Embed Size (px)

Citation preview

Why the Advent of the eCity Will Produce Disruptive Change

March 2015 Walter Kitchenman [email protected]

Disruptive vs Top Down Change in US Payments in 2016

Part of a Series on Global Information Management

1

This presentation is part of a series of work by Walter Kitchenman covering the importance and use of Information. Earlier studies documented the availability, use and benefits of shared consumer data and how such transparency shapes businesses globally; Inhibitors to Information Sharing (Knowledge and Content Management);Trends in Loyalty and Customer Communication; and an Introduction to Digital Marketing.

2

1. Define “Disruptive” vs “Top Down” change

2. Describe the Payments’ Landscape or Ecosystem today

3. Rank the relative importance of developments that impact payments

4. Show how mobile payments and the Cloud, accompanied by a Top Down public mandate, will disrupt dominant networks in 2016

5. Anticipate the requirements of likely eCity networks and APPs that wlll emerge in 2016 and benefit IT innovators and non-FSIs (non-Financial Service Institutions)

Purpose

Innovation in Payments is rarely “Disruptive,” but is normally Top Down, driven by public private cooperation, where change is mandated from the top, and entrepreneurs respond to consumer preferences at the margins.

How the eCity Will Disrupt the Payments’ Ecosystem in 2016

Agenda

1. Overview and Definitions …..…………………………….………….. 4

2. Key Developments in Payments 2016 …………………..…………. 13

3. The eCity as Top Down Catalyst ……..…………………………..… 19

4. Impact of Emerging eCity Networks 2016 ………………………….. 23

5. Summary …………………………….……………..………………….. 27

3

OVERVIEW AND DEFINITIONS Disruptive vs Top Down Change in US Payments in 2016

4

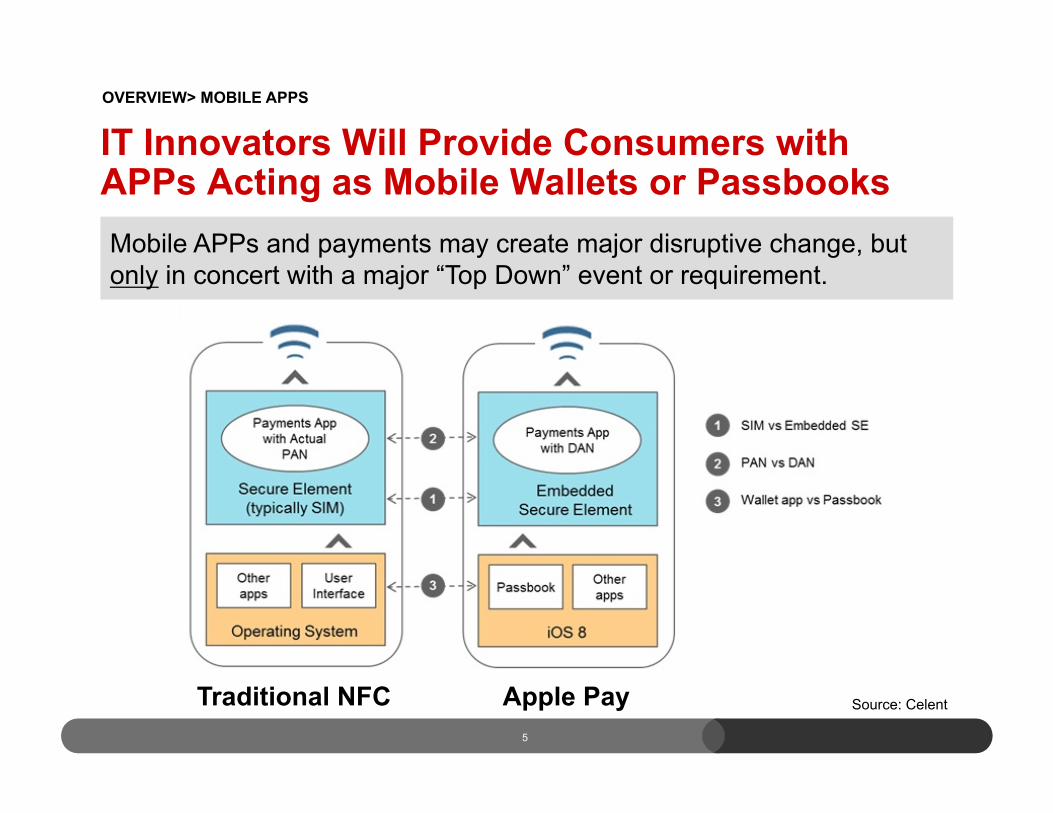

5

Traditional NFC Apple Pay

IT Innovators Will Provide Consumers with APPs Acting as Mobile Wallets or Passbooks Mobile APPs and payments may create major disruptive change, but only in concert with a major “Top Down” event or requirement.

OVERVIEW> MOBILE APPS

Source: Celent

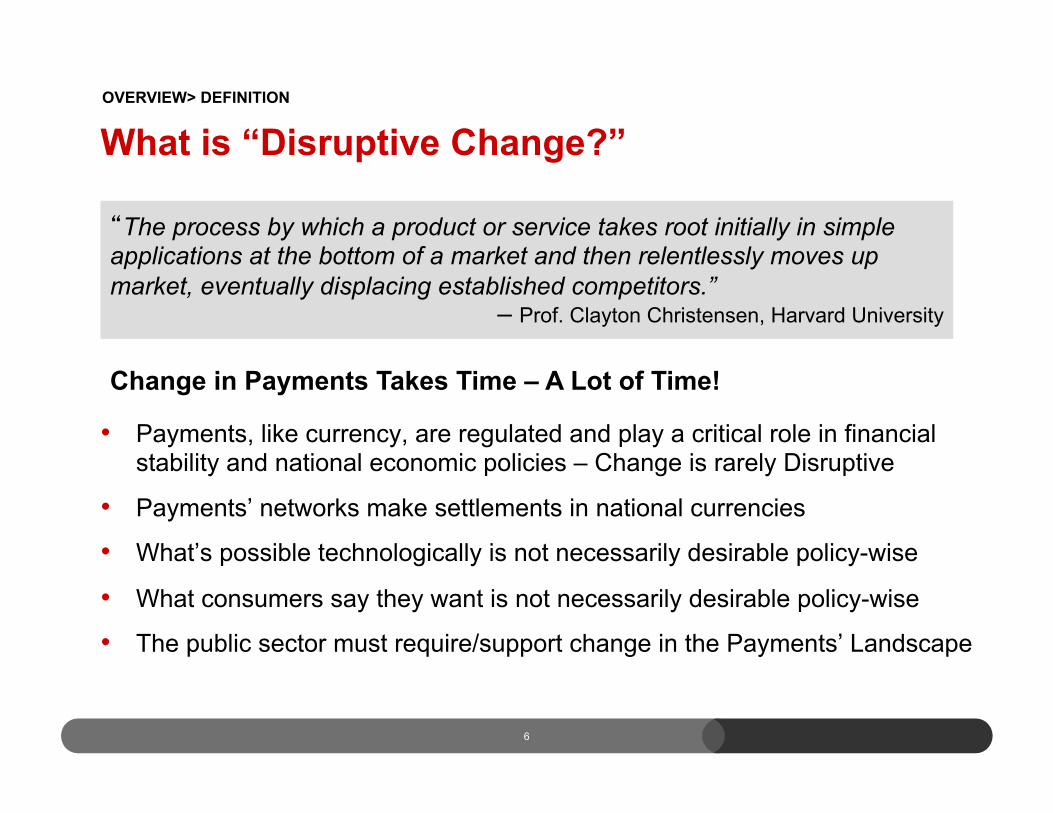

What is “Disruptive Change?”

• Payments, like currency, are regulated and play a critical role in financial stability and national economic policies – Change is rarely Disruptive

• Payments’ networks make settlements in national currencies

• What’s possible technologically is not necessarily desirable policy-wise

• What consumers say they want is not necessarily desirable policy-wise

• The public sector must require/support change in the Payments’ Landscape

6

�The process by which a product or service takes root initially in simple applications at the bottom of a market and then relentlessly moves up market, eventually displacing established competitors.” – Prof. Clayton Christensen, Harvard University

OVERVIEW> DEFINITION

Change in Payments Takes Time – A Lot of Time!

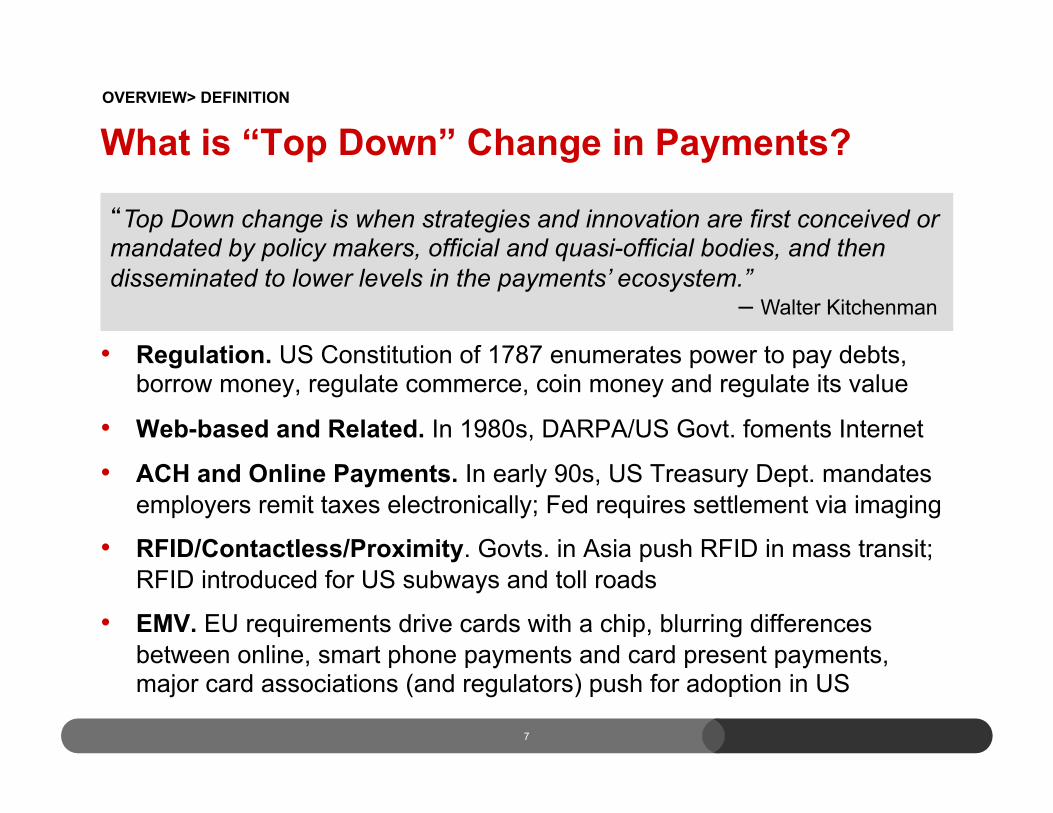

What is “Top Down” Change in Payments?

• Regulation. US Constitution of 1787 enumerates power to pay debts, borrow money, regulate commerce, coin money and regulate its value

• Web-based and Related. In 1980s, DARPA/US Govt. foments Internet

• ACH and Online Payments. In early 90s, US Treasury Dept. mandates employers remit taxes electronically; Fed requires settlement via imaging

• RFID/Contactless/Proximity. Govts. in Asia push RFID in mass transit; RFID introduced for US subways and toll roads

• EMV. EU requirements drive cards with a chip, blurring differences between online, smart phone payments and card present payments, major card associations (and regulators) push for adoption in US

7

�Top Down change is when strategies and innovation are first conceived or mandated by policy makers, official and quasi-official bodies, and then disseminated to lower levels in the payments’ ecosystem.” – Walter Kitchenman

OVERVIEW> DEFINITION

“Top Down Change” Inhibits Innovation Too – and Maybe that’s a Good Thing

• Bitcoins, Other Cyber Currencies and regulatory doubts

• Peer-to-Peer Payments and Small Transfer Difficulty largely due to innovation-killing anti-money laundering compliance

8

�The wrong use of a thing is worse than it’s non-use.” – PLATO, Euthydemus

OVERVIEW> DEFINITION

What is the US Payments’ Landscape Today?

• Payments’ Networks. Dominate and main beneficiaries of the status quo, particularly card settlement (Interchange)

• Card Issuers. Most vulnerable to regulation and disruption (e.g., Durbin and other possible changes that reduce revenues from fees)

• IT Innovators. Non-FSIs that seek innovation and will likely benefit

• Big Box Retailers. Biggest proponents of regulating network fees (that they believe are passed through to them) and litigants to force more regs

• Government Regulators. Possible catalyst for standardization; Durbin limits fees in debit; CFPB will likely regulate non-FSIs by 2016

9

�Many potentially disruptive forces have …minimal impact because there’s … limited operability from one technology to another. If payments …gain something equivalent to open sourcing of mobile APPs … that could change things dramatically.” – George Hofheimer, Filene Research Institute

OVERVIEW> US PAYMENTS TODAY

How Do Today’s Payments’ Networks Work?

1. Cardholders. Make purchases and are billed – IT innovators (e.g. Apple Pay) may act as intermediaries

2. Merchants. Accept payments’ cards and other instruments and pay fees – Third party processors may act as intermediaries – Big Box Retailers may create their own independent network to capture all fees

3. Acquirers. FSIs that enlist merchants to accept payments’ instruments

4. Card Co.’s (or Assoc.). Visa, MasterCard, etc. determine network fees (Interchange), settle payments and control most payments

5. Card Issuers. FSIs that Acquire/Retain cardholders, manage Rewards – Third party processors may act as intermediaries

10

Payments involve a four part process through which settlement is made between the merchant’s and consumer’s banks. There are five participants.

OVERVIEW> US PAYMENTS TODAY

Example of Payments’ Card Settlement

Example of Payments’ Network (e.g., the Interchange): US$100 Purchase @ 2% Fee (with Innovative Device)

5 Processor Pays $98.00 ($2.00 discount)

7 Issuer Pays $98.00

ISSUING BANK (aka ISSUER)

CARD COMPANIES /PROCESSORS

MERCHANT (aka RETAILER)

CONSUMERS (aka CARDHOLDERS)

1 $100 Purchase with Card or Device

2 Merchant Submits $100

3 Acquiring bank pays merchant $97.55 ($2.45 Discount)

4 Bank Submits $100

ACQUIRING BANK (aka MERCHANT BANK)

8 Issuer Bills Cardholder $100

6 Processor Submits $100

9 Cardholder Pays $100 or Revolves (if credit card)

NFC, WALLET APPLE PAY,

CLOUD, OTHER

OVERVIEW> EXAMPLE INTERCHANGE

11

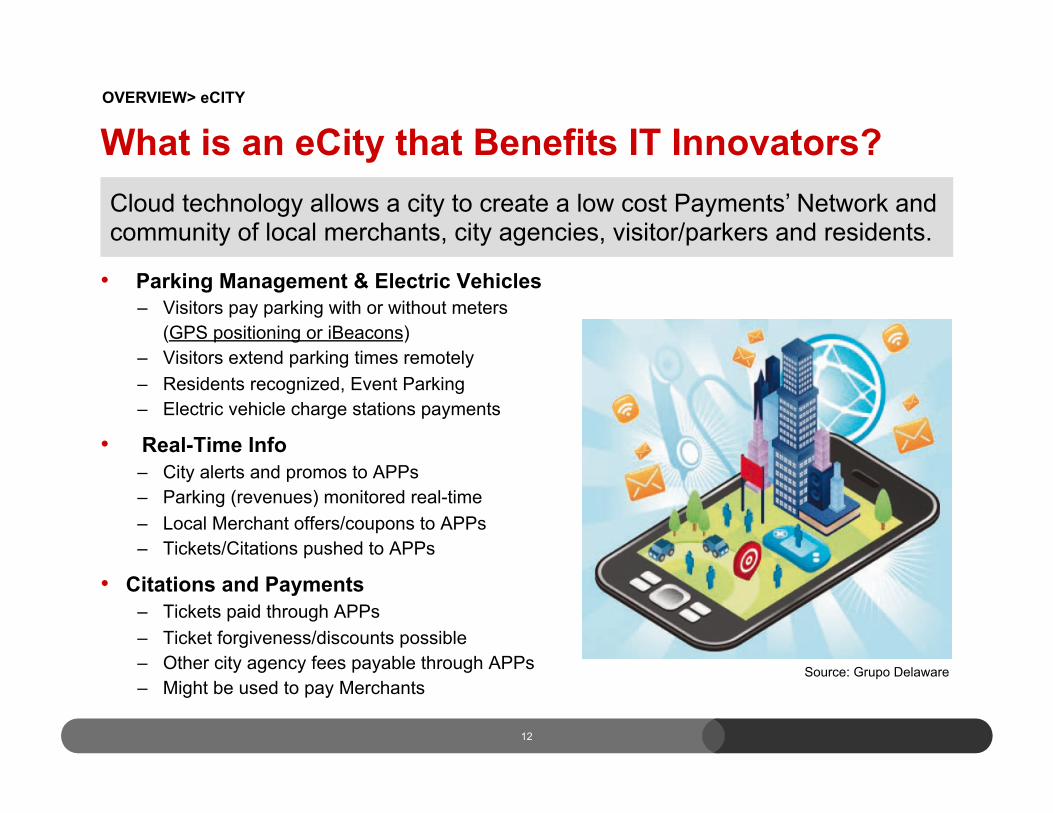

What is an eCity that Benefits IT Innovators?

• Parking Management & Electric Vehicles – Visitors pay parking with or without meters (GPS positioning or iBeacons) – Visitors extend parking times remotely – Residents recognized, Event Parking – Electric vehicle charge stations payments

• Real-Time Info – City alerts and promos to APPs – Parking (revenues) monitored real-time – Local Merchant offers/coupons to APPs – Tickets/Citations pushed to APPs

• Citations and Payments – Tickets paid through APPs – Ticket forgiveness/discounts possible – Other city agency fees payable through APPs – Might be used to pay Merchants

12

Cloud technology allows a city to create a low cost Payments’ Network and community of local merchants, city agencies, visitor/parkers and residents.

OVERVIEW> eCITY

Source: Grupo Delaware

KEY DEVELOPMENTS IN PAYMENTS 2016 Disruptive vs Top Down Change in US Payments in 2016

13

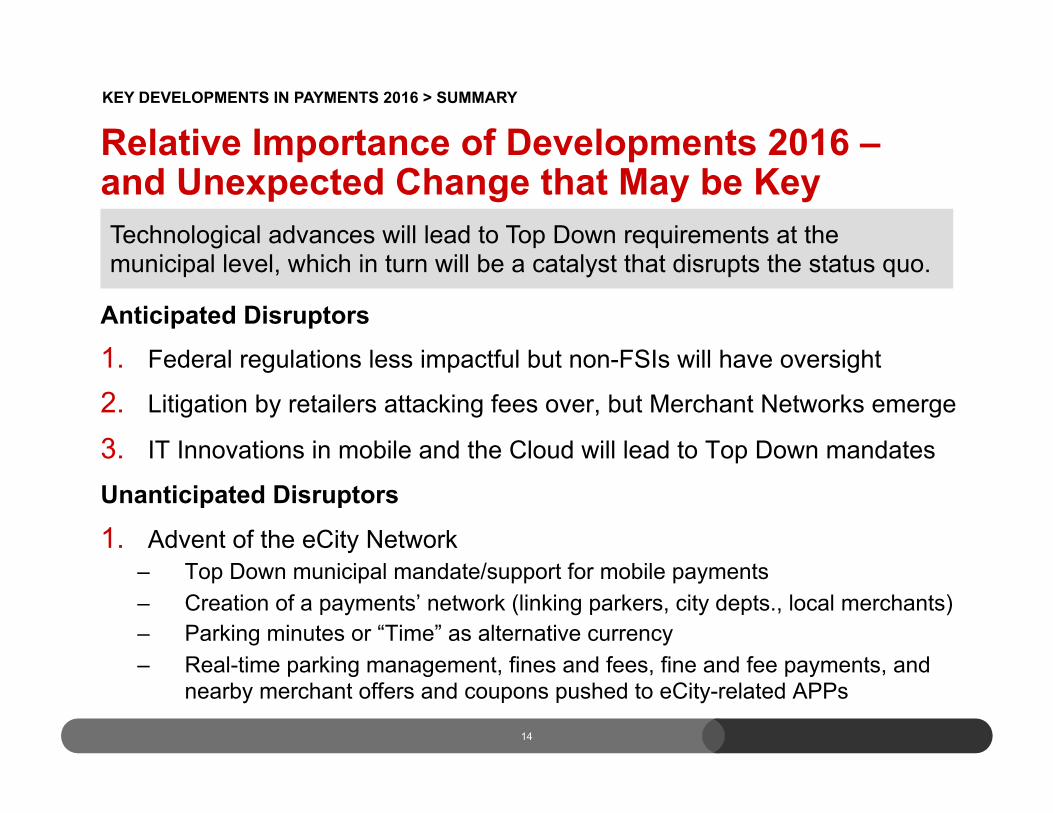

14

Anticipated Disruptors

1. Federal regulations less impactful but non-FSIs will have oversight

2. Litigation by retailers attacking fees over, but Merchant Networks emerge

3. IT Innovations in mobile and the Cloud will lead to Top Down mandates

Unanticipated Disruptors

1. Advent of the eCity Network – Top Down municipal mandate/support for mobile payments – Creation of a payments’ network (linking parkers, city depts., local merchants) – Parking minutes or “Time” as alternative currency – Real-time parking management, fines and fees, fine and fee payments, and

nearby merchant offers and coupons pushed to eCity-related APPs

Technological advances will lead to Top Down requirements at the municipal level, which in turn will be a catalyst that disrupts the status quo.

Relative Importance of Developments 2016 – and Unexpected Change that May be Key

KEY DEVELOPMENTS IN PAYMENTS 2016 > SUMMARY

15

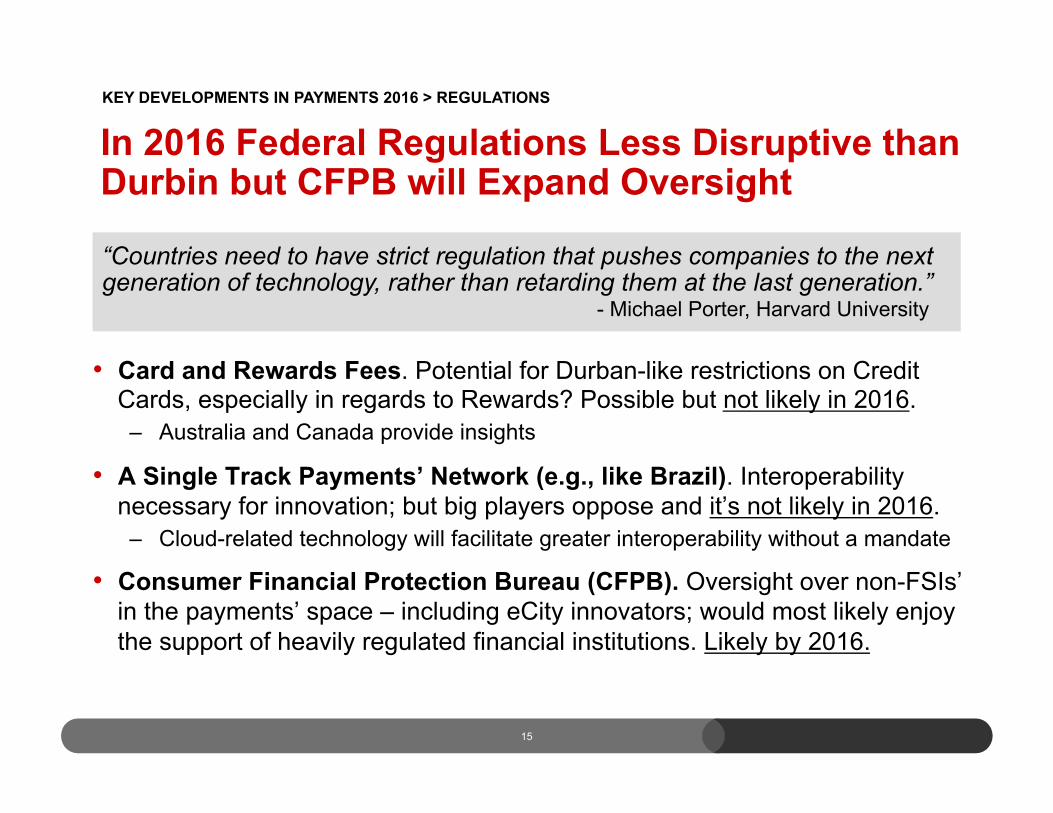

• Card and Rewards Fees. Potential for Durban-like restrictions on Credit Cards, especially in regards to Rewards? Possible but not likely in 2016. – Australia and Canada provide insights

• A Single Track Payments’ Network (e.g., like Brazil). Interoperability necessary for innovation; but big players oppose and it’s not likely in 2016. – Cloud-related technology will facilitate greater interoperability without a mandate

• Consumer Financial Protection Bureau (CFPB). Oversight over non-FSIs’ in the payments’ space – including eCity innovators; would most likely enjoy the support of heavily regulated financial institutions. Likely by 2016.

“Countries need to have strict regulation that pushes companies to the next generation of technology, rather than retarding them at the last generation.” - Michael Porter, Harvard University

In 2016 Federal Regulations Less Disruptive than Durbin but CFPB will Expand Oversight

KEY DEVELOPMENTS IN PAYMENTS 2016 > REGULATIONS

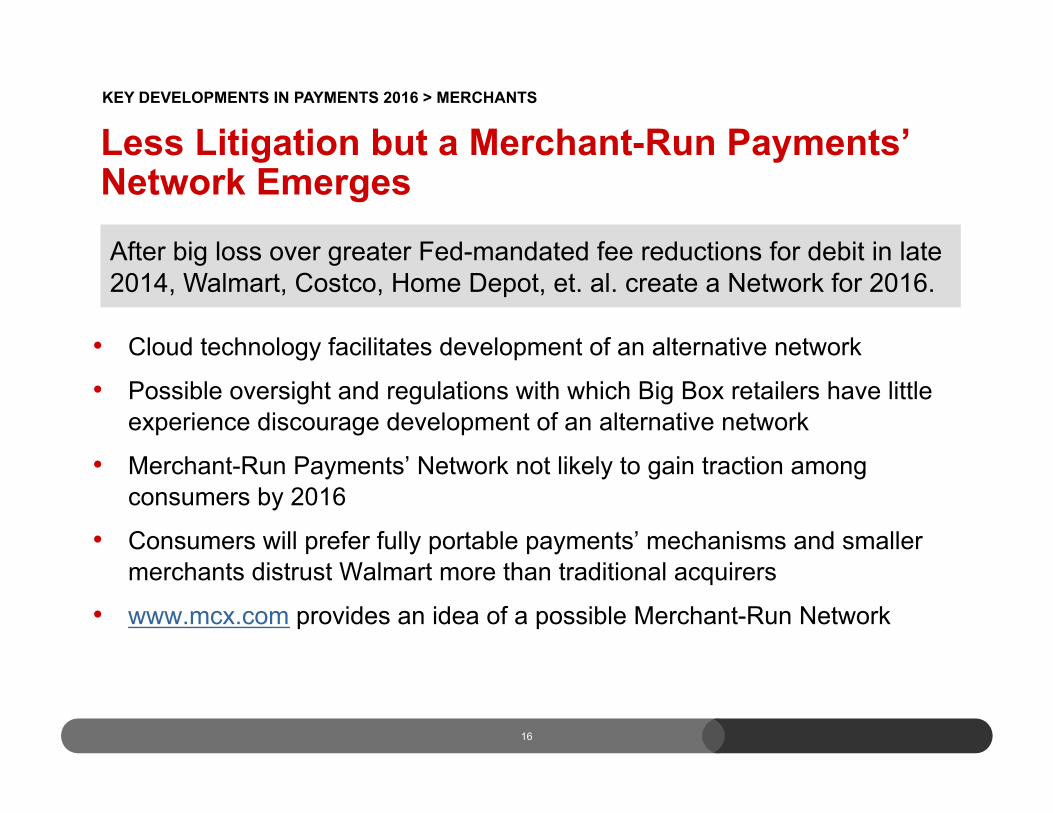

Less Litigation but a Merchant-Run Payments’ Network Emerges

• Cloud technology facilitates development of an alternative network

• Possible oversight and regulations with which Big Box retailers have little experience discourage development of an alternative network

• Merchant-Run Payments’ Network not likely to gain traction among consumers by 2016

• Consumers will prefer fully portable payments’ mechanisms and smaller merchants distrust Walmart more than traditional acquirers

• www.mcx.com provides an idea of a possible Merchant-Run Network

16

After big loss over greater Fed-mandated fee reductions for debit in late 2014, Walmart, Costco, Home Depot, et. al. create a Network for 2016.

KEY DEVELOPMENTS IN PAYMENTS 2016 > MERCHANTS

17

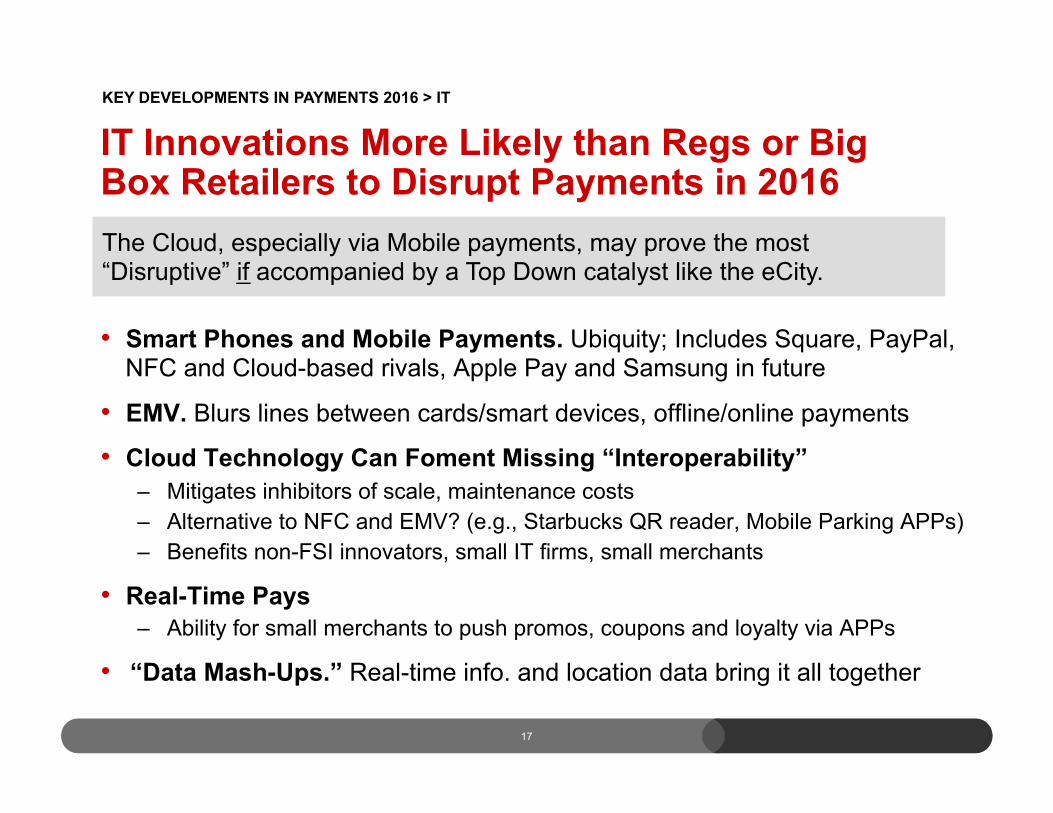

• Smart Phones and Mobile Payments. Ubiquity; Includes Square, PayPal, NFC and Cloud-based rivals, Apple Pay and Samsung in future

• EMV. Blurs lines between cards/smart devices, offline/online payments

• Cloud Technology Can Foment Missing “Interoperability” – Mitigates inhibitors of scale, maintenance costs – Alternative to NFC and EMV? (e.g., Starbucks QR reader, Mobile Parking APPs) – Benefits non-FSI innovators, small IT firms, small merchants

• Real-Time Pays – Ability for small merchants to push promos, coupons and loyalty via APPs

• “Data Mash-Ups.” Real-time info. and location data bring it all together

The Cloud, especially via Mobile payments, may prove the most “Disruptive” if accompanied by a Top Down catalyst like the eCity.

IT Innovations More Likely than Regs or Big Box Retailers to Disrupt Payments in 2016

KEY DEVELOPMENTS IN PAYMENTS 2016 > IT

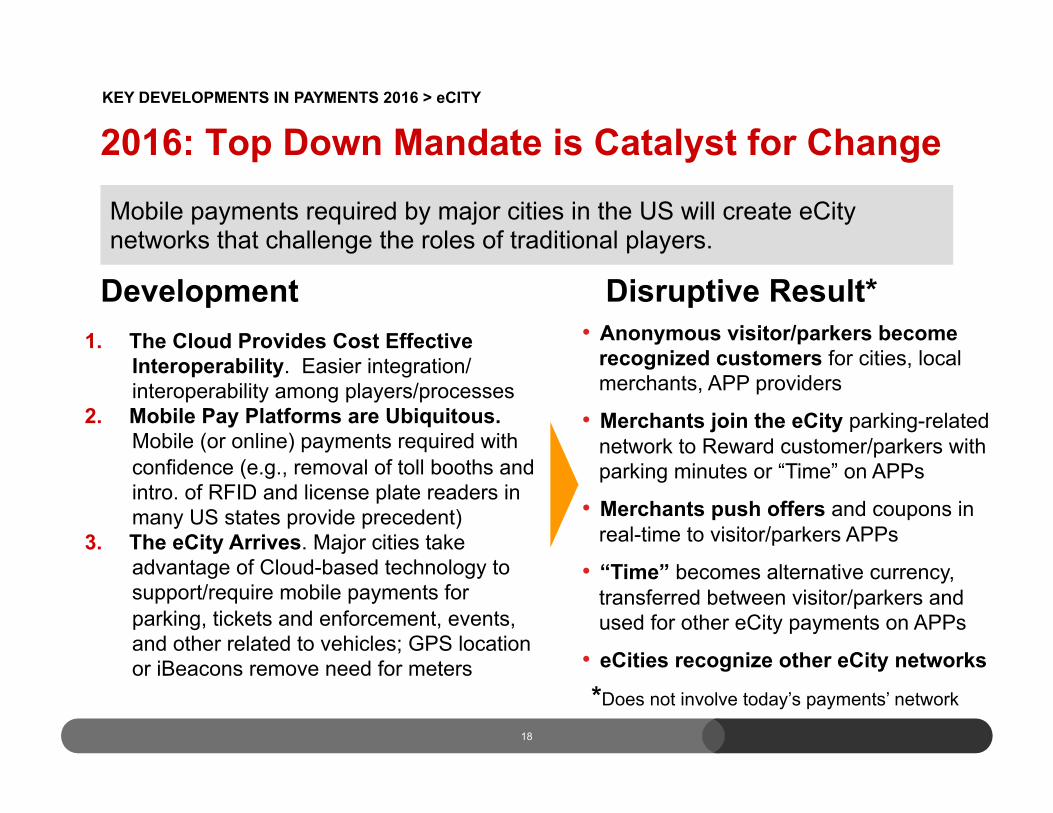

18

Development 1. The Cloud Provides Cost Effective

Interoperability. Easier integration/interoperability among players/processes

2. Mobile Pay Platforms are Ubiquitous. Mobile (or online) payments required with confidence (e.g., removal of toll booths and intro. of RFID and license plate readers in many US states provide precedent)

3. The eCity Arrives. Major cities take advantage of Cloud-based technology to support/require mobile payments for parking, tickets and enforcement, events, and other related to vehicles; GPS location or iBeacons remove need for meters

Disruptive Result* • Anonymous visitor/parkers become

recognized customers for cities, local merchants, APP providers

• Merchants join the eCity parking-related network to Reward customer/parkers with parking minutes or “Time” on APPs

• Merchants push offers and coupons in real-time to visitor/parkers APPs

• “Time” becomes alternative currency, transferred between visitor/parkers and used for other eCity payments on APPs

• eCities recognize other eCity networks

Mobile payments required by major cities in the US will create eCity networks that challenge the roles of traditional players.

2016: Top Down Mandate is Catalyst for Change

*Does not involve today’s payments’ network

KEY DEVELOPMENTS IN PAYMENTS 2016 > eCITY

THE eCITY AS TOP DOWN CATALYST Disruptive vs Top Down Change in US Payments in 2016

19

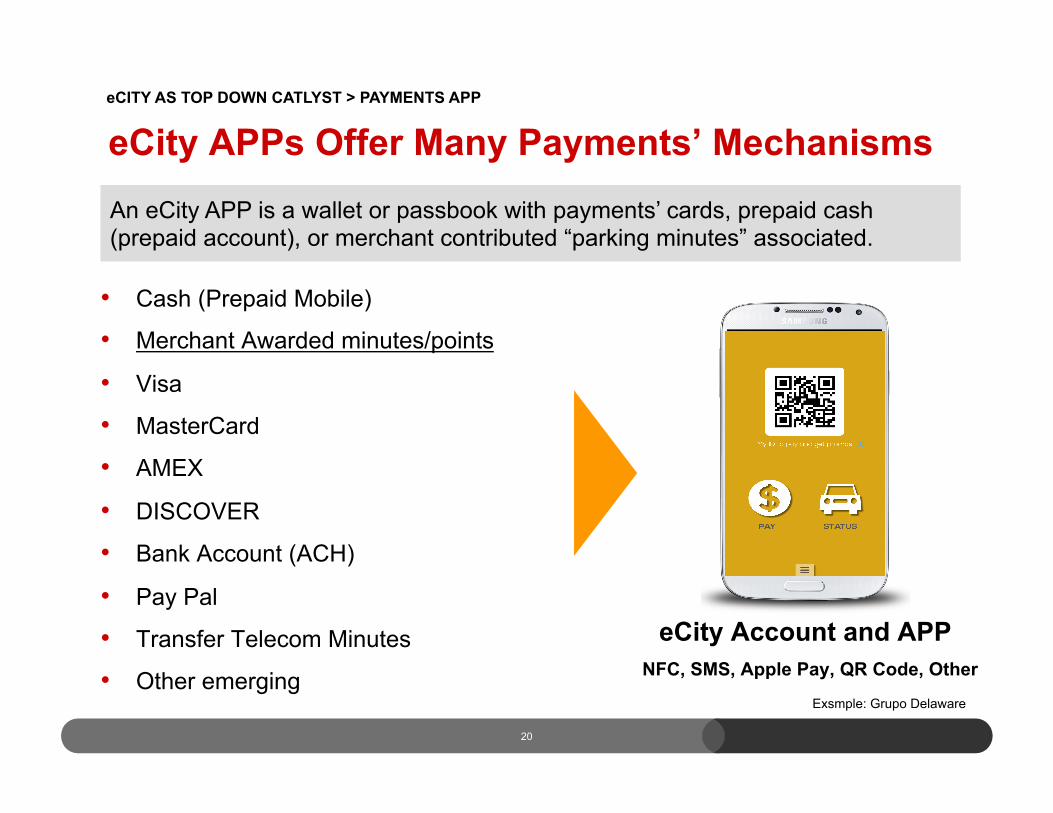

eCity APPs Offer Many Payments’ Mechanisms

• Cash (Prepaid Mobile)

• Merchant Awarded minutes/points

• Visa

• MasterCard

• AMEX

• DISCOVER

• Bank Account (ACH)

• Pay Pal

• Transfer Telecom Minutes

• Other emerging

eCity Account and APP NFC, SMS, Apple Pay, QR Code, Other

20

An eCity APP is a wallet or passbook with payments’ cards, prepaid cash (prepaid account), or merchant contributed “parking minutes” associated.

eCITY AS TOP DOWN CATLYST > PAYMENTS APP

Exsmple: Grupo Delaware

New Process: Merchant Acquistion and Loyalty Programs Using an eCity Network

• Highly targeted promos to visitor/parkers within a block or two of a merchant • Consumer location identified via GPS, iBeacons, or parking spot number • Minutes/points accumulate by paying for parking or through spend at

merchants in the eCity network • Minutes/points are a percentage of spend or fixed dollar amount (flexible) • eCity APPs automatically calculate and display minutes/points based on

individual merchant policies and agreements • Push notifications inform eCity APP users of points awarded or redeemed • Spend on APPs results in municipal parking being complimentary de facto • The eCity manages parking efficiently and captures significant revenue

21

21

Local businesses provide parking minutes/points and highly targeted promos to visitor/parkers via a Loyalty back-end incorporated into the eCity APP.

eCITY AS TOP DOWN CATLYST > eCITY NETWORK

22

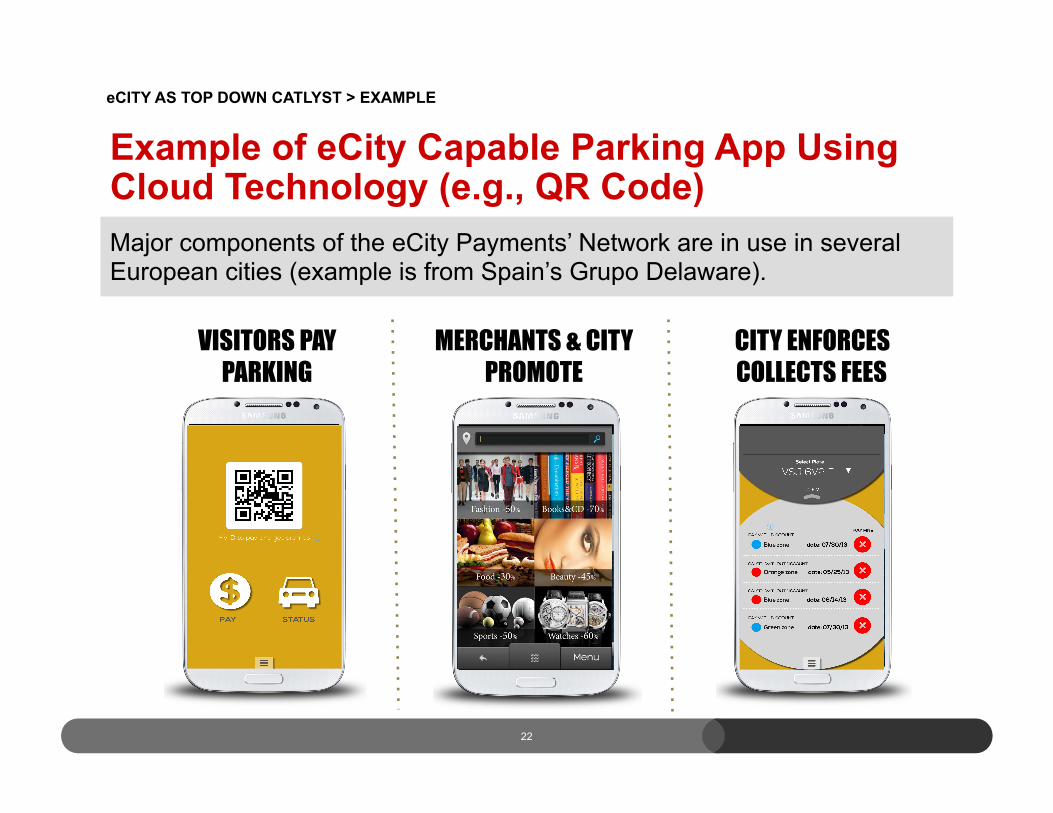

VISITORS PAY PARKING

MERCHANTS & CITY PROMOTE

CITY ENFORCES COLLECTS FEES

Example of eCity Capable Parking App Using Cloud Technology (e.g., QR Code) Major components of the eCity Payments’ Network are in use in several European cities (example is from Spain’s Grupo Delaware).

eCITY AS TOP DOWN CATLYST > EXAMPLE

IMPACT OF EMERGING eCITY NETWORKS 2016 Disruptive vs Top Down Change in US Payments in 2016

23

• eCity networks facilitate the crediting of “Time” by local merchants to visitor/parkers accounts to generate traffic and reward loyalty

• Coupons pushed to APPs introduce goods and services as alternative means of settlement outside traditional payments’ networks – For example, a participant in the eCity network exchanges a coupon for a free

soda for 1 hour of parking from another participant

• eCity networks and related mobile APPs bring benefits of digital marketing and major loyalty and Rewards programs to smaller merchants

24

New Process: eCity Networks May Settle in Other Than National Currencies

Dominant players in today’s Payments’ Landscape are limited to settling transactions in national currencies.

IMPACT OF eCITY NETWORKS > SETTLEMENT

The eCity Network Has Advantages Over Other Potential Payments’ Network Start-Ups

• Facebook, Apple (via iTunes), Google Plus and Social Networks – Apple best positioned with hundreds of millions of customers and payments

mechanisms associated with iTunes, and Apple Pay in place ! Apple Pay platform with iPhone 6 increasingly socialized ! iBeacons incorporated into payments' platform

• Amazon, Netflix, Hulu and other online content providers – Millions of registered payments’ methods – Deep knowledge of customer location and preferences – Ability to reach millions of users in near real-time

25

Governments mandate participation as they do with mass transit oriented RFID technology and recognition software; Online social and media networks have no such advantages but could partner with existing or emerging networks.

IMPACT OF eCITY NETWORKS > ALTERNATIVE NETWORKS

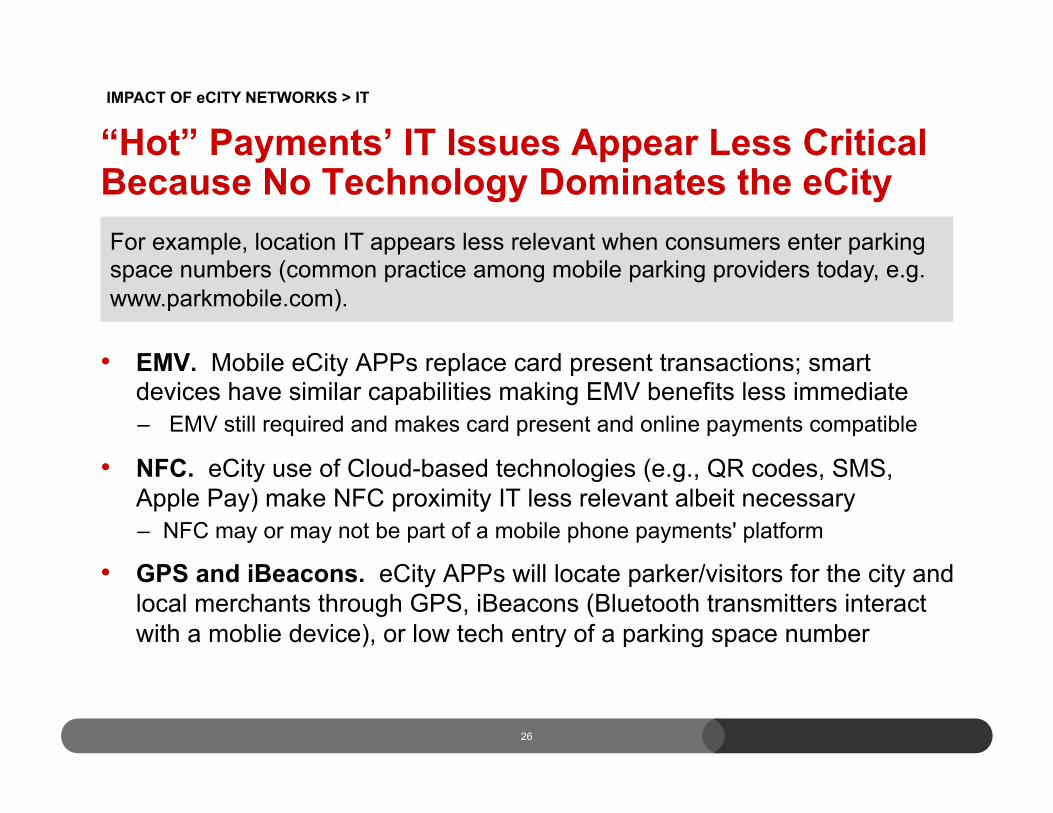

“Hot” Payments’ IT Issues Appear Less Critical Because No Technology Dominates the eCity

• EMV. Mobile eCity APPs replace card present transactions; smart devices have similar capabilities making EMV benefits less immediate – EMV still required and makes card present and online payments compatible

• NFC. eCity use of Cloud-based technologies (e.g., QR codes, SMS, Apple Pay) make NFC proximity IT less relevant albeit necessary – NFC may or may not be part of a mobile phone payments' platform

• GPS and iBeacons. eCity APPs will locate parker/visitors for the city and local merchants through GPS, iBeacons (Bluetooth transmitters interact with a moblie device), or low tech entry of a parking space number

26

For example, location IT appears less relevant when consumers enter parking space numbers (common practice among mobile parking providers today, e.g. www.parkmobile.com).

IMPACT OF eCITY NETWORKS > IT

SUMMARY Disruptive vs Top Down Change in US Payments in 2016

27

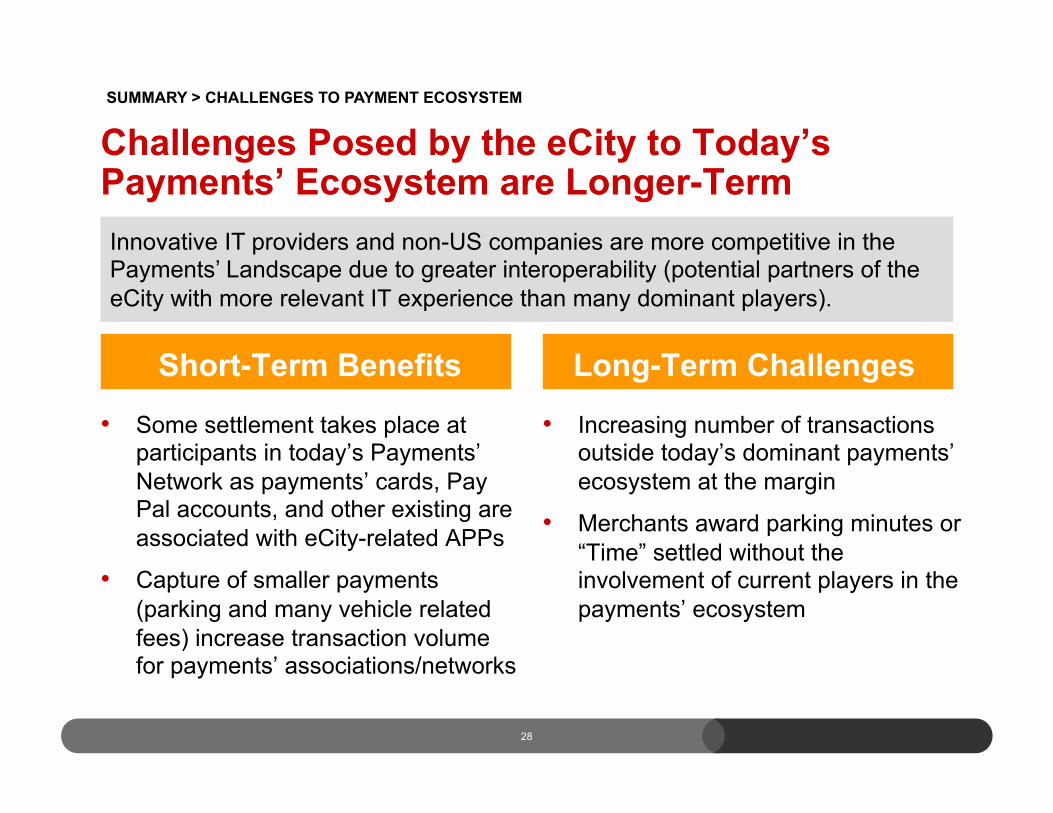

Short-Term Benefits

• Some settlement takes place at participants in today’s Payments’ Network as payments’ cards, Pay Pal accounts, and other existing are associated with eCity-related APPs

• Capture of smaller payments (parking and many vehicle related fees) increase transaction volume for payments’ associations/networks

Long-Term Challenges

• Increasing number of transactions outside today’s dominant payments’ ecosystem at the margin

• Merchants award parking minutes or “Time” settled without the involvement of current players in the payments’ ecosystem

28

Challenges Posed by the eCity to Today’s Payments’ Ecosystem are Longer-Term Innovative IT providers and non-US companies are more competitive in the Payments’ Landscape due to greater interoperability (potential partners of the eCity with more relevant IT experience than many dominant players).

SUMMARY > CHALLENGES TO PAYMENT ECOSYSTEM

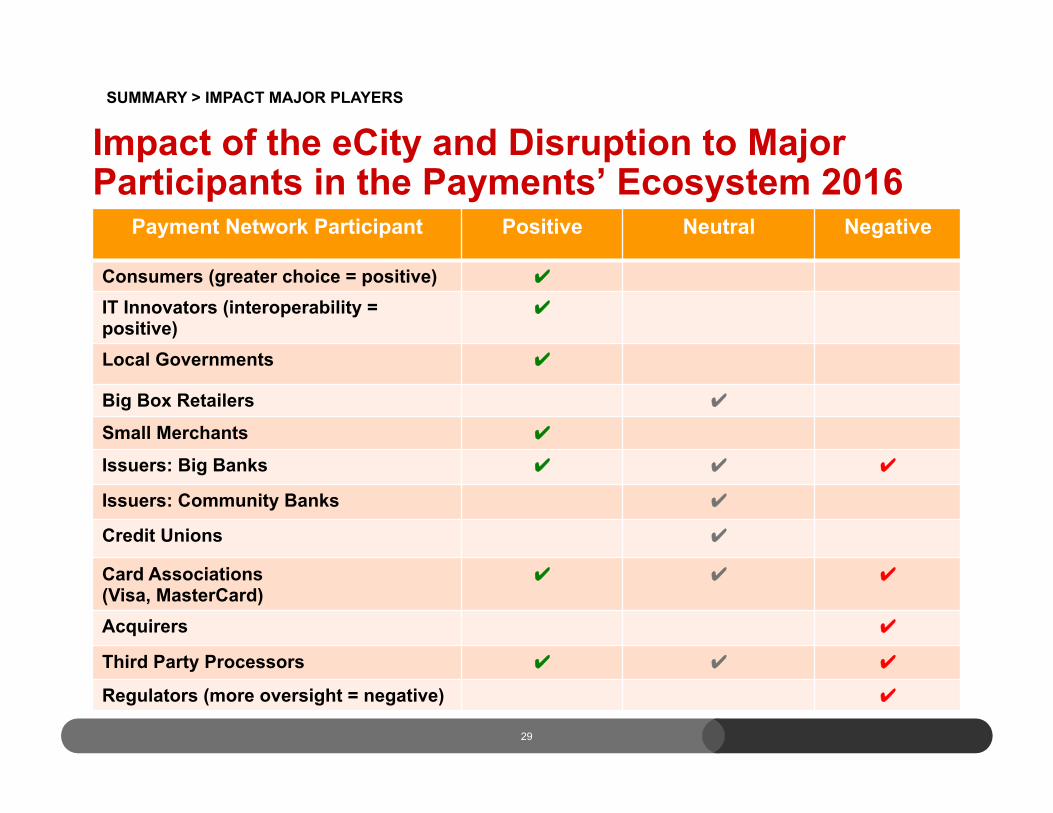

Impact of the eCity and Disruption to Major Participants in the Payments’ Ecosystem 2016

29

Payment Network Participant Positive Neutral Negative

Consumers (greater choice = positive) ✔ IT Innovators (interoperability = positive)

✔"

Local Governments ✔"

Big Box Retailers ✔"

Small Merchants ✔"

Issuers: Big Banks ✔" ✔" ✔"

Issuers: Community Banks ✔"

Credit Unions ✔"

Card Associations (Visa, MasterCard)

✔"

✔"

✔"

Acquirers ✔"

Third Party Processors ✔" ✔" ✔"

Regulators (more oversight = negative) ✔"

SUMMARY > IMPACT MAJOR PLAYERS

30

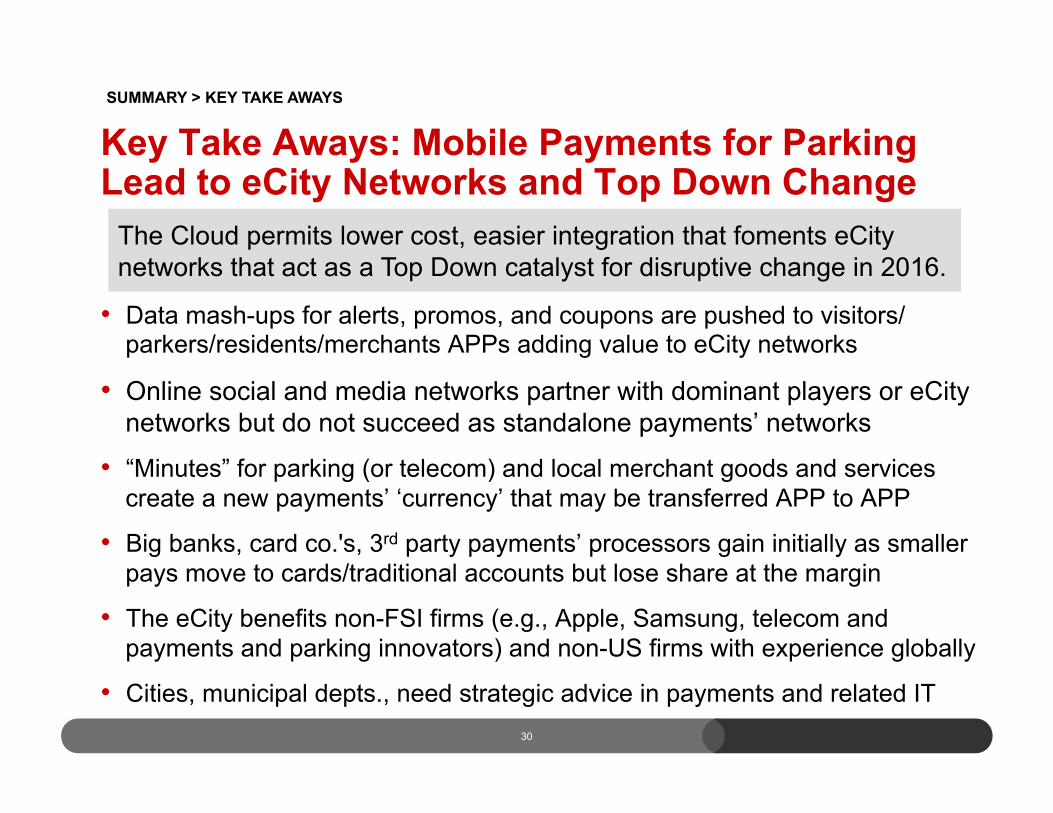

• Data mash-ups for alerts, promos, and coupons are pushed to visitors/parkers/residents/merchants APPs adding value to eCity networks

• Online social and media networks partner with dominant players or eCity networks but do not succeed as standalone payments’ networks

• “Minutes” for parking (or telecom) and local merchant goods and services create a new payments’ ‘currency’ that may be transferred APP to APP

• Big banks, card co.'s, 3rd party payments’ processors gain initially as smaller pays move to cards/traditional accounts but lose share at the margin

• The eCity benefits non-FSI firms (e.g., Apple, Samsung, telecom and payments and parking innovators) and non-US firms with experience globally

• Cities, municipal depts., need strategic advice in payments and related IT

The Cloud permits lower cost, easier integration that foments eCity networks that act as a Top Down catalyst for disruptive change in 2016.

Key Take Aways: Mobile Payments for Parking Lead to eCity Networks and Top Down Change

SUMMARY > KEY TAKE AWAYS

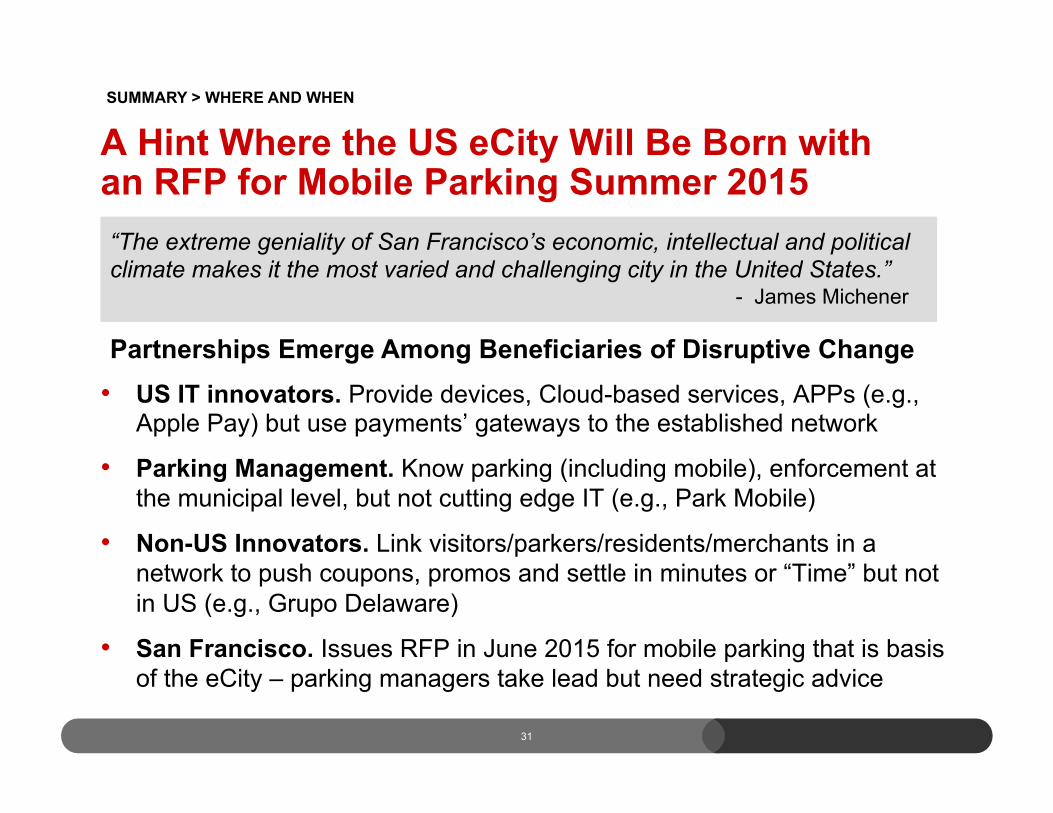

A Hint Where the US eCity Will Be Born with an RFP for Mobile Parking Summer 2015

• US IT innovators. Provide devices, Cloud-based services, APPs (e.g., Apple Pay) but use payments’ gateways to the established network

• Parking Management. Know parking (including mobile), enforcement at the municipal level, but not cutting edge IT (e.g., Park Mobile)

• Non-US Innovators. Link visitors/parkers/residents/merchants in a network to push coupons, promos and settle in minutes or “Time” but not in US (e.g., Grupo Delaware)

• San Francisco. Issues RFP in June 2015 for mobile parking that is basis of the eCity – parking managers take lead but need strategic advice

31

SUMMARY > WHERE AND WHEN

“The extreme geniality of San Francisco’s economic, intellectual and political climate makes it the most varied and challenging city in the United States.” - James Michener

Partnerships Emerge Among Beneficiaries of Disruptive Change

Why the Advent of the eCity Will Produce Disruptive Change

March 2015 Walter Kitchenman [email protected]

Disruptive vs Top Down Change in US Payments in 2016