Embed Size (px)

Citation preview

A new consolidation wave in internet marketing services

Daan Witteveenpartner Deloitte – leader Technology Fast50

© 2010 Deloitte Touche Tohmatsu2

What will we discuss today?

TrendsOnline Marketing

ConsolidationDrivers

What can we expect?

Who will be leading?

© 2010 Deloitte Touche Tohmatsu3

© 2010 Deloitte Touche Tohmatsu

Numerous brands and business models are competing online

4

© 2010 Deloitte Touche Tohmatsu5

Online marketing services provides guidance on the internet

© 2010 Deloitte Touche Tohmatsu

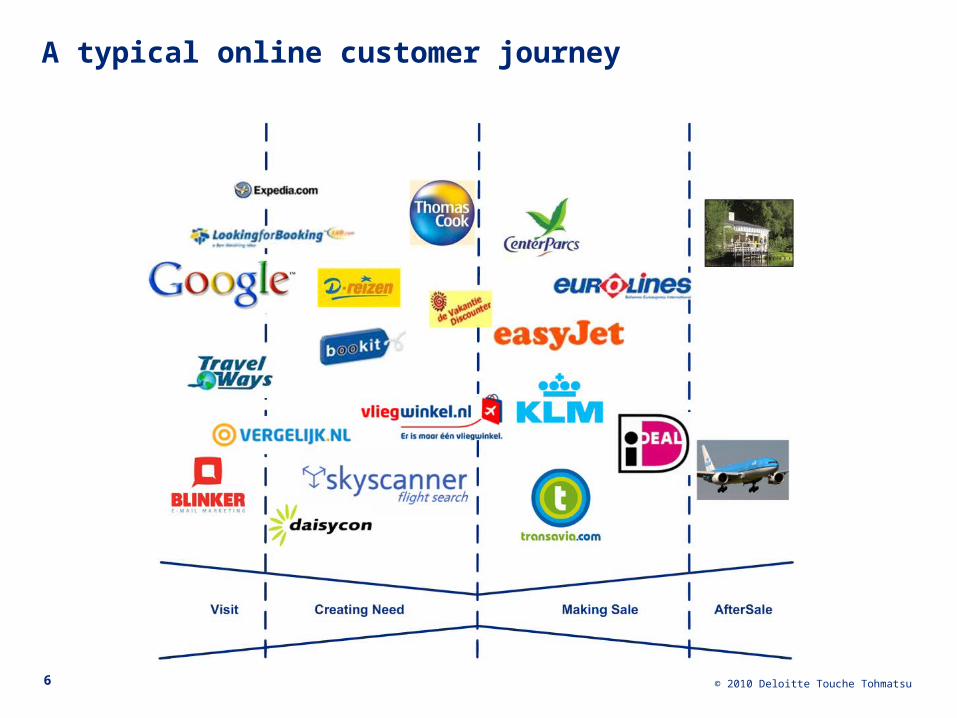

A typical online customer journey

6

© 2010 Deloitte Touche Tohmatsu

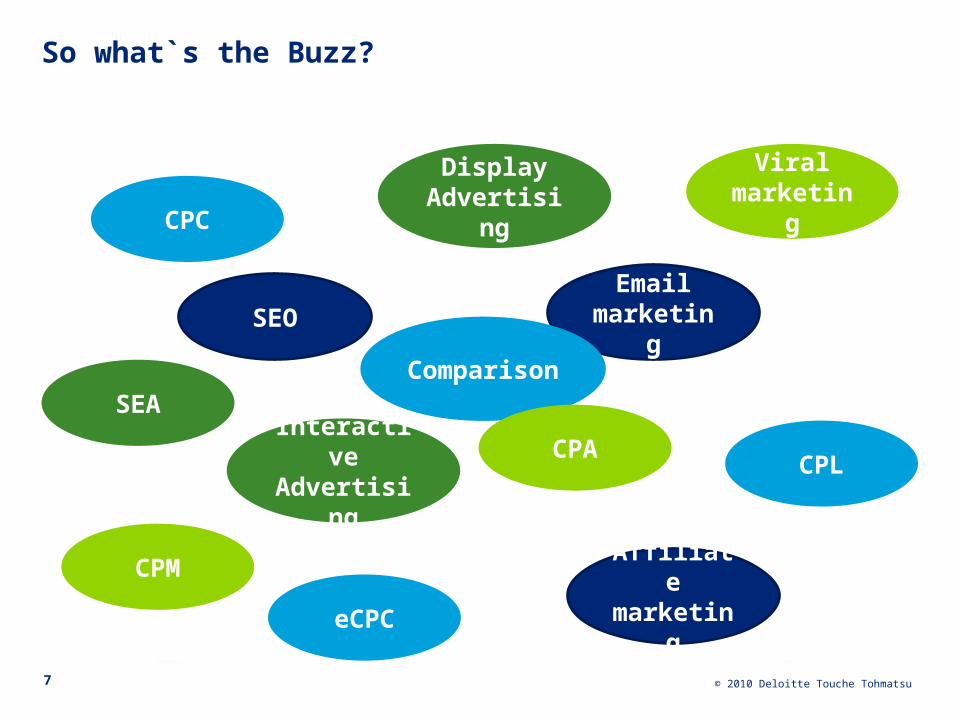

So what`s the Buzz?

7

SEA

Display Advertising

Interactive Advertising

eCPC

CPL

CPM

CPC

SEO

Affiliate marketing

Viral marketing

Email marketing

Comparison

CPA

© 2010 Deloitte Touche Tohmatsu

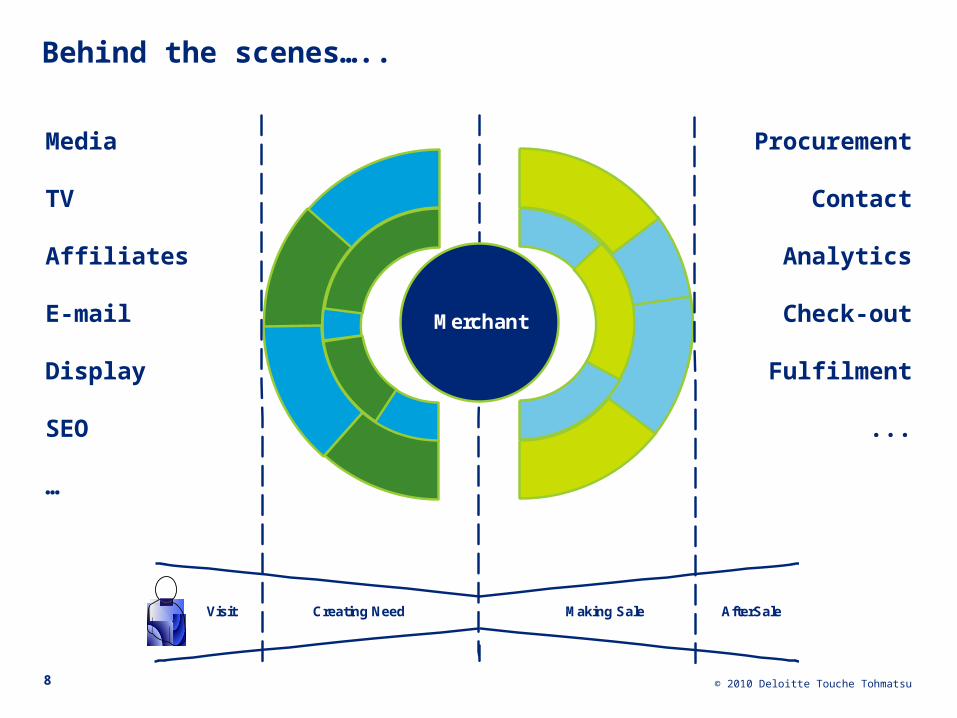

Behind the scenes…..

8

Media

TV

Affiliates

Display

SEO

…

Procurement

Contact

Analytics

Check-out

Fulfilment

...

Merchant

Visit Creating Need Making Sale AfterSale

© 2010 Deloitte Touche Tohmatsu

Drivers for online consolidation in online marketing

9

• Internet becomes core to the business

• Preferred suppliership (~IT)

• No single optimal solution best of breed & integrated solutions

• Platform costs (cost border sharing)

• Shift towards per performance based

• Shift from traditional media budget to sales costs

• High growth value creation opportunity

© 2010 Deloitte Touche Tohmatsu

Consolidation

10

Dea

l siz

e in

EU

R m

ln

0

200

400

600

800

2008 Compete Inc., USA Taylor Nelson Sofres Plc., UK

2010 Mitchell Com. Ltd., Australia Aegis Group Plc., UK

2010 Razorfish Inc., USA Publicis Group SA, France

2009 AdMob Inc., USA Google Inc., USA

2008 D+S Europe AG, Germany Pyramus S.a r.I, Luxembourg

Home run exits

Playing field??

Selection of online marketing deals over the last 24 months

© 2010 Deloitte Touche Tohmatsu

Horizontal and Vertical integration in the Online Value chain

11

Merchant

Online Marketing

I & M services

Ad agencies

Publishers

Telecom / CDN

PE

© 2010 Deloitte Touche Tohmatsu

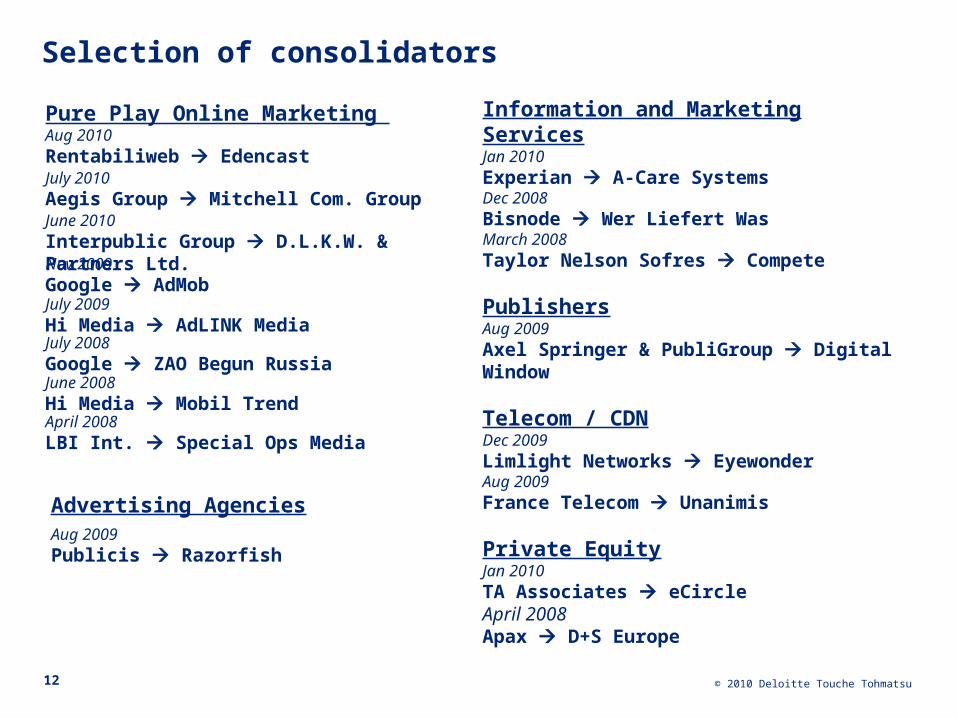

Selection of consolidators

12

Pure Play Online Marketing Information and Marketing ServicesJan 2010Experian A-Care SystemsDec 2008Bisnode Wer Liefert WasMarch 2008Taylor Nelson Sofres Compete

PublishersAug 2009Axel Springer & PubliGroup Digital Window

Telecom / CDNDec 2009Limlight Networks EyewonderAug 2009France Telecom Unanimis

Private EquityJan 2010TA Associates eCircleApril 2008Apax D+S Europe

Advertising Agencies

Aug 2010Rentabiliweb EdencastJuly 2010Aegis Group Mitchell Com. GroupJune 2010Interpublic Group D.L.K.W. & Partners Ltd.Nov 2009Google AdMobJuly 2009 Hi Media AdLINK MediaJuly 2008 Google ZAO Begun RussiaJune 2008 Hi Media Mobil TrendApril 2008 LBI Int. Special Ops Media

Aug 2009 Publicis Razorfish

© 2010 Deloitte Touche Tohmatsu

While the online marketing industry is maturing, new start-ups drive innovation

13

TVMagazines

Newspapers

Radio

Games

Internet Music

BillboardsOnline Marketing

Introduction Growth Maturity Decline

Typical strategy

Build portfolio of ‘real options’: limited investments that can be grown fast when succesful

Create group of synergistic businesses

Either consolidate the sector, exit earlyor concentrate on profitable niches

Strategic objective

Build portfolio of assets Capture synergy within group

Consolidate market

Key screening criterium

Upside potentialLeveraging core’s competences

Revenue and cost synergies

Cost synergies

© 2010 Deloitte Touche Tohmatsu

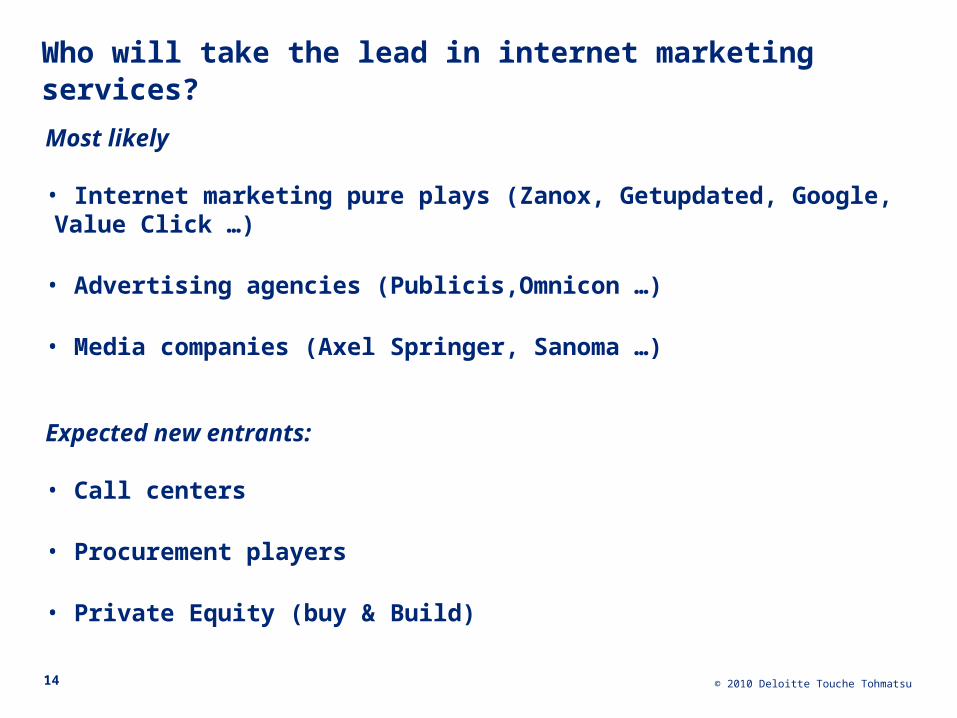

Who will take the lead in internet marketing services?

14

Most likely

• Internet marketing pure plays (Zanox, Getupdated, Google, Value Click …)

• Advertising agencies (Publicis,Omnicon …)

• Media companies (Axel Springer, Sanoma …)

Expected new entrants:

• Call centers

• Procurement players

• Private Equity (buy & Build)

© 2010 Deloitte Touche Tohmatsu15

Discussion

© 2010 Deloitte Touche Tohmatsu

Disclaimer: Deloitte refers to one or more of Deloitte Touche Tohmatsu, a Swiss Verein, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu and its member firms.

16

![Daan and Other Giving Traditions in India-finalaccountaid.net/Books/Daan/Daan - Aug 10- Adobe 7.pdf · Nakshatra Daan(n]Ç dan)61 ... Daan and Other Giving Traditions in Indiaat the](https://img.pdfslide.net/doc/110x75/5ac56ae07f8b9ae06c8dc016/daan-and-other-giving-traditions-in-india-aug-10-adobe-7pdfnakshatra-daann.jpg)