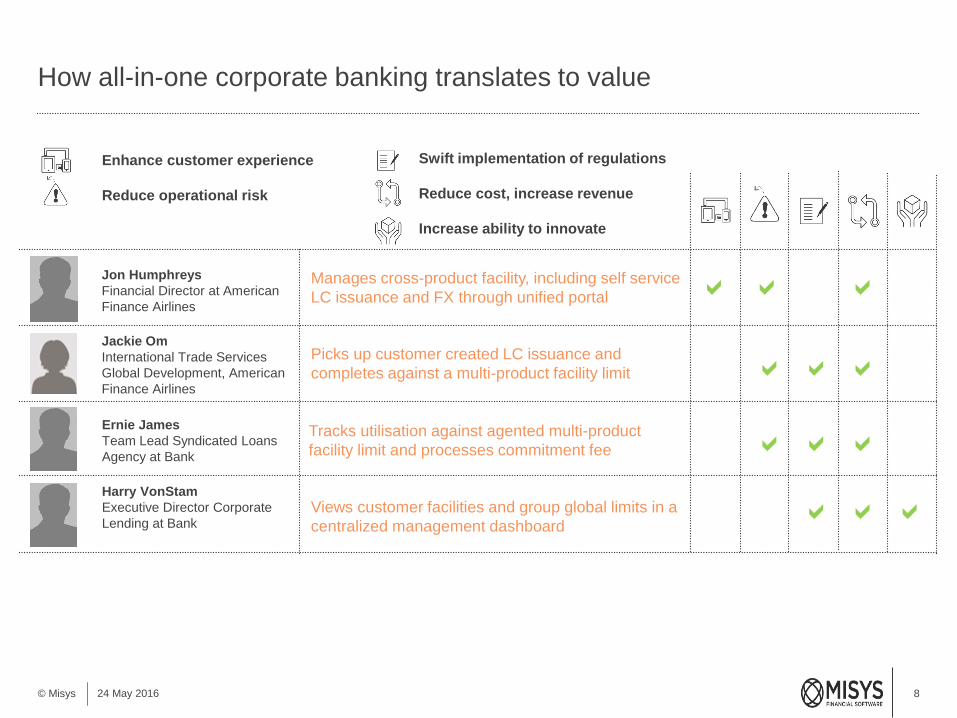

How all-in-one corporate banking translates to value

© Misys 24 May 2016

Harry VonStam

Executive Director Corporate

Lending at Bank

Jon Humphreys

Financial Director at American

Finance Airlines

Jackie Om

International Trade Services

Global Development, American

Finance Airlines

Ernie James

Team Lead Syndicated Loans

Agency at Bank

Manages cross-product facility, including self service

LC issuance and FX through unified portal

Picks up customer created LC issuance and

completes against a multi-product facility limit

Tracks utilisation against agented multi-product

facility limit and processes commitment fee

Views customer facilities and group global limits in a

centralized management dashboard

a

Enhance customer experience

Reduce operational risk

Swift implementation of regulations

Reduce cost, increase revenue

Increase ability to innovate

a a

aaa

aaa

aaa

9

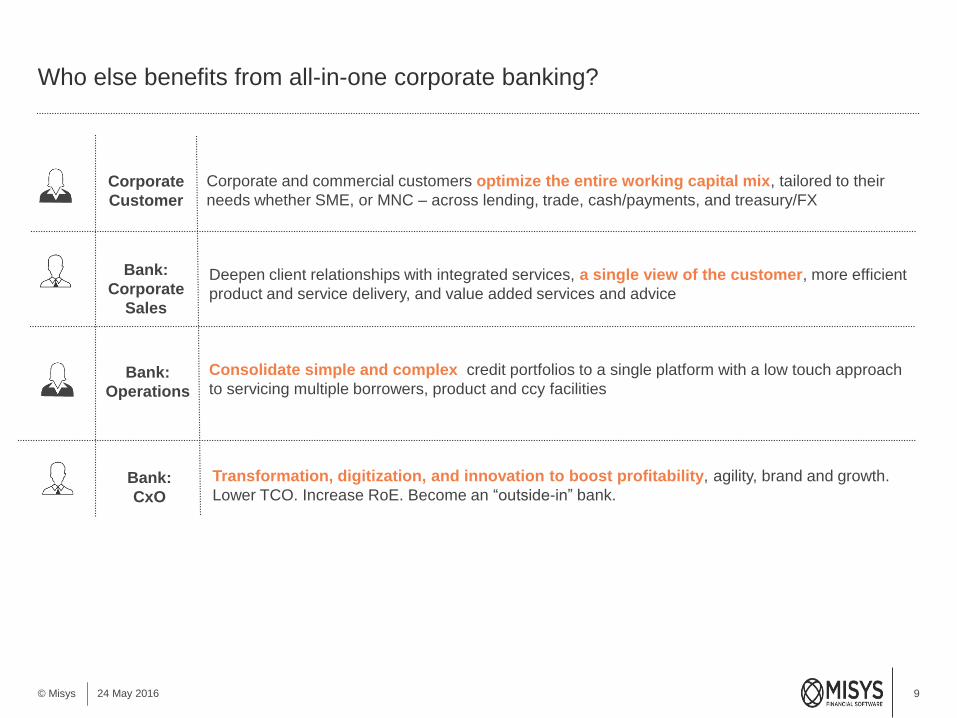

Who else benefits from all-in-one corporate banking?

© Misys 24 May 2016

Bank:

Corporate

Sales

Corporate

Customer

Bank:

Operations

Corporate and commercial customers optimize the entire working capital mix, tailored to their

needs whether SME, or MNC – across lending, trade, cash/payments, and treasury/FX

Consolidate simple and complex credit portfolios to a single platform with a low touch approach

to servicing multiple borrowers, product and ccy facilities

Deepen client relationships with integrated services, a single view of the customer, more efficient

product and service delivery, and value added services and advice

Bank:

CxO

Transformation, digitization, and innovation to boost profitability, agility, brand and growth.

Lower TCO. Increase RoE. Become an “outside-in” bank.

10

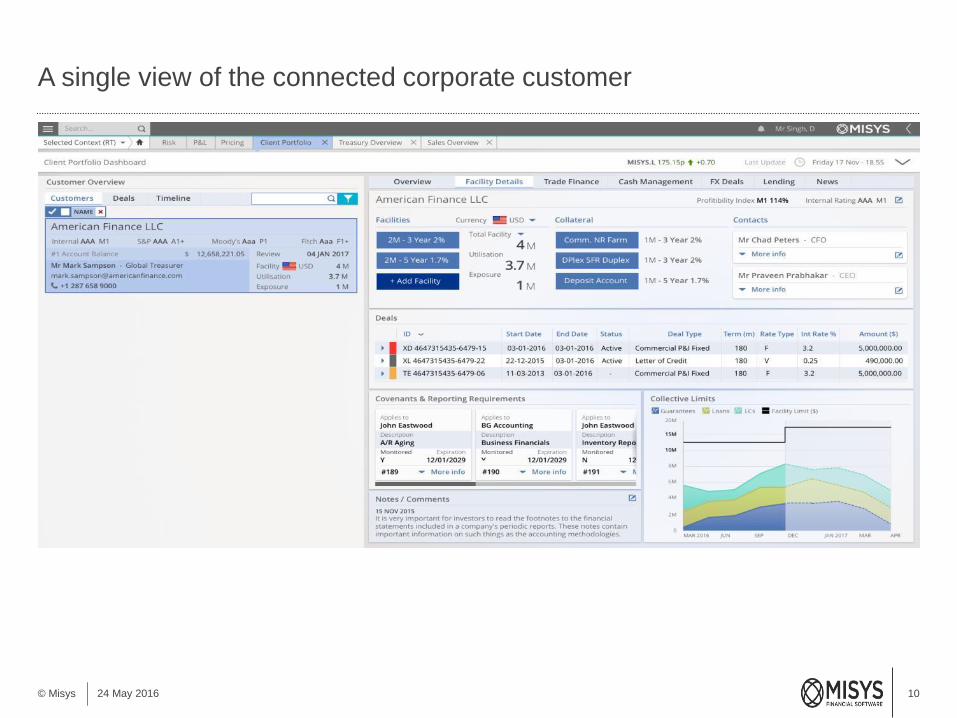

A single view of the connected corporate customer

© Misys 24 May 2016

11

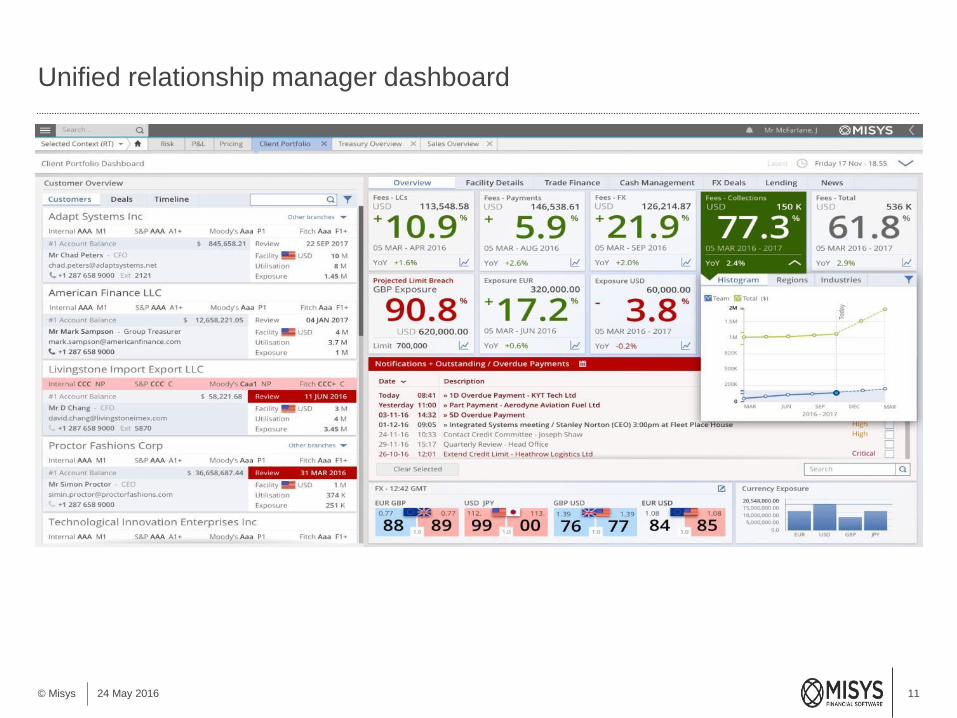

Unified relationship manager dashboard

© Misys 24 May 2016

12

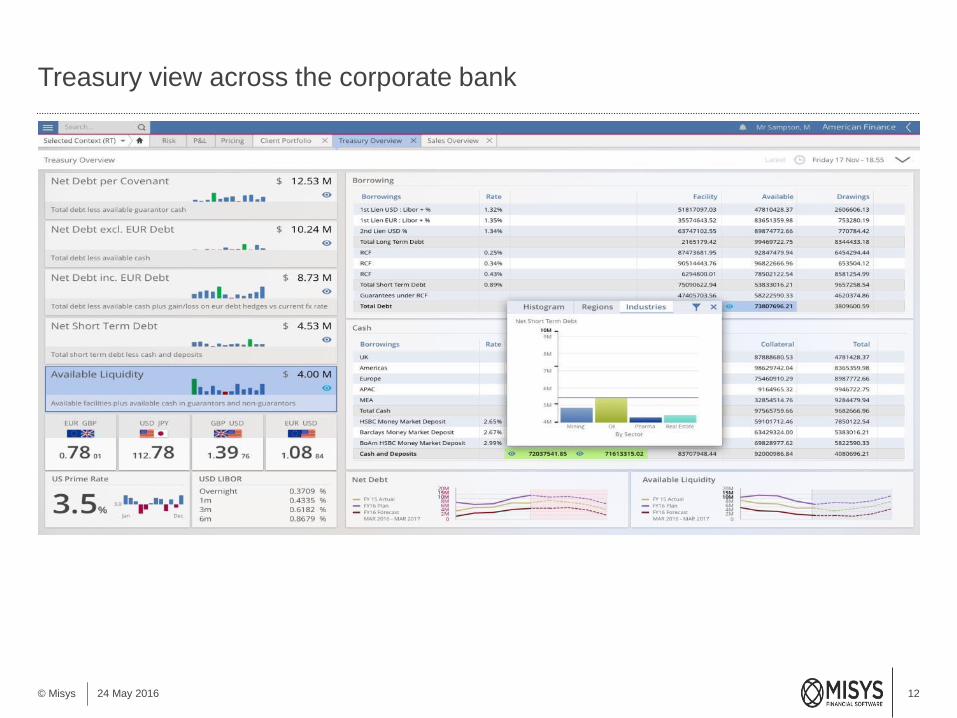

Treasury view across the corporate bank

© Misys 24 May 2016

13

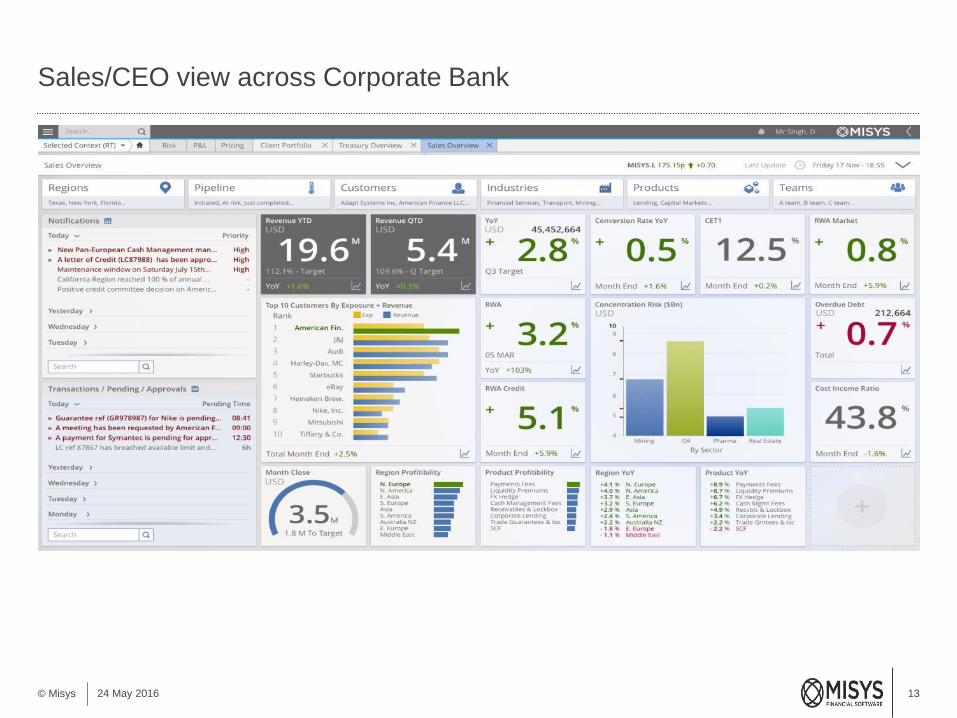

Sales/CEO view across Corporate Bank

© Misys 24 May 2016

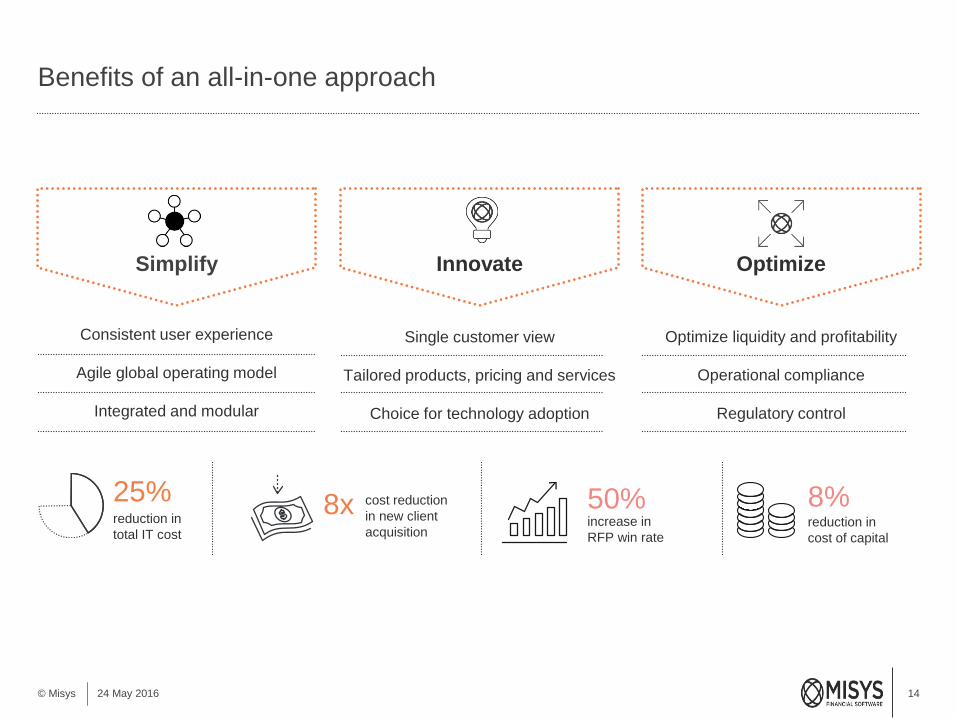

Benefits of an all-in-one approach

14© Misys 24 May 2016

Consistent user experience

Agile global operating model

Integrated and modular

Single customer view

Tailored products, pricing and services

Choice for technology adoption

Optimize liquidity and profitability

Operational compliance

Regulatory control

Simplify Innovate Optimize

reduction in

total IT cost

25%increase in

RFP win rate

50%8x cost reduction

in new client

acquisition

8%reduction in

cost of capital

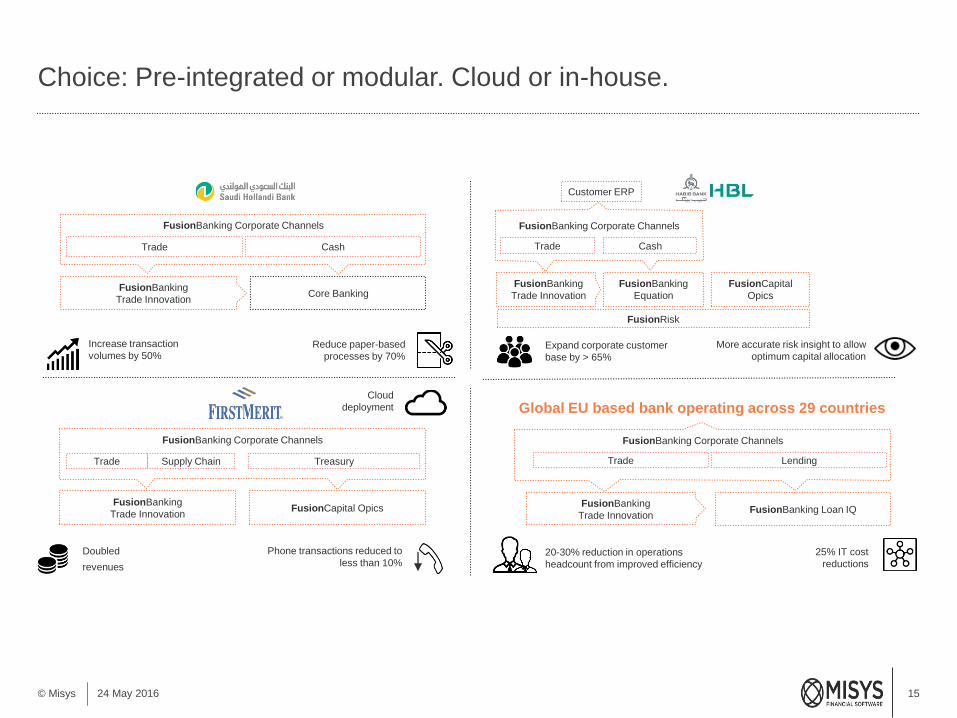

Choice: Pre-integrated or modular. Cloud or in-house.

15© Misys 24 May 2016

FusionBanking Corporate Channels

FusionBanking

Trade Innovation

FusionBanking

Equation

Trade Cash

FusionCapital

Opics

FusionRisk

Customer ERP

More accurate risk insight to allow

optimum capital allocation Expand corporate customer

base by > 65%

Phone transactions reduced to

less than 10%

Supply Chain

FusionBanking Corporate Channels

FusionCapital Opics

Trade Treasury

FusionBanking

Trade Innovation

Doubled

revenues

Cloud

deployment

FusionBanking Corporate Channels

FusionBanking

Trade InnovationCore Banking

Trade Cash

Increase transaction

volumes by 50%Reduce paper-based

processes by 70%

FusionBanking Loan IQ

20-30% reduction in operations

headcount from improved efficiency

25% IT cost

reductions

FusionBanking

Trade Innovation

Trade Lending

FusionBanking Corporate Channels

Global EU based bank operating across 29 countries

16

Three key imperatives

© Misys 24 May 2016

Simplify Innovate Optimize

digitalization

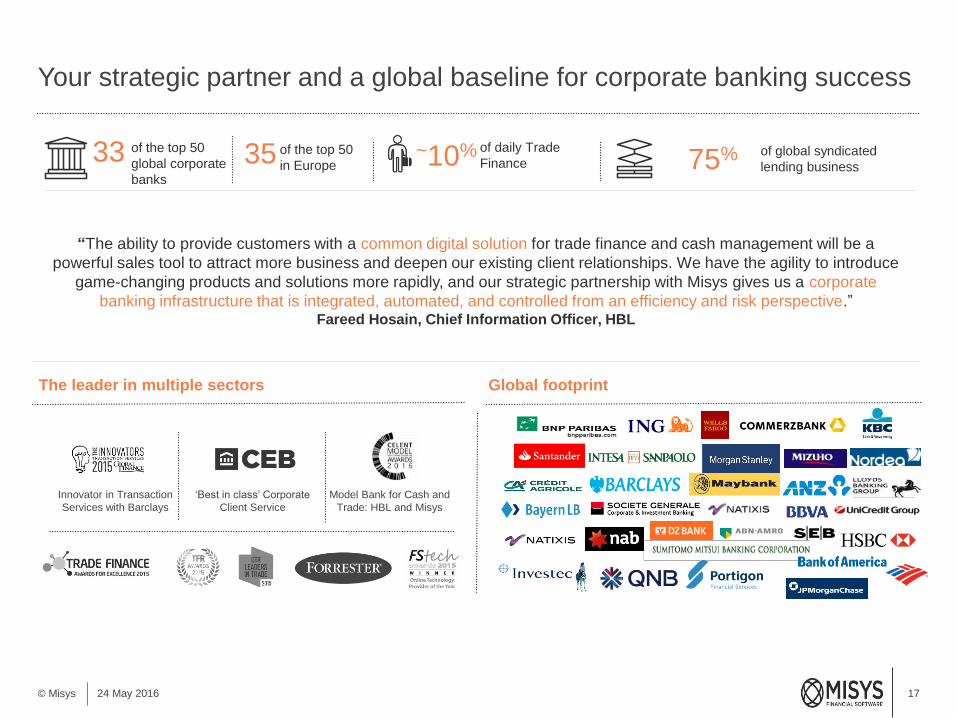

Your strategic partner and a global baseline for corporate banking success

17© Misys 24 May 2016

~10% of daily Trade

Finance

The leader in multiple sectors Global footprint

of the top 50

global corporate

banks

33 of global syndicated

lending business75%of the top 50

in Europe35

Innovator in Transaction

Services with Barclays

‘Best-in-Class’ fo

‘Best in class’ Corporate

Client Service

Model Bank for Cash and

Trade: HBL and Misys

“The ability to provide customers with a common digital solution for trade finance and cash management will be a

powerful sales tool to attract more business and deepen our existing client relationships. We have the agility to introduce

game-changing products and solutions more rapidly, and our strategic partnership with Misys gives us a corporate

banking infrastructure that is integrated, automated, and controlled from an efficiency and risk perspective.” Fareed Hosain, Chief Information Officer, HBL